Concrete Pumping (BBCP)

We’re skeptical of Concrete Pumping. Its sales have underperformed and its low returns on capital show it has few growth opportunities.― StockStory Analyst Team

1. News

2. Summary

Why We Think Concrete Pumping Will Underperform

Going public via SPAC in 2018, Concrete Pumping (NASDAQ:BBCP) is a provider of concrete pumping and waste management services in the United States and the United Kingdom.

- Estimated sales growth of 2.4% for the next 12 months is soft and implies weaker demand

- ROIC of 7.8% reflects management’s challenges in identifying attractive investment opportunities

- A positive is that its earnings growth has outpaced its peers over the last five years as its EPS has compounded at 28.9% annually

Concrete Pumping lacks the business quality we seek. We’re redirecting our focus to better businesses.

Why There Are Better Opportunities Than Concrete Pumping

Concrete Pumping is trading at $6.87 per share, or 45.1x forward P/E. This valuation is extremely expensive, especially for the weaker revenue growth you get.

There are stocks out there similarly priced with better business quality. We prefer owning these.

3. Concrete Pumping (BBCP) Research Report: Q4 CY2025 Update

Concrete and waste management company Concrete Pumping (NASDAQ:BBCP) reported Q4 CY2025 results beating Wall Street’s revenue expectations, with sales up 4.8% year on year to $90.56 million. The company expects the full year’s revenue to be around $400 million, close to analysts’ estimates. Its GAAP loss of $0.06 per share was $0.02 above analysts’ consensus estimates.

Concrete Pumping (BBCP) Q4 CY2025 Highlights:

- Revenue: $90.56 million vs analyst estimates of $84.19 million (4.8% year-on-year growth, 7.6% beat)

- EPS (GAAP): -$0.06 vs analyst estimates of -$0.08 ($0.02 beat)

- Adjusted EBITDA: $18.03 million vs analyst estimates of $15.98 million (19.9% margin, 12.8% beat)

- The company reconfirmed its revenue guidance for the full year of $400 million at the midpoint

- EBITDA guidance for the full year is $95 million at the midpoint, below analyst estimates of $96.98 million

- Operating Margin: 5%, in line with the same quarter last year

- Free Cash Flow Margin: 13.1%, up from 0.2% in the same quarter last year

- Market Capitalization: $340.3 million

Company Overview

Going public via SPAC in 2018, Concrete Pumping (NASDAQ:BBCP) is a provider of concrete pumping and waste management services in the United States and the United Kingdom.

The company operates under several established brands, including Brundage-Bone Concrete Pumping for U.S. concrete pumping, Camfaud Group Limited in the U.K., and Eco-Pan for waste management services in both regions.

The company has expanded its reach through numerous strategic acquisitions, establishing a strong presence across both countries. Concrete Pumping Holdings utilizes a large fleet of specialized pumping equipment, washout pans, and trucks, operated by highly-trained professionals to deliver precise concrete placement and efficient waste management solutions.

Concrete Pumping Holdings operates through three main segments: U.S. Concrete Pumping, U.S. Concrete Waste Management Services, and U.K. Operations. The U.S. Concrete Pumping segment, operating under the Brundage-Bone and Capital Pumping brands, provides operated concrete pumping services across numerous states. The U.S. Concrete Waste Management Services segment, under the Eco-Pan brand, offers full-service, route-based concrete washout solutions. The U.K. Operations segment encompasses both concrete pumping and waste management services in the United Kingdom.

The company's business model is primarily based on negotiated time and volume pricing for concrete pumping services, with additional charges for specific project requirements. For waste management services, Concrete Pumping Holdings utilizes a fixed-fee structure that includes delivery, pickup, and disposal of concrete washout.

4. Construction and Maintenance Services

Construction and maintenance services companies not only boast technical know-how in specialized areas but also may hold special licenses and permits. Those who work in more regulated areas can enjoy more predictable revenue streams - for example, fire escapes need to be inspected every five years. More recently, services to address energy efficiency and labor availability are also creating incremental demand. But like the broader industrials sector, construction and maintenance services companies are at the whim of economic cycles as external factors like interest rates can greatly impact the new construction that drives incremental demand for these companies’ offerings.

Concrete Pumping’s competitors include United Rentals (NYSE:URI), Cemex (NYSE:CX), and Vulcan Materials (NYSE:VMC).

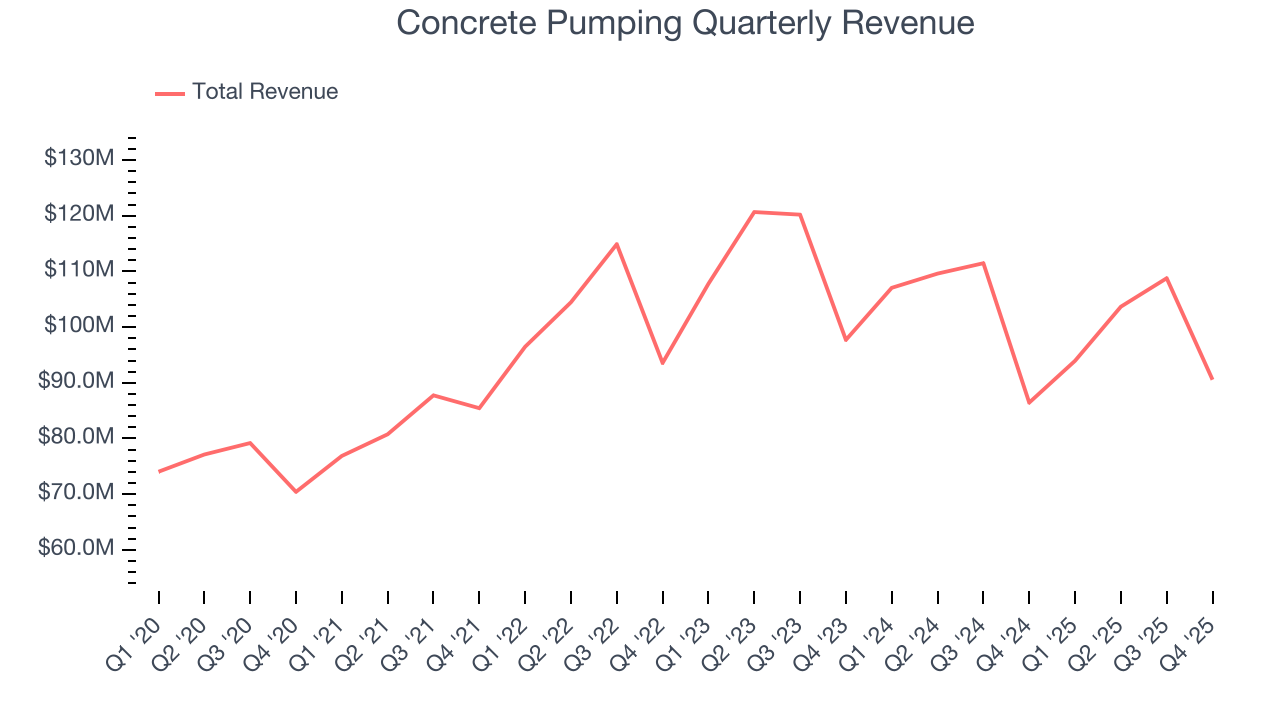

5. Revenue Growth

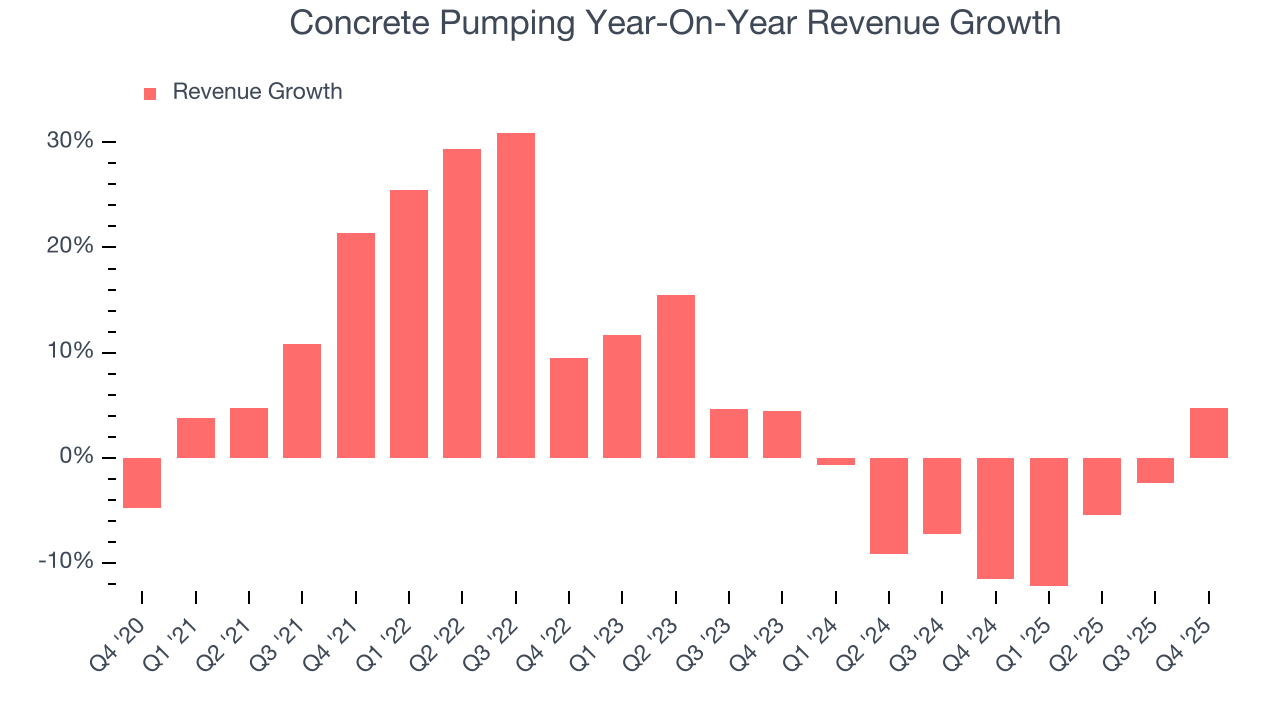

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Unfortunately, Concrete Pumping’s 5.7% annualized revenue growth over the last five years was tepid. This was below our standard for the industrials sector and is a tough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Concrete Pumping’s performance shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 5.7% annually.

This quarter, Concrete Pumping reported modest year-on-year revenue growth of 4.8% but beat Wall Street’s estimates by 7.6%.

Looking ahead, sell-side analysts expect revenue to grow 2.4% over the next 12 months. Although this projection indicates its newer products and services will spur better top-line performance, it is still below the sector average.

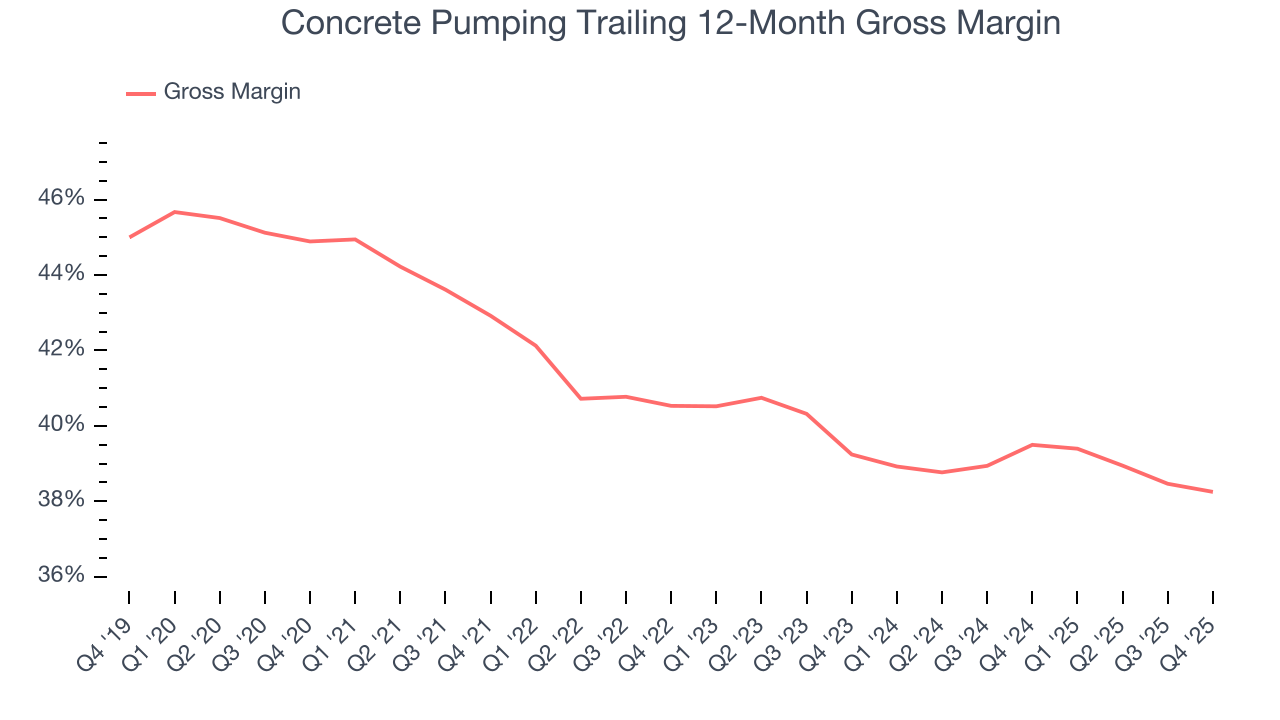

6. Gross Margin & Pricing Power

Concrete Pumping’s unit economics are great compared to the broader industrials sector and signal that it enjoys product differentiation through quality or brand. As you can see below, it averaged an excellent 40% gross margin over the last five years. Said differently, roughly $39.97 was left to spend on selling, marketing, R&D, and general administrative overhead for every $100 in revenue.

Concrete Pumping produced a 35.3% gross profit margin in Q4, in line with the same quarter last year. On a wider time horizon, Concrete Pumping’s full-year margin has been trending down over the past 12 months, decreasing by 1.2 percentage points. If this move continues, it could suggest a more competitive environment with some pressure to lower prices and higher input costs (such as raw materials and manufacturing expenses).

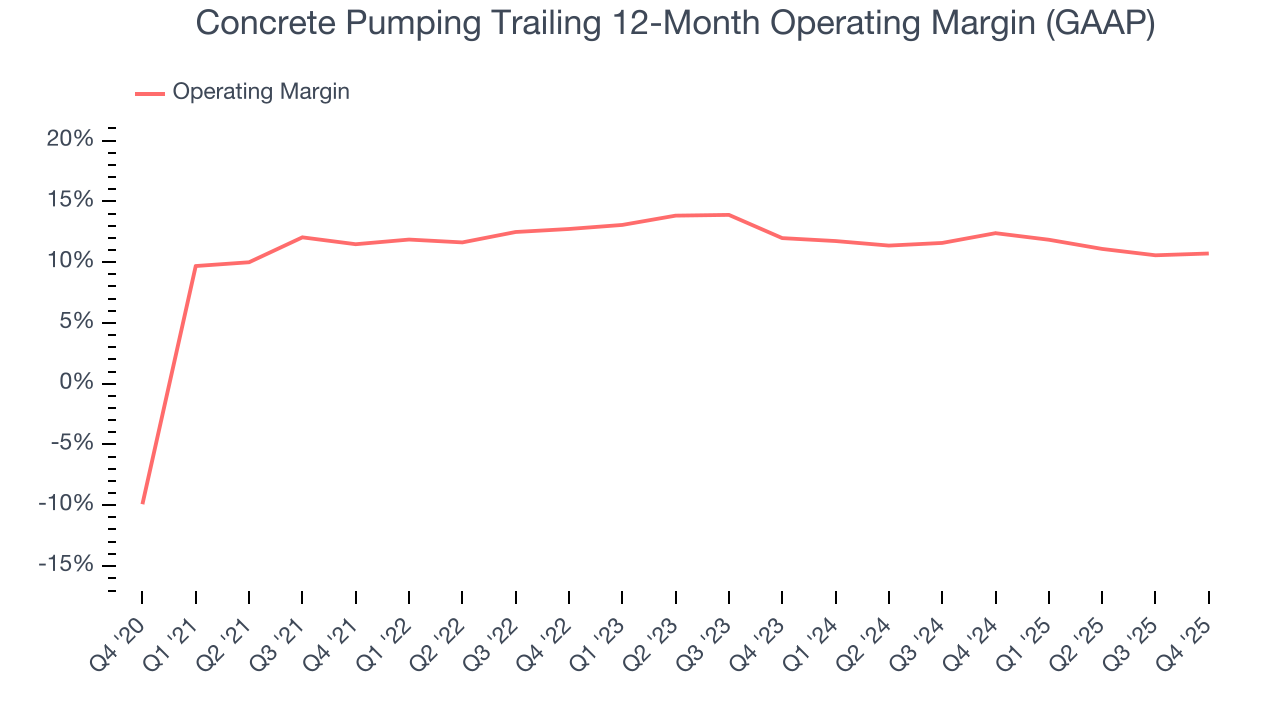

7. Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Concrete Pumping’s operating margin has generally stayed the same over the last 12 months, averaging 11.9% over the last five years. This profitability was top-notch for an industrials business, showing it’s an well-run company with an efficient cost structure. This result isn’t surprising as its high gross margin gives it a favorable starting point.

Analyzing the trend in its profitability, Concrete Pumping’s operating margin might fluctuated slightly but has generally stayed the same over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

In Q4, Concrete Pumping generated an operating margin profit margin of 5%, in line with the same quarter last year. This indicates the company’s cost structure has recently been stable.

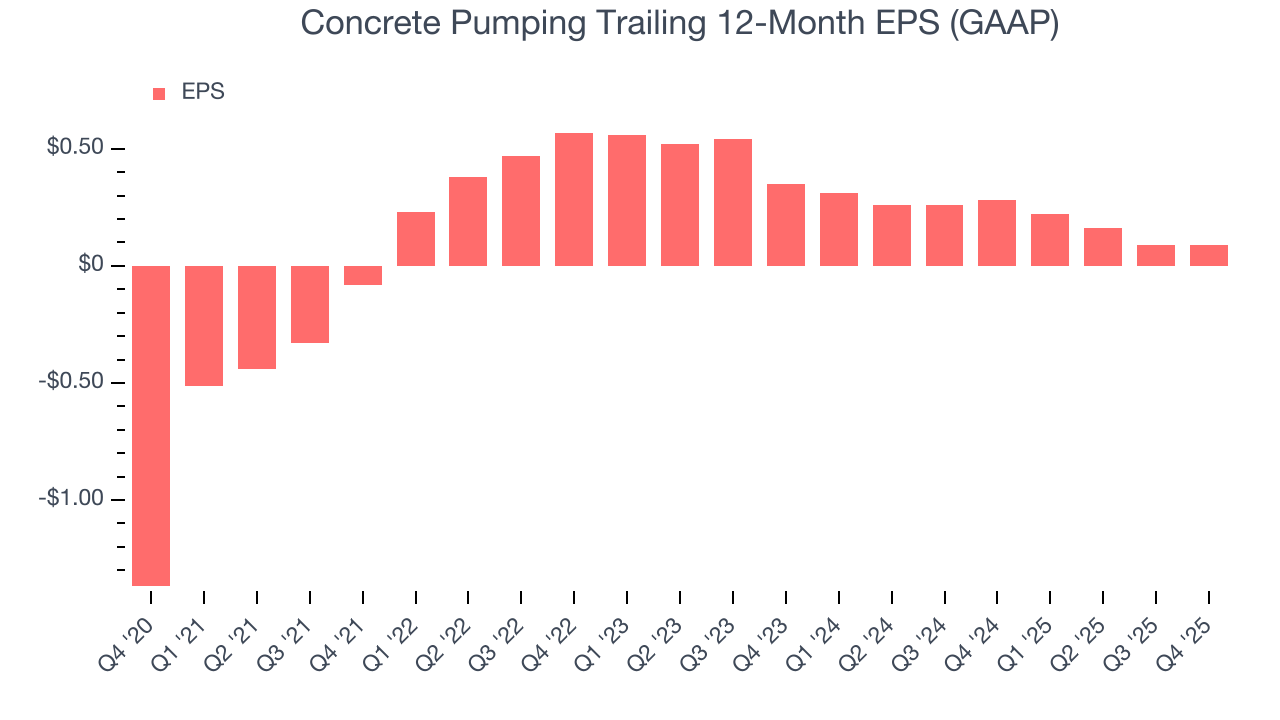

8. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Concrete Pumping’s full-year EPS flipped from negative to positive over the last five years. This is encouraging and shows it’s at a critical moment in its life.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

Sadly for Concrete Pumping, its EPS declined by more than its revenue over the last two years, dropping 49.3%. This tells us the company struggled to adjust to shrinking demand.

In Q4, Concrete Pumping reported EPS of negative $0.06, in line with the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Concrete Pumping’s full-year EPS of $0.09 to grow 63%.

9. Cash Is King

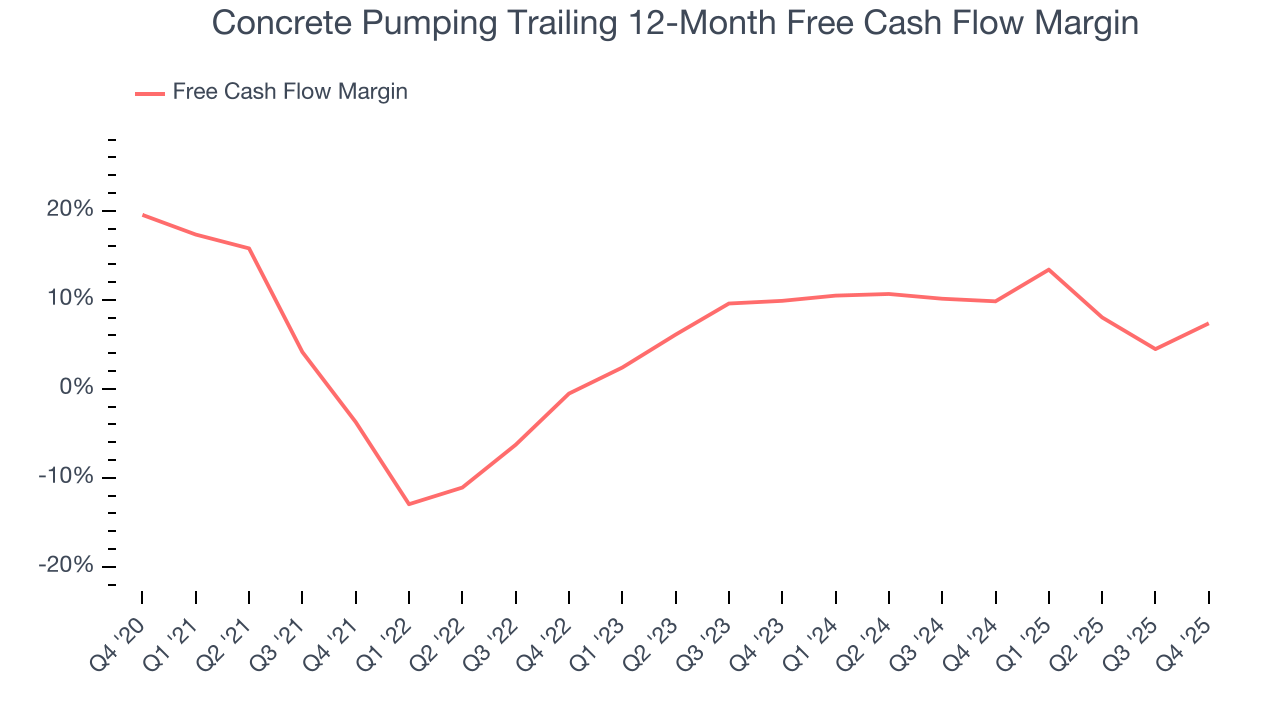

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

Concrete Pumping has shown mediocre cash profitability relative to peers over the last five years, giving the company fewer opportunities to return capital to shareholders. Its free cash flow margin averaged 5%, below what we’d expect for an industrials business. The divergence from its good operating margin stems from its capital-intensive business model, which requires Concrete Pumping to make large cash investments in working capital and capital expenditures.

Taking a step back, an encouraging sign is that Concrete Pumping’s margin expanded by 11.1 percentage points during that time. The company’s improvement shows it’s heading in the right direction, and we can see it became a less capital-intensive business because its free cash flow profitability rose while its operating profitability was flat.

Concrete Pumping’s free cash flow clocked in at $11.85 million in Q4, equivalent to a 13.1% margin. This result was good as its margin was 12.9 percentage points higher than in the same quarter last year, building on its favorable historical trend.

10. Return on Invested Capital (ROIC)

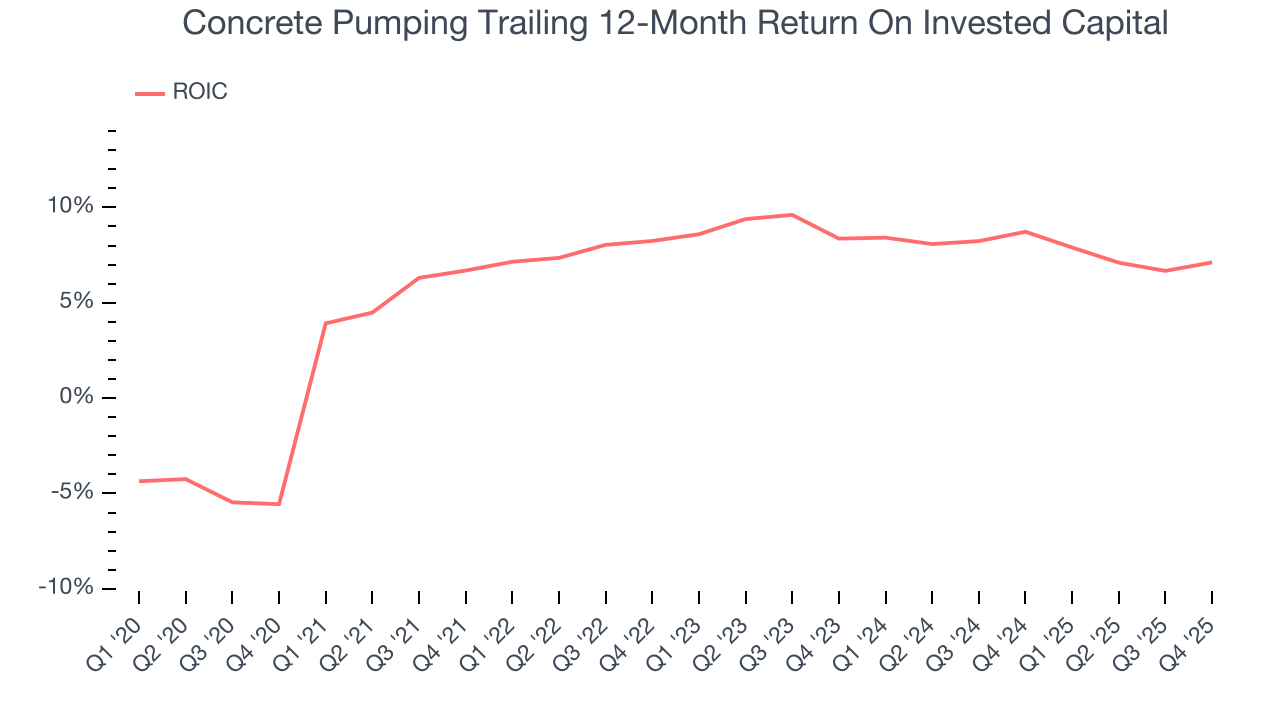

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Concrete Pumping historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 7.8%, somewhat low compared to the best industrials companies that consistently pump out 20%+.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Unfortunately, Concrete Pumping’s ROIC has stayed the same over the last few years. If the company wants to become an investable business, it must improve its returns by generating more profitable growth.

11. Balance Sheet Assessment

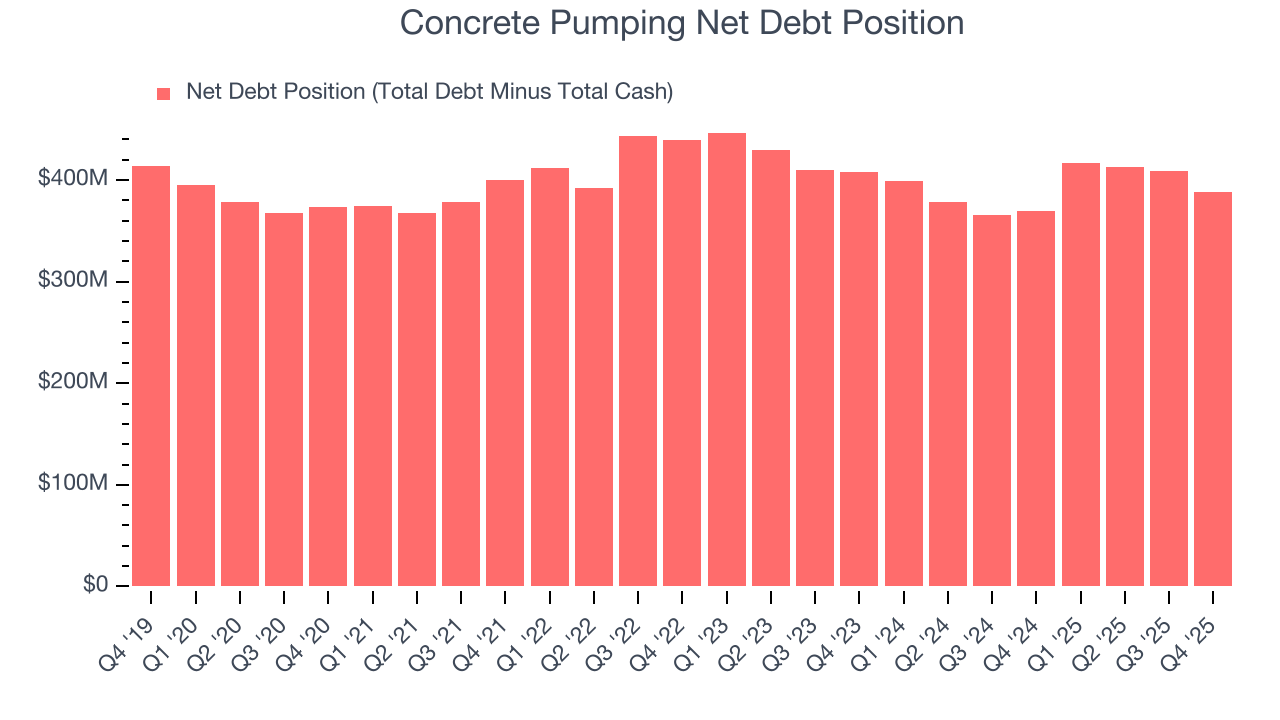

Concrete Pumping reported $53.02 million of cash and $441.5 million of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $98.03 million of EBITDA over the last 12 months, we view Concrete Pumping’s 4.0× net-debt-to-EBITDA ratio as safe. We also see its $16.54 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

12. Key Takeaways from Concrete Pumping’s Q4 Results

It was good to see Concrete Pumping beat analysts’ EPS expectations this quarter. We were also excited its EBITDA outperformed Wall Street’s estimates by a wide margin. On the other hand, its full-year EBITDA guidance missed. Overall, we think this was a solid quarter with some key areas of upside. The stock remained flat at $6.80 immediately after reporting.

13. Is Now The Time To Buy Concrete Pumping?

Updated: March 19, 2026 at 11:25 PM EDT

When considering an investment in Concrete Pumping, investors should account for its valuation and business qualities as well as what’s happened in the latest quarter.

Concrete Pumping’s business quality ultimately falls short of our standards. First off, its revenue growth was uninspiring over the last five years, and analysts expect its demand to deteriorate over the next 12 months. While its rising cash profitability gives it more optionality, the downside is its relatively low ROIC suggests management has struggled to find compelling investment opportunities. On top of that, its low free cash flow margins give it little breathing room.

Concrete Pumping’s P/E ratio based on the next 12 months is 45.1x. Investors with a higher risk tolerance might like the company, but we think the potential downside is too great. We're fairly confident there are better stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $8 on the company (compared to the current share price of $6.87).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.