Asure Software (ASUR)

We aren’t fans of Asure Software. Its underwhelming revenue growth and failure to generate meaningful free cash flow is a concerning trend.― StockStory Analyst Team

1. News

2. Summary

Why We Think Asure Software Will Underperform

Operating in the often-overlooked smaller metropolitan markets where HR expertise can be scarce, Asure Software (NASDAQ:ASUR) provides cloud-based human capital management software and services that help small and medium-sized businesses manage payroll, taxes, time tracking, and HR compliance.

- Operating profits and efficiency rose over the last year as it benefited from some fixed cost leverage

- Ability to fund investments or reward shareholders with increased buybacks or dividends is restricted by its weak free cash flow margin of 5.5% for the last year

- On the bright side, its well-designed software integrates seamlessly with other workflows, enabling swift payback periods on marketing expenses and customer growth at scale

Asure Software falls short of our quality standards. There are better opportunities in the market.

Why There Are Better Opportunities Than Asure Software

At $8.58 per share, Asure Software trades at 1.5x forward price-to-sales. Asure Software’s valuation may seem like a bargain, but we think there are valid reasons why it’s so cheap.

Cheap stocks can look like great bargains at first glance, but you often get what you pay for. These mediocre businesses often have less earnings power, meaning there is more reliance on a re-rating to generate good returns - an unlikely scenario for low-quality companies.

3. Asure Software (ASUR) Research Report: Q4 CY2025 Update

HR software provider Asure Software (NASDAQ:ASUR) reported Q4 CY2025 results exceeding the market’s revenue expectations, with sales up 27.7% year on year to $39.31 million. The company expects next quarter’s revenue to be around $42 million, close to analysts’ estimates. Its GAAP profit of $0.03 per share was significantly above analysts’ consensus estimates.

Asure Software (ASUR) Q4 CY2025 Highlights:

- Revenue: $39.31 million vs analyst estimates of $38.78 million (27.7% year-on-year growth, 1.4% beat)

- EPS (GAAP): $0.03 vs analyst estimates of -$0.04 (significant beat)

- Adjusted EBITDA: $11.36 million vs analyst estimates of $10.72 million (28.9% margin, 6% beat)

- Revenue Guidance for Q1 CY2026 is $42 million at the midpoint, roughly in line with what analysts were expecting

- EBITDA guidance for Q1 CY2026 is $10.5 million at the midpoint, in line with analyst expectations

- Operating Margin: 4.5%, up from -8.1% in the same quarter last year

- Free Cash Flow was -$14.52 million, down from $1.85 million in the previous quarter

- Billings: $43.49 million at quarter end, up 16.6% year on year

- Market Capitalization: $207.5 million

Company Overview

Operating in the often-overlooked smaller metropolitan markets where HR expertise can be scarce, Asure Software (NASDAQ:ASUR) provides cloud-based human capital management software and services that help small and medium-sized businesses manage payroll, taxes, time tracking, and HR compliance.

Asure's software suite includes five main product lines that work together to reduce administrative burdens for employers throughout the entire employee lifecycle. Its Payroll & Tax solution handles wage calculations, benefits, overtime, garnishments, and direct deposits while ensuring compliance with federal, state, and local tax regulations. The Tax Management Solutions offers specialized tax processing services, including bulk filing for Employee Retention Tax Credits. For tracking work hours, Asure's Time & Attendance product integrates with biometric time clocks and mobile apps that use geo-positioning to verify employee locations.

The company's HR Compliance services provide varying levels of support, from on-demand resources to complete HR outsourcing. A distinctive offering is AsureMarketplace, which connects the company's systems with third-party applications to extend capabilities for both employers and employees, including services like income verification and earned wage access.

Asure follows a dual distribution strategy, selling directly to clients and through partners. Regional payroll providers and trusted SMB advisors (like CPAs and regional banks) can white-label Asure's solutions as "Reseller Partners" or simply refer clients as "Referral Partners." This partnership network has become a primary acquisition source, allowing Asure to expand into specific geographic areas and industry niches while minimizing technology integration risks.

4. HR Software

Modern HR software has two powerful benefits: cost savings and ease of use. For cost savings, businesses large and small much prefer the flexibility of cloud-based, web-browser-delivered software paid for on a subscription basis rather than the hassle and complexity of purchasing and managing on-premise enterprise software. On the usability side, the consumerization of business software creates seamless experiences whereby multiple standalone processes like payroll processing and compliance are aggregated into a single, easy-to-use platform.

Asure Software competes with larger, national players in the HR software space including ADP, Paychex, UKG, Paylocity, Paycor, Paycom, Ceridian, and newer entrants like Gusto. For its time tracking products, it specifically competes with UKG, Paychex, ADP and Time Simplicity.

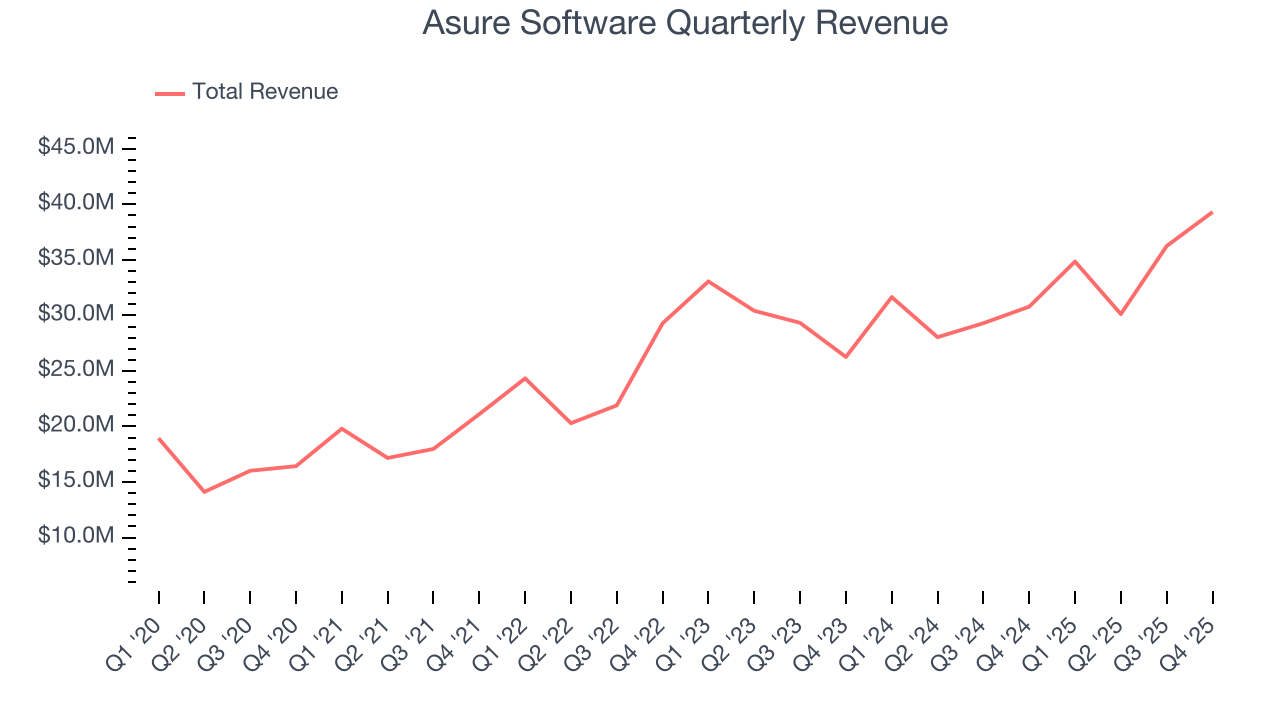

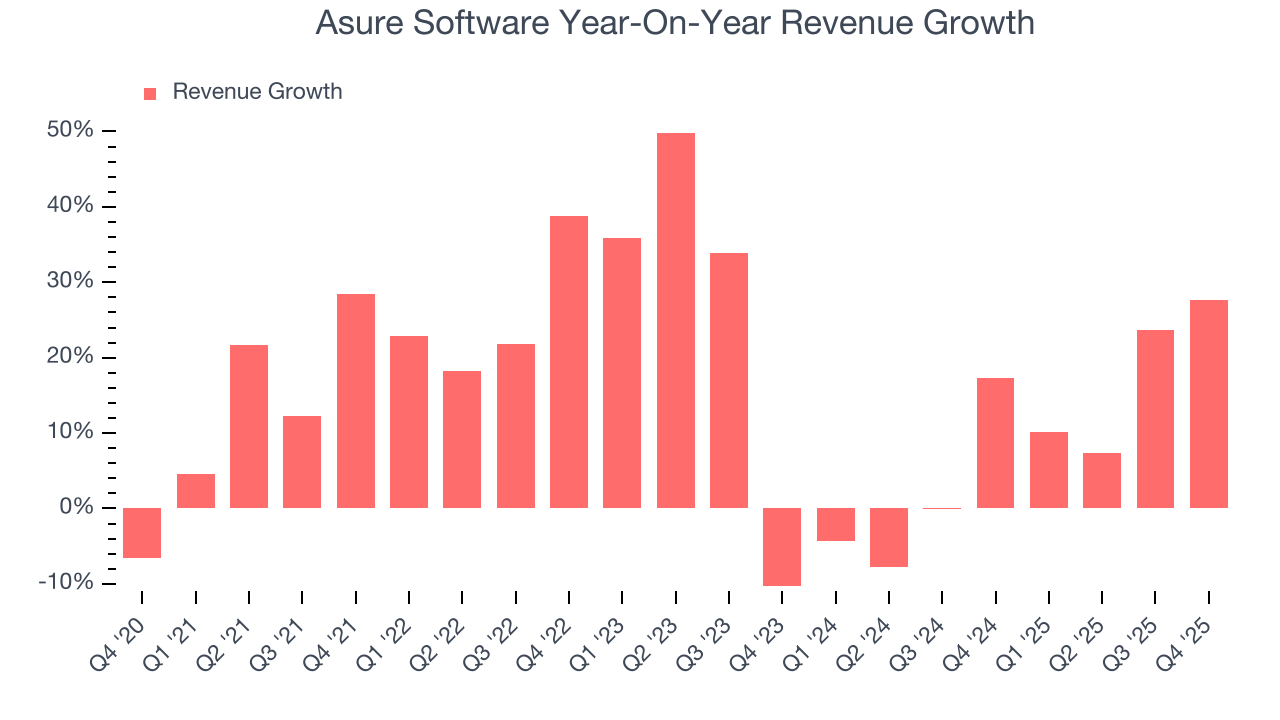

5. Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Over the last five years, Asure Software grew its sales at a 16.5% annual rate. Though this growth is acceptable on an absolute basis, we need to see more than just topline growth for the software sector, which can display significant earnings volatility. This means our bar for the sector is particularly high, reflecting the non-essential and hit-driven nature of the products and services offered. Additionally, five-year CAGR starts around Covid, when revenue was depressed then rebounded.

Long-term growth is the most important, but within software, a half-decade historical view may miss new innovations or demand cycles. Asure Software’s recent performance shows its demand has slowed as its annualized revenue growth of 8.6% over the last two years was below its five-year trend. We’re wary when companies in the sector see decelerations in revenue growth, as it could signal changing consumer tastes aided by low switching costs.

This quarter, Asure Software reported robust year-on-year revenue growth of 27.7%, and its $39.31 million of revenue topped Wall Street estimates by 1.4%. Company management is currently guiding for a 20.5% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 13.5% over the next 12 months. While this projection implies its newer products and services will catalyze better top-line performance, it is still below average for the sector.

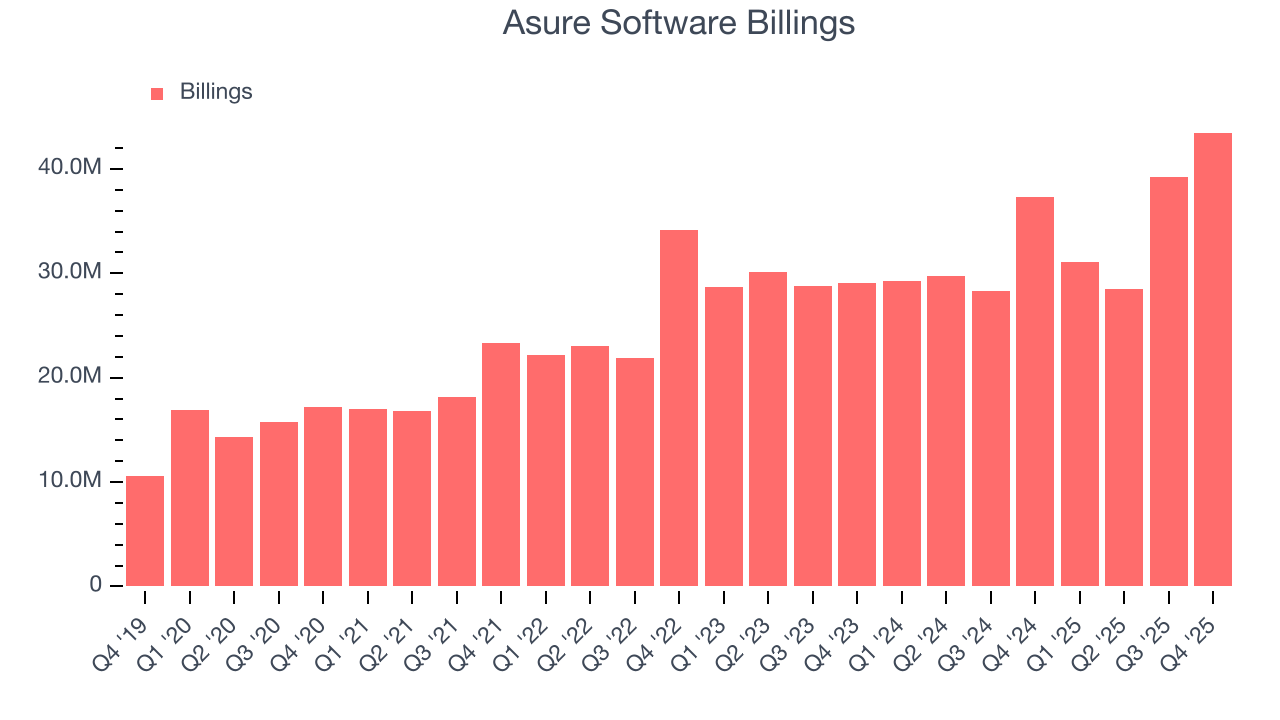

6. Billings

Billings is a non-GAAP metric that is often called “cash revenue” because it shows how much money the company has collected from customers in a certain period. This is different from revenue, which must be recognized in pieces over the length of a contract.

Asure Software’s billings came in at $43.49 million in Q4, and over the last four quarters, its growth slightly lagged the sector as it averaged 14.2% year-on-year increases. This alternate topline metric grew slower than total sales, meaning the company recognizes revenue faster than it collects cash - a headwind for its liquidity that could also signal a slowdown in future revenue growth.

7. Customer Acquisition Efficiency

The customer acquisition cost (CAC) payback period measures the months a company needs to recoup the money spent on acquiring a new customer. This metric helps assess how quickly a business can break even on its sales and marketing investments.

Asure Software is extremely efficient at acquiring new customers, and its CAC payback period checked in at 4.6 months this quarter. The company’s rapid recovery of its customer acquisition costs means it can attempt to spur growth by increasing its sales and marketing investments.

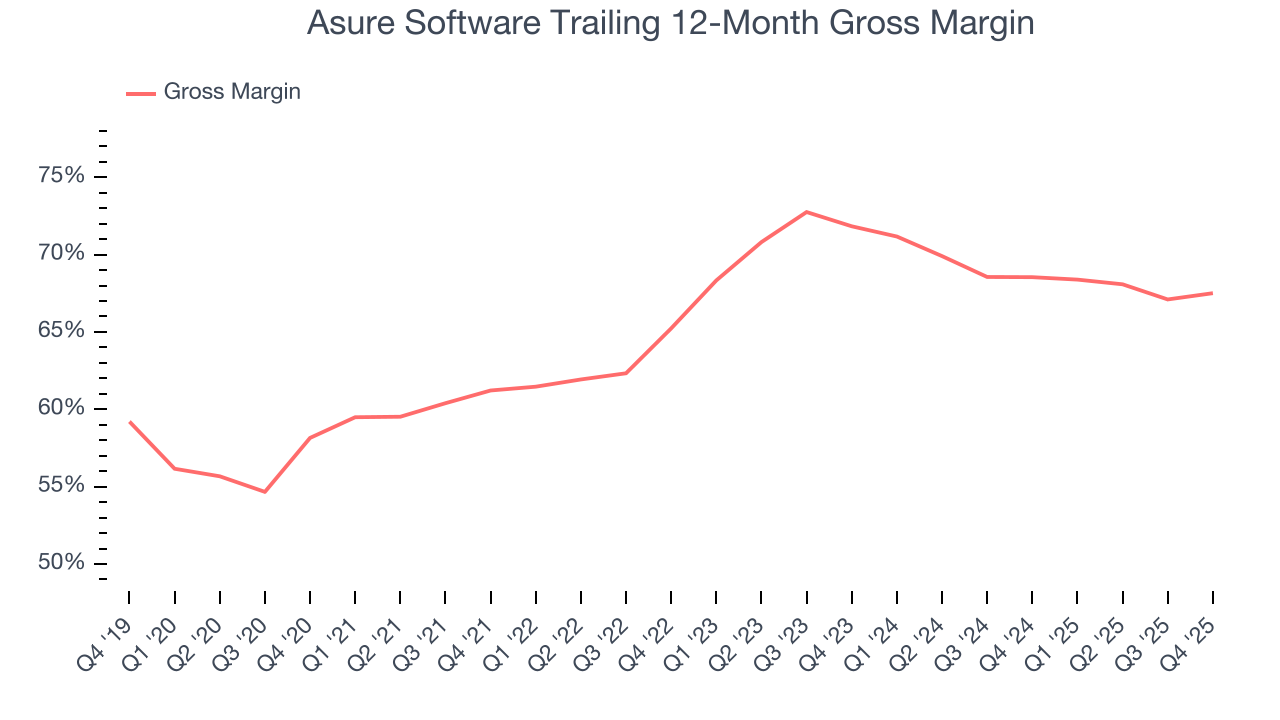

8. Gross Margin & Pricing Power

For software companies like Asure Software, gross profit tells us how much money remains after paying for the base cost of products and services (typically servers, licenses, and certain personnel). These costs are usually low as a percentage of revenue, explaining why software is more lucrative than other sectors.

Asure Software’s gross margin is worse than the software industry average, giving it less room than its competitors to hire new talent that can expand its products and services. As you can see below, it averaged a 67.5% gross margin over the last year. That means Asure Software paid its providers a lot of money ($32.49 for every $100 in revenue) to run its business.

The market not only cares about gross margin levels but also how they change over time because expansion creates firepower for profitability and free cash generation. Asure Software has seen gross margins decline by 4.3 percentage points over the last 2 year, which is among the worst in the software space.

Asure Software’s gross profit margin came in at 69.2% this quarter, up 1.3 percentage points year on year. Zooming out, however, Asure Software’s full-year margin has been trending down over the past 12 months, decreasing by 1 percentage points. If this move continues, it could suggest a more competitive environment with some pressure to lower prices and higher input costs.

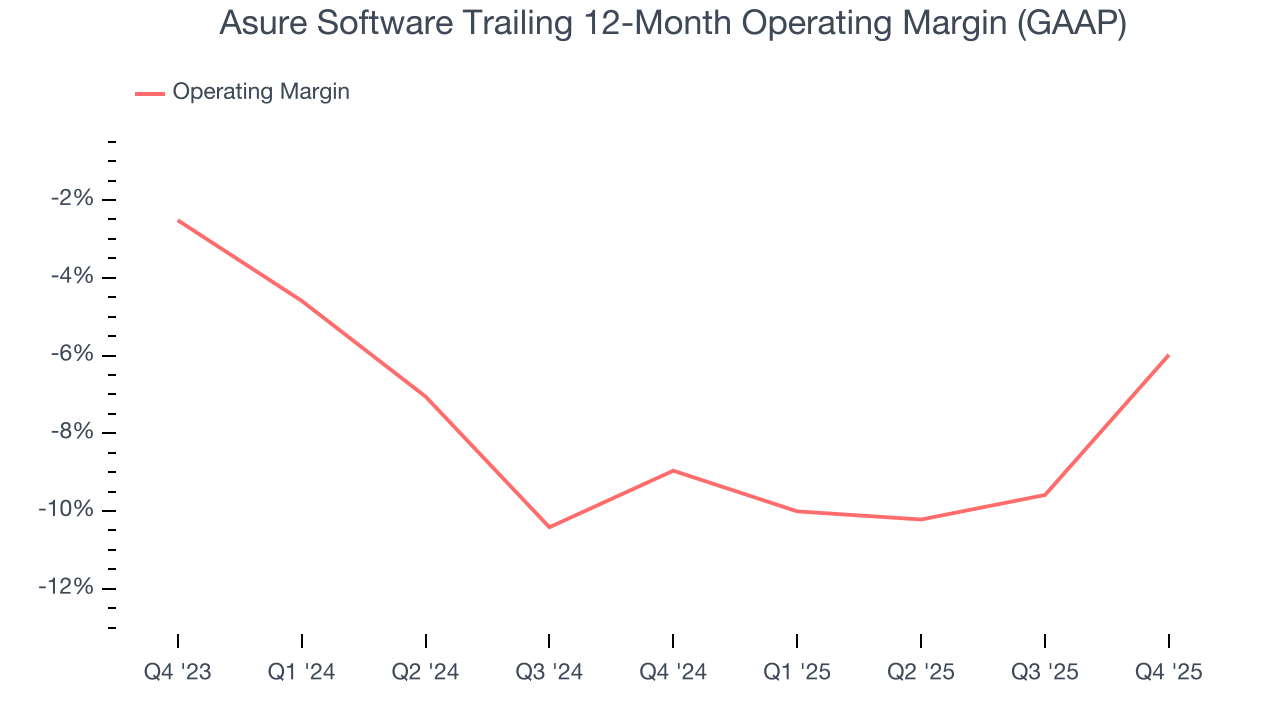

9. Operating Margin

Many software businesses adjust their profits for stock-based compensation (SBC), but we prioritize GAAP operating margin because SBC is a real expense used to attract and retain engineering and sales talent. This is one of the best measures of profitability because it shows how much money a company takes home after developing, marketing, and selling its products.

Although Asure Software was profitable this quarter from an operational perspective, it’s generally struggled over a longer time period. Its expensive cost structure has contributed to an average operating margin of negative 6% over the last year. Unprofitable software companies require extra attention because they spend heaps of money to capture market share. As seen in its historically underwhelming revenue performance, this strategy hasn’t worked so far, and it’s unclear what would happen if Asure Software reeled back its investments. Wall Street seems to think it will face some obstacles, and we tend to agree.

Over the last two years, Asure Software’s expanding sales gave it operating leverage as its margin rose by 3 percentage points. Still, it will take much more for the company to show consistent profitability.

In Q4, Asure Software generated an operating margin profit margin of 4.5%, up 12.6 percentage points year on year. The increase was solid, and because its operating margin rose more than its gross margin, we can infer it was more efficient with expenses such as marketing, R&D, and administrative overhead.

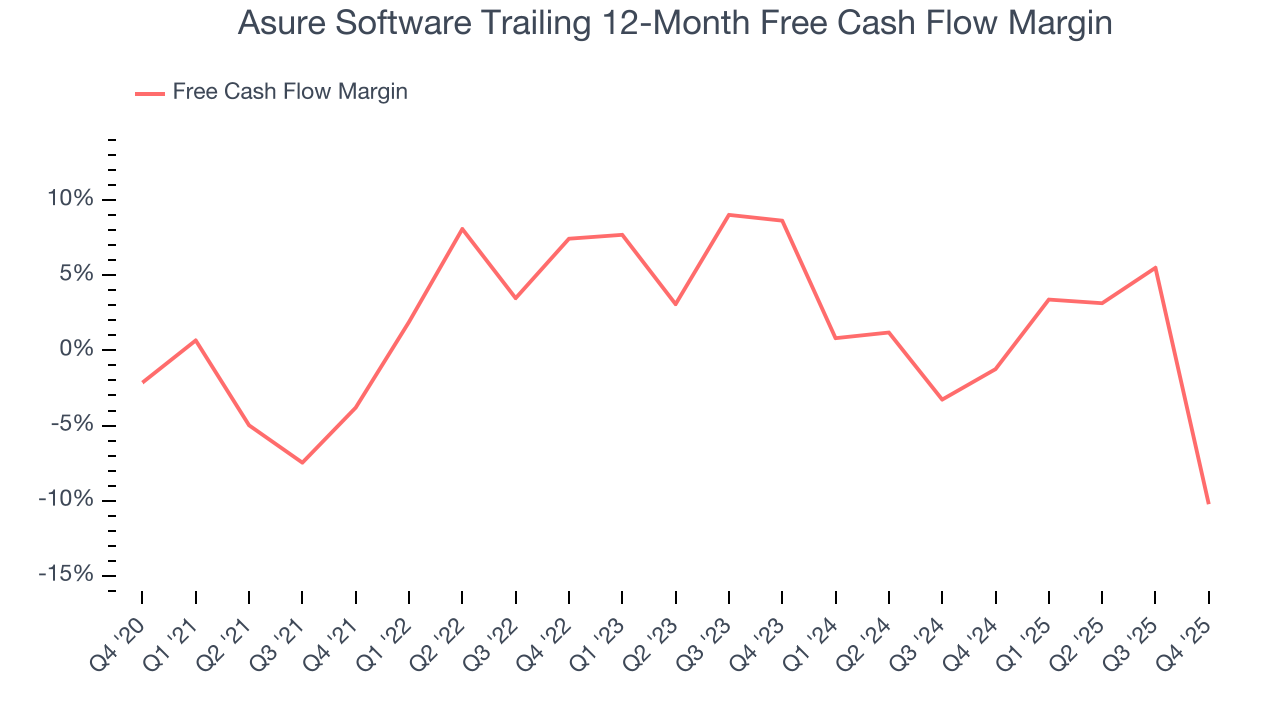

10. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Asure Software’s demanding reinvestments have drained its resources over the last year, putting it in a pinch and limiting its ability to return capital to investors. Its free cash flow margin averaged negative 10.2%, meaning it lit $10.23 of cash on fire for every $100 in revenue.

Asure Software burned through $14.52 million of cash in Q4, equivalent to a negative 36.9% margin. The company’s cash flow turned negative after being positive in the same quarter last year, prompting us to pay closer attention. Short-term fluctuations typically aren’t a big deal because investment needs can be seasonal, but we’ll be watching to see if the trend extrapolates into future quarters.

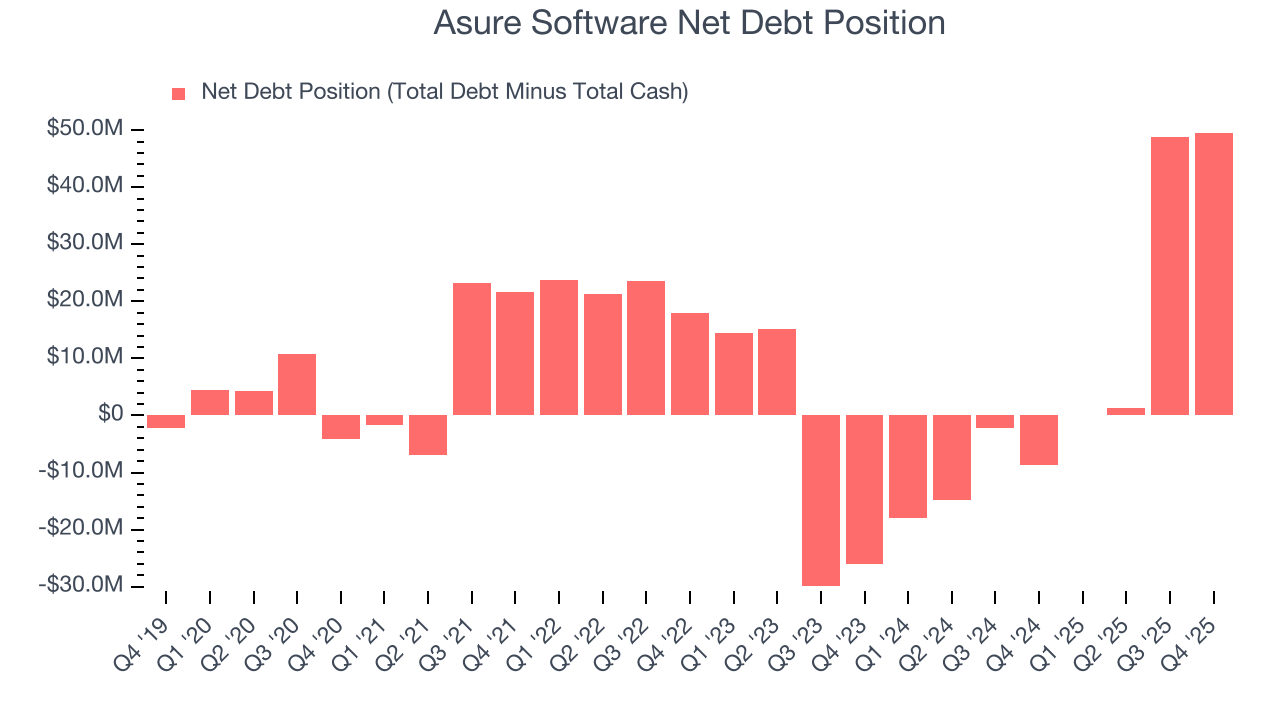

11. Balance Sheet Risk

As long-term investors, the risk we care about most is the permanent loss of capital, which can happen when a company goes bankrupt or raises money from a disadvantaged position. This is separate from short-term stock price volatility, something we are much less bothered by.

Asure Software burned through $14.38 million of cash over the last year, and its $74.8 million of debt exceeds the $25.24 million of cash on its balance sheet. This is a deal breaker for us because indebted loss-making companies spell trouble.

Unless the Asure Software’s fundamentals change quickly, it might find itself in a position where it must raise capital from investors to continue operating. Whether that would be favorable is unclear because dilution is a headwind for shareholder returns.

We remain cautious of Asure Software until it generates consistent free cash flow or any of its announced financing plans materialize on its balance sheet.

12. Key Takeaways from Asure Software’s Q4 Results

We were impressed by how significantly Asure Software blew past analysts’ billings expectations this quarter. We were also glad its EBITDA outperformed Wall Street’s estimates. Overall, we think this was a decent quarter with some key metrics above expectations. The stock traded up 7.6% to $8.37 immediately following the results.

13. Is Now The Time To Buy Asure Software?

Updated: March 23, 2026 at 10:14 PM EDT

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in Asure Software.

Asure Software’s business quality ultimately falls short of our standards. To kick things off, its revenue growth was mediocre over the last five years, and analysts expect its demand to deteriorate over the next 12 months. While its efficient sales strategy allows it to target and onboard new users at scale, the downside is its expanding operating margin shows it’s becoming more efficient at building and selling its software. On top of that, its low free cash flow margins give it little breathing room.

Asure Software’s price-to-sales ratio based on the next 12 months is 1.5x. While this valuation is reasonable, we don’t really see a big opportunity at the moment. We're pretty confident there are more exciting stocks to buy at the moment.

Wall Street analysts have a consensus one-year price target of $13.38 on the company (compared to the current share price of $8.58).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.