McCormick (NYSE:MKC) Reports Q2 In Line With Expectations

Max Juang /

June 27, 2024

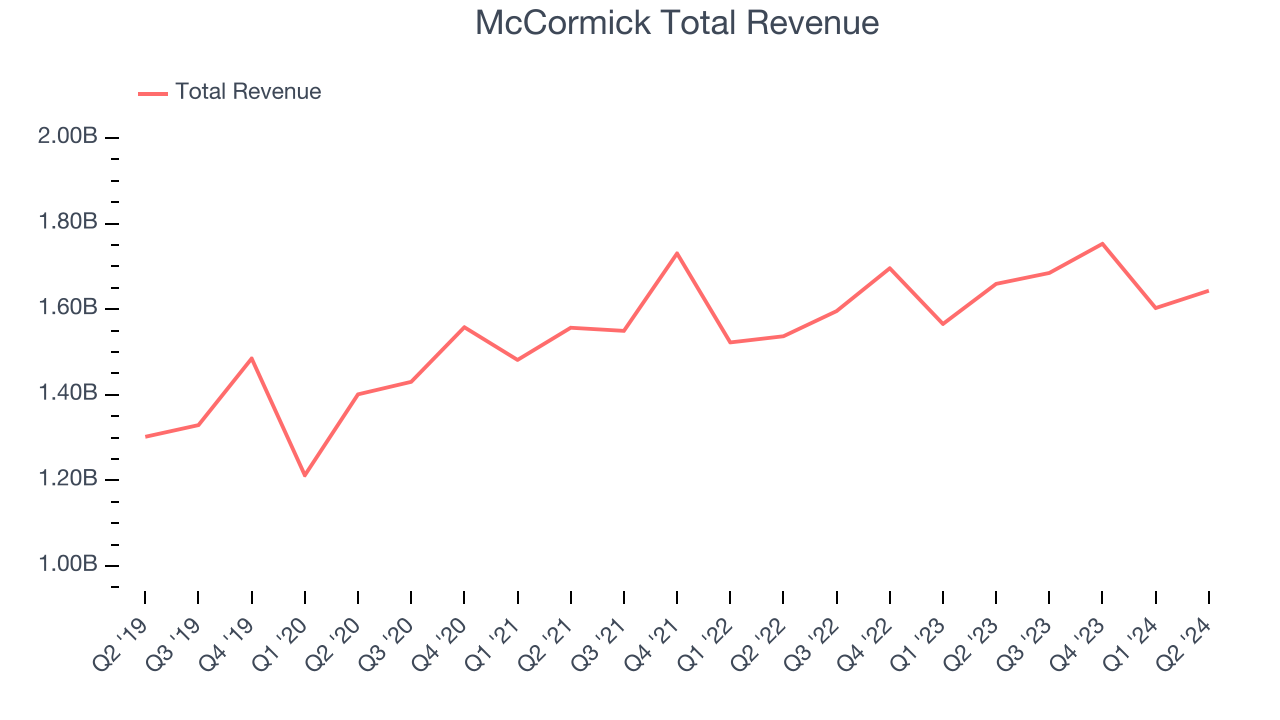

Food flavoring company McCormick (NYSE:MKC) reported results in line with analysts' expectations in Q2 CY2024, with revenue flat year on year at $1.64 billion. It made a non-GAAP profit of $0.69 per share, improving from its profit of $0.60 per share in the same quarter last year.

Is now the time to buy McCormick? Find out in our full research report.

McCormick (MKC) Q2 CY2024 Highlights:

- Revenue: $1.64 billion vs analyst estimates of $1.63 billion (small beat)

- EPS (non-GAAP): $0.69 vs analyst estimates of $0.59 (17.3% beat)

- Full year guidance reaffirmed for sales, operating profit, and adjusted earnings per share

- Gross Margin (GAAP): 37.7%, up from 37.1% in the same quarter last year

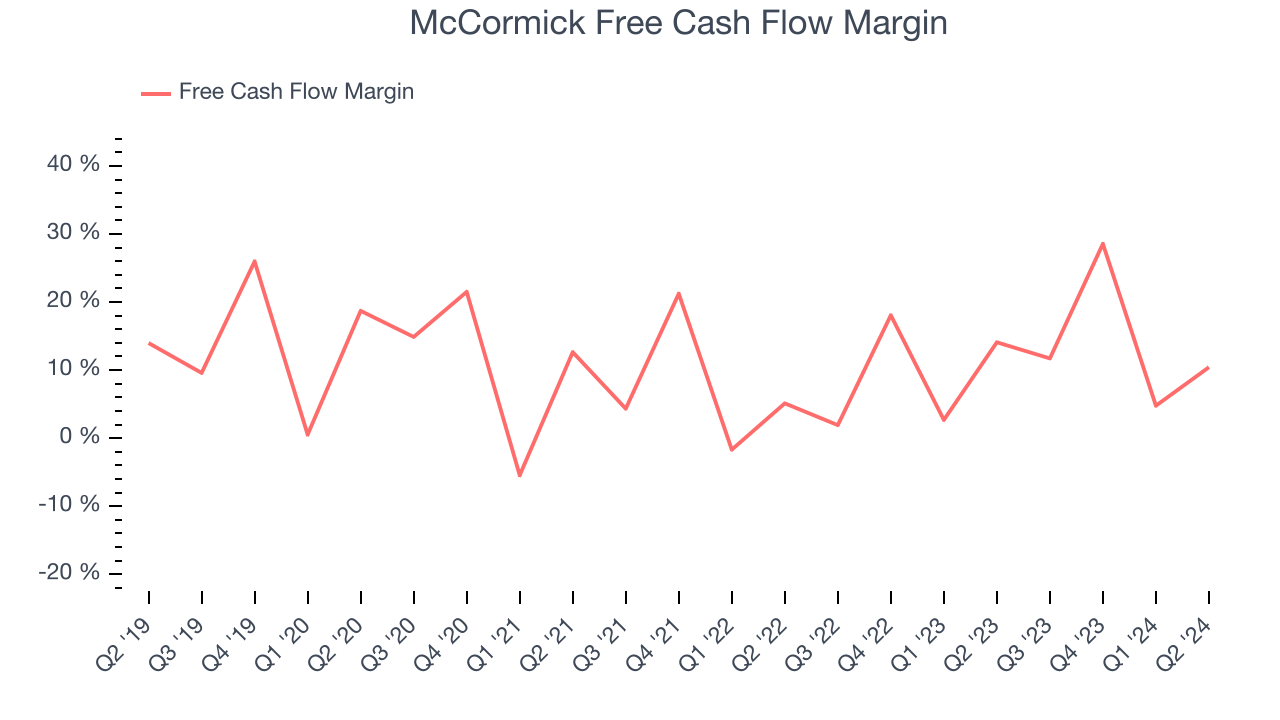

- Free Cash Flow of $171.2 million, up 124% from the previous quarter

- Sales Volumes were down 1% year on year

- Market Capitalization: $17.99 billion

Brendan M. Foley, President and CEO, stated, "We are pleased with our performance for the first half of the year, which was in line with our expectations and reflects the success of our prioritized business investments to drive improving results and trends. The investments we made in our Consumer segment drove substantial sequential volume improvement in the second quarter, leading to volume growth, and we expect continued momentum for the second half of the year. In Flavor Solutions, lower demand from some quick service restaurant and packaged food customers combined with the timing of customer activities, impacted our second quarter performance. We believe our collaboration and strong innovation pipeline with our customers will drive improved volume performance in the second half of the year.

The classic red Heinz ketchup bottle’s competitor, McCormick (NYSE:MKC) sells food-flavoring products like condiments, spices, and seasoning mixes.

Shelf-Stable Food

As America industrialized and moved away from an agricultural economy, people faced more demands on their time. Packaged foods emerged as a solution offering convenience to the evolving American family, whether it be canned goods or snacks. Today, Americans seek brands that are high in quality, reliable, and reasonably priced. Furthermore, there's a growing emphasis on health-conscious and sustainable food options. Packaged food stocks are considered resilient investments. People always need to eat, so these companies can enjoy consistent demand as long as they stay on top of changing consumer preferences. The industry spans from multinational corporations to smaller specialized firms and is subject to food safety and labeling regulations.

Sales Growth

McCormick is larger than most consumer staples companies and benefits from economies of scale, giving it an edge over its smaller competitors.

As you can see below, the company's annualized revenue growth rate of 3.5% over the last three years was sluggish as consumers bought less of its products. We'll explore what this means in the "Volume Growth" section.

This quarter, McCormick reported a rather uninspiring 1% year-on-year revenue decline to $1.64 billion in revenue, in line with Wall Street's estimates. Looking ahead, Wall Street expects sales to grow 1.2% over the next 12 months, an acceleration from this quarter.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefitting from the rise of AI, available to you FREE via this link.

Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can't use accounting profits to pay the bills.

McCormick has shown robust cash profitability, giving it an edge over its competitors and the option to reinvest or return capital to investors. The company's free cash flow margin averaged 11.8% over the last two years, quite impressive for a consumer staples business.

Taking a step back, we can see that McCormick's margin expanded by 4.7 percentage points during that time. This is encouraging.

McCormick's free cash flow clocked in at $171.2 million in Q2, equivalent to a 10.4% margin. The company's margin regressed as it was 3.7 percentage points lower than in the same quarter last year, but we wouldn't read too much into it because working capital needs can be seasonal and cause short-term swings.

Key Takeaways from McCormick's Q2 Results

It was good to see McCormick beat analysts' EPS expectations this quarter. We were also happy its revenue narrowly outperformed Wall Street's estimates. Full year guidance was reaffirmed across the board, showing the company is staying on track. Overall, this quarter seemed fairly positive and shareholders should feel optimistic. The stock traded up 4.9% to $71 immediately following the results.

So should you invest in McCormick right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.