Privia Health (PRVA)

We’re cautious of Privia Health. Its negative returns on capital show it destroyed shareholder value by losing money.― StockStory Analyst Team

1. News

2. Summary

Why Privia Health Is Not Exciting

Operating in 13 states and the District of Columbia with over 4,300 providers serving more than 4.8 million patients, Privia Health (NASDAQ:PRVA) is a technology-driven company that helps physicians optimize their practices, improve patient experiences, and transition to value-based care models.

- Push for growth has led to negative returns on capital, signaling value destruction

- Adjusted operating margin falls short of the industry average, and the smaller profit dollars make it harder to react to unexpected market developments

- The good news is that its earnings growth has beaten its peers over the last four years as its EPS has compounded at 27% annually

Privia Health doesn’t live up to our standards. Better businesses are for sale in the market.

Why There Are Better Opportunities Than Privia Health

Privia Health is trading at $21.69 per share, or 19.7x forward P/E. We acknowledge that the current valuation is justified, but we’re passing on this stock for the time being.

We prefer to invest in similarly-priced but higher-quality companies with superior earnings growth.

3. Privia Health (PRVA) Research Report: Q4 CY2025 Update

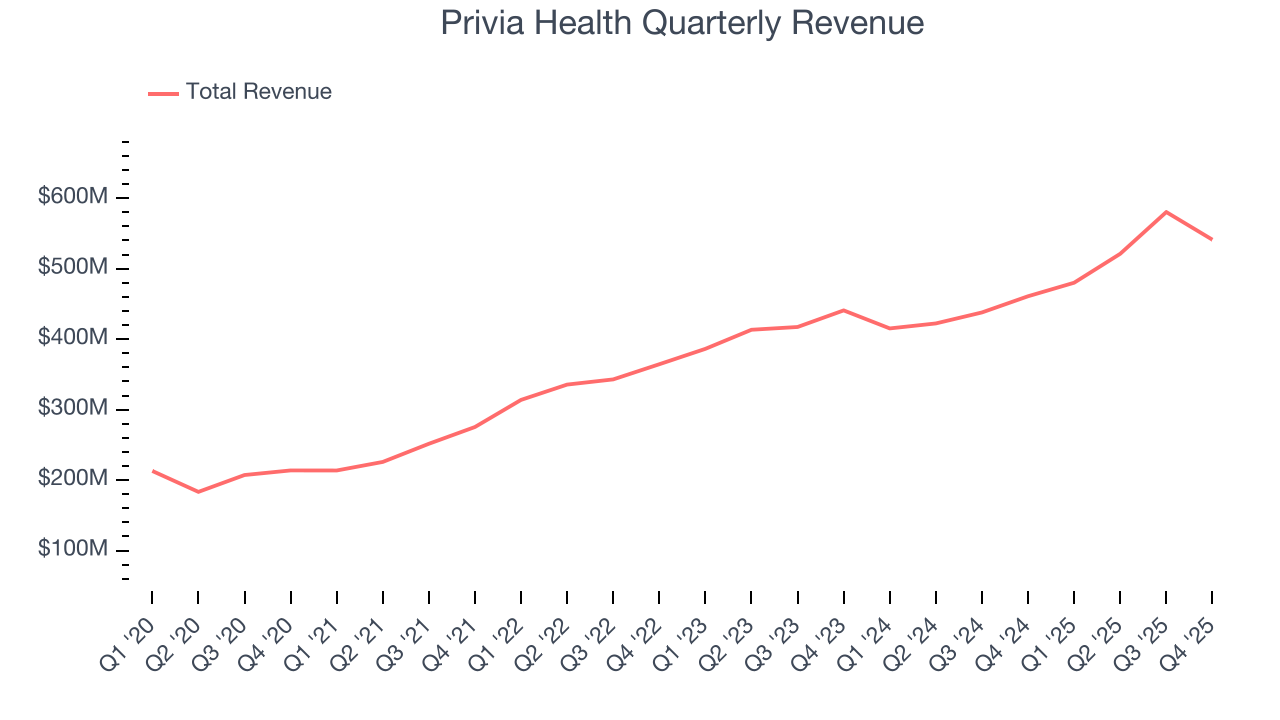

Healthcare tech company Privia Health Group (NASDAQ:PRVA) reported Q4 CY2025 results exceeding the market’s revenue expectations, with sales up 17.4% year on year to $541.2 million. The company’s full-year revenue guidance of $2.4 billion at the midpoint came in 3.7% above analysts’ estimates. Its non-GAAP profit of $0.25 per share was 30.2% above analysts’ consensus estimates.

Privia Health (PRVA) Q4 CY2025 Highlights:

- Revenue: $541.2 million vs analyst estimates of $516.3 million (17.4% year-on-year growth, 4.8% beat)

- Adjusted EPS: $0.25 vs analyst estimates of $0.19 (30.2% beat)

- Adjusted EBITDA: $31.46 million vs analyst estimates of $26.01 million (5.8% margin, 20.9% beat)

- EBITDA guidance for the upcoming financial year 2026 is $150 million at the midpoint, above analyst estimates of $142.9 million

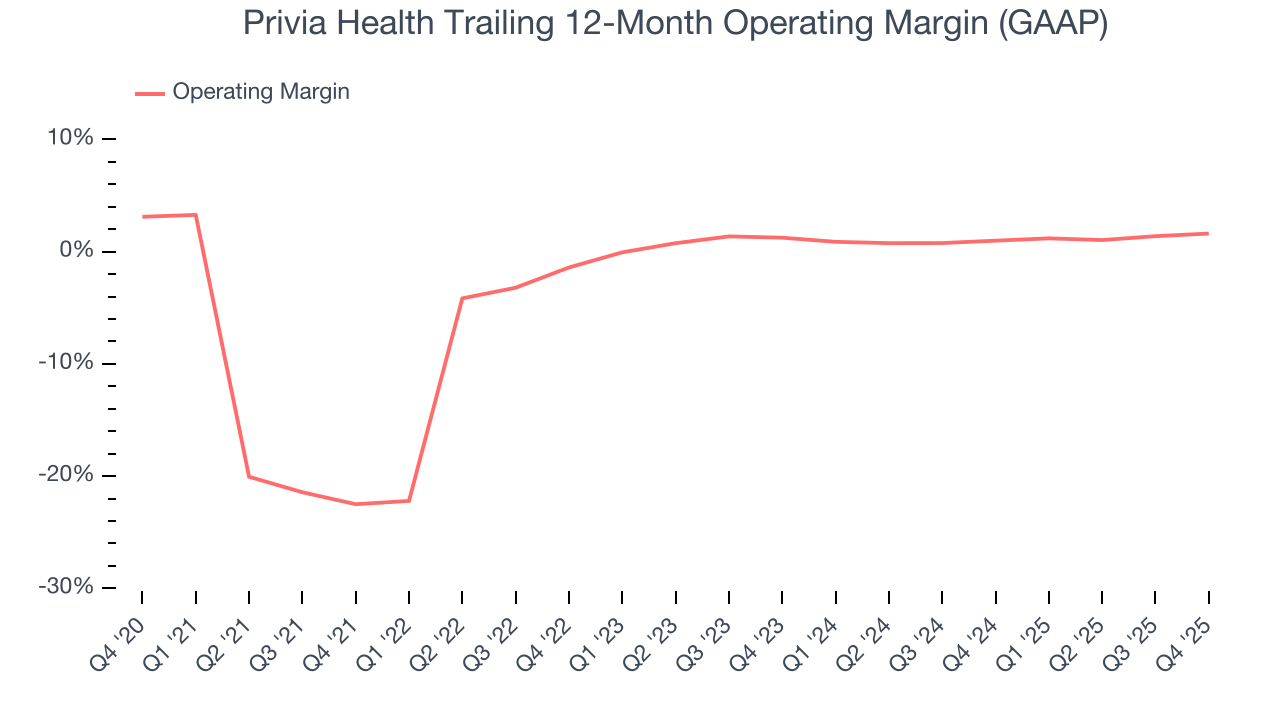

- Operating Margin: 2.1%, in line with the same quarter last year

- Free Cash Flow Margin: 23.6%, up from 16.2% in the same quarter last year

- Sales Volumes rose 12.3% year on year (11.2% in the same quarter last year)

- Market Capitalization: $2.79 billion

Company Overview

Operating in 13 states and the District of Columbia with over 4,300 providers serving more than 4.8 million patients, Privia Health (NASDAQ:PRVA) is a technology-driven company that helps physicians optimize their practices, improve patient experiences, and transition to value-based care models.

Privia Health partners with medical groups, health plans, and health systems through its physician-led medical groups. The company's platform addresses three key challenges physicians face: transitioning to value-based care reimbursement models, managing administrative burdens, and engaging patients with modern technology.

When physicians join Privia, they become part of a larger medical group in their geographic market while maintaining autonomy over clinical decisions. Privia provides comprehensive management services through local Management Services Organizations (MSOs), handling everything from revenue cycle management and payer contracting to data analytics and practice operations.

The Privia Technology Solution is central to the company's value proposition. This cloud-based platform integrates electronic medical records, telehealth capabilities, patient portals, and analytics tools into a seamless workflow. The technology helps identify care gaps, streamline administrative tasks, and enable both in-person and virtual care delivery. Privia's virtual visit platform has facilitated over 3 million telehealth visits across more than 50 medical specialties.

Privia's business model generates revenue through fee-for-service patient care, administrative services to medical groups, and value-based care arrangements. In value-based programs, Privia creates Accountable Care Organizations (ACOs) that allow physicians to participate in shared savings programs with payers. As of 2023, Privia operated ten ACOs serving approximately 198,000 Medicare beneficiaries.

The company emphasizes physician leadership and governance, with doctors holding the majority of board positions in Privia's medical groups and ACOs. This governance structure allows physicians to maintain clinical autonomy while benefiting from Privia's scale, technology, and expertise in navigating the shift toward value-based care.

Privia's approach has proven particularly effective in helping independent physicians remain independent while gaining the advantages typically associated with larger healthcare systems. The company's platform works across various patient demographics and reimbursement models, including traditional Medicare, Medicare Advantage, Medicaid, and commercial insurance.

4. Healthcare Technology for Providers

The healthcare technology sector provides software and data analytics to help hospitals and clinics streamline operations and improve patient outcomes, often through value-based care models. Future growth is expected as providers prioritize digital transformation to manage rising costs and patient demands. Tailwinds include the adoption of AI-driven tools and government incentives for digitization. There challenges as well, including long sales cycles and slow adoption by providers, who may be resistance to change. Tightening hospital budgets and cybersecurity threats are additional risks that could slow adoption.

Privia Health's competitors include Agilon Health (NYSE: AGL), Oak Street Health (acquired by CVS Health), VillageMD (majority-owned by Walgreens Boots Alliance), and Aledade, along with traditional physician practice management companies and health system-affiliated physician networks.

5. Revenue Scale

Larger companies benefit from economies of scale, where fixed costs like infrastructure, technology, and administration are spread over a higher volume of goods or services, reducing the cost per unit. Scale can also lead to bargaining power with suppliers, greater brand recognition, and more investment firepower. A virtuous cycle can ensue if a scaled company plays its cards right.

With just $2.12 billion in revenue over the past 12 months, Privia Health lacks scale in an industry where it matters. This makes it difficult to build trust with customers because healthcare is heavily regulated, complex, and resource-intensive.

6. Revenue Growth

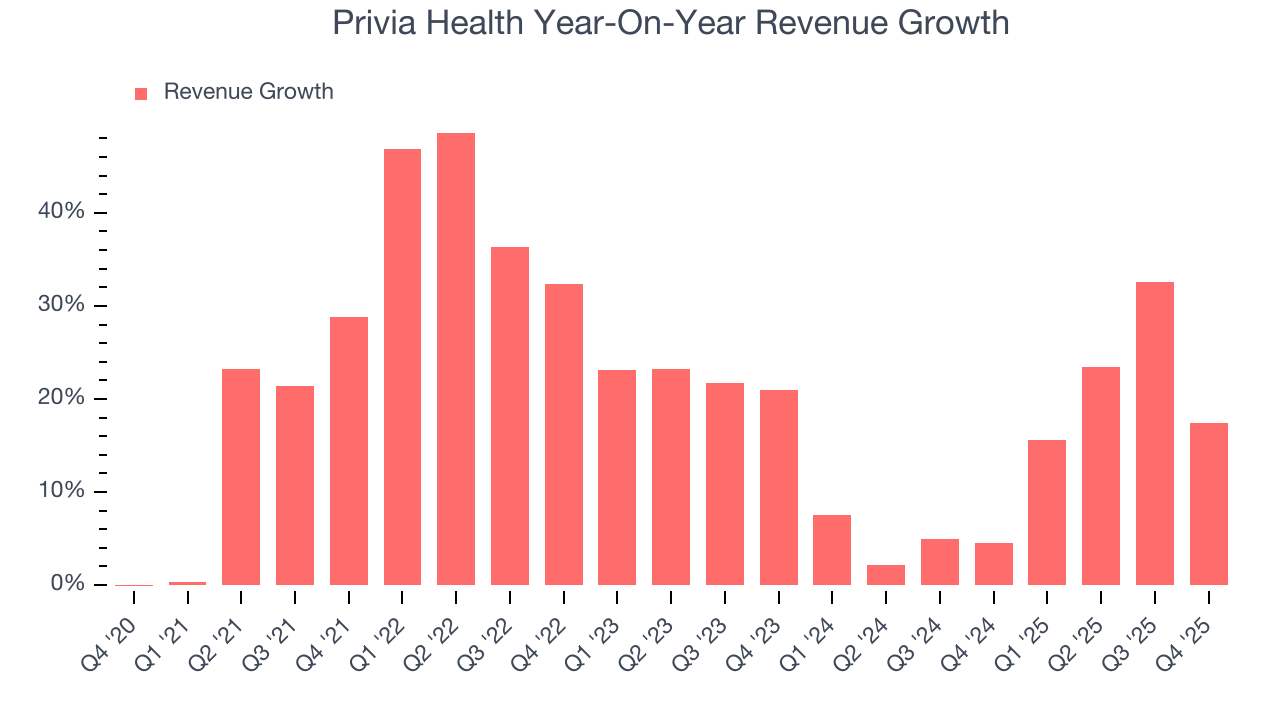

A company’s long-term sales performance is one signal of its overall quality. Any business can have short-term success, but a top-tier one grows for years. Over the last five years, Privia Health grew its sales at an excellent 21% compounded annual growth rate. Its growth beat the average healthcare company and shows its offerings resonate with customers.

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. Privia Health’s annualized revenue growth of 13.2% over the last two years is below its five-year trend, but we still think the results suggest healthy demand.

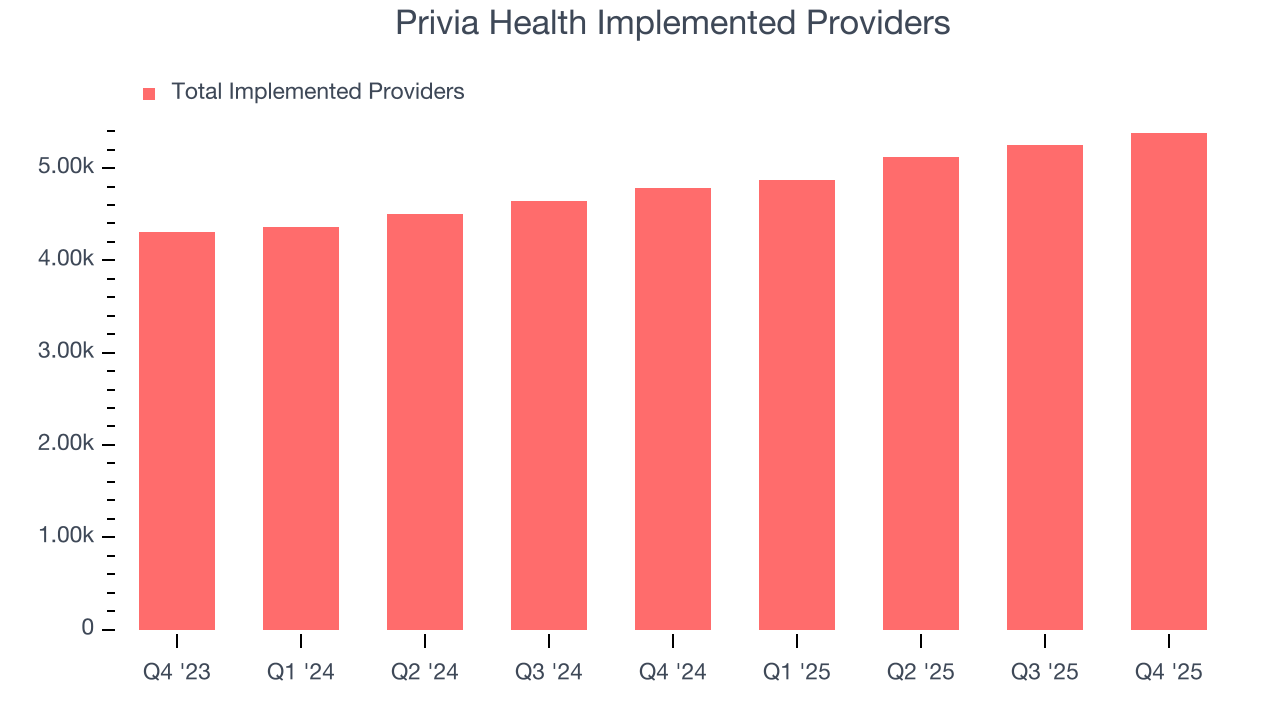

We can better understand the company’s revenue dynamics by analyzing its number of implemented providers, which reached 5,380 in the latest quarter. Over the last two years, Privia Health’s implemented providers averaged 12.4% year-on-year growth. Because this number is in line with its sales growth, we can see the company’s underlying demand was fairly consistent.

This quarter, Privia Health reported year-on-year revenue growth of 17.4%, and its $541.2 million of revenue exceeded Wall Street’s estimates by 4.8%.

Looking ahead, sell-side analysts expect revenue to grow 8% over the next 12 months, a deceleration versus the last two years. Despite the slowdown, this projection is above the sector average and indicates the market is baking in some success for its newer products and services.

7. Operating Margin

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after subtracting all core expenses, like marketing and R&D.

Although Privia Health was profitable this quarter from an operational perspective, it’s generally struggled over a longer time period. Its expensive cost structure has contributed to an average operating margin of negative 2.1% over the last five years. Unprofitable healthcare companies require extra attention because they could get caught swimming naked when the tide goes out. It’s hard to trust that the business can endure a full cycle.

On the plus side, Privia Health’s operating margin rose by 24.1 percentage points over the last five years, as its sales growth gave it operating leverage. Still, it will take much more for the company to show consistent profitability.

This quarter, Privia Health generated an operating margin profit margin of 2.1%, in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

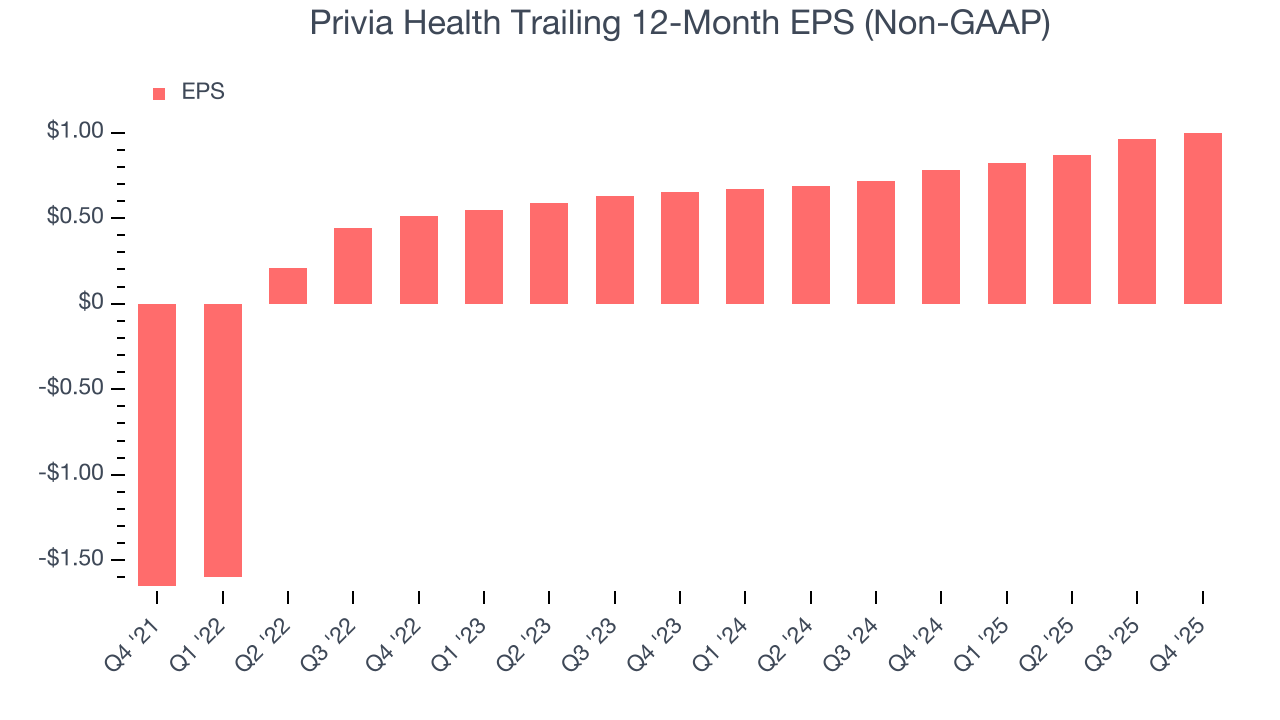

8. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Privia Health’s full-year EPS flipped from negative to positive over the last four years. This is encouraging and shows it’s at a critical moment in its life.

In Q4, Privia Health reported adjusted EPS of $0.25, up from $0.21 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Privia Health’s full-year EPS of $1 to grow 1.6%.

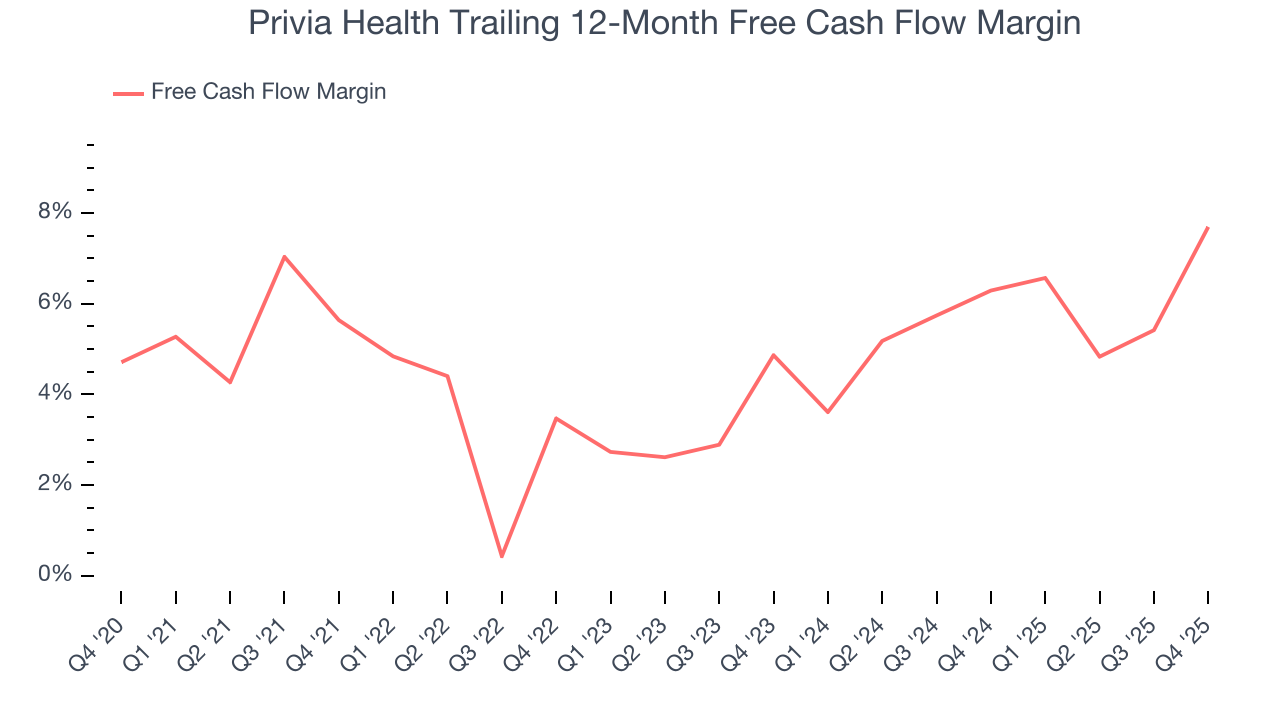

9. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Privia Health has shown decent cash profitability, giving it some flexibility to reinvest or return capital to investors. The company’s free cash flow margin averaged 5.8% over the last five years, slightly better than the broader healthcare sector.

Taking a step back, we can see that Privia Health’s margin expanded by 2.1 percentage points during that time. This is encouraging because it gives the company more optionality.

Privia Health’s free cash flow clocked in at $127.5 million in Q4, equivalent to a 23.6% margin. This result was good as its margin was 7.3 percentage points higher than in the same quarter last year, building on its favorable historical trend.

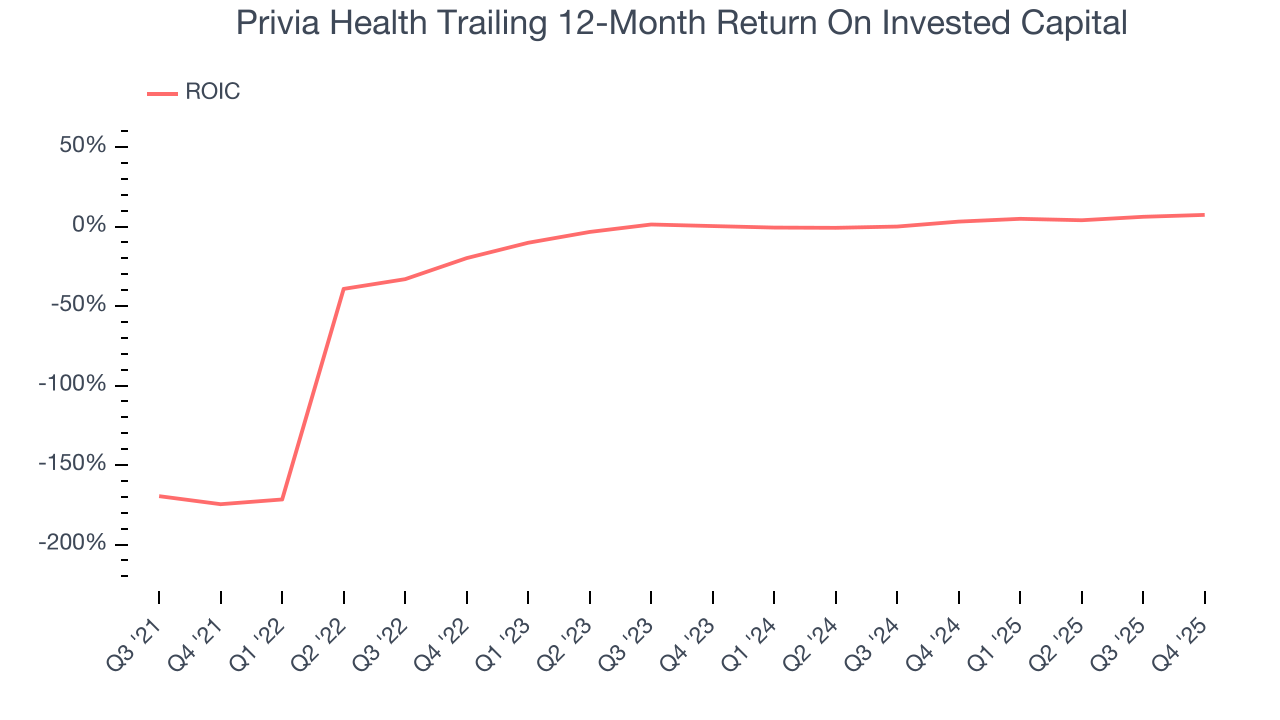

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Privia Health’s four-year average ROIC was negative 2.3%, meaning management lost money while trying to expand the business. Investors are likely hoping for a change soon.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Over the last few years, Privia Health’s ROIC has increased. This is a good sign, but we recognize its lack of profitable growth during the COVID era was the primary reason for the change.

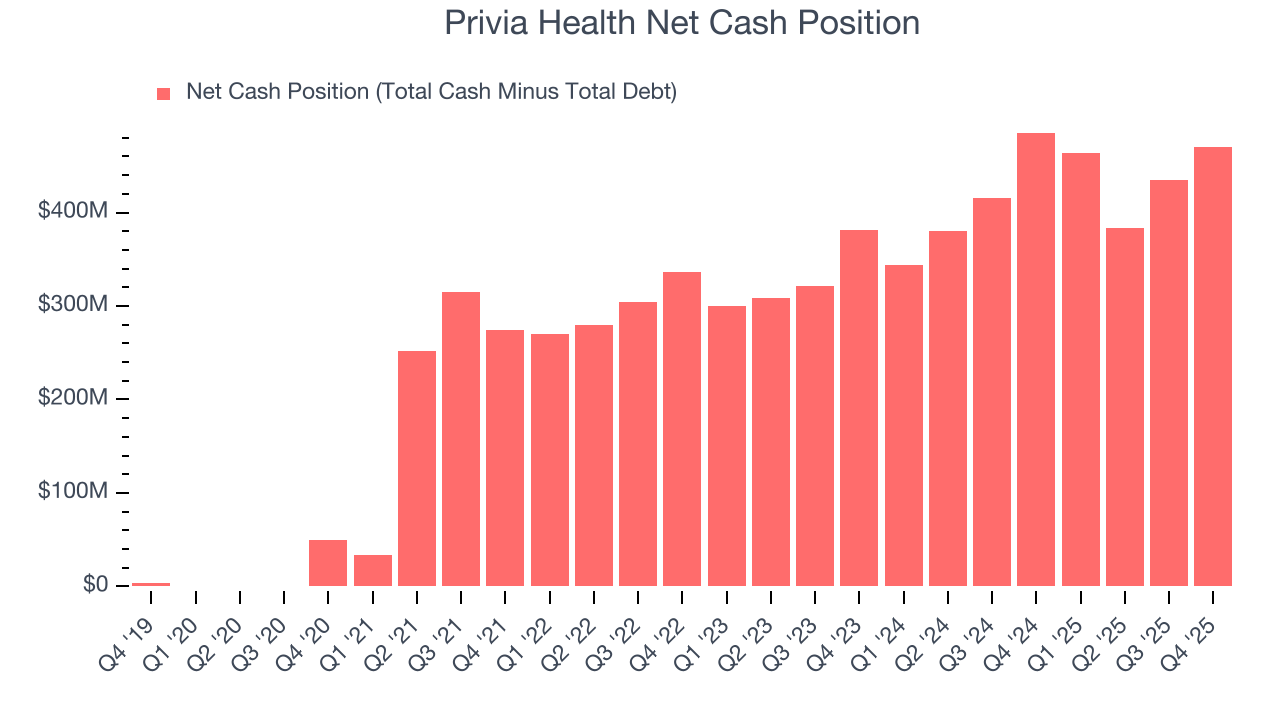

11. Balance Sheet Assessment

One of the best ways to mitigate bankruptcy risk is to hold more cash than debt.

Privia Health is a profitable, well-capitalized company with $479.7 million of cash and $9.53 million of debt on its balance sheet. This $470.2 million net cash position is 16.9% of its market cap and gives it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

12. Key Takeaways from Privia Health’s Q4 Results

It was good to see Privia Health beat analysts’ EPS expectations this quarter. We were also glad its full-year revenue guidance trumped Wall Street’s estimates. Zooming out, we think this quarter featured some important positives. The stock remained flat at $22.52 immediately following the results.

13. Is Now The Time To Buy Privia Health?

Updated: March 16, 2026 at 12:15 AM EDT

When considering an investment in Privia Health, investors should account for its valuation and business qualities as well as what’s happened in the latest quarter.

Privia Health isn’t a terrible business, but it doesn’t pass our quality test. Although its revenue growth was impressive over the last five years, it’s expected to deteriorate over the next 12 months and its relatively low ROIC suggests management has struggled to find compelling investment opportunities. And while the company’s astounding EPS growth over the last four years shows its profits are trickling down to shareholders, the downside is its operating margins are low compared to other healthcare companies.

Privia Health’s P/E ratio based on the next 12 months is 19.7x. This valuation multiple is fair, but we don’t have much faith in the company. We're fairly confident there are better stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $31.85 on the company (compared to the current share price of $21.69).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.