America's Car-Mart (CRMT)

We wouldn’t buy America's Car-Mart. Not only are its sales cratering but also its low returns on capital suggest it struggles to generate profits.― StockStory Analyst Team

1. News

2. Summary

Why We Think America's Car-Mart Will Underperform

With a strong presence in the Southern and Central US, America’s Car-Mart (NASDAQ:CRMT) sells used cars to budget-conscious consumers.

- Earnings per share have dipped by 31.2% annually over the past three years, which is concerning because stock prices follow EPS over the long term

- Modest revenue base of $1.34 billion gives it less fixed cost leverage and fewer distribution channels than larger companies

- 46× net-debt-to-EBITDA ratio shows it’s overleveraged and increases the probability of shareholder dilution if things turn unexpectedly

America's Car-Mart’s quality doesn’t meet our hurdle. There’s a wealth of better opportunities.

Why There Are Better Opportunities Than America's Car-Mart

At $12.75 per share, America's Car-Mart trades at 21.5x forward EV-to-EBITDA. This multiple expensive for its subpar fundamentals.

Paying a premium for high-quality companies with strong long-term earnings potential is preferable to owning challenged businesses with questionable prospects. That helps the prudent investor sleep well at night.

3. America's Car-Mart (CRMT) Research Report: Q4 CY2025 Update

Used-car retailer America’s Car-Mart (NASDAQ:CRMT) missed Wall Street’s revenue expectations in Q4 CY2025, with sales falling 11.6% year on year to $286.8 million. Its non-GAAP loss of $7.72 per share was significantly below analysts’ consensus estimates.

America's Car-Mart (CRMT) Q4 CY2025 Highlights:

- Revenue: $286.8 million vs analyst estimates of $329.3 million (11.6% year-on-year decline, 12.9% miss)

- Adjusted EPS: -$7.72 vs analyst estimates of -$0.26 (significant miss)

- Adjusted EBITDA: -$10.75 million vs analyst estimates of $18.04 million (-3.7% margin, significant miss)

- Operating Margin: -4.5%, down from 6.6% in the same quarter last year

- Free Cash Flow was -$6.20 million compared to -$31.53 million in the same quarter last year

- Locations: 149 at quarter end, down from 154 in the same quarter last year

- Same-Store Sales fell 13.4% year on year (3.1% in the same quarter last year)

- Market Capitalization: $158 million

Company Overview

With a strong presence in the Southern and Central US, America’s Car-Mart (NASDAQ:CRMT) sells used cars to budget-conscious consumers.

This core customer is usually a credit-constrained consumer who may have difficulty securing financing from traditional lenders such as banks. These customers may have poor or limited credit histories, which traditional lenders rely on to underwrite auto loans. America’s Car-Mart’s ‘buy here, pay here’ model addresses these difficulties. In this model, the dealership acts as both the seller of the vehicle and the financier, allowing a customer to purchase a car directly from America’s Car-Mart and make their payments directly to the company rather than a bank or other finance provider.

America’s Car-Mart locations are 8,000 to 10,000 square feet with ample outdoor space to display used cars for sale. These locations are primarily located in smaller cities and towns, especially ones with credit-challenged and likely lower-income populations. While the company does have an e-commerce presence, it was only established in 2020 and physical locations remain the primary avenue for doing business.

4. Vehicle Retailer

Buying a vehicle is a big decision and usually the second-largest purchase behind a home for many people, so retailers that sell new and used cars try to offer selection, convenience, and customer service to shoppers. While there is online competition, especially for research and discovery, the vehicle sales market is still very fragmented and localized given the magnitude of the purchase and the logistical costs associated with moving cars over long distances. At the end of the day, a large swath of the population relies on cars to get from point A to point B, and vehicle sellers are acutely aware of this need.

Competitors in the auto retail space include AutoNation (NYSE:AN), CarMax (NYSE:KMX), and Group 1 Automotive (NYSE:GPI).

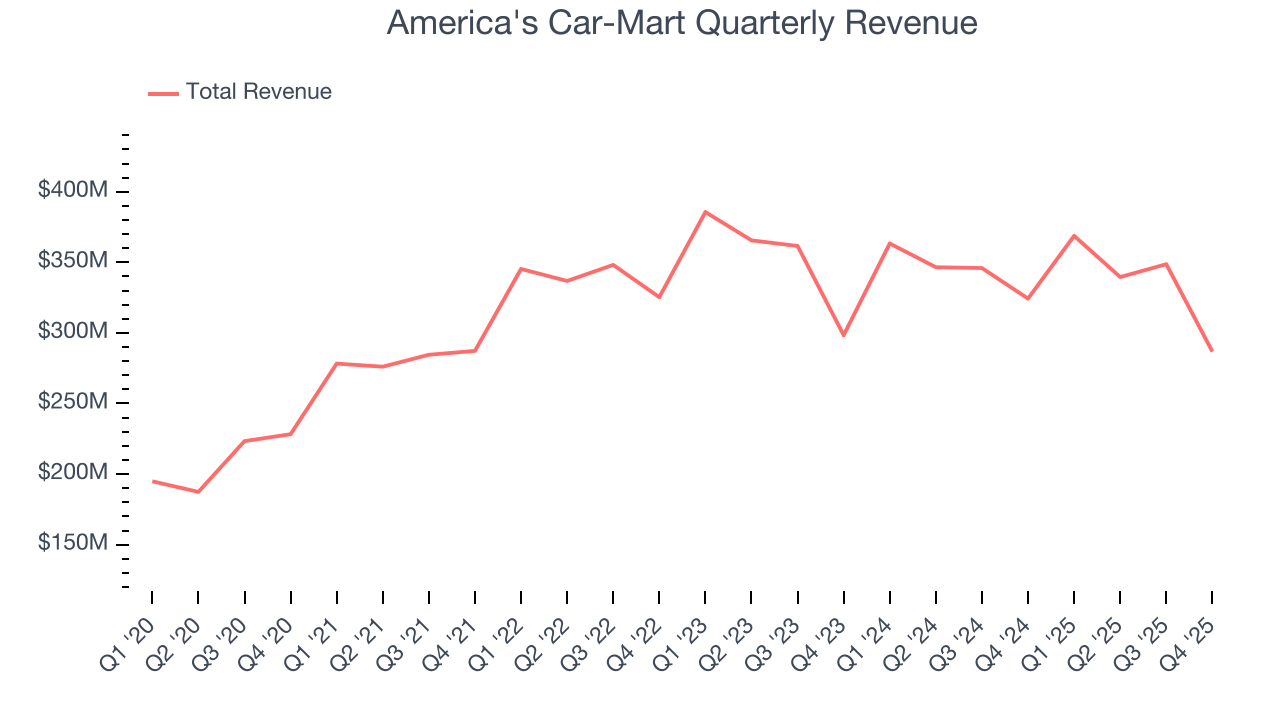

5. Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years.

With $1.34 billion in revenue over the past 12 months, America's Car-Mart is a small retailer, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage with suppliers.

As you can see below, America's Car-Mart struggled to increase demand as its $1.34 billion of sales for the trailing 12 months was close to its revenue three years ago. This was mainly because it didn’t open many new stores and observed lower sales at existing, established locations.

This quarter, America's Car-Mart missed Wall Street’s estimates and reported a rather uninspiring 11.6% year-on-year revenue decline, generating $286.8 million of revenue.

Looking ahead, sell-side analysts expect revenue to grow 4.9% over the next 12 months, an acceleration versus the last three years. This projection is noteworthy and suggests its newer products will catalyze better top-line performance.

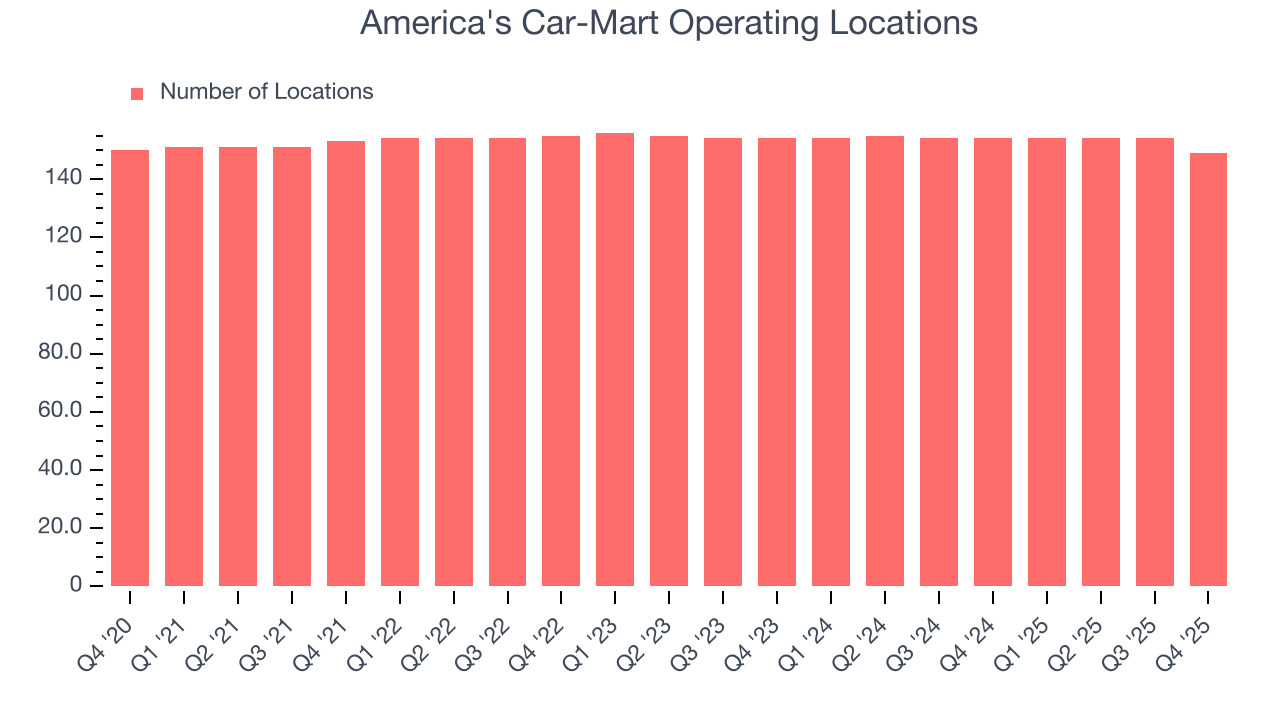

6. Store Performance

Number of Stores

The number of stores a retailer operates is a critical driver of how quickly company-level sales can grow.

America's Car-Mart listed 149 locations in the latest quarter and has kept its store count flat over the last two years while other consumer retail businesses have opted for growth.

When a retailer keeps its store footprint steady, it usually means demand is stable and it’s focusing on operational efficiency to increase profitability.

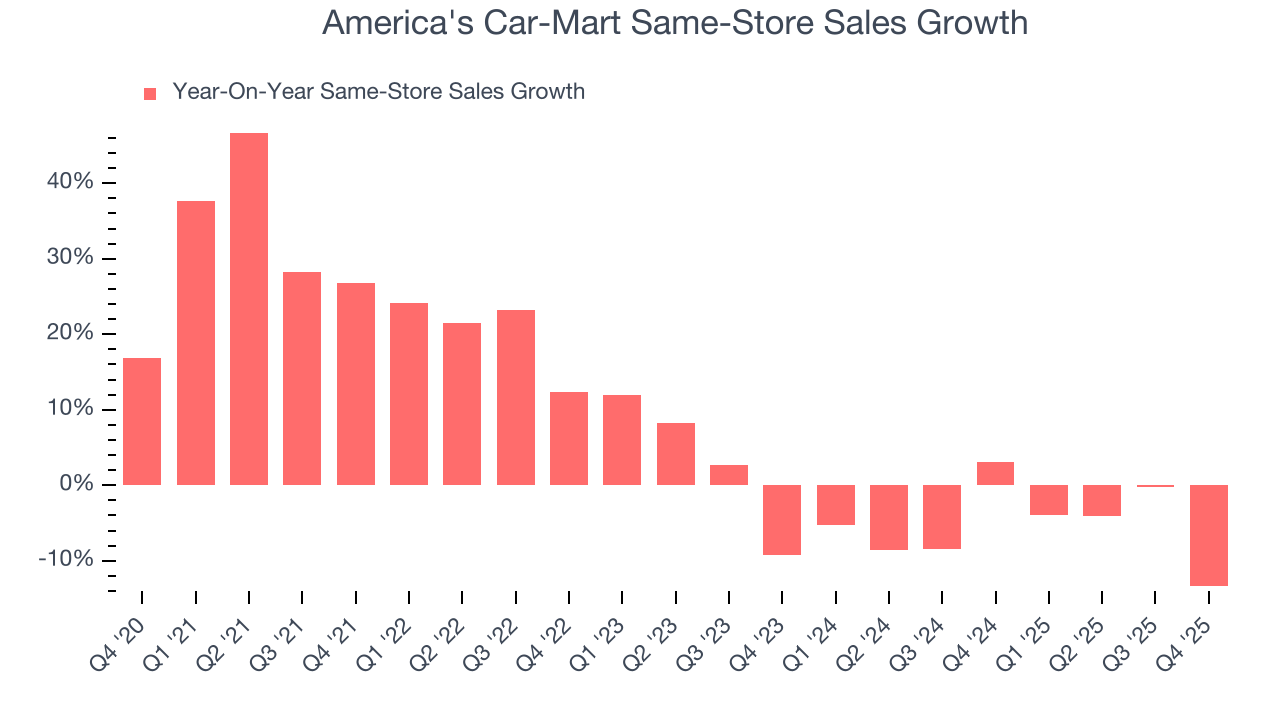

Same-Store Sales

The change in a company's store base only tells one side of the story. The other is the performance of its existing locations and e-commerce sales, which informs management teams whether they should expand or downsize their physical footprints. Same-store sales gives us insight into this topic because it measures organic growth for a retailer's e-commerce platform and brick-and-mortar shops that have existed for at least a year.

America's Car-Mart’s demand has been shrinking over the last two years as its same-store sales have averaged 5.1% annual declines. This performance isn’t ideal, and we’d be concerned if America's Car-Mart starts opening new stores to artificially boost revenue growth.

In the latest quarter, America's Car-Mart’s same-store sales fell by 13.4% year on year. This decrease represents a further deceleration from its historical levels. We hope the business can get back on track.

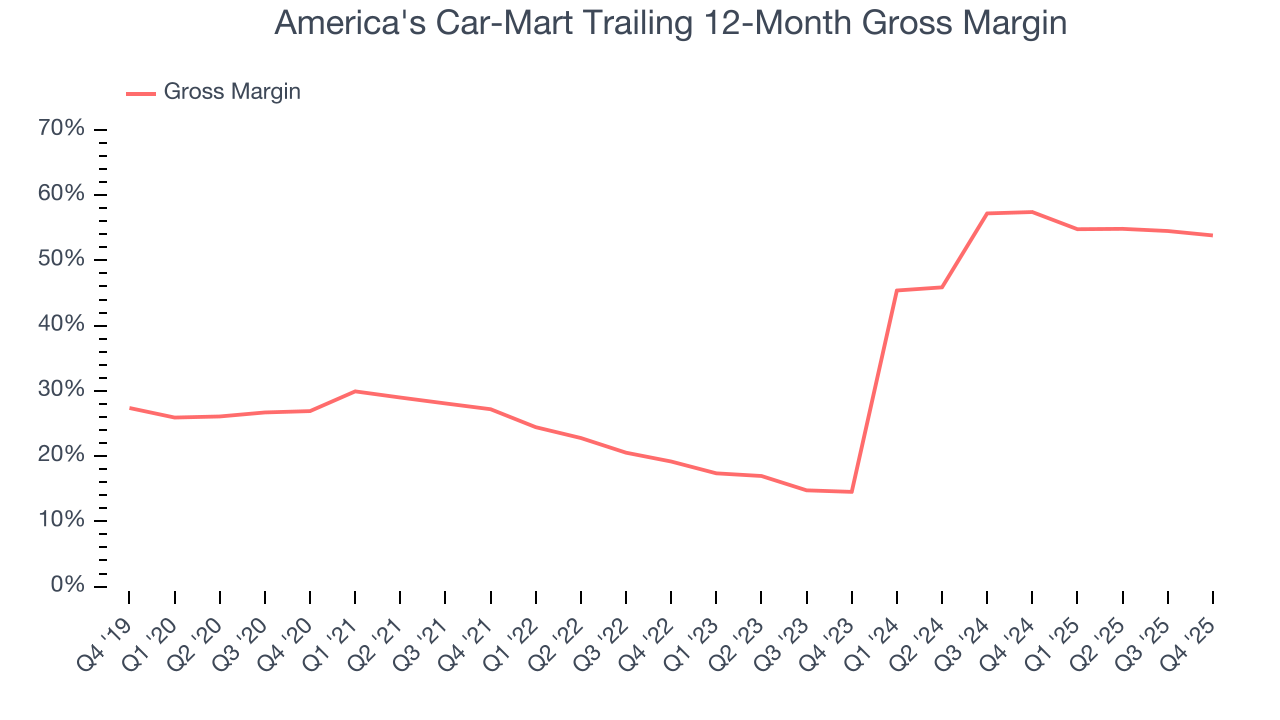

7. Gross Margin & Pricing Power

We prefer higher gross margins because they not only make it easier to generate more operating profits but also indicate product differentiation, negotiating leverage, and pricing power.

America's Car-Mart has best-in-class unit economics for a retailer, enabling it to invest in areas such as marketing and talent to grow its brand. As you can see below, it averaged an elite 55.6% gross margin over the last two years. That means America's Car-Mart only paid its suppliers $44.36 for every $100 in revenue.

America's Car-Mart produced a 13.5% gross profit margin in Q4 , marking a 7.6 percentage point decrease from 21.1% in the same quarter last year. America's Car-Mart’s full-year margin has also been trending down over the past 12 months, decreasing by 3.6 percentage points. If this move continues, it could suggest a more competitive environment with some pressure to discount products and higher input costs (such as labor and freight expenses to transport goods).

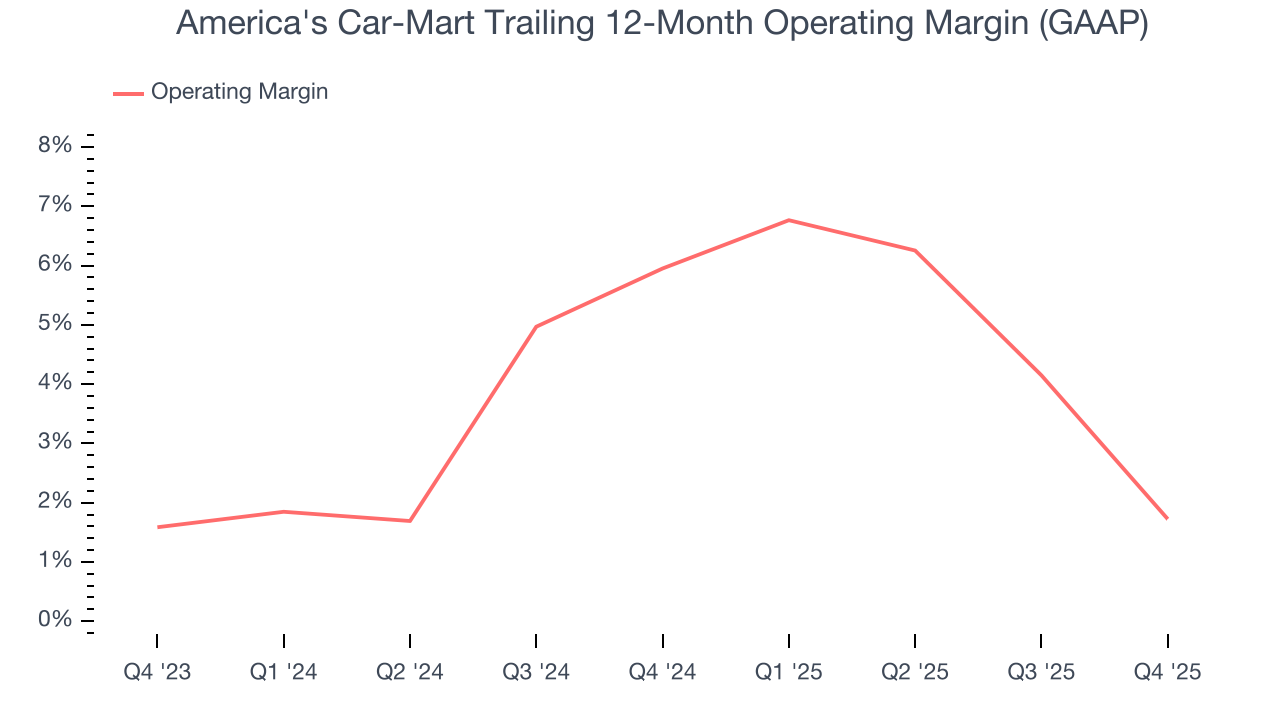

8. Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

America's Car-Mart was profitable over the last two years but held back by its large cost base. Its average operating margin of 3.9% was weak for a consumer retail business. This result is surprising given its high gross margin as a starting point.

Analyzing the trend in its profitability, America's Car-Mart’s operating margin decreased by 4.2 percentage points over the last year. America's Car-Mart’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers.

This quarter, America's Car-Mart generated an operating margin profit margin of negative 4.5%, down 11 percentage points year on year. Since America's Car-Mart’s operating margin decreased more than its gross margin, we can assume it was less efficient because expenses such as marketing, and administrative overhead increased.

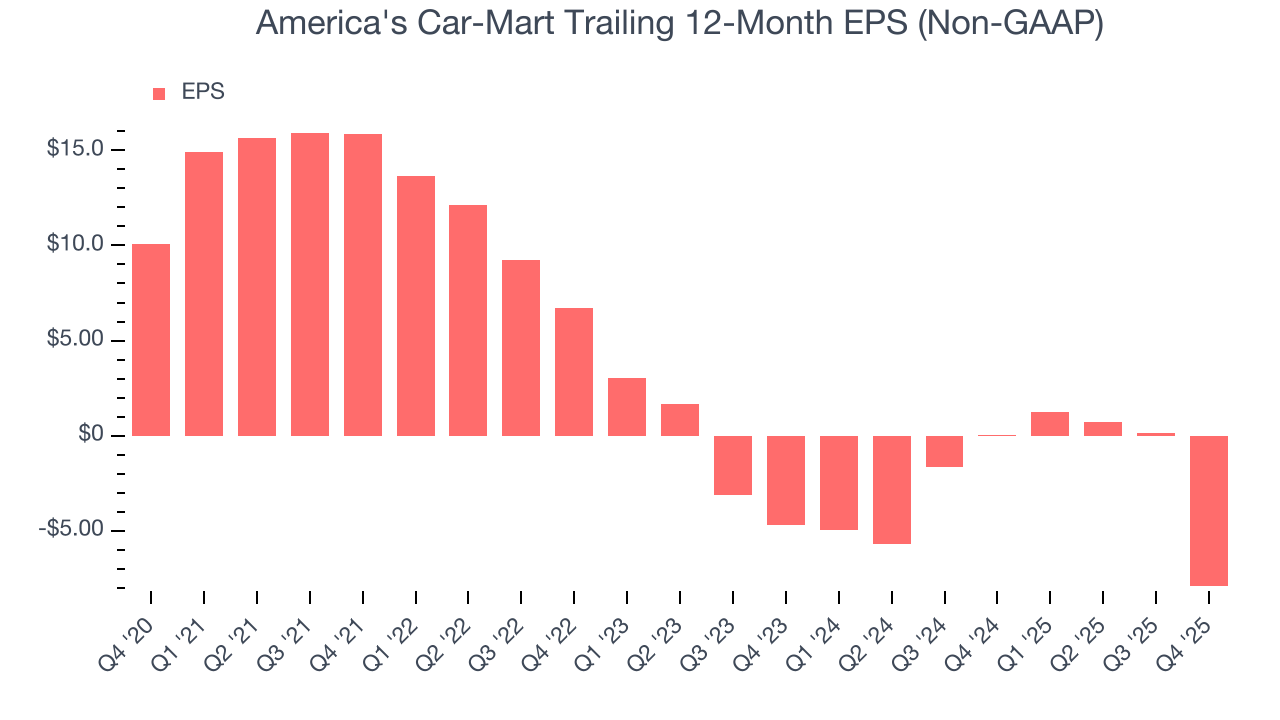

9. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Sadly for America's Car-Mart, its EPS declined by 47.1% annually over the last three years while its revenue was flat. This tells us the company struggled because its fixed cost base made it difficult to adjust to choppy demand.

In Q4, America's Car-Mart reported adjusted EPS of negative $7.72, down from $0.37 in the same quarter last year. This print missed analysts’ estimates. Over the next 12 months, Wall Street is optimistic. Analysts forecast America's Car-Mart’s full-year EPS of negative $7.94 will flip to positive $1.20.

10. Cash Is King

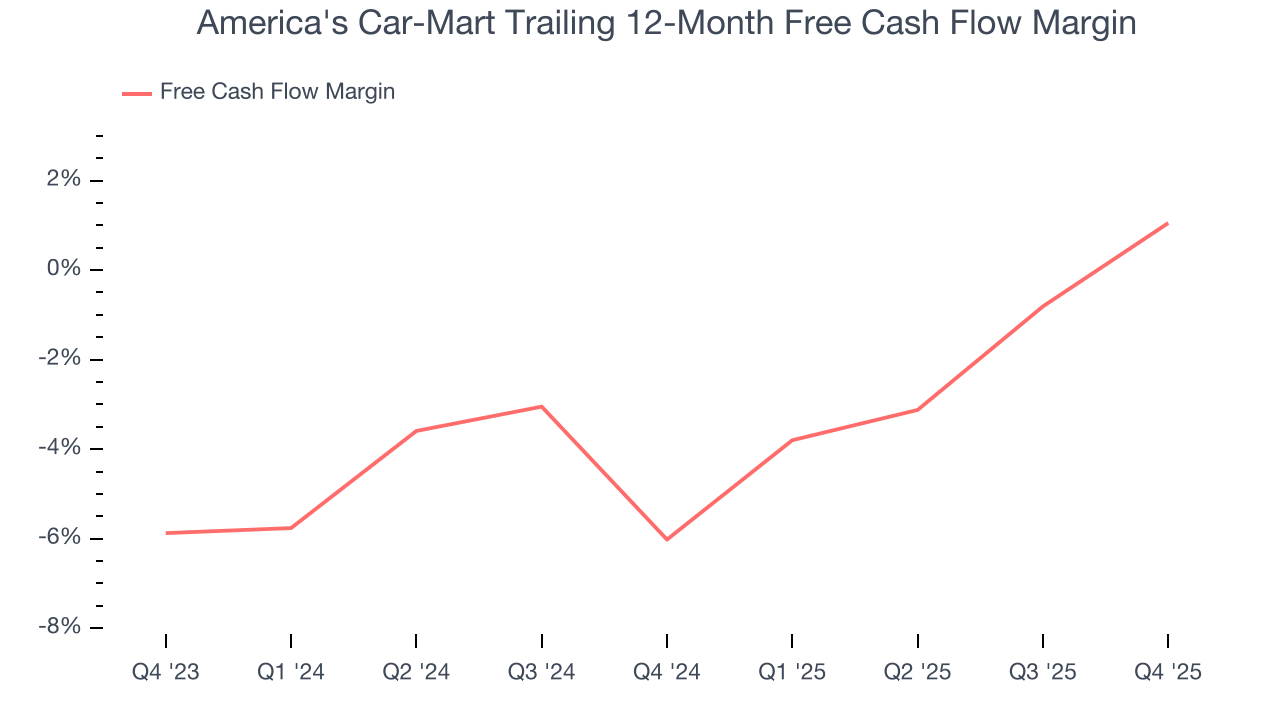

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

America's Car-Mart’s demanding reinvestments have consumed many resources over the last two years, contributing to an average free cash flow margin of negative 2.5%. This means it lit $2.53 of cash on fire for every $100 in revenue.

Taking a step back, an encouraging sign is that America's Car-Mart’s margin expanded by 7.1 percentage points over the last year. We have no doubt shareholders would like to continue seeing its cash conversion rise.

America's Car-Mart burned through $6.20 million of cash in Q4, equivalent to a negative 2.2% margin. The company’s cash burn slowed from $31.53 million of lost cash in the same quarter last year.

11. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

America's Car-Mart historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 6.2%, somewhat low compared to the best consumer retail companies that consistently pump out 25%+.

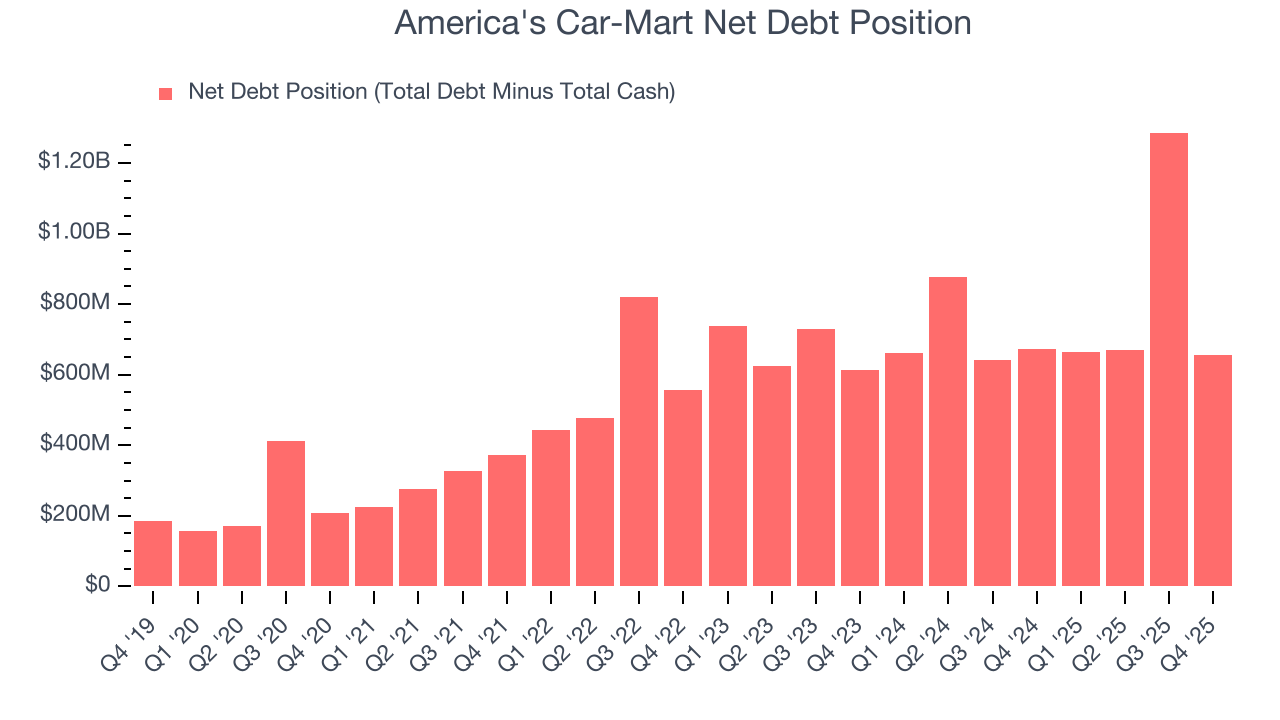

12. Balance Sheet Risk

Debt is a tool that can boost company returns but presents risks if used irresponsibly. As long-term investors, we aim to avoid companies taking excessive advantage of this instrument because it could lead to insolvency.

America's Car-Mart’s $892.2 million of debt exceeds the $237 million of cash on its balance sheet. Furthermore, its 23× net-debt-to-EBITDA ratio (based on its EBITDA of $28.56 million over the last 12 months) shows the company is overleveraged.

At this level of debt, incremental borrowing becomes increasingly expensive and credit agencies could downgrade the company’s rating if profitability falls. America's Car-Mart could also be backed into a corner if the market turns unexpectedly – a situation we seek to avoid as investors in high-quality companies.

We hope America's Car-Mart can improve its balance sheet and remain cautious until it increases its profitability or pays down its debt.

13. Key Takeaways from America's Car-Mart’s Q4 Results

We struggled to find many positives in these results. Its revenue missed and its EBITDA fell short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock traded down 6.9% to $17.74 immediately after reporting.

14. Is Now The Time To Buy America's Car-Mart?

Updated: March 16, 2026 at 10:36 PM EDT

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in America's Car-Mart.

America's Car-Mart falls short of our quality standards. For starters, its revenue has declined over the last three years, and analysts expect its demand to deteriorate over the next 12 months. While its gross margins are a strong starting point for the overall profitability of the business, the downside is its declining EPS over the last three years makes it a less attractive asset to the public markets. On top of that, its shrinking same-store sales tell us it will need to change its strategy to succeed.

America's Car-Mart’s EV-to-EBITDA ratio based on the next 12 months is 21.5x. This valuation tells us a lot of optimism is priced in - we think other companies feature superior fundamentals at the moment.

Wall Street analysts have a consensus one-year price target of $27.50 on the company (compared to the current share price of $12.75).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.