Boyd Gaming (BYD)

We wouldn’t buy Boyd Gaming. Its weak sales growth and low returns on capital show it struggled to generate demand and profits.― StockStory Analyst Team

1. News

2. Summary

Why We Think Boyd Gaming Will Underperform

Run by the Boyd family, Boyd Gaming (NYSE:BYD) is a diversified operator of gaming entertainment properties across the United States, offering casino games, hotel accommodations, and dining.

- Lackluster 11.4% annual revenue growth over the last five years indicates the company is losing ground to competitors

- Demand will likely fall over the next 12 months as Wall Street expects flat revenue

- Ability to fund investments or reward shareholders with increased buybacks or dividends is restricted by its weak free cash flow margin of 11.9% for the last two years

Boyd Gaming doesn’t meet our quality criteria. There are more appealing investments to be made.

Why There Are Better Opportunities Than Boyd Gaming

Boyd Gaming is trading at $83.77 per share, or 11.1x forward P/E. Boyd Gaming’s multiple may seem like a great deal among consumer discretionary peers, but we think there are valid reasons why it’s this cheap.

Cheap stocks can look like a great deal at first glance, but they can be value traps. They often have less earnings power, meaning there is more reliance on a re-rating to generate good returns - an unlikely scenario for low-quality companies.

3. Boyd Gaming (BYD) Research Report: Q3 CY2025 Update

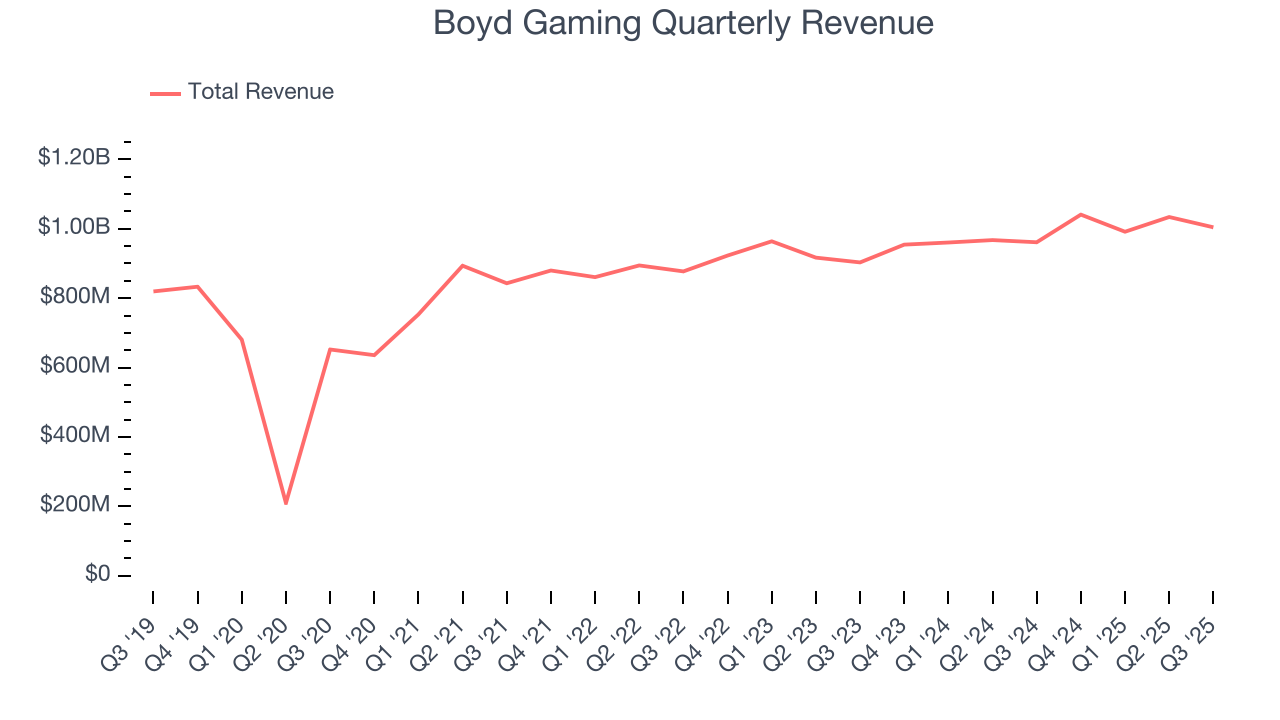

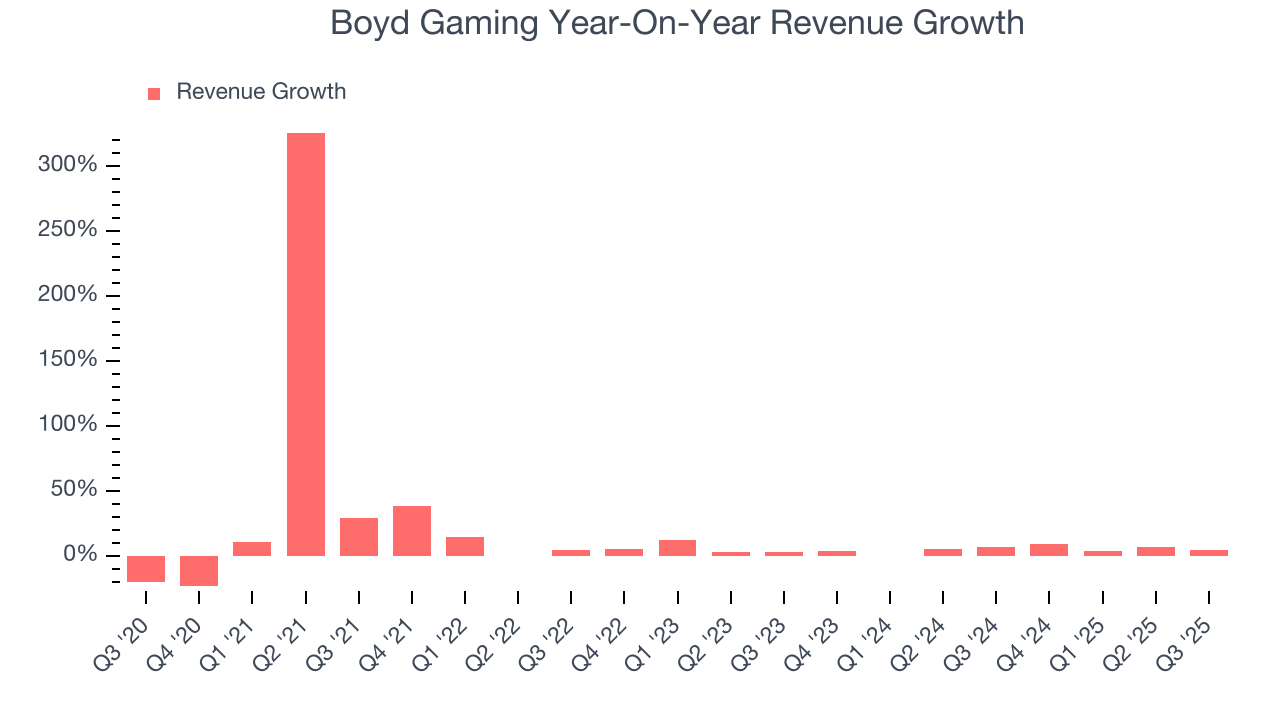

Gaming and hospitality company Boyd Gaming (NYSE:BYD) reported revenue ahead of Wall Street’s expectations in Q3 CY2025, with sales up 4.5% year on year to $1.00 billion. Its non-GAAP profit of $1.72 per share was 5.8% above analysts’ consensus estimates.

Boyd Gaming (BYD) Q3 CY2025 Highlights:

- Revenue: $1.00 billion vs analyst estimates of $867.8 million (4.5% year-on-year growth, 15.7% beat)

- Adjusted EPS: $1.72 vs analyst estimates of $1.63 (5.8% beat)

- Adjusted EBITDA: $293.2 million vs analyst estimates of $280.6 million (29.2% margin, 4.5% beat)

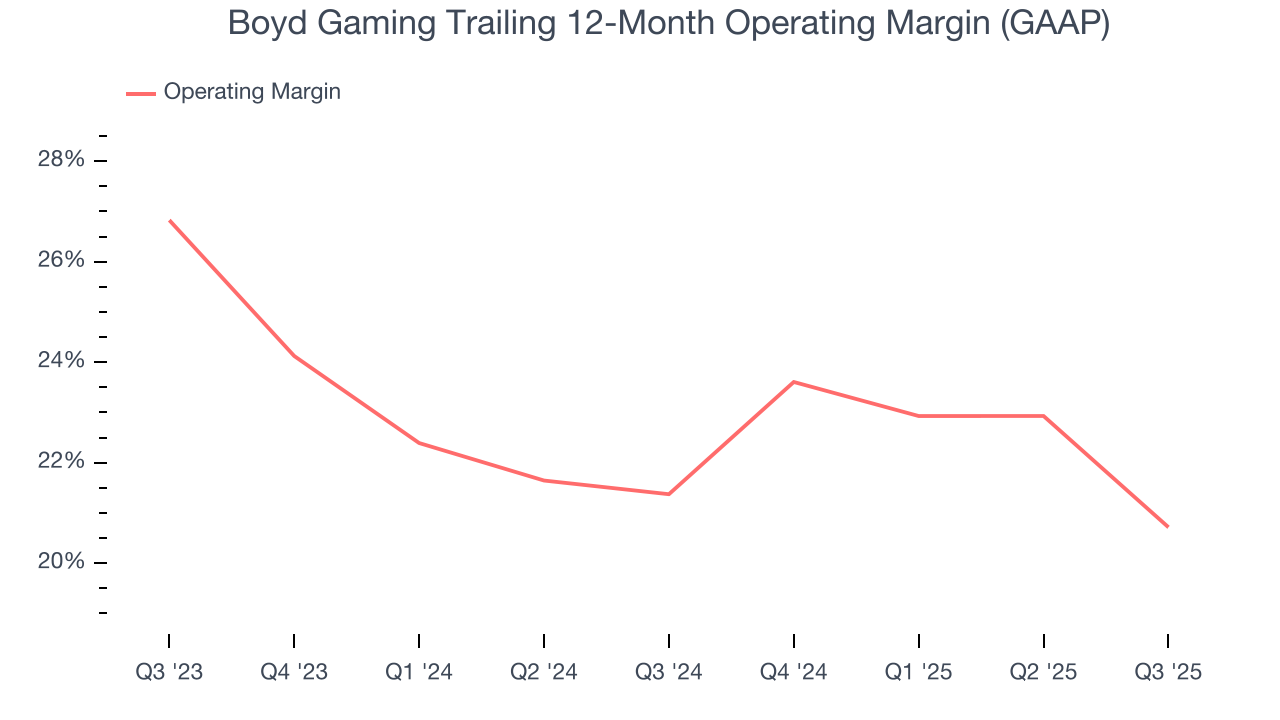

- Operating Margin: 13.9%, down from 22.9% in the same quarter last year

- Market Capitalization: $6.65 billion

Company Overview

Run by the Boyd family, Boyd Gaming (NYSE:BYD) is a diversified operator of gaming entertainment properties across the United States, offering casino games, hotel accommodations, and dining.

Boyd Gaming was established in 1975 by Sam Boyd, a former casino dealer with extensive experience in the gaming industry. Today, Boyd Gaming operates a diverse portfolio of properties across various states that allow its guests to gamble.

The company's offerings include not only casino games but also hotel accommodations, dining options, and recreational activities. This holistic approach caters to a broad audience, from gaming enthusiasts to families seeking a complete entertainment experience. Boyd Gaming's properties often feature amenities like pools, spas, shopping centers, and convention spaces.

The primary revenue streams for Boyd Gaming come from its casino operations, hotel services, food and beverage sales, and entertainment offerings. Despite being based in Paradise, Nevada, the company is geographically diversified, allowing it to appeal to both local customers and tourists.

4. Casino Operator

Casino operators enjoy limited competition because gambling is a highly regulated industry. These companies can also enjoy healthy margins and profits. Have you ever heard the phrase ‘the house always wins’? Regulation cuts both ways, however, and casinos may face stroke-of-the-pen risk that suddenly limits what they can or can't do and where they can do it. Furthermore, digitization is changing the game, pun intended. Whether it’s online poker or sports betting on your smartphone, innovation is forcing these players to adapt to changing consumer preferences, such as being able to wager anywhere on demand.

Competitors in the gaming sector include Caesars Entertainment (NASDAQ:CZR), MGM Resorts (NYSE:MGM), and PENN Entertainment (NASDAQ:PENN).

5. Revenue Growth

A company’s long-term sales performance can indicate its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Over the last five years, Boyd Gaming grew its sales at a 11.4% compounded annual growth rate. Although this growth is acceptable on an absolute basis, it fell short of our standards for the consumer discretionary sector, which enjoys a number of secular tailwinds.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new product or trend. Boyd Gaming’s recent performance shows its demand has slowed as its annualized revenue growth of 4.8% over the last two years was below its five-year trend. Note that COVID hurt Boyd Gaming’s business in 2020 and part of 2021, and it bounced back in a big way thereafter.

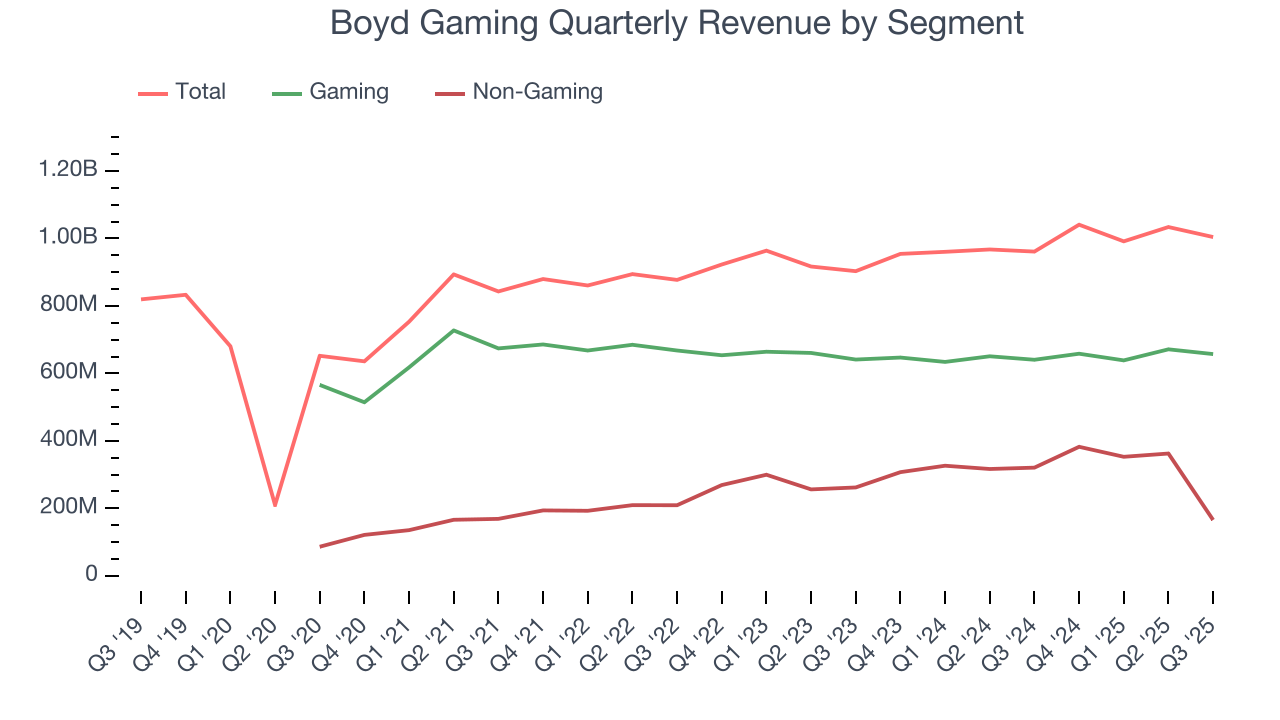

We can better understand the company’s revenue dynamics by analyzing its most important segments, Gaming and Non-Gaming, which are 65.5% and 16.5% of revenue. Over the last two years, Boyd Gaming’s Gaming revenue (casino games) was flat while its Non-Gaming revenue (hotel, food, beverage) averaged 8.5% year-on-year growth.

This quarter, Boyd Gaming reported modest year-on-year revenue growth of 4.5% but beat Wall Street’s estimates by 15.7%.

Looking ahead, sell-side analysts expect revenue to decline by 12.6% over the next 12 months, a deceleration versus the last two years. This projection doesn't excite us and indicates its products and services will see some demand headwinds.

6. Operating Margin

Boyd Gaming’s operating margin might fluctuated slightly over the last 12 months but has generally stayed the same, averaging 21% over the last two years. This profitability was top-notch for a consumer discretionary business, showing it’s an well-run company with an efficient cost structure.

In Q3, Boyd Gaming generated an operating margin profit margin of 13.9%, down 9 percentage points year on year. This contraction shows it was less efficient because its expenses grew faster than its revenue.

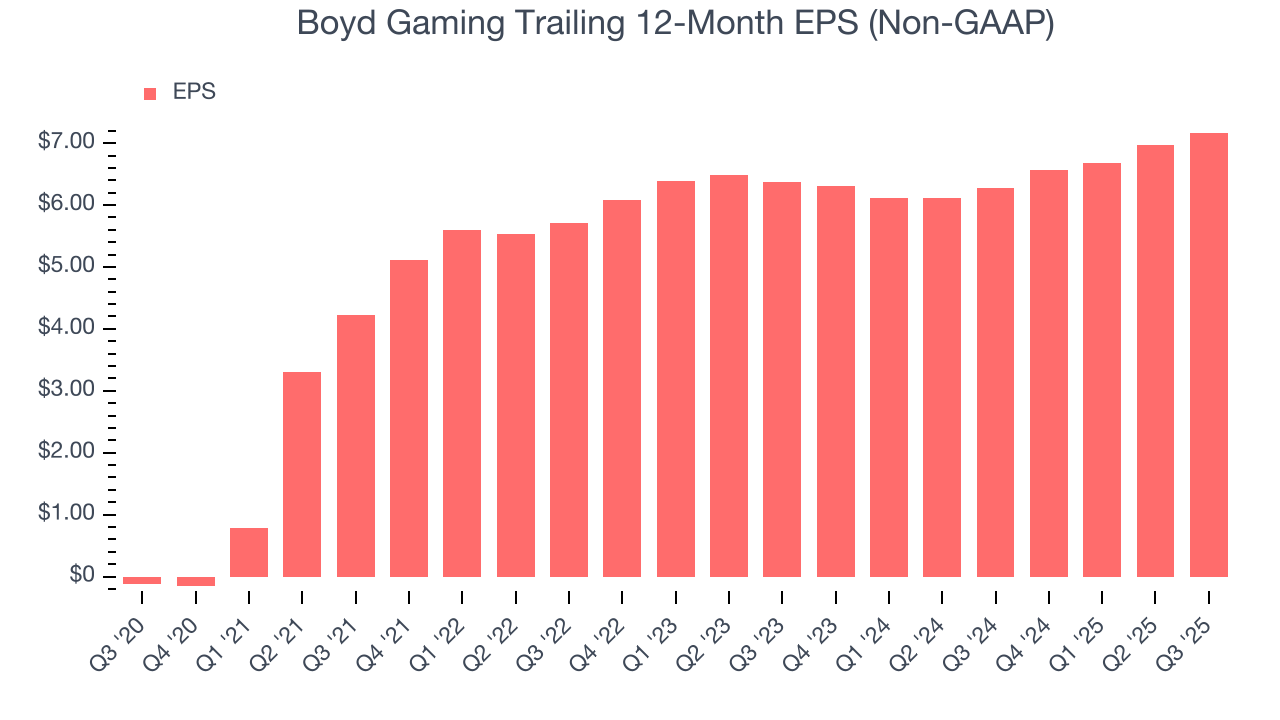

7. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Boyd Gaming’s full-year EPS flipped from negative to positive over the last five years. This is encouraging and shows it’s at a critical moment in its life.

In Q3, Boyd Gaming reported adjusted EPS of $1.72, up from $1.52 in the same quarter last year. This print beat analysts’ estimates by 5.8%. Over the next 12 months, Wall Street expects Boyd Gaming’s full-year EPS of $7.17 to grow 9.1%.

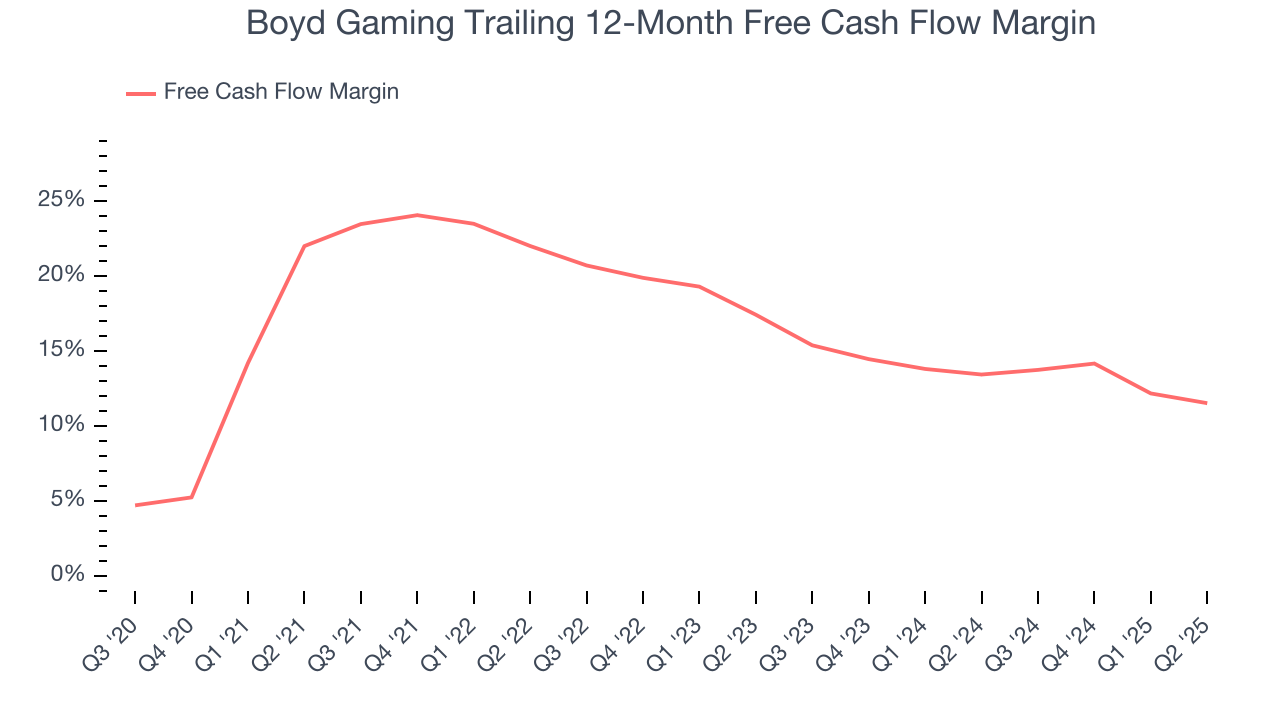

8. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Boyd Gaming has shown decent cash profitability, giving it some flexibility to reinvest or return capital to investors. The company’s free cash flow margin averaged 12.2% over the last two years, slightly better than the broader consumer discretionary sector.

9. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Boyd Gaming’s management team makes decent investment decisions and generates value for shareholders. Its five-year average ROIC was 17%, slightly better than typical consumer discretionary business.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Uneventfully, Boyd Gaming’s ROIC has stayed the same over the last few years. Given the company’s underwhelming financial performance in other areas, we’d like to see its returns improve before recommending the stock.

10. Balance Sheet Assessment

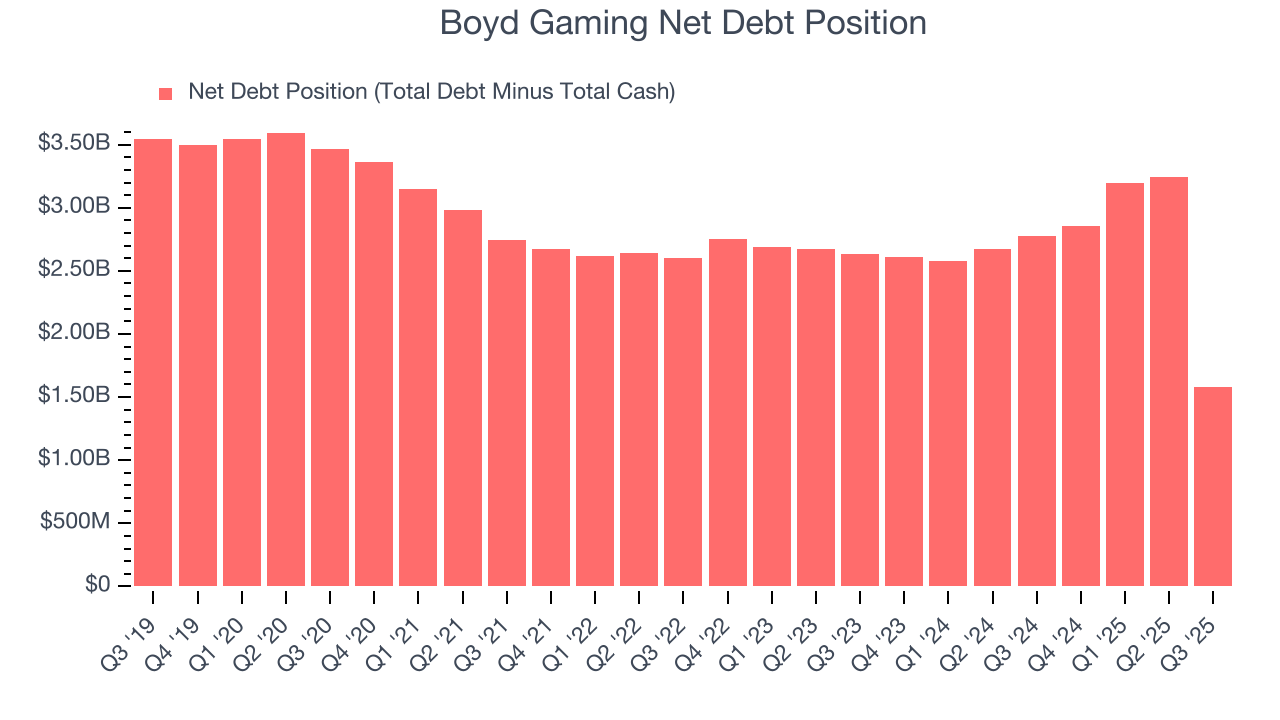

Boyd Gaming reported $319.1 million of cash and $1.9 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $1.28 billion of EBITDA over the last 12 months, we view Boyd Gaming’s 1.2× net-debt-to-EBITDA ratio as safe. We also see its $110.7 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

11. Key Takeaways from Boyd Gaming’s Q3 Results

We were impressed by how significantly Boyd Gaming blew past analysts’ revenue expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. Overall, we think this was a solid quarter with some key areas of upside. The stock remained flattish immediately following the results.

12. Is Now The Time To Buy Boyd Gaming?

Updated: January 24, 2026 at 9:49 PM EST

We think that the latest earnings result is only one piece of the bigger puzzle. If you’re deciding whether to own Boyd Gaming, you should also grasp the company’s longer-term business quality and valuation.

Boyd Gaming doesn’t pass our quality test. To kick things off, its revenue growth was weak over the last five years, and analysts expect its demand to deteriorate over the next 12 months. And while its astounding EPS growth over the last five years shows its profits are trickling down to shareholders, the downside is its Forecasted free cash flow margin suggests the company will ramp up its investments next year. On top of that, its projected EPS for the next year is lacking.

Boyd Gaming’s P/E ratio based on the next 12 months is 11.1x. While this valuation is fair, the upside isn’t great compared to the potential downside. There are superior stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $94.33 on the company (compared to the current share price of $83.77).