Astrana Health (ASTH)

Astrana Health is interesting. It’s one of the fastest-growing companies we cover, and there’s a solid chance its momentum will continue.― StockStory Analyst Team

1. News

2. Summary

Why Astrana Health Is Interesting

Formerly known as Apollo Medical Holdings until early 2024, Astrana Health (NASDAQ:ASTH) operates a technology-powered healthcare platform that enables physicians to deliver coordinated care while successfully participating in value-based payment models.

- Impressive 35.9% annual revenue growth over the last five years indicates it’s winning market share this cycle

- Notable projected revenue growth of 25.4% for the next 12 months hints at market share gains

- On the flip side, its adjusted operating margin falls short of the industry average, and the smaller profit dollars make it harder to react to unexpected market developments

Astrana Health has the potential to be a high-quality business. If you like the story, the valuation looks reasonable.

3. Astrana Health (ASTH) Research Report: Q4 CY2025 Update

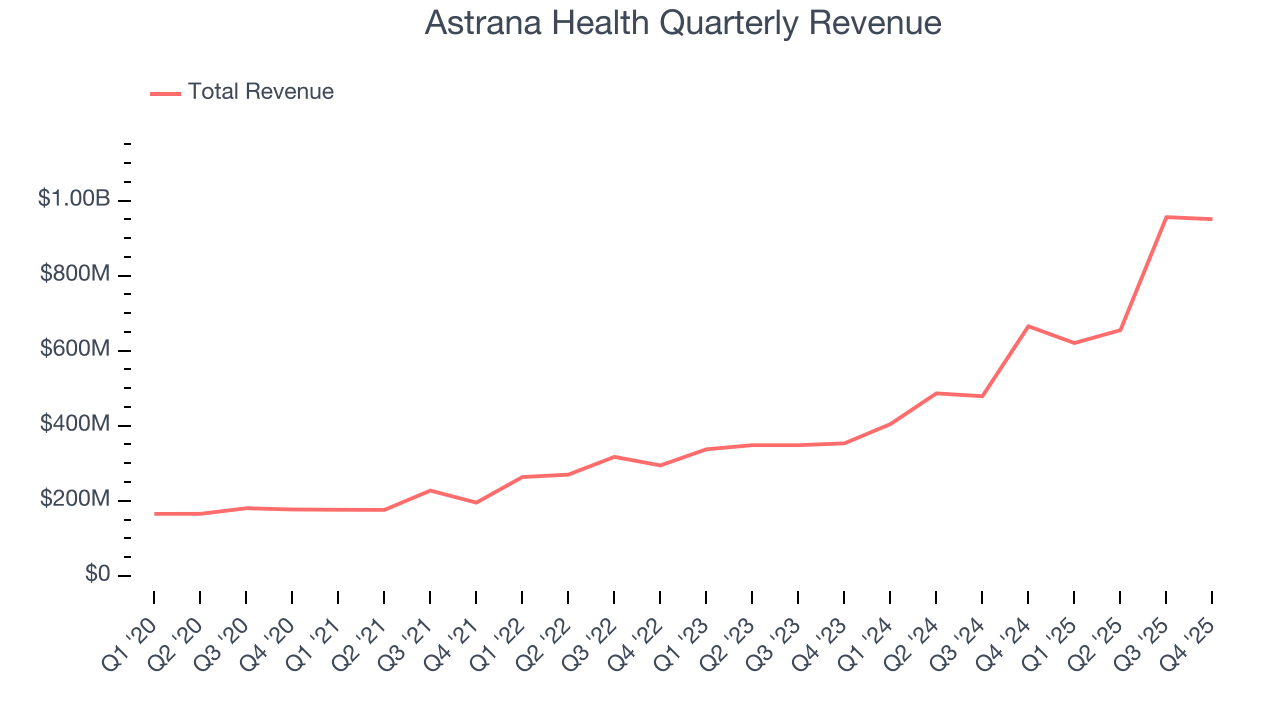

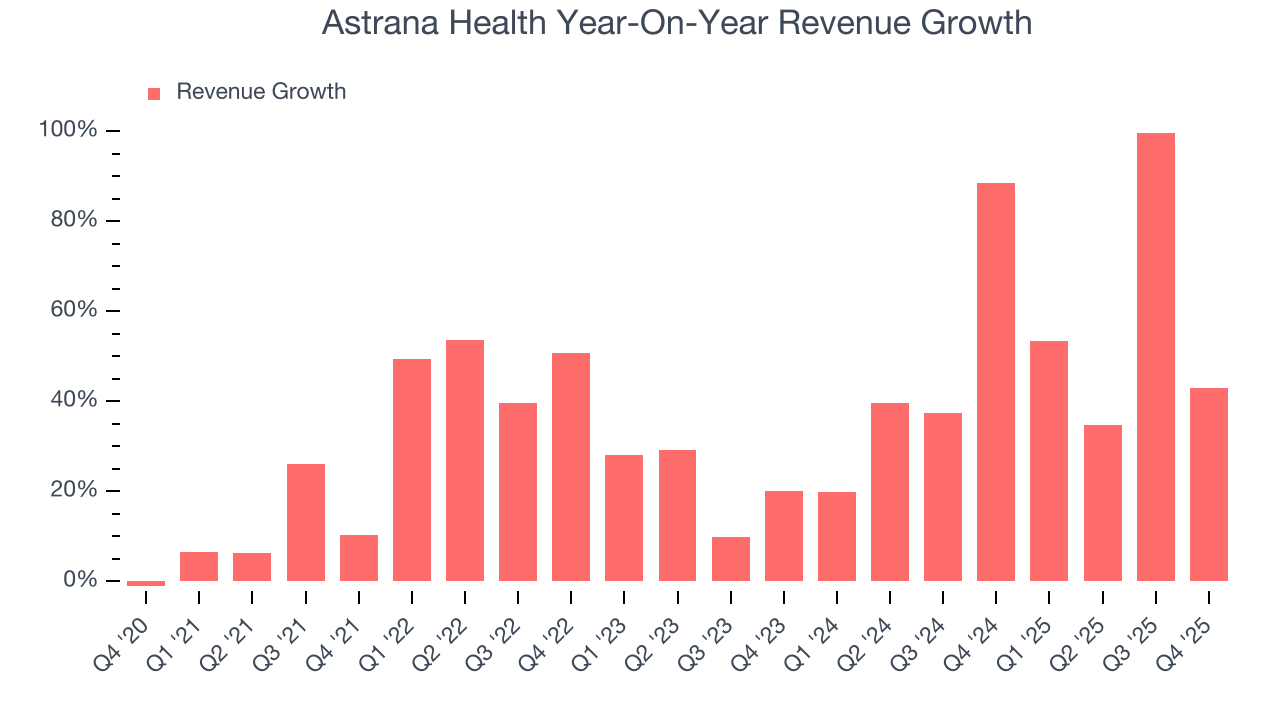

Healthcare services company Astrana Health reported Q4 CY2025 results beating Wall Street’s revenue expectations, with sales up 42.9% year on year to $950.5 million. The company expects next quarter’s revenue to be around $950 million, close to analysts’ estimates. Its GAAP profit of $0.12 per share was in line with analysts’ consensus estimates.

Astrana Health (ASTH) Q4 CY2025 Highlights:

- Revenue: $950.5 million vs analyst estimates of $929.1 million (42.9% year-on-year growth, 2.3% beat)

- EPS (GAAP): $0.12 vs analyst estimates of $0.12 (in line)

- Adjusted EBITDA: $52.45 million vs analyst estimates of $52.21 million (5.5% margin, in line)

- Revenue Guidance for Q1 CY2026 is $950 million at the midpoint, roughly in line with what analysts were expecting

- EBITDA guidance for the upcoming financial year 2026 is $265 million at the midpoint, below analyst estimates of $267.3 million

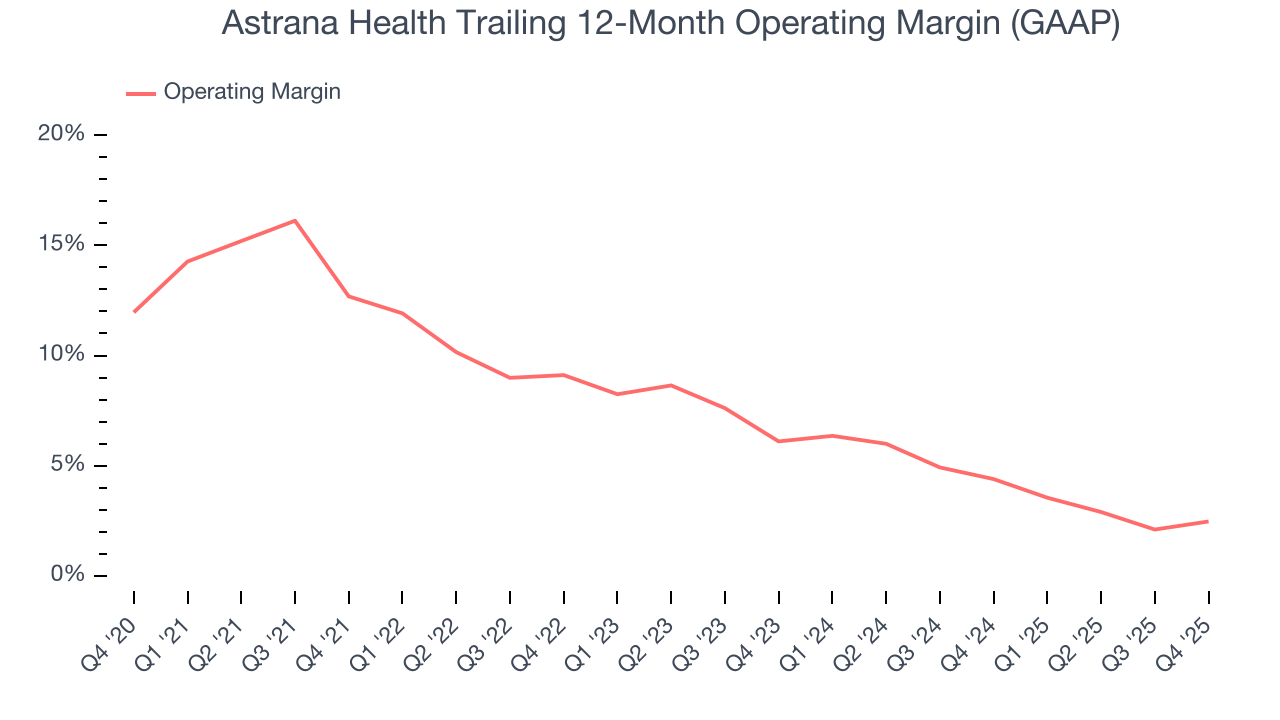

- Operating Margin: 1.9%, up from 0.1% in the same quarter last year

- Free Cash Flow was -$5.95 million compared to -$13.48 million in the same quarter last year

- Market Capitalization: $1.02 billion

Company Overview

Formerly known as Apollo Medical Holdings until early 2024, Astrana Health (NASDAQ:ASTH) operates a technology-powered healthcare platform that enables physicians to deliver coordinated care while successfully participating in value-based payment models.

Astrana's business model bridges the gap between traditional fee-for-service healthcare and value-based care arrangements where providers are financially rewarded for improving patient outcomes while controlling costs. The company operates through three interconnected segments: Care Partners, Care Delivery, and Care Enablement.

The Care Partners segment builds and manages networks of physicians through independent practice associations (IPAs) and accountable care organizations (ACOs). These networks allow independent physicians to remain autonomous while gaining the scale and support needed to succeed in risk-bearing contracts with Medicare, Medicaid, and commercial insurers.

Through its Care Delivery segment, Astrana operates approximately 60 healthcare facilities across California, Nevada, and Texas. These include primary care clinics, multi-specialty centers, urgent care facilities, imaging centers, and ambulatory surgery centers. This physical footprint serves over 800,000 patients annually and strategically fills gaps in healthcare access within the communities Astrana serves.

The Care Enablement segment provides the technological backbone of Astrana's operations. This proprietary platform offers clinical, operational, and administrative tools that help providers manage population health effectively. For example, a primary care physician using Astrana's system might receive alerts about patients due for preventive screenings or those with chronic conditions requiring follow-up care.

A typical patient experience might involve someone with diabetes being assigned to an Astrana-affiliated primary care physician who coordinates with specialists, monitors medication adherence, and schedules regular check-ups—all supported by Astrana's technology platform that tracks outcomes and identifies opportunities for intervention.

Astrana generates revenue primarily through capitated arrangements where it receives fixed monthly payments per patient and assumes financial responsibility for their healthcare costs. The company also earns shared savings bonuses when its networks successfully reduce costs while maintaining quality standards in programs like Medicare's ACO REACH Model.

4. Healthcare Technology for Providers

The healthcare technology sector provides software and data analytics to help hospitals and clinics streamline operations and improve patient outcomes, often through value-based care models. Future growth is expected as providers prioritize digital transformation to manage rising costs and patient demands. Tailwinds include the adoption of AI-driven tools and government incentives for digitization. There challenges as well, including long sales cycles and slow adoption by providers, who may be resistance to change. Tightening hospital budgets and cybersecurity threats are additional risks that could slow adoption.

Astrana Health competes with other healthcare management organizations including Optum (owned by UnitedHealth Group), Privia Health (NASDAQ:PRVA), Oak Street Health (acquired by CVS Health), and Agilon Health (NYSE:AGL), as well as regional players like Heritage Provider Network in California.

5. Economies of Scale

Larger companies benefit from economies of scale, where fixed costs like infrastructure, technology, and administration are spread over a higher volume of goods or services, reducing the cost per unit. Scale can also lead to bargaining power with suppliers, greater brand recognition, and more investment firepower. A virtuous cycle can ensue if a scaled company plays its cards right.

With $3.18 billion in revenue over the past 12 months, Astrana Health has decent scale. This is important as it gives the company more leverage in a heavily regulated, competitive environment that is complex and resource-intensive.

6. Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Luckily, Astrana Health’s sales grew at an incredible 35.9% compounded annual growth rate over the last five years. Its growth beat the average healthcare company and shows its offerings resonate with customers, a helpful starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within healthcare, a half-decade historical view may miss recent innovations or disruptive industry trends. Astrana Health’s annualized revenue growth of 51.5% over the last two years is above its five-year trend, suggesting its demand was strong and recently accelerated.

This quarter, Astrana Health reported magnificent year-on-year revenue growth of 42.9%, and its $950.5 million of revenue beat Wall Street’s estimates by 2.3%. Company management is currently guiding for a 53.1% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 24.5% over the next 12 months, a deceleration versus the last two years. Despite the slowdown, this projection is commendable and implies the market sees success for its products and services.

7. Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Astrana Health was profitable over the last five years but held back by its large cost base. Its average operating margin of 5.3% was weak for a healthcare business.

Looking at the trend in its profitability, Astrana Health’s operating margin decreased by 10.2 percentage points over the last five years. The company’s two-year trajectory also shows it failed to get its profitability back to the peak as its margin fell by 3.6 percentage points. This performance was poor no matter how you look at it - it shows its expenses were rising and it couldn’t pass those costs onto its customers.

In Q4, Astrana Health generated an operating margin profit margin of 1.9%, up 1.8 percentage points year on year. This increase was a welcome development and shows it was more efficient.

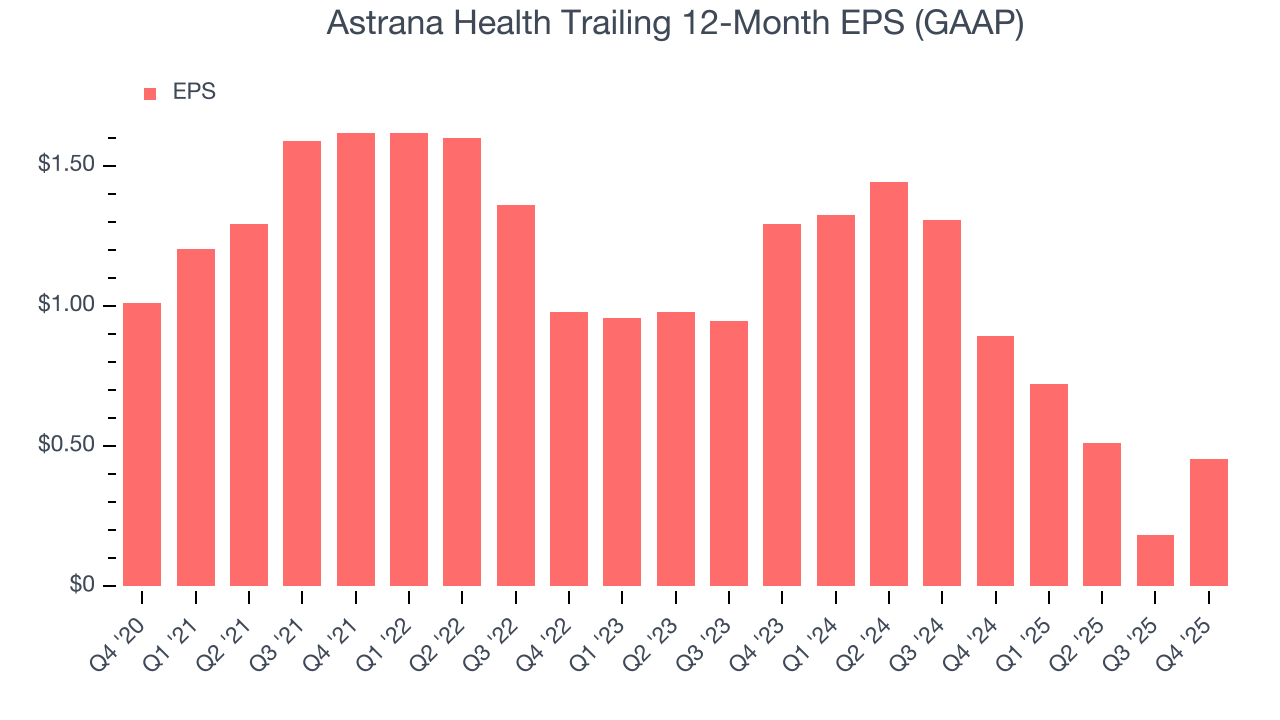

8. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Sadly for Astrana Health, its EPS declined by 14.7% annually over the last five years while its revenue grew by 35.9%. This tells us the company became less profitable on a per-share basis as it expanded.

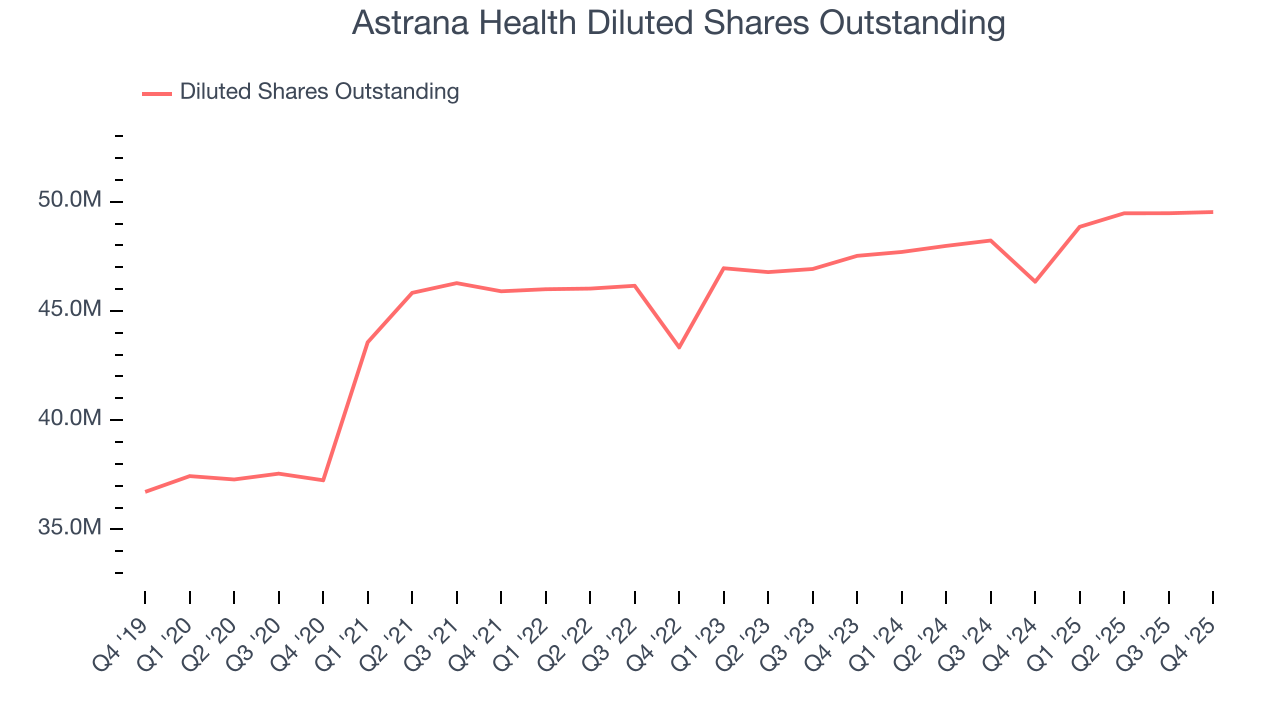

Diving into the nuances of Astrana Health’s earnings can give us a better understanding of its performance. As we mentioned earlier, Astrana Health’s operating margin expanded this quarter but declined by 10.2 percentage points over the last five years. Its share count also grew by 33%, meaning the company not only became less efficient with its operating expenses but also diluted its shareholders.

In Q4, Astrana Health reported EPS of $0.12, up from negative $0.15 in the same quarter last year. This print beat analysts’ estimates by 3.8%. Over the next 12 months, Wall Street expects Astrana Health’s full-year EPS of $0.46 to grow 117%.

9. Cash Is King

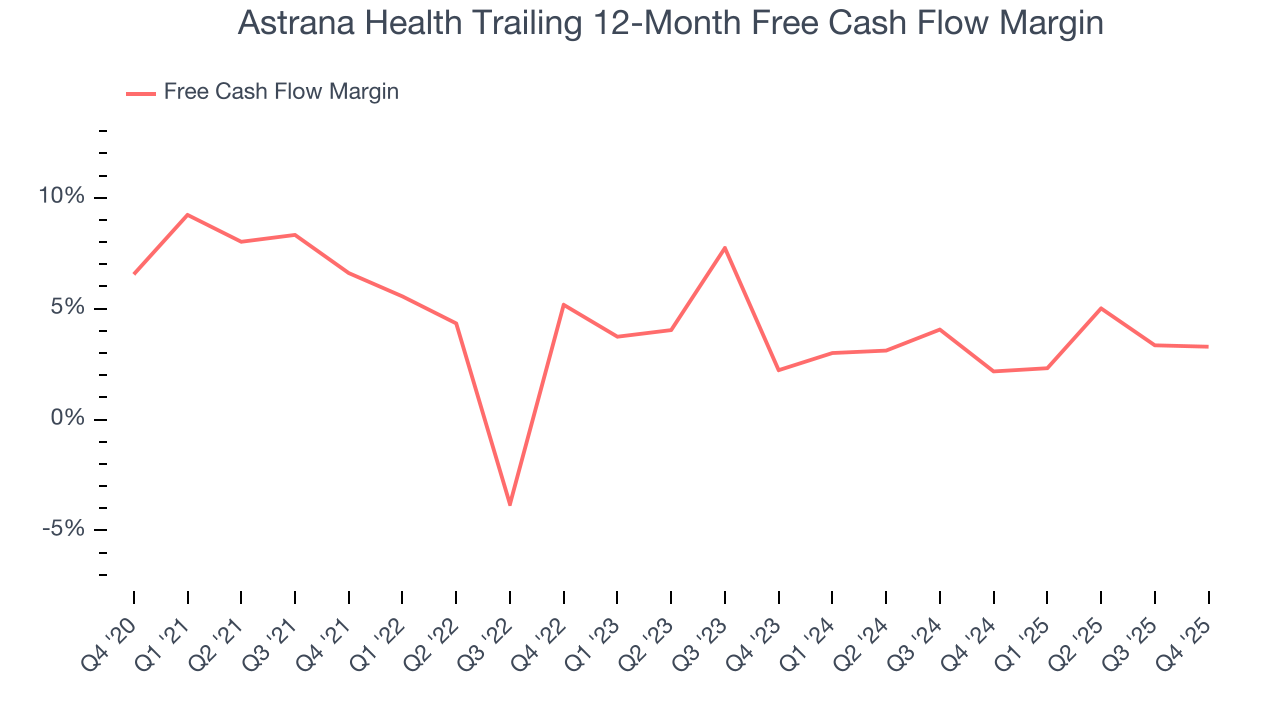

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

Astrana Health has shown mediocre cash profitability over the last five years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 3.4%, subpar for a healthcare business.

Taking a step back, we can see that Astrana Health’s margin dropped by 3.3 percentage points during that time. If the trend continues, it could signal it’s in the middle of an investment cycle.

Astrana Health broke even from a free cash flow perspective in Q4. This result was good as its margin was 1.4 percentage points higher than in the same quarter last year, but we note it was lower than its five-year cash profitability. Nevertheless, we wouldn’t put too much weight on a single quarter because investment needs can be seasonal, causing short-term swings. Long-term trends carry greater meaning.

10. Return on Invested Capital (ROIC)

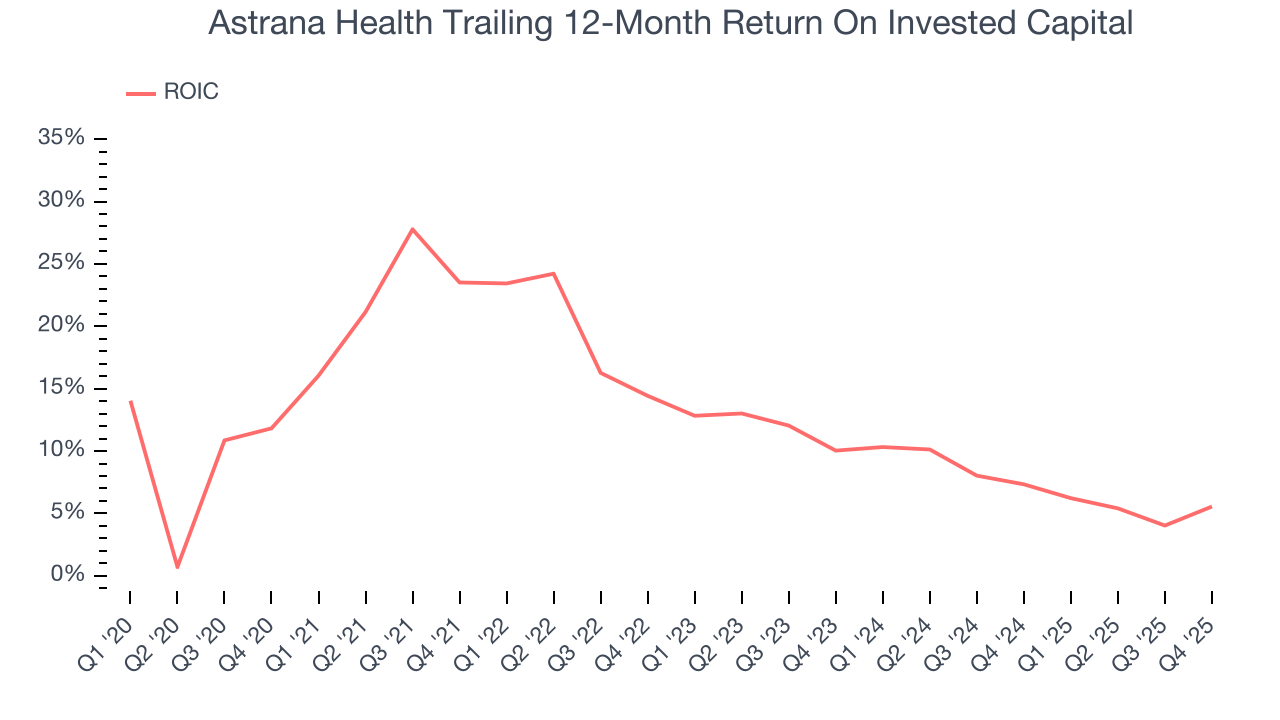

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Astrana Health’s five-year average ROIC was 12.2%, higher than most healthcare businesses. This illustrates its management team’s ability to invest in profitable growth opportunities and generate value for shareholders.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Over the last few years, Astrana Health’s ROIC has unfortunately decreased significantly. Only time will tell if its new bets can bear fruit and potentially reverse the trend.

11. Balance Sheet Assessment

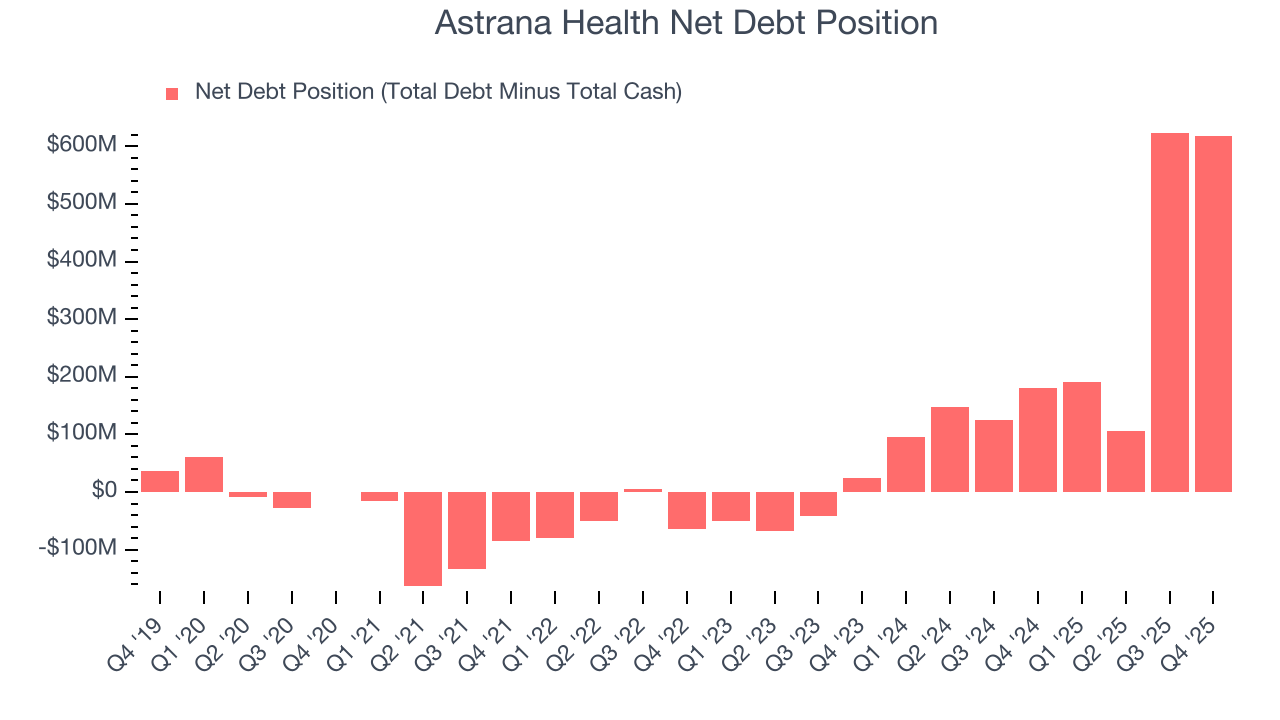

Astrana Health reported $429.5 million of cash and $1.05 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $205.4 million of EBITDA over the last 12 months, we view Astrana Health’s 3.0× net-debt-to-EBITDA ratio as safe. We also see its $10.71 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

12. Key Takeaways from Astrana Health’s Q4 Results

We were impressed by Astrana Health’s optimistic EBITDA guidance for next quarter, which blew past analysts’ expectations. We were also happy its revenue outperformed Wall Street’s estimates. On the other hand, its revenue guidance for next quarter was in line. Overall, this print had some key positives. The stock traded up 3.9% to $21.13 immediately after reporting.

13. Is Now The Time To Buy Astrana Health?

Updated: March 14, 2026 at 12:02 AM EDT

We think that the latest earnings result is only one piece of the bigger puzzle. If you’re deciding whether to own Astrana Health, you should also grasp the company’s longer-term business quality and valuation.

Astrana Health is a fine business. First off, its revenue growth was exceptional over the last five years. And while its diminishing returns show management's recent bets still have yet to bear fruit, its astounding EPS growth over the last five years shows its profits are trickling down to shareholders. On top of that, its solid ROIC suggests it has grown profitably in the past.

Astrana Health’s P/E ratio based on the next 12 months is 8.6x. Looking at the healthcare space right now, Astrana Health trades at a compelling valuation. If you believe in the company and its growth potential, now is an opportune time to buy shares.

Wall Street analysts have a consensus one-year price target of $36 on the company (compared to the current share price of $24.26), implying they see 48.4% upside in buying Astrana Health in the short term.