Floor And Decor (FND)

We wouldn’t recommend Floor And Decor. Its weak sales growth and low returns on capital show it struggled to generate demand and profits.― StockStory Analyst Team

1. News

2. Summary

Why We Think Floor And Decor Will Underperform

Operating large, warehouse-style stores, Floor & Decor (NYSE:FND) is a specialty retailer that specializes in hard flooring surfaces for the home such as tiles, hardwood, stone, and laminates.

- Weak same-store sales trends over the past two years suggest there may be few opportunities in its core markets to open new locations

- Below-average returns on capital indicate management struggled to find compelling investment opportunities, and its shrinking returns suggest its past profit sources are losing steam

- Performance over the past three years shows its incremental sales were much less profitable, as its earnings per share fell by 11.5% annually

Floor And Decor is skating on thin ice. We’d rather invest in businesses with stronger moats.

Why There Are Better Opportunities Than Floor And Decor

Floor And Decor is trading at $57.00 per share, or 26.8x forward P/E. This multiple expensive for its subpar fundamentals.

Paying up for elite businesses with strong earnings potential is better than investing in lower-quality companies with shaky fundamentals. That’s how you avoid big downside over the long term.

3. Floor And Decor (FND) Research Report: Q4 CY2025 Update

Specialty flooring retailer Floor & Decor (NYSE:FND) met Wall Street’s revenue expectations in Q4 CY2025, with sales up 2% year on year to $1.13 billion. On the other hand, the company’s full-year revenue guidance of $4.96 billion at the midpoint came in 1.4% below analysts’ estimates. Its GAAP profit of $0.36 per share was 3.3% above analysts’ consensus estimates.

Floor And Decor (FND) Q4 CY2025 Highlights:

- Revenue: $1.13 billion vs analyst estimates of $1.13 billion (2% year-on-year growth, in line)

- EPS (GAAP): $0.36 vs analyst estimates of $0.35 (3.3% beat)

- Adjusted EBITDA: $119.4 million vs analyst estimates of $117.9 million (10.6% margin, 1.3% beat)

- EPS (GAAP) guidance for the upcoming financial year 2026 is $2.08 at the midpoint, missing analyst estimates by 2.2%

- EBITDA guidance for the upcoming financial year 2026 is $575 million at the midpoint, below analyst estimates of $586.8 million

- Operating Margin: 4.6%, in line with the same quarter last year

- Free Cash Flow Margin: 4%, up from 0.4% in the same quarter last year

- Same-Store Sales rose 4.8% year on year (-0.8% in the same quarter last year)

- Market Capitalization: $7.54 billion

Company Overview

Operating large, warehouse-style stores, Floor & Decor (NYSE:FND) is a specialty retailer that specializes in hard flooring surfaces for the home such as tiles, hardwood, stone, and laminates.

While other home improvement retailers sell flooring products in addition to a whole host of other categories such as paint, appliances, lumber, and even plants, Floor & Decor is focused largely

The core customer is both the do-it-yourself (DIY) homeowner as well as the professional contractor. The DIY shopper values the ability to touch and feel products as well as the helpful sales associates trained strictly in flooring. For the professional contractor, Floor & Decor’s vast selection and high in-stock positions mean they don’t have to shop around to find everything they need, allowing them to maximize time devoted to their projects. There are also loyalty programs and volume discounts for Pros.

The company has a vertically integrated business model, which means they control every aspect of the supply chain from product development to procurement to distribution. Since Floor & Decor deals directly with manufacturers (competitors often use buying agents and middlemen), they can keep prices extremely competitive. It also allows the company to introduce new products and respond to trends in a more timely manner.

4. Home Improvement Retailer

Home improvement retailers serve the maintenance and repair needs of do-it-yourself homeowners as well as professional contractors. Home is where the heart is, so any homeowner will want to keep that home in good shape by maintaining the yard, fixing leaks, or improving lighting fixtures, for example. Home improvement stores win with depth and breadth of product, in-store consultations for customers who need help, and services that cater to professionals. It is hard for non-focused retailers and e-commerce competitors to match these. However, the research, convenience, and prices of online platforms means they can’t be fully written off, either.

Competitors offering flooring products and materials include LL Flooring (NYSE:LL), Tile Shop (NASDAQ:TTSH), Home Depot (NYSE:HD), and Lowe’s (NYSE:LOW).

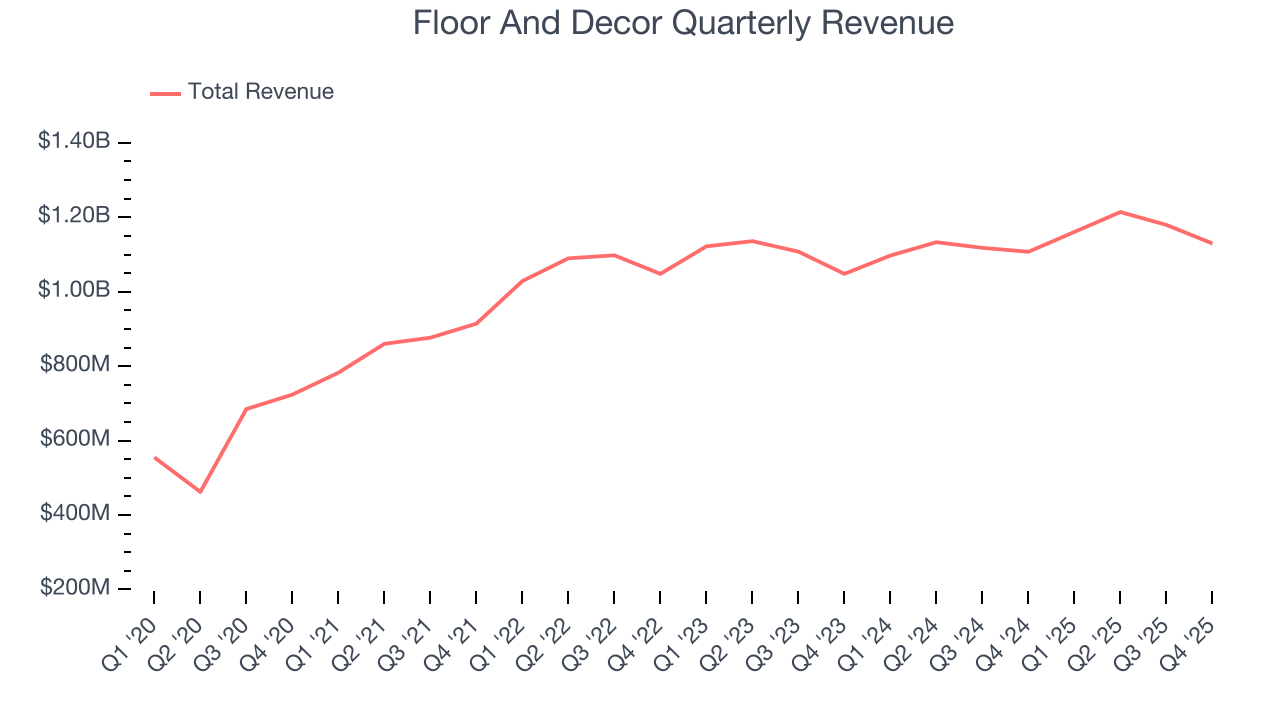

5. Revenue Growth

A company’s long-term sales performance can indicate its overall quality. Any business can have short-term success, but a top-tier one grows for years.

With $4.68 billion in revenue over the past 12 months, Floor And Decor is a small retailer, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage with suppliers.

As you can see below, Floor And Decor’s 3.2% annualized revenue growth over the last three years was sluggish.

This quarter, Floor And Decor grew its revenue by 2% year on year, and its $1.13 billion of revenue was in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 7.6% over the next 12 months, an acceleration versus the last three years. This projection is noteworthy and implies its newer products will catalyze better top-line performance.

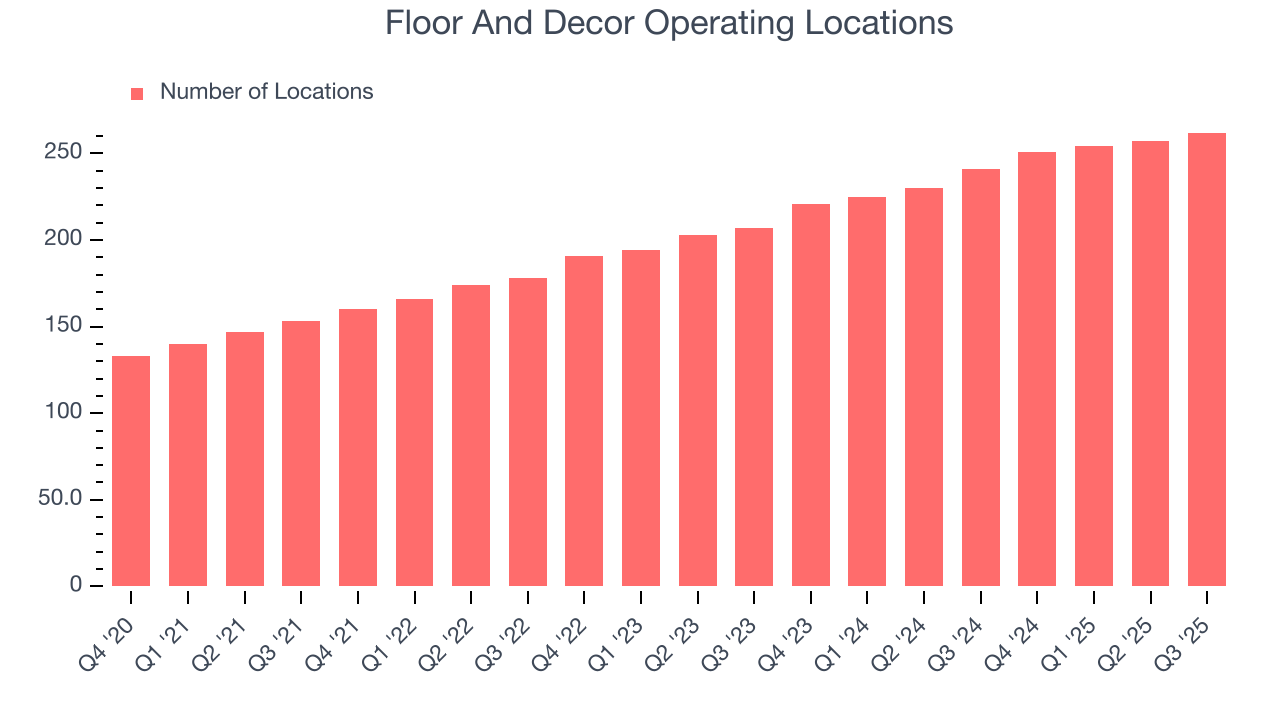

6. Store Performance

Number of Stores

Over the last two years, Floor And Decor opened new stores at a rapid clip by averaging 13.2% annual growth, among the fastest in the consumer retail sector. This gives it a chance to scale into a mid-sized business over time.

When a retailer opens new stores, it usually means it’s investing for growth because demand is greater than supply, especially in areas where consumers may not have a store within reasonable driving distance.

Note that Floor And Decor reports its store count intermittently, so some data points are missing in the chart below.

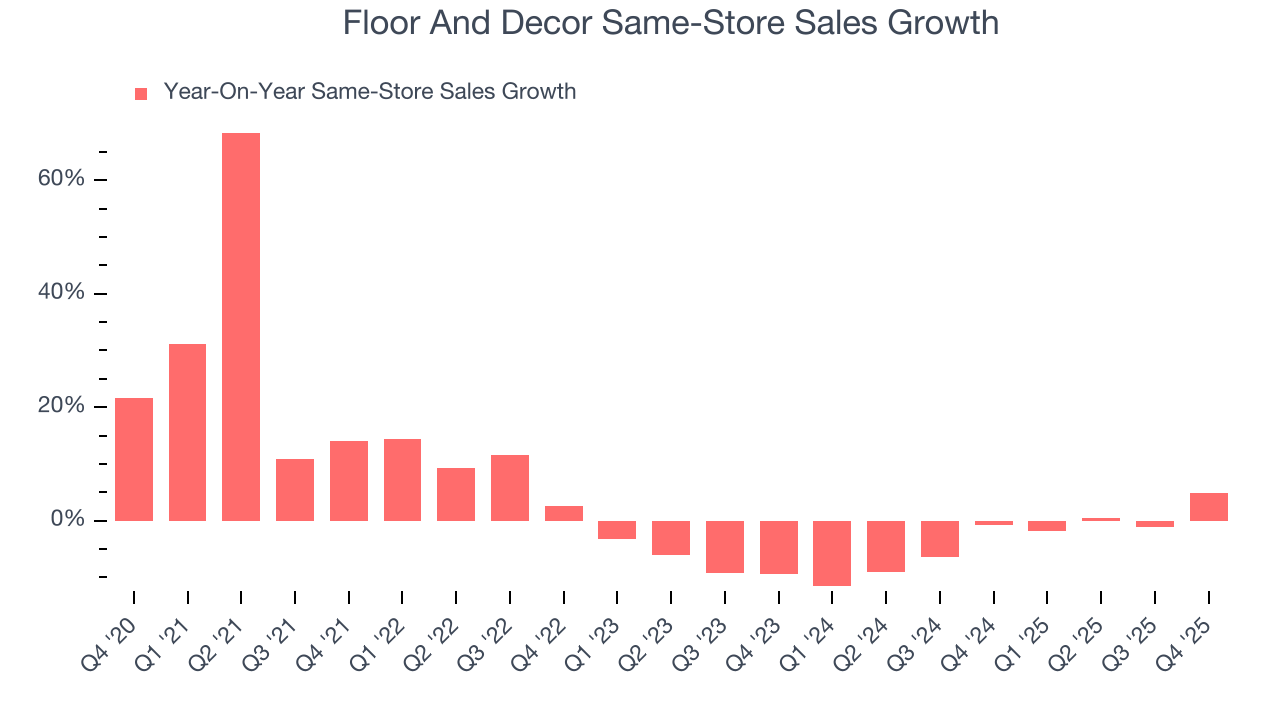

Same-Store Sales

The change in a company's store base only tells one side of the story. The other is the performance of its existing locations and e-commerce sales, which informs management teams whether they should expand or downsize their physical footprints. Same-store sales provides a deeper understanding of this issue because it measures organic growth at brick-and-mortar shops for at least a year.

Floor And Decor’s demand has been shrinking over the last two years as its same-store sales have averaged 3.2% annual declines. This performance is concerning - it shows Floor And Decor artificially boosts its revenue by building new stores. We’d like to see a company’s same-store sales rise before it takes on the costly, capital-intensive endeavor of expanding its store base.

In the latest quarter, Floor And Decor’s same-store sales rose 4.8% year on year. This growth was a well-appreciated turnaround from its historical levels, showing the business is regaining momentum.

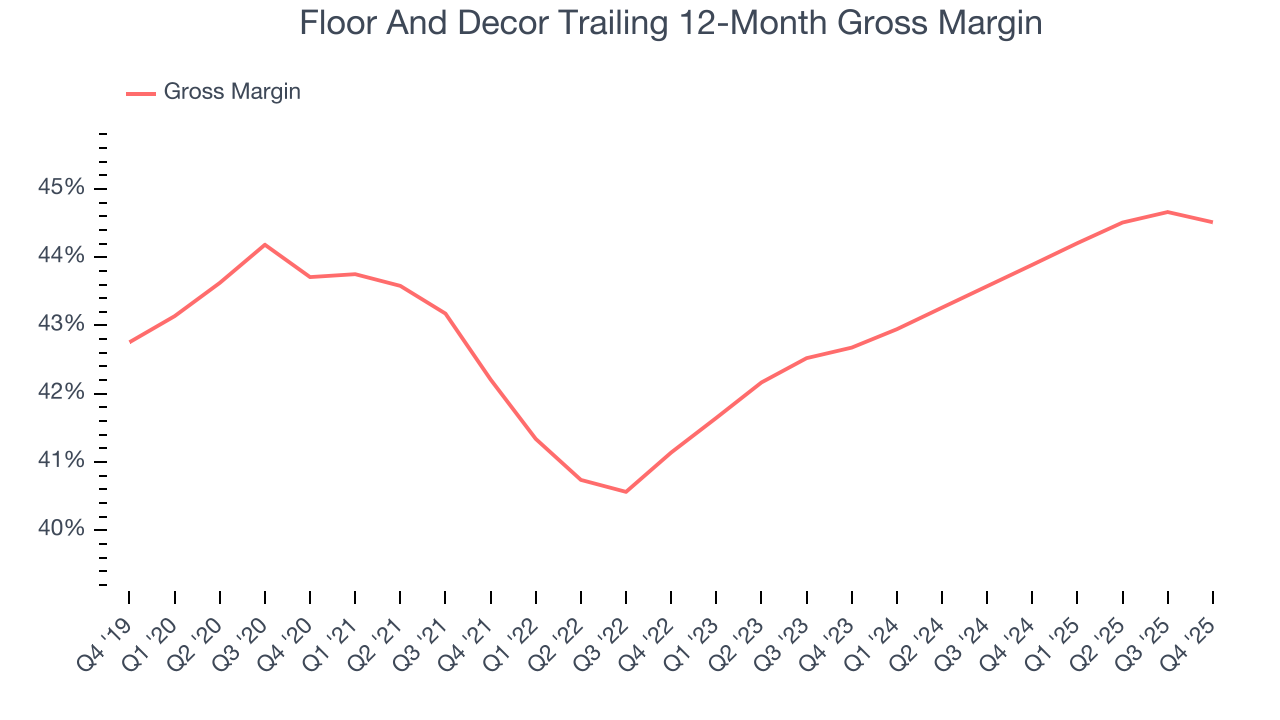

7. Gross Margin & Pricing Power

Floor And Decor has good unit economics for a retailer, giving it the opportunity to invest in areas such as marketing and talent to stay competitive. As you can see below, it averaged an impressive 44.2% gross margin over the last two years. Said differently, Floor And Decor paid its suppliers $55.79 for every $100 in revenue.

Floor And Decor’s gross profit margin came in at 43.5% this quarter, in line with the same quarter last year. On a wider time horizon, the company’s full-year margin has remained steady over the past four quarters, suggesting it strives to keep prices low for customers and has stable input costs (such as labor and freight expenses to transport goods).

8. Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Floor And Decor’s operating margin might fluctuated slightly over the last 12 months but has remained more or less the same, averaging 5.8% over the last two years. This profitability was paltry for a consumer retail business and caused by its suboptimal cost structure.

Analyzing the trend in its profitability, Floor And Decor’s operating margin might fluctuated slightly but has generally stayed the same over the last year. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

This quarter, Floor And Decor generated an operating margin profit margin of 4.6%, in line with the same quarter last year. This indicates the company’s cost structure has recently been stable.

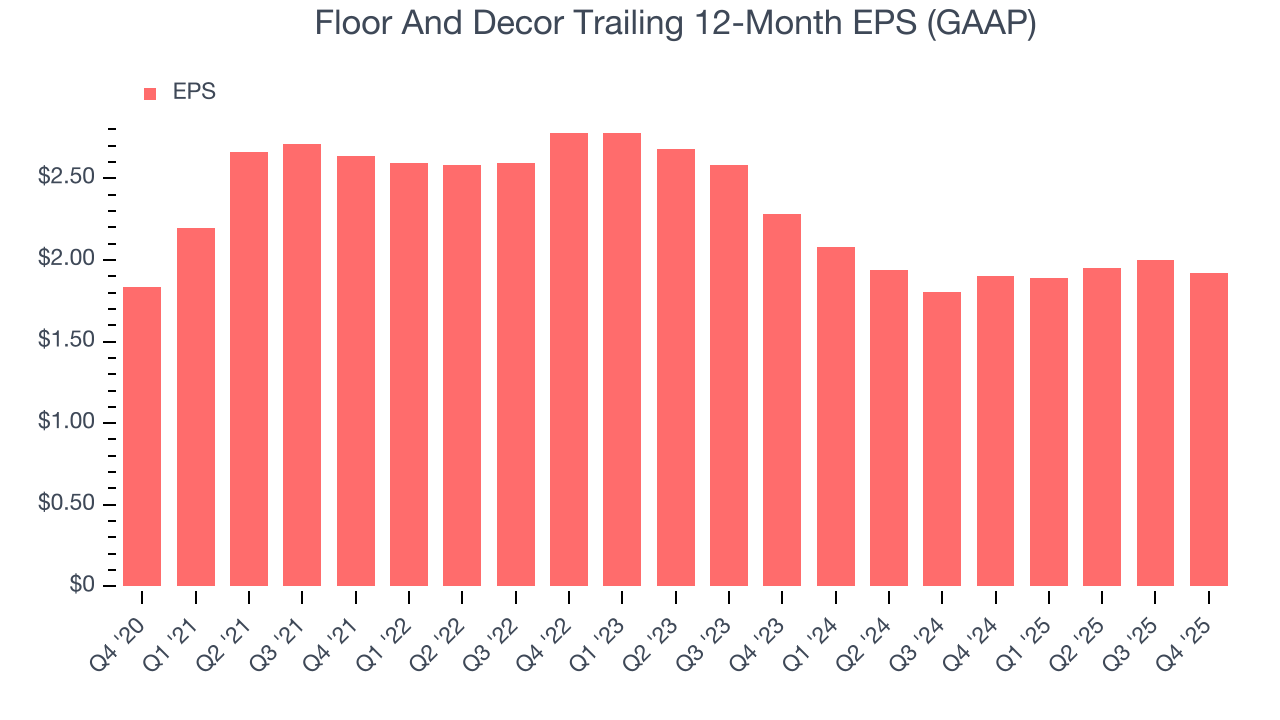

9. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Sadly for Floor And Decor, its EPS declined by 11.5% annually over the last three years while its revenue grew by 3.2%. This tells us the company became less profitable on a per-share basis as it expanded.

In Q4, Floor And Decor reported EPS of $0.36, down from $0.44 in the same quarter last year. Despite falling year on year, this print beat analysts’ estimates by 3.3%. Over the next 12 months, Wall Street expects Floor And Decor’s full-year EPS of $1.92 to grow 10.4%.

10. Cash Is King

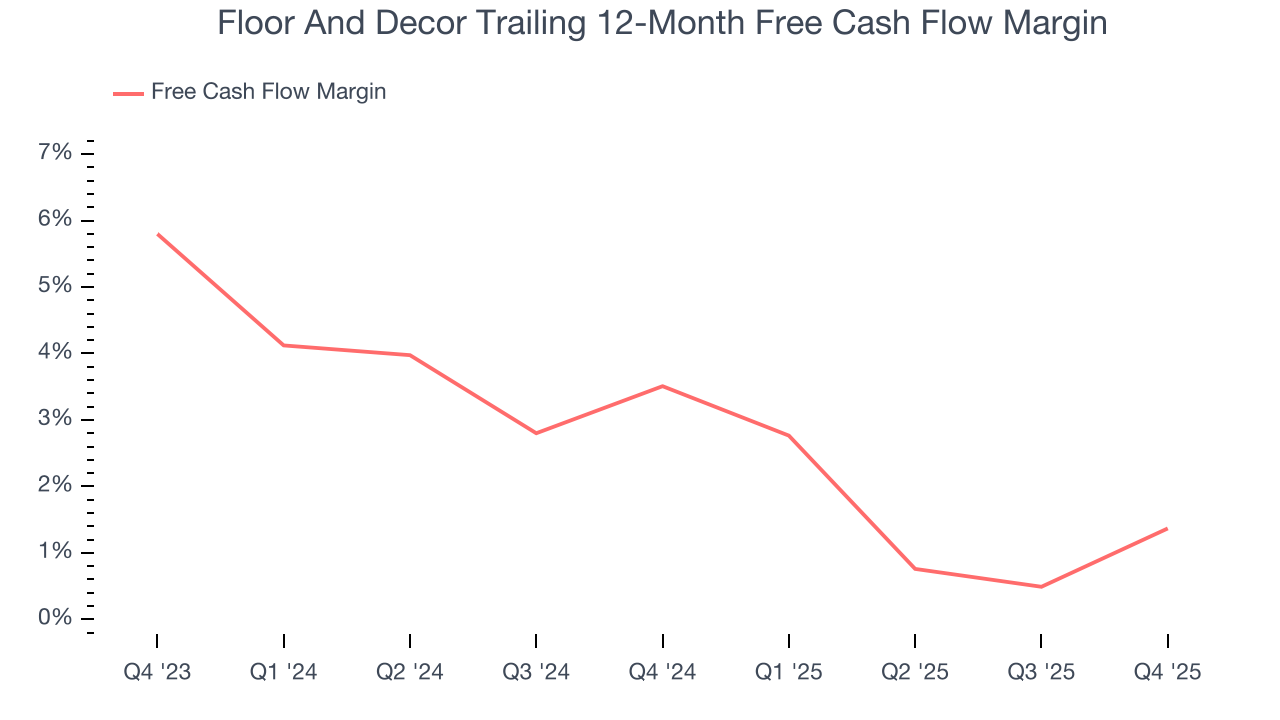

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Floor And Decor has shown mediocre cash profitability over the last two years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 2.4%, subpar for a consumer retail business.

Taking a step back, we can see that Floor And Decor’s margin dropped by 2.1 percentage points over the last year. This decrease came from the higher costs associated with opening more stores.

Floor And Decor’s free cash flow clocked in at $45.14 million in Q4, equivalent to a 4% margin. This result was good as its margin was 3.6 percentage points higher than in the same quarter last year, but we wouldn’t read too much into the short term because investment needs can be seasonal, leading to temporary swings. Long-term trends carry greater meaning.

11. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Floor And Decor historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 8.4%, somewhat low compared to the best consumer retail companies that consistently pump out 25%+.

12. Balance Sheet Assessment

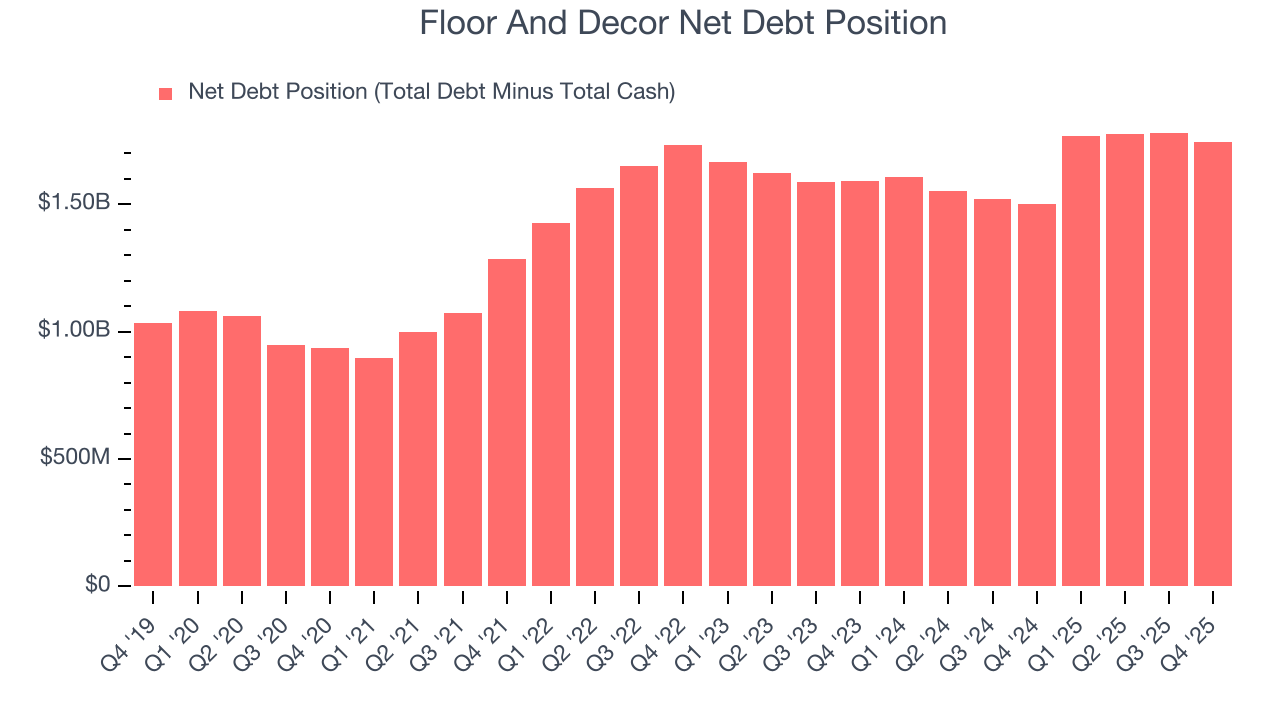

Floor And Decor reported $249.3 million of cash and $1.99 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $538.2 million of EBITDA over the last 12 months, we view Floor And Decor’s 3.2× net-debt-to-EBITDA ratio as safe. We also see its $3.02 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

13. Key Takeaways from Floor And Decor’s Q4 Results

It was good to see Floor And Decor narrowly top analysts’ EBITDA expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. On the other hand, its full-year EBITDA guidance missed and its full-year revenue guidance fell slightly short of Wall Street’s estimates. Overall, this was a mixed quarter, but it seems like a better-than-feared result that is driving shares higher. The stock traded up 6.9% to $70.64 immediately after reporting.

14. Is Now The Time To Buy Floor And Decor?

Updated: March 15, 2026 at 10:32 PM EDT

When considering an investment in Floor And Decor, investors should account for its valuation and business qualities as well as what’s happened in the latest quarter.

We see the value of companies helping consumers, but in the case of Floor And Decor, we’re out. First off, its revenue growth was uninspiring over the last three years. While its new store openings have increased its brand equity, the downside is its shrinking same-store sales tell us it will need to change its strategy to succeed. On top of that, its relatively low ROIC suggests management has struggled to find compelling investment opportunities.

Floor And Decor’s P/E ratio based on the next 12 months is 26.8x. This valuation tells us a lot of optimism is priced in - we think other companies feature superior fundamentals at the moment.

Wall Street analysts have a consensus one-year price target of $75.64 on the company (compared to the current share price of $57.00).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.