Sweetgreen (SG)

Sweetgreen faces an uphill battle. Its negative returns on capital suggest it eroded shareholder value by squandering business opportunities.― StockStory Analyst Team

1. News

2. Summary

Why We Think Sweetgreen Will Underperform

Founded in 2007 by three Georgetown University alum, Sweetgreen (NYSE:SG) is a casual quick service chain known for its healthy salads and bowls.

- Persistent operating margin losses and eroding margin over the last year point to its preference for growth over profits

- Cash-burning history and the downward spiral in its margin profile make us wonder if it has a viable business model

- Unfavorable liquidity position could lead to additional equity financing that dilutes shareholders

Sweetgreen falls below our quality standards. We believe there are better businesses elsewhere.

Why There Are Better Opportunities Than Sweetgreen

At $5.75 per share, Sweetgreen trades at 310.8x forward EV-to-EBITDA. This valuation multiple seems a bit much considering the quality you get.

We prefer to invest in similarly-priced but higher-quality companies with superior earnings growth.

3. Sweetgreen (SG) Research Report: Q4 CY2025 Update

Casual salad chain Sweetgreen (NYSE:SG) missed Wall Street’s revenue expectations in Q4 CY2025, with sales falling 3.5% year on year to $155.2 million. Its GAAP loss of $0.42 per share was 28.2% below analysts’ consensus estimates.

Sweetgreen (SG) Q4 CY2025 Highlights:

- Revenue: $155.2 million vs analyst estimates of $158.9 million (3.5% year-on-year decline, 2.3% miss)

- EPS (GAAP): -$0.42 vs analyst expectations of -$0.33 (28.2% miss)

- Adjusted EBITDA: -$13.34 million (-8.6% margin, 2,227% year-on-year decline)

- EBITDA guidance for the upcoming financial year 2026 is $3.5 million at the midpoint, below analyst estimates of $4.98 million

- Adjusted EBITDA Margin: -8.6%, down from -0.4% in the same quarter last year

- Same-Store Sales fell 11.5% year on year (4% in the same quarter last year)

- Market Capitalization: $693.7 million

Company Overview

Founded in 2007 by three Georgetown University alum, Sweetgreen (NYSE:SG) is a casual quick service chain known for its healthy salads and bowls.

The three thought that the market was missing a so-called fast casual option that offered healthy, fresh, and locally-sourced food. If it was fast, it leaned unhealthy and if it was healthy and fresh, it leaned upscale and full service.

Sweetgreen specifically offers salads and bowls that use fresh, organic ingredients. The ‘Guacamole Greens’, for example, is a cold salad that includes roasted chicken, avocado, and a slew of traditional salad ingredients. The ‘Shroomami’ is a warm bowl that features roasted tofu, warm portobello mushrooms, beets, warm wild rice, and a few other ingredients. You can alter existing menu items with substitutions, and if you’re really not inspired by what’s offered, you can feel free to create a completely custom salad or bowl.

The typical Sweetgreen customer is a health-conscious individual, often a busy millennial who wants a quick and convenient lunch or dinner without breaking the bank. These individuals care about the origin of their food, and Sweetgreen often has a board in their locations showing where each ingredient is sourced, down to the names of the farms themselves.

Sweetgreen’s locations feature a modern and minimalist vibe. Unlike traditional fast-food joints, these stores favor neutral colors, wood and exposed concrete, and plants. To cater to their often tech-forward customers, the company’s app features the full menu along with nutritional information about items. It also allows users to order ahead of time for pickup to maximize convenience and efficiency.

4. Modern Fast Food

Modern fast food is a relatively newer category representing a middle ground between traditional fast food and sit-down restaurants. These establishments feature an expanded menu selection priced above traditional fast food options, often incorporating fresher and cleaner ingredients to serve customers prioritizing quality. These eateries are capitalizing on the perception that your drive-through burger and fries joint is detrimental to your health because of inferior ingredients.

Competitors in the casual quick service industry include Chipotle (NYSE:CMG), CAVA (NYSE:CAVA), Noodles & Company (NASDAQ:NDLS), and private companies such as Chopt Creative Salad and Just Salad.

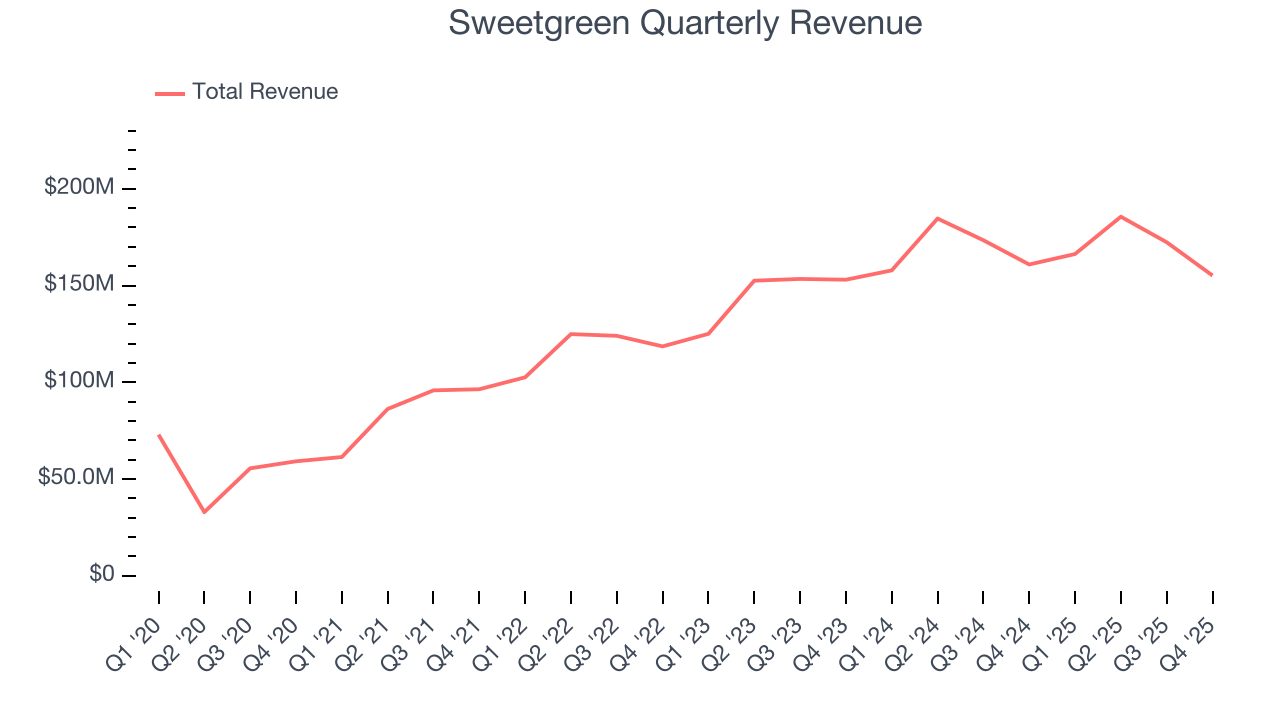

5. Revenue Growth

A company’s long-term performance is an indicator of its overall quality. Any business can have short-term success, but a top-tier one grows for years.

With $679.5 million in revenue over the past 12 months, Sweetgreen is a small restaurant chain, which sometimes brings disadvantages compared to larger competitors benefiting from better brand awareness and economies of scale. On the bright side, it can grow faster because it has more white space to build new restaurants.

As you can see below, Sweetgreen’s 16.3% annualized revenue growth over the last six years was excellent as it opened new restaurants and expanded its reach.

This quarter, Sweetgreen missed Wall Street’s estimates and reported a rather uninspiring 3.5% year-on-year revenue decline, generating $155.2 million of revenue.

Looking ahead, sell-side analysts expect revenue to grow 11% over the next 12 months, a deceleration versus the last six years. Despite the slowdown, this projection is admirable and implies the market is forecasting success for its menu offerings.

6. Restaurant Performance

Number of Restaurants

A restaurant chain’s total number of dining locations influences how much it can sell and how quickly revenue can grow.

Sweetgreen opened new restaurants at a rapid clip over the last two years, averaging 11.9% annual growth, much faster than the broader restaurant sector. This gives it a chance to scale into a mid-sized business over time.

When a chain opens new restaurants, it usually means it’s investing for growth because there’s healthy demand for its meals and there are markets where its concepts have few or no locations.

Note that Sweetgreen reports its restaurant count intermittently, so some data points are missing in the chart below.

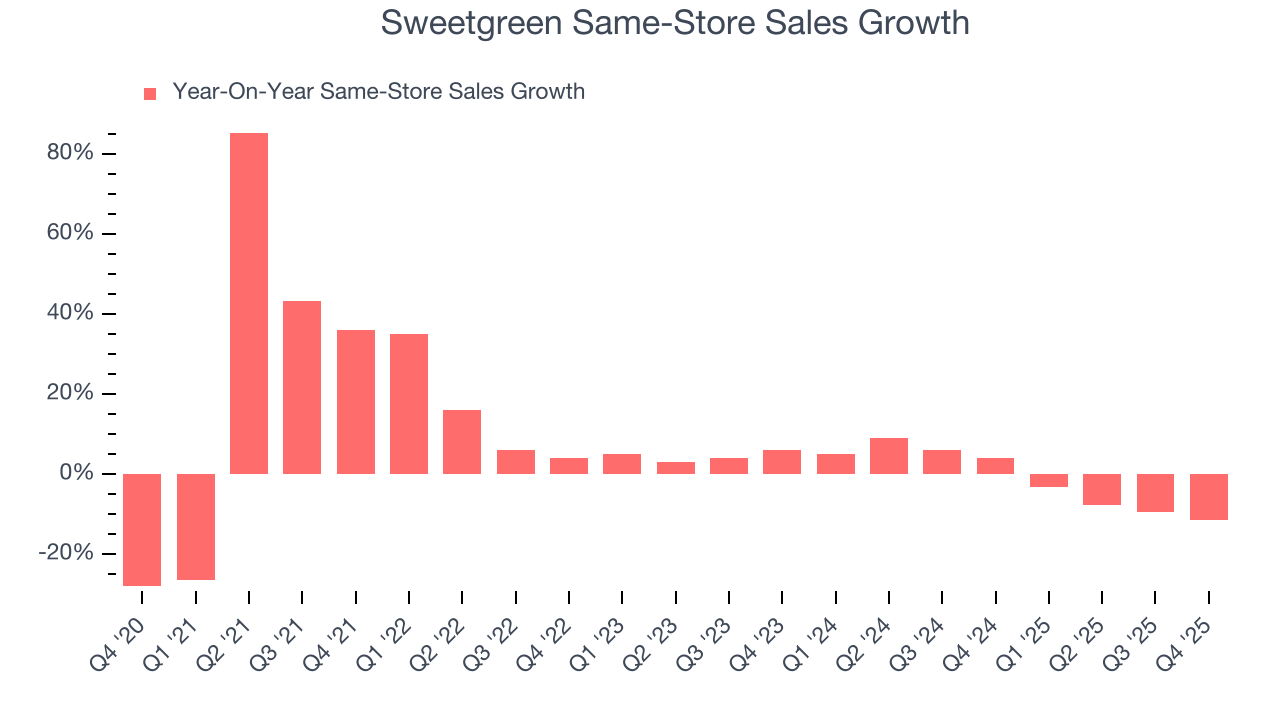

Same-Store Sales

The change in a company's restaurant base only tells one side of the story. The other is the performance of its existing locations, which informs management teams whether they should expand or downsize their physical footprints. Same-store sales gives us insight into this topic because it measures organic growth at restaurants open for at least a year.

Sweetgreen’s demand within its existing dining locations has barely increased over the last two years as its same-store sales were flat. Sweetgreen should consider improving its foot traffic and efficiency before expanding its restaurant base.

In the latest quarter, Sweetgreen’s same-store sales fell by 11.5% year on year. This decrease represents a further deceleration from its historical levels. We hope the business can get back on track.

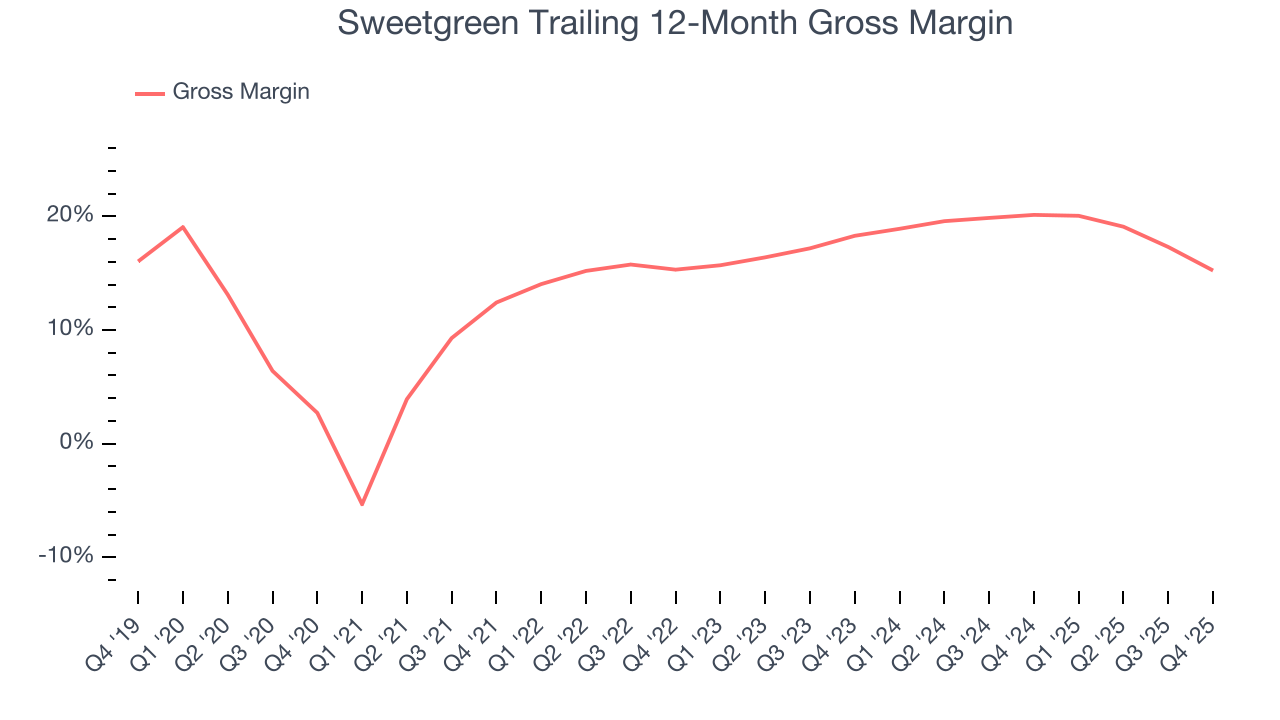

7. Gross Margin & Pricing Power

Sweetgreen has bad unit economics for a restaurant company, signaling it operates in a competitive market and has little room for error if demand unexpectedly falls. As you can see below, it averaged a 17.7% gross margin over the last two years. Said differently, Sweetgreen had to pay a chunky $82.32 to its suppliers for every $100 in revenue.

In Q4, Sweetgreen produced a 10.4% gross profit margin, down 9 percentage points year on year. Sweetgreen’s full-year margin has also been trending down over the past 12 months, decreasing by 4.9 percentage points. If this move continues, it could suggest a more competitive environment with some pressure to lower prices and higher input costs (such as ingredients and transportation expenses).

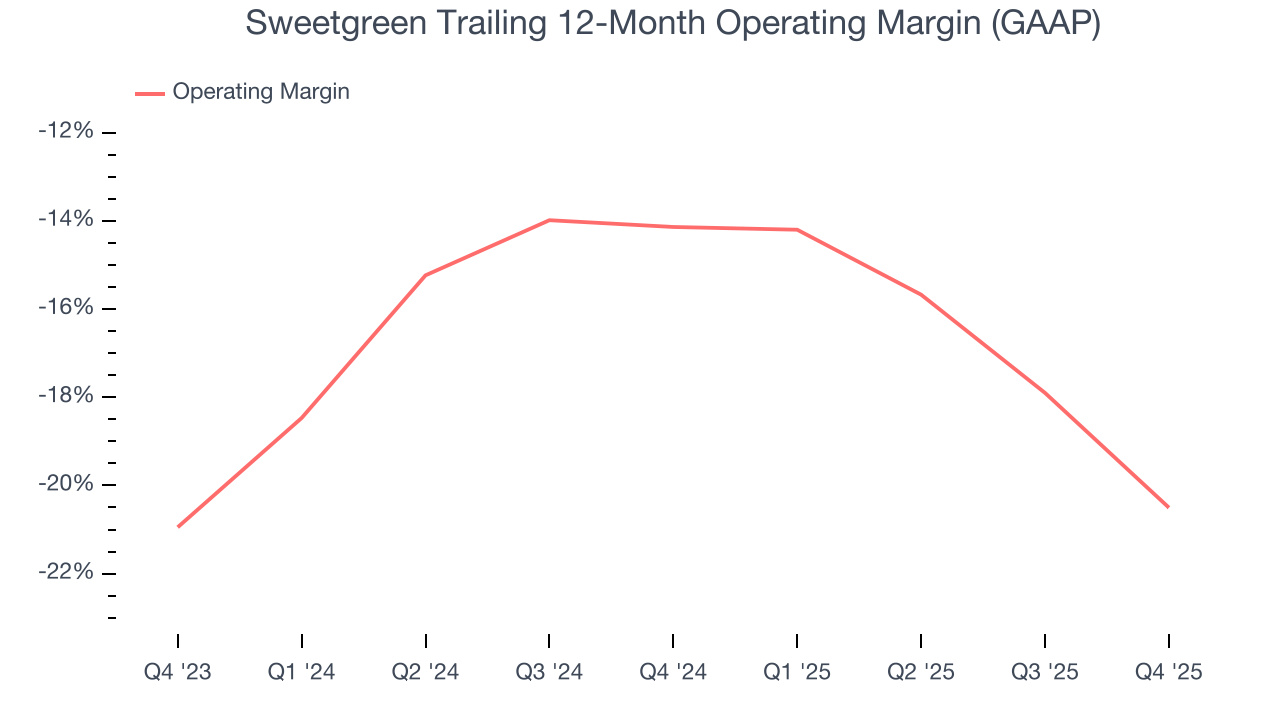

8. Operating Margin

Operating margin is a key profitability metric because it accounts for all expenses keeping the business in motion, including food costs, wages, rent, advertising, and other administrative costs.

The restaurant business is tough to succeed in because of its unpredictability, whether it be employees not showing up for work, sudden changes in consumer preferences, or the cost of ingredients skyrocketing thanks to supply shortages.Sweetgreen has been a victim of these challenges over the last two years, and its high expenses have contributed to an average operating margin of negative 17.3%.

Looking at the trend in its profitability, Sweetgreen’s operating margin decreased by 6.4 percentage points over the last year. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. Sweetgreen’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers.

This quarter, Sweetgreen generated a negative 31% operating margin.

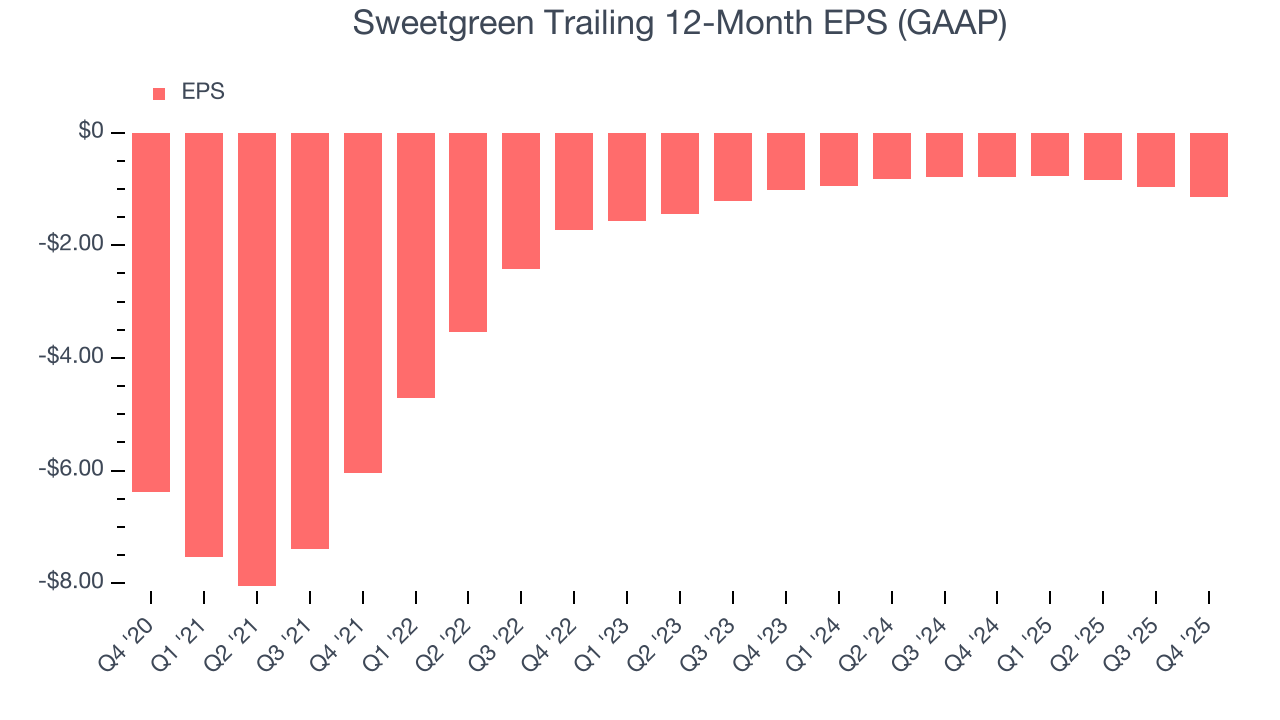

9. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Sweetgreen’s earnings losses deepened over the last six years as its EPS dropped 12.1% annually. We tend to steer our readers away from companies with falling EPS, where diminishing earnings could imply changing secular trends and preferences. If the tide turns unexpectedly, Sweetgreen’s low margin of safety could leave its stock price susceptible to large downswings.

In Q4, Sweetgreen reported EPS of negative $0.42, down from negative $0.25 in the same quarter last year. This print missed analysts’ estimates. Over the next 12 months, Wall Street expects Sweetgreen to improve its earnings losses. Analysts forecast its full-year EPS of negative $1.14 will advance to negative $0.77.

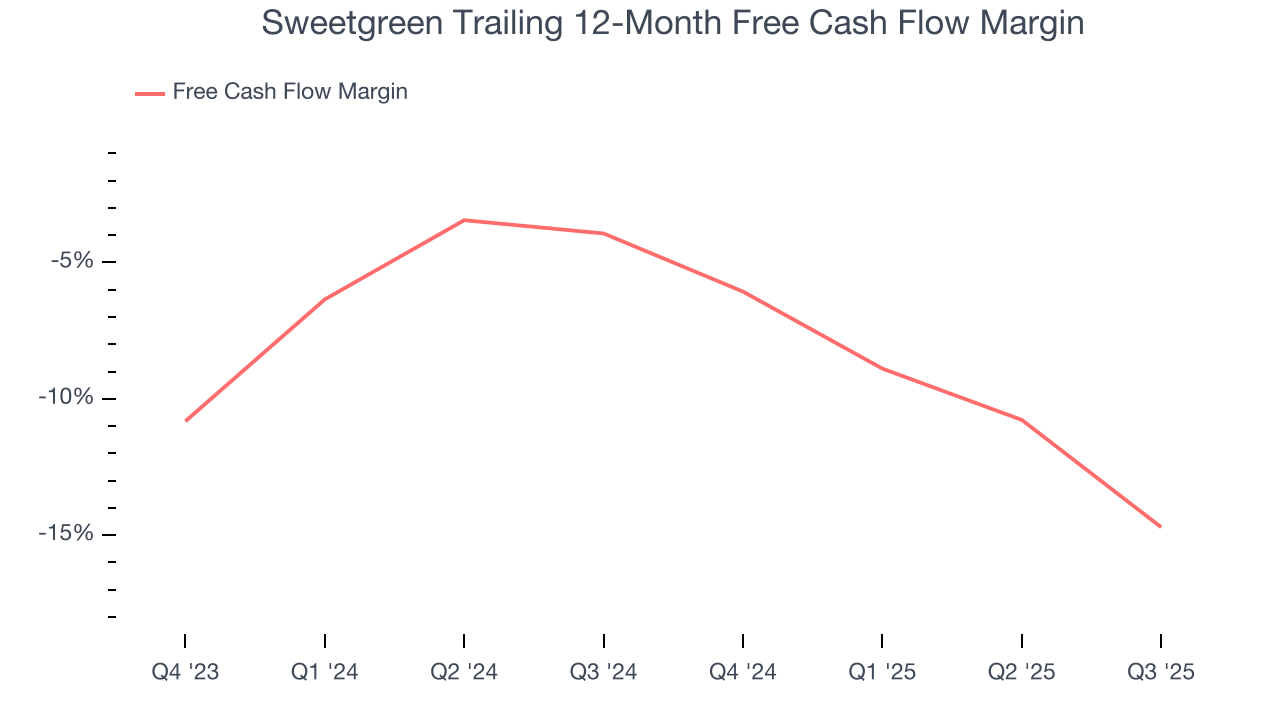

10. Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

Over the last two years, Sweetgreen’s capital-intensive business model and large investments in new physical locations have drained its resources, putting it in a pinch and limiting its ability to return capital to investors. Its free cash flow margin averaged negative 10.1%, meaning it lit $10.10 of cash on fire for every $100 in revenue.

11. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Sweetgreen’s four-year average ROIC was negative 45.3%, meaning management lost money while trying to expand the business. Its returns were among the worst in the restaurant sector.

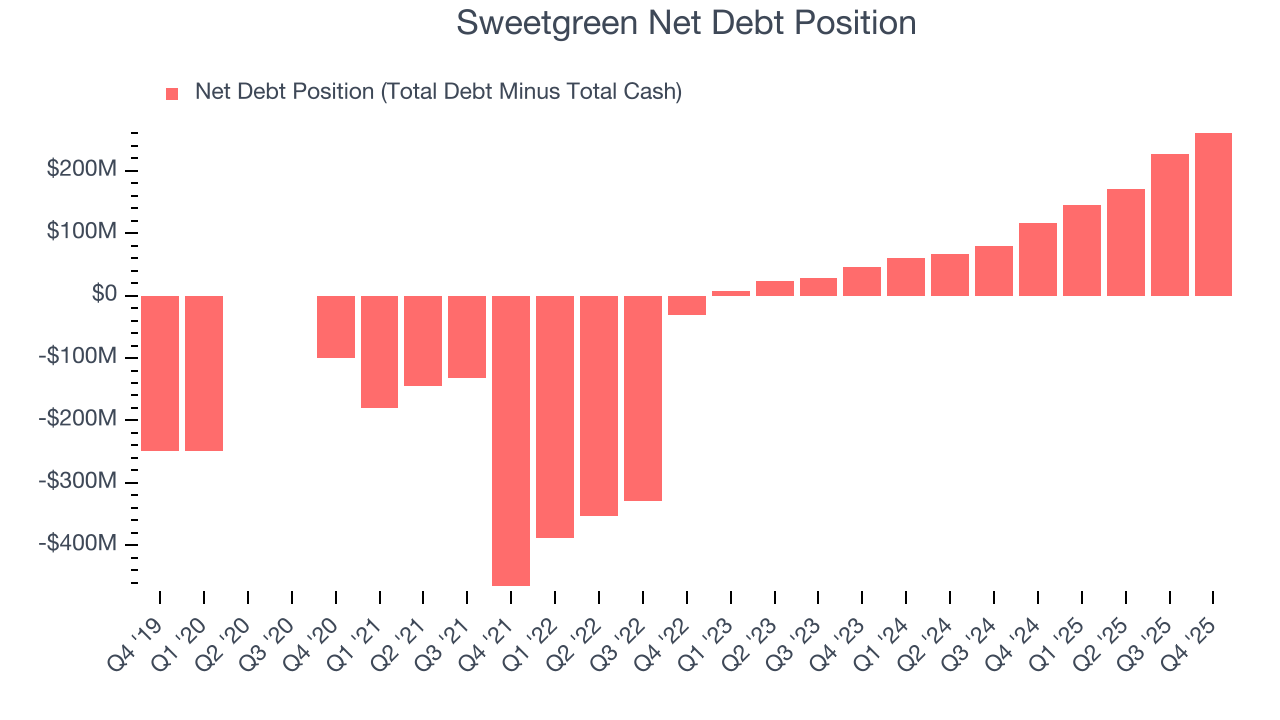

12. Balance Sheet Risk

Debt is a tool that can boost company returns but presents risks if used irresponsibly. As long-term investors, we aim to avoid companies taking excessive advantage of this instrument because it could lead to insolvency.

Sweetgreen posted negative $11 million of EBITDA over the last 12 months, and its $354.5 million of debt exceeds the $93.34 million of cash on its balance sheet. This is a deal breaker for us because indebted loss-making companies spell trouble.

We implore our readers to tread carefully because credit agencies could downgrade Sweetgreen if its unprofitable ways continue, making incremental borrowing more expensive and restricting growth prospects. The company could also be backed into a corner if the market turns unexpectedly. We hope Sweetgreen can improve its profitability and remain cautious until then.

13. Key Takeaways from Sweetgreen’s Q4 Results

We were impressed by how significantly Sweetgreen blew past analysts’ EBITDA expectations this quarter. We were also happy its same-store sales was in line with Wall Street’s estimates. On the other hand, its full-year EBITDA guidance missed and its EPS fell short of Wall Street’s estimates. Overall, this was a softer quarter. The stock remained flat at $6.11 immediately after reporting.

14. Is Now The Time To Buy Sweetgreen?

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in Sweetgreen.

Sweetgreen doesn’t pass our quality test. Although its revenue growth was impressive over the last six years, it’s expected to deteriorate over the next 12 months and its declining EPS over the last six years makes it a less attractive asset to the public markets. And while the company’s new restaurant openings have increased its brand equity, the downside is its relatively low ROIC suggests management has struggled to find compelling investment opportunities.

Sweetgreen’s EV-to-EBITDA ratio based on the next 12 months is 161x. At this valuation, there’s a lot of good news priced in - you can find more timely opportunities elsewhere.

Wall Street analysts have a consensus one-year price target of $7.90 on the company (compared to the current share price of $6.11).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.