Clover Health (CLOV)

Clover Health catches our eye, but its cash burn shows it only has 21 months of runway left.― StockStory Analyst Team

1. News

2. Summary

Why Clover Health Is Not Exciting

Founded in 2014 to improve healthcare for America's seniors through technology, Clover Health (NASDAQ:CLOV) provides Medicare Advantage plans for seniors with a focus on affordable care and uses its proprietary Clover Assistant software to help physicians manage patient care.

- Historical adjusted operating margin losses point to an inefficient cost structure

- Negative free cash flow raises questions about the return timeline for its investments

- Short cash runway increases the probability of a capital raise that dilutes existing shareholders

Clover Health has some noteworthy aspects, but we wouldn’t invest until its EBITDA can comfortably service its debt.

Why There Are Better Opportunities Than Clover Health

Clover Health’s stock price of $1.82 implies a valuation ratio of 22.7x forward P/E. This multiple is higher than most healthcare companies, and we think it’s quite expensive for the quality you get.

We’d rather invest in similarly-priced but higher-quality companies with more reliable earnings growth.

3. Clover Health (CLOV) Research Report: Q4 CY2025 Update

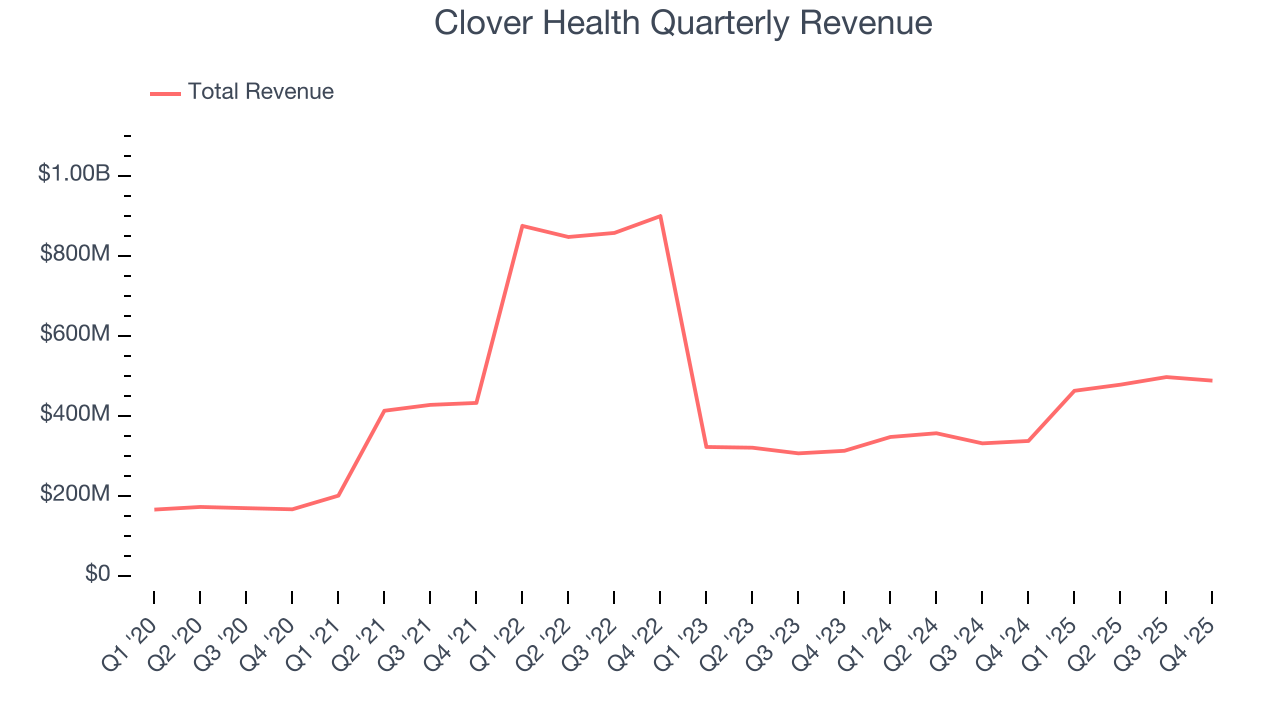

Health insurance company Clover Health (NASDAQ:CLOV) reported Q4 CY2025 results beating Wall Street’s revenue expectations, with sales up 44.7% year on year to $487.7 million. Its non-GAAP loss of $0.05 per share was in line with analysts’ consensus estimates.

Clover Health (CLOV) Q4 CY2025 Highlights:

- Revenue: $487.7 million vs analyst estimates of $467.1 million (44.7% year-on-year growth, 4.4% beat)

- Adjusted EPS: -$0.05 vs analyst estimates of -$0.05 (in line)

- Adjusted EBITDA: -$23.33 million (-4.8% margin, 399% year-on-year decline)

- EBITDA guidance for the upcoming financial year 2026 is $60 million at the midpoint, below analyst estimates of $60.81 million

- Operating Margin: -10.1%, down from -6.4% in the same quarter last year

- Free Cash Flow was -$68.75 million compared to -$86.15 million in the same quarter last year

- Customers: 113,803, up from 109,226 in the previous quarter

- Market Capitalization: $954.9 million

Company Overview

Founded in 2014 to improve healthcare for America's seniors through technology, Clover Health (NASDAQ:CLOV) provides Medicare Advantage plans for seniors with a focus on affordable care and uses its proprietary Clover Assistant software to help physicians manage patient care.

Clover Health operates primarily in the Medicare Advantage (MA) market, offering both Preferred Provider Organization (PPO) and Health Maintenance Organization (HMO) plans across five states and 200 counties. The company differentiates itself by providing low out-of-pocket costs for primary care and specialist visits, and often offers the same cost-sharing for both in-network and out-of-network primary care providers, giving members greater flexibility in their healthcare choices.

At the core of Clover's business model is its Clover Assistant platform, a cloud-based software tool that synthesizes millions of data points daily from various sources including claims, medical charts, medication data, and diagnostic information. This technology uses machine learning and clinical rules to generate personalized insights for healthcare providers at the point of care. For example, a physician seeing a diabetic patient might receive alerts about missed screenings, medication adherence issues, or potential complications based on the patient's comprehensive health history.

The company also operates Clover Home Care, an in-home primary care program targeting medically complex patients with multiple chronic conditions. This program allows physicians to deliver care directly in patients' homes, using the Clover Assistant to access patient data and receive clinical recommendations during these visits.

Clover Health generates revenue primarily through capitated payments from the Centers for Medicare & Medicaid Services (CMS) for each Medicare Advantage member enrolled in its plans. The company aims to manage healthcare costs by empowering providers with data-driven insights that can lead to earlier disease detection and more effective chronic condition management.

The company has made serving underserved markets a priority, focusing on Medicare beneficiaries who identify as people of color, those with multiple chronic conditions, and those living in areas of socioeconomic deprivation.

4. Health Insurance Providers

Upfront premiums collected by health insurers lead to reliable revenue, but profitability ultimately depends on accurate risk assessments and the ability to control medical costs. Health insurers are also highly sensitive to regulatory changes and economic conditions such as unemployment. Going forward, the industry faces tailwinds from an aging population, increasing demand for personalized healthcare services, and advancements in data analytics to improve cost management. However, continued regulatory scrutiny on pricing practices, the potential for government-led reforms such as expanded public healthcare options, and inflation in medical costs could add volatility to margins. One big debate among investors is the long-term impact of AI and whether it will help underwriting, fraud detection, and claims processing or whether it may wade into ethical grey areas like reinforcing biases and widening disparities in medical care.

Clover Health competes with large national insurers like UnitedHealth, Aetna, Humana, Cigna, Centene, and Elevance Health, as well as regional players such as Blue Cross Blue Shield affiliates. It also faces competition from newer tech-focused Medicare Advantage providers like Alignment Health, Devoted Health, and Oscar Health, as well as provider-sponsored plans.

5. Revenue Scale

Larger companies benefit from economies of scale, where fixed costs like infrastructure, technology, and administration are spread over a higher volume of goods or services, reducing the cost per unit. Scale can also lead to bargaining power with suppliers, greater brand recognition, and more investment firepower. A virtuous cycle can ensue if a scaled company plays its cards right.

With just $1.92 billion in revenue over the past 12 months, Clover Health is a small company in an industry where scale matters. This makes it difficult to build trust with customers because healthcare is heavily regulated, complex, and resource-intensive.

6. Revenue Growth

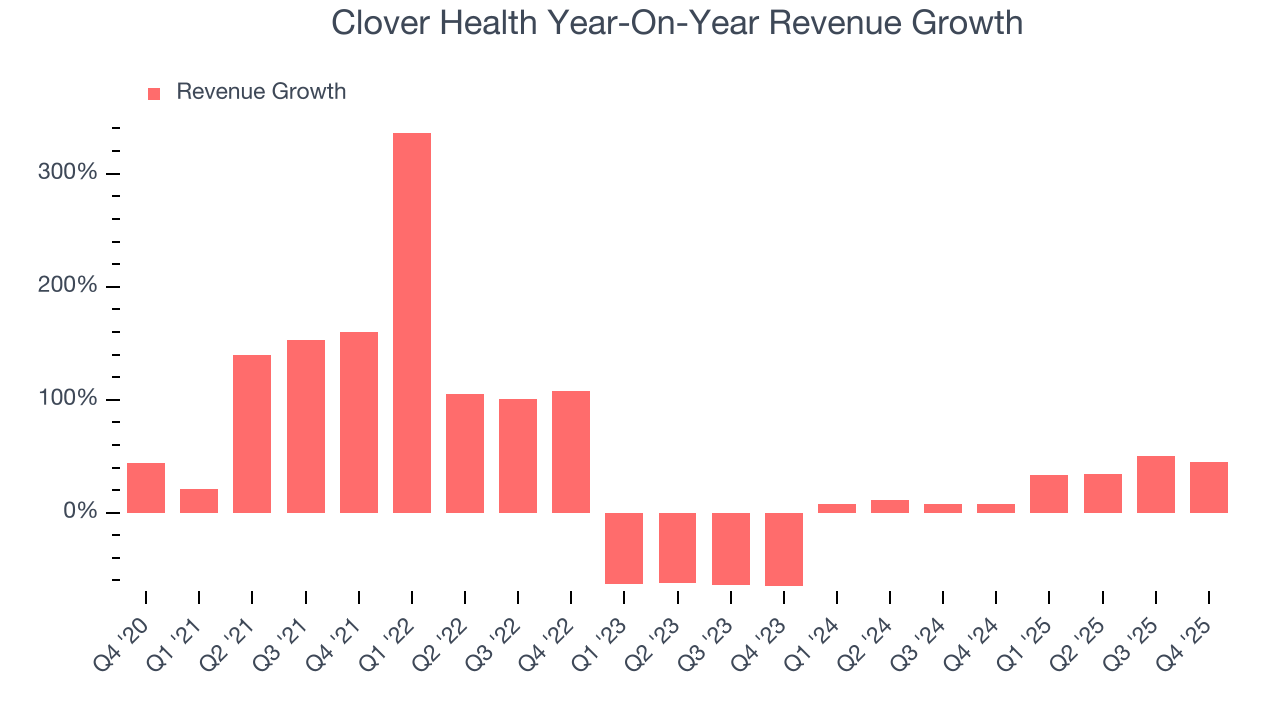

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Luckily, Clover Health’s sales grew at an excellent 23.4% compounded annual growth rate over the last five years. Its growth beat the average healthcare company and shows its offerings resonate with customers.

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. Clover Health’s annualized revenue growth of 23.6% over the last two years aligns with its five-year trend, suggesting its demand was predictably strong.

This quarter, Clover Health reported magnificent year-on-year revenue growth of 44.7%, and its $487.7 million of revenue beat Wall Street’s estimates by 4.4%.

Looking ahead, sell-side analysts expect revenue to grow 49.6% over the next 12 months, an improvement versus the last two years. This projection is eye-popping and indicates its newer products and services will fuel better top-line performance.

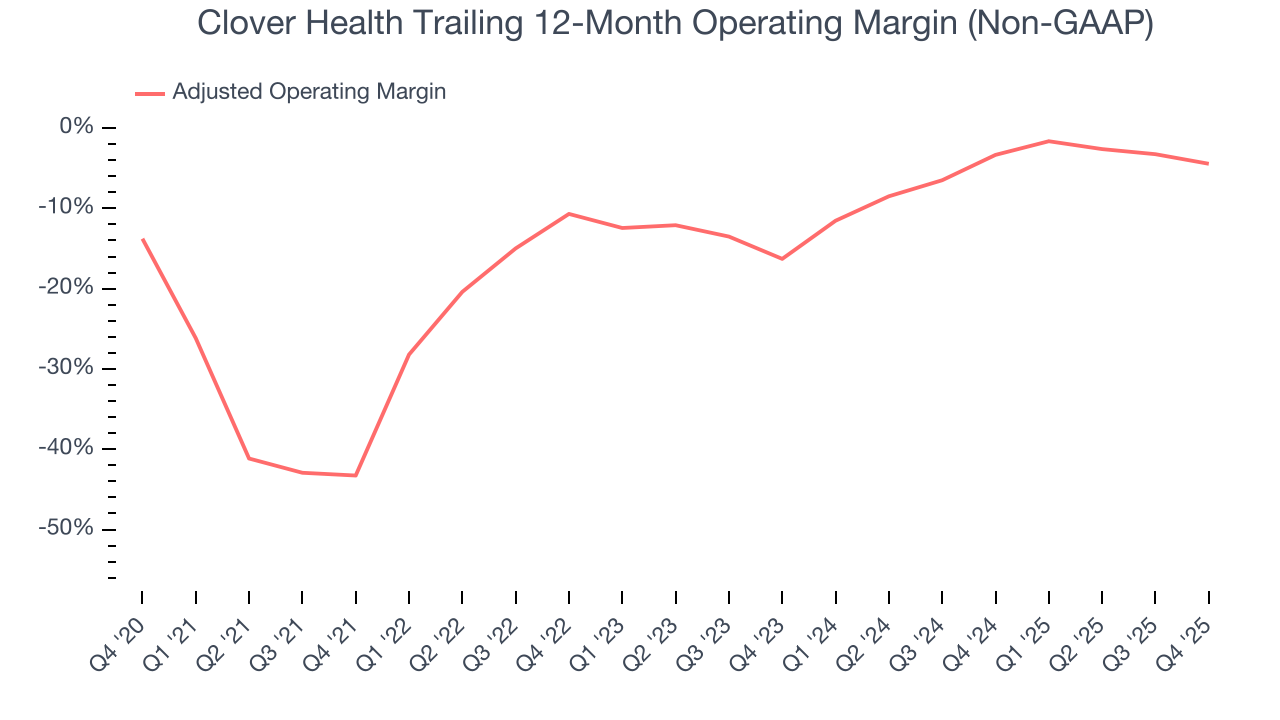

7. Adjusted Operating Margin

Adjusted operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies because it excludes non-recurring expenses, interest on debt, and taxes.

Clover Health’s high expenses have contributed to an average adjusted operating margin of negative 14.2% over the last five years. Unprofitable healthcare companies require extra attention because they could get caught swimming naked when the tide goes out. It’s hard to trust that the business can endure a full cycle.

On the plus side, Clover Health’s adjusted operating margin rose by 38.8 percentage points over the last five years, as its sales growth gave it operating leverage. Zooming in on its more recent performance, we can see the company’s trajectory is intact as its margin has also increased by 11.8 percentage points on a two-year basis. These data points are very encouraging and show momentum is on its side.

Clover Health’s adjusted operating margin was negative 10.1% this quarter.

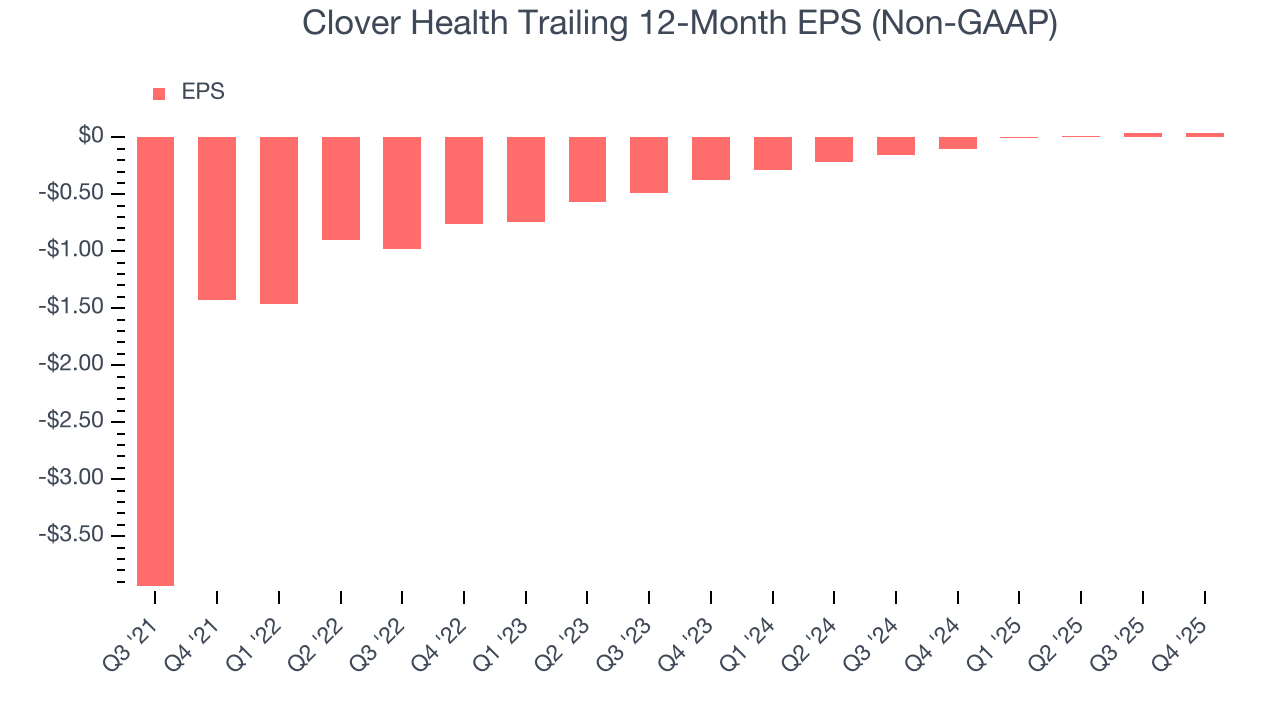

8. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Clover Health’s full-year EPS flipped from negative to positive over the last four years. This is a good sign and shows it’s at an inflection point.

In Q4, Clover Health reported adjusted EPS of negative $0.05, in line with the same quarter last year. This print beat analysts’ estimates by 8.2%. Over the next 12 months, Wall Street expects Clover Health’s full-year EPS of $0.04 to grow 93.9%.

9. Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

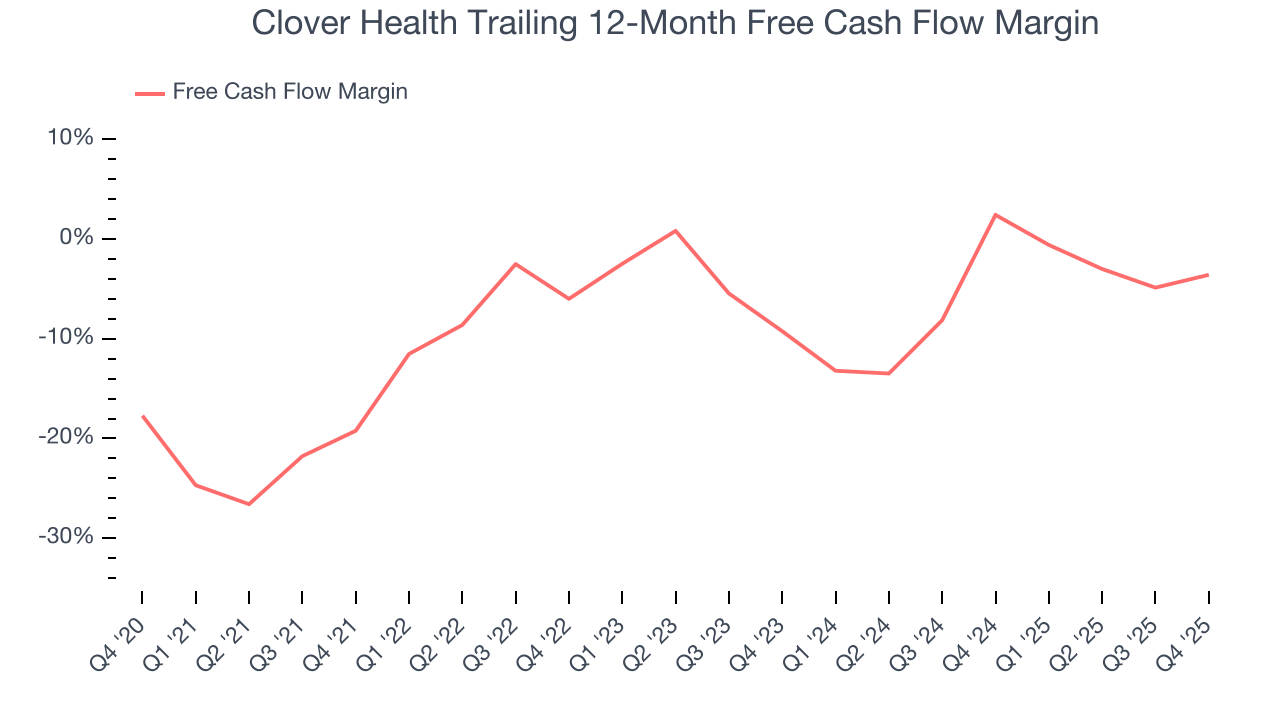

Clover Health’s demanding reinvestments have consumed many resources over the last five years, contributing to an average free cash flow margin of negative 6.8%. This means it lit $6.77 of cash on fire for every $100 in revenue.

Taking a step back, an encouraging sign is that Clover Health’s margin expanded by 15.6 percentage points during that time. The company’s improvement shows it’s heading in the right direction, and continued increases could help it achieve long-term cash profitability.

Clover Health burned through $68.75 million of cash in Q4, equivalent to a negative 14.1% margin. The company’s cash burn was similar to its $86.15 million of lost cash in the same quarter last year.

10. Balance Sheet Risk

As long-term investors, the risk we care about most is the permanent loss of capital, which can happen when a company goes bankrupt or raises money from a disadvantaged position. This is separate from short-term stock price volatility, something we are much less bothered by.

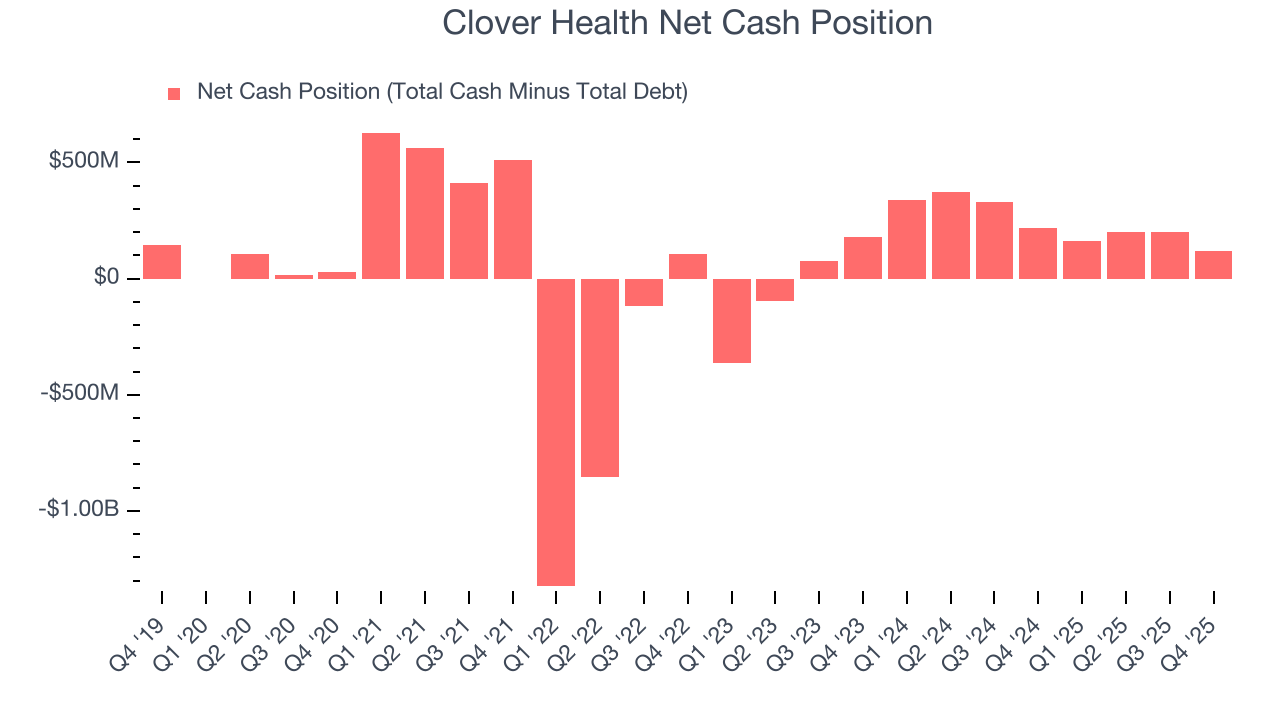

Clover Health burned through $68.98 million of cash over the last year. With $120.3 million of cash and no debt on its balance sheet, the company has around 21 months of runway left.

Unless the Clover Health’s fundamentals change quickly, it might find itself in a position where it must raise capital from investors to continue operating. Whether that would be favorable is unclear because dilution is a headwind for shareholder returns.

We remain cautious of Clover Health until it generates consistent free cash flow or any of its announced financing plans materialize on its balance sheet.

11. Key Takeaways from Clover Health’s Q4 Results

We enjoyed seeing Clover Health beat analysts’ revenue expectations this quarter. We were also glad its EPS was in line with Wall Street’s estimates. On the other hand, its full-year EBITDA guidance slightly missed. Overall, we think this was a solid quarter with some key areas of upside. The stock remained flat at $1.83 immediately after reporting.

12. Is Now The Time To Buy Clover Health?

Updated: March 26, 2026 at 12:24 AM EDT

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in Clover Health.

Aside from its balance sheet, Clover Health is a pretty good company. For starters, its revenue growth was impressive over the last five years and is expected to accelerate over the next 12 months. And while its operating margins reveal poor profitability compared to other healthcare companies, its rising cash profitability gives it more optionality. Additionally, Clover Health’s expanding adjusted operating margin shows the business has become more efficient.

Clover Health’s P/E ratio based on the next 12 months is 22.7x. Despite its notable business characteristics, we’d hold off for now because its balance sheet concerns us. We recommend investors interested in the company wait until it reduces its leverage or increases its profits before getting involved.

Wall Street analysts have a consensus one-year price target of $2.82 on the company (compared to the current share price of $1.82).