CSX (NASDAQ:CSX) Reports Q2 In Line With Expectations

Adam Hejl /

August 5, 2024

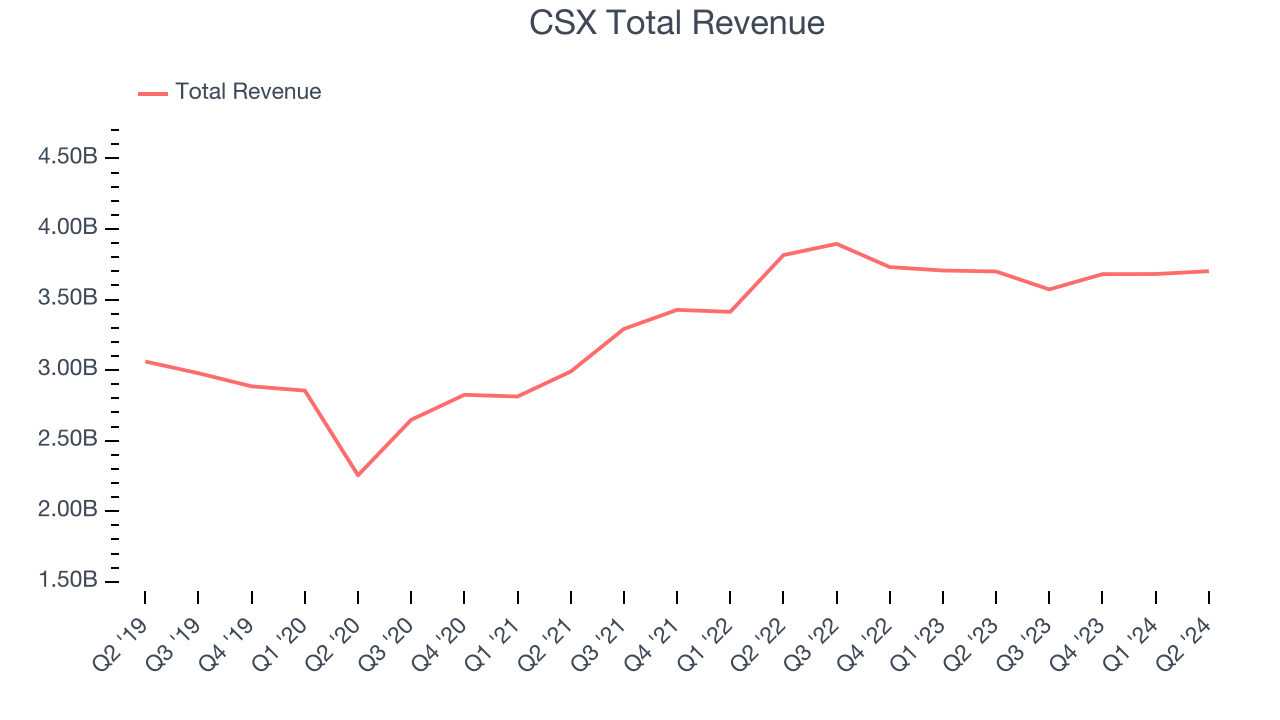

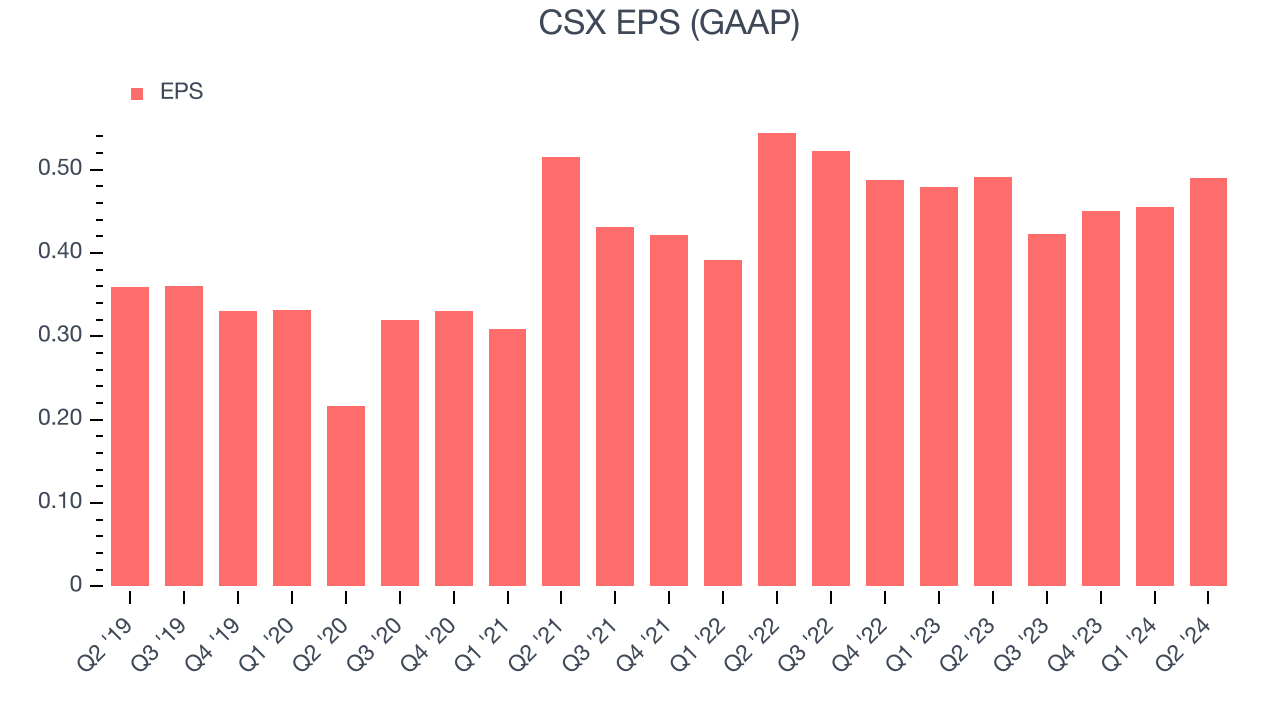

Freight rail services provider CSX (NASDAQ:CSX) reported results in line with analysts' expectations in Q2 CY2024, with revenue flat year on year at $3.70 billion. Its GAAP profit of $0.49 per share was flat year on year.

Is now the time to buy CSX? Find out in our full research report.

CSX (CSX) Q2 CY2024 Highlights:

- Revenue: $3.70 billion vs analyst estimates of $3.70 billion (small miss)

- EPS: $0.49 vs analyst estimates of $0.48 (2.6% beat)

- Gross Margin (GAAP): 52.3%, up from 50.8% in the same quarter last year

- Adjusted EBITDA Margin: 50%, in line with the same quarter last year

- Free Cash Flow of $547 million, similar to the previous quarter

- Sales Volumes rose 2.1% year on year (-3% in the same quarter last year)

- Market Capitalization: $66.62 billion

Established as part of the Chessie System and Seaboard Coast Line Industries merger, CSX (NASDAQ:CSX) is a transportation company specializing in freight rail services.

Rail Transportation

The growth of e-commerce and global trade continues to drive demand for shipping services, presenting opportunities for rail transportation companies. While moving large volumes by rail can be highly cost-efficient for customers compared to air and ground transport, this mode of transportation results in slower delivery times, presenting a trade off. To improve transit times, the industry continues to invest in digitization to optimize fleets, loads, and even braking systems. However, rail transportation companies are still at the whim of economic cycles. Consumer spending, for example, can greatly impact the demand for these companies’ offerings while fuel costs can influence profit margins.

Sales Growth

A company’s long-term performance can give signals about its business quality. Even a bad business can shine for one or two quarters, but a top-tier one tends to grow for years. Over the last five years, CSX grew its sales at a weak 3.5% compounded annual growth rate. This shows it failed to expand in any major way and is a rough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. CSX's recent history shows its demand slowed as its annualized revenue growth of 2.4% over the last two years is below its five-year trend.

We can better understand the company's revenue dynamics by analyzing its sales volumes, which reached 1.58 million in the latest quarter. Over the last two years, CSX's sales volumes were flat. Because this number is lower than its revenue growth, we can see the company benefited from price increases.

This quarter, CSX's $3.70 billion of revenue was flat year on year and in line with Wall Street's estimates. Looking ahead, Wall Street expects sales to grow 4.6% over the next 12 months, an acceleration from this quarter.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) semiconductor stock benefitting from the rise of AI. Click here to access our free report on our favorite semiconductor growth story.

Operating Margin

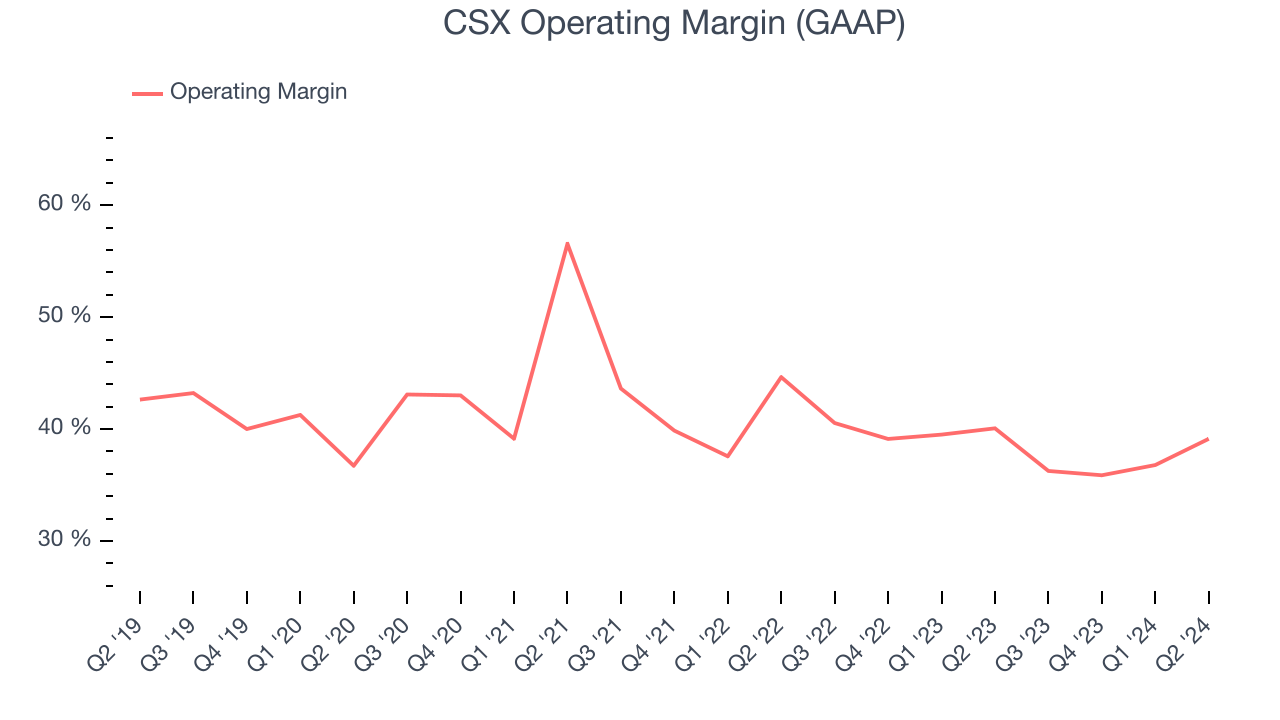

CSX has been a well-oiled machine over the last five years. It demonstrated elite profitability for an industrials business, boasting an average operating margin of 40.7%. This result isn't surprising as its high gross margin gives it a favorable starting point.

Looking at the trend in its profitability, CSX's annual operating margin decreased by 3.5 percentage points over the last five years. Even though its margin is still high, shareholders will want to see CSX become more profitable in the future.

In Q2, CSX generated an operating profit margin of 39.1%, in line with the same quarter last year. This indicates the company's cost structure has recently been stable.

EPS

Analyzing long-term revenue trends tells us about a company's historical growth, but the long-term change in its earnings per share (EPS) points to the profitability of that growth–for example, a company could inflate its sales through excessive spending on advertising and promotions.

CSX's EPS grew at an unimpressive 5.5% compounded annual growth rate over the last five years. This performance was better than its 3.5% annualized revenue growth but doesn't tell us much about its day-to-day operations because its operating margin didn't expand.

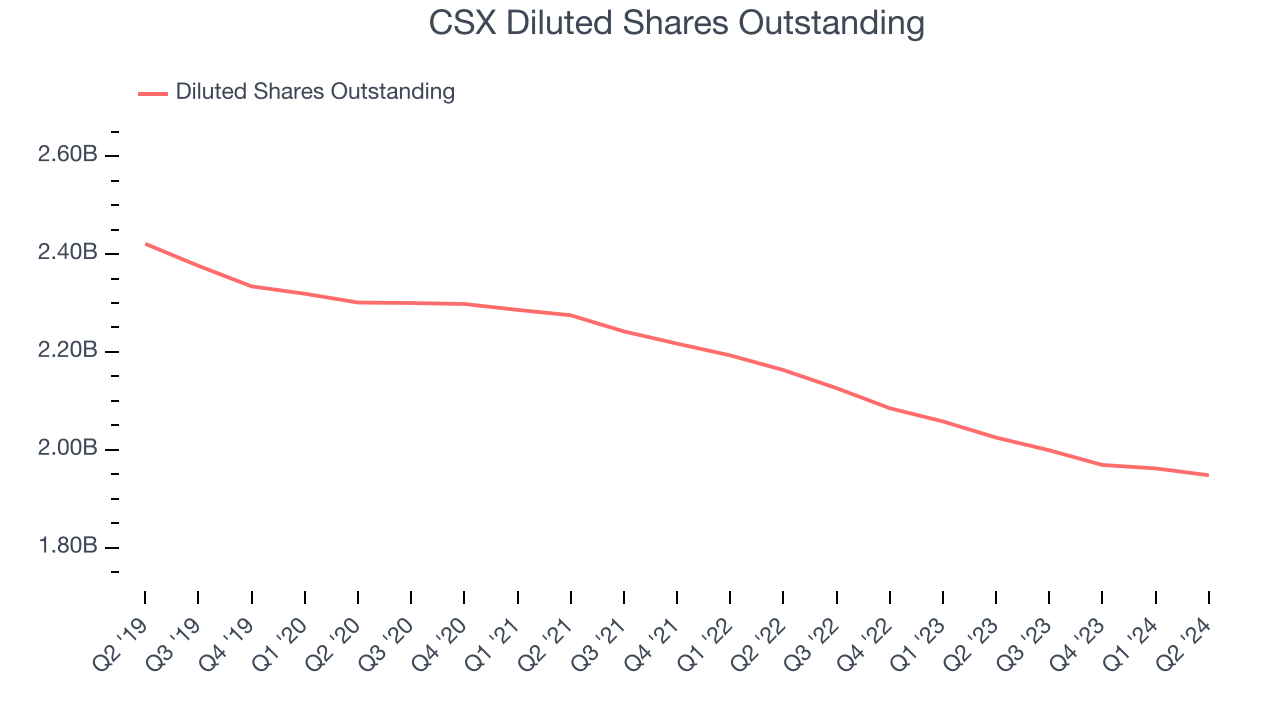

We can take a deeper look into CSX's earnings to better understand the drivers of its performance. A five-year view shows that CSX has repurchased its stock, shrinking its share count by 19.5%. This tells us its EPS outperformed its revenue not because of increased operational efficiency but financial engineering, as buybacks boost per share earnings.

Like with revenue, we also analyze EPS over a shorter period to see if we are missing a change in the business. For CSX, EPS didn't budge over the last two years, a regression from its five-year trend. We hope it can revert to earnings growth in the coming years.

In Q2, CSX reported EPS at $0.49, in line with the same quarter last year. This print beat analysts' estimates by 2.6%. Over the next 12 months, Wall Street expects CSX to grow its earnings. Analysts are projecting its EPS of $1.82 in the last year to climb by 12.6% to $2.05.

Key Takeaways from CSX's Q2 Results

It was encouraging to see CSX beat analysts' volume expectations this quarter. We were also glad its EPS outperformed Wall Street's estimates. Zooming out, we think this was a decent quarter, showing the company is staying on target. The stock remained flat at $33 immediately after reporting.

So should you invest in CSX right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.