Arhaus (ARHS)

We’re skeptical of Arhaus. Its poor sales growth and falling returns on capital suggest its growth opportunities are shrinking.― StockStory Analyst Team

1. News

2. Summary

Why We Think Arhaus Will Underperform

With an aesthetic that features natural materials such as reclaimed wood, Arhaus (NASDAQ:ARHS) is a high-end furniture retailer that sells everything from sofas to rugs to bookcases.

- Disappointing same-store sales over the past two years show customers aren’t responding well to its product selection and store experience

- Smaller revenue base of $1.38 billion means it hasn’t achieved the economies of scale that some industry juggernauts enjoy

- A consolation is that its ROIC punches in at 36%, illustrating management’s expertise in identifying profitable investments

Arhaus’s quality is lacking. You should search for better opportunities.

Why There Are Better Opportunities Than Arhaus

At $7.71 per share, Arhaus trades at 15.4x forward P/E. This valuation is fair for the quality you get, but we’re on the sidelines for now.

There are stocks out there featuring similar valuation multiples with better fundamentals. We prefer to invest in those.

3. Arhaus (ARHS) Research Report: Q4 CY2025 Update

Luxury furniture retailer Arhaus (NASDAQ:ARHS) beat Wall Street’s revenue expectations in Q4 CY2025, with sales up 5.1% year on year to $364.8 million. On the other hand, next quarter’s revenue guidance of $310 million was less impressive, coming in 5% below analysts’ estimates. Its GAAP profit of $0.11 per share was 15.8% above analysts’ consensus estimates.

Arhaus (ARHS) Q4 CY2025 Highlights:

- Revenue: $364.8 million vs analyst estimates of $350.6 million (5.1% year-on-year growth, 4.1% beat)

- EPS (GAAP): $0.11 vs analyst estimates of $0.10 (15.8% beat)

- Adjusted EBITDA: $34.98 million vs analyst estimates of $32.41 million (9.6% margin, 7.9% beat)

- Revenue Guidance for Q1 CY2026 is $310 million at the midpoint, below analyst estimates of $326.4 million

- EBITDA guidance for the upcoming financial year 2026 is $155.5 million at the midpoint, above analyst estimates of $152.4 million

- Operating Margin: 5.6%, down from 8.2% in the same quarter last year

- Free Cash Flow was -$8.81 million, down from $13 million in the same quarter last year

- Locations: 107 at quarter end, up from 103 in the same quarter last year

- Same-Store Sales fell 2.8% year on year (-6.4% in the same quarter last year)

- Market Capitalization: $1.18 billion

Company Overview

With an aesthetic that features natural materials such as reclaimed wood, Arhaus (NASDAQ:ARHS) is a high-end furniture retailer that sells everything from sofas to rugs to bookcases.

The Arhaus core customer is affluent and values quality and a style that is not cookie-cutter. Arhaus’s aesthetic can be described as having rich, warm finishes and textures, such as handcrafted woodwork, natural stone, and organic fabrics. Some products are hand-crafted or one-of-a-kind, which speaks to customers who value uniqueness. The company also offers a range of eco-friendly products such as reclaimed wood products and other recycled materials for the customer who is especially concerned about the environment.

The average Arhaus store is around 20,000 square feet in size and is typically located in upscale shopping centers or lifestyle centers alongside other luxury brands. The stores are designed to feel like a home, with cozy seating areas and a relaxed, inviting atmosphere where customers are free to lounge and experience the products directly. Arhaus also has an e-commerce platform, launched in 2005, allowing customers to shop online and have products delivered directly to their homes. The company’s online platform also offers virtual design consultations.

4. Home Furniture Retailer

Furniture retailers understand that ‘home is where the heart is’ but that no home is complete without that comfy sofa to kick back on or a dreamy bed to rest in. These stores focus on providing not only what is practically needed in a house but also aesthetics, style, and charm in the form of tables, lamps, and mirrors. Decades ago, it was thought that furniture would resist e-commerce because of the logistical challenges of shipping large furniture, but now you can buy a mattress online and get it in a box a few days later; so just like other retailers, furniture stores need to adapt to new realities and consumer behaviors.

Competitors offering higher-end furniture include public companies Restoration Hardware (NYSE:RH), MillerKnoll (NASDAQ:MLKN), and Williams Sonoma (NYSE:WSM). Private company West Elm is also a competitor.

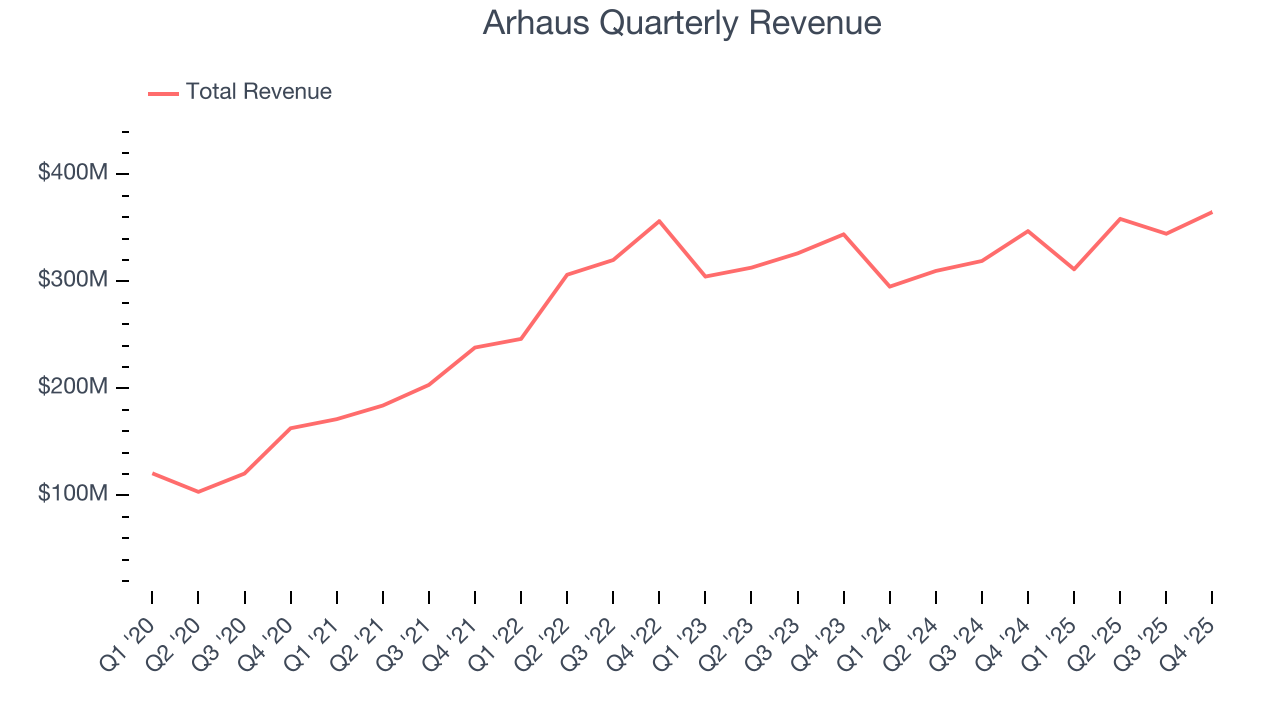

5. Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but many enduring ones grow for years.

With $1.38 billion in revenue over the past 12 months, Arhaus is a small retailer, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage with suppliers.

As you can see below, Arhaus’s 3.9% annualized revenue growth over the last three years was sluggish.

This quarter, Arhaus reported year-on-year revenue growth of 5.1%, and its $364.8 million of revenue exceeded Wall Street’s estimates by 4.1%. Company management is currently guiding for flat sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 4.8% over the next 12 months, similar to its three-year rate. This projection is commendable and indicates the market is forecasting success for its products.

6. Store Performance

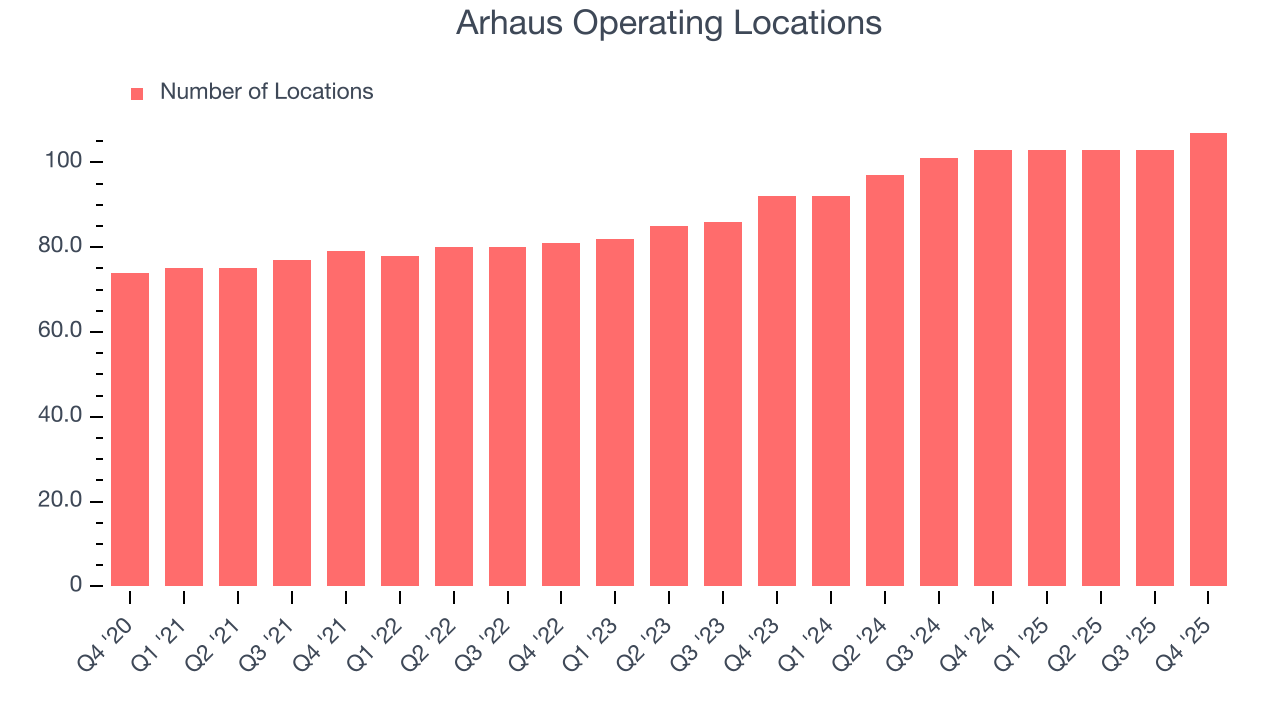

Number of Stores

A retailer’s store count influences how much it can sell and how quickly revenue can grow.

Arhaus operated 107 locations in the latest quarter. It has opened new stores at a rapid clip over the last two years, averaging 10% annual growth, much faster than the broader consumer retail sector. This gives it a chance to scale into a mid-sized business over time.

When a retailer opens new stores, it usually means it’s investing for growth because demand is greater than supply, especially in areas where consumers may not have a store within reasonable driving distance.

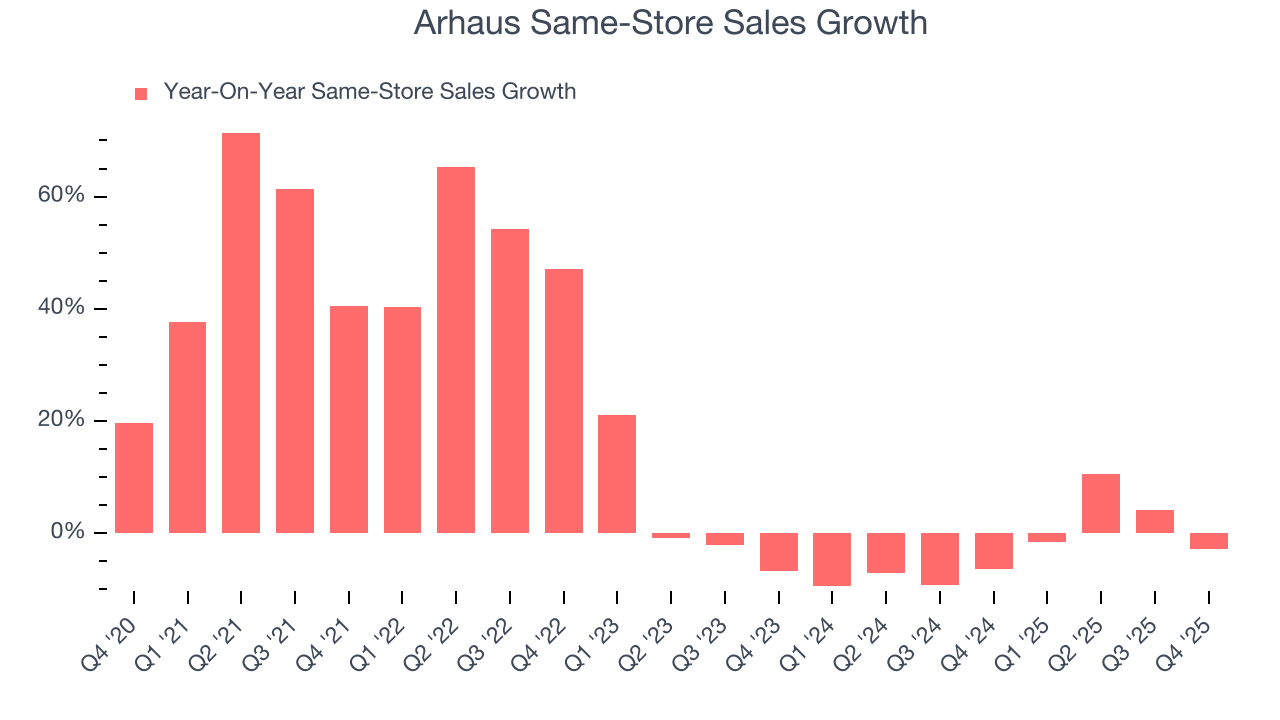

Same-Store Sales

A company's store base only paints one part of the picture. When demand is high, it makes sense to open more. But when demand is low, it’s prudent to close some locations and use the money in other ways. Same-store sales is an industry measure of whether revenue is growing at those existing stores and is driven by customer visits (often called traffic) and the average spending per customer (ticket).

Arhaus’s demand has been shrinking over the last two years as its same-store sales have averaged 2.7% annual declines. This performance is concerning - it shows Arhaus artificially boosts its revenue by building new stores. We’d like to see a company’s same-store sales rise before it takes on the costly, capital-intensive endeavor of expanding its store base.

In the latest quarter, Arhaus’s same-store sales fell by 2.8% year on year. This performance was more or less in line with its historical levels.

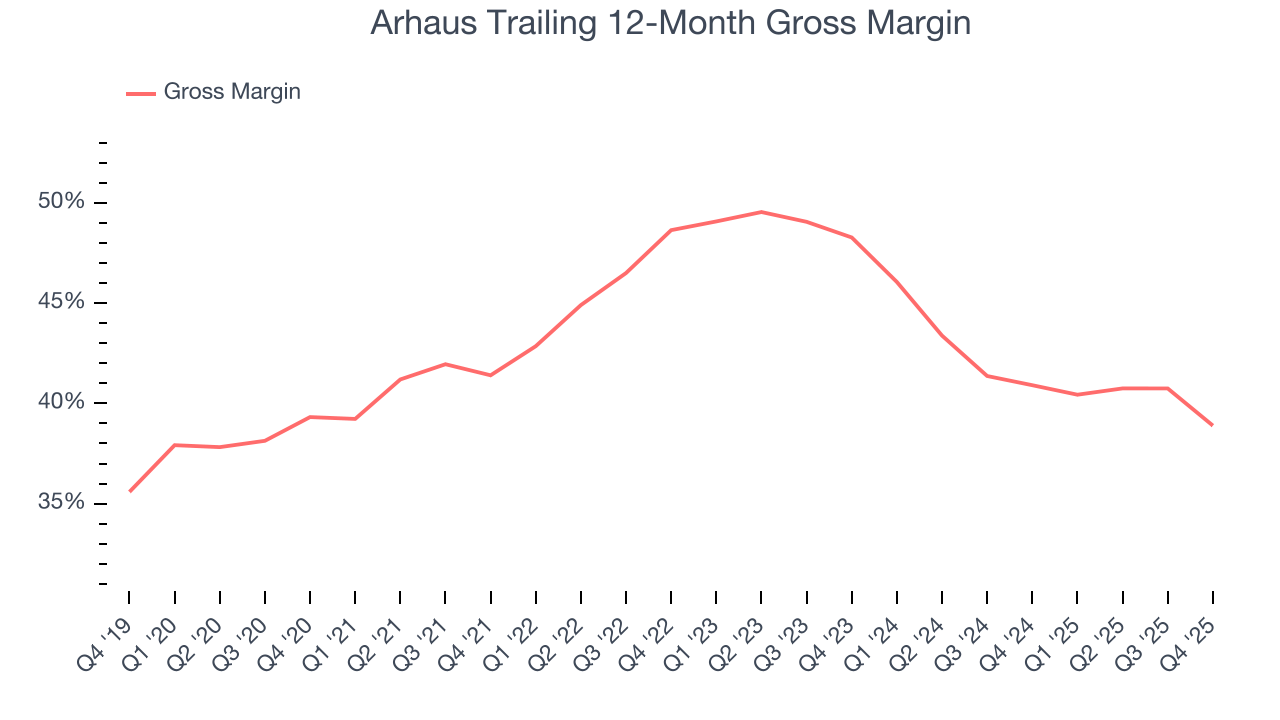

7. Gross Margin & Pricing Power

Arhaus’s gross margin is slightly below the average retailer, giving it less room to invest in areas such as marketing and talent to grow its brand. As you can see below, it averaged a 39.9% gross margin over the last two years. That means Arhaus paid its suppliers a lot of money ($60.14 for every $100 in revenue) to run its business.

In Q4, Arhaus produced a 38.1% gross profit margin , marking a 7.2 percentage point decrease from 45.4% in the same quarter last year. Arhaus’s full-year margin has also been trending down over the past 12 months, decreasing by 2 percentage points. If this move continues, it could suggest a more competitive environment with some pressure to discount products and higher input costs (such as labor and freight expenses to transport goods).

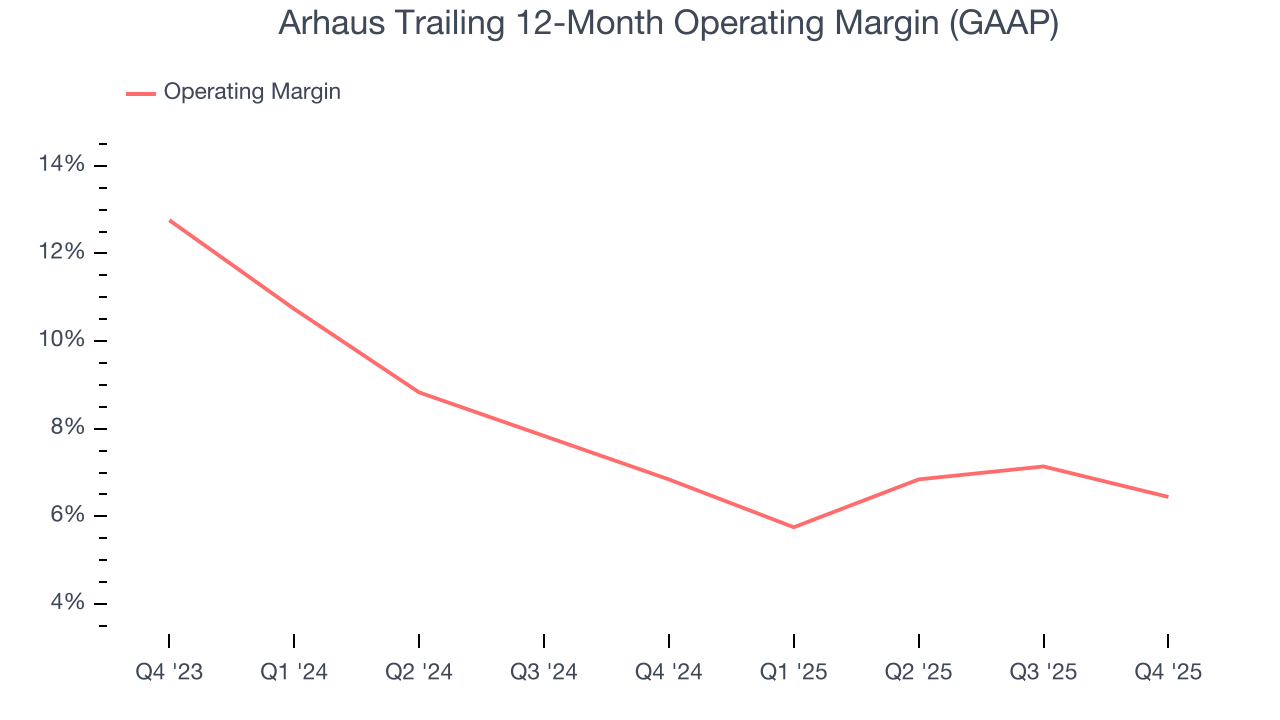

8. Operating Margin

Operating margin is an important measure of profitability for retailers as it accounts for all expenses necessary to run a store, including wages, inventory, rent, advertising, and other administrative costs.

Arhaus’s operating margin might fluctuated slightly over the last 12 months but has remained more or less the same, averaging 6.6% over the last two years. This profitability was mediocre for a consumer retail business and caused by its suboptimal cost structureand low gross margin.

Looking at the trend in its profitability, Arhaus’s operating margin might fluctuated slightly but has generally stayed the same over the last year. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

In Q4, Arhaus generated an operating margin profit margin of 5.6%, down 2.7 percentage points year on year. Since Arhaus’s gross margin decreased more than its operating margin, we can assume its recent inefficiencies were driven more by weaker leverage on its cost of sales rather than increased marketing, and administrative overhead expenses.

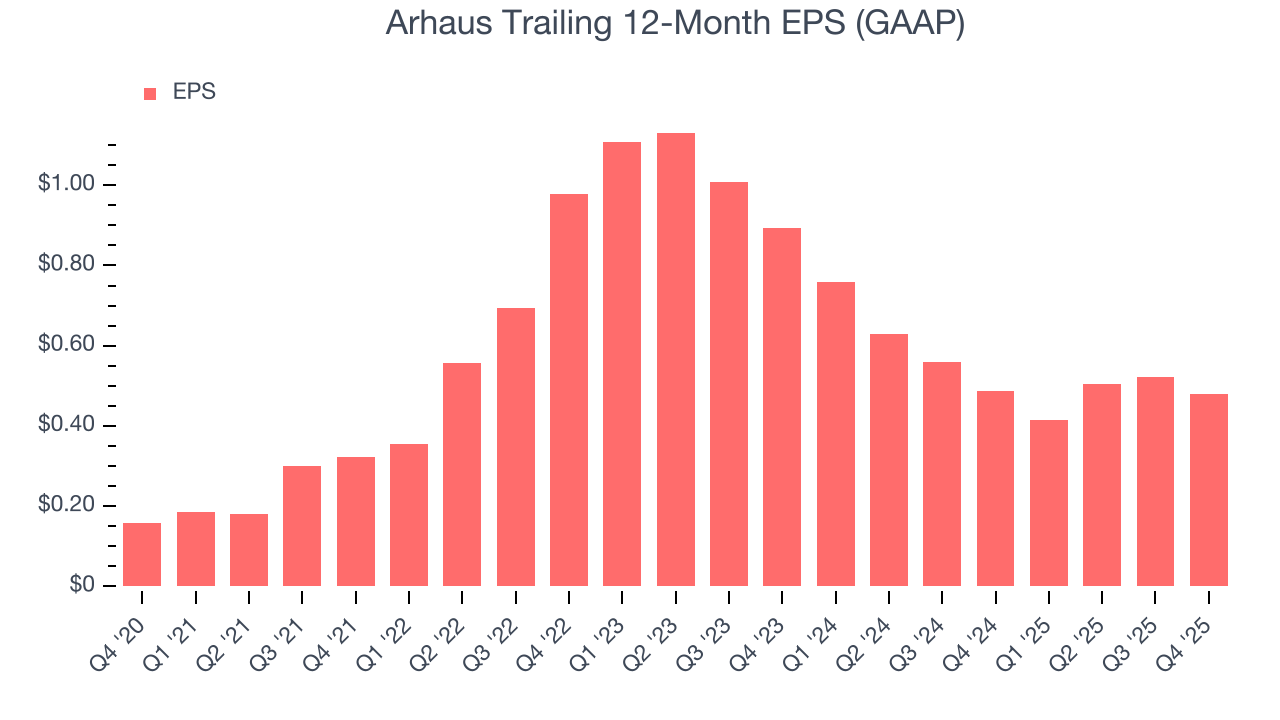

9. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Sadly for Arhaus, its EPS declined by 21.2% annually over the last three years while its revenue grew by 3.9%. This tells us the company became less profitable on a per-share basis as it expanded.

In Q4, Arhaus reported EPS of $0.11, down from $0.15 in the same quarter last year. Despite falling year on year, this print easily cleared analysts’ estimates. Over the next 12 months, Wall Street expects Arhaus’s full-year EPS of $0.48 to grow 3.7%.

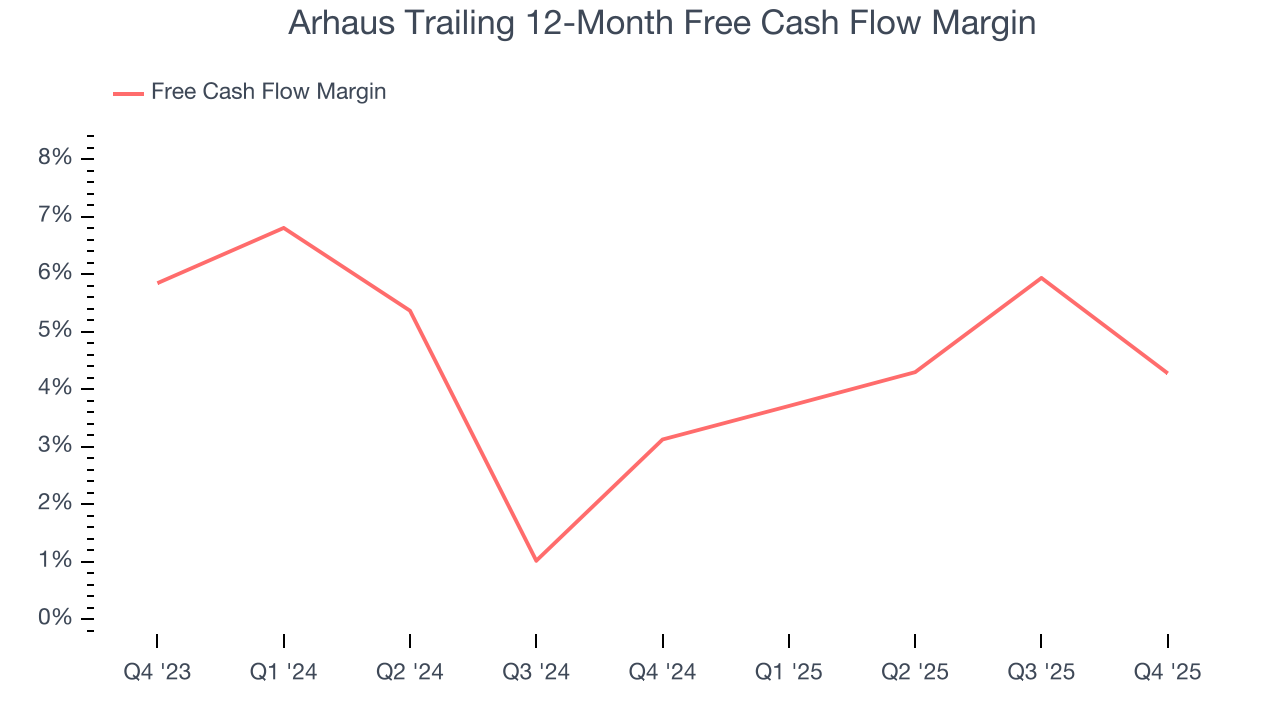

10. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Arhaus has shown decent cash profitability, giving it some flexibility to reinvest or return capital to investors. The company’s free cash flow margin averaged 3.7% over the last two years, slightly better than the broader consumer retail sector.

Taking a step back, we can see that Arhaus’s margin expanded by 1.1 percentage points over the last year. This shows the company is heading in the right direction, and we can see it became a less capital-intensive business because its free cash flow profitability rose while its operating profitability was flat.

Arhaus burned through $8.81 million of cash in Q4, equivalent to a negative 2.4% margin. The company’s cash flow turned negative after being positive in the same quarter last year, prompting us to pay closer attention. Short-term fluctuations typically aren’t a big deal because investment needs can be seasonal, but we’ll be watching to see if the trend extrapolates into future quarters.

11. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Although Arhaus hasn’t been the highest-quality company lately because of its poor revenue and EPS performance, it found a few growth initiatives in the past that worked out wonderfully. Its four-year average ROIC was 36.2%, splendid for a consumer retail business.

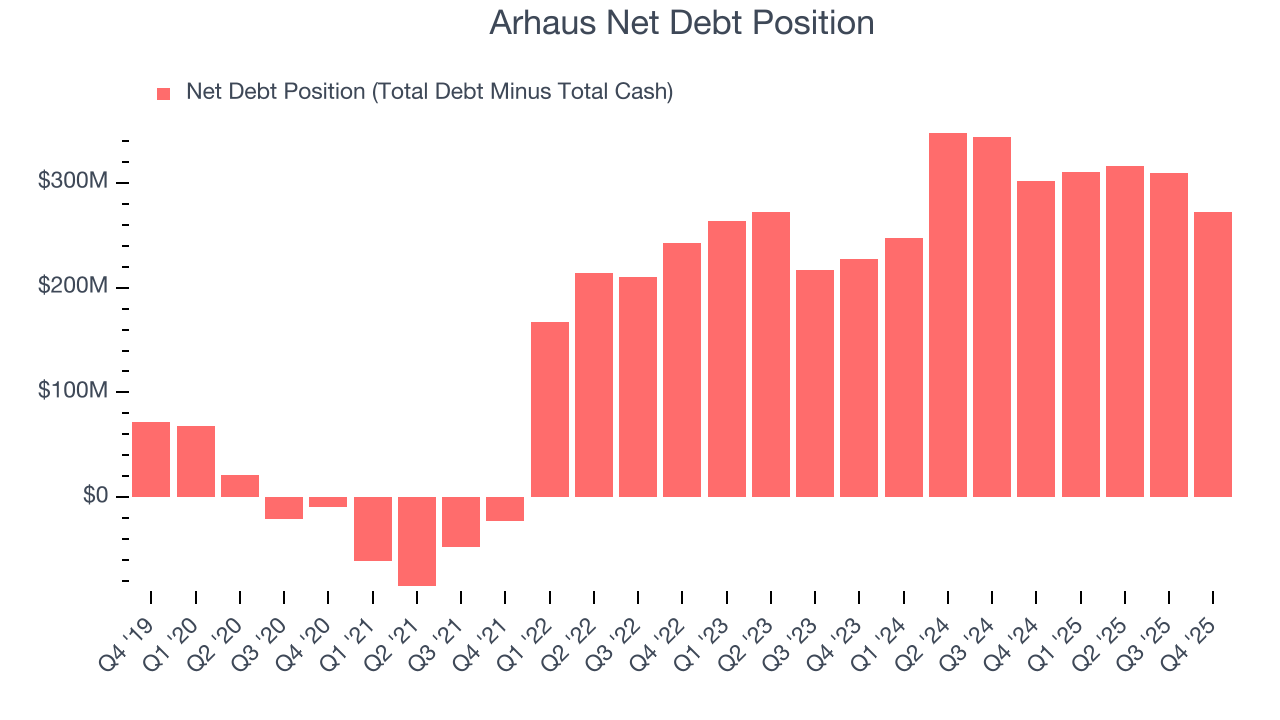

12. Balance Sheet Assessment

Arhaus reported $256.5 million of cash and $528.3 million of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $145.1 million of EBITDA over the last 12 months, we view Arhaus’s 1.9× net-debt-to-EBITDA ratio as safe. We also see its $1.24 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

13. Key Takeaways from Arhaus’s Q4 Results

We were impressed by how significantly Arhaus blew past analysts’ EBITDA expectations this quarter. We were also excited its revenue outperformed Wall Street’s estimates by a wide margin. On the other hand, its revenue guidance for next quarter missed and its EBITDA guidance for next quarter fell short of Wall Street’s estimates. Overall, this print was mixed but still had some key positives. The stock traded up 3.9% to $8.71 immediately following the results.

14. Is Now The Time To Buy Arhaus?

Updated: March 6, 2026 at 9:50 PM EST

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in Arhaus.

Arhaus’s business quality ultimately falls short of our standards. For starters, its revenue growth was a little slower over the last three years. While its new store openings have increased its brand equity, the downside is its shrinking same-store sales tell us it will need to change its strategy to succeed. On top of that, its brand caters to a niche market.

Arhaus’s P/E ratio based on the next 12 months is 15.4x. While this valuation is fair, the upside isn’t great compared to the potential downside. We're pretty confident there are more exciting stocks to buy at the moment.

Wall Street analysts have a consensus one-year price target of $11.12 on the company (compared to the current share price of $7.71).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.