Coinbase (COIN)

Coinbase is interesting. Its marriage of growth and profitability makes it a strong business with attractive upside.― StockStory Analyst Team

1. News

2. Summary

Why Coinbase Is Interesting

Widely regarded as the face of crypto, Coinbase (NASDAQ:COIN) is a blockchain infrastructure company updating the financial system with its trading, staking, stablecoin, and other payment solutions.

- Platform is difficult to replicate at scale and leads to a best-in-class gross margin of 85.9%

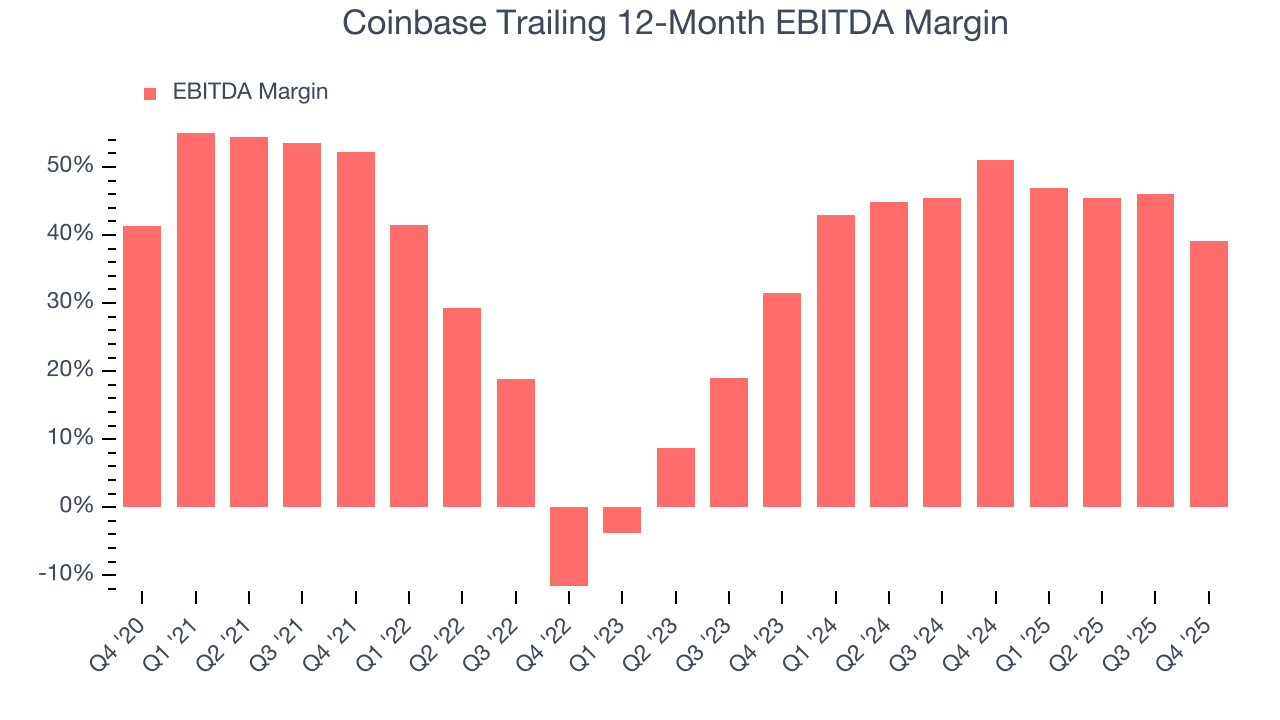

- Excellent EBITDA margin highlights the strength of its business model, and its rise over the last few years was fueled by some leverage on its fixed costs

- One pitfall is its estimated sales growth of 1.6% for the next 12 months implies demand will slow from its three-year trend

Coinbase has the potential to be a high-quality business. Consider adding this company to your watchlist.

Why Should You Watch Coinbase

At $152.20 per share, Coinbase trades at 12.8x forward EV/EBITDA. This valuation multiple hovers around the sector average.

We’re not buyers right now, but we’ll keep tabs on this stock. We prefer to invest in higher-quality companies that trade at comparable valuation multiples.

3. Coinbase (COIN) Research Report: Q4 CY2025 Update

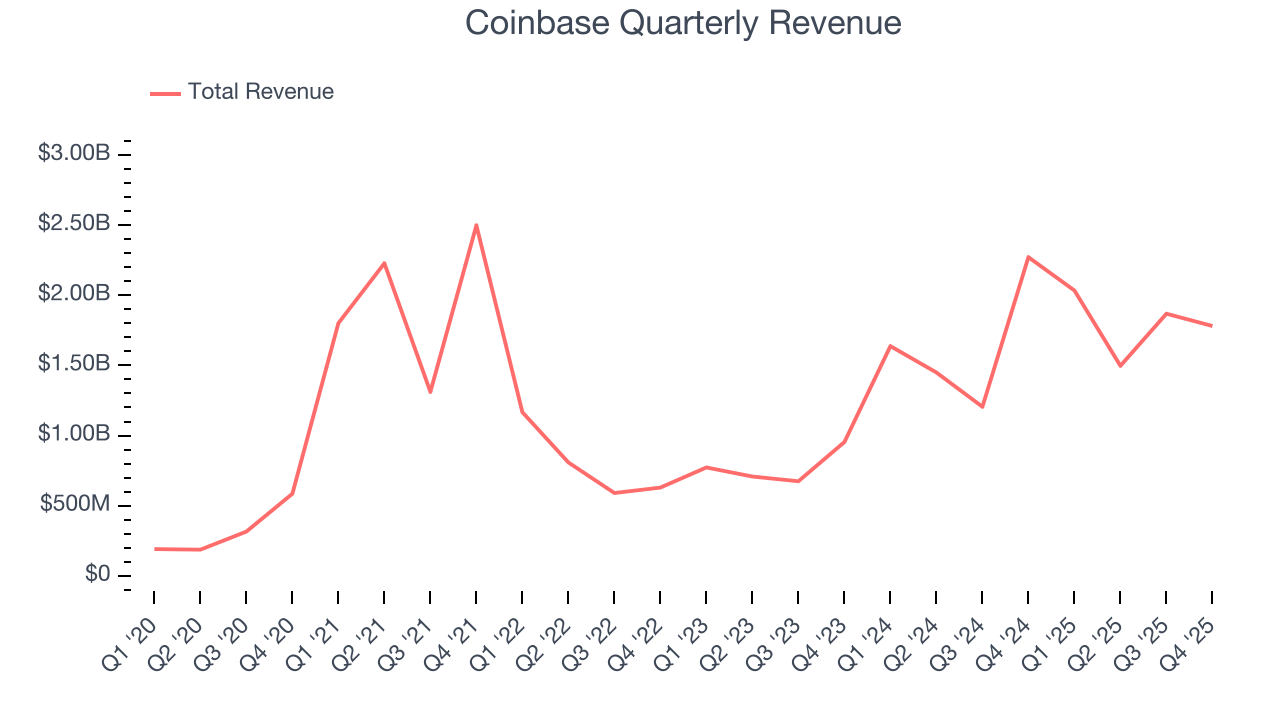

Blockchain infrastructure company Coinbase (NASDAQ:COIN) fell short of the market’s revenue expectations in Q4 CY2025, with sales falling 21.6% year on year to $1.78 billion. Its non-GAAP profit of $0.66 per share was 31.2% below analysts’ consensus estimates.

Coinbase (COIN) Q4 CY2025 Highlights:

- Revenue: $1.78 billion vs analyst estimates of $1.83 billion (21.6% year-on-year decline, 2.5% miss)

- Adjusted EPS: $0.66 vs analyst expectations of $0.96 (31.2% miss)

- Adjusted EBITDA: $566 million vs analyst estimates of $680.8 million (31.8% margin, 16.9% miss)

- Operating Margin: 15.4%, down from 45.5% in the same quarter last year

- Free Cash Flow was $3.07 billion, up from -$784.5 million in the previous quarter

- Market Capitalization: $41.31 billion

Company Overview

Widely regarded as the face of crypto, Coinbase (NASDAQ:COIN) is a blockchain infrastructure company updating the financial system with its trading, staking, stablecoin, and other payment solutions.

What exactly is the blockchain? Simply put, it’s a technology that makes payments faster, cheaper, and safer while making money independent of governments, central banks, and large financial institutions. Due to its benefits over legacy payment rails, this infrastructure fundamentally improves traditional finance, just like how the internet changed paper-based news and information sharing.

The main player supplying the picks and shovels for this nascent industry is Coinbase, which was founded in 2012 to inject sound financial infrastructure into underdeveloped and corrupt countries.

In its early days, Coinbase primarily acted as a cryptocurrency exchange, facilitating trades and taking a cut of each transaction. The exchange is still its largest source of revenue, but it reinvented itself in 2017/2018 when a protocol named Ethereum surfaced the concept of “smart contracts”, or self-executing programs that automate cryptocurrency creation, distribution, and governance.

Ethereum was pivotal as it enabled much more than speculative trading. For example, USDC, one of Coinbase’s most popular products, is a stablecoin built on Ethereum that tracks the value of the U.S. dollar by backing each newly minted token with U.S. Treasury Bills. It’s revolutionary because it enables faster transfer speeds (instant vs 3 days for banks), cheaper fees (less than one cent), and higher security thanks to the blockchain’s distributed computing system.

Other notable Coinbase products include Prime (institutional trading platform), Digital Wallet (think PayPal for crypto), Developer Platform (helps businesses integrate crypto payments), the Base protocol (makes Ethereum more efficient), and staking services (validates blockchain transactions on behalf of users to generate gas fees). These offerings combined with Coinbase Ventures, its investment arm, amplify the company’s influence over the industry and diversify its business from the violent cyclicality in crypto markets.

4. Financial Technology

Financial technology companies benefit from the increasing consumer demand for digital payments, banking, and finance. Tailwinds fueling this trend include e-commerce along with improvements in blockchain infrastructure and AI-driven credit underwriting, which make access to money faster and cheaper. Despite regulatory scrutiny and resistance from traditional financial institutions, fintechs are poised for long-term growth as they disrupt legacy systems by expanding financial services to underserved population segments.

Coinbase’s competitors include Robinhood (NASDAQ:HOOD) and private companies like Binance, Kraken, Gemini, and Crypto.com.

5. Revenue Growth

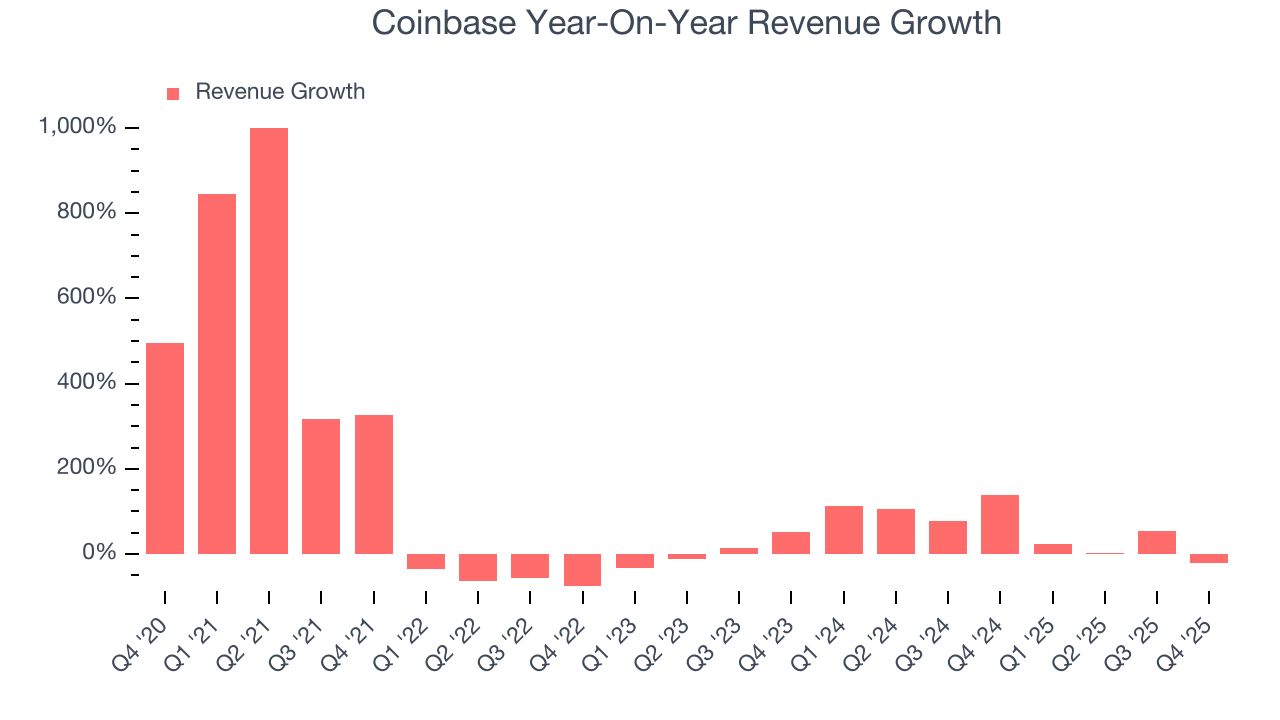

A company’s long-term sales performance is one signal of its overall quality. Any business can have short-term success, but a top-tier one grows for years. Luckily, Coinbase’s sales grew at an incredible 41.2% compounded annual growth rate over the last five years. Its growth beat the average consumer internet company and shows its offerings resonate with customers, a helpful starting point for our analysis.

Long-term growth is the most important, but within consumer internet, a half-decade historical view may miss new innovations or demand cycles. Coinbase’s annualized revenue growth of 52% over the last two years is above its five-year trend, suggesting its demand was strong and recently accelerated.

This quarter, Coinbase missed Wall Street’s estimates and reported a rather uninspiring 21.6% year-on-year revenue decline, generating $1.78 billion of revenue.

Looking ahead, sell-side analysts expect revenue to grow 14.3% over the next 12 months, a deceleration versus the last two years. Despite the slowdown, this projection is admirable and suggests the market is forecasting success for its products and services.

6. Gross Margin & Pricing Power

A company’s gross profit margin has a significant impact on its ability to exert pricing power, develop new products, and invest in marketing. These factors can determine the winner in a competitive market.

For fintech businesses like Coinbase, gross profit tells us how much money the company gets to keep after covering the base cost of its products and services, which typically include transaction/payment processing, hosting, and bandwidth fees in addition to the costs necessary to onboard customers, such as identity verification.

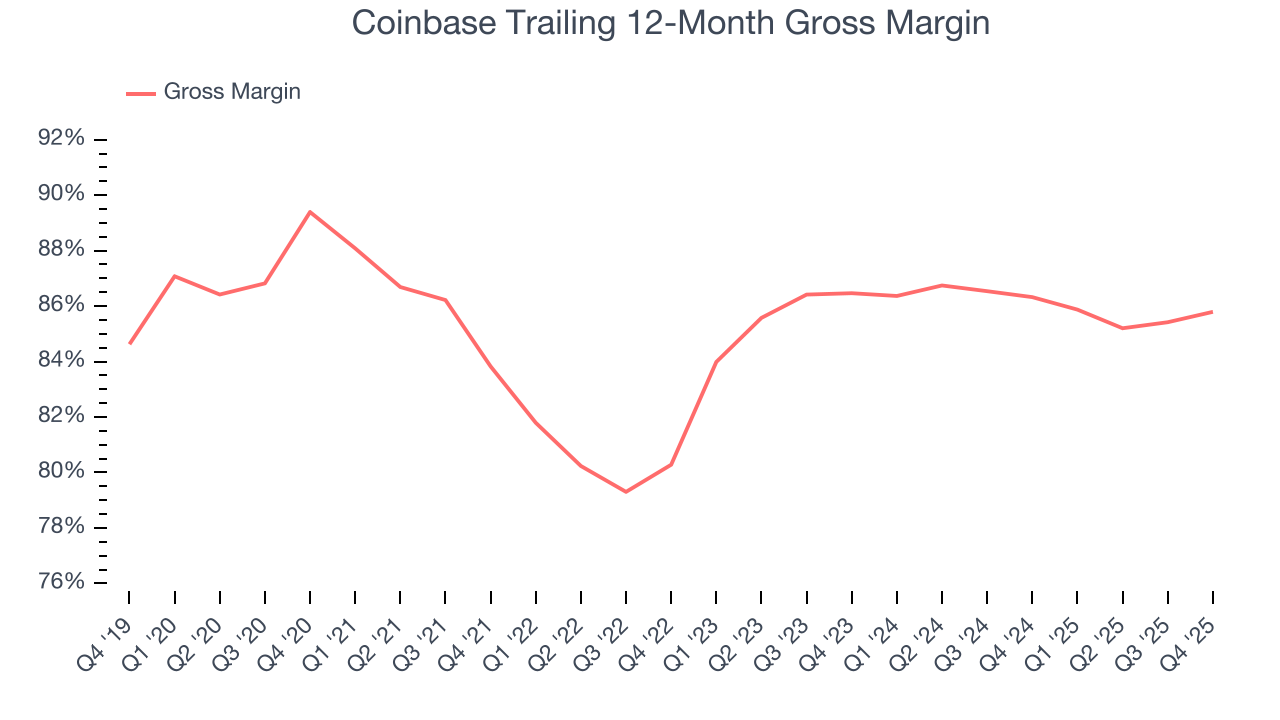

Coinbase’s gross margin is one of the highest in the consumer internet sector, an output of its asset-lite business model and strong pricing power. It also enables the company to fund large investments in product and marketing during periods of rapid growth to achieve higher profits in the future. As you can see below, it averaged an elite 86% gross margin over the last two years. Said differently, roughly $86.05 was left to spend on selling, marketing, and R&D for every $100 in revenue.

Coinbase produced a 87.7% gross profit margin in Q4 , marking a 1.7 percentage point increase from 86% in the same quarter last year. Zooming out, the company’s full-year margin has remained steady over the past 12 months, suggesting its input costs have been stable and it isn’t under pressure to lower prices.

7. User Acquisition Efficiency

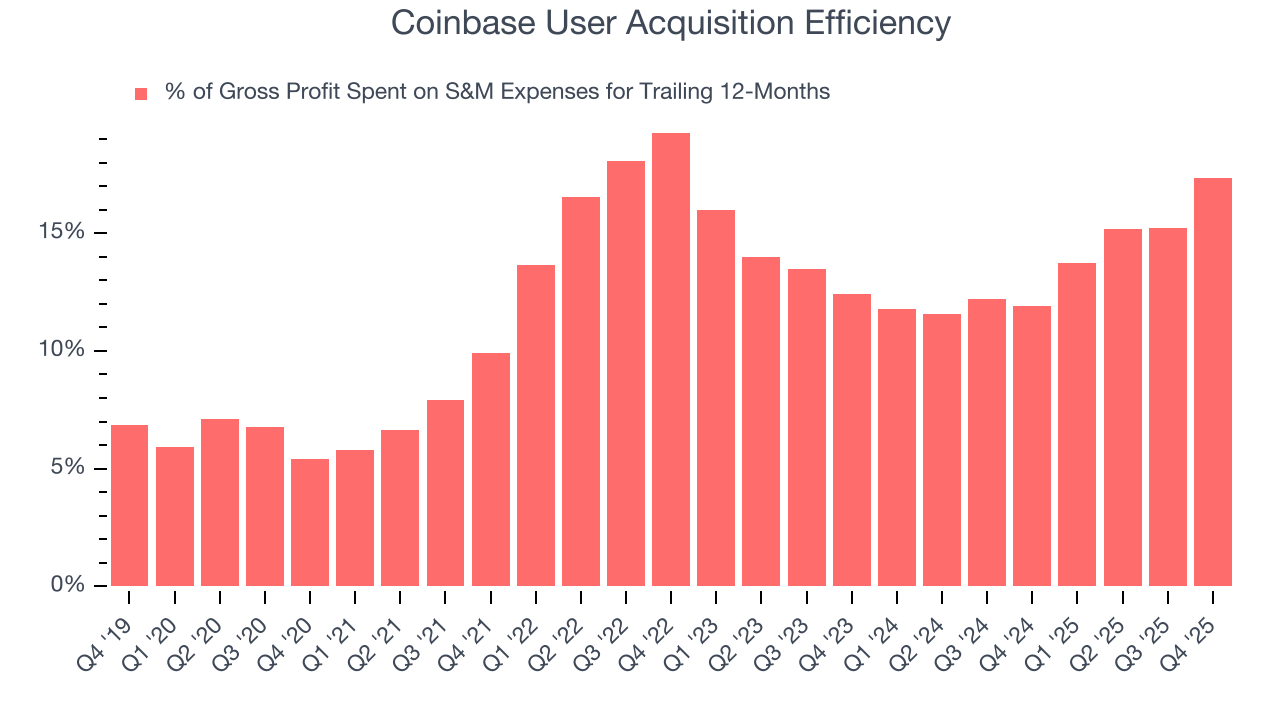

Unlike enterprise software that’s typically sold by dedicated sales teams, consumer internet businesses like Coinbase grow from a combination of product virality, paid advertisement, and incentives.

Coinbase is extremely efficient at acquiring new users, spending only 17.4% of its gross profit on sales and marketing expenses over the last year. This efficiency indicates that it has a highly differentiated product offering and strong brand reputation, giving Coinbase the freedom to invest its resources into new growth initiatives while maintaining optionality.

8. EBITDA

Investors regularly analyze operating income to understand a company’s profitability. Similarly, EBITDA is a common profitability metric for consumer internet companies because it excludes various one-time or non-cash expenses, offering a better perspective of the business’s profit potential.

Coinbase has been a well-oiled machine over the last two years. It demonstrated elite profitability for a consumer internet business, boasting an average EBITDA margin of 44.8%. This result isn’t surprising as its high gross margin gives it a favorable starting point.

Looking at the trend in its profitability, Coinbase’s EBITDA margin decreased by 13.1 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

In Q4, Coinbase generated an EBITDA margin profit margin of 31.8%, down 25 percentage points year on year. Conversely, its gross margin actually rose, so we can assume its recent inefficiencies were driven by increased operating expenses like marketing, R&D, and administrative overhead.

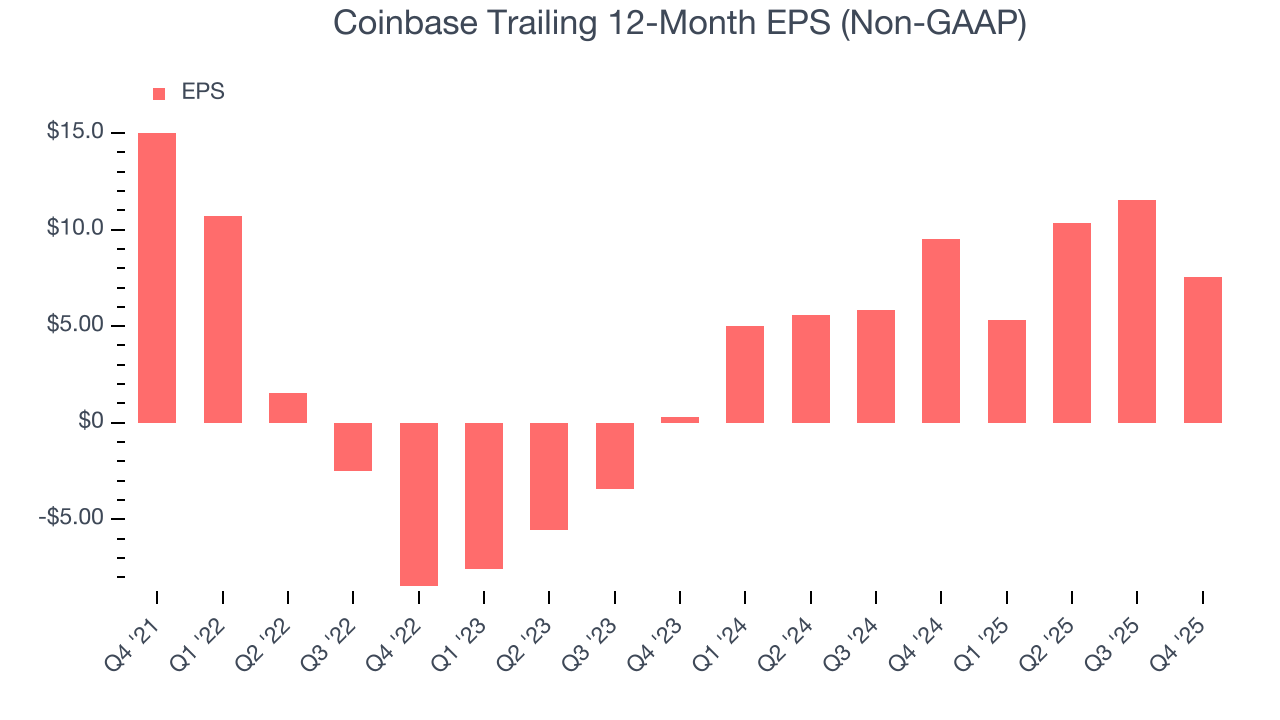

9. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Coinbase’s full-year EPS dropped 80%, or 15.8% annually, over the last four years. We’ll keep a close eye on the company as diminishing earnings could imply changing secular trends and preferences.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

Coinbase’s EPS grew at an astounding 428% compounded annual growth rate over the last two years, higher than its 52% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

In Q4, Coinbase reported adjusted EPS of $0.66, down from $4.68 in the same quarter last year. This print missed analysts’ estimates. Over the next 12 months, Wall Street expects Coinbase’s full-year EPS of $7.54 to shrink by 15.7%.

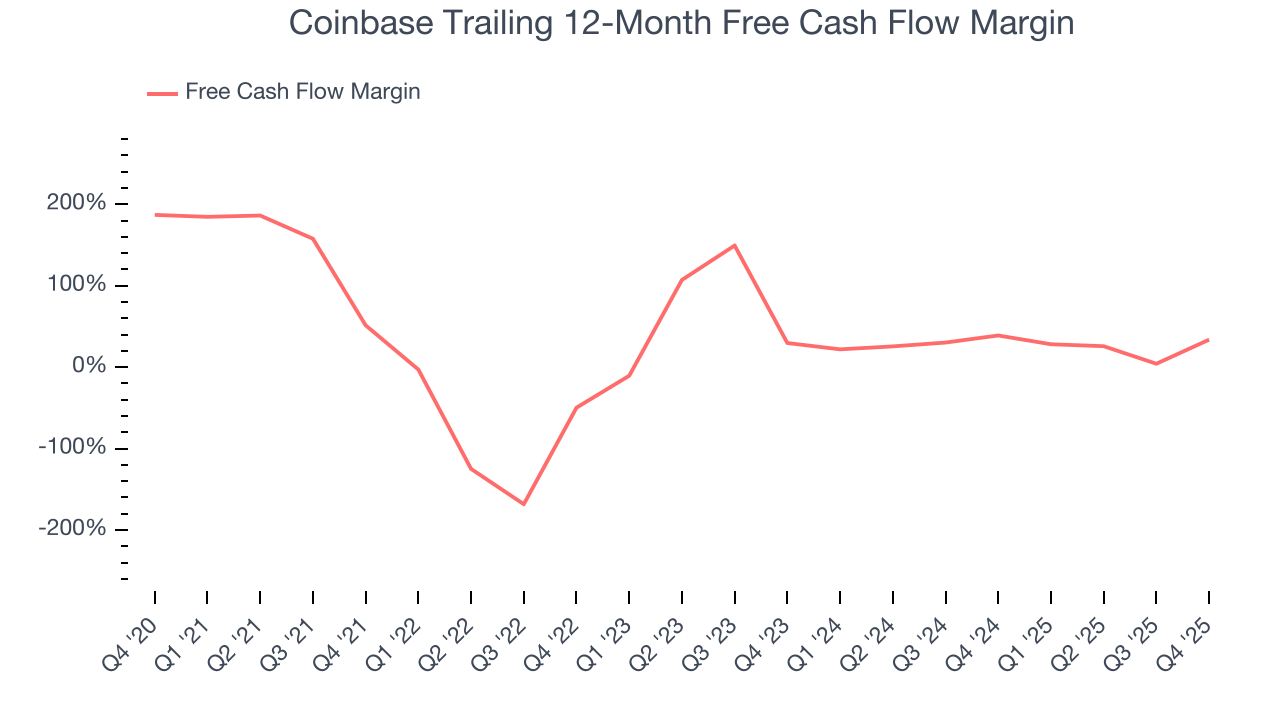

10. Cash Is King

Although EBITDA is undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

Coinbase has shown terrific cash profitability, driven by its lucrative business model and cost-effective customer acquisition strategy that enable it to stay ahead of the competition through investments in new products rather than sales and marketing. The company’s free cash flow margin was among the best in the consumer internet sector, averaging an eye-popping 36.3% over the last two years.

Taking a step back, we can see that Coinbase’s margin dropped by 17.7 percentage points over the last five years. If its declines continue, it could signal increasing investment needs and capital intensity.

Coinbase’s free cash flow clocked in at $3.07 billion in Q4, equivalent to a 172% margin. This result was good as its margin was 129.6 percentage points higher than in the same quarter last year. Its cash profitability was also above its two-year level, and we hope the company can build on this trend.

11. Balance Sheet Assessment

Companies with more cash than debt have lower bankruptcy risk.

Coinbase is a profitable, well-capitalized company with $11.62 billion of cash and $7.66 billion of debt on its balance sheet. This $3.96 billion net cash position is 9.6% of its market cap and gives it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

12. Key Takeaways from Coinbase’s Q4 Results

We struggled to find many positives in these results. Its revenue missed and its EBITDA fell short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock remained flat at $141.73 immediately after reporting.

13. Is Now The Time To Buy Coinbase?

Updated: February 12, 2026 at 4:17 PM EST

Before investing in or passing on Coinbase, we urge you to understand the company’s business quality (or lack thereof), valuation, and the latest quarterly results - in that order.

For starters, its revenue growth was exceptional over the last five years. And while its projected EPS for the next year is lacking, its admirable gross margins are a wonderful starting point for the overall profitability of the business. Additionally, Coinbase’s powerful free cash flow generation enables it to stay ahead of the competition through consistent reinvestment of profits.

Coinbase’s EV/EBITDA ratio based on the next 12 months is 10x. Looking at the consumer internet space right now, Coinbase trades at a compelling valuation. If you believe in the company and its growth potential, now is an opportune time to buy shares.

Wall Street analysts have a consensus one-year price target of $325.56 on the company (compared to the current share price of $141.73), implying they see 130% upside in buying Coinbase in the short term.