Mondelez (MDLZ)

We’re wary of Mondelez. Its underwhelming returns on capital show it struggled to generate meaningful profits for shareholders.― StockStory Analyst Team

1. News

2. Summary

Why We Think Mondelez Will Underperform

Founded as Nabisco in 1903, Mondelez (NASDAQ:MDLZ) is a packaged snacks powerhouse best known for its Oreo, Cadbury, Toblerone, Ritz, and Trident brands.

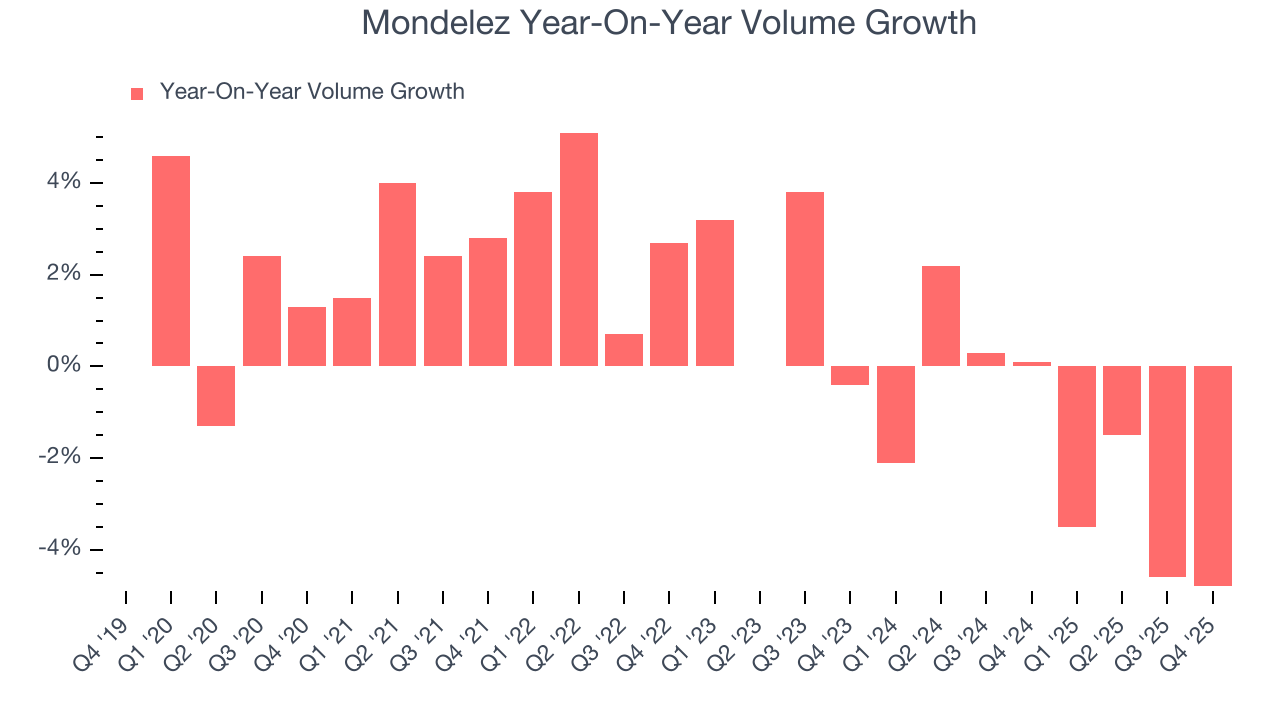

- Falling unit sales over the past two years imply it may need to invest in product improvements to get back on track

- Performance over the past three years shows its incremental sales were less profitable as its earnings per share were flat

- A silver lining is that its dominant market position is represented by its $38.54 billion in revenue, which gives it negotiating power with suppliers and retailers

Mondelez falls below our quality standards. Better stocks can be found in the market.

Why There Are Better Opportunities Than Mondelez

At $54.83 per share, Mondelez trades at 17.9x forward P/E. This multiple is quite expensive for the quality you get.

It’s better to pay up for high-quality businesses with strong long-term earnings potential rather than to buy lower-quality companies with open questions and big downside risks.

3. Mondelez (MDLZ) Research Report: Q4 CY2025 Update

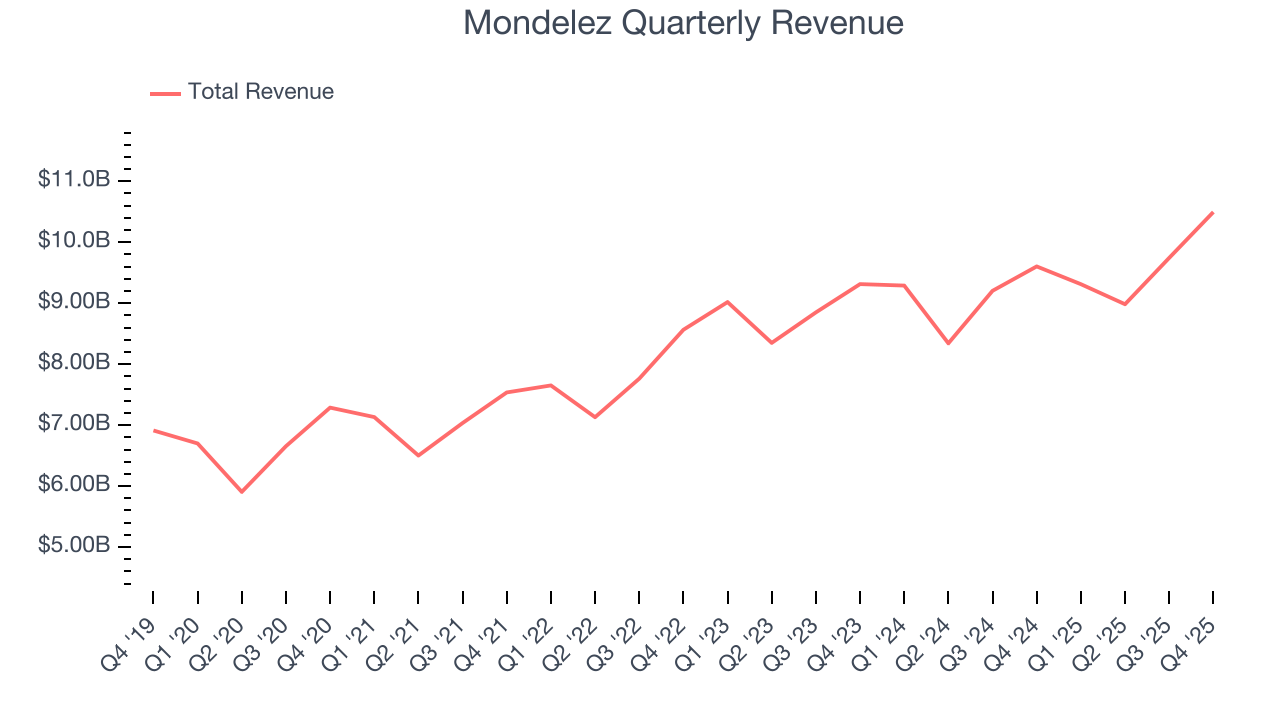

Packaged snacks company Mondelez (NASDAQ:MDLZ) beat Wall Street’s revenue expectations in Q4 CY2025, with sales up 9.3% year on year to $10.5 billion. Its non-GAAP profit of $0.68 per share was 2.4% below analysts’ consensus estimates.

Mondelez (MDLZ) Q4 CY2025 Highlights:

- Revenue: $10.5 billion vs analyst estimates of $10.31 billion (9.3% year-on-year growth, 1.8% beat)

- Adjusted EPS: $0.68 vs analyst expectations of $0.70 (2.4% miss)

- Adjusted EBITDA: $917 million vs analyst estimates of $1.66 billion (8.7% margin, 44.6% miss)

- Operating Margin: 9.1%, down from 16.8% in the same quarter last year

- Free Cash Flow Margin: 19%, up from 11% in the same quarter last year

- Organic Revenue rose 5.1% year on year (beat)

- Sales Volumes fell 4.8% year on year (0.1% in the same quarter last year)

- Market Capitalization: $75.73 billion

Company Overview

Founded as Nabisco in 1903, Mondelez (NASDAQ:MDLZ) is a packaged snacks powerhouse best known for its Oreo, Cadbury, Toblerone, Ritz, and Trident brands.

Although its product portfolio is vast, diverse, and international today, Mondelez traces its roots back to the merger of several small bakeries and cracker manufacturers to form Nabisco (The National Biscuit Company). From there, the company launched the Uneeda Biscuit, which was the first packaged biscuit to be sold nationwide, and in 1921, the Oreo cookie was introduced. In the ensuing decades, Nabisco was owned by a tobacco company, a private equity firm, and Kraft. Present-day Mondelez is the result of a major restructuring of Kraft in 2012.

Today, Modelez produces packaged foods in the snacks, confectionery/candy, and beverages categories. Because of its breadth of brands and products, Mondelez's products cater to a wide variety of consumer preferences and dietary needs–the company sells everything from gluten-free snacks to decadent candies. Almost anyone is a Mondelez potential core customer.

Because of its long-standing, well-known brands, Mondelez's products can be found in a wide variety of stores and retailers worldwide. Global supermarkets, grocery stores, convenience stores, mass merchandisers, and online retailers sell the company’s products, which means consumers are never far from a shelf carrying a Mondelez offering.

4. Shelf-Stable Food

As America industrialized and moved away from an agricultural economy, people faced more demands on their time. Packaged foods emerged as a solution offering convenience to the evolving American family, whether it be canned goods or snacks. Today, Americans seek brands that are high in quality, reliable, and reasonably priced. Furthermore, there's a growing emphasis on health-conscious and sustainable food options. Packaged food stocks are considered resilient investments. People always need to eat, so these companies can enjoy consistent demand as long as they stay on top of changing consumer preferences. The industry spans from multinational corporations to smaller specialized firms and is subject to food safety and labeling regulations.

Competitors in the packaged snacks and confectionary space include PepsiCo (NASDAQ:PEP), Nestle (SWX:NESN), Hershey (NYSE:HSY), and Kraft Heinz (NASDAQ:KHC).

5. Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can have short-term success, but a top-tier one grows for years.

With $38.54 billion in revenue over the past 12 months, Mondelez is one of the most widely recognized consumer staples companies. Its influence over consumers gives it negotiating leverage with distributors, enabling it to pick and choose where it sells its products (a luxury many don’t have).

As you can see below, Mondelez grew its sales at a decent 7.4% compounded annual growth rate over the last three years despite consumers buying less of its products. We’ll explore what this means in the "Volume Growth" section.

This quarter, Mondelez reported year-on-year revenue growth of 9.3%, and its $10.5 billion of revenue exceeded Wall Street’s estimates by 1.8%.

Looking ahead, sell-side analysts expect revenue to grow 3.2% over the next 12 months, a deceleration versus the last three years. This projection doesn't excite us and indicates its products will see some demand headwinds.

6. Volume Growth

Revenue growth can be broken down into changes in price and volume (the number of units sold). While both are important, volume is the lifeblood of a successful staples business as there’s a ceiling to what consumers will pay for everyday goods; they can always trade down to non-branded products if the branded versions are too expensive.

To analyze whether Mondelez generated its growth from changes in price or volume, we can compare its volume growth to its organic revenue growth, which excludes non-fundamental impacts on company financials like mergers and currency fluctuations.

Over the last two years, Mondelez’s average quarterly sales volumes have shrunk by 1.7%. This decrease isn’t ideal as the quantity demanded for consumer staples products is typically stable. Luckily, Mondelez was able to offset fewer customers purchasing its products by charging higher prices, enabling it to generate 4.3% average organic revenue growth. We hope the company can grow its volumes soon, however, as consistent price increases (on top of inflation) aren’t sustainable over the long term unless the business is really really special.

In Mondelez’s Q4 2025, sales volumes dropped 4.8% year on year. This result represents a further deceleration from its historical levels, showing the business is struggling to move its products.

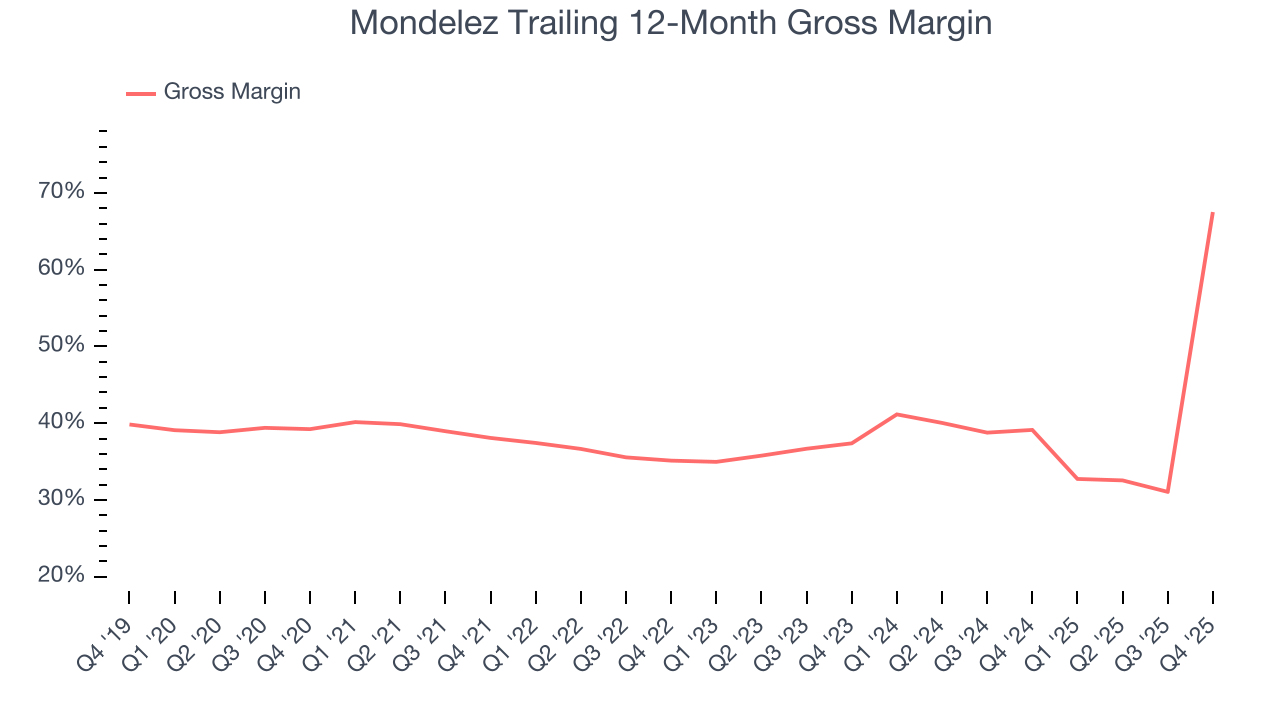

7. Gross Margin & Pricing Power

At StockStory, we prefer high gross margin businesses because they indicate pricing power or differentiated products, giving the company a chance to generate higher operating profits.

Mondelez has great unit economics for a consumer staples company, giving it ample room to invest in areas such as marketing and talent to grow its brand. As you can see below, it averaged an excellent 53.7% gross margin over the last two years. That means for every $100 in revenue, only $46.29 went towards paying for raw materials, production of goods, transportation, and distribution.

This quarter, Mondelez’s gross profit margin was 172%, marking a 133.2 percentage point increase from 38.6% in the same quarter last year. Mondelez’s full-year margin has also been trending up over the past 12 months, increasing by 28.4 percentage points. If this move continues, it could suggest a less competitive environment where the company has better pricing power and leverage from its growing sales on the fixed portion of its cost of goods sold (such as manufacturing expenses).

8. Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Mondelez has managed its cost base well over the last two years. It demonstrated solid profitability for a consumer staples business, producing an average operating margin of 13.2%. This result isn’t surprising as its high gross margin gives it a favorable starting point.

Looking at the trend in its profitability, Mondelez’s operating margin decreased by 8.2 percentage points over the last year. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

In Q4, Mondelez generated an operating margin profit margin of 9.1%, down 7.7 percentage points year on year. Conversely, its revenue and gross margin actually rose, so we can assume it was less efficient because its operating expenses like marketing, and administrative overhead grew faster than its revenue.

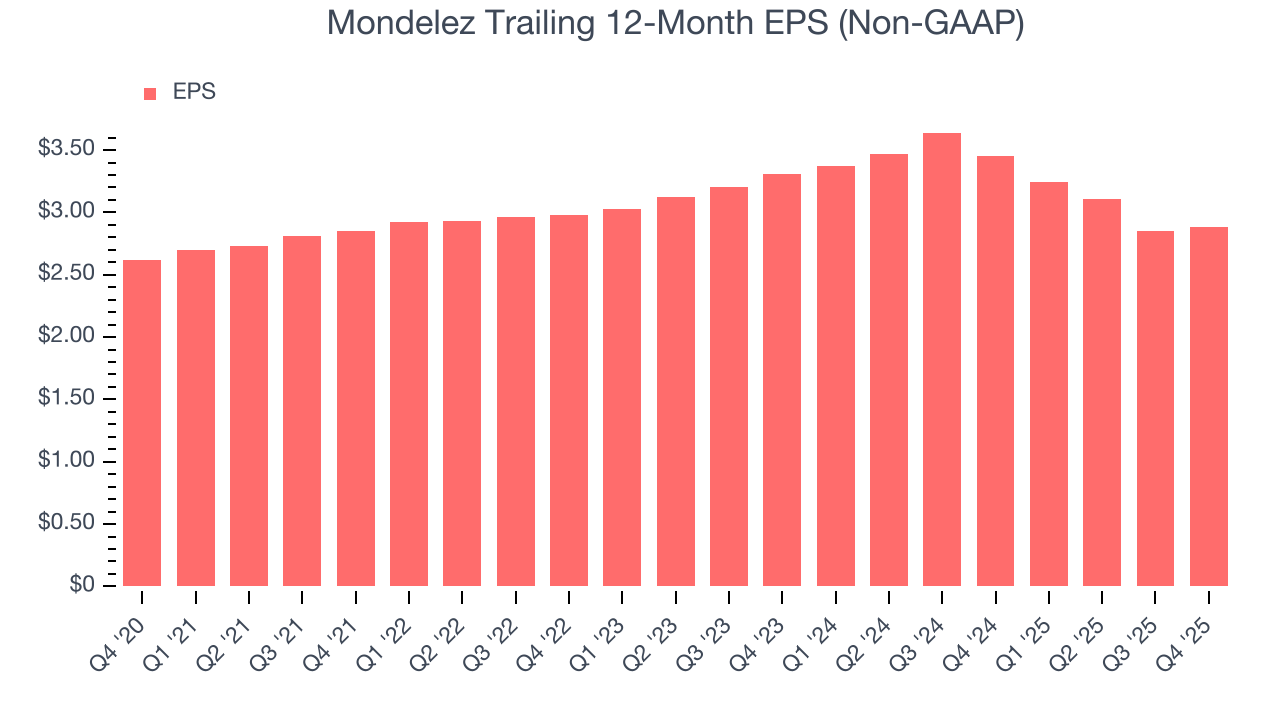

9. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Sadly for Mondelez, its EPS declined by 1.1% annually over the last three years while its revenue grew by 7.4%. However, its operating margin didn’t change during this time, telling us that non-fundamental factors such as interest and taxes affected its ultimate earnings.

In Q4, Mondelez reported adjusted EPS of $0.68, up from $0.65 in the same quarter last year. Despite growing year on year, this print missed analysts’ estimates. Over the next 12 months, Wall Street expects Mondelez’s full-year EPS of $2.88 to grow 8.5%.

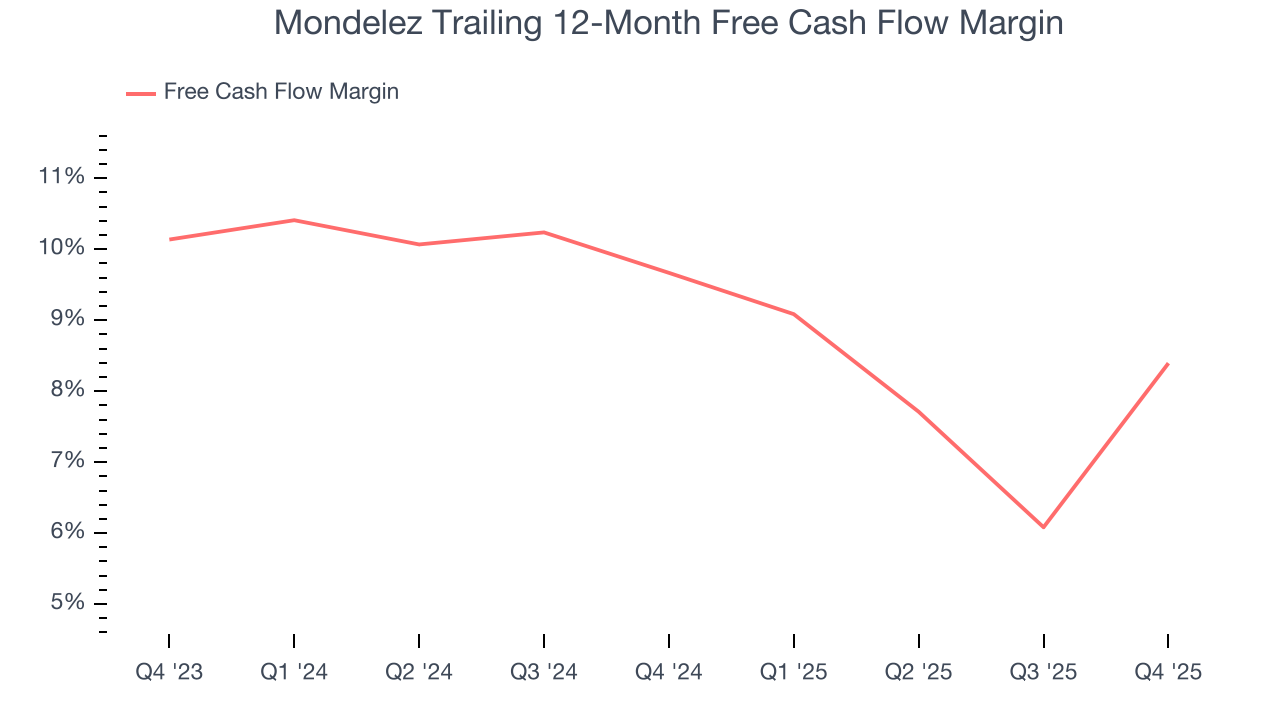

10. Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Mondelez has shown robust cash profitability, driven by its attractive business model that enables it to reinvest or return capital to investors. The company’s free cash flow margin averaged 9% over the last two years, quite impressive for a consumer staples business.

Taking a step back, we can see that Mondelez’s margin dropped by 1.3 percentage points over the last year. Continued declines could signal it is in the middle of an investment cycle.

Mondelez’s free cash flow clocked in at $2.00 billion in Q4, equivalent to a 19% margin. This result was good as its margin was 8.1 percentage points higher than in the same quarter last year, but we wouldn’t read too much into the short term because investment needs can be seasonal, causing temporary swings. Long-term trends trump fluctuations.

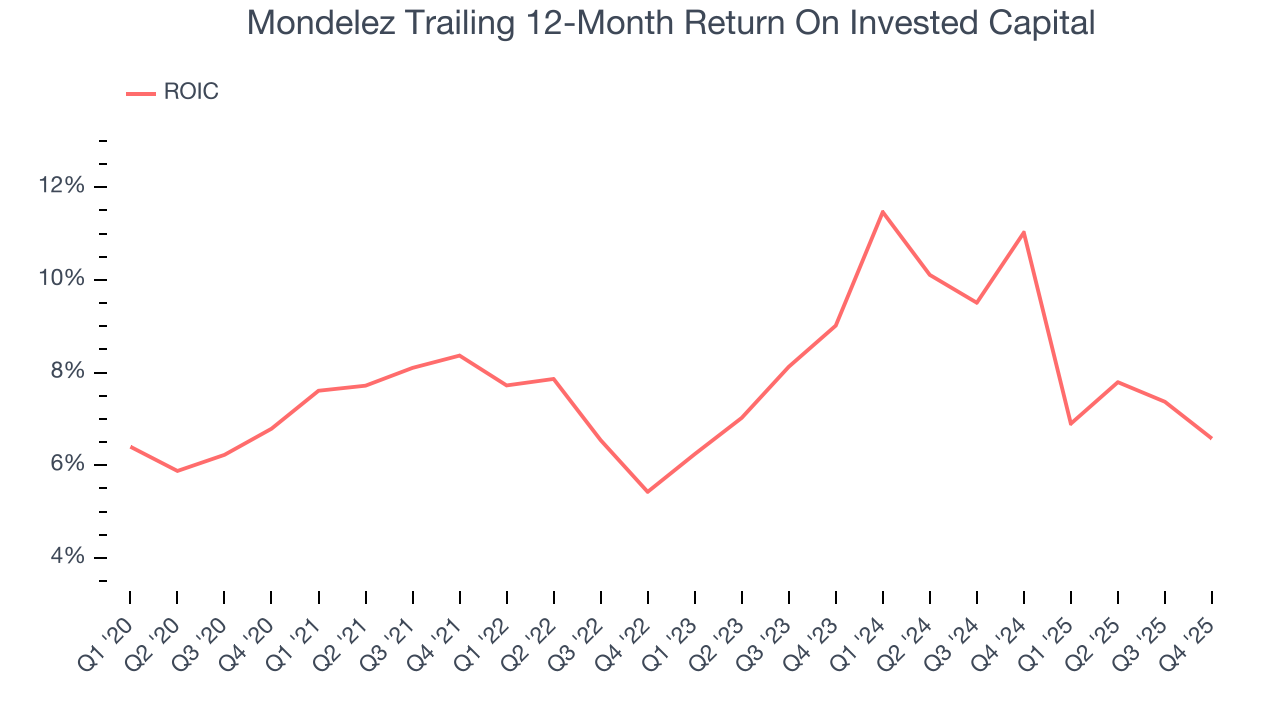

11. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Mondelez historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 8.1%, somewhat low compared to the best consumer staples companies that consistently pump out 20%+.

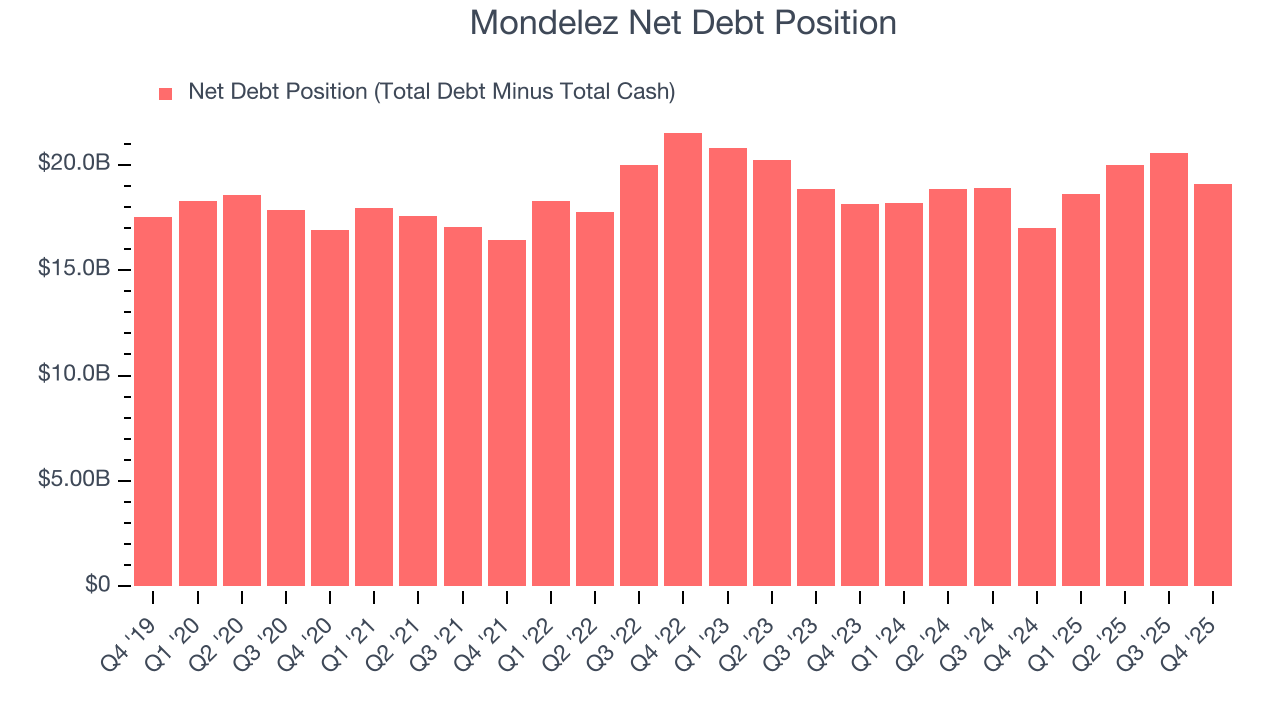

12. Balance Sheet Assessment

Mondelez reported $2.13 billion of cash and $21.21 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $5.75 billion of EBITDA over the last 12 months, we view Mondelez’s 3.3× net-debt-to-EBITDA ratio as safe. We also see its $492 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

13. Key Takeaways from Mondelez’s Q4 Results

We were impressed by how significantly Mondelez blew past analysts’ gross margin expectations this quarter. We were also happy its revenue outperformed Wall Street’s estimates. On the other hand, its EBITDA missed and its EPS fell short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock traded down 2.6% to $57.98 immediately after reporting.

14. Is Now The Time To Buy Mondelez?

Updated: March 14, 2026 at 10:51 PM EDT

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in Mondelez.

Mondelez’s business quality ultimately falls short of our standards. Although its revenue growth was decent over the last three years, it’s expected to deteriorate over the next 12 months and its declining operating margin shows the business has become less efficient. And while the company’s unparalleled brand awareness makes it a household name consumers consistently turn to, the downside is its shrinking sales volumes suggest it’ll need to change its strategy to succeed.

Mondelez’s P/E ratio based on the next 12 months is 17.9x. Beauty is in the eye of the beholder, but our analysis shows the upside isn’t great compared to the potential downside. We're pretty confident there are superior stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $66.96 on the company (compared to the current share price of $54.83).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.