Lockheed Martin (LMT)

Lockheed Martin is up against the odds. Its poor sales growth and falling returns on capital suggest its growth opportunities are shrinking.― StockStory Analyst Team

1. News

2. Summary

Why We Think Lockheed Martin Will Underperform

Headquartered in Maryland, Famous for the F-35 aircraft, Lockheed Martin (NYSE:LMT) specializes in defense, space, homeland security, and information technology products.

- Incremental sales over the last five years were much less profitable as its earnings per share fell by 2.6% annually while its revenue grew

- Scale is a double-edged sword because it limits the company’s growth potential compared to its smaller competitors, as reflected in its below-average annual revenue increases of 2.8% for the last five years

- Anticipated sales growth of 5.5% for the next year implies demand will be shaky

Lockheed Martin’s quality isn’t great. Our attention is focused on better businesses.

Why There Are Better Opportunities Than Lockheed Martin

Lockheed Martin is trading at $597.98 per share, or 20.6x forward P/E. Lockheed Martin’s multiple may seem like a great deal among industrials peers, but we think there are valid reasons why it’s this cheap.

It’s better to pay up for high-quality businesses with higher long-term earnings potential rather than to buy lower-quality stocks because they appear cheap. These challenged businesses often don’t re-rate, a phenomenon known as a “value trap”.

3. Lockheed Martin (LMT) Research Report: Q4 CY2025 Update

Security and Aerospace company Lockheed Martin (NYSE:LMT) reported Q4 CY2025 results beating Wall Street’s revenue expectations, with sales up 9.1% year on year to $20.32 billion. The company’s full-year revenue guidance of $78.75 billion at the midpoint came in 1.2% above analysts’ estimates. Its GAAP profit of $5.80 per share was 0.9% above analysts’ consensus estimates.

Lockheed Martin (LMT) Q4 CY2025 Highlights:

- Revenue: $20.32 billion vs analyst estimates of $19.84 billion (9.1% year-on-year growth, 2.4% beat)

- EPS (GAAP): $5.80 vs analyst estimates of $5.75 (0.9% beat)

- Adjusted EBITDA: $2.88 billion vs analyst estimates of $2.66 billion (14.2% margin, 8.2% beat)

- EPS (GAAP) guidance for the upcoming financial year 2026 is $29.80 at the midpoint, beating analyst estimates by 1.3%

- Operating Margin: 11.5%, up from 3.7% in the same quarter last year

- Free Cash Flow Margin: 15.8%, up from 2.4% in the same quarter last year

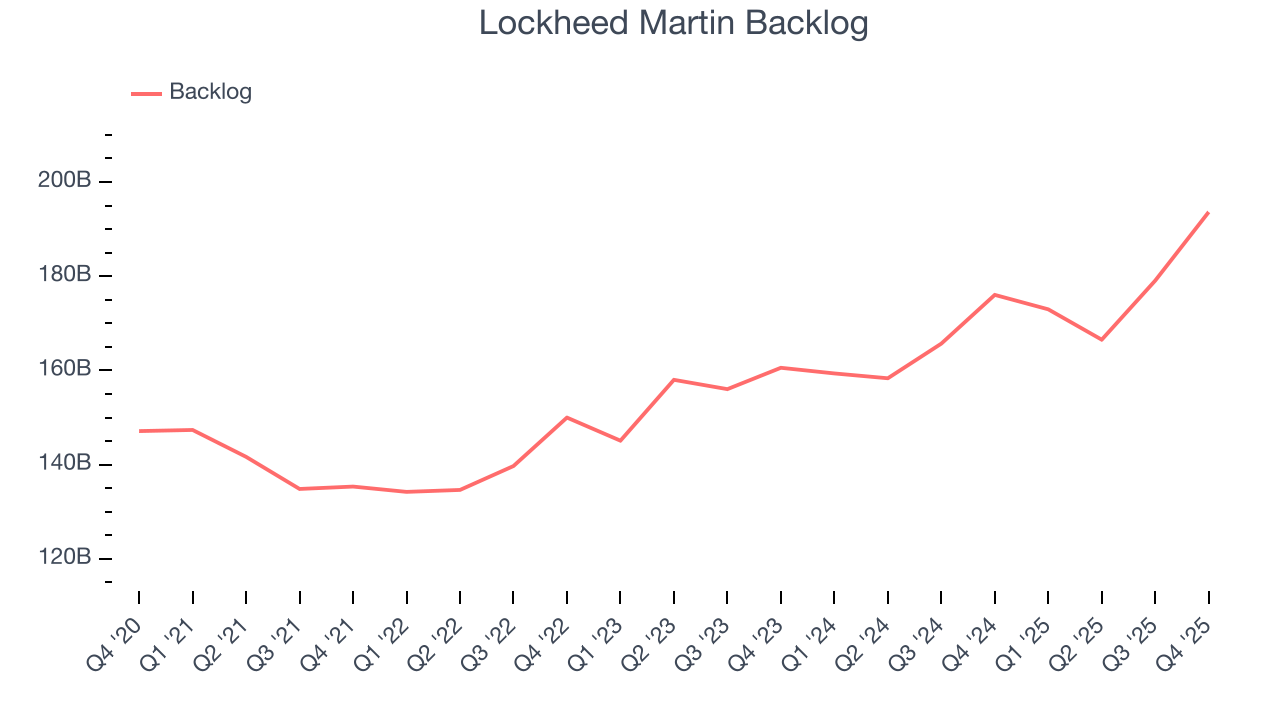

- Backlog: $193.6 billion at quarter end, up 10% year on year

- Market Capitalization: $138.2 billion

Company Overview

Headquartered in Maryland, Famous for the F-35 aircraft, Lockheed Martin (NYSE:LMT) specializes in defense, space, homeland security, and information technology products.

In 1995, Lockheed Corporation and Martin Marietta merged to form Lockheed Martin, creating one of the largest aerospace, defense, security, and technologies companies globally. This merger combined the strengths of both legacy companies, enhancing Lockheed Martin's role in the development and production of technological systems for defense and commercial use. Over the years, Lockheed Martin has played a crucial role in advancing technology across various domains, including aircraft, spacecraft, and missile systems.

Lockheed Martin specializes in advanced technology systems and services across aerospace and defense sectors. Its offerings include the F-35 Lightning II, a stealth fighter jet, and the Sikorsky BLACK HAWK helicopters, crucial for military engagements and humanitarian missions. Furthermore, Lockheed Martin extends its product line to space exploration and satellite communications, enabling everything from GPS navigation to global communications.

Lockheed Martin generates the bulk of its revenue from contracts with the U.S. government, particularly from the Department of Defense and various intelligence agencies. These contracts typically involve the development, manufacture, and maintenance of its systems. In addition to its primary market in defense, Lockheed Martin also earns revenue from international customers, including foreign military sales that are often facilitated by the U.S. government. These international contracts help to diversify its revenue streams beyond the domestic market.

On a smaller scale, Lockheed Martin is involved in the commercial aviation sector. Here, the company provides various products and services, including aircraft components and logistical support, though this represents a minor portion of its overall business compared to its government contracts.

4. Defense Contractors

Defense contractors typically require technical expertise and government clearance. Companies in this sector can also enjoy long-term contracts with government bodies, leading to more predictable revenues. Combined, these factors create high barriers to entry and can lead to limited competition. Lately, geopolitical tensions–whether it be Russia’s invasion of Ukraine or China’s aggression towards Taiwan–highlight the need for defense spending. On the other hand, demand for these products can ebb and flow with defense budgets and even who is president, as different administrations can have vastly different ideas of how to allocate federal funds.

Lockheed’s peers and competitors include Boeing (NYSE:BA), Raytheon (NYSE:RTX), General Dynamics (NYSE:GD), and Northrop Grumman (NYSE:NOC) among others.

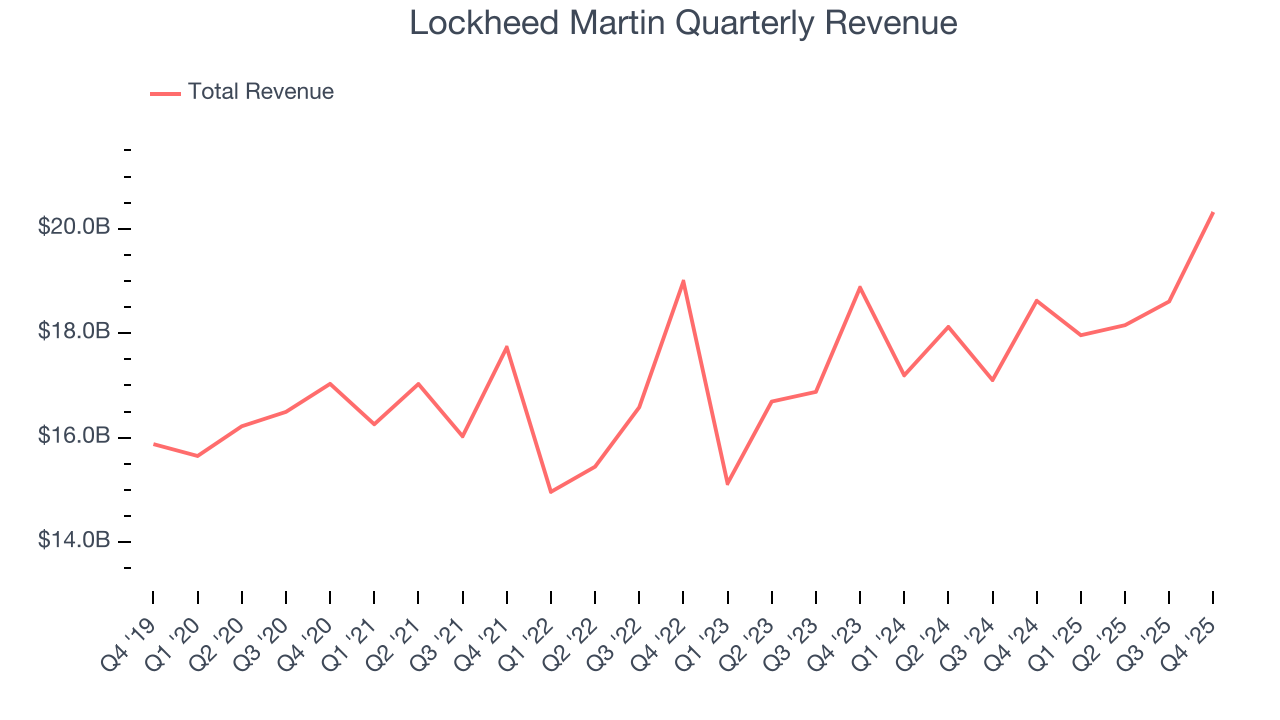

5. Revenue Growth

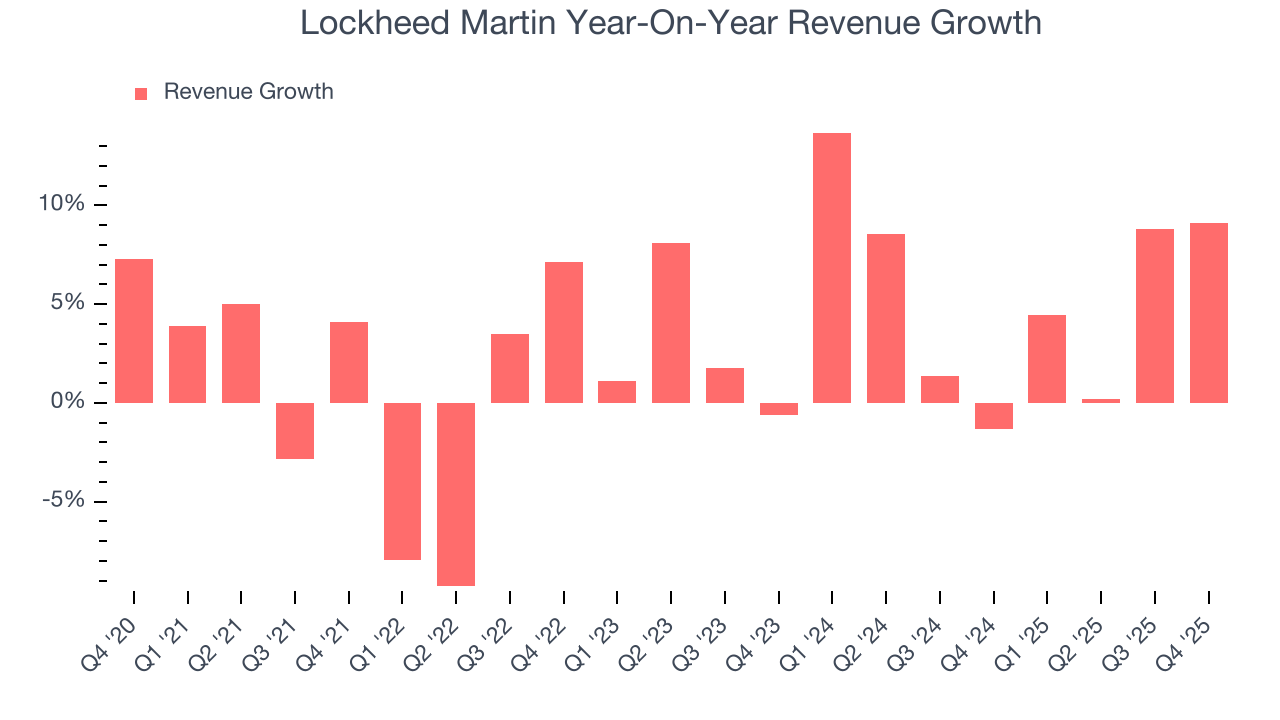

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Unfortunately, Lockheed Martin’s 2.8% annualized revenue growth over the last five years was sluggish. This was below our standards and is a tough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Lockheed Martin’s annualized revenue growth of 5.4% over the last two years is above its five-year trend, but we were still disappointed by the results.

We can dig further into the company’s revenue dynamics by analyzing its backlog, or the value of its outstanding orders that have not yet been executed or delivered. Lockheed Martin’s backlog reached $193.6 billion in the latest quarter and averaged 7.2% year-on-year growth over the last two years. Because this number is better than its revenue growth, we can see the company accumulated more orders than it could fulfill and deferred revenue to the future. This could imply elevated demand for Lockheed Martin’s products and services but raises concerns about capacity constraints.

This quarter, Lockheed Martin reported year-on-year revenue growth of 9.1%, and its $20.32 billion of revenue exceeded Wall Street’s estimates by 2.4%.

Looking ahead, sell-side analysts expect revenue to grow 4% over the next 12 months, similar to its two-year rate. This projection doesn't excite us and suggests its products and services will see some demand headwinds.

6. Operating Margin

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after procuring and manufacturing its products, marketing and selling those products, and most importantly, keeping them relevant through research and development.

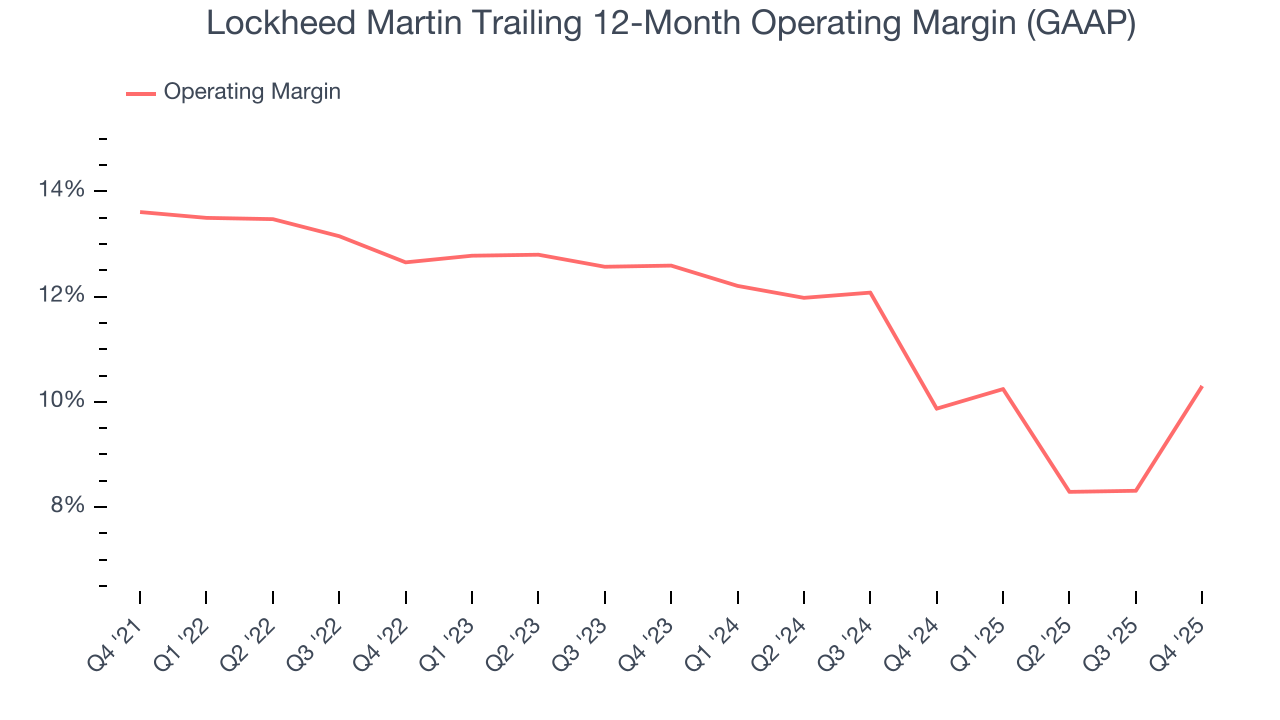

Lockheed Martin has managed its cost base well over the last five years. It demonstrated solid profitability for an industrials business, producing an average operating margin of 11.7%.

Looking at the trend in its profitability, Lockheed Martin’s operating margin decreased by 3.3 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

This quarter, Lockheed Martin generated an operating margin profit margin of 11.5%, up 7.7 percentage points year on year. This increase was a welcome development and shows it was more efficient.

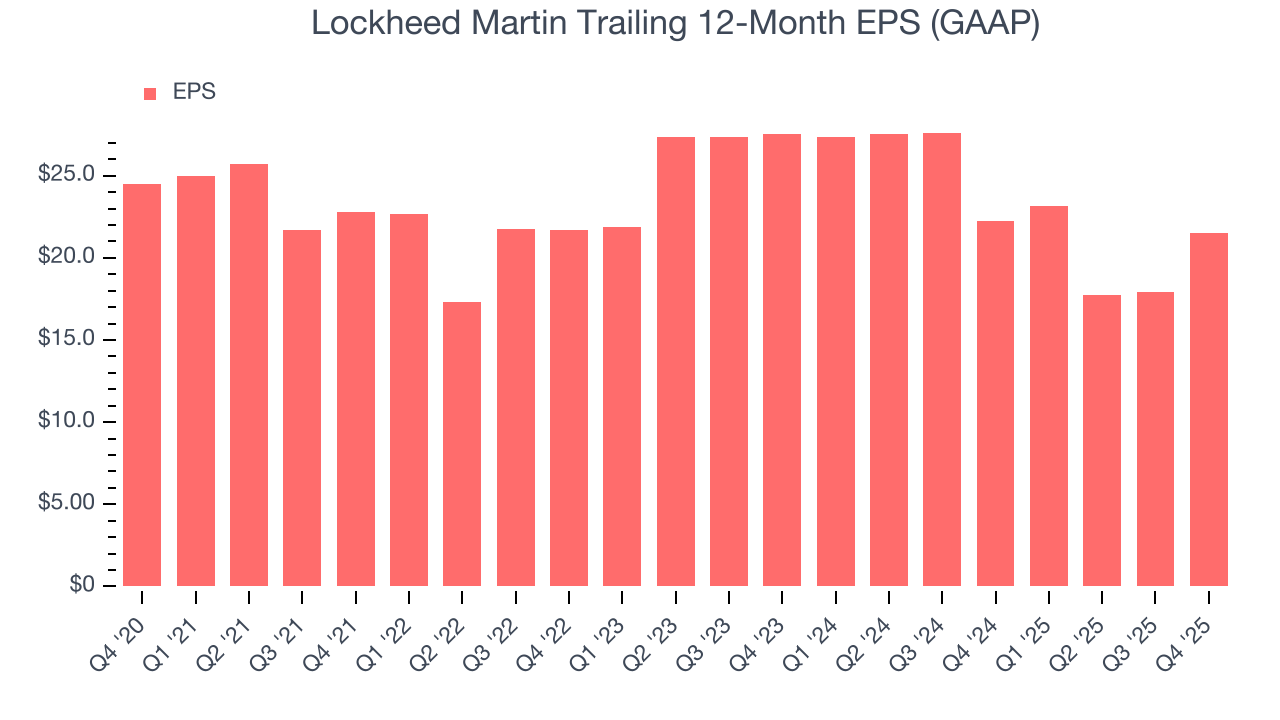

7. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Sadly for Lockheed Martin, its EPS declined by 2.6% annually over the last five years while its revenue grew by 2.8%. This tells us the company became less profitable on a per-share basis as it expanded due to non-fundamental factors such as interest expenses and taxes.

Diving into the nuances of Lockheed Martin’s earnings can give us a better understanding of its performance. As we mentioned earlier, Lockheed Martin’s operating margin expanded this quarter but declined by 3.3 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its lower earnings; interest expenses and taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Lockheed Martin, its two-year annual EPS declines of 11.7% show it’s continued to underperform. These results were bad no matter how you slice the data.

In Q4, Lockheed Martin reported EPS of $5.80, up from $2.22 in the same quarter last year. This print was close to analysts’ estimates. Over the next 12 months, Wall Street expects Lockheed Martin’s full-year EPS of $21.49 to grow 37.7%.

8. Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

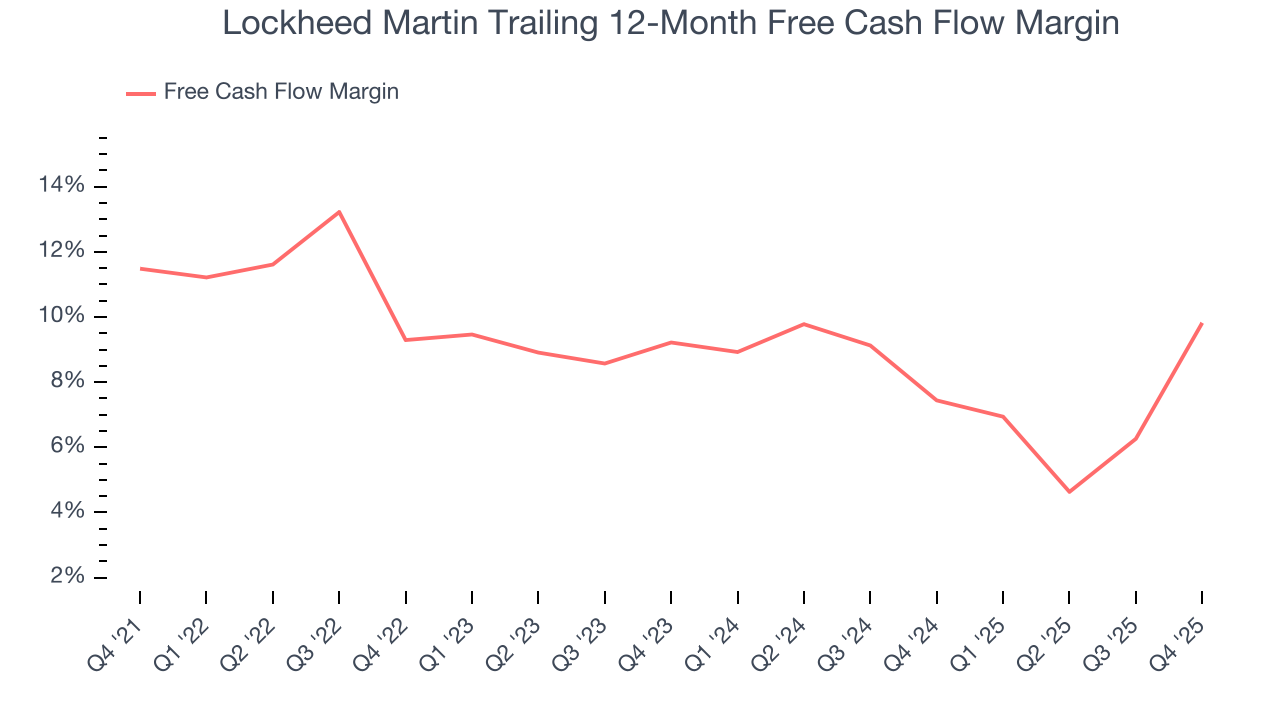

Lockheed Martin has shown impressive cash profitability, enabling it to ride out cyclical downturns more easily while maintaining its investments in new and existing offerings. The company’s free cash flow margin averaged 9.4% over the last five years, better than the broader industrials sector.

Taking a step back, we can see that Lockheed Martin’s margin dropped by 1.7 percentage points during that time. It may have ticked higher more recently, but shareholders are likely hoping for its margin to at least revert to its historical level. If the longer-term trend returns, it could signal it is in the middle of an investment cycle.

Lockheed Martin’s free cash flow clocked in at $3.22 billion in Q4, equivalent to a 15.8% margin. This result was good as its margin was 13.5 percentage points higher than in the same quarter last year, but we wouldn’t put too much weight on the short term because investment needs can be seasonal, causing temporary swings. Long-term trends are more important.

9. Return on Invested Capital (ROIC)

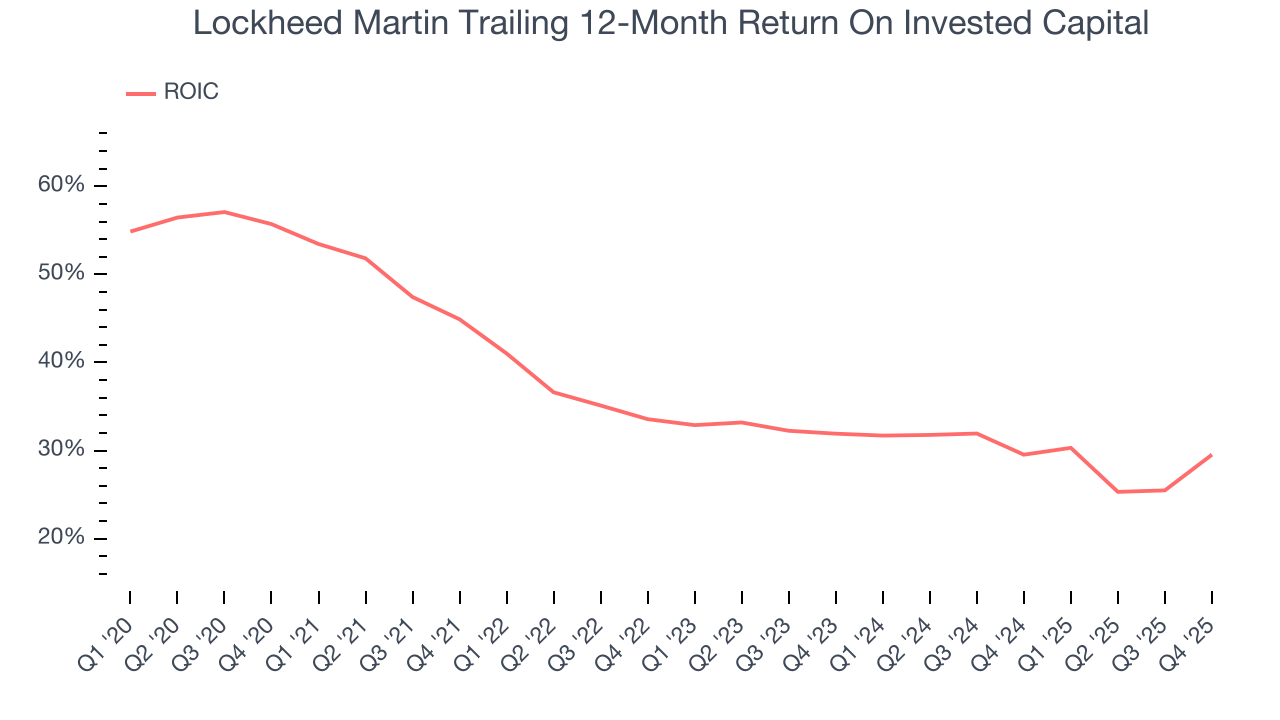

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Although Lockheed Martin hasn’t been the highest-quality company lately because of its poor revenue and EPS performance, it found a few growth initiatives in the past that worked out wonderfully. Its five-year average ROIC was 33.9%, splendid for an industrials business.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Over the last few years, Lockheed Martin’s ROIC has unfortunately decreased. We like what management has done in the past, but its declining returns are perhaps a symptom of fewer profitable growth opportunities.

10. Balance Sheet Assessment

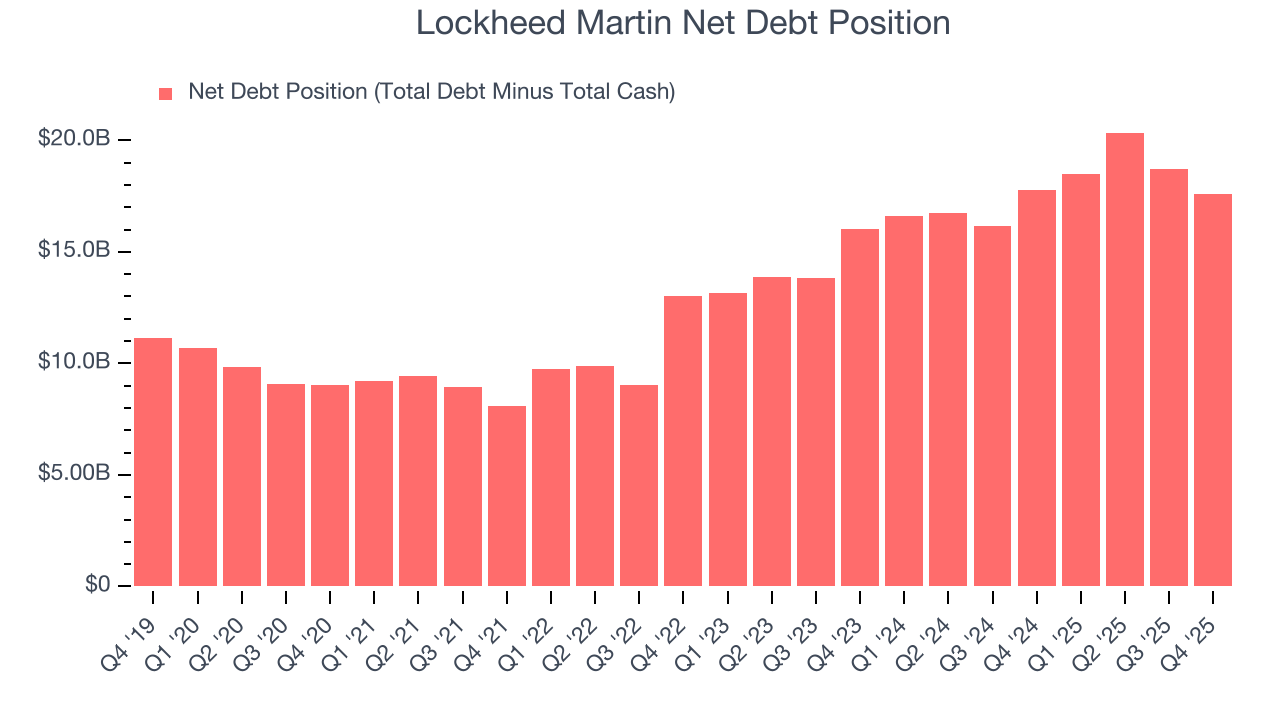

Lockheed Martin reported $4.12 billion of cash and $21.7 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $8.79 billion of EBITDA over the last 12 months, we view Lockheed Martin’s 2.0× net-debt-to-EBITDA ratio as safe. We also see its $538 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

11. Key Takeaways from Lockheed Martin’s Q4 Results

We were impressed by how significantly Lockheed Martin blew past analysts’ backlog expectations this quarter. We were also excited its EBITDA outperformed Wall Street’s estimates by a wide margin. Zooming out, we think this was a good print with some key areas of upside. The stock traded up 2.8% to $614.00 immediately following the results.

12. Is Now The Time To Buy Lockheed Martin?

Updated: March 30, 2026 at 11:46 PM EDT

Before investing in or passing on Lockheed Martin, we urge you to understand the company’s business quality (or lack thereof), valuation, and the latest quarterly results - in that order.

Lockheed Martin falls short of our quality standards. For starters, its revenue growth was weak over the last five years. While its projected EPS for the next year implies the company’s fundamentals will improve, the downside is its diminishing returns show management's prior bets haven't worked out. On top of that, its declining EPS over the last five years makes it a less attractive asset to the public markets.

Lockheed Martin’s P/E ratio based on the next 12 months is 20.6x. This valuation tells us it’s a bit of a market darling with a lot of good news priced in - you can find more timely opportunities elsewhere.

Wall Street analysts have a consensus one-year price target of $664.26 on the company (compared to the current share price of $597.98).