Hims & Hers Health (HIMS)

We’re firm believers in Hims & Hers Health. Its innovative offerings are driving strong demand, as seen by the increase in its customer base.― StockStory Analyst Team

1. News

2. Summary

Why We Like Hims & Hers Health

Originally launched with a focus on stigmatized conditions like hair loss and sexual health, Hims & Hers Health (NYSE:HIMS) operates a consumer-focused telehealth platform that connects patients with healthcare providers for prescriptions and wellness products.

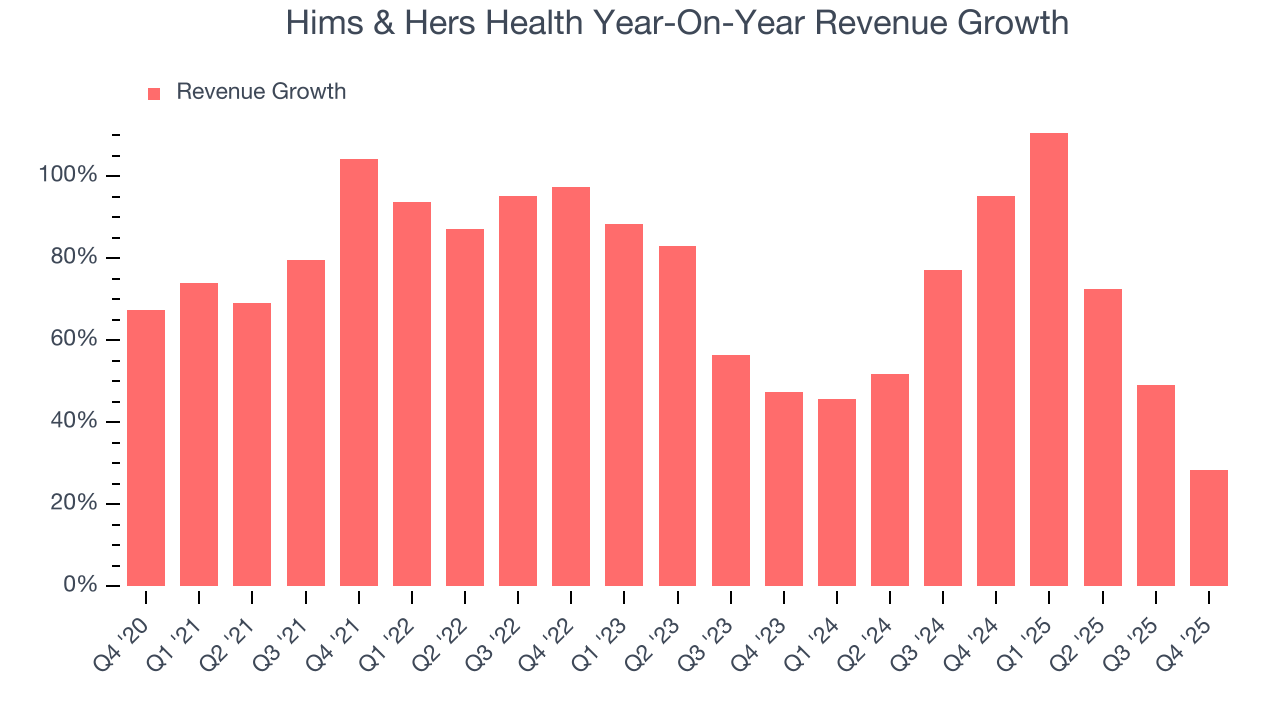

- Annual revenue growth of 73.6% over the last five years was superb and indicates its market share increased during this cycle

- Earnings per share have massively outperformed its peers over the last four years, increasing by 40.4% annually

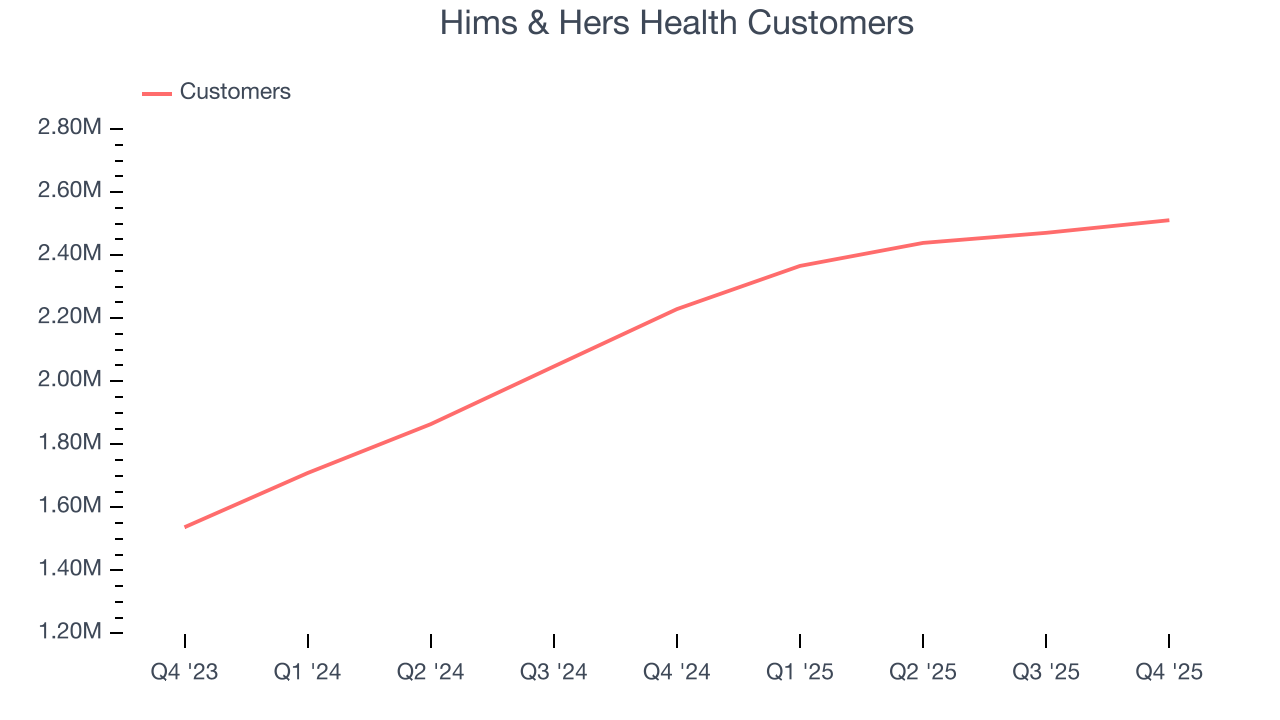

- Business is winning new contracts that can potentially increase in value as its customer base averaged 29.5% growth over the past two years

We’re optimistic about Hims & Hers Health. The valuation seems reasonable relative to its quality, so this might be a favorable time to invest in some shares.

Why Is Now The Time To Buy Hims & Hers Health?

Hims & Hers Health’s stock price of $24.55 implies a valuation ratio of 21.6x forward P/E. This valuation is fair - even cheap depending on how much you like the story - for the quality you get.

Entry price matters far less than business fundamentals if you’re investing for a multi-year period. But if you can get a bargain price it’s certainly icing on the cake.

3. Hims & Hers Health (HIMS) Research Report: Q4 CY2025 Update

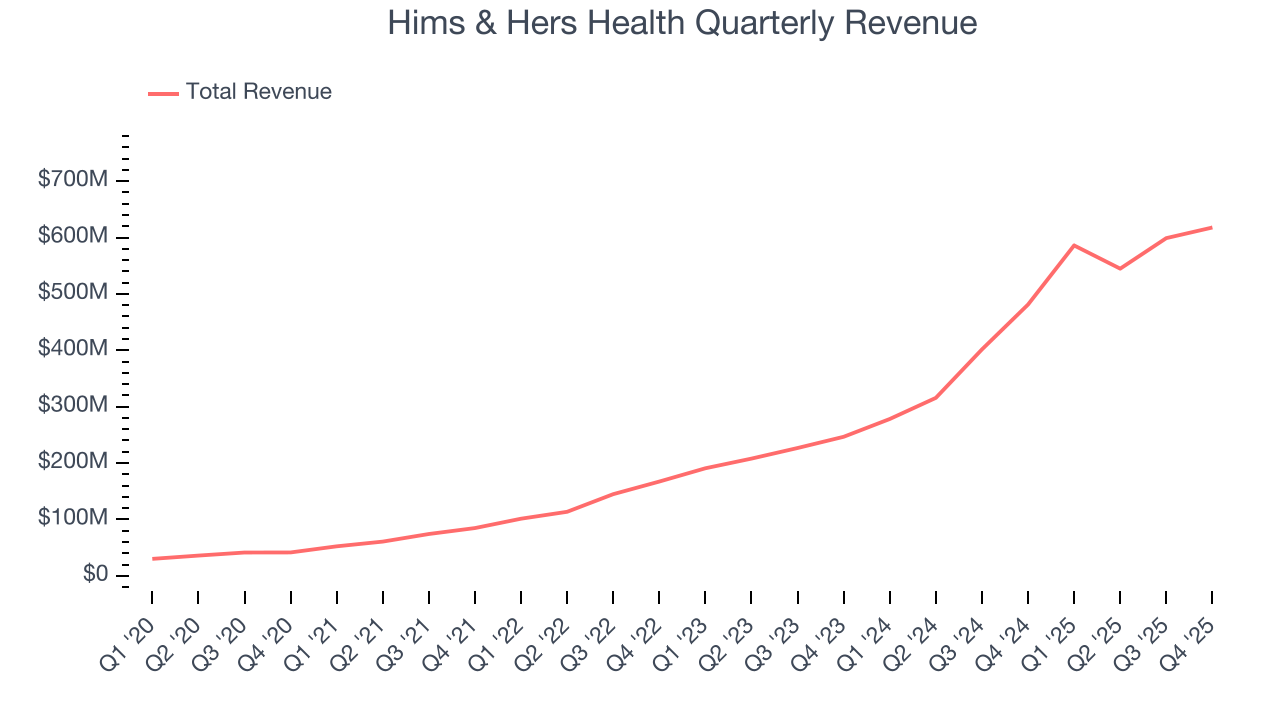

Telehealth company Hims & Hers Health (NYSE:HIMS) met Wall Street’s revenue expectations in Q4 CY2025, with sales up 28.4% year on year to $617.8 million. On the other hand, next quarter’s revenue guidance of $612.5 million was less impressive, coming in 5.6% below analysts’ estimates. Its GAAP profit of $0.08 per share was 92.5% above analysts’ consensus estimates.

Hims & Hers Health (HIMS) Q4 CY2025 Highlights:

- Revenue: $617.8 million vs analyst estimates of $617.9 million (28.4% year-on-year growth, in line)

- EPS (GAAP): $0.08 vs analyst estimates of $0.04 (92.5% beat)

- Adjusted EBITDA: $66.33 million vs analyst estimates of $60.45 million (10.7% margin, 9.7% beat)

- Revenue Guidance for Q1 CY2026 is $612.5 million at the midpoint, below analyst estimates of $649 million

- EBITDA guidance for the upcoming financial year 2026 is $337.5 million at the midpoint, below analyst estimates of $356.1 million

- Operating Margin: 1.5%, down from 3.9% in the same quarter last year

- Free Cash Flow was -$2.57 million, down from $59.5 million in the same quarter last year

- Customers: 2.51 million, up from 2.47 million in the previous quarter

- Market Capitalization: $3.56 billion

Company Overview

Originally launched with a focus on stigmatized conditions like hair loss and sexual health, Hims & Hers Health (NYSE:HIMS) operates a consumer-focused telehealth platform that connects patients with healthcare providers for prescriptions and wellness products.

The company's digital platform enables customers to consult with licensed healthcare professionals remotely for a range of conditions, including sexual health, hair loss, dermatology, mental health, and weight management. When appropriate, providers can prescribe medications that are then fulfilled through partner pharmacies and delivered to customers, typically on a subscription basis. This recurring revenue model creates predictable income streams while providing customers with convenient ongoing care.

Hims & Hers also offers a variety of over-the-counter products, including both white-labeled items and proprietary formulations developed with manufacturing partners. These products span categories like skincare, wellness supplements, and sexual health accessories. Many of these non-prescription items are available not only through the company's digital channels but also in thousands of retail locations across the United States.

For example, a customer experiencing hair loss might take an online assessment, connect with a provider through the platform for a virtual consultation, receive a prescription for finasteride if appropriate, and set up regular deliveries of both the medication and complementary non-prescription products like specialized shampoos.

The company's business model navigates the complex regulatory landscape of healthcare through contractual relationships with independent medical groups that employ the providers who deliver care through the platform. These "Affiliated Medical Groups" work exclusively with Hims & Hers, while the company provides the technology infrastructure, administrative support, and customer service that enables the entire ecosystem to function efficiently.

Hims & Hers has also established partnerships with traditional healthcare systems like Mount Sinai and Ochsner Health, creating pathways for customers to access in-person care when needed, complementing the digital-first approach that defines the company's core offering.

4. Healthcare Technology for Patients

The consumer-focused healthcare technology sector leverages digital platforms to make healthcare more accessible and affordable, offering services like telemedicine and prescription discounts. Looking forward, growth is supported by increasing consumer comfort with telehealth and the demand for cost-saving tools amidst rising healthcare expenses. AI-powered diagnostics and personalized digital care also present significant opportunities. However, the sector faces headwinds from heightened competition as large technology and established healthcare companies expand their digital presence.

Hims & Hers Health competes with other telehealth providers like Teladoc Health (NYSE:TDOC) and Amwell (NYSE:AMWL), direct-to-consumer health companies such as Roman Health (parent company Ro is private), and traditional healthcare providers that have expanded into telehealth services.

5. Revenue Scale

Larger companies benefit from economies of scale, where fixed costs like infrastructure, technology, and administration are spread over a higher volume of goods or services, reducing the cost per unit. Scale can also lead to bargaining power with suppliers, greater brand recognition, and more investment firepower. A virtuous cycle can ensue if a scaled company plays its cards right.

With just $2.35 billion in revenue over the past 12 months, Hims & Hers Health lacks scale in an industry where it matters. This makes it difficult to build trust with customers because healthcare is heavily regulated, complex, and resource-intensive. On the bright side, Hims & Hers Health’s smaller revenue base allows it to grow faster if it can execute well.

6. Revenue Growth

A company’s long-term sales performance can indicate its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Thankfully, Hims & Hers Health’s 73.6% annualized revenue growth over the last five years was incredible. Its growth beat the average healthcare company and shows its offerings resonate with customers, a helpful starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within healthcare, a half-decade historical view may miss recent innovations or disruptive industry trends. Hims & Hers Health’s annualized revenue growth of 64.1% over the last two years is below its five-year trend, but we still think the results suggest healthy demand.

We can dig further into the company’s revenue dynamics by analyzing its number of customers, which reached 2.51 million in the latest quarter. Over the last two years, Hims & Hers Health’s customer base averaged 29.5% year-on-year growth. Because this number is lower than its revenue growth, we can see the average customer spent more money each year on the company’s products and services.

This quarter, Hims & Hers Health’s year-on-year revenue growth of 28.4% was excellent, and its $617.8 million of revenue was in line with Wall Street’s estimates. Company management is currently guiding for a 4.5% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 18.2% over the next 12 months, a deceleration versus the last two years. Still, this projection is commendable and suggests the market sees success for its products and services.

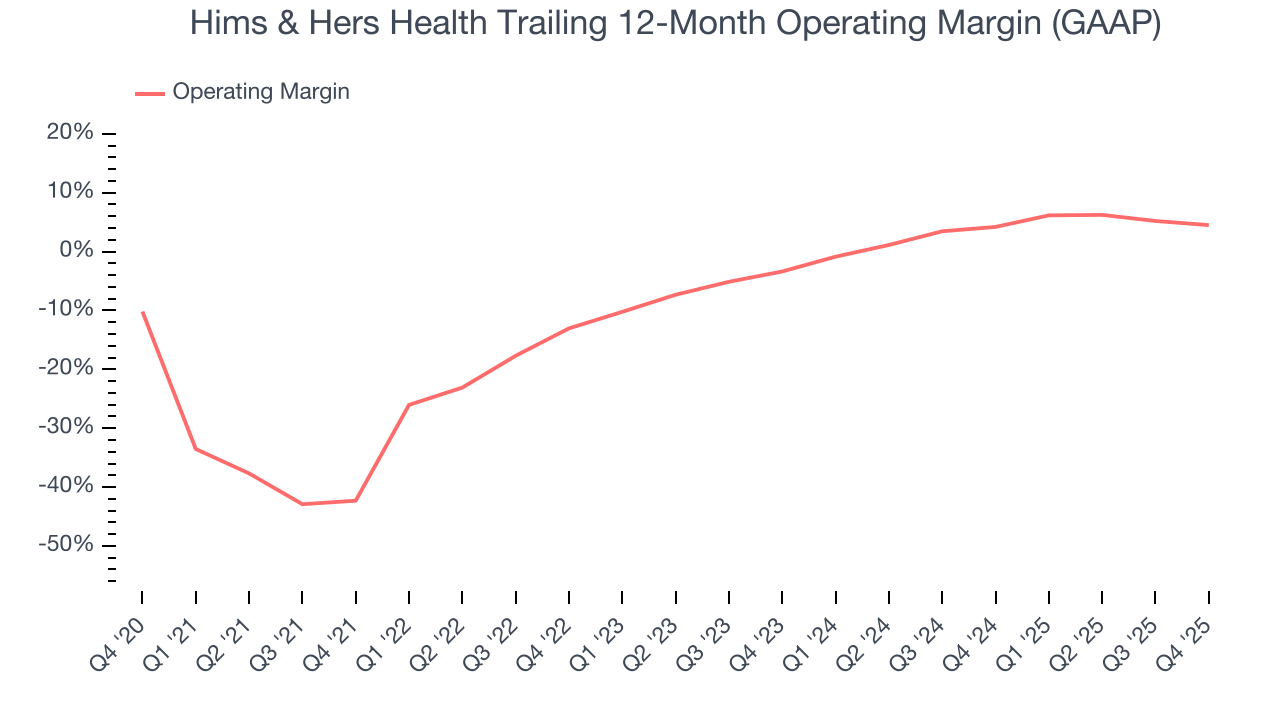

7. Operating Margin

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after subtracting all core expenses, like marketing and R&D.

Hims & Hers Health was roughly breakeven when averaging the last five years of quarterly operating profits, lousy for a healthcare business.

On the plus side, Hims & Hers Health’s operating margin rose by 46.8 percentage points over the last five years, as its sales growth gave it operating leverage. Zooming in on its more recent performance, we can see the company’s trajectory is intact as its margin has also increased by 7.9 percentage points on a two-year basis. These data points are very encouraging and show momentum is on its side.

This quarter, Hims & Hers Health generated an operating margin profit margin of 1.5%, down 2.4 percentage points year on year. This contraction shows it was less efficient because its expenses grew faster than its revenue.

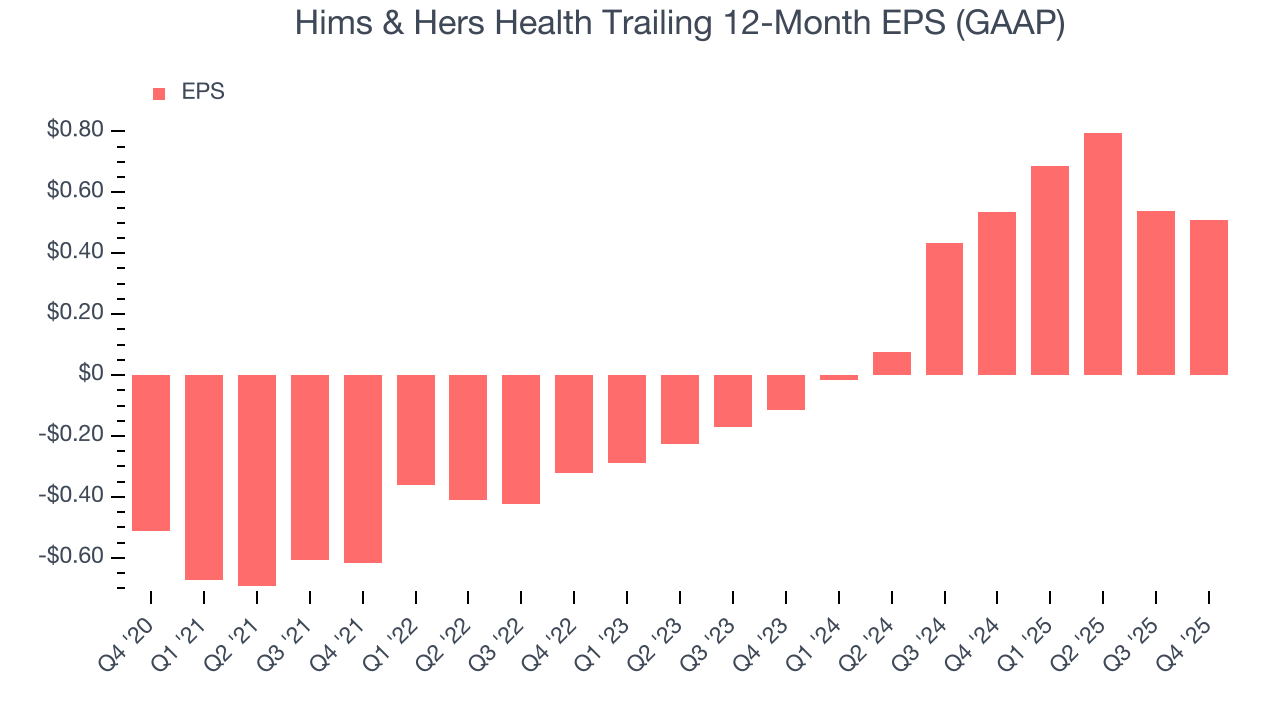

8. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Hims & Hers Health’s full-year EPS flipped from negative to positive over the last five years. This is a good sign and shows it’s at an inflection point.

In Q4, Hims & Hers Health reported EPS of $0.08, down from $0.11 in the same quarter last year. Despite falling year on year, this print easily cleared analysts’ estimates. Over the next 12 months, Wall Street expects Hims & Hers Health’s full-year EPS of $0.51 to grow 44.2%.

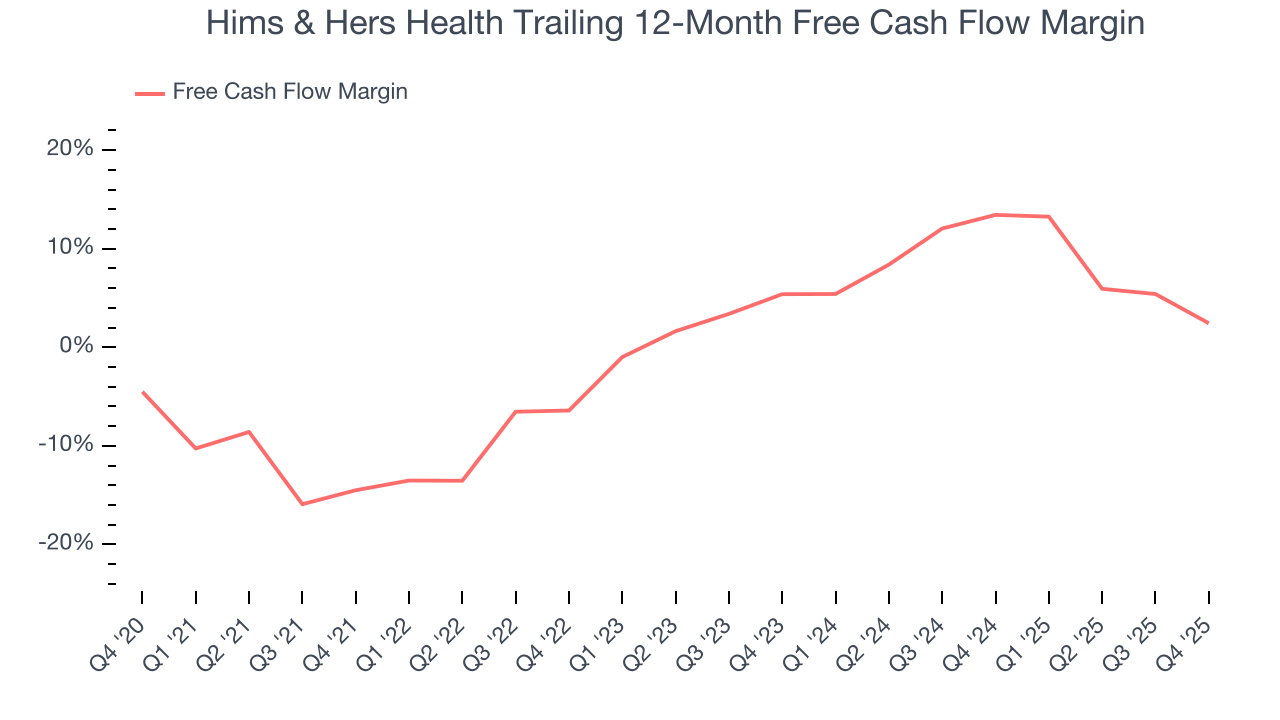

9. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Hims & Hers Health has shown mediocre cash profitability over the last five years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 4.2%, subpar for a healthcare business.

Taking a step back, an encouraging sign is that Hims & Hers Health’s margin expanded by 16.9 percentage points during that time. We have no doubt shareholders would like to continue seeing its cash conversion rise as it gives the company more optionality.

Hims & Hers Health broke even from a free cash flow perspective in Q4. The company’s cash profitability regressed as it was 12.8 percentage points lower than in the same quarter last year, but we wouldn’t read too much into the short term because investment needs can be seasonal, causing temporary swings. Long-term trends trump fluctuations.

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Although Hims & Hers Health has shown solid fundamentals lately, it historically did a mediocre job investing in profitable growth initiatives. Its four-year average ROIC was 1.1%, lower than the typical cost of capital (how much it costs to raise money) for healthcare companies.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Over the last few years, Hims & Hers Health’s ROIC has increased. This is a good sign, but we recognize its lack of profitable growth during the COVID era was the primary reason for the change.

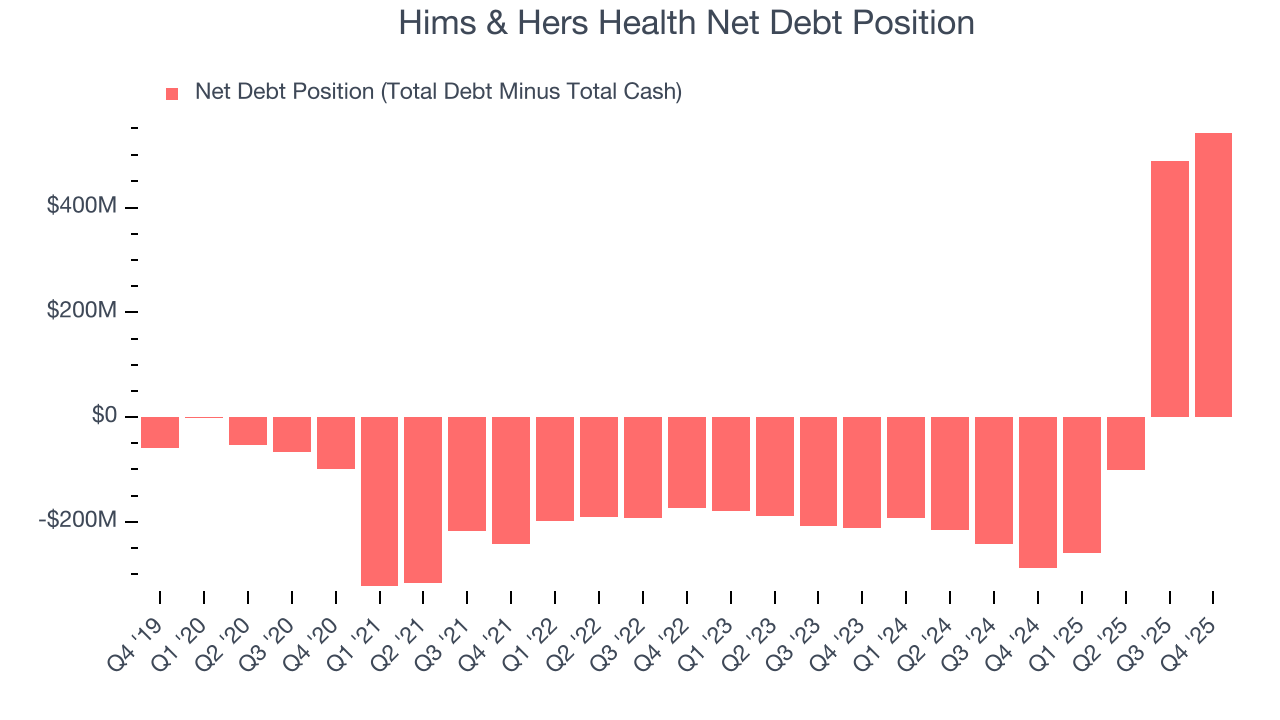

11. Balance Sheet Assessment

Hims & Hers Health reported $577.5 million of cash and $1.12 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $318 million of EBITDA over the last 12 months, we view Hims & Hers Health’s 1.7× net-debt-to-EBITDA ratio as safe. We also see its $9.93 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

12. Key Takeaways from Hims & Hers Health’s Q4 Results

It was good to see Hims & Hers Health beat analysts’ EPS expectations this quarter. We were also glad its full-year revenue guidance trumped Wall Street’s estimates. On the other hand, its revenue guidance for next quarter missed and its EBITDA guidance for next quarter fell short of Wall Street’s estimates. Overall, this print was mixed but still had some key positives. Investors were likely hoping for more, and shares traded down 2% to $15.34 immediately following the results.

13. Is Now The Time To Buy Hims & Hers Health?

Updated: March 15, 2026 at 11:44 PM EDT

A common mistake we notice when investors are deciding whether to buy a stock or not is that they simply look at the latest earnings results. Business quality and valuation matter more, so we urge you to understand these dynamics as well.

Hims & Hers Health is an amazing business ranking highly on our list. First of all, the company’s revenue growth was exceptional over the last five years. And while its relatively low ROIC suggests management has struggled to find compelling investment opportunities, its customer growth has been marvelous. On top of that, Hims & Hers Health’s rising cash profitability gives it more optionality.

Hims & Hers Health’s P/E ratio based on the next 12 months is 21.6x. Looking at the healthcare landscape today, Hims & Hers Health’s fundamentals really stand out, and we like it at this price.

Wall Street analysts have a consensus one-year price target of $23.12 on the company (compared to the current share price of $24.55).