AeroVironment (AVAV)

We’re skeptical of AeroVironment. Not only has its sales growth been weak but also its negative returns on capital show it destroyed value.― StockStory Analyst Team

1. News

2. Summary

Why We Think AeroVironment Will Underperform

Focused on the future of autonomous military combat, AeroVironment (NASDAQ:AVAV) specializes in advanced unmanned aircraft systems and electric vehicle charging solutions.

- Persistent operating margin losses and eroding margin over the last five years point to its preference for growth over profits

- Cash burn has widened over the last five years, making us question whether it can reliably generate shareholder value

- A silver lining is that its annual revenue growth of 32.5% over the past five years was outstanding, reflecting market share gains this cycle

AeroVironment’s quality doesn’t meet our expectations. There are more profitable opportunities elsewhere.

Why There Are Better Opportunities Than AeroVironment

AeroVironment’s stock price of $196.28 implies a valuation ratio of 51x forward P/E. We consider this valuation aggressive considering the business fundamentals.

There are stocks out there similarly priced with better business quality. We prefer owning these.

3. AeroVironment (AVAV) Research Report: Q4 CY2025 Update

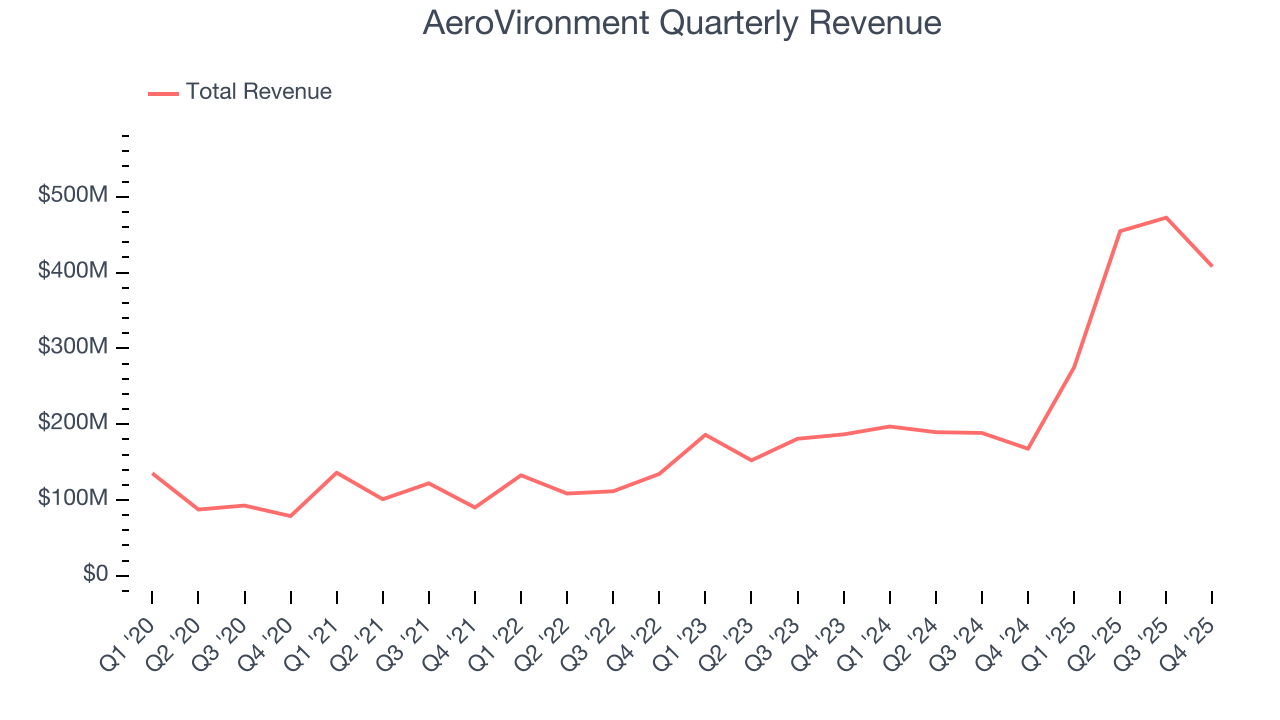

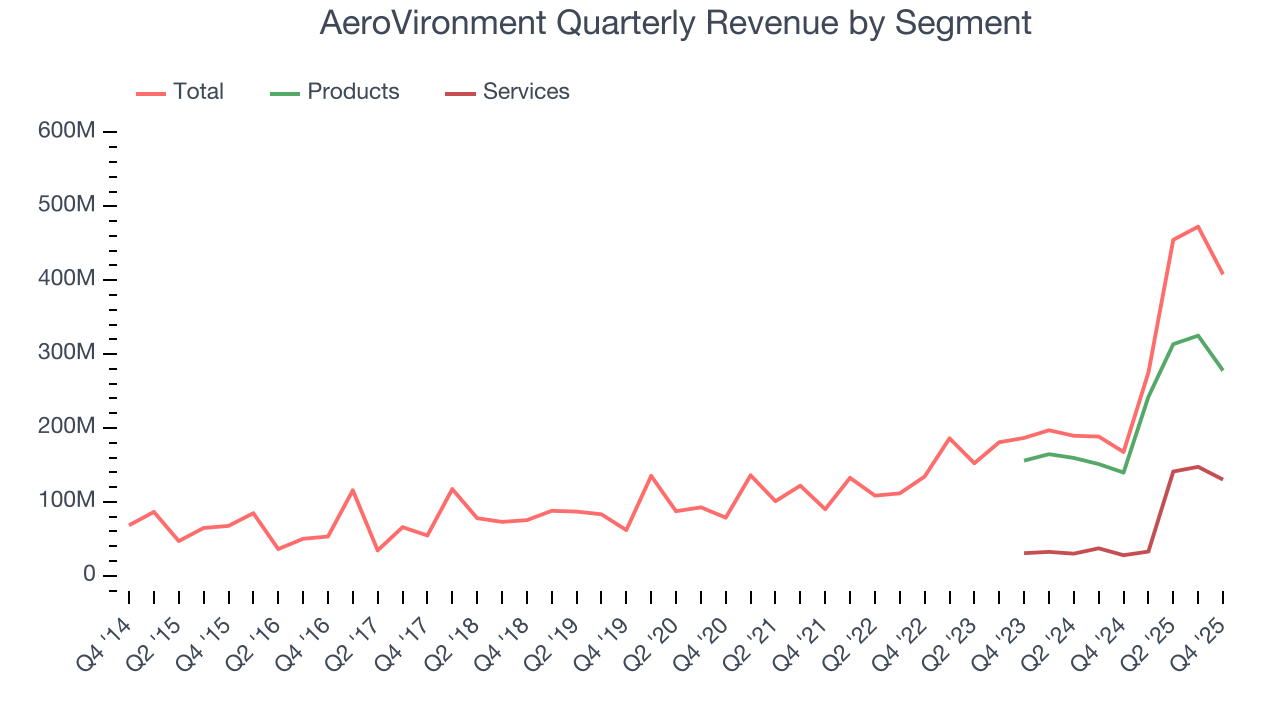

Aerospace and defense company AeroVironment (NASDAQ:AVAV) missed Wall Street’s revenue expectations in Q4 CY2025, but sales rose 143% year on year to $408 million. The company’s full-year revenue guidance of $1.9 billion at the midpoint came in 3.2% below analysts’ estimates. Its non-GAAP profit of $0.64 per share was 7.4% below analysts’ consensus estimates.

AeroVironment (AVAV) Q4 CY2025 Highlights:

- Revenue: $408 million vs analyst estimates of $478 million (143% year-on-year growth, 14.6% miss)

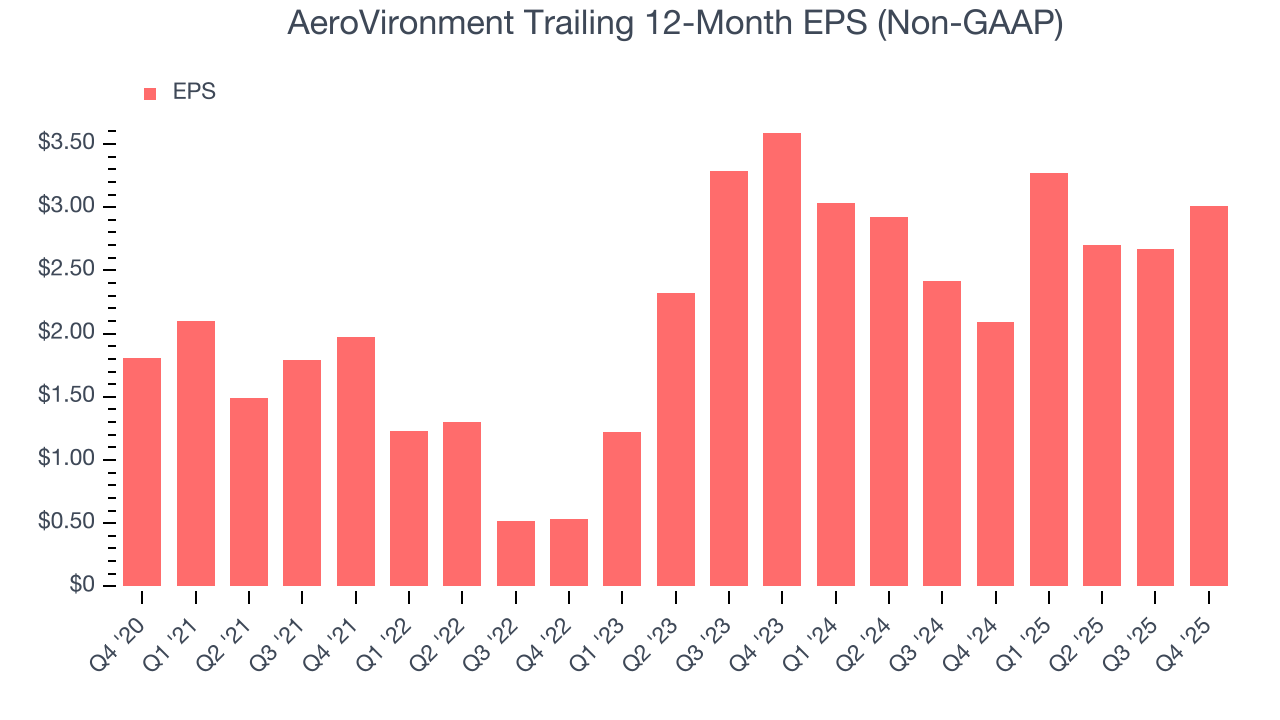

- Adjusted EPS: $0.64 vs analyst expectations of $0.69 (7.4% miss)

- Adjusted EBITDA: $44.48 million vs analyst estimates of $66.87 million (10.9% margin, 33.5% miss)

- The company dropped its revenue guidance for the full year to $1.9 billion at the midpoint from $1.98 billion, a 3.8% decrease

- Management lowered its full-year Adjusted EPS guidance to $2.93 at the midpoint, a 15.8% decrease

- EBITDA guidance for the full year is $275 million at the midpoint, below analyst estimates of $305.9 million

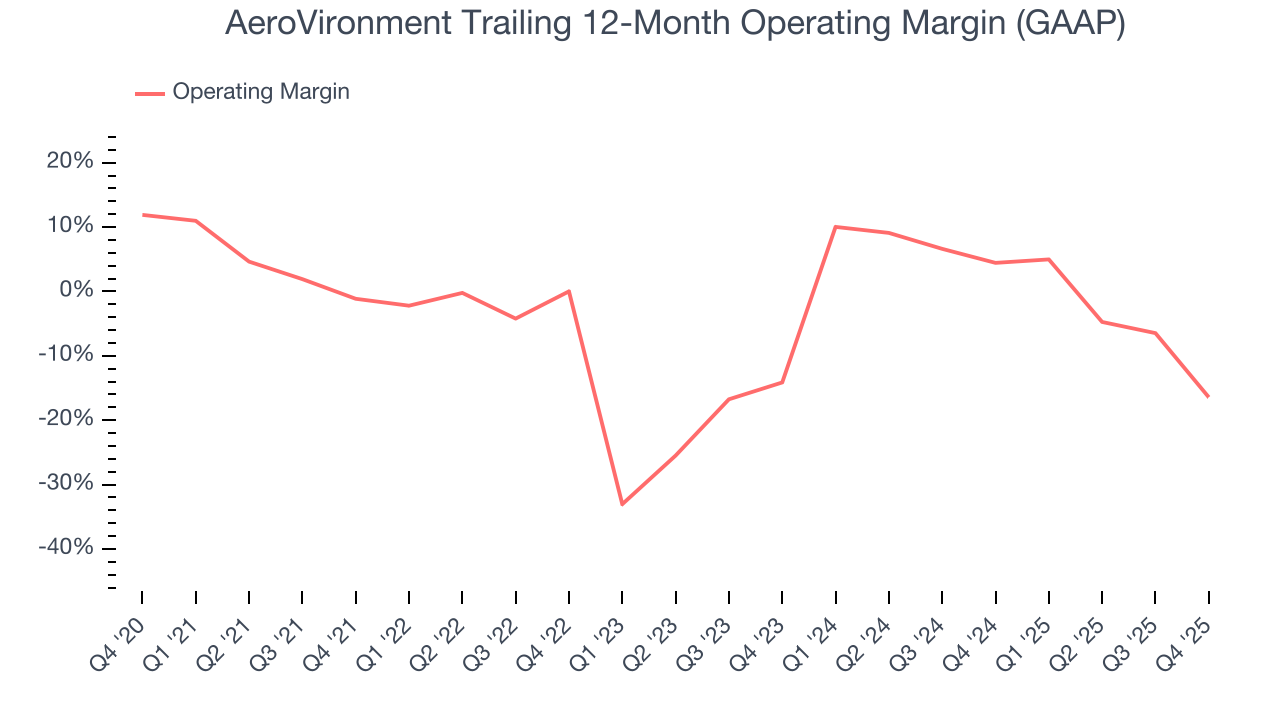

- Operating Margin: -43.9%, down from -1.8% in the same quarter last year

- Free Cash Flow was -$4.44 million compared to -$29.61 million in the same quarter last year

- Market Capitalization: $11.3 billion

Company Overview

Focused on the future of autonomous military combat, AeroVironment (NASDAQ:AVAV) specializes in advanced unmanned aircraft systems and electric vehicle charging solutions.

AeroVironment was founded in 1971 by Dr. Paul MacCready, an inventor and aerospace engineer, renowned for developing human-powered flight. The company's early focus was on creating lightweight, and energy-efficient vehicles. AeroVironment gained prominence after creating the Gossamer Condor in 1977, the first human-powered aircraft capable of controlled and sustained flight, which won the prestigious Kremer Prize.

Over the years, AeroVironment expanded its focus to include unmanned aerial vehicles (UAVs), becoming one of the pioneers in the field. The company developed a series of UAVs, including the Global Observer, a high-altitude, long-endurance aircraft powered by hydrogen, and smaller drones widely used by the U.S. military and allied forces.

Today, AeroVironment develops and supports a range of advanced robotic systems and services used by government and commercial sectors. Its products include unmanned aircraft, ground robots, and special missile systems primarily used by the U.S. Department of Defense, other federal agencies, and allied international governments. The company's technologies are designed for use in all kinds of environments, from the earth’s surface to space, offering efficient and sophisticated solutions for complicated operations. Notable products from AeroVironment include high-flying drones, electric propulsion systems, advanced control systems for flight, and interfaces that allow humans to interact smoothly with machines. These products are particularly aimed at improving the safety and effectiveness of critical operations in challenging locations. For example, its small unmanned aircraft systems are often used for surveillance in military operations, providing vital information without putting human lives at risk.

AeroVironment primarily markets its unmanned systems products and loitering munitions to various branches of the U.S. Department of Defense (DoD), such as the Army, Marine Corps, Special Operations Command, Air Force, and Navy. The company also caters to public safety agencies and allied governments worldwide, as well as private sector companies that subcontract for these government entities. Additionally, AeroVironment collaborates with SoftBank Corp to develop High Altitude Pseudo-Satellite (HAPS) systems for commercial use, while retaining the exclusive rights to sell HAPS systems for defense applications outside of Japan. This includes dealing with agencies like NASA and the U.S. DoD. The company's revenue is largely derived from contracts for these specialized unmanned aircraft systems, advanced munitions, and high-altitude platforms, reflecting a diverse but focused customer base in both defense and commercial sectors.

AeroVironment's cost structure is significantly influenced by its substantial investment in research and development (R&D). The company prioritizes R&D to innovate and advance its portfolio of unmanned systems and related technologies. This strategic focus on development is essential for maintaining its competitive edge in designing cutting-edge solutions for its customers. Additionally, AeroVironment enhances its product offerings and expands its technological capabilities through strategic acquisitions, continuously integrating new technology into its product offerings. This is particularly crucial for the defense sector, where maintaining a technological edge is highly valued.

4. Defense Contractors

Defense contractors typically require technical expertise and government clearance. Companies in this sector can also enjoy long-term contracts with government bodies, leading to more predictable revenues. Combined, these factors create high barriers to entry and can lead to limited competition. Lately, geopolitical tensions–whether it be Russia’s invasion of Ukraine or China’s aggression towards Taiwan–highlight the need for defense spending. On the other hand, demand for these products can ebb and flow with defense budgets and even who is president, as different administrations can have vastly different ideas of how to allocate federal funds.

AeroVironment’s competitors include Northrop Grumman (NYSE:NOC), Lockheed Martin (NYSE:LMT), and Textron (NYSE:TXT).

5. Revenue Growth

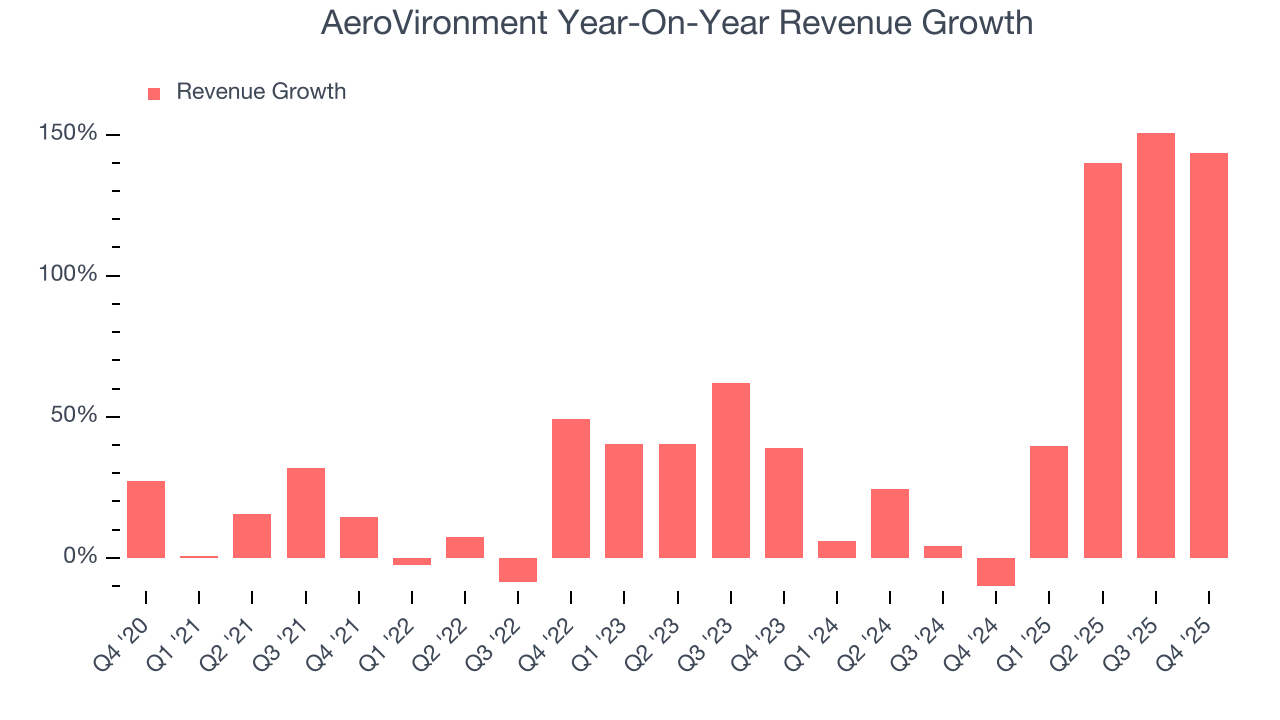

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Thankfully, AeroVironment’s 32.5% annualized revenue growth over the last five years was incredible. Its growth beat the average industrials company and shows its offerings resonate with customers.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. AeroVironment’s annualized revenue growth of 51% over the last two years is above its five-year trend, suggesting its demand was strong and recently accelerated.

We can dig further into the company’s revenue dynamics by analyzing its most important segments, Products and Services, which are 68.1% and 31.9% of revenue. Over the last two years, AeroVironment’s Products revenue (aircrafts, missile systems, satellites) averaged 69.4% year-on-year growth while its Services revenue (maintenance, training, consulting) averaged 205% growth.

This quarter, AeroVironment achieved a magnificent 143% year-on-year revenue growth rate, but its $408 million of revenue fell short of Wall Street’s lofty estimates.

Looking ahead, sell-side analysts expect revenue to grow 35.6% over the next 12 months, a deceleration versus the last two years. Despite the slowdown, this projection is commendable and indicates the market sees success for its products and services.

6. Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

AeroVironment’s high expenses have contributed to an average operating margin of negative 8.4% over the last five years. Unprofitable industrials companies require extra attention because they could get caught swimming naked when the tide goes out. It’s hard to trust that the business can endure a full cycle.

Looking at the trend in its profitability, AeroVironment’s operating margin decreased by 15.3 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. AeroVironment’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers.

This quarter, AeroVironment generated a negative 43.9% operating margin.

7. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

AeroVironment’s EPS grew at a solid 10.7% compounded annual growth rate over the last five years. However, this performance was lower than its 32.5% annualized revenue growth, telling us the company became less profitable on a per-share basis as it expanded.

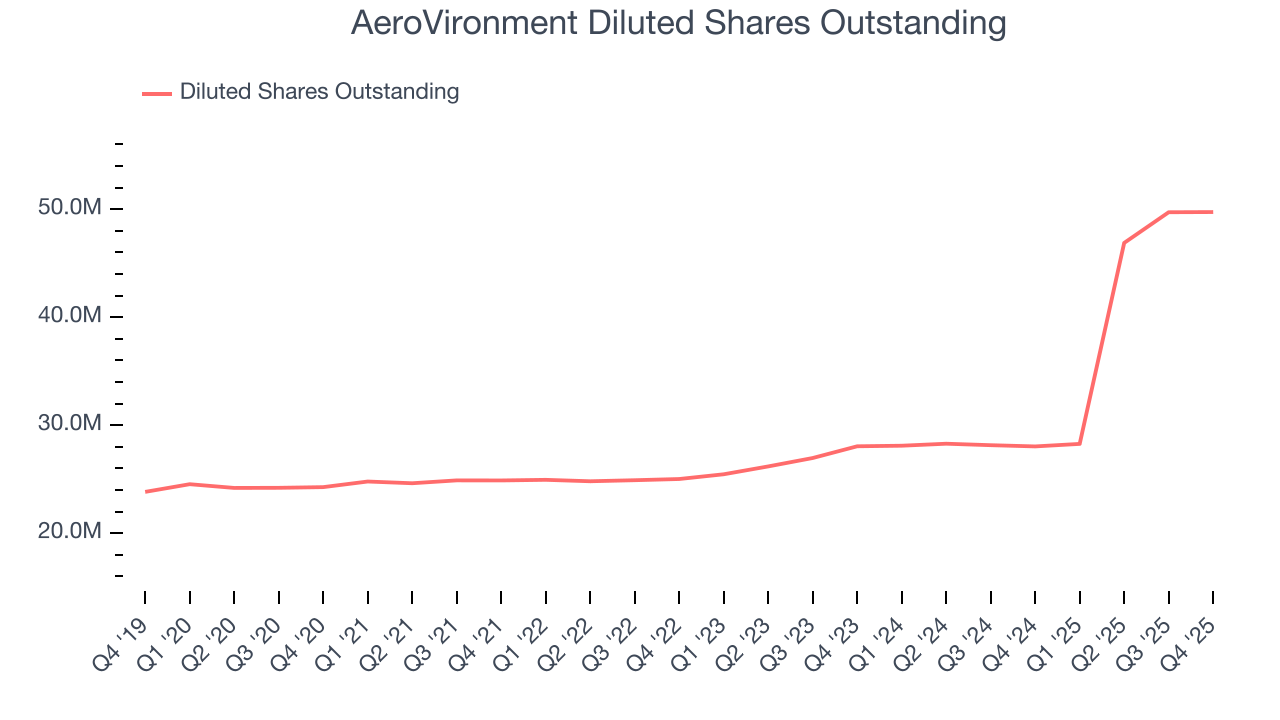

We can take a deeper look into AeroVironment’s earnings quality to better understand the drivers of its performance. As we mentioned earlier, AeroVironment’s operating margin declined by 15.3 percentage points over the last five years. Its share count also grew by 105%, meaning the company not only became less efficient with its operating expenses but also diluted its shareholders.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For AeroVironment, its two-year annual EPS declines of 8.4% mark a reversal from its (seemingly) healthy five-year trend. We hope AeroVironment can return to earnings growth in the future.

In Q4, AeroVironment reported adjusted EPS of $0.64, up from $0.30 in the same quarter last year. Despite growing year on year, this print missed analysts’ estimates, but we care more about long-term adjusted EPS growth than short-term movements. Over the next 12 months, Wall Street expects AeroVironment’s full-year EPS of $3.01 to grow 54.6%.

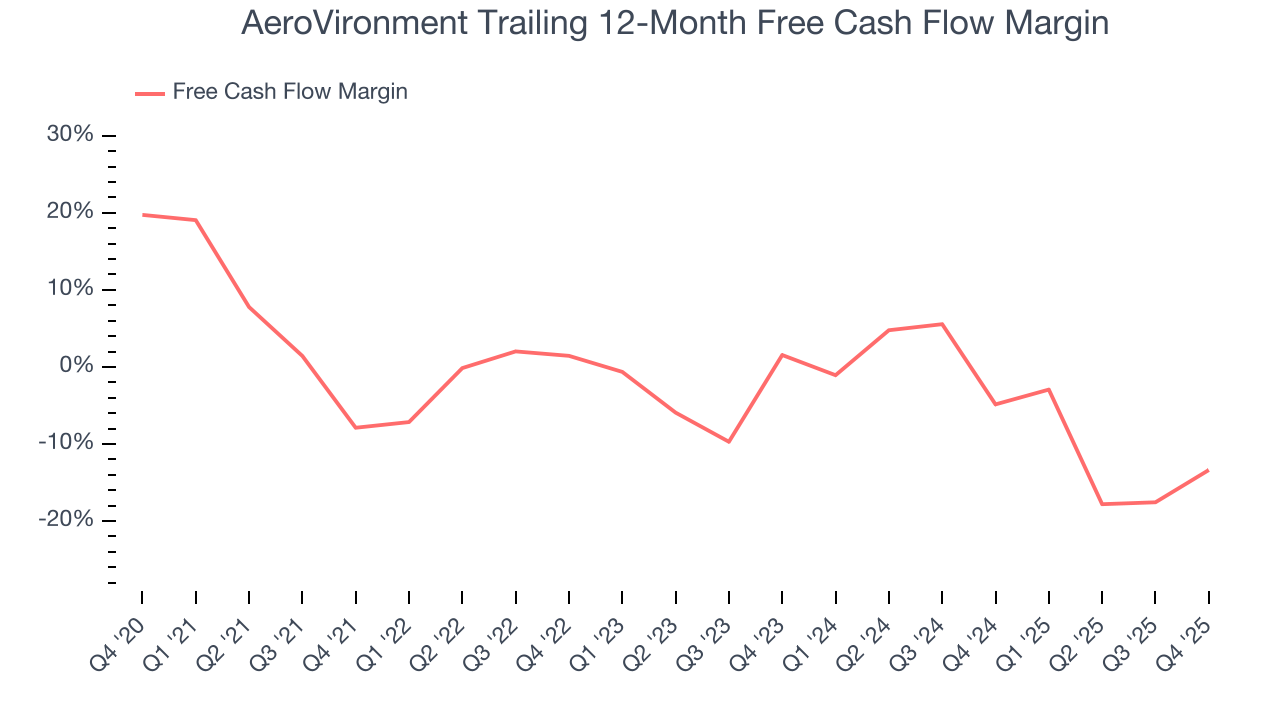

8. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

AeroVironment’s demanding reinvestments have drained its resources over the last five years, putting it in a pinch and limiting its ability to return capital to investors. Its free cash flow margin averaged negative 6.7%, meaning it lit $6.74 of cash on fire for every $100 in revenue.

Taking a step back, we can see that AeroVironment’s margin dropped by 5.5 percentage points during that time. Almost any movement in the wrong direction is undesirable because it is already burning cash. If the trend continues, it could signal it’s in the middle of a big investment cycle.

AeroVironment burned through $4.44 million of cash in Q4, equivalent to a negative 1.1% margin. The company’s cash burn slowed from $29.61 million of lost cash in the same quarter last year.

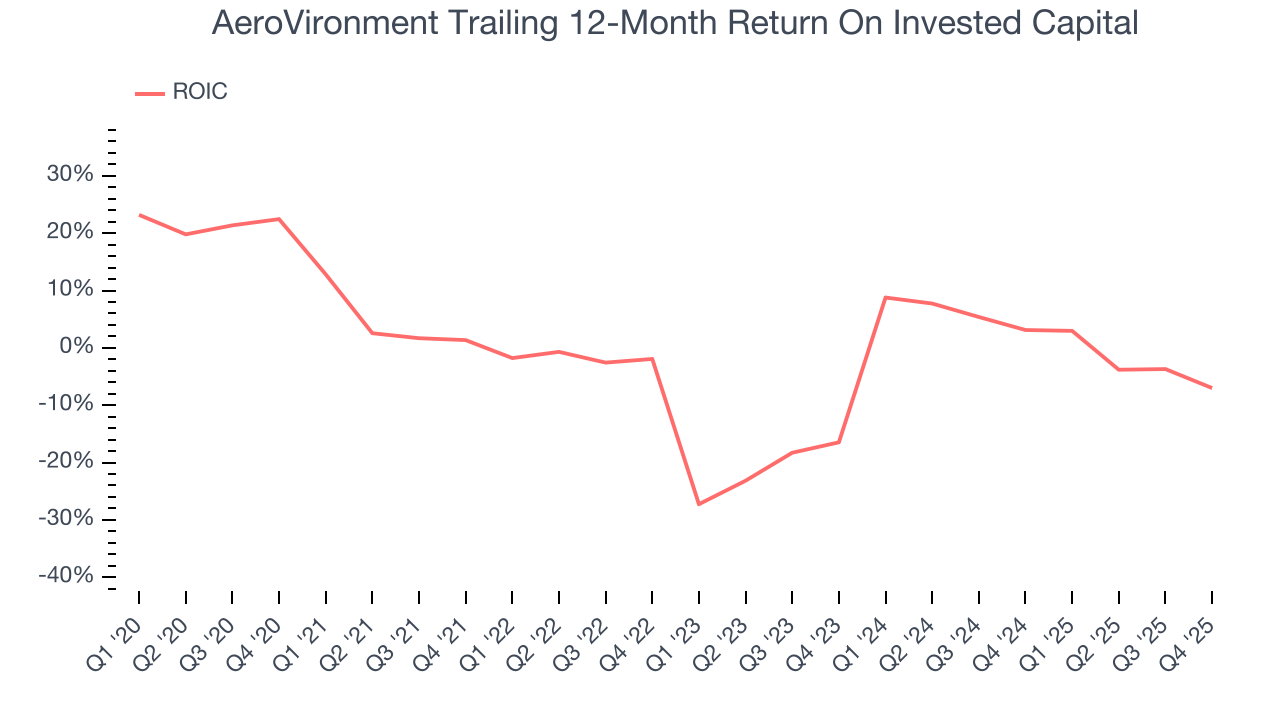

9. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

AeroVironment’s five-year average ROIC was negative 4.2%, meaning management lost money while trying to expand the business. Its returns were among the worst in the industrials sector.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Unfortunately, AeroVironment’s ROIC averaged 1.7 percentage point decreases each year over the last few years. Paired with its already low returns, these declines suggest its profitable growth opportunities are few and far between.

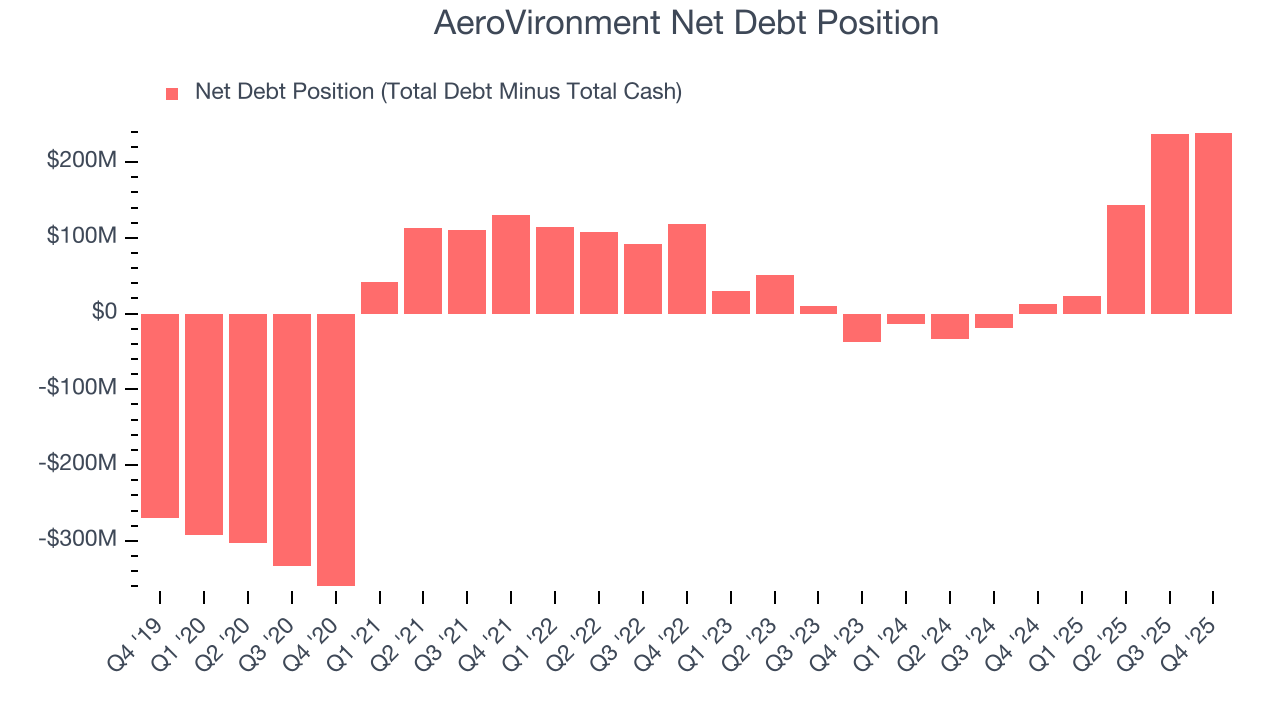

10. Balance Sheet Assessment

AeroVironment reported $587.1 million of cash and $826 million of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $207.6 million of EBITDA over the last 12 months, we view AeroVironment’s 1.2× net-debt-to-EBITDA ratio as safe. We also see its $10.02 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

11. Key Takeaways from AeroVironment’s Q4 Results

We struggled to find many positives in these results. Its full-year revenue guidance missed and its full-year EBITDA guidance fell short of Wall Street’s estimates. Overall, this quarter could have been better. The stock traded down 8.3% to $203.95 immediately after reporting.

12. Is Now The Time To Buy AeroVironment?

Updated: March 26, 2026 at 11:19 PM EDT

Are you wondering whether to buy AeroVironment or pass? We urge investors to not only consider the latest earnings results but also longer-term business quality and valuation as well.

AeroVironment isn’t a terrible business, but it doesn’t pass our bar. Although its revenue growth was exceptional over the last five years, it’s expected to deteriorate over the next 12 months and its relatively low ROIC suggests management has struggled to find compelling investment opportunities. And while the company’s projected EPS for the next year implies the company’s fundamentals will improve, the downside is its declining operating margin shows the business has become less efficient.

AeroVironment’s P/E ratio based on the next 12 months is 51x. This valuation tells us it’s a bit of a market darling with a lot of good news priced in - we think there are better stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $311.47 on the company (compared to the current share price of $196.28).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.