Shake Shack (SHAK)

We’re wary of Shake Shack. Its weak returns on capital indicate management was inefficient with its resources and missed opportunities.― StockStory Analyst Team

1. News

2. Summary

Why Shake Shack Is Not Exciting

Started as a hot dog cart in New York City's Madison Square Park, Shake Shack (NYSE:SHAK) is a fast-food restaurant known for its burgers and milkshakes.

- Underwhelming 0.1% return on capital reflects management’s difficulties in finding profitable growth opportunities

- Operating margin falls short of the industry average, and the smaller profit dollars make it harder to react to unexpected market developments

- Rapid rollout of new restaurants to capitalize on market opportunities makes sense given its strong same-store sales performance

Shake Shack doesn’t check our boxes. There are more profitable opportunities elsewhere.

Why There Are Better Opportunities Than Shake Shack

Shake Shack is trading at $87.33 per share, or 63.8x forward P/E. The current multiple is quite expensive, especially for the fundamentals of the business.

We prefer to invest in similarly-priced but higher-quality companies with superior earnings growth.

3. Shake Shack (SHAK) Research Report: Q4 CY2025 Update

Fast-food chain Shake Shack (NYSE:SHAK) met Wall Street’s revenue expectations in Q4 CY2025, with sales up 21.9% year on year to $400.5 million. Its non-GAAP profit of $0.37 per share was 6.1% above analysts’ consensus estimates.

Shake Shack (SHAK) Q4 CY2025 Highlights:

- Revenue: $400.5 million vs analyst estimates of $401.2 million (21.9% year-on-year growth, in line)

- Adjusted EPS: $0.37 vs analyst estimates of $0.35 (6.1% beat)

- Q1 guidance: same-store sales (+4% at the midpoint) and revenue guidance ($368 million at the midpoint) both beat expectations

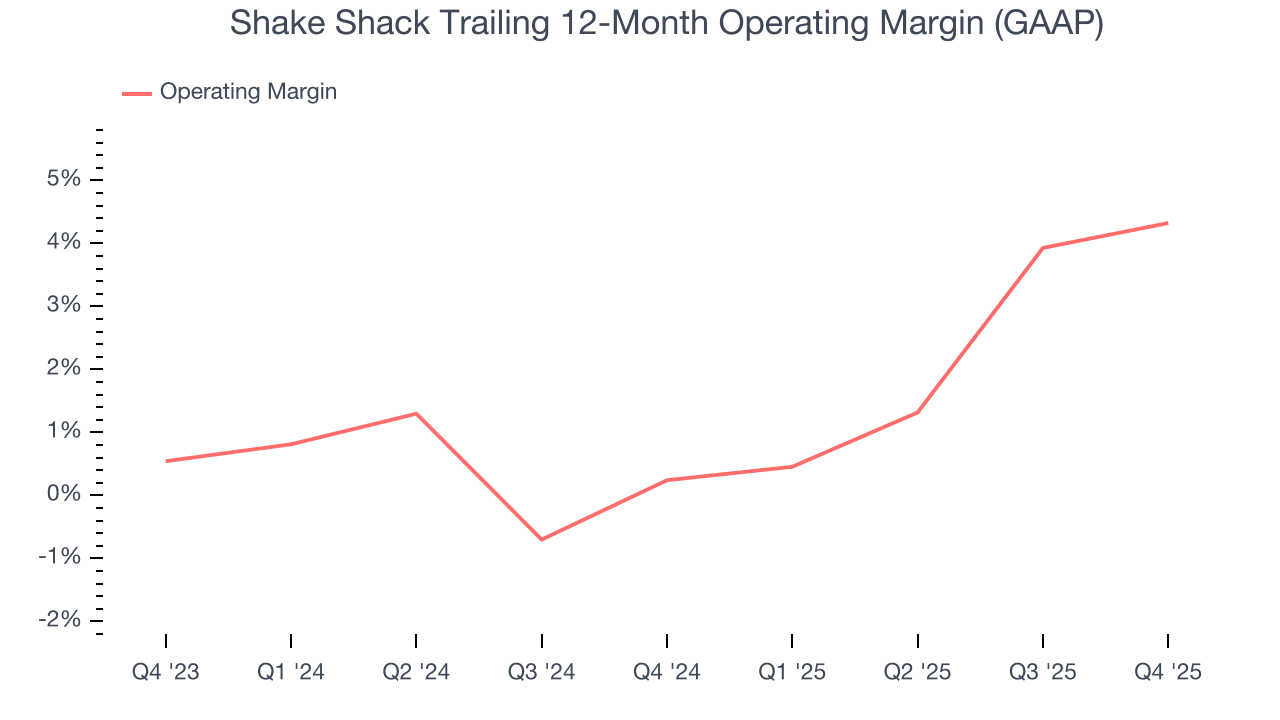

- Operating Margin: 4.7%, up from 3.1% in the same quarter last year

- Free Cash Flow Margin: 1%, down from 3.2% in the same quarter last year

- Locations: 670 at quarter end, up from 579 in the same quarter last year

- Same-Store Sales rose 2.1% year on year (4.3% in the same quarter last year)

- Market Capitalization: $3.71 billion

Company Overview

Started as a hot dog cart in New York City's Madison Square Park, Shake Shack (NYSE:SHAK) is a fast-food restaurant known for its burgers and milkshakes.

The company was founded in 2004 by Danny Meyer, an acclaimed restaurateur, who envisioned a concept of serving high-quality food made from premium ingredients. Although burgers are its most popular menu items, Shake Shack also offers french fries, hot dogs, chicken sandwiches, and milkshakes made with sustainably-sourced ingredients.

Shake Shack’s diehard fans will argue that the company’s burgers are the best in the business. Preparation is unique, using a "smash and sear" technique that involves quickly pressing a beef patty onto a hot griddle. This leads to caramelized edges while sealing in the juices.

Shake Shack primarily targets consumers who seek the convenience of fast food but with better ingredients and the halo of a famous restaurateur behind the brand. This target customer is therefore willing to pay more for their burgers, hot dogs, and fries compared to mainstream fast-food restaurants.

The average Shake Shack location has a sleek but inviting aesthetic, often incorporating elements of its humble hot dog cart beginnings. To respond to evolving customer demands, the company offers online ordering and delivery through third-party platforms such as DoorDash and Seamless (Grubhub).

4. Modern Fast Food

Modern fast food is a relatively newer category representing a middle ground between traditional fast food and sit-down restaurants. These establishments feature an expanded menu selection priced above traditional fast food options, often incorporating fresher and cleaner ingredients to serve customers prioritizing quality. These eateries are capitalizing on the perception that your drive-through burger and fries joint is detrimental to your health because of inferior ingredients.

Top competitors that also specialize in burgers include The Habit Burger Grill (owned by YUM! Brands, NYSE:YUM), Fatburger (owned by FAT Brands, NASDAQ:FAT), Burger King (owned by Restaurant Brands, NYSE:QSR), McDonald’s (NYSE:MCD), Wendy’s (NASDAQ:WEN), and Jack in the Box (NASDAQ:JACK).

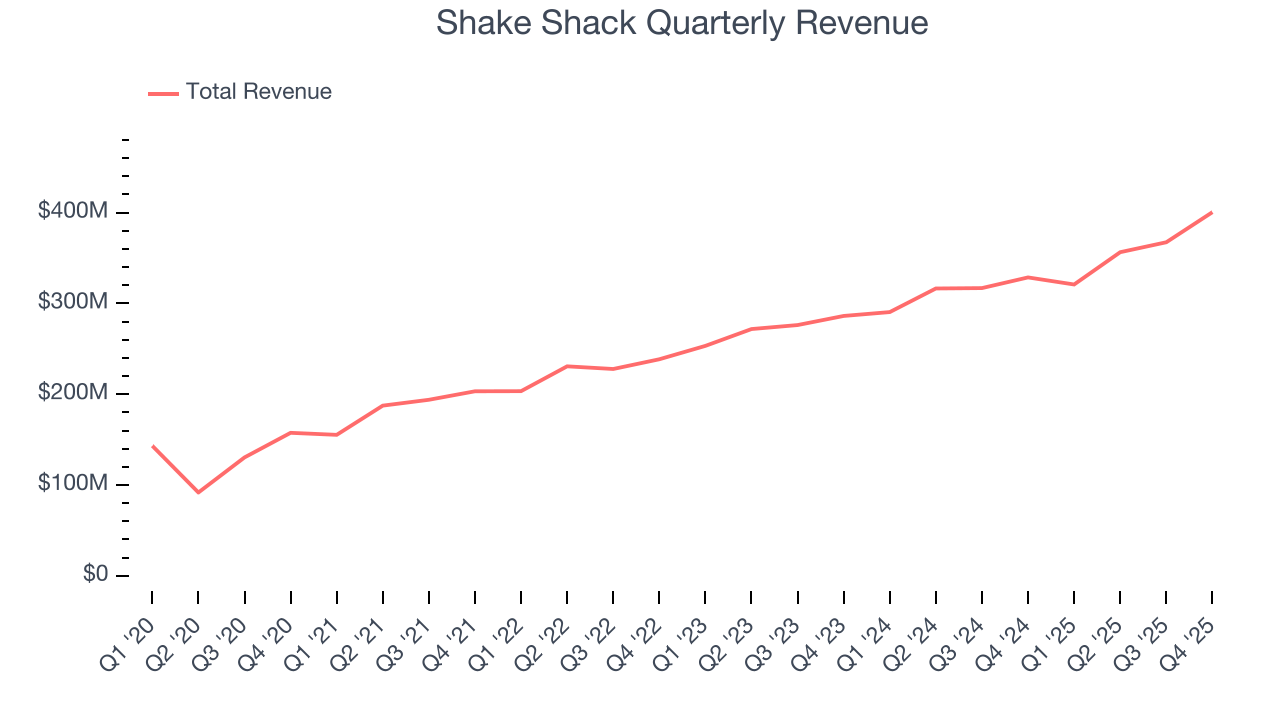

5. Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years.

With $1.45 billion in revenue over the past 12 months, Shake Shack is a mid-sized restaurant chain, which sometimes brings disadvantages compared to larger competitors benefiting from better brand awareness and economies of scale. On the bright side, it can still flex high growth rates because it’s working from a smaller revenue base.

As you can see below, Shake Shack’s 16% annualized revenue growth over the last six years was impressive as it opened new restaurants and increased sales at existing, established dining locations.

This quarter, Shake Shack’s year-on-year revenue growth of 21.9% was excellent, and its $400.5 million of revenue was in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 13.7% over the next 12 months, a slight deceleration versus the last six years. Still, this projection is healthy and suggests the market is forecasting success for its menu offerings.

6. Restaurant Performance

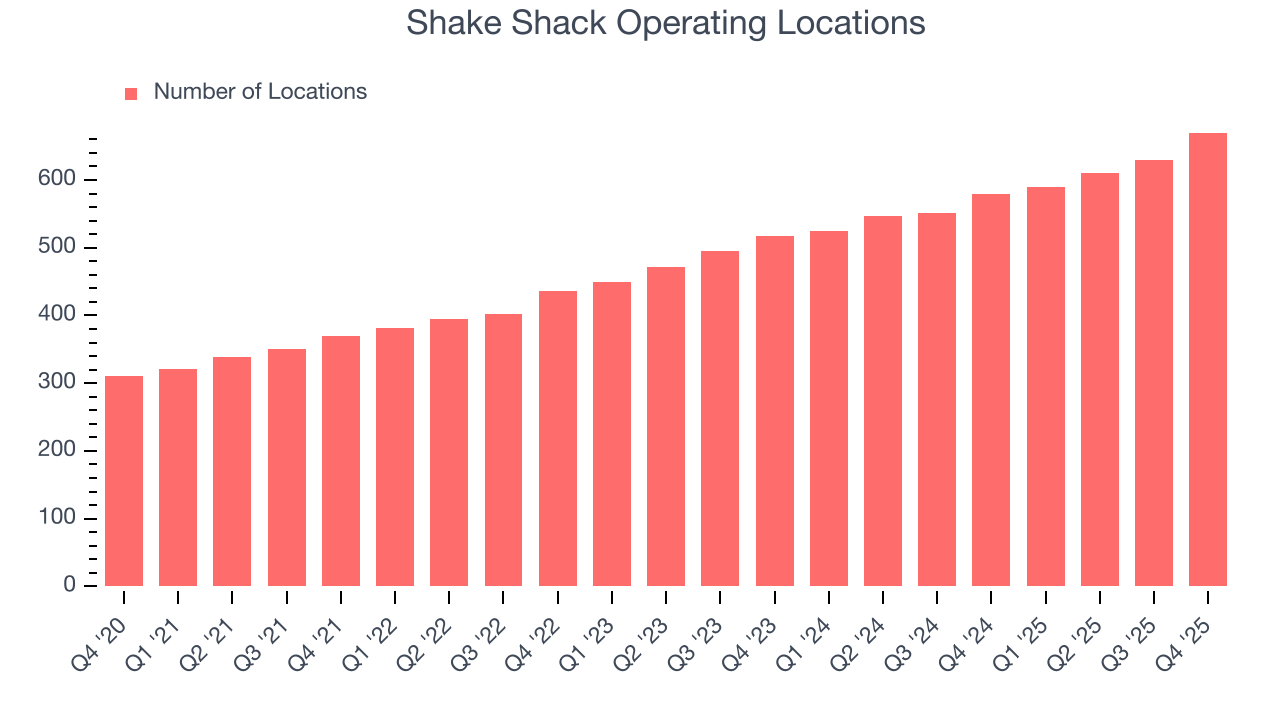

Number of Restaurants

Shake Shack sported 670 locations in the latest quarter. Over the last two years, it has opened new restaurants at a rapid clip by averaging 13.7% annual growth, among the fastest in the restaurant sector. This gives it a chance to become a large, scaled business over time.

When a chain opens new restaurants, it usually means it’s investing for growth because there’s healthy demand for its meals and there are markets where its concepts have few or no locations.

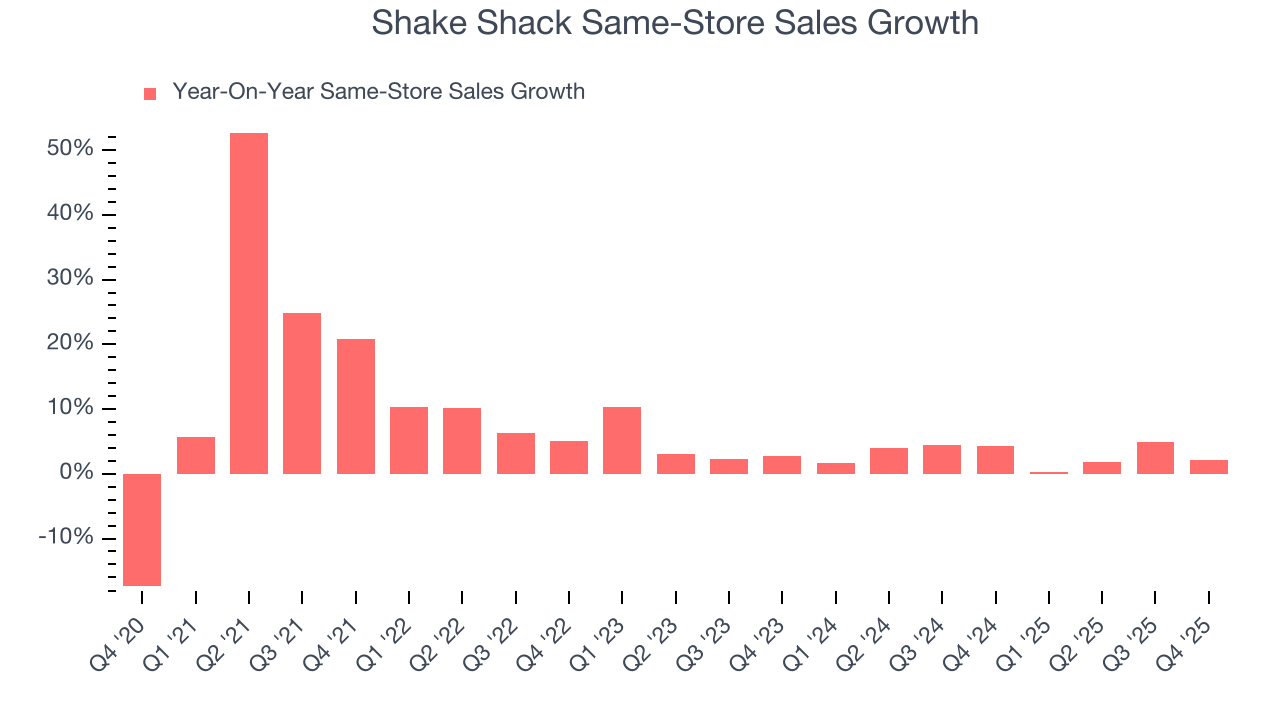

Same-Store Sales

The change in a company's restaurant base only tells one side of the story. The other is the performance of its existing locations, which informs management teams whether they should expand or downsize their physical footprints. Same-store sales gives us insight into this topic because it measures organic growth at restaurants open for at least a year.

Shake Shack’s demand has been healthy for a restaurant chain over the last two years. On average, the company has grown its same-store sales by a robust 2.9% per year. This performance gives it the confidence to meaningfully expand its restaurant base.

In the latest quarter, Shake Shack’s same-store sales rose 2.1% year on year. This performance was more or less in line with its historical levels.

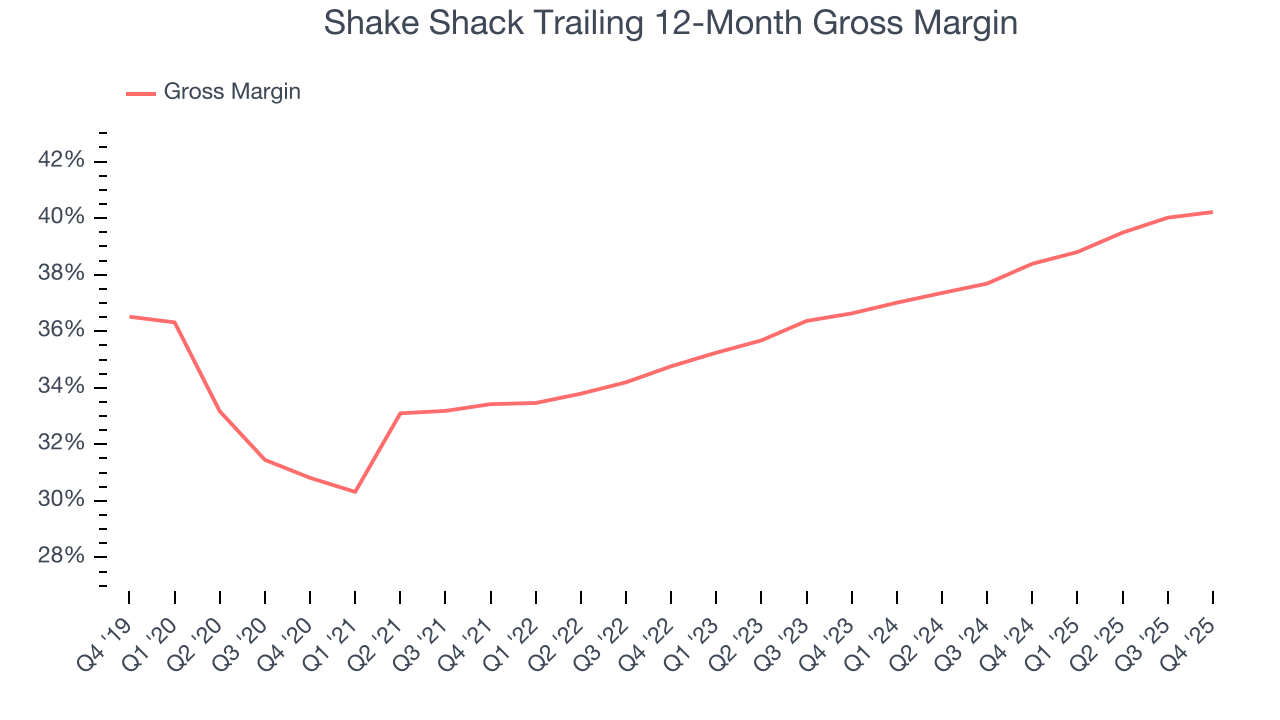

7. Gross Margin & Pricing Power

Gross profit margins tell us how much money a restaurant gets to keep after paying for the direct costs of the meals it sells, like ingredients, and indicate its level of pricing power.

Shake Shack has great unit economics for a restaurant company, giving it ample room to invest in areas such as marketing and talent to grow its brand. As you can see below, it averaged an excellent 39.4% gross margin over the last two years. Said differently, roughly $39.37 was left to spend on selling, marketing, and general administrative overhead for every $100 in revenue.

Shake Shack produced a 40.6% gross profit margin in Q4, in line with the same quarter last year. Zooming out, Shake Shack’s full-year margin has been trending up over the past 12 months, increasing by 1.8 percentage points. If this move continues, it could suggest better unit economics due to more leverage from its growing sales on the fixed portion of its cost of goods sold

8. Operating Margin

Shake Shack was profitable over the last two years but held back by its large cost base. Its average operating margin of 2.4% was weak for a restaurant business. This result is surprising given its high gross margin as a starting point.

On the plus side, Shake Shack’s operating margin rose by 4.1 percentage points over the last year, as its sales growth gave it immense operating leverage.

This quarter, Shake Shack generated an operating margin profit margin of 4.7%, up 1.6 percentage points year on year. The increase was encouraging, and because its operating margin rose more than its gross margin, we can infer it was more efficient with expenses such as marketing, and administrative overhead.

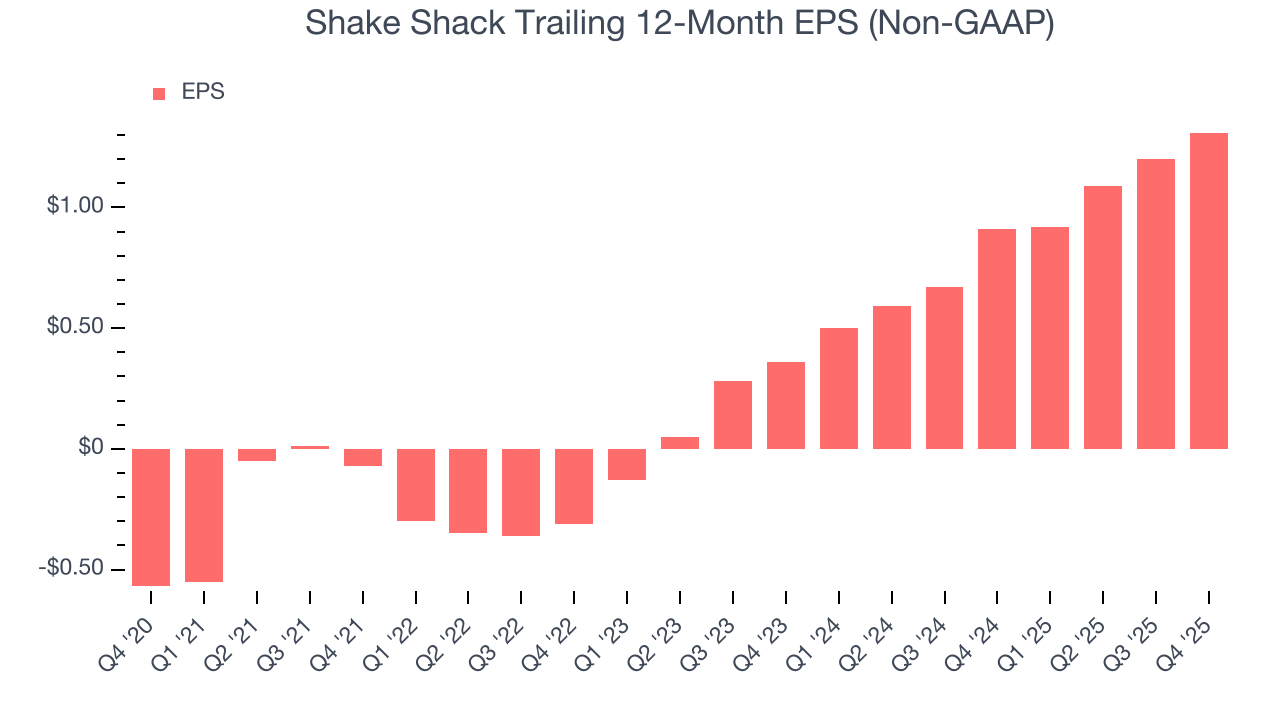

9. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Shake Shack’s EPS grew at a decent 10.5% compounded annual growth rate over the last six years. Despite its operating margin improvement during that time, this performance was lower than its 16% annualized revenue growth, telling us that non-fundamental factors such as interest and taxes affected its ultimate earnings.

In Q4, Shake Shack reported adjusted EPS of $0.37, up from $0.26 in the same quarter last year. This print beat analysts’ estimates by 6.1%. Over the next 12 months, Wall Street expects Shake Shack’s full-year EPS of $1.31 to grow 3%.

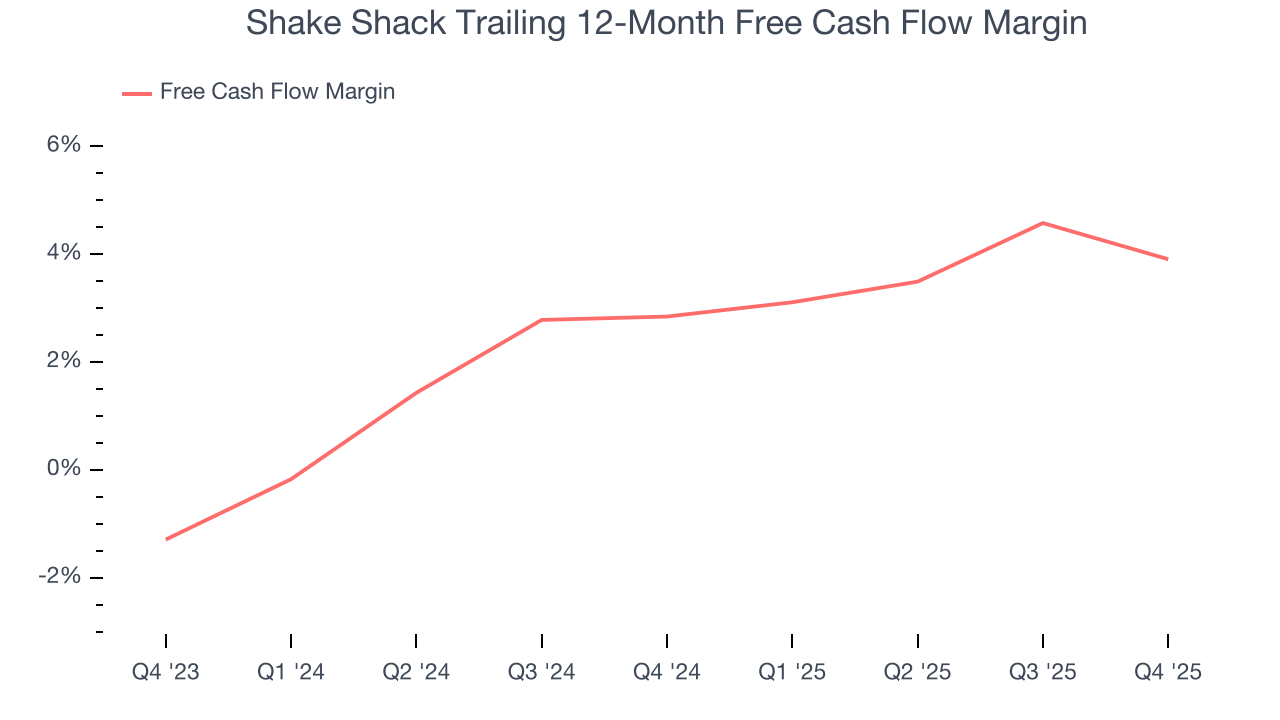

10. Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Shake Shack has shown decent cash profitability, giving it some flexibility to reinvest or return capital to investors. The company’s free cash flow margin averaged 3.4% over the last two years, slightly better than the broader restaurant sector.

Taking a step back, we can see that Shake Shack’s margin expanded by 1.1 percentage points over the last year. This is encouraging because it gives the company more optionality.

Shake Shack broke even from a free cash flow perspective in Q4. The company’s cash profitability regressed as it was 2.2 percentage points lower than in the same quarter last year, prompting us to pay closer attention. Short-term fluctuations typically aren’t a big deal because investment needs can be seasonal, but we’ll be watching to see if the trend extrapolates into future quarters.

11. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Shake Shack historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 0%, lower than the typical cost of capital (how much it costs to raise money) for restaurant companies.

12. Balance Sheet Assessment

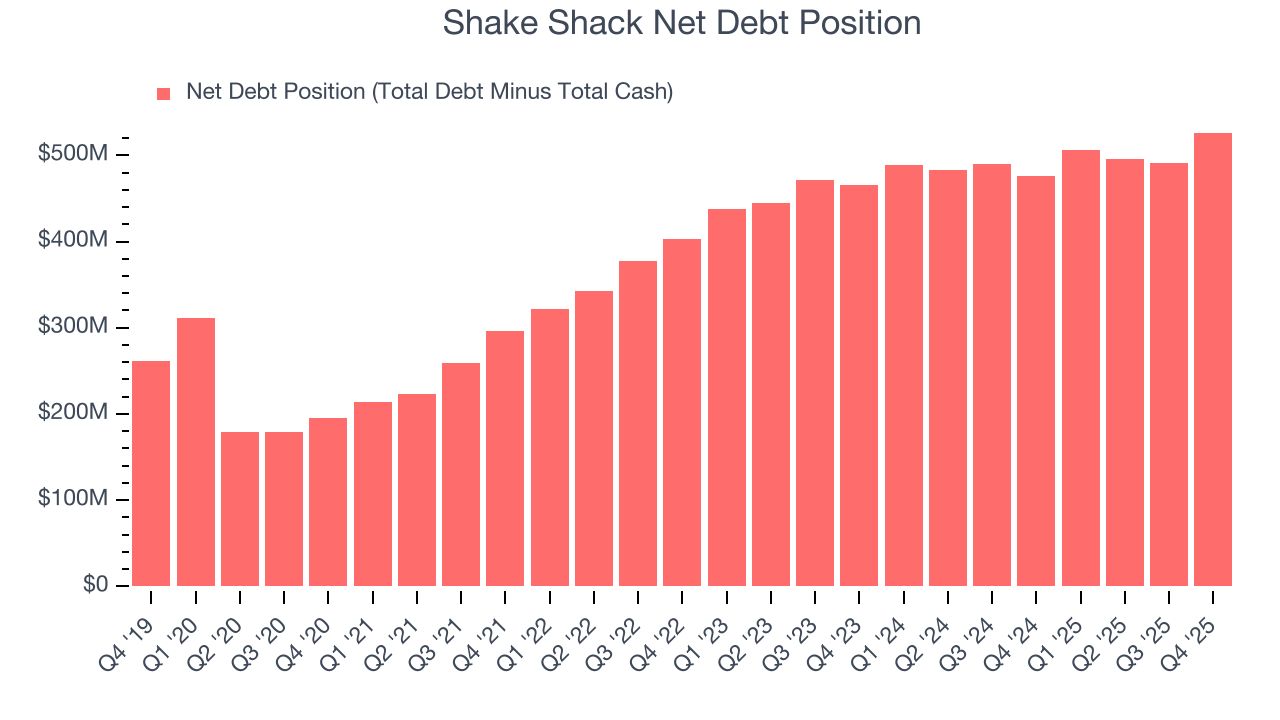

Shake Shack reported $360.1 million of cash and $886.4 million of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $209.9 million of EBITDA over the last 12 months, we view Shake Shack’s 2.5× net-debt-to-EBITDA ratio as safe. We also see its $1.02 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

13. Key Takeaways from Shake Shack’s Q4 Results

It was good to see Shake Shack beat analysts’ EPS expectations this quarter. Looking ahead, Q1 guidance for same-store sales and revenue also exceeded Wall Street's estimates. Zooming out, we think this was a decent quarter. The stock traded up 4% to $95.79 immediately after reporting.

14. Is Now The Time To Buy Shake Shack?

Updated: March 14, 2026 at 10:44 PM EDT

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in Shake Shack.

Shake Shack isn’t a terrible business, but it isn’t one of our picks. Although its revenue growth was impressive over the last six years, it’s expected to deteriorate over the next 12 months and its relatively low ROIC suggests management has struggled to find compelling investment opportunities. And while the company’s new restaurant openings have increased its brand equity, the downside is its projected EPS for the next year is lacking.

Shake Shack’s P/E ratio based on the next 12 months is 63.8x. This valuation tells us it’s a bit of a market darling with a lot of good news priced in - we think there are better opportunities elsewhere.

Wall Street analysts have a consensus one-year price target of $113.96 on the company (compared to the current share price of $87.33).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.