American Woodmark (AMWD)

American Woodmark is in for a bumpy ride. Its low returns on capital and plummeting sales suggest it struggles to generate demand and profits, a red flag.― StockStory Analyst Team

1. News

2. Summary

Why We Think American Woodmark Will Underperform

Starting as a small millwork shop, American Woodmark (NASDAQ:AMWD) is a cabinet manufacturing company that helps customers from inspiration to installation.

- Customers postponed purchases of its products and services this cycle as its revenue declined by 1.8% annually over the last five years

- Falling earnings per share over the last five years has some investors worried as stock prices ultimately follow EPS over the long term

- Sales are expected to decline once again over the next 12 months as it continues working through a challenging demand environment

American Woodmark’s quality isn’t up to par. We see more attractive opportunities in the market.

Why There Are Better Opportunities Than American Woodmark

American Woodmark’s stock price of $39.52 implies a valuation ratio of 26x forward P/E. This multiple is higher than that of industrials peers; it’s also rich for the top-line growth of the company. Not a great combination.

There are stocks out there featuring similar valuation multiples with better fundamentals. We prefer to invest in those.

3. American Woodmark (AMWD) Research Report: Q4 CY2025 Update

Cabinet manufacturing company American Woodmark (NASDAQ:AMWD) fell short of the market’s revenue expectations in Q4 CY2025, with sales falling 18.4% year on year to $324.3 million. Its non-GAAP profit of $0.45 per share was significantly above analysts’ consensus estimates.

American Woodmark (AMWD) Q4 CY2025 Highlights:

- Revenue: $324.3 million vs analyst estimates of $359.7 million (18.4% year-on-year decline, 9.8% miss)

- Adjusted EPS: $0.45 vs analyst estimates of $0.11 (significant beat)

- Adjusted EBITDA: $21.59 million vs analyst estimates of $23.67 million (6.7% margin, 8.8% miss)

- Operating Margin: -10.4%, down from 5.3% in the same quarter last year

- Free Cash Flow was -$21.88 million, down from $1.35 million in the same quarter last year

- Market Capitalization: $757 million

Company Overview

Starting as a small millwork shop, American Woodmark (NASDAQ:AMWD) is a cabinet manufacturing company that helps customers from inspiration to installation.

The company specializes in the design, manufacture, and distribution of kitchen cabinets and vanities for new home construction markets and home renovations. Its products are available through a variety of channels, including home centers, builders, and independent dealers and distributors, catering to a wide customer base.

Its product offerings include kitchen cabinetry, bath cabinetry, office cabinetry, home organization cabinetry, and cabinetry hardware. All of these types of cabinetry are then offered in a variety of designs, finishes, finish colors, and door styles. Its products are available in made-to-order styles (AKA customizable) and stock styles.

Most of the company’s sales are generated through its cabinetry and related product offerings. Its net sales are divided into three categories: sales to home centers such as The Home Depot and Lowes, builders, and independent dealers & distributors. Home center sales generate most of the company’s revenue, with The Home Depot being its top customer. Service revenue from the installation of its products also makes up a portion of its revenue, as the company operates eight strategically placed service centers across the US.

4. Home Construction Materials

Traditionally, home construction materials companies have built economic moats with expertise in specialized areas, brand recognition, and strong relationships with contractors. More recently, advances to address labor availability and job site productivity have spurred innovation that is driving incremental demand. However, these companies are at the whim of residential construction volumes, which tend to be cyclical and can be impacted heavily by economic factors such as interest rates. Additionally, the costs of raw materials can be driven by a myriad of worldwide factors and greatly influence the profitability of home construction materials companies.

Other companies in the cabinetry market include Masco (NYSE:MAS), Fortune Brands Home & Security (NYSE:FBHS), and private company MasterBrand Cabinets.

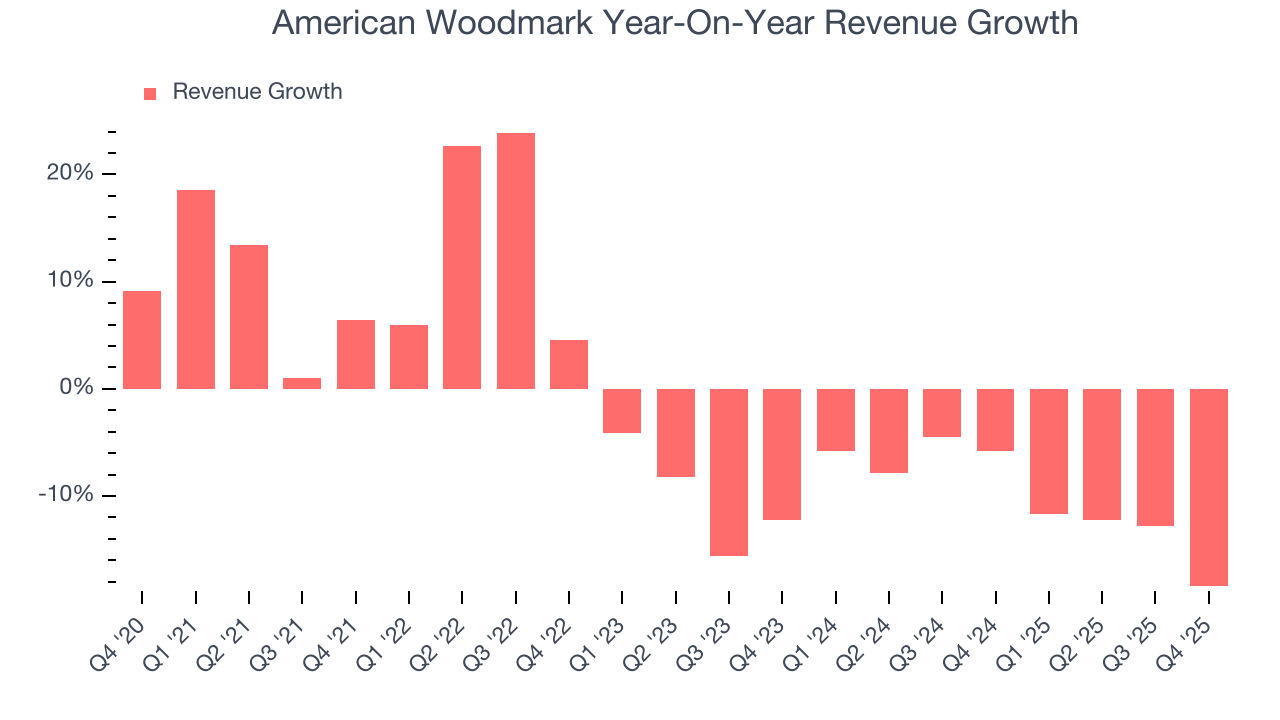

5. Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last five years, American Woodmark’s demand was weak and its revenue declined by 1.8% per year. This wasn’t a great result and is a sign of poor business quality.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. American Woodmark’s recent performance shows its demand remained suppressed as its revenue has declined by 9.9% annually over the last two years.

This quarter, American Woodmark missed Wall Street’s estimates and reported a rather uninspiring 18.4% year-on-year revenue decline, generating $324.3 million of revenue.

Looking ahead, sell-side analysts expect revenue to remain flat over the next 12 months. Although this projection suggests its newer products and services will fuel better top-line performance, it is still below the sector average.

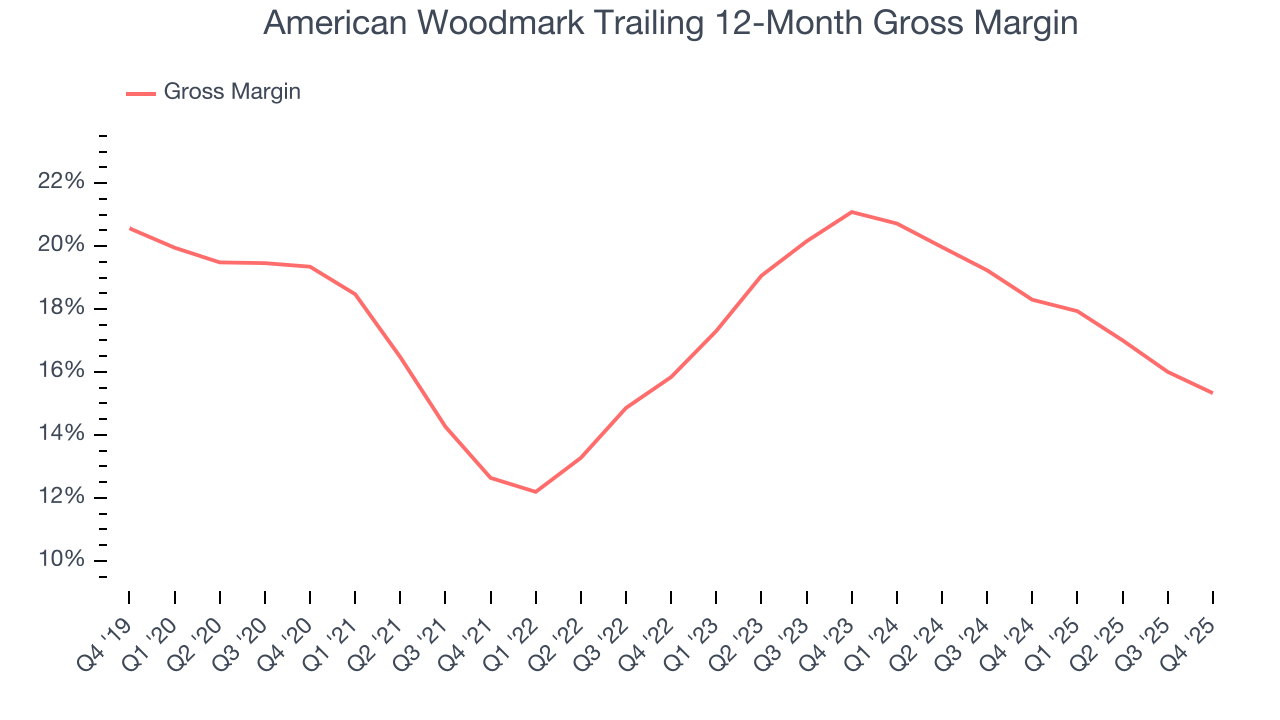

6. Gross Margin & Pricing Power

American Woodmark has bad unit economics for an industrials business, signaling it operates in a competitive market. As you can see below, it averaged a 16.7% gross margin over the last five years. Said differently, American Woodmark had to pay a chunky $83.33 to its suppliers for every $100 in revenue.

In Q4, American Woodmark produced a 11.6% gross profit margin , marking a 3.4 percentage point decrease from 15% in the same quarter last year. American Woodmark’s full-year margin has also been trending down over the past 12 months, decreasing by 3 percentage points. If this move continues, it could suggest a more competitive environment with some pressure to lower prices and higher input costs (such as raw materials and manufacturing expenses).

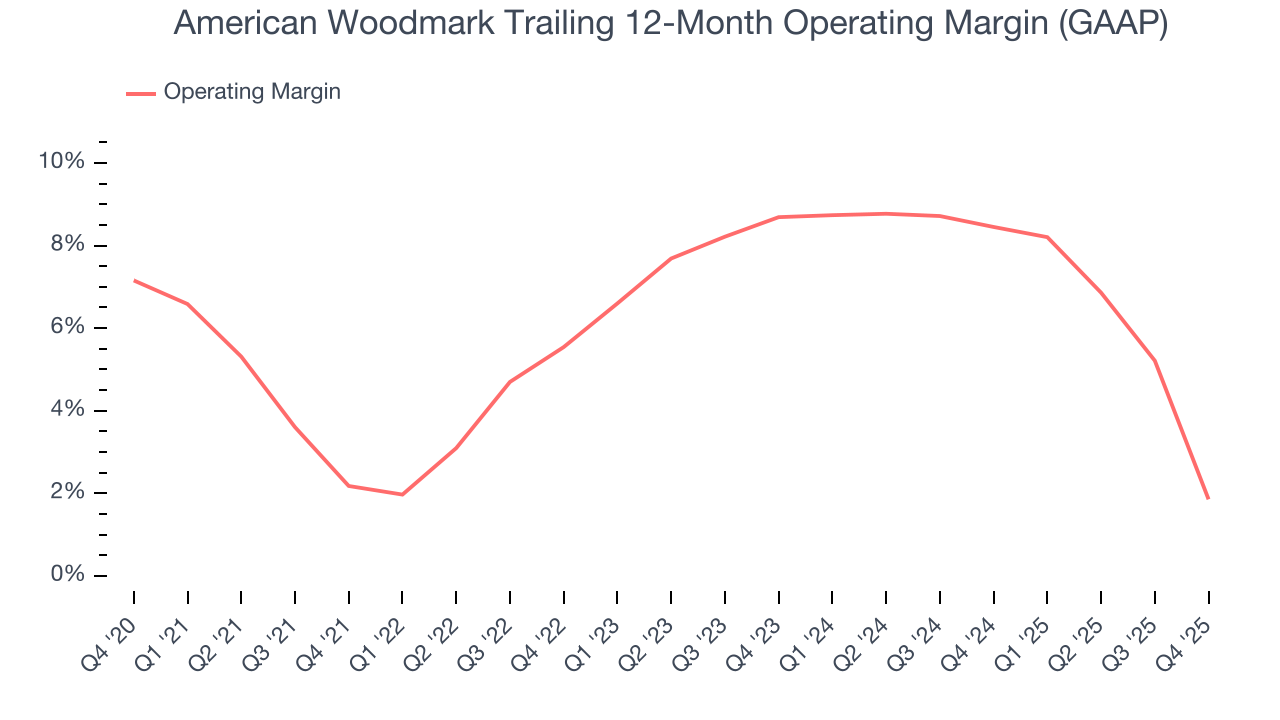

7. Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

American Woodmark’s operating margin might fluctuated slightly over the last 12 months but has generally stayed the same, averaging 5.5% over the last five years. This profitability was paltry for an industrials business and caused by its suboptimal cost structureand low gross margin.

Analyzing the trend in its profitability, American Woodmark’s operating margin might fluctuated slightly but has generally stayed the same over the last five years, which doesn’t help its cause.

This quarter, American Woodmark generated an operating margin profit margin of negative 10.4%, down 15.7 percentage points year on year. Since American Woodmark’s operating margin decreased more than its gross margin, we can assume it was less efficient because expenses such as marketing, R&D, and administrative overhead increased.

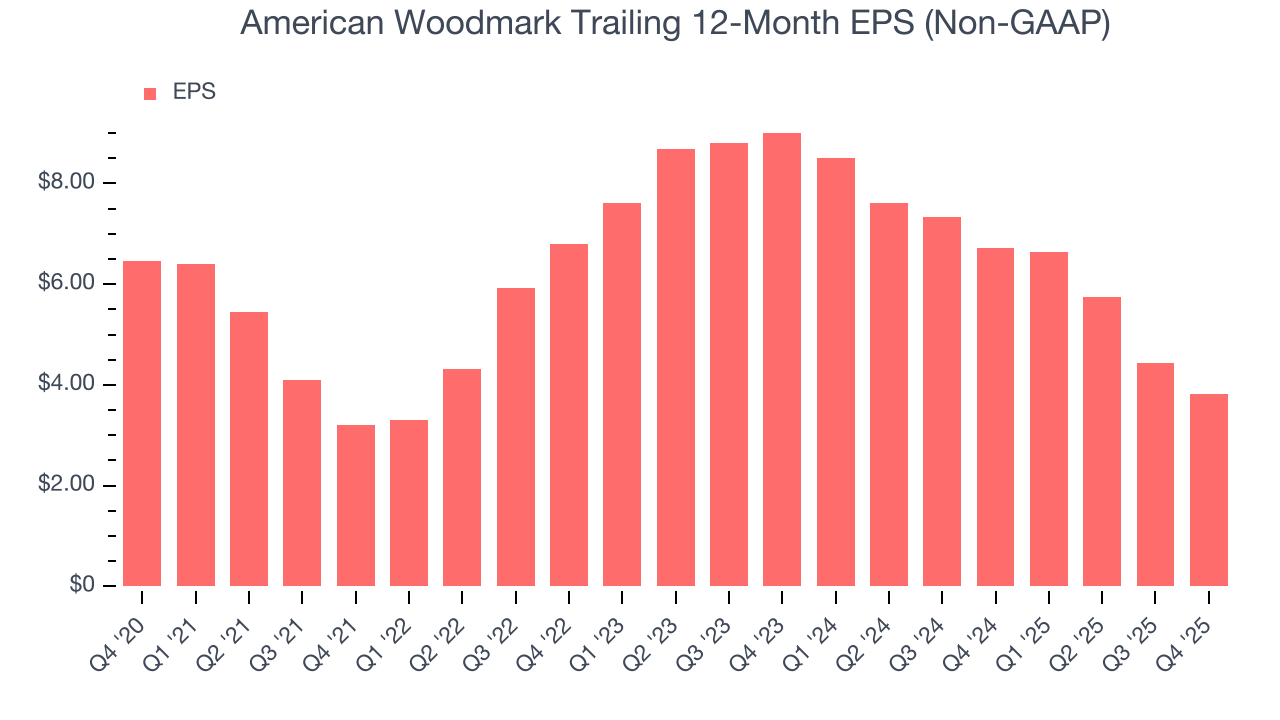

8. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Sadly for American Woodmark, its EPS declined by 9.9% annually over the last five years, more than its revenue. This tells us the company struggled because its fixed cost base made it difficult to adjust to shrinking demand.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For American Woodmark, its two-year annual EPS declines of 34.8% show it’s continued to underperform. These results were bad no matter how you slice the data.

In Q4, American Woodmark reported adjusted EPS of $0.45, down from $1.05 in the same quarter last year. Despite falling year on year, this print easily cleared analysts’ estimates. Over the next 12 months, Wall Street expects American Woodmark’s full-year EPS of $3.83 to shrink by 43.8%.

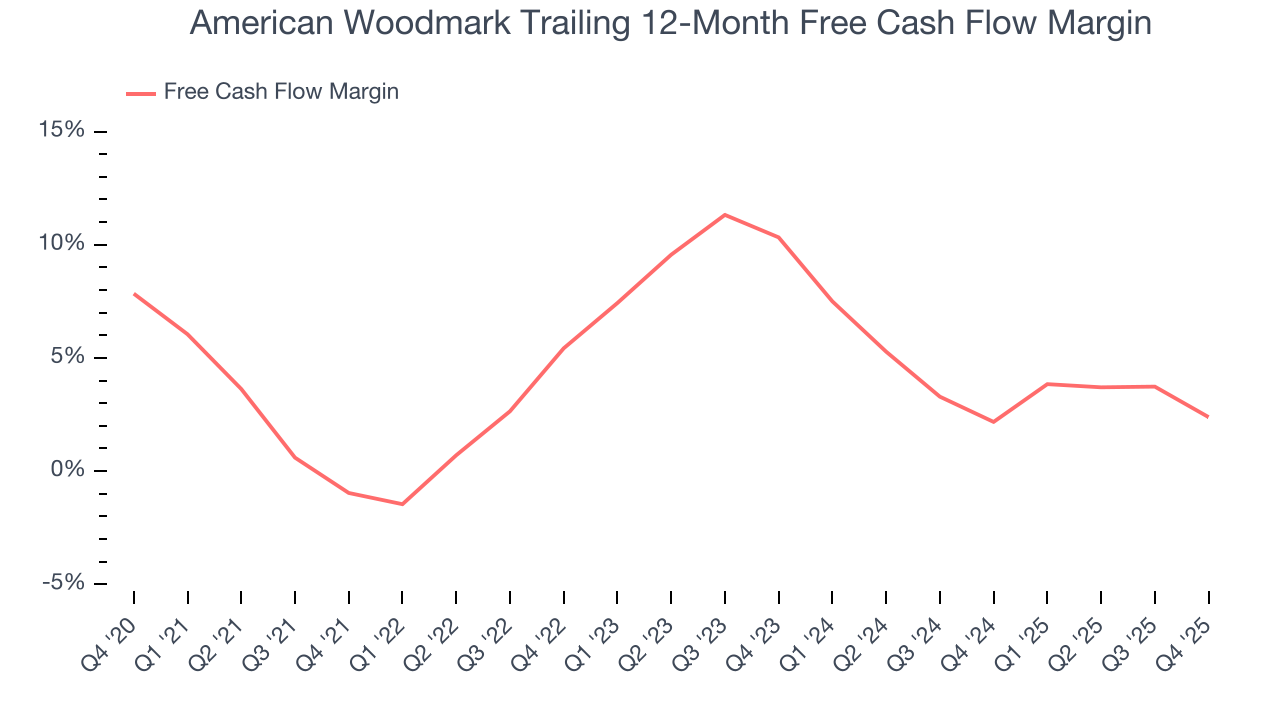

9. Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

American Woodmark has shown weak cash profitability over the last five years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 4%, subpar for an industrials business.

Taking a step back, an encouraging sign is that American Woodmark’s margin expanded by 3.4 percentage points during that time. The company’s improvement shows it’s heading in the right direction, and we can see it became a less capital-intensive business because its free cash flow profitability rose while its operating profitability was flat.

American Woodmark burned through $21.88 million of cash in Q4, equivalent to a negative 6.7% margin. The company’s cash burn increased meaningfully year on year and is a deviation from its longer-term margin, indicating it is a seasonal business that must build up inventory during certain quarters.

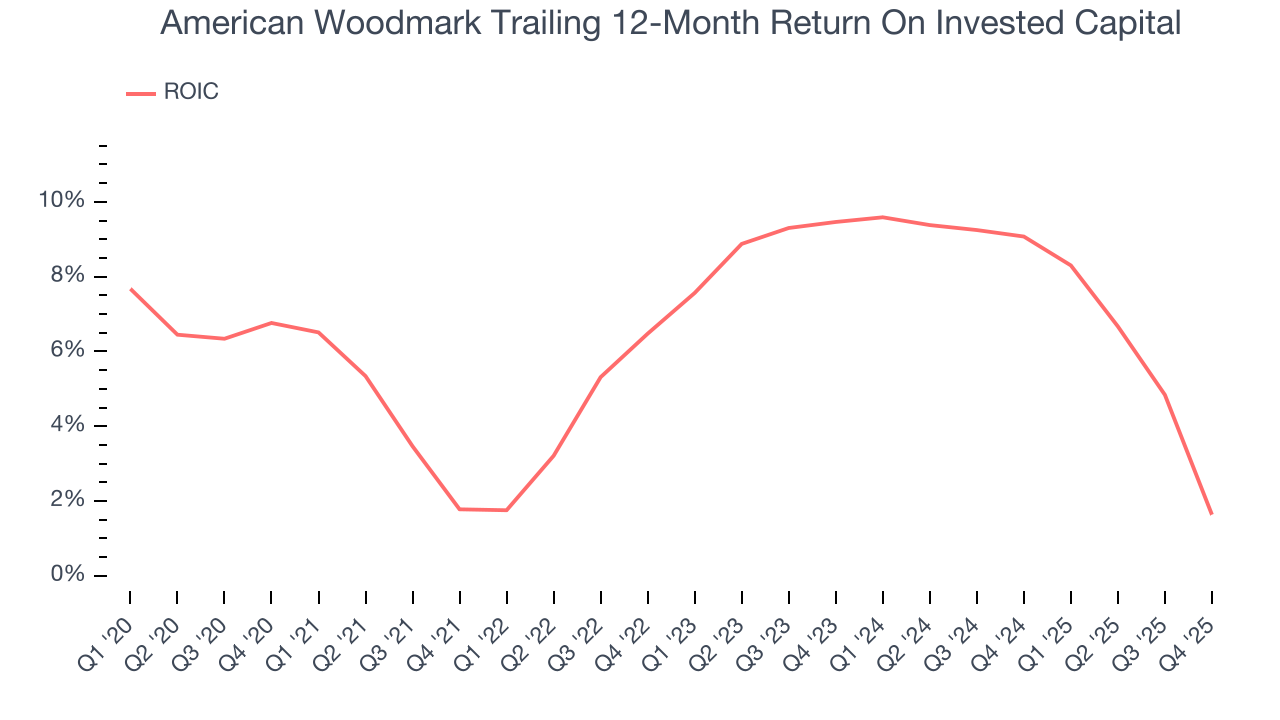

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

American Woodmark historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 5.7%, somewhat low compared to the best industrials companies that consistently pump out 20%+.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. On average, American Woodmark’s ROIC increased by 1.2 percentage points annually each year over the last few years. This is a good sign, and we hope the company can continue improving.

11. Balance Sheet Assessment

American Woodmark reported $28.26 million of cash and $483.7 million of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $150.6 million of EBITDA over the last 12 months, we view American Woodmark’s 3.0× net-debt-to-EBITDA ratio as safe. We also see its $7.78 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

12. Key Takeaways from American Woodmark’s Q4 Results

It was good to see American Woodmark beat analysts’ EPS expectations this quarter. On the other hand, its revenue missed and its EBITDA fell short of Wall Street’s estimates. Overall, this was a softer quarter. The stock remained flat at $51.66 immediately following the results.

13. Is Now The Time To Buy American Woodmark?

Updated: March 17, 2026 at 12:13 AM EDT

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in American Woodmark.

We cheer for all companies making their customers lives easier, but in the case of American Woodmark, we’ll be cheering from the sidelines. First off, its revenue has declined over the last five years, and analysts expect its demand to deteriorate over the next 12 months. While its rising cash profitability gives it more optionality, the downside is its projected EPS for the next year is lacking. On top of that, its declining EPS over the last five years makes it a less attractive asset to the public markets.

American Woodmark’s P/E ratio based on the next 12 months is 26x. This valuation tells us it’s a bit of a market darling with a lot of good news priced in - you can find more timely opportunities elsewhere.

Wall Street analysts have a consensus one-year price target of $59 on the company (compared to the current share price of $39.52).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.