Guidewire Software (GWRE)

We like Guidewire Software. Its elite ARR growth suggests it not only generates recurring revenue but also is winning market share.― StockStory Analyst Team

1. News

2. Summary

Why We Like Guidewire Software

With its systems powering the operations of hundreds of insurance brands across 42 countries, Guidewire Software (NYSE:GWRE) provides a technology platform that helps property and casualty insurance companies manage their core operations, digital engagement, and analytics.

- User-friendly software enables clients to ramp up spending quickly, leading to the speedy recovery of customer acquisition costs

- Average billings growth of 21.1% over the last year enhances its liquidity and shows there is steady demand for its products

- Free cash flow profile clocks in well above its peers, giving it the option to reinvest

Guidewire Software is a standout company. The valuation looks fair based on its quality, so this could be a prudent time to buy some shares.

Why Is Now The Time To Buy Guidewire Software?

At $156.88 per share, Guidewire Software trades at 8.6x forward price-to-sales. While this multiple is higher than most software companies, we think the valuation is fair given its quality characteristics.

By definition, where you buy a stock impacts returns. But according to our work on the topic, business quality is a much bigger determinant of market outperformance over the long term compared to entry price.

3. Guidewire Software (GWRE) Research Report: Q4 CY2025 Update

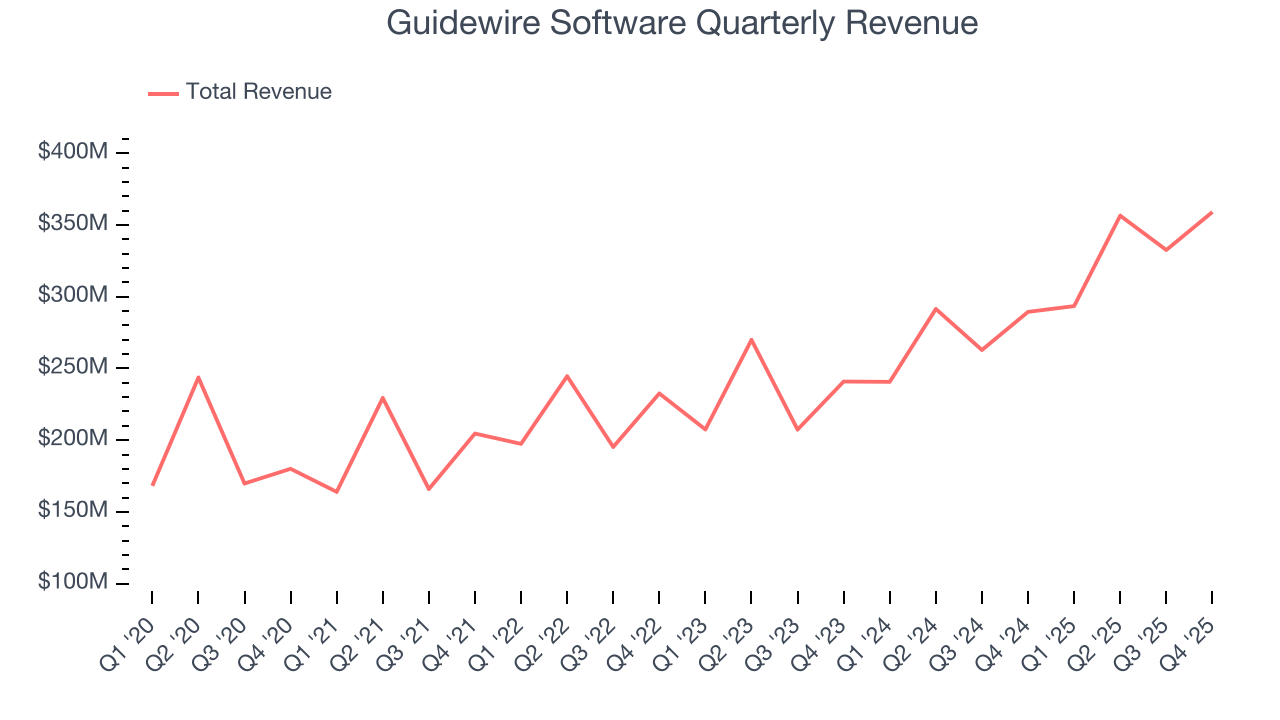

Insurance software provider Guidewire Software (NYSE:GWRE) reported Q4 CY2025 results beating Wall Street’s revenue expectations, with sales up 24% year on year to $359.1 million. On top of that, next quarter’s revenue guidance ($355 million at the midpoint) was surprisingly good and 4.6% above what analysts were expecting. Its non-GAAP profit of $1.17 per share was 52.5% above analysts’ consensus estimates.

Guidewire Software (GWRE) Q4 CY2025 Highlights:

- Revenue: $359.1 million vs analyst estimates of $342.7 million (24% year-on-year growth, 4.8% beat)

- Adjusted EPS: $1.17 vs analyst estimates of $0.77 (52.5% beat)

- Adjusted Operating Income: $87.39 million vs analyst estimates of $71.68 million (24.3% margin, 21.9% beat)

- The company lifted its revenue guidance for the full year to $1.44 billion at the midpoint from $1.41 billion, a 2.3% increase

- Operating Margin: 10.7%, up from 4% in the same quarter last year

- Free Cash Flow was $105.7 million, up from -$77.36 million in the previous quarter

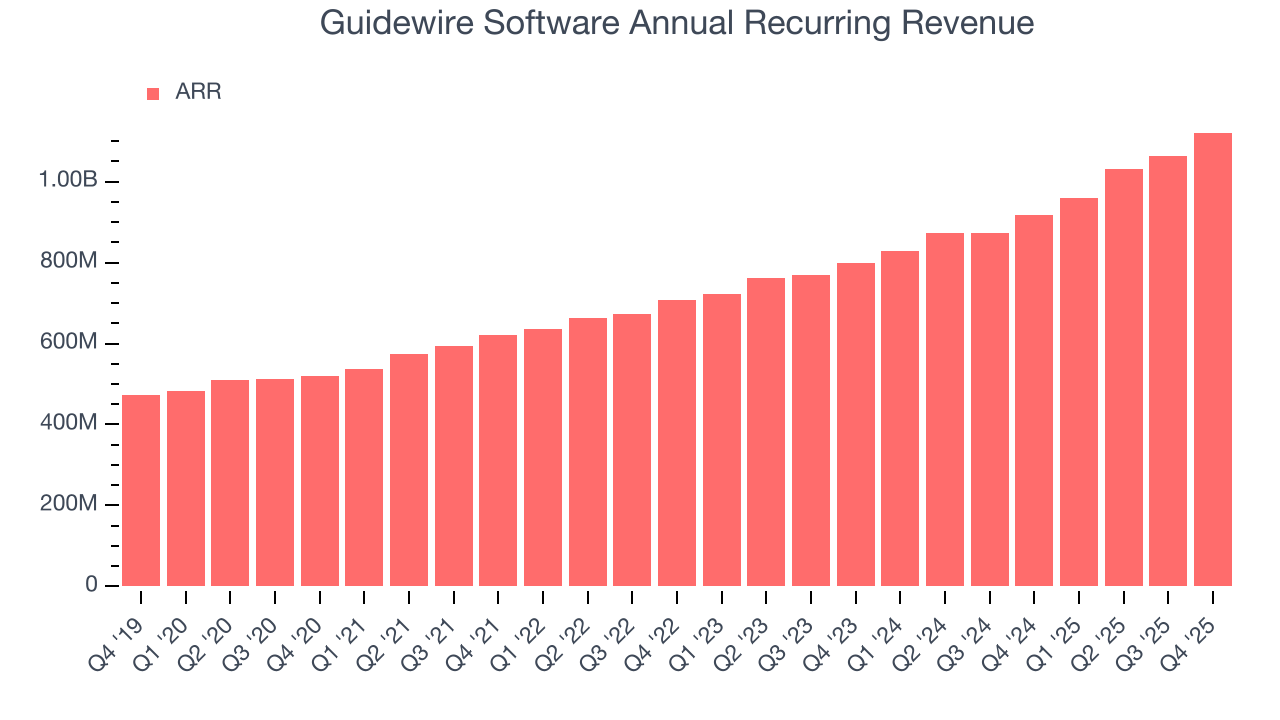

- Annual Recurring Revenue: $1.12 billion (22.1% year-on-year growth, beat)

- Billings: $415.4 million at quarter end, up 25.8% year on year

- Market Capitalization: $13.08 billion

Company Overview

With its systems powering the operations of hundreds of insurance brands across 42 countries, Guidewire Software (NYSE:GWRE) provides a technology platform that helps property and casualty insurance companies manage their core operations, digital engagement, and analytics.

The company's flagship offering, InsuranceSuite Cloud, consists of three core applications that can be used together or separately: PolicyCenter for underwriting and policy administration, BillingCenter for managing billing and payments, and ClaimCenter for end-to-end claims processing. These applications run on the Guidewire Cloud Platform, built on Amazon Web Services, which combines multi-tenant cloud services with isolated database instances for each customer.

Guidewire serves the specific needs of the property and casualty (P&C) insurance industry, with customers ranging from global insurance giants to regional and state-level providers. For example, an auto insurer might use Guidewire's platform to streamline the entire process from policy creation to claims settlement after an accident, while providing digital self-service options for policyholders and data analytics to improve underwriting decisions.

The company monetizes its offerings primarily through subscription services for cloud-delivered products and term licenses for self-managed installations. Guidewire also provides implementation, migration, and integration services, either directly or through system integrator partners. Additionally, the company maintains the Guidewire Marketplace, where customers can find complementary applications and content from partners to extend the platform's capabilities.

4. Vertical Software

Software is eating the world, and while a large number of solutions such as project management or video conferencing software can be useful to a wide array of industries, some have very specific needs. As a result, vertical software, which addresses industry-specific workflows, is growing and fueled by the pressures to improve productivity, whether it be for a life sciences, education, or banking company.

Guidewire competes with insurers' internally developed solutions as well as specialized P&C insurance software vendors like Duck Creek, EIS Group, Insurity, Majesco, and Sapiens. The company also faces competition from horizontal software providers such as SAP and Salesforce that offer broader enterprise solutions.

5. Revenue Growth

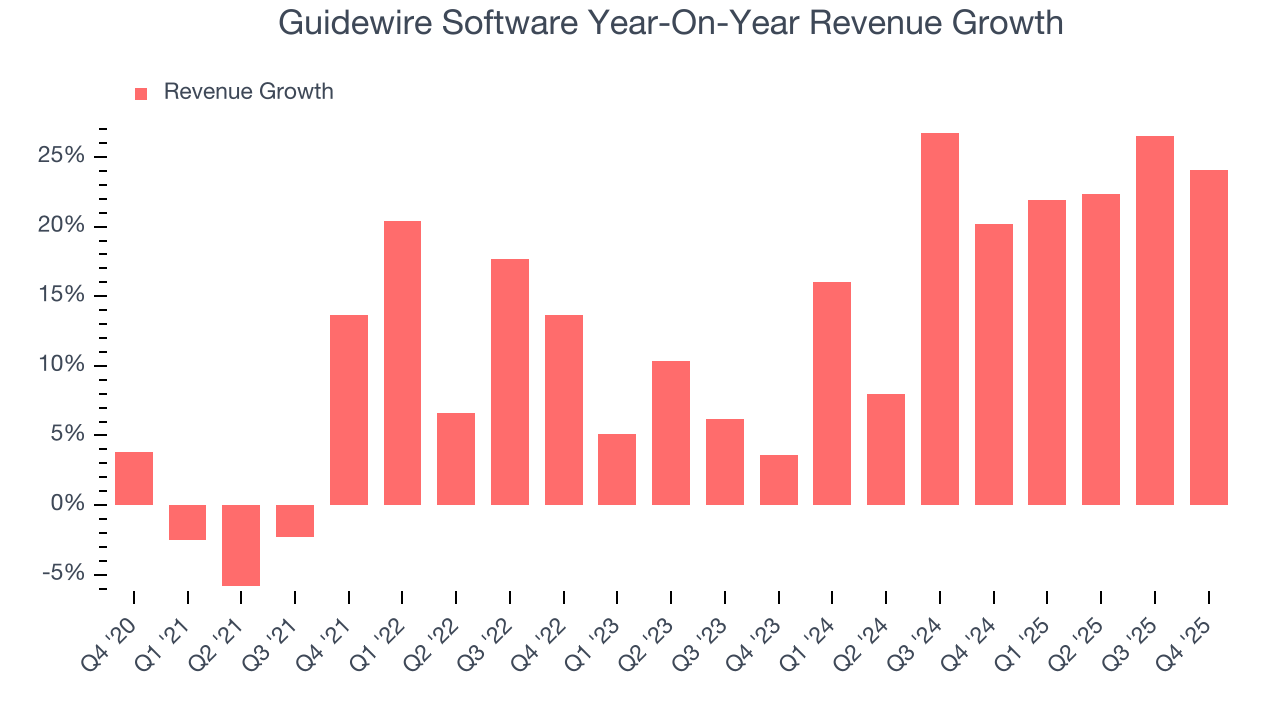

A company’s long-term performance is an indicator of its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Over the last five years, Guidewire Software grew its sales at a 12% annual rate. Though this growth is acceptable on an absolute basis, we need to see more than just topline growth for the software sector, which can display significant earnings volatility. This means our bar for the sector is particularly high, reflecting the non-essential and hit-driven nature of the products and services offered. Additionally, five-year CAGR starts around Covid, when revenue was depressed then rebounded. Luckily, there are other things to like about Guidewire Software.

Long-term growth is the most important, but within software, a half-decade historical view may miss new innovations or demand cycles. Guidewire Software’s annualized revenue growth of 20.4% over the last two years is above its five-year trend, suggesting its demand recently accelerated.

This quarter, Guidewire Software reported robust year-on-year revenue growth of 24%, and its $359.1 million of revenue topped Wall Street estimates by 4.8%. Company management is currently guiding for a 21% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 12.8% over the next 12 months, a deceleration versus the last two years. This projection doesn't excite us and suggests its products and services will face some demand challenges. At least the company is tracking well in other measures of financial health.

6. Annual Recurring Revenue

While reported revenue for a software company can include low-margin items like implementation fees, annual recurring revenue (ARR) is a sum of the next 12 months of contracted revenue purely from software subscriptions, or the high-margin, predictable revenue streams that make SaaS businesses so valuable.

Guidewire Software’s ARR punched in at $1.12 billion in Q4, and over the last four quarters, its growth was impressive as it averaged 19.5% year-on-year increases. This alternate topline metric grew slower than total sales, which likely means that the recurring portions of the business are growing slower than less predictable, choppier ones such as implementation fees. If this continues, the quality of its revenue base could decline.

7. Customer Acquisition Efficiency

The customer acquisition cost (CAC) payback period measures the months a company needs to recoup the money spent on acquiring a new customer. This metric helps assess how quickly a business can break even on its sales and marketing investments.

Guidewire Software is extremely efficient at acquiring new customers, and its CAC payback period checked in at 17.2 months this quarter. The company’s rapid recovery of its customer acquisition costs indicates it has a highly differentiated product offering and a strong brand reputation. These dynamics give Guidewire Software more resources to pursue new product initiatives while maintaining the flexibility to increase its sales and marketing investments.

8. Gross Margin & Pricing Power

For software companies like Guidewire Software, gross profit tells us how much money remains after paying for the base cost of products and services (typically servers, licenses, and certain personnel). These costs are usually low as a percentage of revenue, explaining why software is more lucrative than other sectors.

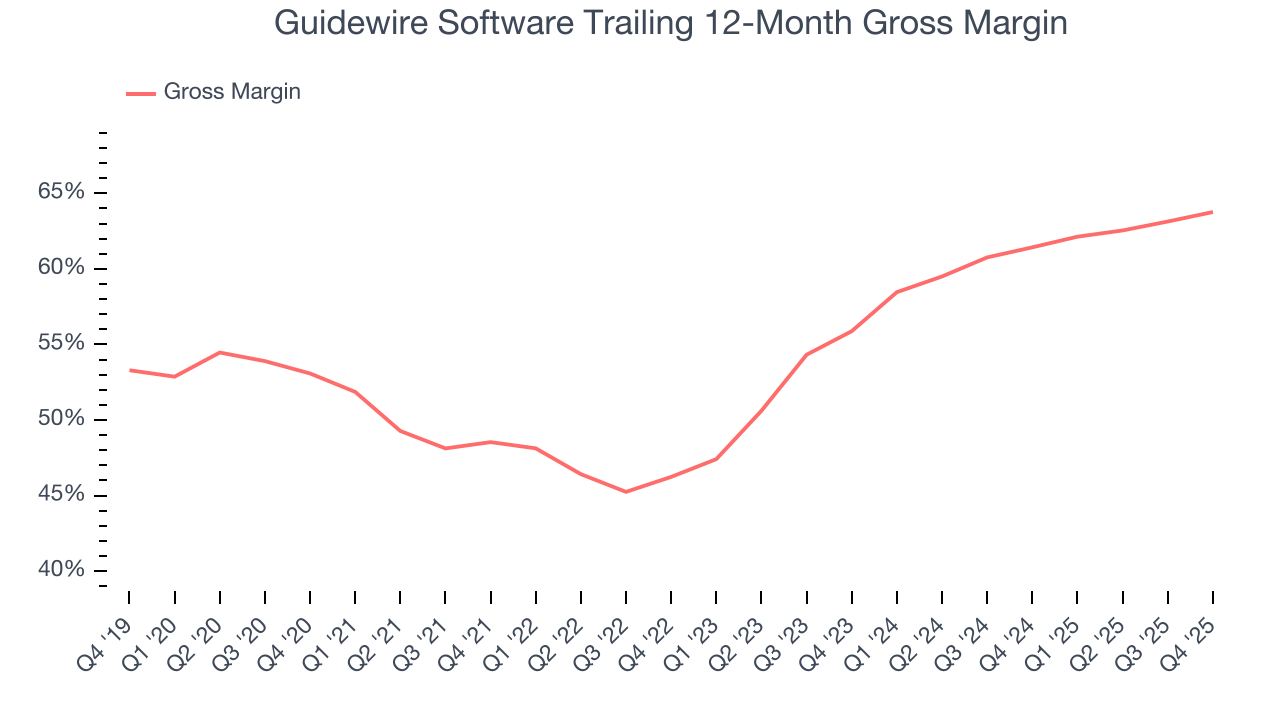

Guidewire Software’s gross margin is substantially worse than most software businesses, signaling it has relatively high infrastructure costs compared to asset-lite businesses like ServiceNow. As you can see below, it averaged a 63.8% gross margin over the last year. That means Guidewire Software paid its providers a lot of money ($36.24 for every $100 in revenue) to run its business.

The market not only cares about gross margin levels but also how they change over time because expansion creates firepower for profitability and free cash generation. Guidewire Software has seen gross margins improve by 7.9 percentage points over the last 2 year, which is elite in the software space.

This quarter, Guidewire Software’s gross profit margin was 64.5%, up 2.6 percentage points year on year. Guidewire Software’s full-year margin has also been trending up over the past 12 months, increasing by 2.3 percentage points. If this move continues, it could suggest better unit economics due to more leverage from its growing sales on the fixed portion of its cost of goods sold (such as servers).

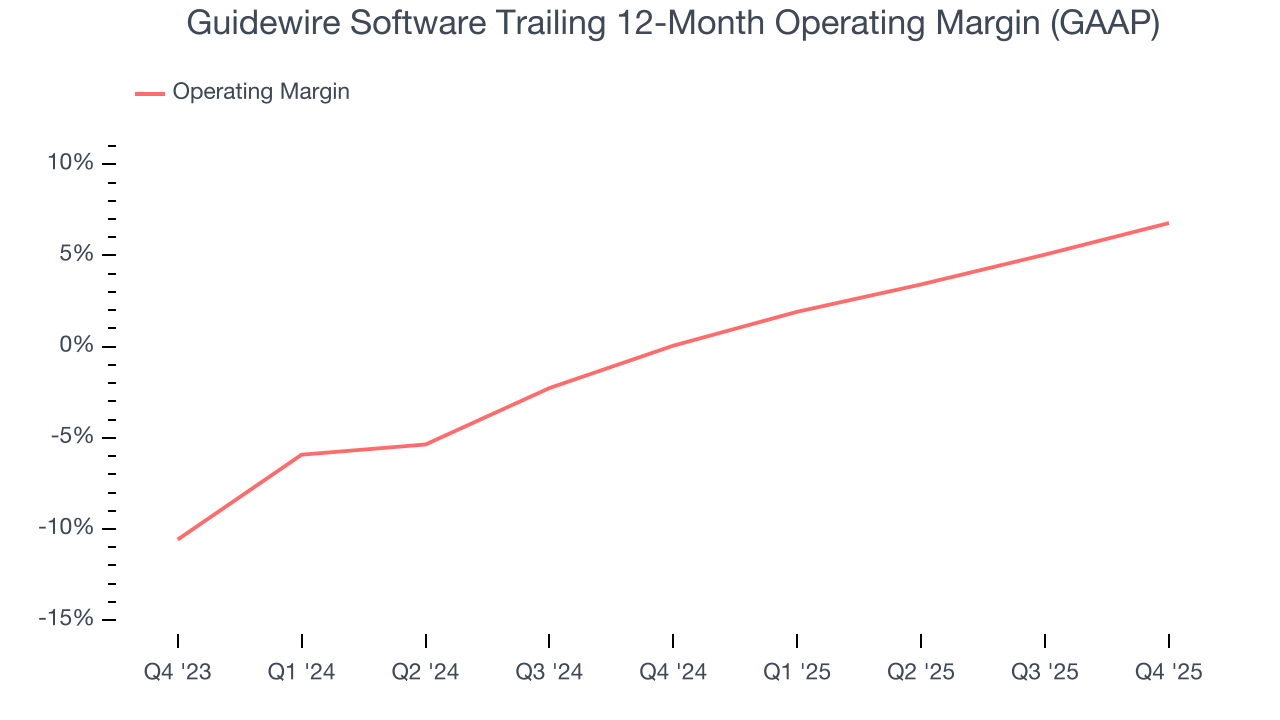

9. Operating Margin

While many software businesses point investors to their adjusted profits, which exclude stock-based compensation (SBC), we prefer GAAP operating margin because SBC is a legitimate expense used to attract and retain talent. This metric shows how much revenue remains after accounting for all core expenses – everything from the cost of goods sold to sales and R&D.

Guidewire Software has managed its cost base well over the last year. It demonstrated solid profitability for a software business, producing an average operating margin of 6.8%. This result was particularly impressive because of its low gross margin, which is mostly a factor of what it sells and takes huge shifts to move meaningfully. Companies have more control over their operating margins, and it’s a show of well-managed operations if they’re high when gross margins are low.

Looking at the trend in its profitability, Guidewire Software’s operating margin rose by 6.7 percentage points over the last two years, as its sales growth gave it operating leverage.

In Q4, Guidewire Software generated an operating margin profit margin of 10.7%, up 6.7 percentage points year on year. The increase was solid, and because its operating margin rose more than its gross margin, we can infer it was more efficient with expenses such as marketing, R&D, and administrative overhead.

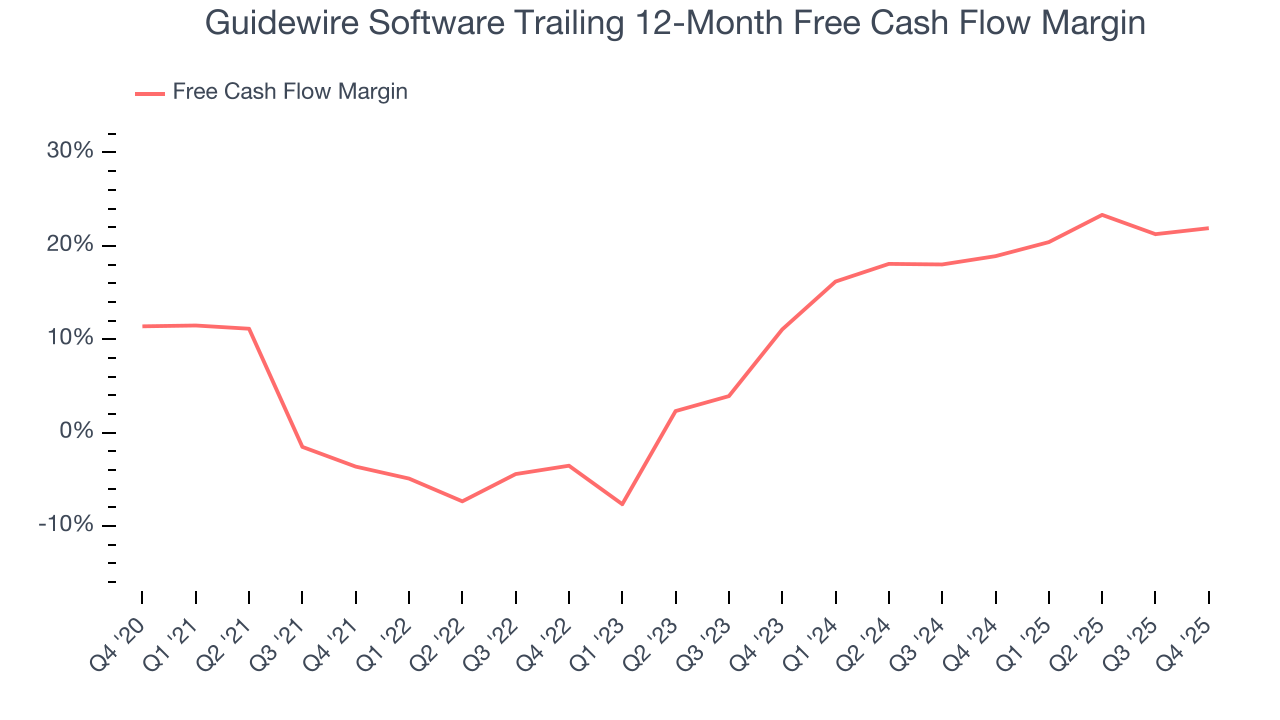

10. Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Guidewire Software has shown impressive cash profitability, driven by its cost-effective customer acquisition strategy that gives it the option to invest in new products and services rather than sales and marketing. The company’s free cash flow margin averaged 21.9% over the last year, better than the broader software sector. Guidewire Software has shown impressive cash profitability relative to peers over the last year, giving the company fewer opportunities to return capital to shareholders.

Guidewire Software’s free cash flow clocked in at $105.7 million in Q4, equivalent to a 29.4% margin. This result was good as its margin was 1 percentage points higher than in the same quarter last year. Its cash profitability was also above its one-year level, and we hope the company can build on this trend.

Over the next year, analysts predict Guidewire Software’s cash conversion will improve. Their consensus estimates imply its free cash flow margin of 21.9% for the last 12 months will increase to 23.4%, giving it more flexibility for investments, share buybacks, and dividends.

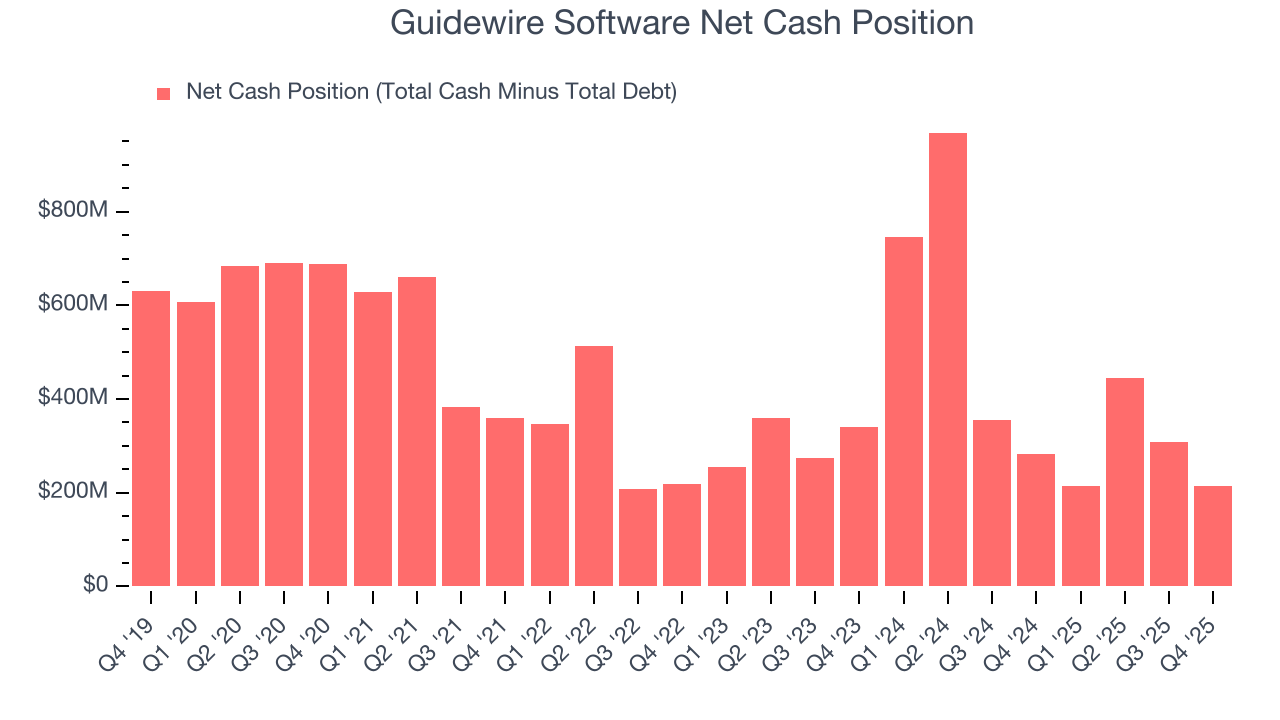

11. Balance Sheet Assessment

One of the best ways to mitigate bankruptcy risk is to hold more cash than debt.

Guidewire Software is a profitable, well-capitalized company with $919.2 million of cash and $705 million of debt on its balance sheet. This $214.2 million net cash position gives it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

12. Key Takeaways from Guidewire Software’s Q4 Results

We were impressed by how significantly Guidewire Software blew past analysts’ billings expectations this quarter. We were also glad its revenue guidance for next quarter exceeded Wall Street’s estimates. Zooming out, we think this was a solid print. The stock traded up 2.1% to $166.24 immediately after reporting.

13. Is Now The Time To Buy Guidewire Software?

Updated: March 23, 2026 at 10:42 PM EDT

A common mistake we notice when investors are deciding whether to buy a stock or not is that they simply look at the latest earnings results. Business quality and valuation matter more, so we urge you to understand these dynamics as well.

Guidewire Software is an amazing business ranking highly on our list. Although its revenue growth was uninspiring over the last five years, its growth over the next 12 months is expected to be higher. And while its gross margins show its business model is much less lucrative than other companies, its efficient sales strategy allows it to target and onboard new users at scale. In addition, Guidewire Software’s splendid ARR growth shows it’s securing more long-term contracts and becoming a more predictable business.

Guidewire Software’s price-to-sales ratio based on the next 12 months is 8.6x. Scanning the software space today, Guidewire Software’s fundamentals really stand out, and we like it at this price.

Wall Street analysts have a consensus one-year price target of $234.14 on the company (compared to the current share price of $156.88), implying they see 49.2% upside in buying Guidewire Software in the short term.