Leonardo DRS (DRS)

Leonardo DRS catches our eye. Its eye-popping 25% annualized EPS growth over the last two years has significantly outpaced its peers.― StockStory Analyst Team

1. News

2. Summary

Why Leonardo DRS Is Interesting

Developing submarine detection systems for the U.S. Navy, Leonardo DRS (NASDAQ:DRS) is a provider of defense systems, electronics, and military support services.

- ROIC punches in at 13.2%, illustrating management’s expertise in identifying profitable investments

- Efficient business processes manifest in an operating margin of 10.9%, higher than most industrials companies, and its operating leverage amplified its profits over the last five years

- A downside is its muted 5.6% annual revenue growth over the last five years shows its demand lagged behind its industrials peers

Leonardo DRS shows some potential. You should keep tabs on this company.

Why Should You Watch Leonardo DRS

Leonardo DRS is trading at $45.00 per share, or 36.7x forward P/E. This multiple is higher than most industrials companies.

Leonardo DRS can improve its fundamentals over time by putting up good numbers quarter after quarter, year after year. Once that happens, we’ll be happy to recommend the stock.

3. Leonardo DRS (DRS) Research Report: Q4 CY2025 Update

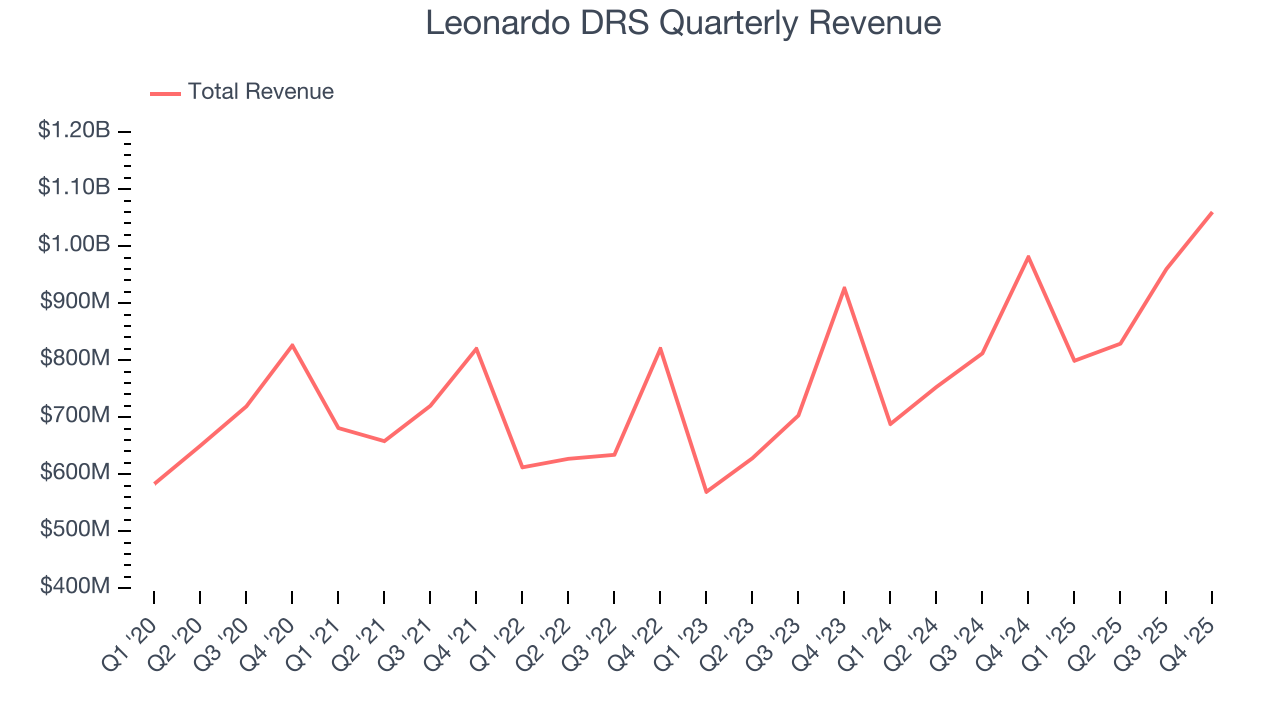

Aerospace and defense company Leonardo DRS (NASDAQ:DRS) announced better-than-expected revenue in Q4 CY2025, with sales up 8.1% year on year to $1.06 billion. The company’s full-year revenue guidance of $3.9 billion at the midpoint came in 2% above analysts’ estimates. Its non-GAAP profit of $0.42 per share was 13.2% above analysts’ consensus estimates.

Leonardo DRS (DRS) Q4 CY2025 Highlights:

- Revenue: $1.06 billion vs analyst estimates of $990.8 million (8.1% year-on-year growth, 7% beat)

- Adjusted EPS: $0.42 vs analyst estimates of $0.37 (13.2% beat)

- Adjusted EBITDA: $158 million vs analyst estimates of $147.1 million (14.9% margin, 7.4% beat)

- Adjusted EPS guidance for the upcoming financial year 2026 is $1.23 at the midpoint, missing analyst estimates by 2.1%

- EBITDA guidance for the upcoming financial year 2026 is $515 million at the midpoint, above analyst estimates of $507.8 million

- Operating Margin: 11.9%, in line with the same quarter last year

- Free Cash Flow Margin: 35.5%, down from 42.2% in the same quarter last year

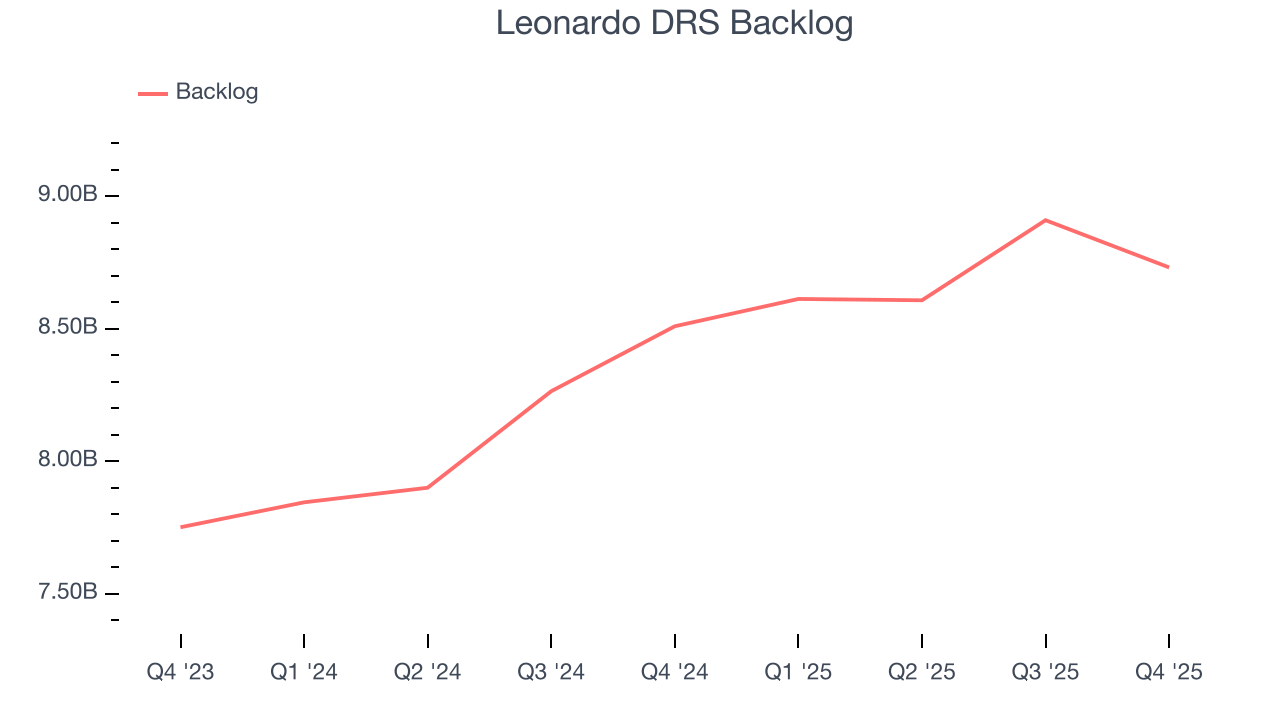

- Backlog: $8.73 billion at quarter end, up 2.6% year on year

- Market Capitalization: $10.15 billion

Company Overview

Developing submarine detection systems for the U.S. Navy, Leonardo DRS (NASDAQ:DRS) is a provider of defense systems, electronics, and military support services.

Specifically, the company specializing in mission systems, sensing, and computing solutions. In the realm of mission systems, its offerings include ship propulsion systems and comprehensive logistic solutions. For sensing and computing, it delivers state-of-the-art radars, satellite surveillance, and robust communication networks.

The U.S. Department of Defense stands as Leonardo DRS's largest customer, with additional clientele spanning aerospace and defense contractors, intelligence agencies, and various industrial markets. Their sensor technologies and propulsion systems are integral to Navy shipbuilding programs and are widely utilized by U.S. government agencies and global defense contractors. Beyond defense, Leonardo DRS's products have significant commercial and industrial applications, including thermography, preventative maintenance, medical diagnostics, and surveillance.

Leonardo DRS engages in strategic contracts and partnerships with defense agencies and government bodies, securing long-term commitments for its products. Additionally, Leonardo DRS expands its market reach and revenue streams through the sale of its products to commercial entities. The company's revenue generation strategy includes leveraging these strategic contracts and direct sales, along with providing aftermarket services and parts, which further support recurring revenue.

4. Defense Contractors

Defense contractors typically require technical expertise and government clearance. Companies in this sector can also enjoy long-term contracts with government bodies, leading to more predictable revenues. Combined, these factors create high barriers to entry and can lead to limited competition. Lately, geopolitical tensions–whether it be Russia’s invasion of Ukraine or China’s aggression towards Taiwan–highlight the need for defense spending. On the other hand, demand for these products can ebb and flow with defense budgets and even who is president, as different administrations can have vastly different ideas of how to allocate federal funds.

Leonardo DRS’s competitors include Raytheon (NYSE:RTX), Lockheed Martin (NYSE:LMT), and Northrop Grumman (NYSE:NOC).

5. Revenue Growth

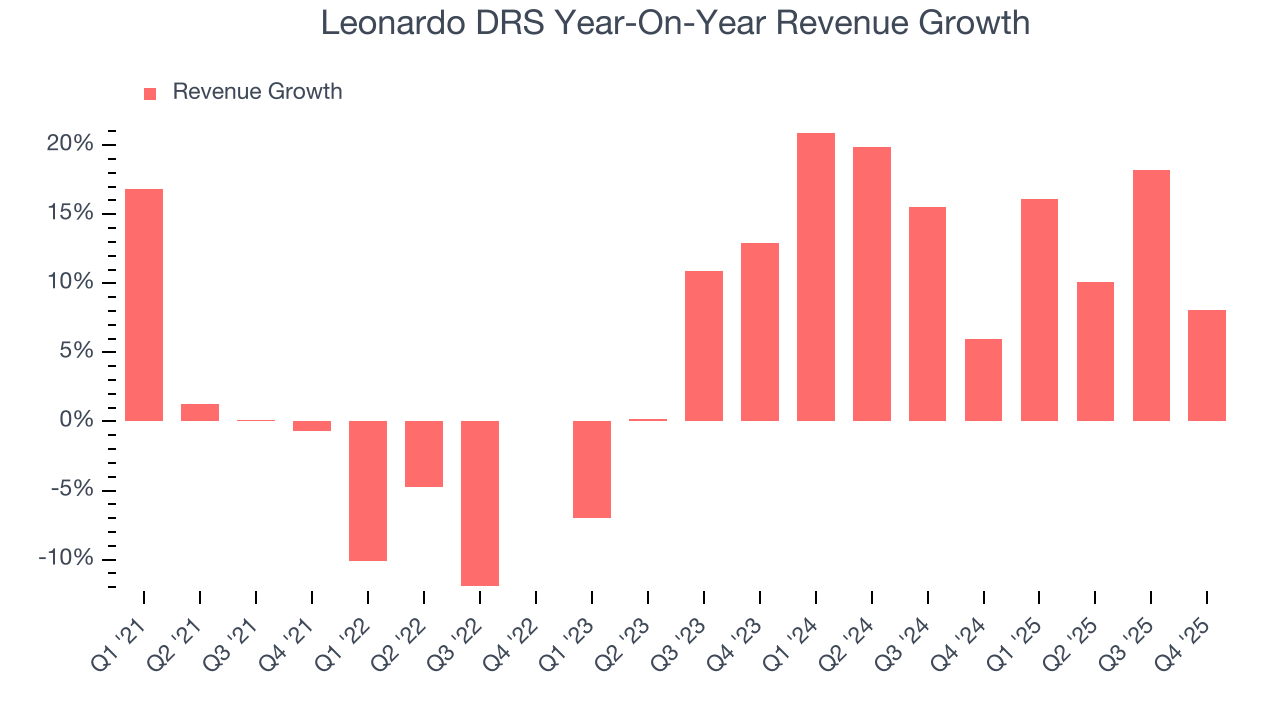

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Regrettably, Leonardo DRS’s sales grew at a tepid 5.6% compounded annual growth rate over the last five years. This wasn’t a great result compared to the rest of the industrials sector, but there are still things to like about Leonardo DRS.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Leonardo DRS’s annualized revenue growth of 13.6% over the last two years is above its five-year trend, suggesting its demand recently accelerated.

We can dig further into the company’s revenue dynamics by analyzing its backlog, or the value of its outstanding orders that have not yet been executed or delivered. Leonardo DRS’s backlog reached $8.73 billion in the latest quarter and averaged 7.8% year-on-year growth over the last two years. Because this number is lower than its revenue growth, we can see the company fulfilled orders at a faster rate than it added new orders to the backlog. This implies Leonardo DRS was operating efficiently but raises questions about the health of its sales pipeline.

This quarter, Leonardo DRS reported year-on-year revenue growth of 8.1%, and its $1.06 billion of revenue exceeded Wall Street’s estimates by 7%.

Looking ahead, sell-side analysts expect revenue to grow 5.3% over the next 12 months, a deceleration versus the last two years. This projection doesn't excite us and implies its products and services will face some demand challenges. At least the company is tracking well in other measures of financial health.

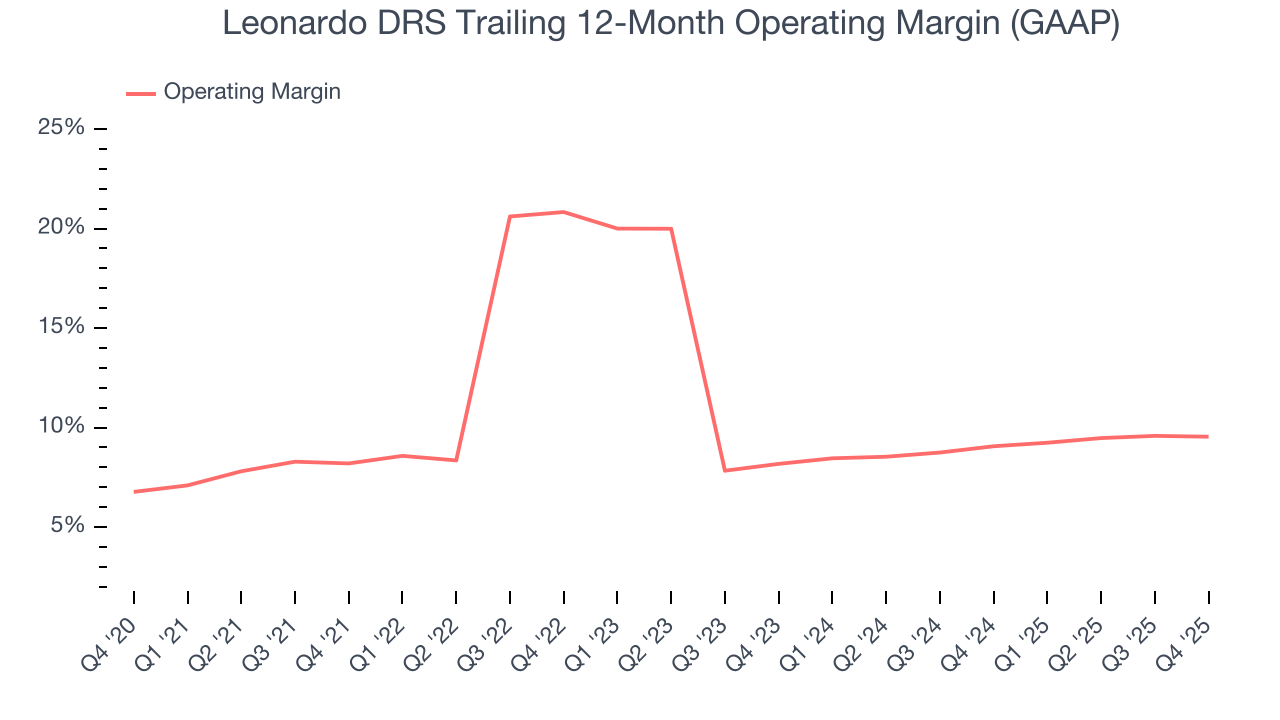

6. Operating Margin

Leonardo DRS has managed its cost base well over the last five years. It demonstrated solid profitability for an industrials business, producing an average operating margin of 10.9%.

Looking at the trend in its profitability, Leonardo DRS’s operating margin rose by 1.3 percentage points over the last five years, as its sales growth gave it operating leverage.

This quarter, Leonardo DRS generated an operating margin profit margin of 11.9%, in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

7. Cash Is King

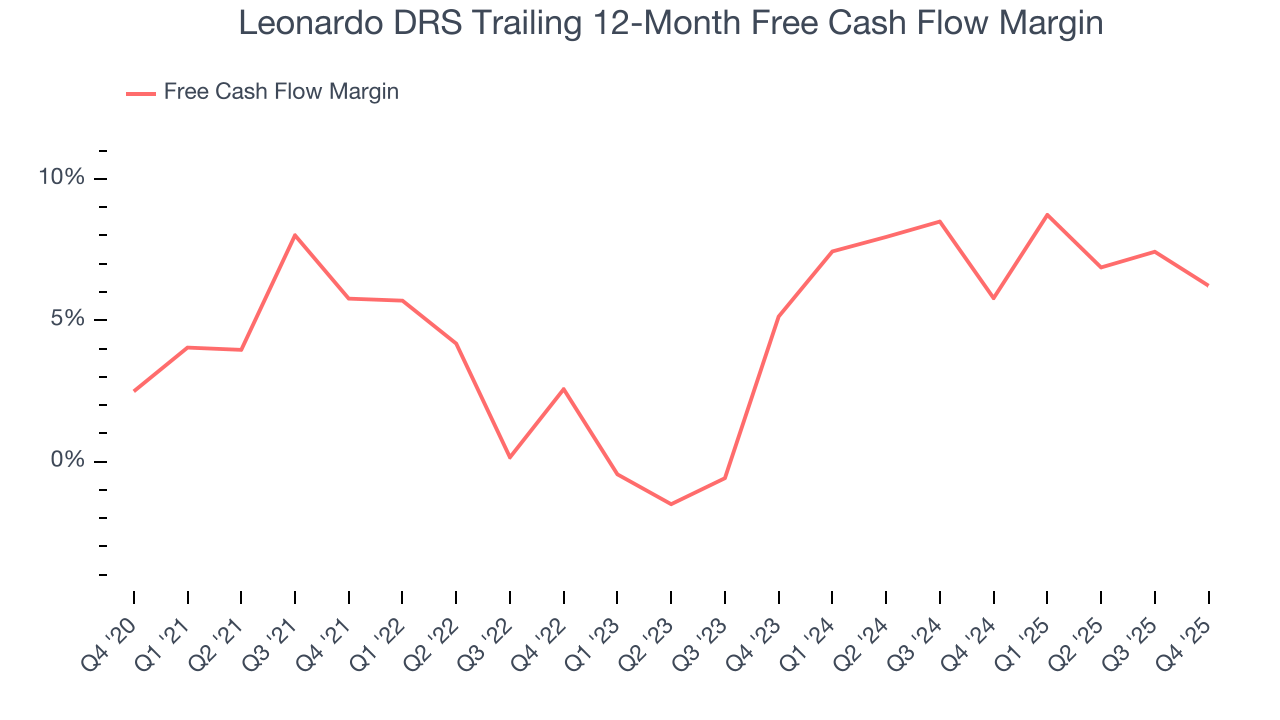

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Leonardo DRS has shown mediocre cash profitability over the last five years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 5.2%, subpar for an industrials business.

Leonardo DRS’s free cash flow clocked in at $376 million in Q4, equivalent to a 35.5% margin. The company’s cash profitability regressed as it was 6.7 percentage points lower than in the same quarter last year, but it’s still above its five-year average. We wouldn’t put too much weight on this quarter’s decline because investment needs can be seasonal, causing short-term swings. Long-term trends carry greater meaning.

8. Balance Sheet Assessment

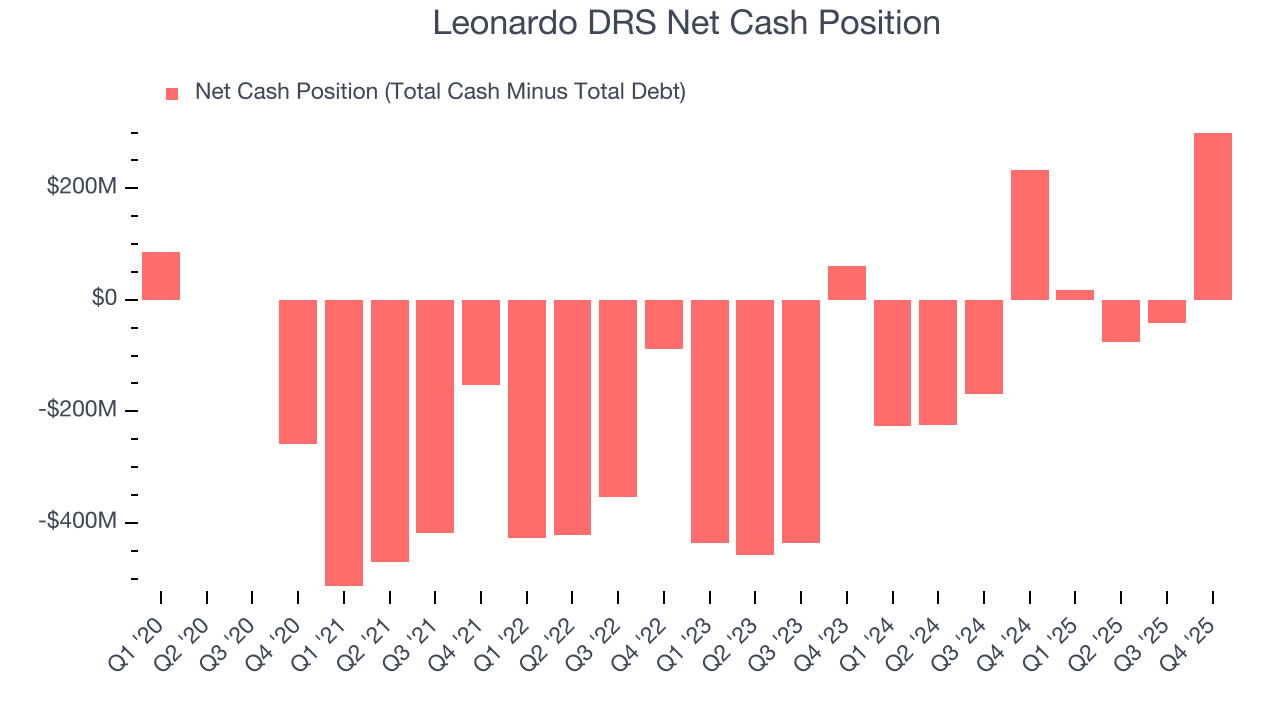

Companies with more cash than debt have lower bankruptcy risk.

Leonardo DRS is a profitable, well-capitalized company with $647 million of cash and $347 million of debt on its balance sheet. This $300 million net cash position is 3% of its market cap and gives it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

9. Key Takeaways from Leonardo DRS’s Q4 Results

We were impressed by how significantly Leonardo DRS blew past analysts’ revenue expectations this quarter. We were also glad its EBITDA outperformed Wall Street’s estimates. Zooming out, we think this was a good print with some key areas of upside. The stock traded up 3% to $39.30 immediately following the results.

10. Is Now The Time To Buy Leonardo DRS?

Updated: March 15, 2026 at 11:48 PM EDT

Are you wondering whether to buy Leonardo DRS or pass? We urge investors to not only consider the latest earnings results but also longer-term business quality and valuation as well.

There are things to like about Leonardo DRS. Although its revenue growth was uninspiring over the last five years, its growth over the next 12 months is expected to be higher. And while Leonardo DRS’s diminishing returns show management's recent bets still have yet to bear fruit, its astounding EPS growth over the last two years shows its profits are trickling down to shareholders. On top of that, its solid ROIC suggests it has grown profitably in the past.

Leonardo DRS’s P/E ratio based on the next 12 months is 36.7x. This valuation tells us it’s a bit of a market darling with a lot of good news priced in. Leonardo DRS is a good one to add to your watchlist - there are companies featuring superior fundamentals at the moment.

Wall Street analysts have a consensus one-year price target of $50.90 on the company (compared to the current share price of $45.00).