Lovesac (LOVE)

We wouldn’t buy Lovesac. Its weak sales growth and low returns on capital show it struggled to generate demand and profits.― StockStory Analyst Team

1. News

2. Summary

Why We Think Lovesac Will Underperform

Known for its oversized, premium beanbags, Lovesac (NASDAQ:LOVE) is a specialty furniture brand selling modular furniture.

- Lackluster 19.5% annual revenue growth over the last five years indicates the company is losing ground to competitors

- Subpar operating margin constrains its ability to invest in process improvements or effectively respond to new competitive threats

- Low free cash flow margin gives it little breathing room, constraining its ability to self-fund growth or return capital to shareholders

Lovesac fails to meet our quality criteria. More profitable opportunities exist elsewhere.

Why There Are Better Opportunities Than Lovesac

Lovesac’s stock price of $10.99 implies a valuation ratio of 9.2x forward EV-to-EBITDA. This valuation is fair for the quality you get, but we’re on the sidelines for now.

It’s better to pay up for high-quality businesses with strong long-term earnings potential rather than buy lower-quality stocks because they appear cheap. These challenged businesses often don’t re-rate, a phenomenon known as a “value trap”.

3. Lovesac (LOVE) Research Report: Q3 CY2025 Update

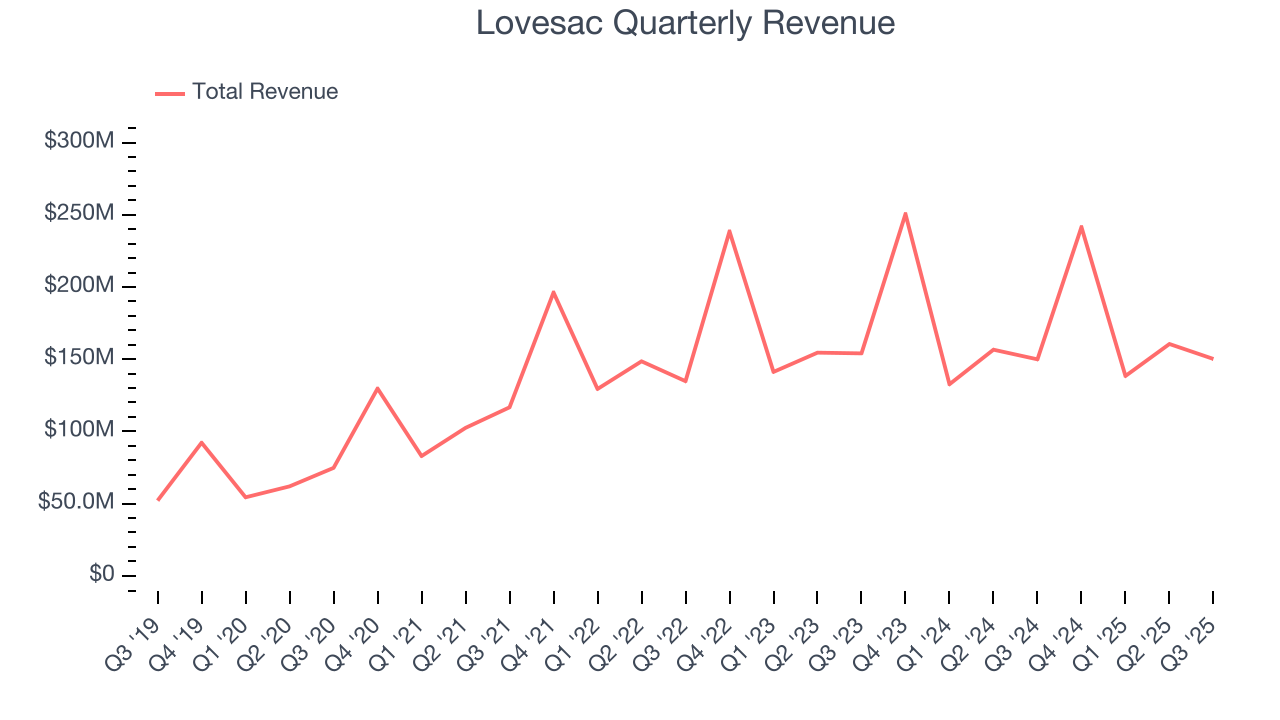

Furniture company Lovesac (NASDAQ:LOVE) fell short of the markets revenue expectations in Q3 CY2025, with sales flat year on year at $150.2 million. Next quarter’s revenue guidance of $246 million underwhelmed, coming in 5.7% below analysts’ estimates. Its GAAP loss of $0.72 per share was 4.6% below analysts’ consensus estimates.

Lovesac (LOVE) Q3 CY2025 Highlights:

- Revenue: $150.2 million vs analyst estimates of $154 million (flat year on year, 2.5% miss)

- EPS (GAAP): -$0.72 vs analyst expectations of -$0.69 (4.6% miss)

- Adjusted EBITDA: -$5.97 million (-4% margin, 323% year-on-year decline)

- Revenue Guidance for Q4 CY2025 is $246 million at the midpoint, below analyst estimates of $260.9 million

- EPS (GAAP) guidance for the full year is $0.32 at the midpoint, missing analyst estimates by 52.9%

- EBITDA guidance for the full year is $40 million at the midpoint, below analyst estimates of $44.6 million

- Operating Margin: -10.5%, down from -5.2% in the same quarter last year

- Free Cash Flow was -$10.18 million compared to -$6.59 million in the same quarter last year

- Market Capitalization: $200.7 million

Company Overview

Known for its oversized, premium beanbags, Lovesac (NASDAQ:LOVE) is a specialty furniture brand selling modular furniture.

The company started with its signature product, the "Lovesac", which is a large and durable beanbag chair. It has since expanded to offer a unique line of modular sectional couches known as Sactionals.

Lovesac's Sactionals are a distinctive product in the furniture market, offering adaptability and customization. These modular couches have sections that can be combined in various configurations to fit any room size or shape, making them a practical choice for diverse living spaces. The Sactionals' design is user-friendly, allowing for easy assembly, reconfiguration, and expansion.

Lovasac products are quite expensive: its beanbags can cost $800 and some Sactionals are upwards of $10,000. As such, the company's products appeal to customers who like experimenting with their furniture and are willing to pay up for home decor.

4. Home Furnishings

A healthy housing market is good for furniture demand as more consumers are buying, renting, moving, and renovating. On the other hand, periods of economic weakness or high interest rates discourage home sales and can squelch demand. In addition, home furnishing companies must contend with shifting consumer preferences such as the growing propensity to buy goods online, including big things like mattresses and sofas that were once thought to be immune from e-commerce competition.

Lovesac’s primary competitors include La-Z-Boy (NYSE:LZB), Wayfair (NYSE:W), West Elm (owned by Williams-Sonoma NYSE:WSM), and private companies IKEA and Ashley Furniture

5. Revenue Growth

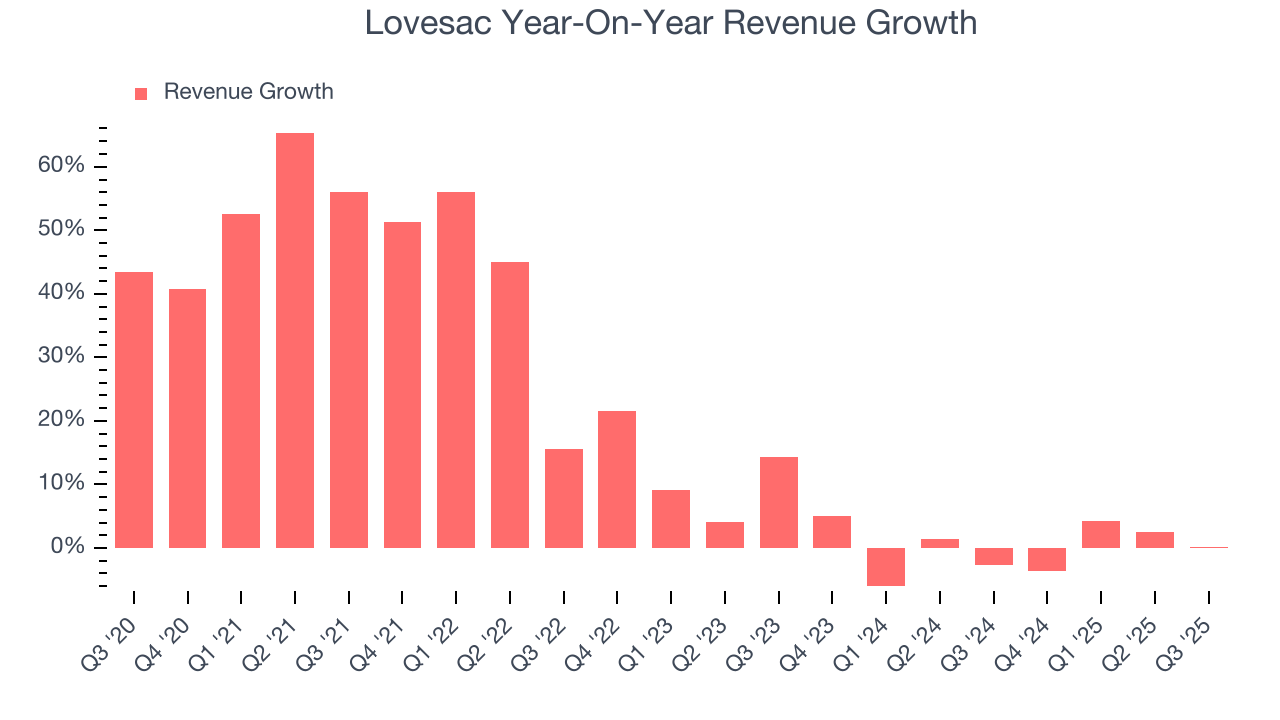

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Over the last five years, Lovesac grew its sales at a 19.5% annual rate. Although this growth is acceptable on an absolute basis, it fell slightly short of our standards for the consumer discretionary sector, which enjoys a number of secular tailwinds.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new product or trend. Lovesac’s recent performance shows its demand has slowed as its revenue was flat over the last two years.

This quarter, Lovesac’s $150.2 million of revenue was flat year on year, falling short of Wall Street’s estimates. Company management is currently guiding for a 1.9% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 7.7% over the next 12 months. While this projection indicates its newer products and services will spur better top-line performance, it is still below average for the sector.

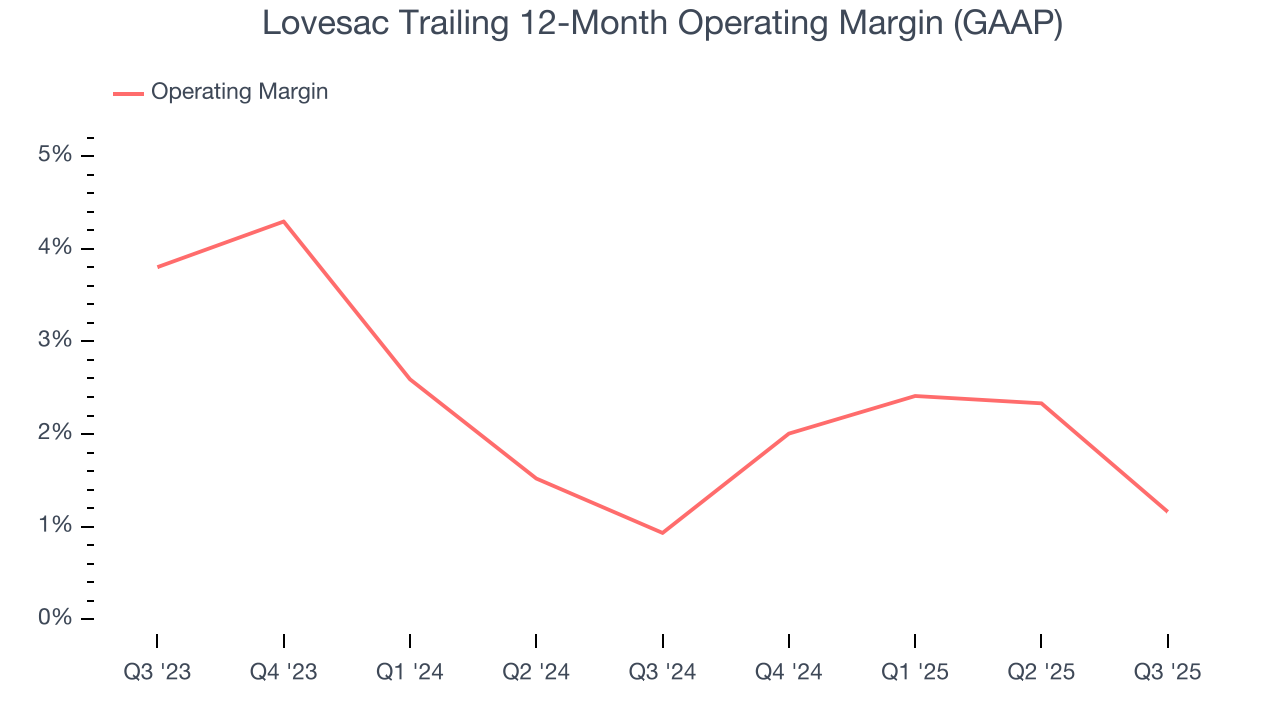

6. Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Lovesac’s operating margin might fluctuated slightly over the last 12 months but has generally stayed the same, averaging 1% over the last two years. This profitability was inadequate for a consumer discretionary business and caused by its suboptimal cost structure.

In Q3, Lovesac generated an operating margin profit margin of negative 10.5%, down 5.4 percentage points year on year. This contraction shows it was less efficient because its expenses increased relative to its revenue.

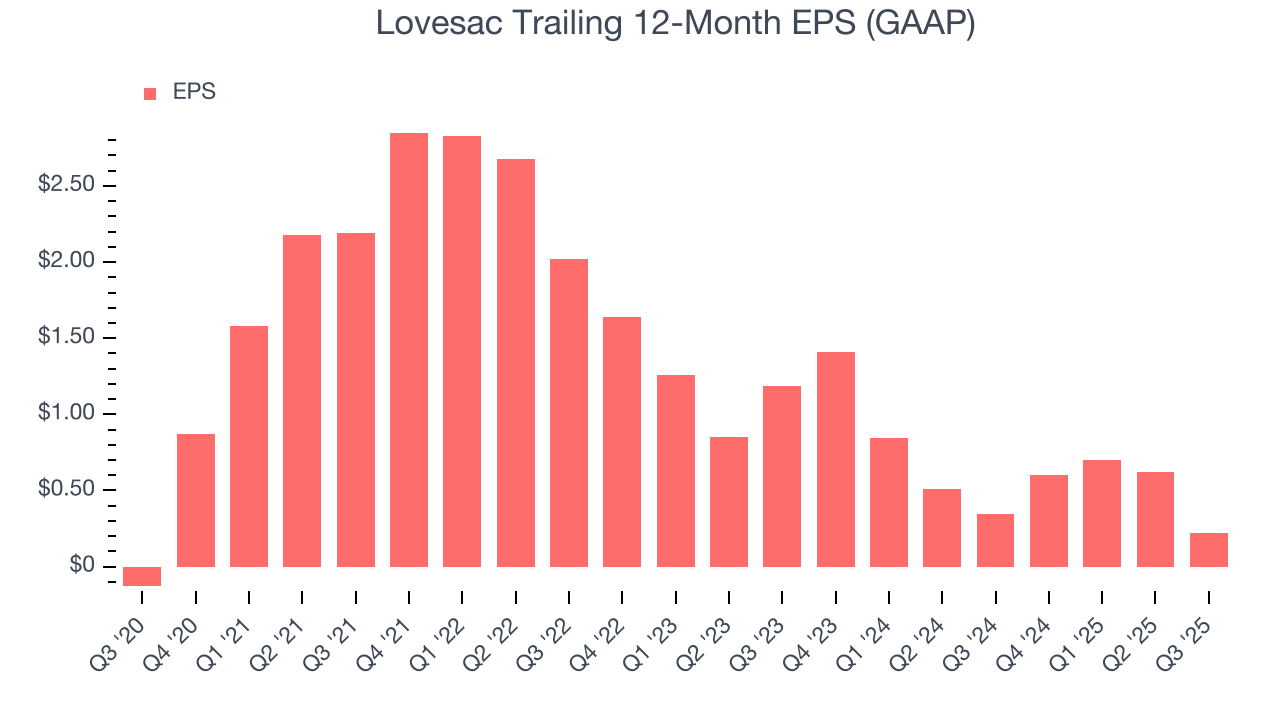

7. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Lovesac’s full-year EPS flipped from negative to positive over the last five years. This is encouraging and shows it’s at a critical moment in its life.

In Q3, Lovesac reported EPS of negative $0.72, down from negative $0.32 in the same quarter last year. This print missed analysts’ estimates. Over the next 12 months, Wall Street expects Lovesac’s full-year EPS of $0.22 to grow 6.2%.

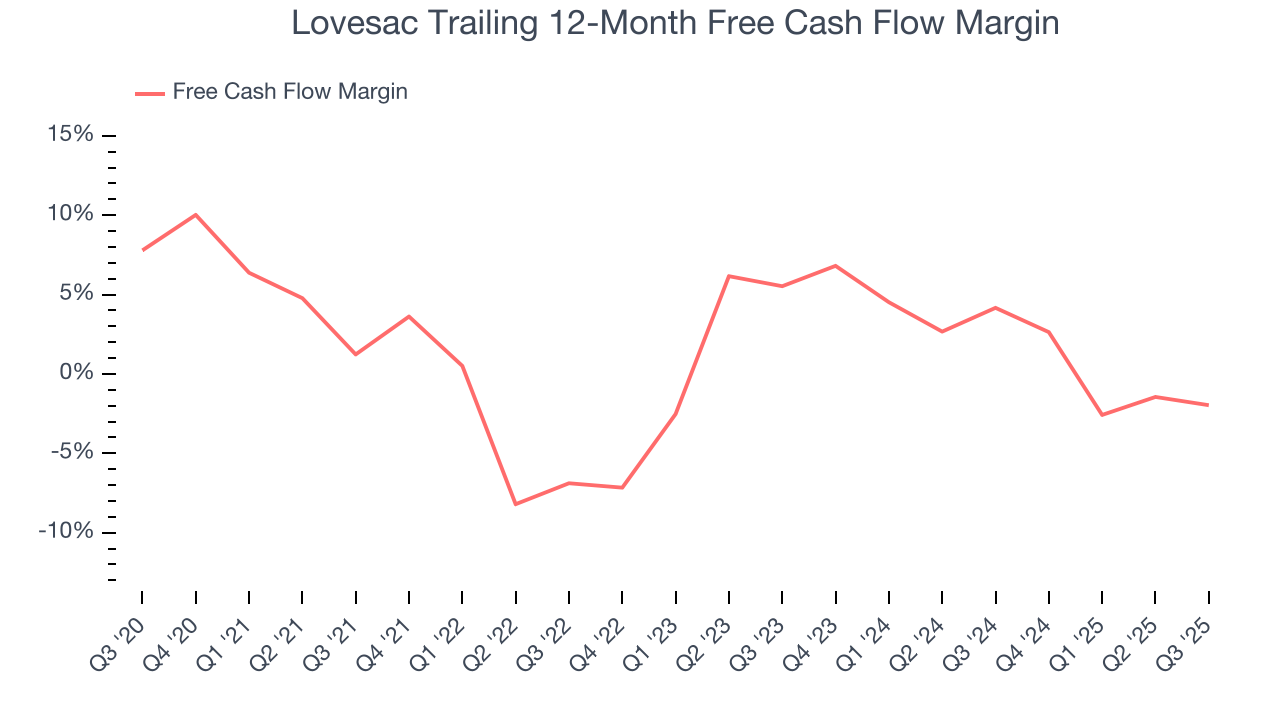

8. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Lovesac has shown poor cash profitability over the last two years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 1.1%, lousy for a consumer discretionary business.

Lovesac burned through $10.18 million of cash in Q3, equivalent to a negative 6.8% margin. The company’s cash burn was similar to its $6.59 million of lost cash in the same quarter last year. These numbers deviate from its longer-term margin, indicating it is a seasonal business that must build up inventory during certain quarters.

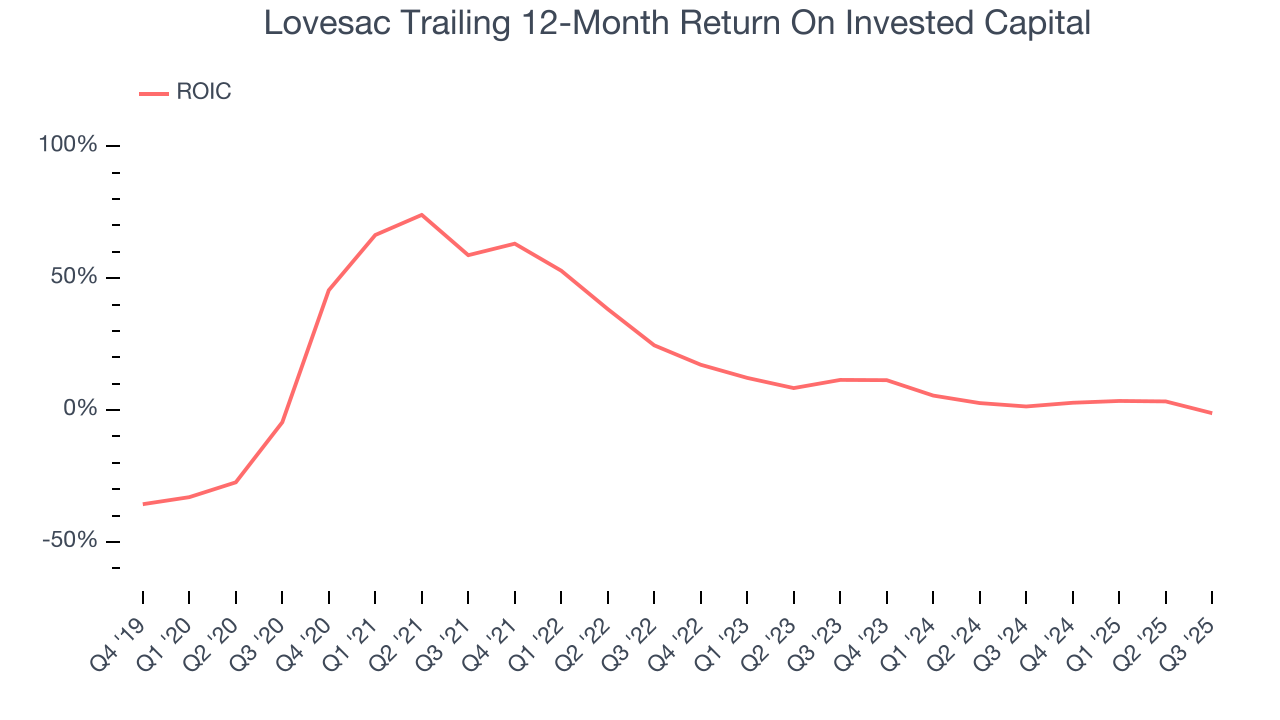

9. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Lovesac historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 19%, somewhat low compared to the best consumer discretionary companies that consistently pump out 25%+.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Unfortunately, Lovesac’s ROIC has decreased significantly over the last few years. Paired with its already low returns, these declines suggest its profitable growth opportunities are few and far between.

10. Balance Sheet Assessment

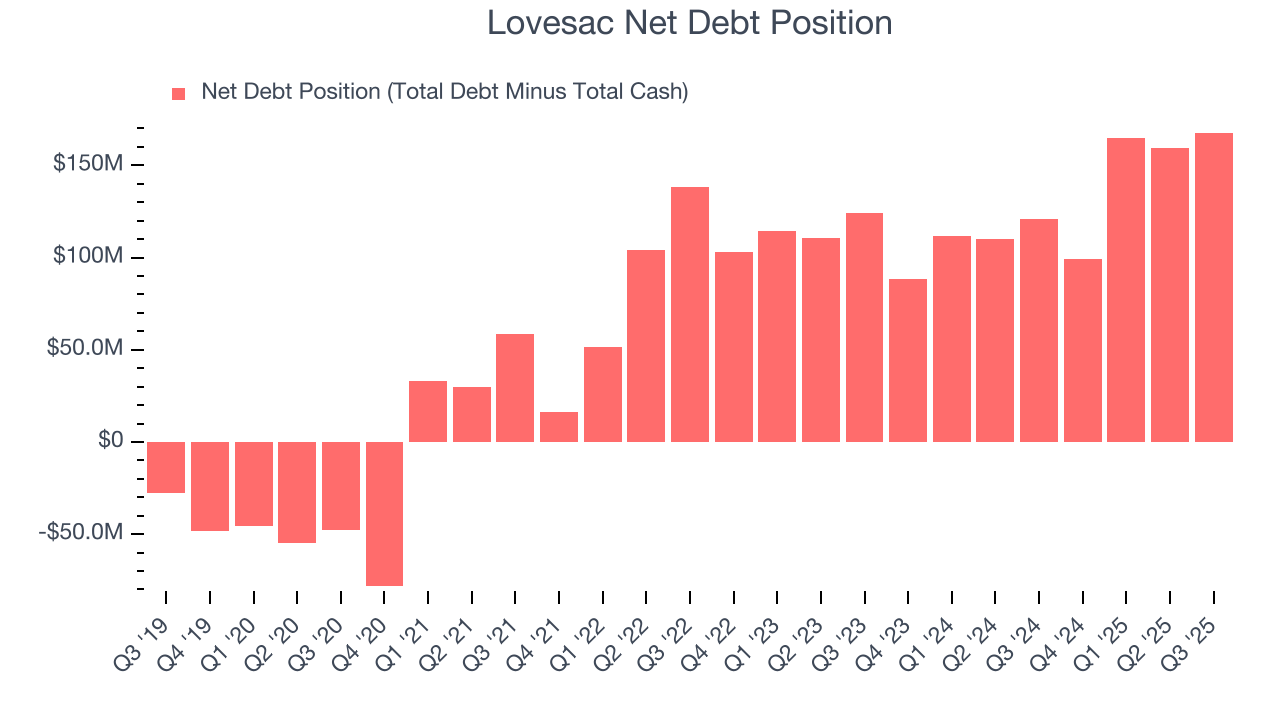

Lovesac reported $23.72 million of cash and $191.5 million of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $40.3 million of EBITDA over the last 12 months, we view Lovesac’s 4.2× net-debt-to-EBITDA ratio as safe. We also see its $1.3 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

11. Key Takeaways from Lovesac’s Q3 Results

We struggled to find many positives in these results. Its full-year EBITDA guidance missed and its full-year revenue guidance fell short of Wall Street’s estimates. Overall, this quarter could have been better. The stock traded down 6.4% to $12.86 immediately following the results.

12. Is Now The Time To Buy Lovesac?

Updated: March 16, 2026 at 10:08 PM EDT

We think that the latest earnings result is only one piece of the bigger puzzle. If you’re deciding whether to own Lovesac, you should also grasp the company’s longer-term business quality and valuation.

We cheer for all companies serving everyday consumers, but in the case of Lovesac, we’ll be cheering from the sidelines. On top of that, Lovesac’s projected EPS for the next year is lacking, and its relatively low ROIC suggests management has struggled to find compelling investment opportunities.

Lovesac’s EV-to-EBITDA ratio based on the next 12 months is 9.2x. This valuation multiple is fair, but we don’t have much confidence in the company. There are more exciting stocks to buy at the moment.

Wall Street analysts have a consensus one-year price target of $24.67 on the company (compared to the current share price of $10.99).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.