American Express Global Business Travel (GBTG)

American Express Global Business Travel is in for a bumpy ride. Its growth has decelerated and its failure to generate meaningful free cash flow makes us question its prospects.― StockStory Analyst Team

1. News

2. Summary

Why We Think American Express Global Business Travel Will Underperform

Originally spun off from American Express in 2014 but maintaining the Amex GBT brand, Global Business Travel Group (NYSE:GBTG) provides end-to-end business travel and expense management solutions, connecting corporate clients with travel suppliers and offering specialized software services.

- Operating margin failed to increase over the last year, indicating the company couldn’t optimize its expenses

- High servicing costs result in a relatively inferior gross margin of 60.1% that must be offset through increased usage

- Annual revenue growth of 8.9% over the last two years was well below our standards for the software sector

American Express Global Business Travel’s quality is inadequate. There are more profitable opportunities elsewhere.

Why There Are Better Opportunities Than American Express Global Business Travel

At $5.48 per share, American Express Global Business Travel trades at 0.9x forward price-to-sales. This is a cheap valuation multiple, but for good reason. You get what you pay for.

Cheap stocks can look like a great deal at first glance, but they can be value traps. They often have less earnings power, meaning there is more reliance on a re-rating to generate good returns - an unlikely scenario for low-quality companies.

3. American Express Global Business Travel (GBTG) Research Report: Q4 CY2025 Update

Business travel management company Global Business Travel Group (NYSE:GBTG) beat Wall Street’s revenue expectations in Q4 CY2025, with sales up 34% year on year to $792 million. The company expects the full year’s revenue to be around $3.27 billion, close to analysts’ estimates. Its GAAP profit of $0.17 per share was significantly above analysts’ consensus estimates.

American Express Global Business Travel (GBTG) Q4 CY2025 Highlights:

- Revenue: $792 million vs analyst estimates of $787.9 million (34% year-on-year growth, 0.5% beat)

- EPS (GAAP): $0.17 vs analyst estimates of $0.04 (significant beat)

- Adjusted EBITDA: $130 million vs analyst estimates of $130 million (16.4% margin, in line)

- EBITDA guidance for the upcoming financial year 2026 is $630 million at the midpoint, below analyst estimates of $635.3 million

- Operating Margin: -39.5%, down from 5.1% in the same quarter last year

- Free Cash Flow Margin: 1.6%, down from 5.6% in the previous quarter

- Market Capitalization: $3.01 billion

Company Overview

Originally spun off from American Express in 2014 but maintaining the Amex GBT brand, Global Business Travel Group (NYSE:GBTG) provides end-to-end business travel and expense management solutions, connecting corporate clients with travel suppliers and offering specialized software services.

Operating at the center of the business travel ecosystem, GBTG serves as an intermediary between corporations, their traveling employees, and travel providers like airlines, hotels, and car rental companies. The company's platform includes proprietary booking software, travel management tools, and the Amex GBT Marketplace that connects travel suppliers with business clients.

GBTG generates revenue through two main channels: transaction-based travel revenues and product/professional services. The transaction revenue comes from fees charged to both clients for arranging travel and suppliers for distributing their content. Meanwhile, the company earns additional income through management fees, meetings and events planning, consulting services, and subscription fees for travel management tools.

A typical corporate client might use GBTG to implement a company-wide travel policy, book flights and accommodations through dedicated travel counselors or self-service channels, manage travel expenses, and ensure traveler safety through care tools. GBTG particularly targets multinational corporations and small-to-medium enterprises (SMEs), which represented nearly half of its total transaction value in 2023. With a global network covering approximately 90% of worldwide business travel spend, the company extends its reach through partnerships with third-party travel management companies in regions where it lacks a direct presence.

4. Spend Management Software

The adoption of financial technology software is propelled by an ongoing drive to reduce costs. The combination of rising transaction volumes and global supply chain complexity is driving demand for cloud-based spend management platforms able to integrate the two.

GBTG competes with other major travel management companies including BCD Travel, CWT (formerly Carlson Wagonlit Travel), and FCM Travel Solutions (part of Flight Centre Travel Group), as well as travel technology providers like SAP Concur (NYSE: SAP) and TripActions (now Navan).

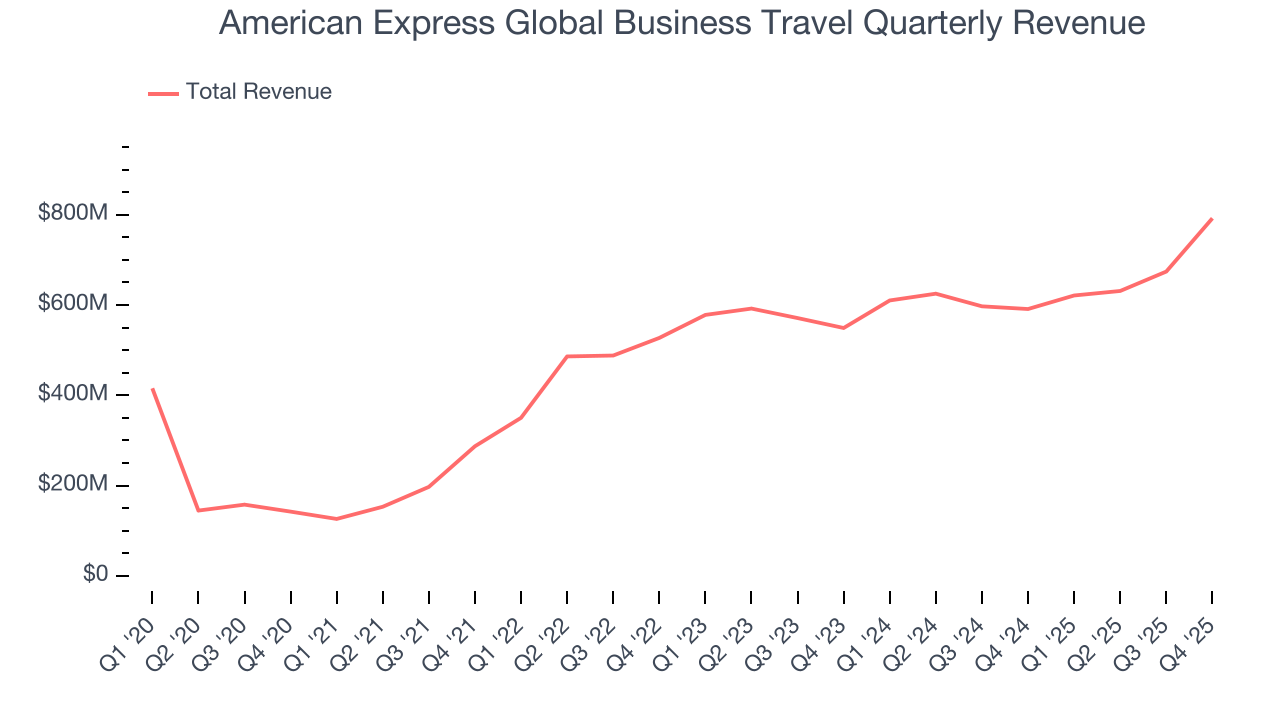

5. Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Luckily, American Express Global Business Travel’s sales grew at a solid 25.9% compounded annual growth rate over the last five years. Its growth beat the average software company and shows its offerings resonate with customers.

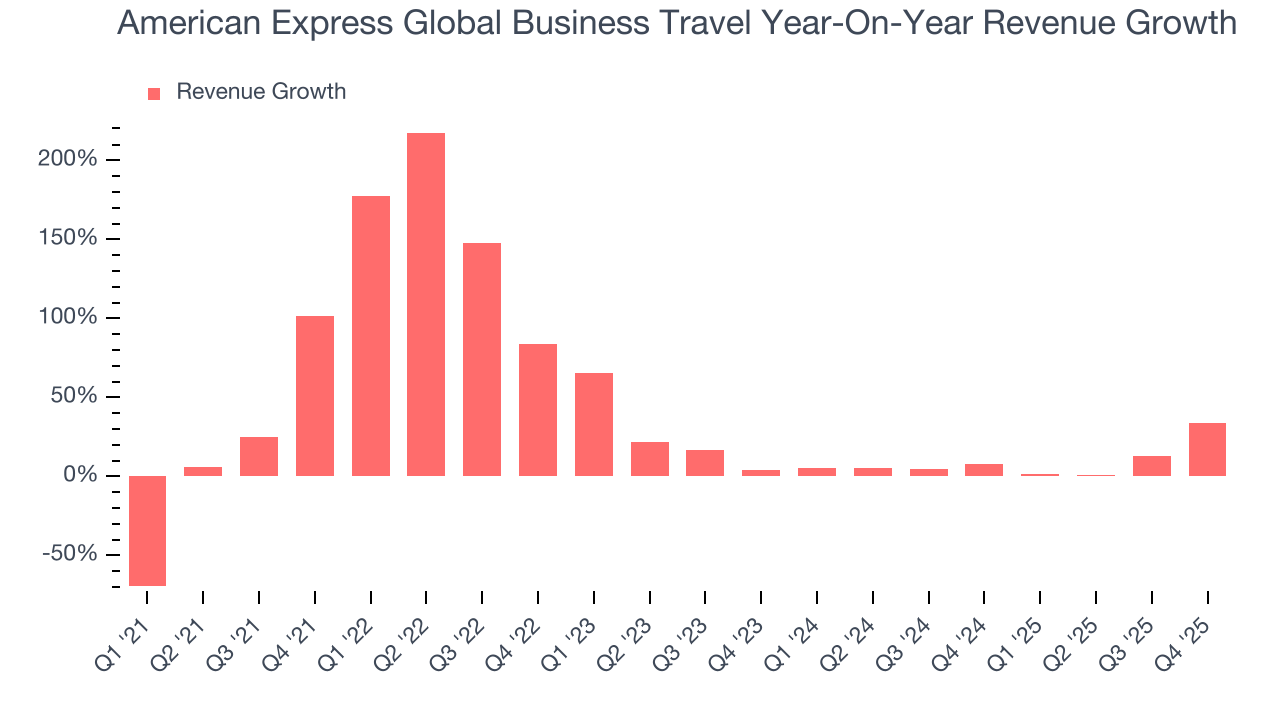

Long-term growth is the most important, but within software, a half-decade historical view may miss new innovations or demand cycles. American Express Global Business Travel’s recent performance shows its demand has slowed as its annualized revenue growth of 8.9% over the last two years was below its five-year trend. We’re wary when companies in the sector see decelerations in revenue growth, as it could signal changing consumer tastes aided by low switching costs.

This quarter, American Express Global Business Travel reported wonderful year-on-year revenue growth of 34%, and its $792 million of revenue exceeded Wall Street’s estimates by 0.5%.

Looking ahead, sell-side analysts expect revenue to grow 19.9% over the next 12 months, an improvement versus the last two years. This projection is healthy and indicates its newer products and services will fuel better top-line performance.

6. Gross Margin & Pricing Power

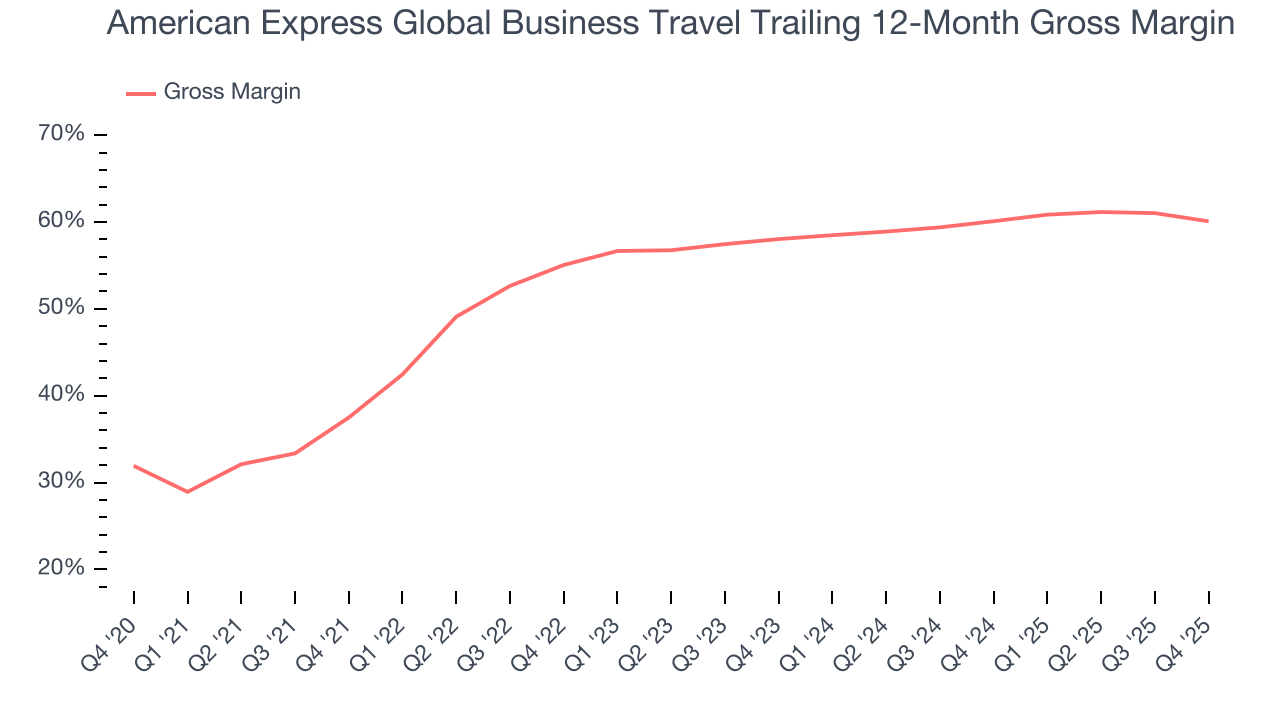

For software companies like American Express Global Business Travel, gross profit tells us how much money remains after paying for the base cost of products and services (typically servers, licenses, and certain personnel). These costs are usually low as a percentage of revenue, explaining why software is more lucrative than other sectors.

American Express Global Business Travel’s gross margin is substantially worse than most software businesses, signaling it has relatively high infrastructure costs compared to asset-lite businesses like ServiceNow. As you can see below, it averaged a 60.1% gross margin over the last year. Said differently, American Express Global Business Travel had to pay a chunky $39.92 to its service providers for every $100 in revenue.

The market not only cares about gross margin levels but also how they change over time because expansion creates firepower for profitability and free cash generation. American Express Global Business Travel has seen gross margins improve by 2 percentage points over the last 2 year, which is solid in the software space.

In Q4, American Express Global Business Travel produced a 56.8% gross profit margin , marking a 2.9 percentage point decrease from 59.7% in the same quarter last year. Zooming out, the company’s full-year margin has remained steady over the past 12 months, suggesting its input costs have been stable and it isn’t under pressure to lower prices.

7. Operating Margin

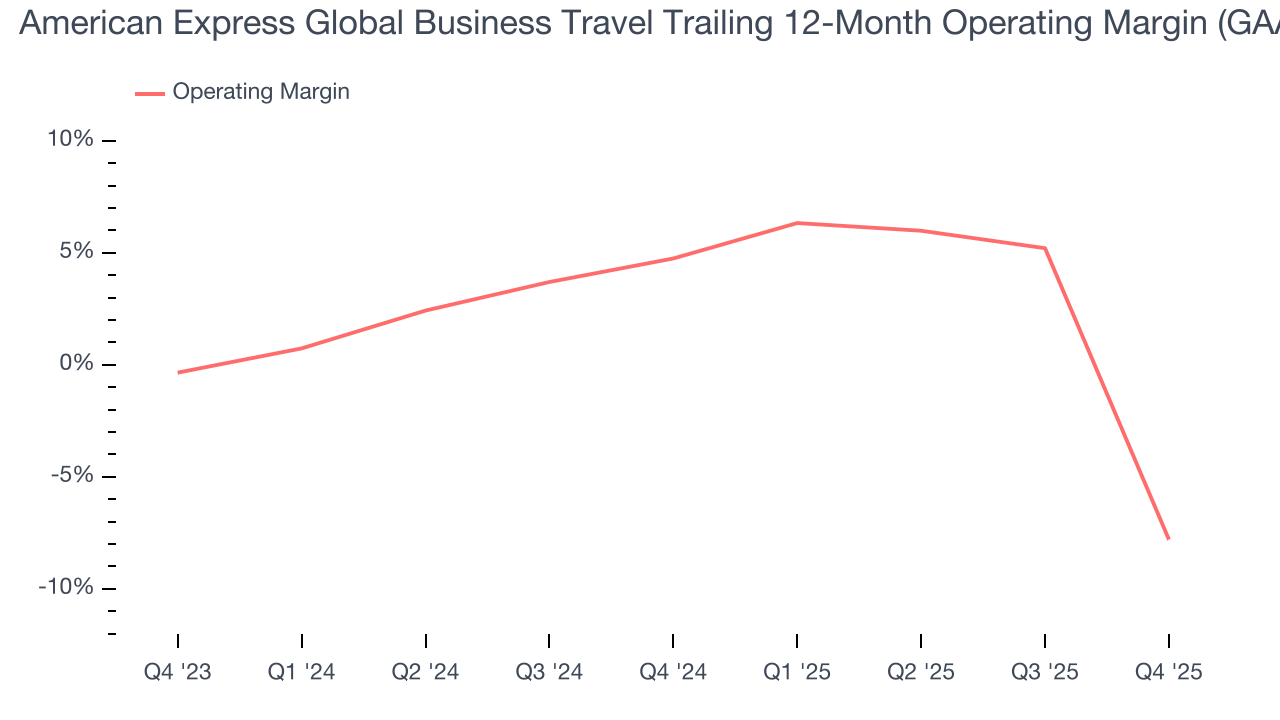

Many software businesses adjust their profits for stock-based compensation (SBC), but we prioritize GAAP operating margin because SBC is a real expense used to attract and retain engineering and sales talent. This metric shows how much revenue remains after accounting for all core expenses – everything from the cost of goods sold to sales and R&D.

American Express Global Business Travel’s expensive cost structure has contributed to an average operating margin of negative 7.8% over the last year. Unprofitable, high-growth software companies require extra attention because they spend heaps of money to capture market share. As seen in its fast historical revenue growth, this strategy seems to have worked so far, but it’s unclear what would happen if American Express Global Business Travel reeled back its investments. Wall Street seems to be optimistic about its growth, but we have some doubts.

Analyzing the trend in its profitability, American Express Global Business Travel’s operating margin decreased by 12.5 percentage points over the last two years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. American Express Global Business Travel’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers.

In Q4, American Express Global Business Travel generated a negative 39.5% operating margin.

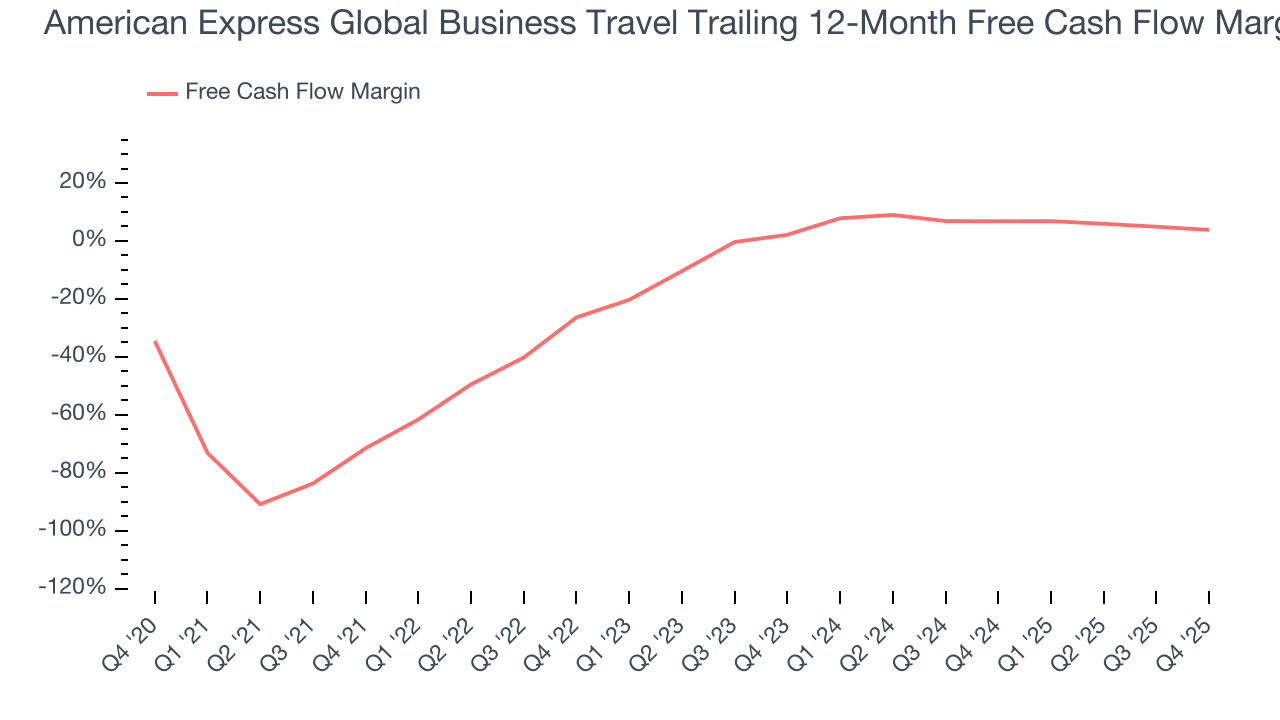

8. Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

American Express Global Business Travel has shown poor cash profitability relative to peers over the last year, giving the company fewer opportunities to return capital to shareholders. Its free cash flow margin averaged 3.8%, below what we’d expect for a software business.

American Express Global Business Travel’s free cash flow clocked in at $13 million in Q4, equivalent to a 1.6% margin. The company’s cash profitability regressed as it was 3.9 percentage points lower than in the same quarter last year, prompting us to pay closer attention. Short-term fluctuations typically aren’t a big deal because investment needs can be seasonal, but we’ll be watching to see if the trend extrapolates into future quarters.

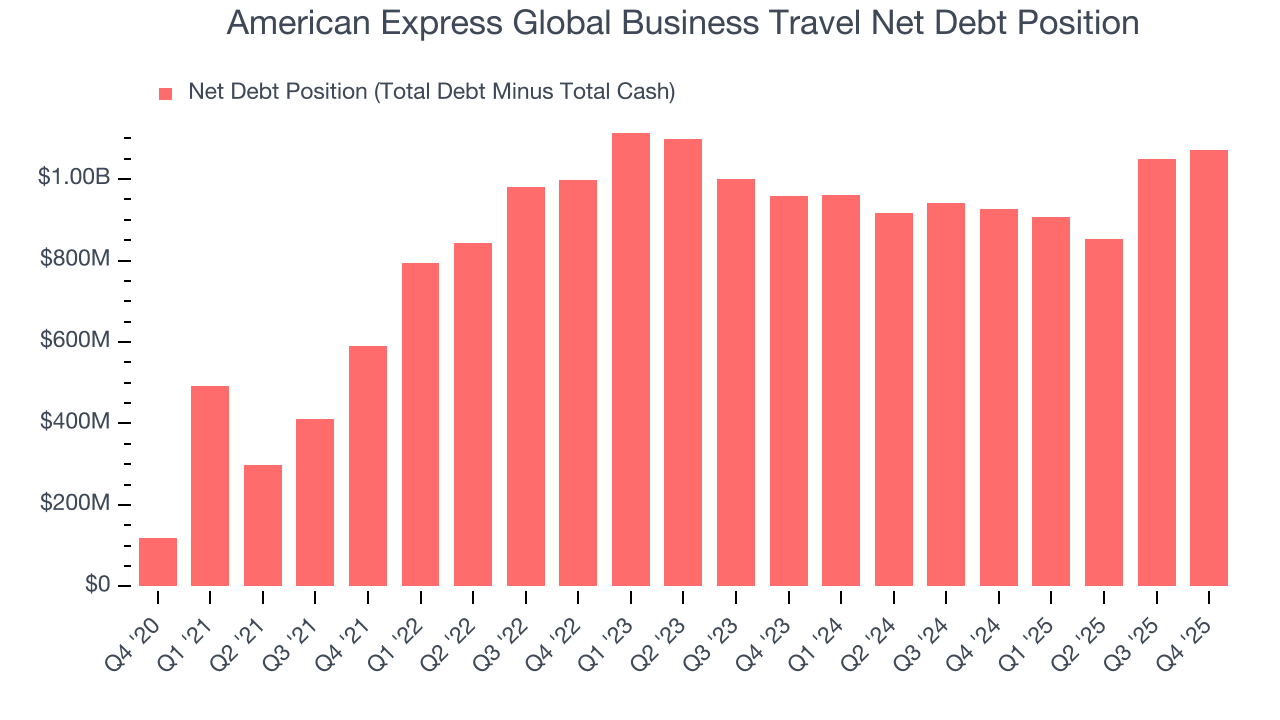

9. Balance Sheet Assessment

American Express Global Business Travel reported $434 million of cash and $1.51 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $532 million of EBITDA over the last 12 months, we view American Express Global Business Travel’s 2.0× net-debt-to-EBITDA ratio as safe. We also see its $43 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

10. Key Takeaways from American Express Global Business Travel’s Q4 Results

It was great to see American Express Global Business Travel expecting revenue growth to accelerate next year. On the other hand, its full-year EBITDA guidance slightly missed. Zooming out, we think this was a mixed quarter. The stock traded up 2.3% to $5.87 immediately following the results.

11. Is Now The Time To Buy American Express Global Business Travel?

Updated: March 14, 2026 at 11:01 PM EDT

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in American Express Global Business Travel.

We see the value of companies addressing major business pain points, but in the case of American Express Global Business Travel, we’re out. Although its revenue growth was strong over the last five years, it’s expected to deteriorate over the next 12 months and its operating margin hasn't moved over the last year. And while the company’s operating margins are in line with the overall software sector, the downside is its gross margins show its business model is much less lucrative than other companies.

American Express Global Business Travel’s price-to-sales ratio based on the next 12 months is 0.9x. While this valuation is optically cheap, the potential downside is huge given its shaky fundamentals. There are superior stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $9.80 on the company (compared to the current share price of $5.48).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.