CAVA (CAVA)

We’re wary of CAVA. Its negative returns on capital suggest it eroded shareholder value by squandering business opportunities.― StockStory Analyst Team

1. News

2. Summary

Why CAVA Is Not Exciting

Starting from a single Washington, D.C. location, CAVA (NYSE:CAVA) operates a fast-casual restaurant chain offering customizable Mediterranean-inspired dishes.

- Negative returns on capital show that some of its growth strategies have backfired

- Falling earnings per share over the last two years has some investors worried as stock prices ultimately follow EPS over the long term

- A positive is that its market share has increased over the last four years as its 23.9% annual revenue growth was exceptional

CAVA lacks the business quality we seek. There are more promising alternatives.

3. CAVA (CAVA) Research Report: Q4 CY2025 Update

Mediterranean fast-casual restaurant chain CAVA (NYSE:CAVA) reported Q4 CY2025 results topping the market’s revenue expectations, with sales up 20.9% year on year to $275 million. Its GAAP profit of $0.04 per share was $0.01 above analysts’ consensus estimates.

CAVA (CAVA) Q4 CY2025 Highlights:

- Revenue: $275 million vs analyst estimates of $268.6 million (20.9% year-on-year growth, 2.4% beat)

- EPS (GAAP): $0.04 vs analyst estimates of $0.03 ($0.01 beat)

- Adjusted EBITDA: $25.76 million vs analyst estimates of $24.3 million (9.4% margin, 6% beat)

- EBITDA guidance for the upcoming financial year 2026 is $180 million at the midpoint, below analyst estimates of $182.8 million

- Operating Margin: 1%, in line with the same quarter last year

- Locations: 439 at quarter end, up from 378 in the same quarter last year

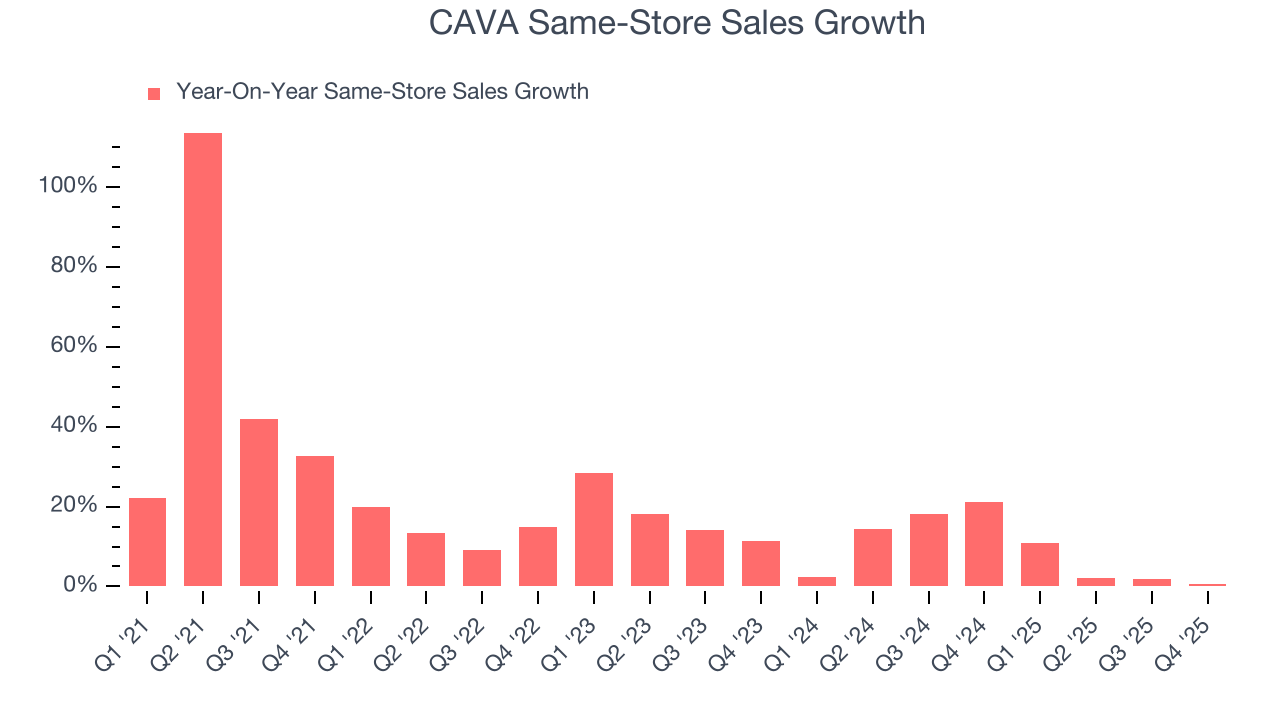

- Same-Store Sales were flat year on year (21.2% in the same quarter last year)

- Market Capitalization: $7.93 billion

Company Overview

Starting from a single Washington, D.C. location, CAVA (NYSE:CAVA) operates a fast-casual restaurant chain offering customizable Mediterranean-inspired dishes.

The company was founded by a group of friends with a desire to bring modern Mediterranean flavors to a broader audience. Starting as a local restaurant, CAVA built its reputation on a build-your-own concept that lets customers choose from a variety of fresh proteins, toppings, and sauces.

CAVA’s restaurants typically feature an open, assembly line-style setup, inviting guests to watch their meals come to life as they move down the line. To reach even more consumers, the brand has expanded beyond its own stores, offering dips and spreads through grocery channels, and further strengthening its presence through the acquisition of Zoës Kitchen. This acquisition helped CAVA break into new markets and scale its operations by converting former Zoës Kitchen sites into new CAVA locations.

In today’s digital age, CAVA provides online ordering and delivery options through its website and mobile app, streamlining the process with real-time tracking and exclusive promotions.

4. Modern Fast Food

Modern fast food is a relatively newer category representing a middle ground between traditional fast food and sit-down restaurants. These establishments feature an expanded menu selection priced above traditional fast food options, often incorporating fresher and cleaner ingredients to serve customers prioritizing quality. These eateries are capitalizing on the perception that your drive-through burger and fries joint is detrimental to your health because of inferior ingredients.

Competitors offering similar menus and service models include Chipotle (NYSE:CMG), Sweetgreen (NYSE:SG), and Noodles & Company (NASDAQ:NDLS).

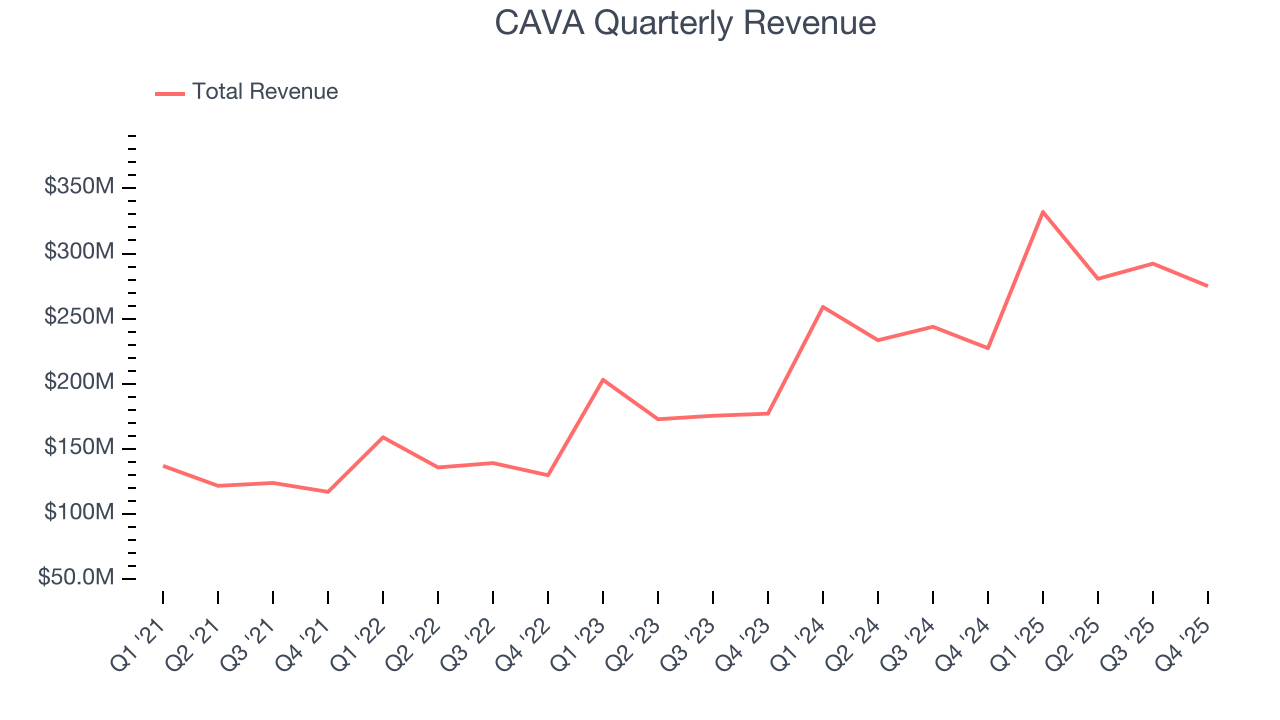

5. Revenue Growth

A company’s long-term performance is an indicator of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years.

With $1.18 billion in revenue over the past 12 months, CAVA is a mid-sized restaurant chain, which sometimes brings disadvantages compared to larger competitors benefiting from better brand awareness and economies of scale. On the bright side, it can still flex high growth rates because it’s working from a smaller revenue base.

As you can see below, CAVA’s 23.9% annualized revenue growth over the last four years was incredible as it opened new restaurants and increased sales at existing, established dining locations.

This quarter, CAVA reported robust year-on-year revenue growth of 20.9%, and its $275 million of revenue topped Wall Street estimates by 2.4%.

Looking ahead, sell-side analysts expect revenue to grow 20.8% over the next 12 months, a deceleration versus the last four years. Still, this projection is commendable and implies the market is baking in success for its menu offerings.

6. Restaurant Performance

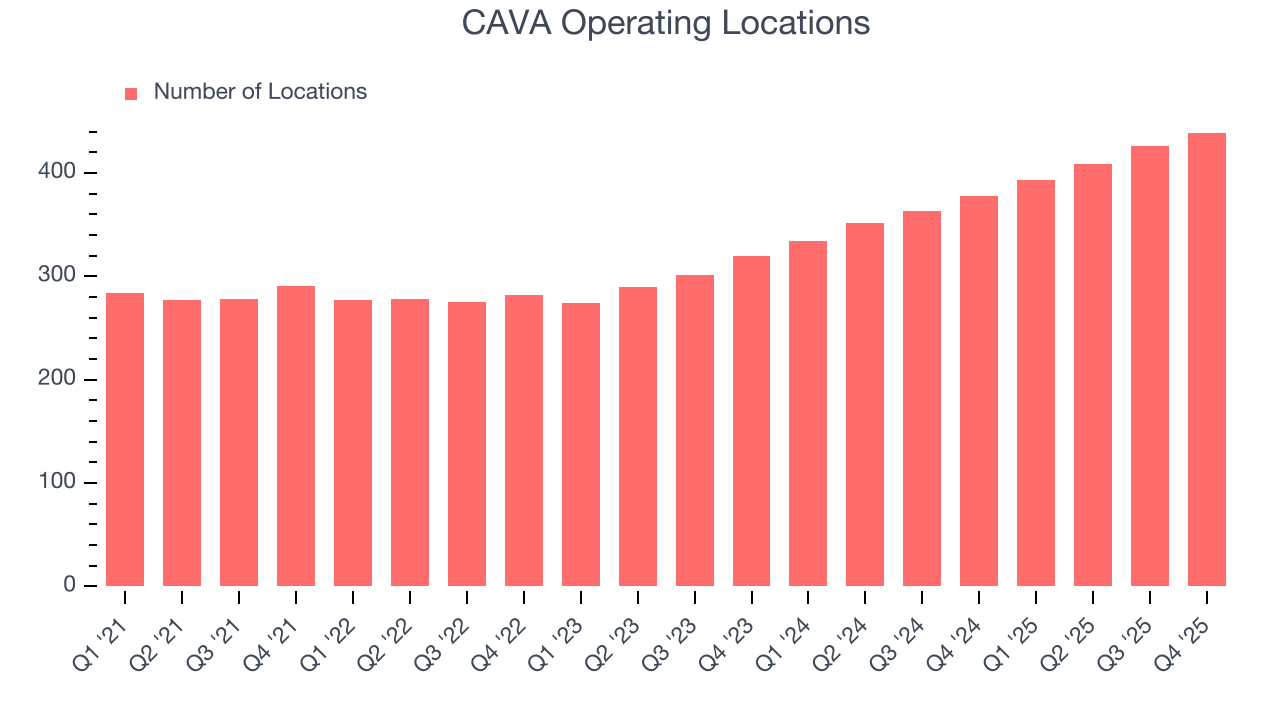

Number of Restaurants

A restaurant chain’s total number of dining locations often determines how much revenue it can generate.

CAVA operated 439 locations in the latest quarter. It has opened new restaurants at a rapid clip over the last two years, averaging 18.7% annual growth, much faster than the broader restaurant sector. This gives it a chance to become a large, scaled business over time.

When a chain opens new restaurants, it usually means it’s investing for growth because there’s healthy demand for its meals and there are markets where its concepts have few or no locations.

Same-Store Sales

A company's restaurant base only paints one part of the picture. When demand is high, it makes sense to open more. But when demand is low, it’s prudent to close some locations and use the money in other ways. Same-store sales provides a deeper understanding of this issue because it measures organic growth at restaurants open for at least a year.

CAVA has been one of the most successful restaurant chains over the last two years thanks to skyrocketing demand within its existing dining locations. On average, the company has posted exceptional year-on-year same-store sales growth of 8.9%. This performance along with its meaningful buildout of new restaurants suggest it’s playing some aggressive offense.

In the latest quarter, CAVA’s year on year same-store sales were flat. This was a meaningful deceleration from its historical levels. We’ll be watching closely to see if CAVA can reaccelerate growth.

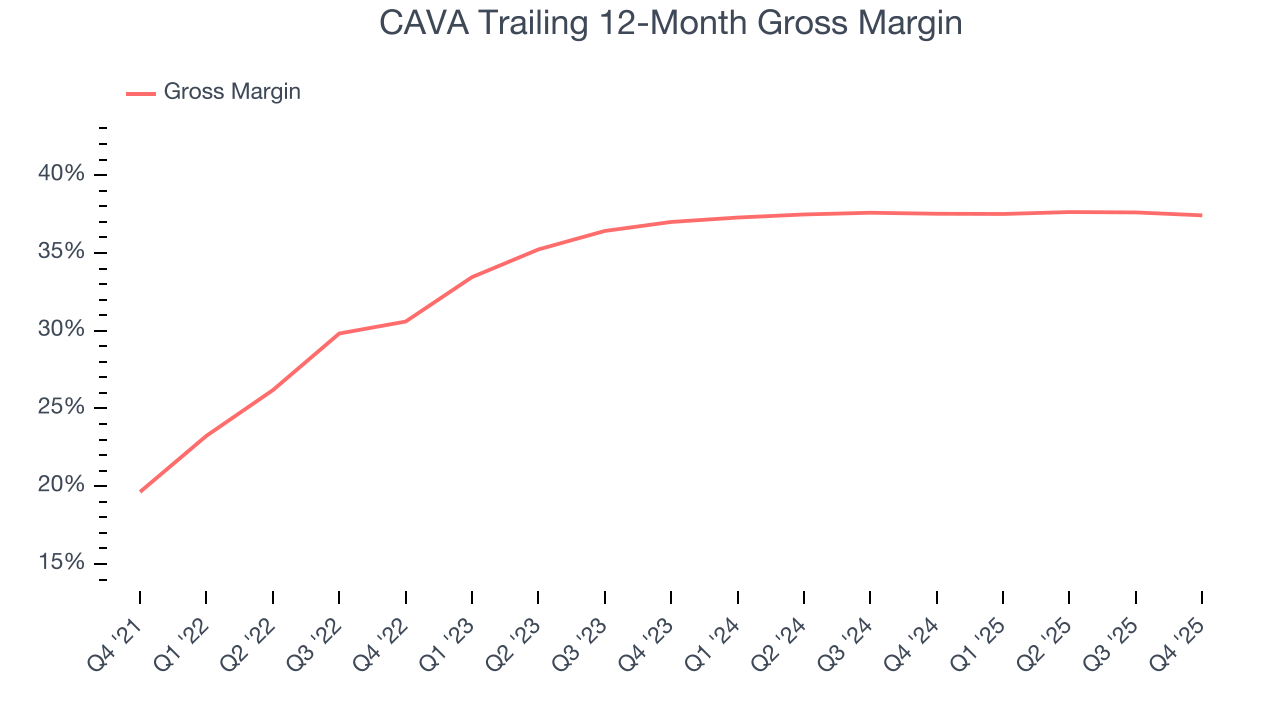

7. Gross Margin & Pricing Power

CAVA has great unit economics for a restaurant company, giving it ample room to invest in areas such as marketing and talent to grow its brand. As you can see below, it averaged an excellent 37.5% gross margin over the last two years. That means CAVA only paid its suppliers $62.53 for every $100 in revenue.

CAVA produced a 35% gross profit margin in Q4, in line with the same quarter last year. On a wider time horizon, the company’s full-year margin has remained steady over the past four quarters, suggesting its input costs (such as ingredients and transportation expenses) have been stable and it isn’t under pressure to lower prices.

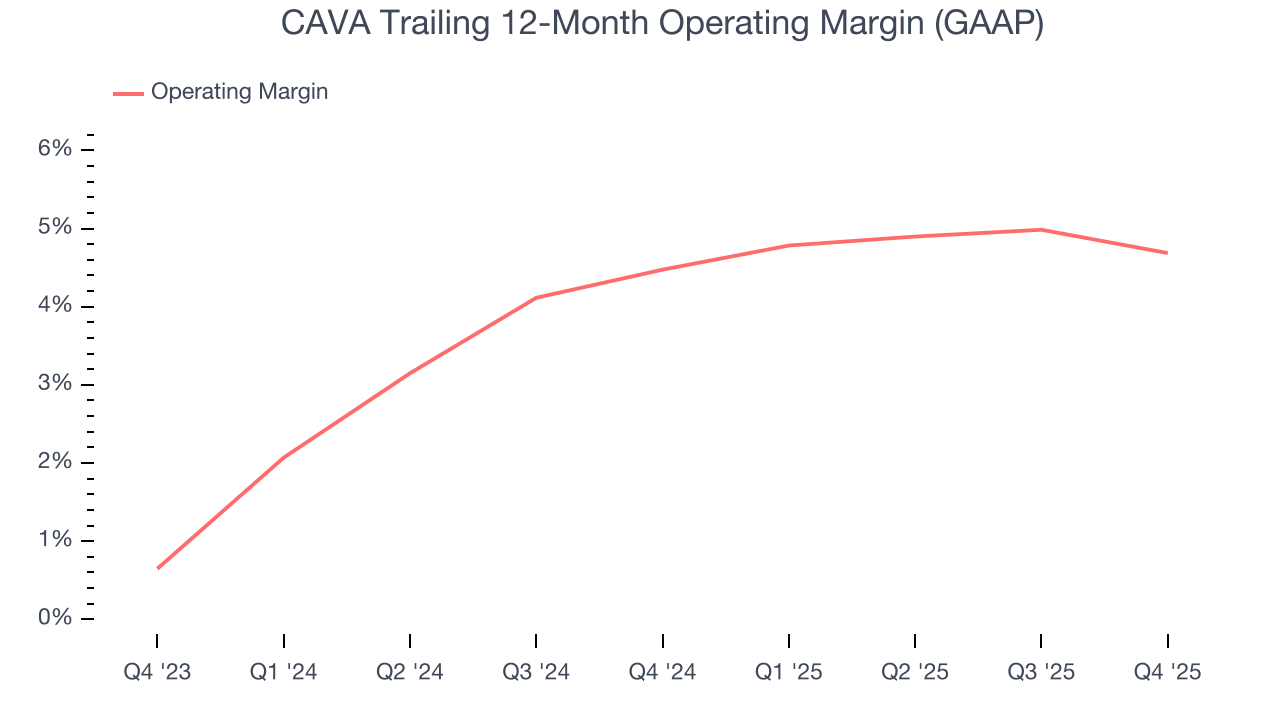

8. Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

CAVA’s operating margin might fluctuated slightly over the last 12 months but has generally stayed the same, averaging 4.6% over the last two years. This profitability was lousy for a restaurant business and caused by its suboptimal cost structure.

Analyzing the trend in its profitability, CAVA’s operating margin might fluctuated slightly but has generally stayed the same over the last year. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

This quarter, CAVA generated an operating margin profit margin of 1%, in line with the same quarter last year. This indicates the company’s cost structure has recently been stable.

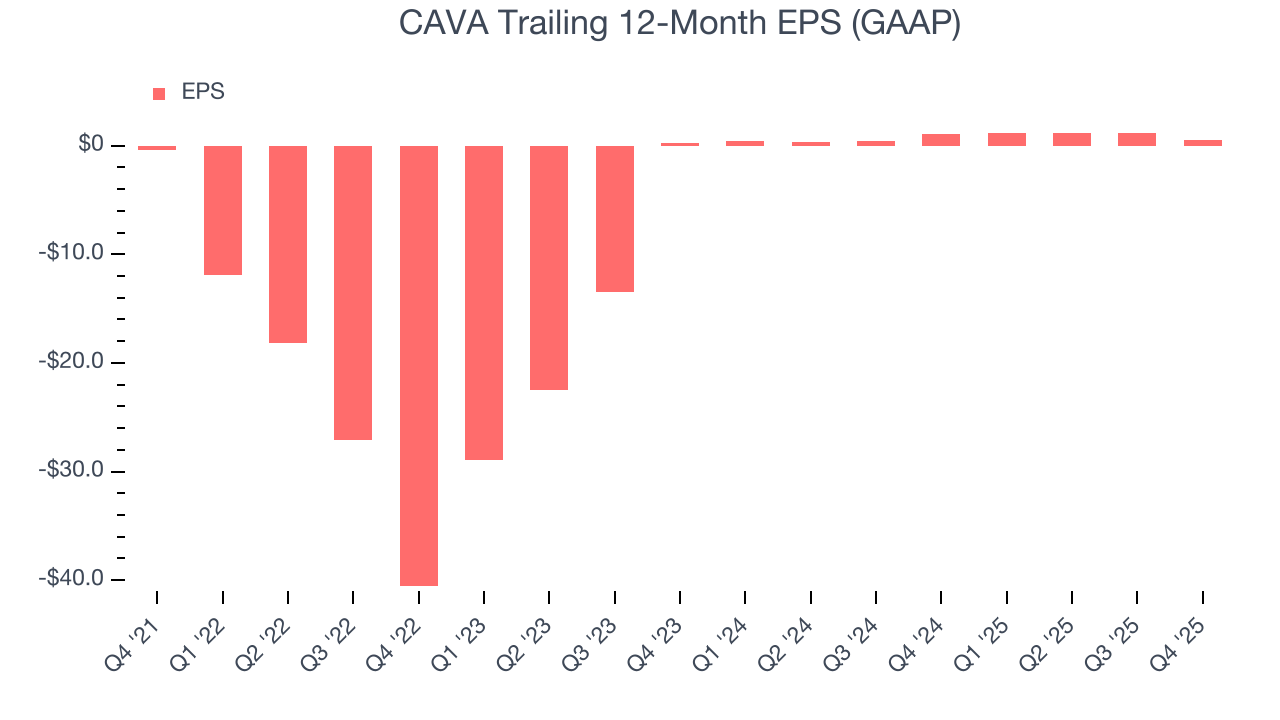

9. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

CAVA’s full-year EPS flipped from negative to positive over the last four years. This is a good sign and shows it’s at an inflection point.

In Q4, CAVA reported EPS of $0.04, down from $0.66 in the same quarter last year. Despite falling year on year, this print easily cleared analysts’ estimates. Over the next 12 months, Wall Street expects CAVA’s full-year EPS of $0.54 to grow 8.5%.

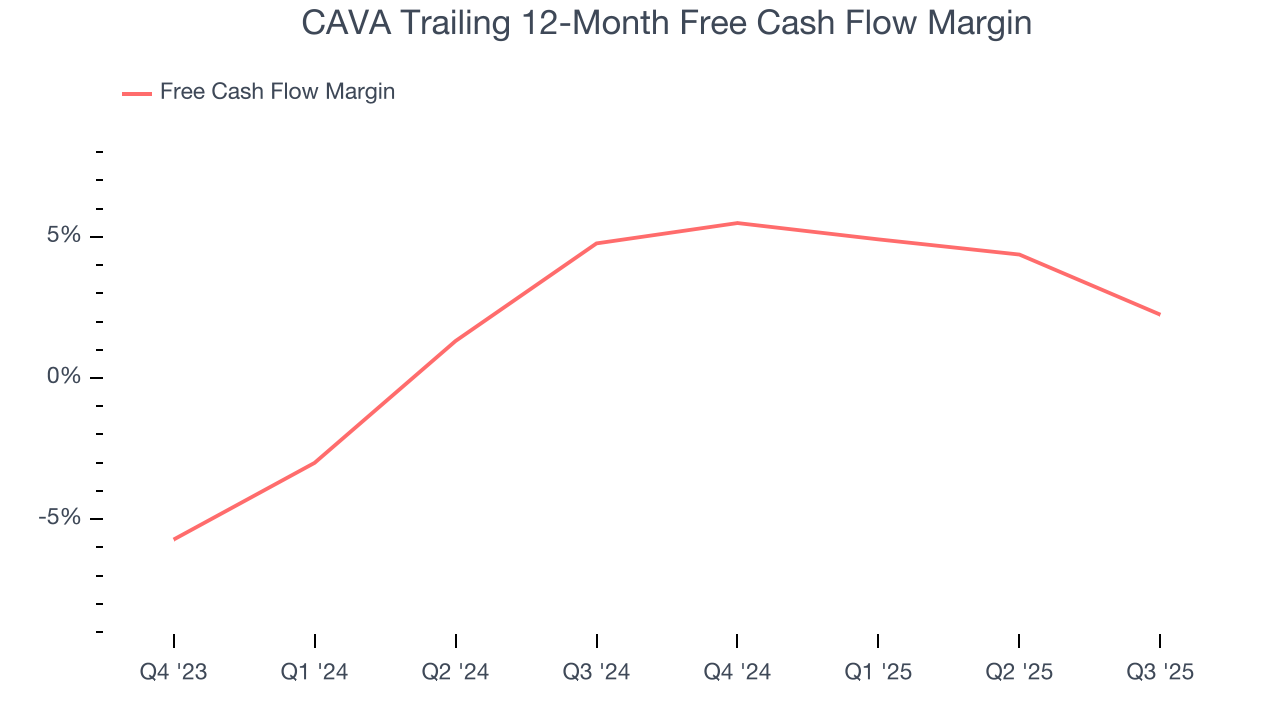

10. Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

CAVA has shown decent cash profitability, giving it some flexibility to reinvest or return capital to investors. The company’s free cash flow margin averaged 4.1% over the last two years, slightly better than the broader restaurant sector.

11. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

CAVA’s five-year average ROIC was negative 11.8%, meaning management lost money while trying to expand the business. Its returns were among the worst in the restaurant sector.

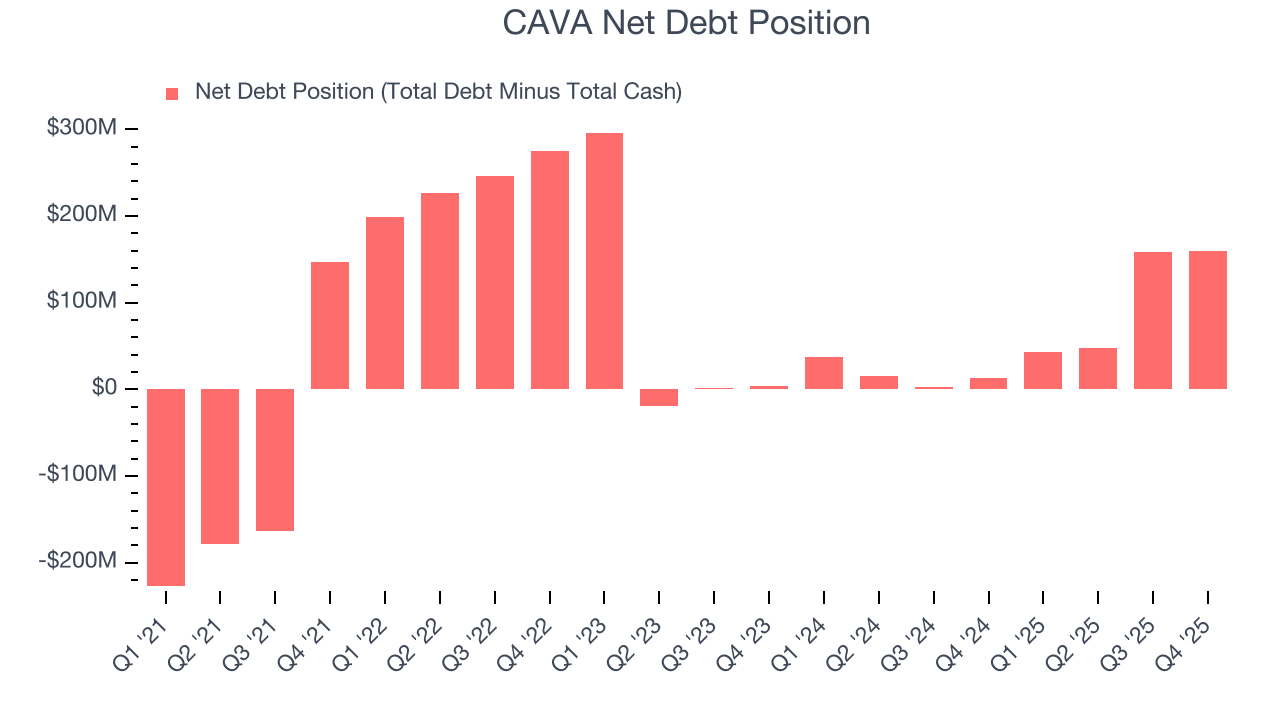

12. Balance Sheet Assessment

CAVA reported $283.9 million of cash and $443.3 million of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $152.8 million of EBITDA over the last 12 months, we view CAVA’s 1.0× net-debt-to-EBITDA ratio as safe. We also see its $8.50 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

13. Key Takeaways from CAVA’s Q4 Results

It was good to see CAVA beat analysts’ EPS expectations this quarter. We were also excited its same-store sales outperformed Wall Street’s estimates by a wide margin. On the other hand, its full-year EBITDA guidance missed. Zooming out, we think this quarter featured some important positives. The stock traded up 8.3% to $73.55 immediately after reporting.

14. Is Now The Time To Buy CAVA?

Updated: March 29, 2026 at 10:40 PM EDT

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in CAVA.

CAVA isn’t a terrible business, but it isn’t one of our picks. Although its revenue growth was exceptional over the last four years and Wall Street believes it will continue to grow, its declining EPS over the last two years makes it a less attractive asset to the public markets. And while the company’s marvelous same-store sales growth is on another level, the downside is its projected EPS for the next year is lacking.

CAVA’s P/E ratio based on the next 12 months is 151.9x. At this valuation, there’s a lot of good news priced in - you can find more timely opportunities elsewhere.

Wall Street analysts have a consensus one-year price target of $84.70 on the company (compared to the current share price of $74.63).