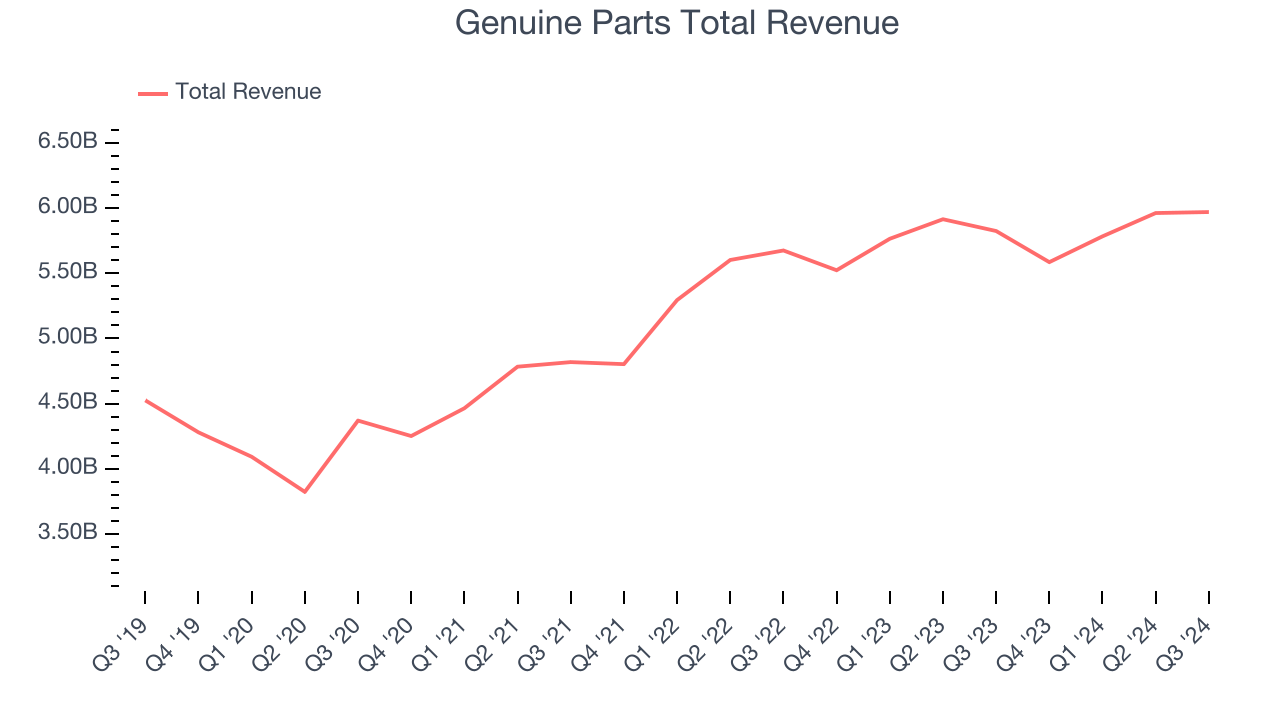

Auto and industrial parts retailer Genuine Parts (NYSE:GPC) met Wall Street’s revenue expectations in Q3 CY2024, with sales up 2.5% year on year to $5.97 billion. Its non-GAAP profit of $1.88 per share was 22.5% below analysts’ consensus estimates.

Is now the time to buy Genuine Parts? Find out in our full research report.

Genuine Parts (GPC) Q3 CY2024 Highlights:

- Revenue: $5.97 billion vs analyst estimates of $5.95 billion (in line)

- Adjusted EPS: $1.88 vs analyst expectations of $2.43 (22.5% miss)

- EBITDA: $582.1 million vs analyst estimates of $563.7 million (3.3% beat)

- Management lowered its full-year Adjusted EPS guidance to $8.10 at the midpoint, a 13.8% decrease

- Gross Margin (GAAP): 36.8%, in line with the same quarter last year

- Free Cash Flow Margin: 6%, down from 8.3% in the same quarter last year

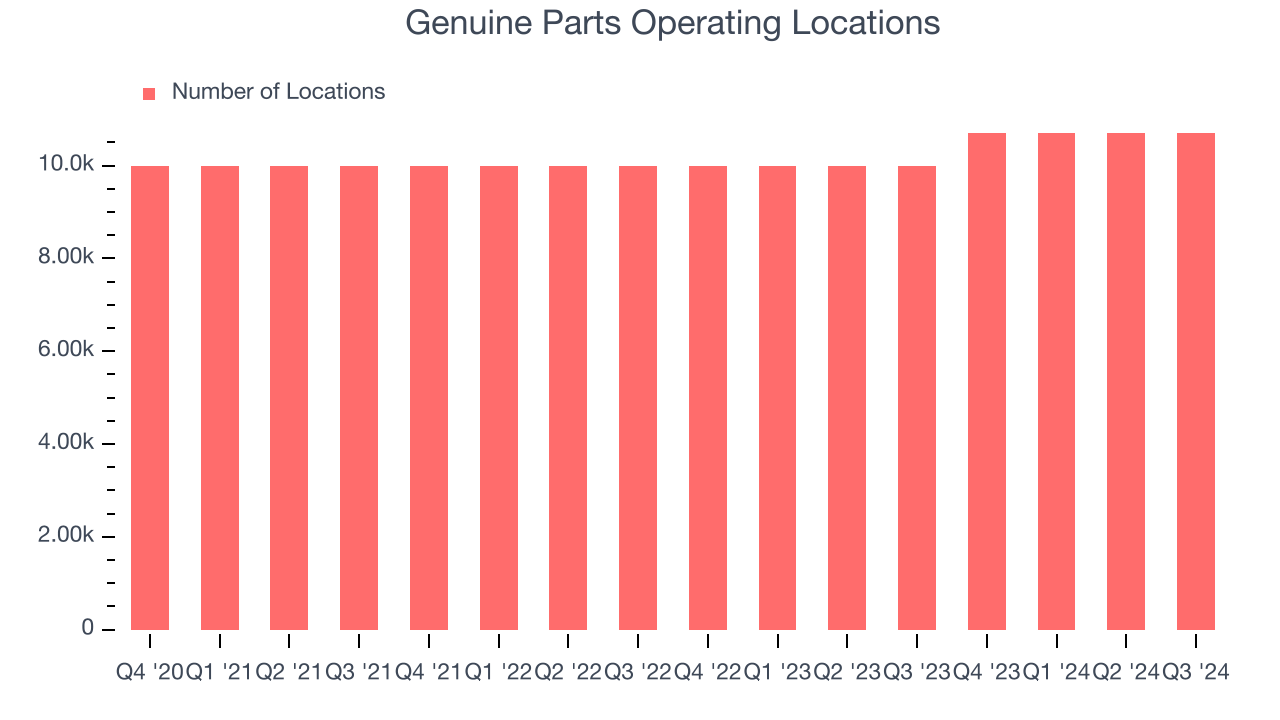

- Locations: 10,700 at quarter end, up from 10,000 in the same quarter last year

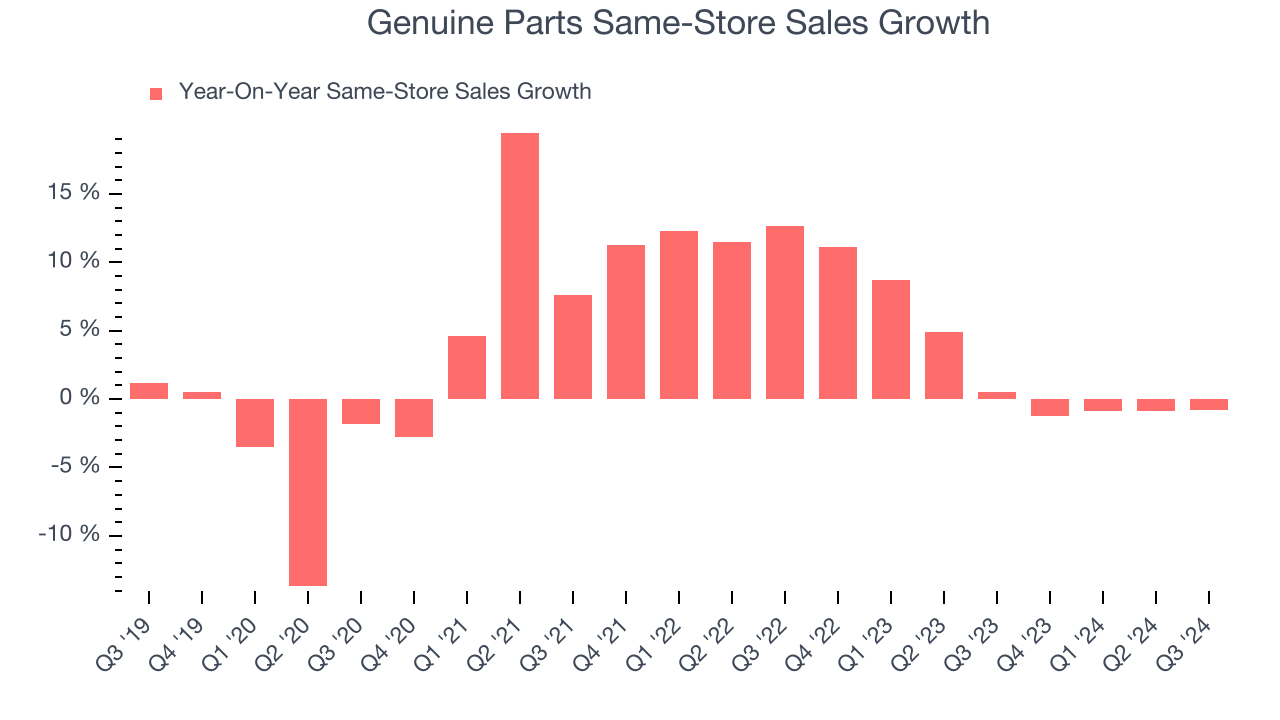

- Same-Store Sales were flat year on year (0.5% in the same quarter last year) (miss)

- Market Capitalization: $19.94 billion

Company Overview

Largely targeting the professional customer, Genuine Parts (NYSE:GPC) sells auto and industrial parts such as batteries, belts, bearings, and machine fluids.

Auto Parts Retailer

Cars are complex machines that need maintenance and occasional repairs, and auto parts retailers cater to the professional mechanic as well as the do-it-yourself (DIY) fixer. Work on cars may entail replacing fluids, parts, or accessories, and these stores have the parts and accessories or these jobs. While e-commerce competition presents a risk, these stores have a leg up due to the combination of broad and deep selection as well as expertise provided by sales associates. Another change on the horizon could be the increasing penetration of electric vehicles.

Sales Growth

A company’s long-term performance can give signals about its business quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years.

Genuine Parts is one of the larger companies in the consumer retail industry and benefits from a well-known brand that influences consumer purchasing decisions. However, its scale is a double-edged sword because it's harder to find incremental growth when you've already penetrated the market.

As you can see below, Genuine Parts’s 5.5% annualized revenue growth over the last five years (we compare to 2019 to normalize for COVID-19 impacts) was tepid, but to its credit, it opened new stores and increased sales at existing, established locations.

This quarter, Genuine Parts grew its revenue by 2.5% year on year, and its $5.97 billion of revenue was in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 3.7% over the next 12 months, a slight deceleration versus the last five years. Some tapering is natural given the magnitude of its revenue base, and we still think its growth trajectory is attractive.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefitting from the rise of AI, available to you FREE via this link.

Store Performance

Number of Stores

A retailer’s store count often determines how much revenue it can generate.

Genuine Parts sported 10,700 locations in the latest quarter. Over the last two years, it has opened new stores at a rapid clip and averaged 3.5% annual growth, among the fastest in the consumer retail sector.

When a retailer opens new stores, it usually means it’s investing for growth because demand is greater than supply, especially in areas where consumers may not have a store within reasonable driving distance.

Same-Store Sales

A company's store base only paints one part of the picture. When demand is high, it makes sense to open more. But when demand is low, it’s prudent to close some locations and use the money in other ways. Same-store sales is an industry measure of whether revenue is growing at those existing stores and is driven by customer visits (often called traffic) and the average spending per customer (ticket).

Genuine Parts’s demand has been healthy for a retailer over the last two years. On average, the company has grown its same-store sales by a robust 2.7% per year. This performance suggests its rollout of new stores could be beneficial for shareholders. When a retailer has demand, more locations should help it reach more customers and boost revenue growth.

In the latest quarter, Genuine Parts’s year on year same-store sales were flat. This performance was more or less in line with the same quarter last year.

Key Takeaways from Genuine Parts’s Q3 Results

It was good to see Genuine Parts beat analysts’ EBITDA expectations this quarter. We were also glad its gross margin outperformed Wall Street’s estimates. On the other hand, its same store sales came in below expectations. Looking ahead, the company's EPS forecast for the full year missed and its EPS missed Wall Street’s estimates. Overall, this was a softer quarter. The stock traded down 9% to $130.25 immediately following the results.

Genuine Parts didn’t show it’s best hand this quarter, but does that create an opportunity to buy the stock right now?If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings.We cover that in our actionable full research report which you can read here, it’s free.