Intuit (INTU)

Intuit catches our eye. Its stellar unit economics and efficient sales strategy tee it up for immense long-term profits.― StockStory Analyst Team

1. News

2. Summary

Why Intuit Is Interesting

Originally named after its founding product "Intuitive for the first-time user," Intuit (NASDAQ:INTU) provides financial management software and services including TurboTax, QuickBooks, Credit Karma, and Mailchimp to help consumers and small businesses manage their finances.

- Healthy operating margin shows it’s a well-run company with efficient processes, and its profits increased over the last year as it scaled

- Impressive free cash flow profitability enables the company to fund new investments or reward investors with share buybacks/dividends

- A downside is its operating margin improvement of 4.8 percentage points over the last year demonstrates its ability to scale efficiently

Intuit shows some potential. If you like the stock, the price seems reasonable.

Why Is Now The Time To Buy Intuit?

At $439.44 per share, Intuit trades at 5.5x forward price-to-sales. When stacked up against other software companies, we think Intuit’s multiple is fair for the fundamentals you get.

If you think the market is undervaluing the company, now could be a good time to build a position.

3. Intuit (INTU) Research Report: Q4 CY2025 Update

Financial technology platform Intuit (NASDAQ:INTU) reported revenue ahead of Wall Street’s expectations in Q4 CY2025, with sales up 17.4% year on year to $4.65 billion. The company expects next quarter’s revenue to be around $8.54 billion, close to analysts’ estimates. Its non-GAAP profit of $4.15 per share was 12.7% above analysts’ consensus estimates.

Intuit (INTU) Q4 CY2025 Highlights:

- Revenue: $4.65 billion vs analyst estimates of $4.54 billion (17.4% year-on-year growth, 2.5% beat)

- Adjusted EPS: $4.15 vs analyst estimates of $3.68 (12.7% beat)

- Adjusted Operating Income: $1.55 billion vs analyst estimates of $1.39 billion (33.3% margin, 11.1% beat)

- The company reconfirmed its revenue guidance for the full year of $21.09 billion at the midpoint

- Management reiterated its full-year Adjusted EPS guidance of $23.08 at the midpoint

- Operating Margin: 18.4%, up from 15% in the same quarter last year

- Free Cash Flow Margin: 32.8%, up from 15.4% in the previous quarter

- Billings: $4.75 billion at quarter end, up 15.8% year on year

- Market Capitalization: $106.1 billion

Company Overview

Originally named after its founding product "Intuitive for the first-time user," Intuit (NASDAQ:INTU) provides financial management software and services including TurboTax, QuickBooks, Credit Karma, and Mailchimp to help consumers and small businesses manage their finances.

Intuit operates a comprehensive ecosystem of financial tools organized into four key segments. The Small Business and Self-Employed segment offers QuickBooks for accounting and financial management, payment processing solutions, payroll services, and Mailchimp for marketing automation. The Consumer segment revolves around TurboTax, helping individuals and small businesses file their taxes with varying levels of assistance. The Credit Karma segment provides a personal finance platform where consumers can access credit scores, financial monitoring tools, and personalized recommendations for financial products. The ProTax segment serves professional accountants with specialized tax preparation software like Lacerte and ProSeries.

Intuit's business model leverages artificial intelligence to create what it calls "done for you" experiences that aim to eliminate manual work for customers. For instance, a small restaurant owner might use QuickBooks to automatically categorize expenses, process employee payroll, and generate financial reports, while using Mailchimp to create targeted email campaigns to regular customers. Meanwhile, an individual consumer might use TurboTax to file taxes with AI-guided assistance and Credit Karma to monitor their credit score and receive personalized loan offers.

The company generates revenue through subscription services, transaction fees from payment processing, and commissions when users acquire financial products through platforms like Credit Karma. Intuit's strategy centers on creating an interconnected platform where data flows between its products, creating more value for customers who use multiple Intuit services.

4. Tax Software

The demand for easy to use, integrated cloud based finance software that integrates tax and accounting operations continues to rise in tandem with the difficulty workers find trying to use existing accounting tools like spreadsheets given the growing volume of finance data littered across a multitude of enterprise applications. A related demand driver is the secular increase of e-commerce and rising adoption of modern point of sales and payments platforms which easily integrate with backend financial software.

Intuit competes with financial software providers like Microsoft (NASDAQ:MSFT) for small business accounting, H&R Block (NYSE:HRB) and private tax preparation services in the tax preparation space, Experian (OTCMKTS:EXPGY) and TransUnion (NYSE:TRU) in the credit monitoring market, and companies like Constant Contact and Adobe (NASDAQ:ADBE) in marketing automation.

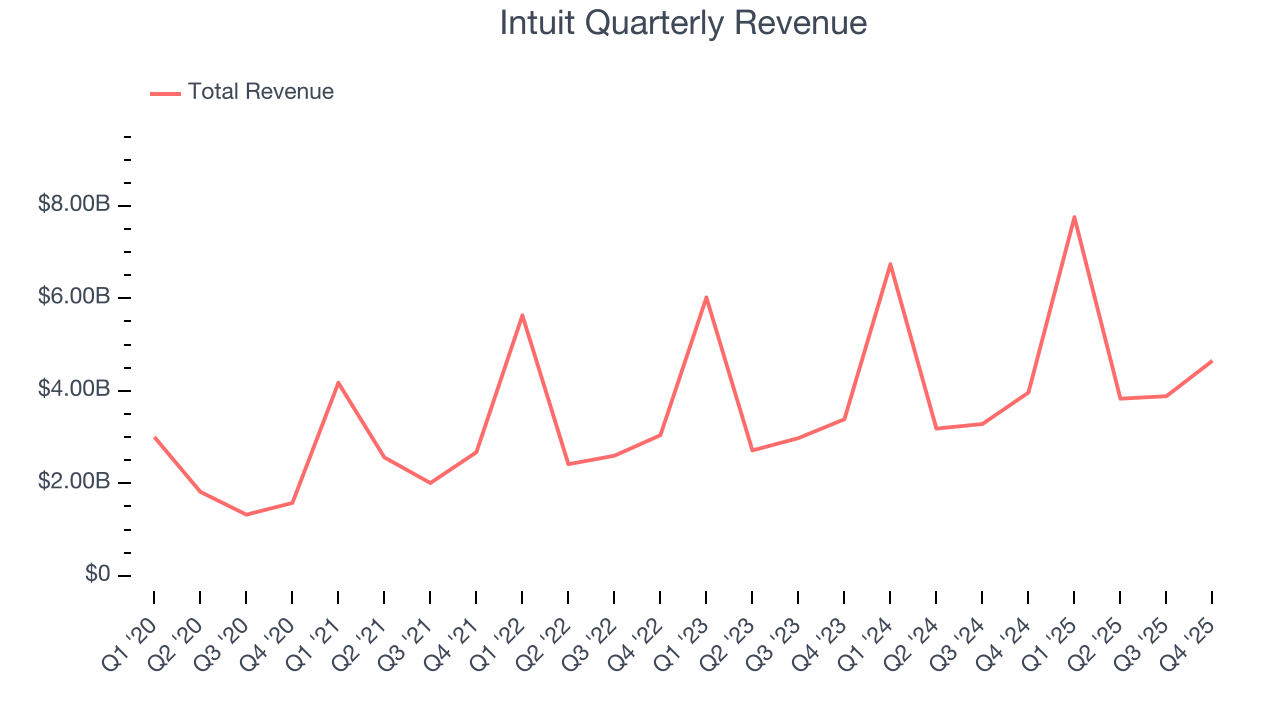

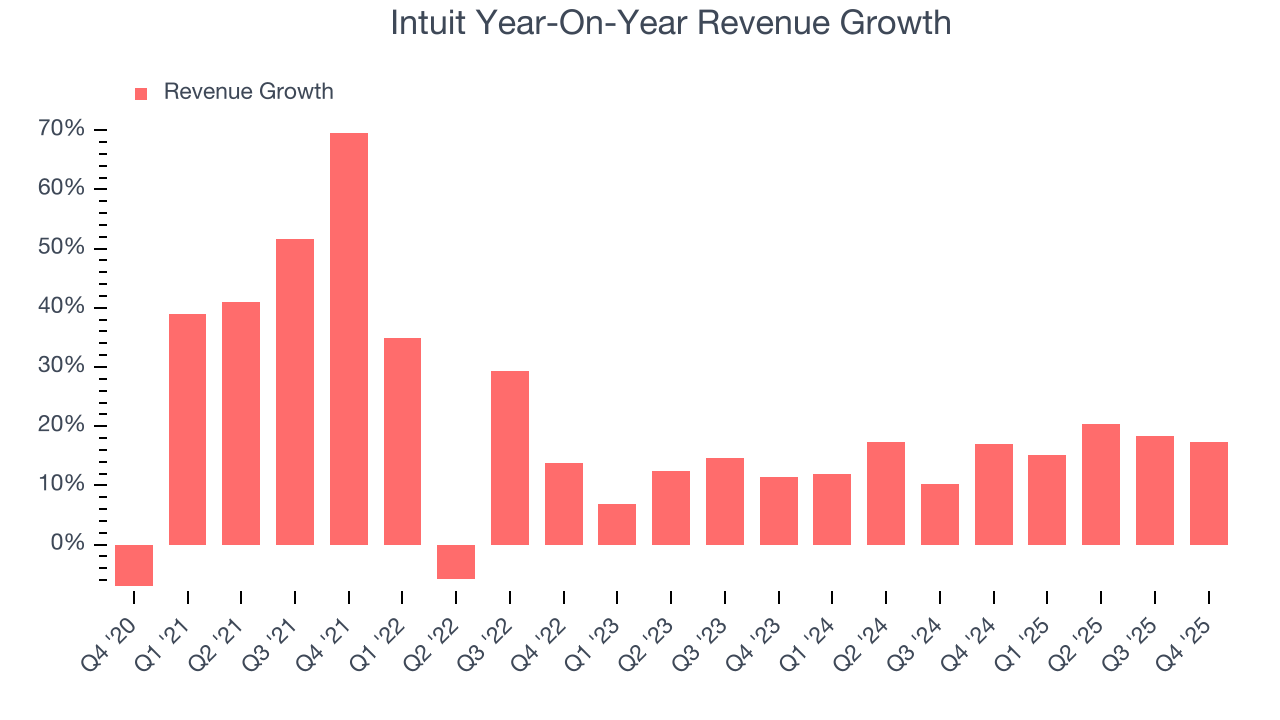

5. Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Over the last five years, Intuit grew its sales at a decent 21.1% compounded annual growth rate. Its growth was slightly above the average software company and shows its offerings resonate with customers.

Long-term growth is the most important, but within software, a half-decade historical view may miss new innovations or demand cycles. Intuit’s annualized revenue growth of 15.5% over the last two years is below its five-year trend, but we still think the results were respectable.

This quarter, Intuit reported year-on-year revenue growth of 17.4%, and its $4.65 billion of revenue exceeded Wall Street’s estimates by 2.5%. Company management is currently guiding for a 10.1% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 11.1% over the next 12 months, a deceleration versus the last two years. This projection doesn't excite us and indicates its products and services will see some demand headwinds. At least the company is tracking well in other measures of financial health.

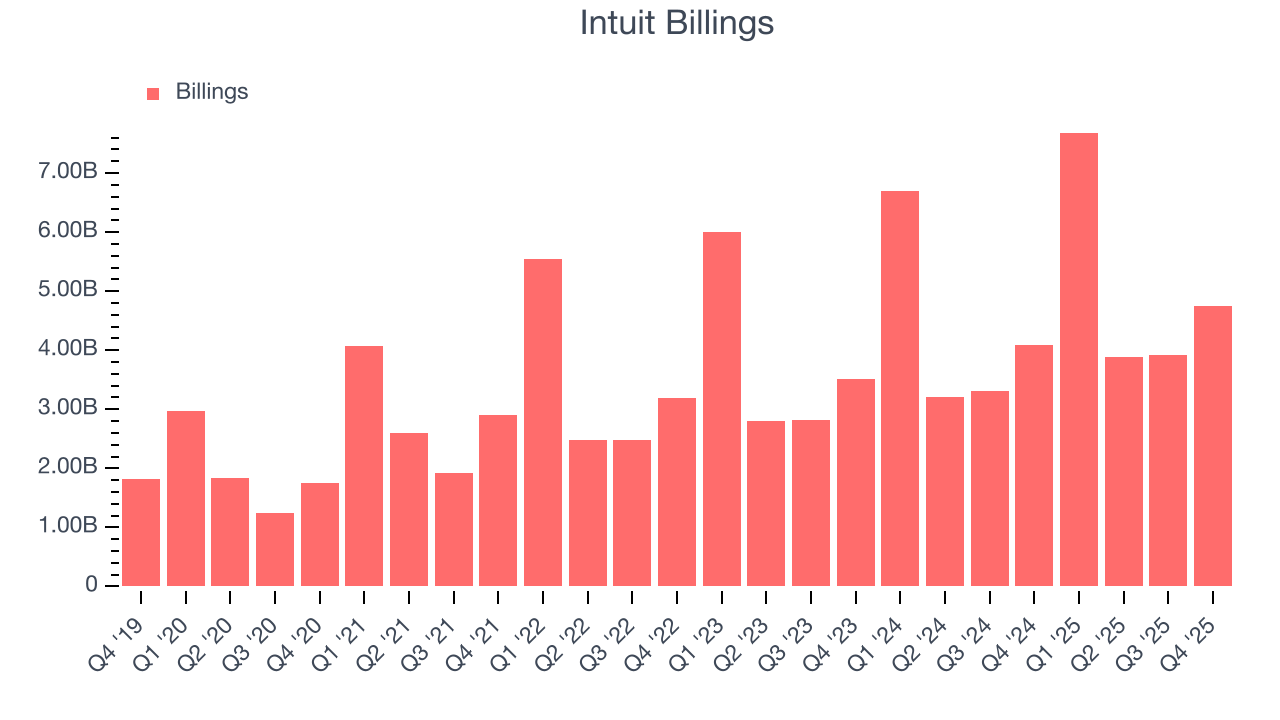

6. Billings

Billings is a non-GAAP metric that is often called “cash revenue” because it shows how much money the company has collected from customers in a certain period. This is different from revenue, which must be recognized in pieces over the length of a contract.

Intuit’s billings punched in at $4.75 billion in Q4, and over the last four quarters, its growth was solid as it averaged 17.6% year-on-year increases. This performance aligned with its total sales growth, indicating robust customer demand. The cash collected from customers also enhances liquidity and provides a solid foundation for future investments and growth.

7. Customer Acquisition Efficiency

The customer acquisition cost (CAC) payback period represents the months required to recover the cost of acquiring a new customer. Essentially, it’s the break-even point for sales and marketing investments. A shorter CAC payback period is ideal, as it implies better returns on investment and business scalability.

Intuit is very efficient at acquiring new customers, and its CAC payback period checked in at 23.4 months this quarter. The company’s rapid recovery of its customer acquisition costs indicates it has a highly differentiated product offering and a strong brand reputation due to its scale. These dynamics give Intuit more resources to pursue new product initiatives while maintaining the flexibility to increase its sales and marketing investments.

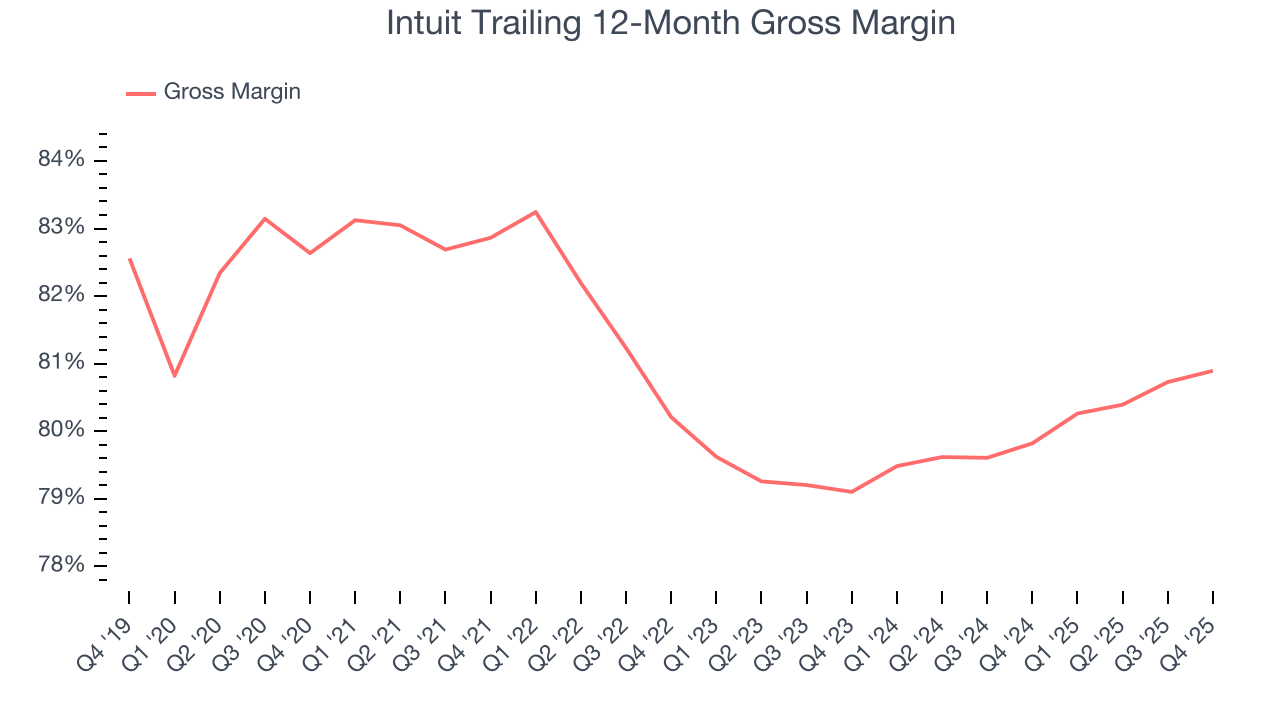

8. Gross Margin & Pricing Power

Software is eating the world. It’s one of our favorite business models because once you develop the product, it usually doesn’t cost much to provide it as an ongoing service. These minimal costs can include servers, licenses, and certain personnel.

Intuit’s robust unit economics are better than the broader software industry, an output of its asset-lite business model and pricing power. They also enable the company to fund large investments in new products and sales during periods of rapid growth to achieve higher profits in the future. As you can see below, it averaged an excellent 80.9% gross margin over the last year. That means Intuit only paid its providers $19.10 for every $100 in revenue.

The market not only cares about gross margin levels but also how they change over time because expansion creates firepower for profitability and free cash generation. Intuit has seen gross margins improve by 1.8 percentage points over the last 2 year, which is solid in the software space.

In Q4, Intuit produced a 78.5% gross profit margin, up 1.2 percentage points year on year. Intuit’s full-year margin has also been trending up over the past 12 months, increasing by 1.1 percentage points. If this move continues, it could suggest better unit economics due to more leverage from its growing sales on the fixed portion of its cost of goods sold (such as servers).

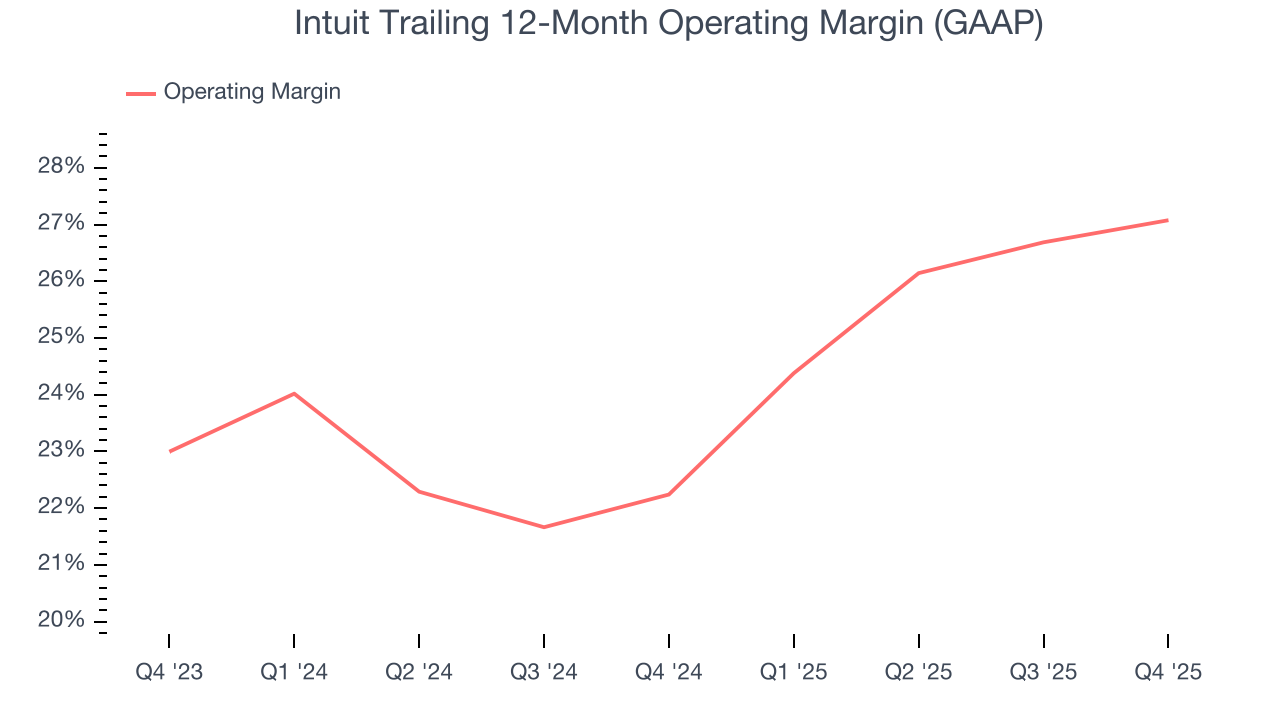

9. Operating Margin

Many software businesses adjust their profits for stock-based compensation (SBC), but we prioritize GAAP operating margin because SBC is a real expense used to attract and retain engineering and sales talent. This metric shows how much revenue remains after accounting for all core expenses – everything from the cost of goods sold to sales and R&D.

Intuit has been a well-oiled machine over the last year. It demonstrated elite profitability for a software business, boasting an average operating margin of 27.1%. This result isn’t surprising as its high gross margin gives it a favorable starting point.

Analyzing the trend in its profitability, Intuit’s operating margin rose by 4.8 percentage points over the last two years, as its sales growth gave it operating leverage.

In Q4, Intuit generated an operating margin profit margin of 18.4%, up 3.4 percentage points year on year. The increase was encouraging, and because its operating margin rose more than its gross margin, we can infer it was more efficient with expenses such as marketing, R&D, and administrative overhead.

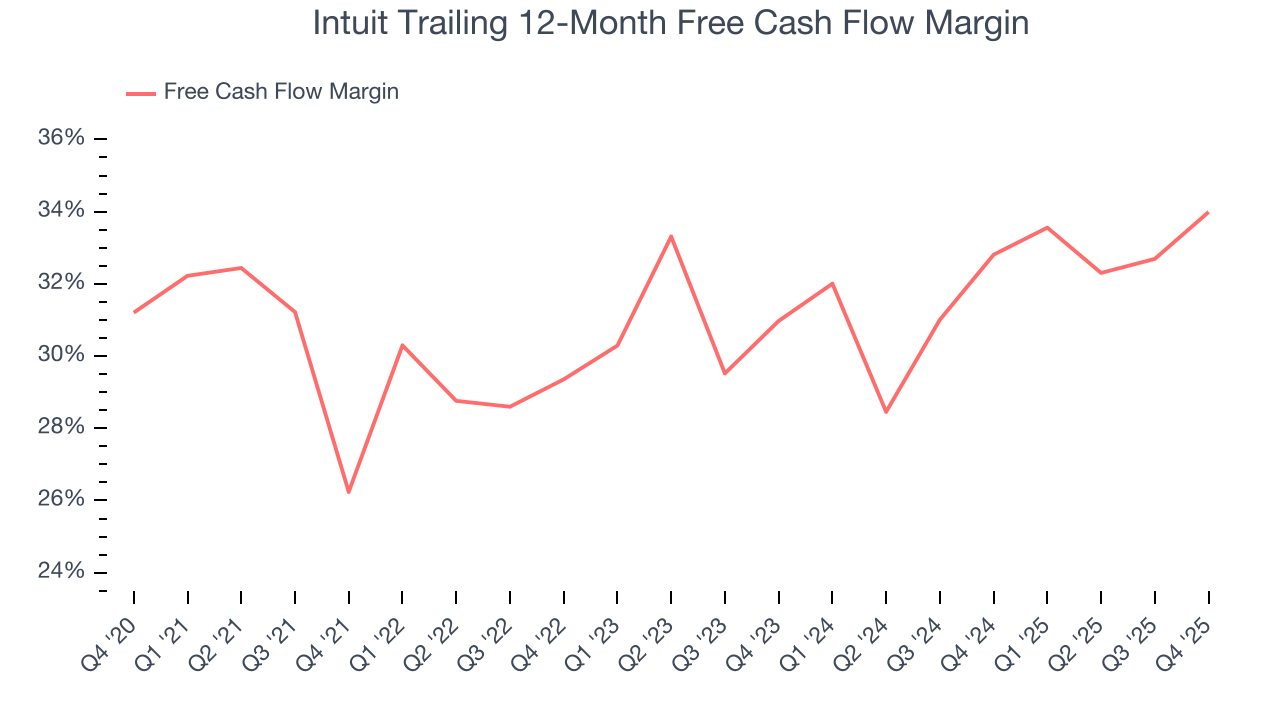

10. Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Intuit has shown terrific cash profitability, driven by its lucrative business model and cost-effective customer acquisition strategy that enable it to stay ahead of the competition through investments in new products rather than sales and marketing. The company’s free cash flow margin was among the best in the software sector, averaging an eye-popping 34% over the last year.

Intuit’s free cash flow clocked in at $1.52 billion in Q4, equivalent to a 32.8% margin. This result was good as its margin was 6.6 percentage points higher than in the same quarter last year, but we note it was lower than its one-year cash profitability. Nevertheless, we wouldn’t read too much into a single quarter because investment needs can be seasonal, causing short-term swings. Long-term trends carry greater meaning.

Over the next year, analysts predict Intuit’s cash conversion will slightly fall. Their consensus estimates imply its free cash flow margin of 34% for the last 12 months will decrease to 30.4%.

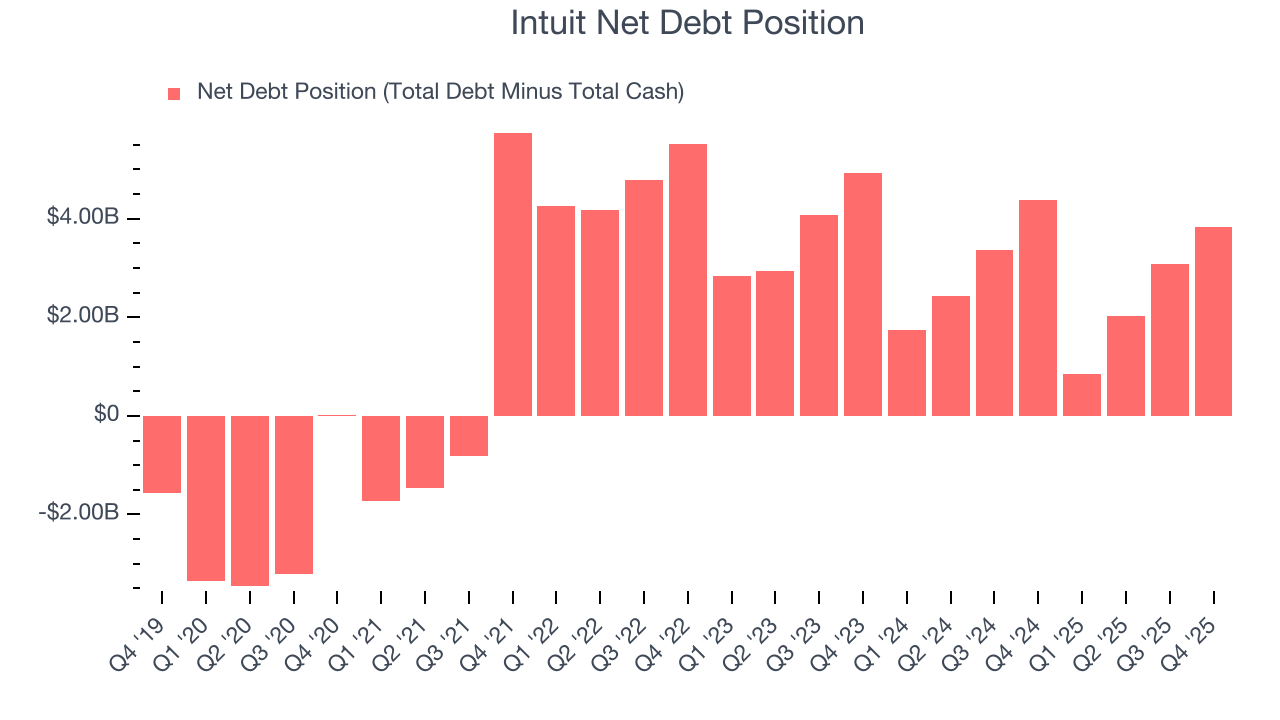

11. Balance Sheet Assessment

Intuit reported $2.98 billion of cash and $6.81 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $8.34 billion of EBITDA over the last 12 months, we view Intuit’s 0.5× net-debt-to-EBITDA ratio as safe. We also see its $71 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

12. Key Takeaways from Intuit’s Q4 Results

It was good to see Intuit narrowly top analysts’ billings expectations this quarter. We were also happy its revenue outperformed Wall Street’s estimates. On the other hand, its EPS guidance for next quarter missed and its full-year revenue guidance fell slightly short of Wall Street’s estimates. Overall, this was a softer quarter. The stock remained flat at $382.50 immediately following the results.

13. Is Now The Time To Buy Intuit?

Updated: March 13, 2026 at 10:01 PM EDT

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in Intuit.

Intuit possesses a number of positive attributes. First off, its revenue growth was solid over the last five years. And while its expanding operating margin shows it’s becoming more efficient at building and selling its software, its impressive operating margins show it has a highly efficient business model. On top of that, its bountiful generation of free cash flow empowers it to invest in growth initiatives.

Intuit’s price-to-sales ratio based on the next 12 months is 5.5x. Looking at the software space right now, Intuit trades at a compelling valuation. If you believe in the company and its growth potential, now is an opportune time to buy shares.

Wall Street analysts have a consensus one-year price target of $606.43 on the company (compared to the current share price of $439.44), implying they see 38% upside in buying Intuit in the short term.