Erie Indemnity (ERIE)

We’re firm believers in Erie Indemnity. Its superb 26.7% ROE illustrates its skill in making high-return investments.― StockStory Analyst Team

1. News

2. Summary

Why We Like Erie Indemnity

Operating under a unique business model dating back to 1925, Erie Indemnity (NASDAQ:ERIE) serves as the attorney-in-fact for Erie Insurance Exchange, managing policy issuance, claims handling, and investment services for this reciprocal insurer.

- Market-beating return on equity illustrates that management has a knack for investing in profitable ventures

- Annual book value per share growth of 14% over the past five years was outstanding, reflecting strong capital accumulation this cycle

- Annual revenue growth of 11.5% over the last two years was superb and indicates its market share increased during this cycle

Erie Indemnity is a standout company. This is easily one of the top insurance stocks.

Is Now The Time To Buy Erie Indemnity?

Erie Indemnity’s stock price of $246.92 implies a valuation ratio of 18x forward P/E. While this isn’t a screaming bargain, the long-term outlook is bright for the patient investor.

If you admire the business model, we suggest making it a small position as its high valuation could cause dicey short-term results.

3. Erie Indemnity (ERIE) Research Report: Q4 CY2025 Update

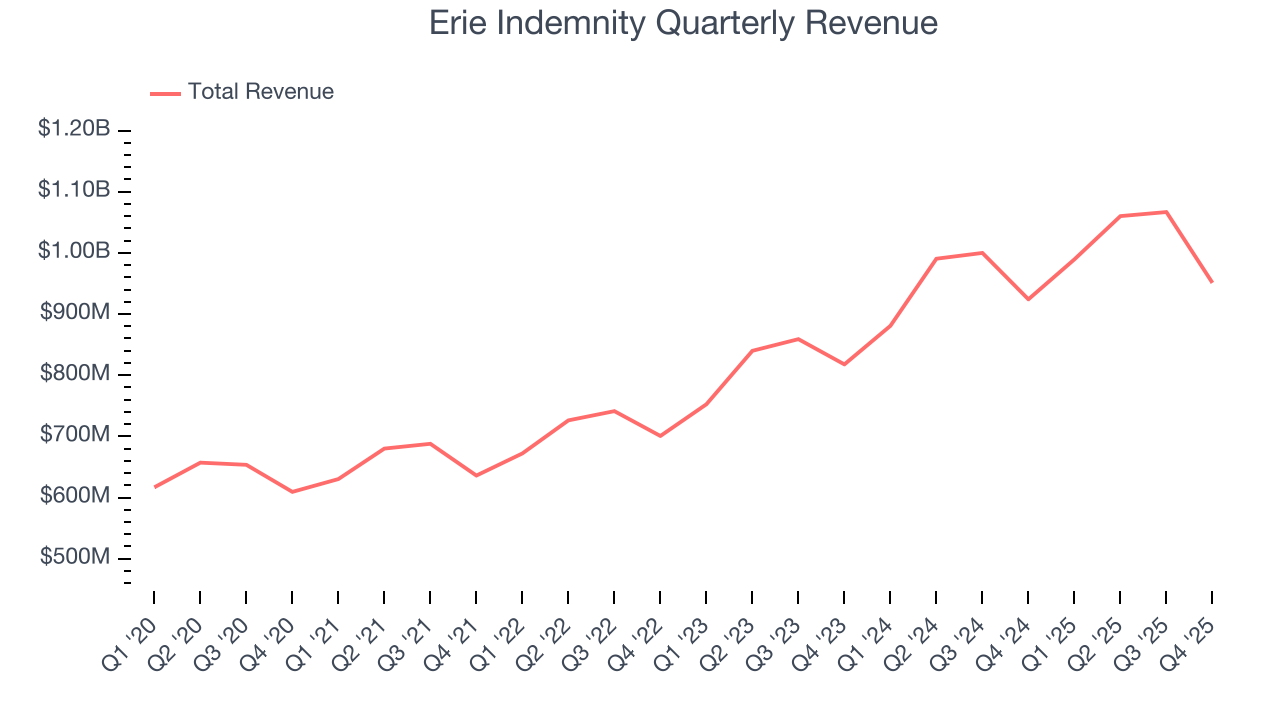

Insurance management company Erie Indemnity (NASDAQ:ERIE) fell short of the market’s revenue expectations in Q4 CY2025 as sales rose 2.9% year on year to $951 million. Its GAAP profit of $1.21 per share was 23.9% below analysts’ consensus estimates.

Erie Indemnity (ERIE) Q4 CY2025 Highlights:

- Revenue: $951 million vs analyst estimates of $975.6 million (2.9% year-on-year growth, 2.5% miss)

- Pre-tax Profit: $82.35 million (8.7% margin)

- EPS (GAAP): $1.21 vs analyst expectations of $1.59 (23.9% miss)

- Market Capitalization: $14.28 billion

Company Overview

Operating under a unique business model dating back to 1925, Erie Indemnity (NASDAQ:ERIE) serves as the attorney-in-fact for Erie Insurance Exchange, managing policy issuance, claims handling, and investment services for this reciprocal insurer.

Erie Indemnity's relationship with Erie Insurance Exchange is governed by a subscriber's agreement—essentially a limited power of attorney—signed by each policyholder. This arrangement authorizes Erie Indemnity to handle various aspects of the insurance business on behalf of the Exchange's subscribers. The company's services fall into two main categories: policy issuance and renewal services, and administrative services.

Policy issuance and renewal services include managing agent compensation (which accounts for about two-thirds of these expenses), sales support, underwriting, and policy processing. Administrative services encompass claims handling, life insurance management, and investment activities. For these services, Erie Indemnity receives management fees based on premiums written by the Exchange.

The Exchange itself operates as a property and casualty insurer with several wholly owned subsidiaries, including Erie Insurance Company and Erie Family Life Insurance Company. It markets exclusively through independent, non-exclusive insurance agencies across its operating territories. The Exchange's business mix consists of approximately 70% personal lines (primarily auto and homeowners insurance) and 30% commercial lines (including commercial multi-peril, commercial auto, and workers compensation).

This symbiotic relationship creates a unique business model where Erie Indemnity's financial performance is directly tied to the growth and stability of the Exchange. The company has no direct competitors for providing these specific management services to the Exchange, though the Exchange itself competes with other property and casualty insurers in its markets. This arrangement provides Erie Indemnity with a stable revenue stream while allowing the Exchange to operate without employees of its own, as required by its structure as a reciprocal insurer.

4. Property & Casualty Insurance

Property & Casualty (P&C) insurers protect individuals and businesses against financial loss from damage to property or from legal liability. This is a cyclical industry, and the sector benefits when there is 'hard market', characterized by strong premium rate increases that outpace loss and cost inflation, resulting in robust underwriting margins. The opposite is true in a 'soft market'. Interest rates also matter, as they determine the yields earned on fixed-income portfolios. On the other hand, P&C insurers face a major secular headwind from the increasing frequency and severity of catastrophe losses due to climate change. Furthermore, the liability side of the business is pressured by 'social inflation'—the trend of rising litigation costs and larger jury awards.

While Erie Indemnity has no direct competitors for its management services to Erie Insurance Exchange, the Exchange itself competes with major property and casualty insurers such as State Farm, Allstate (NYSE:ALL), Progressive (NYSE:PGR), and Travelers (NYSE:TRV) in its regional markets.

5. Revenue Growth

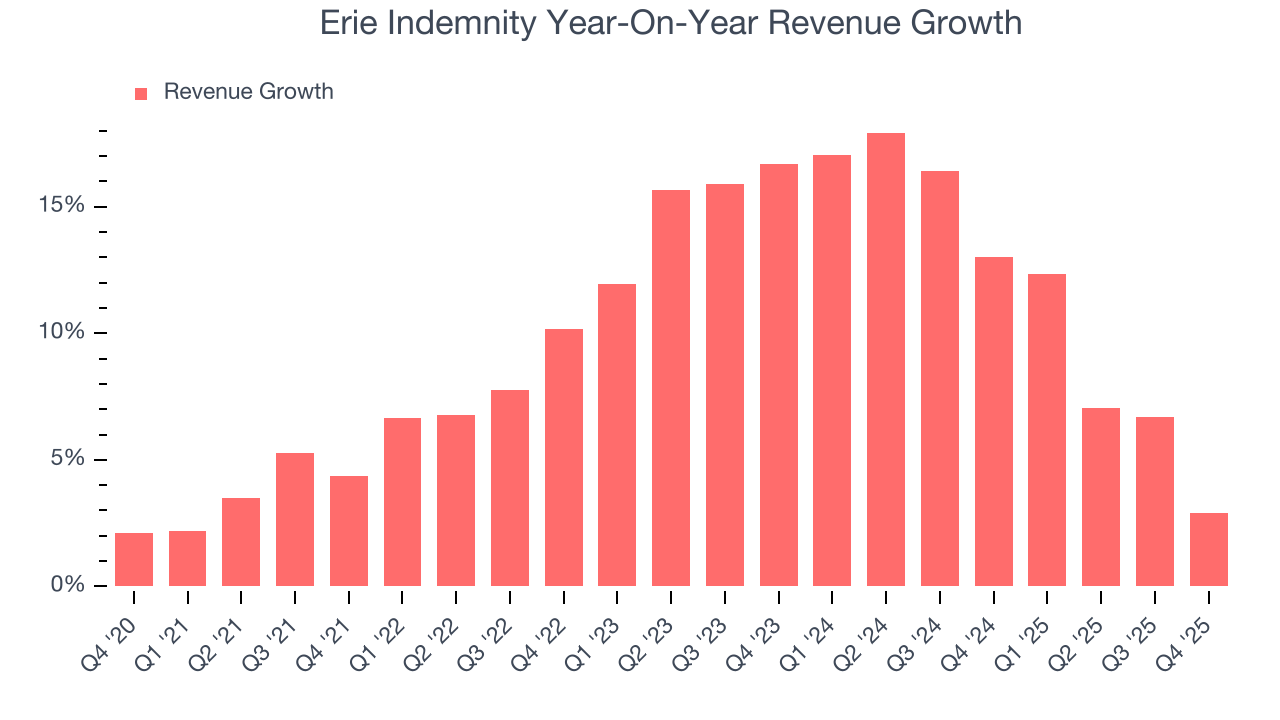

In general, insurance companies earn revenue from three primary sources. The first is the core insurance business itself, often called underwriting and represented in the income statement as premiums earned. The second source is investment income from investing the “float” (premiums collected upfront not yet paid out as claims) in assets such as fixed-income assets and equities. The third is fees from various sources such as policy administration, annuities, or other value-added services. Luckily, Erie Indemnity’s revenue grew at a solid 9.9% compounded annual growth rate over the last five years. Its growth surpassed the average insurance company and shows its offerings resonate with customers, a great starting point for our analysis.

Long-term growth is the most important, but within financials, a half-decade historical view may miss recent interest rate changes and market returns. Erie Indemnity’s annualized revenue growth of 11.5% over the last two years is above its five-year trend, suggesting its demand was strong and recently accelerated.

This quarter, Erie Indemnity’s revenue grew by 2.9% year on year to $951 million, falling short of Wall Street’s estimates.

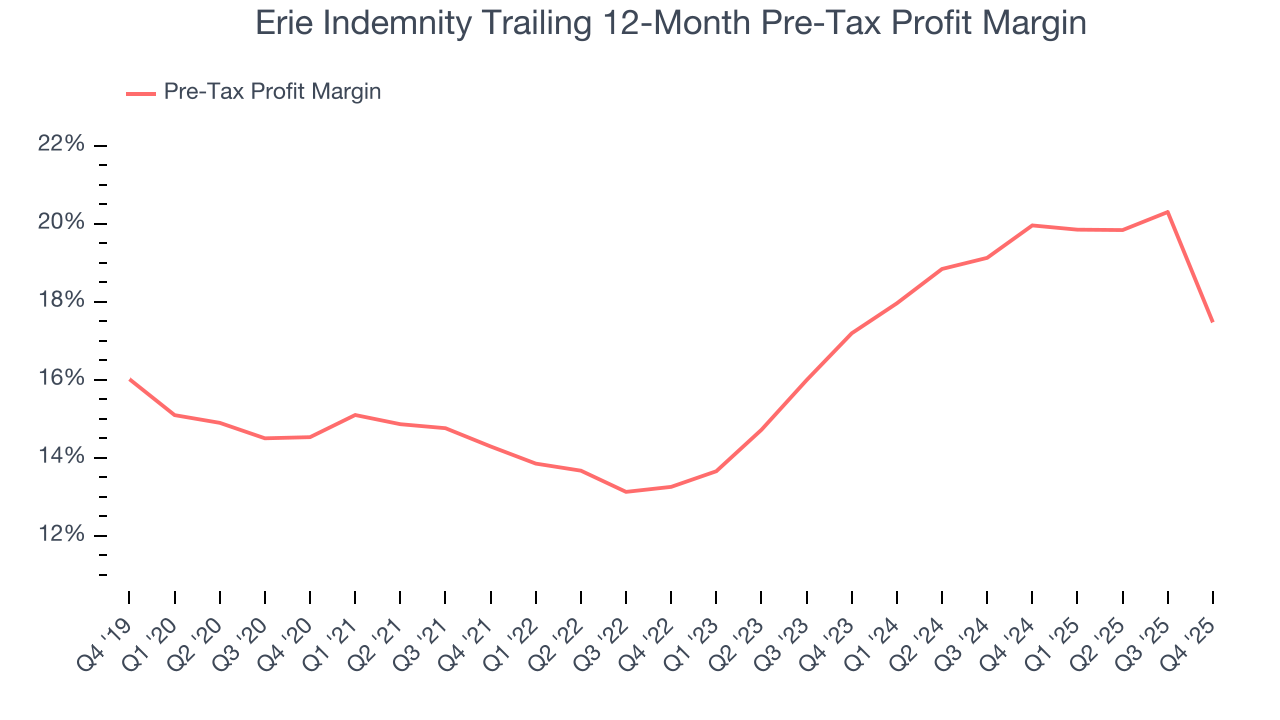

6. Pre-Tax Profit Margin

Revenue growth is one major determinant of business quality, and the efficiency of operations is another. For insurance companies, we look at pre-tax profit rather than the operating margin that defines sectors such as consumer, tech, and industrials.

This is because insurers are balance sheet businesses, where assets and liabilities define the core economics. This means that interest income and expense should be factored into the definition of profit but taxes - which are largely out of a company’s control - should not.

Over the last five years, Erie Indemnity’s pre-tax profit margin has fallen by 2.9 percentage points, going from 14.3% to 17.5%. However, fixed cost leverage was muted more recently as the company’s pre-tax profit margin was flat on a two-year basis.

Erie Indemnity’s pre-tax profit margin came in at 8.7% this quarter. This result was 12.1 percentage points worse than the same quarter last year.

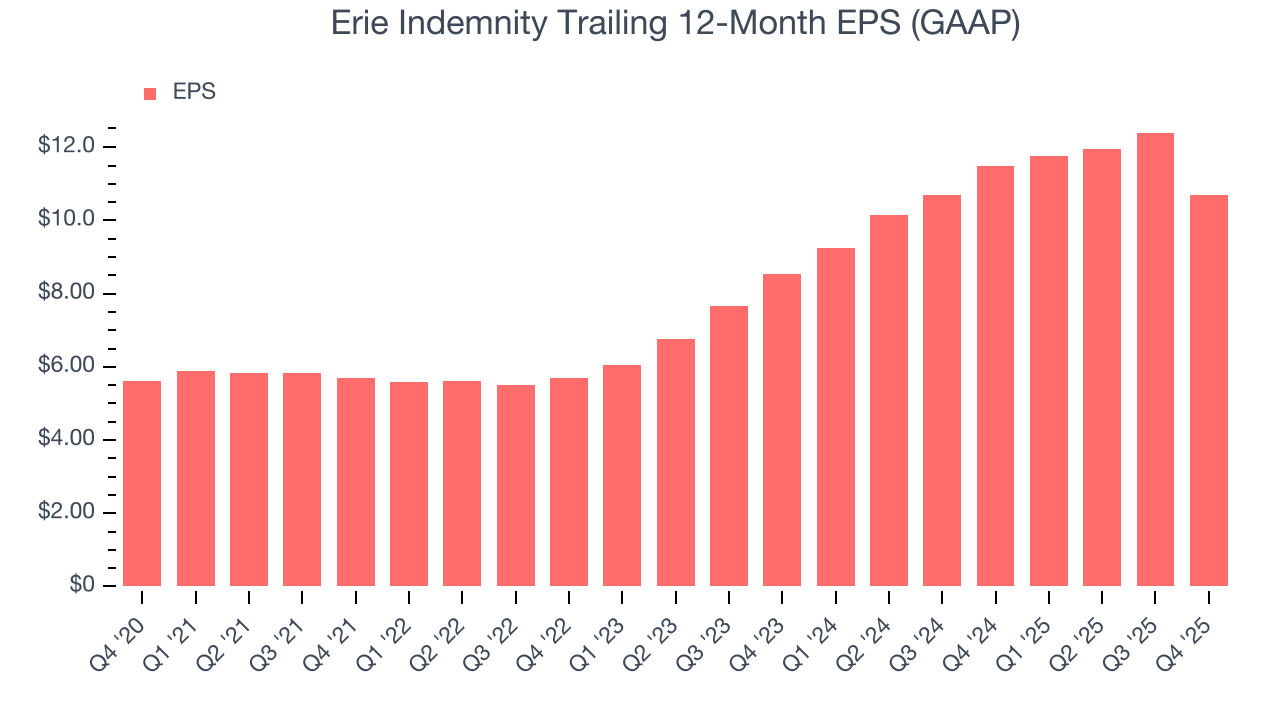

7. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Erie Indemnity’s EPS grew at a solid 13.8% compounded annual growth rate over the last five years, higher than its 9.9% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Erie Indemnity, its two-year annual EPS growth of 12% was lower than its five-year trend. This wasn’t great, but at least the company was successful in other measures of financial health.

In Q4, Erie Indemnity reported EPS of $1.21, down from $2.91 in the same quarter last year. This print missed analysts’ estimates, but we care more about long-term EPS growth than short-term movements. Over the next 12 months, Wall Street expects Erie Indemnity’s full-year EPS of $10.70 to grow 30.9%.

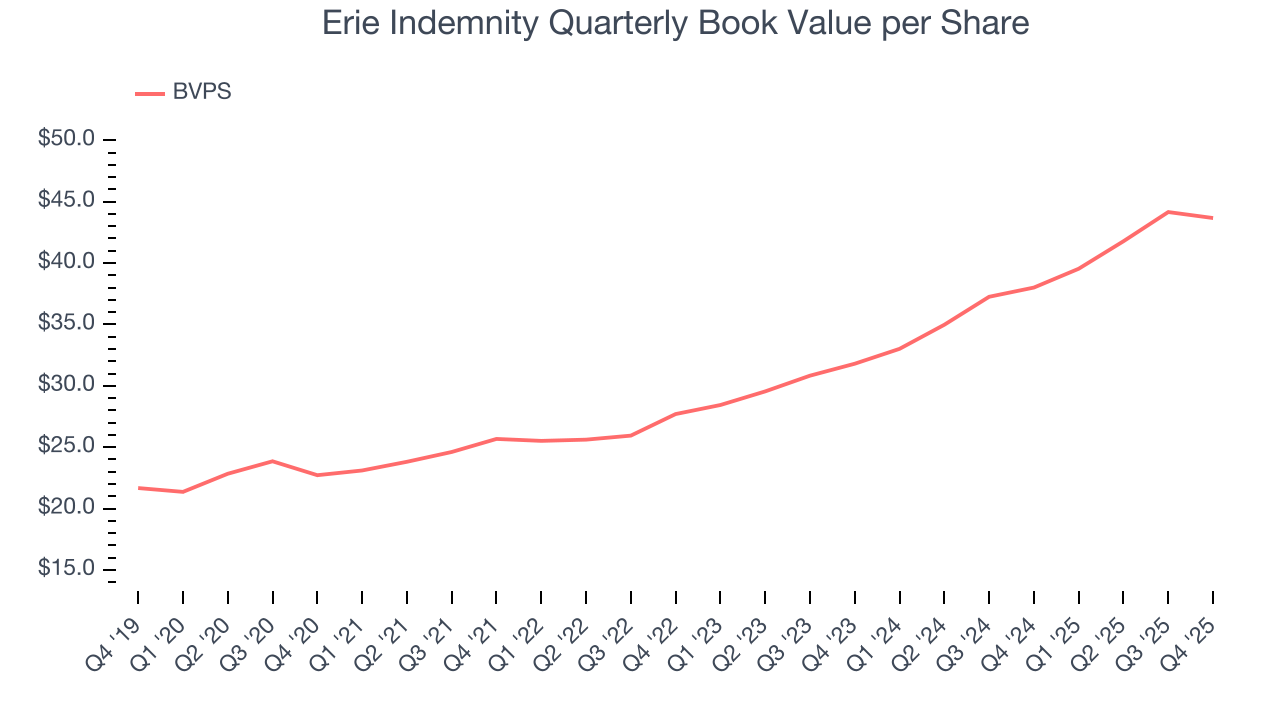

8. Book Value Per Share (BVPS)

Insurance companies are balance sheet businesses, collecting premiums upfront and paying out claims over time. The float – premiums collected but not yet paid out – are invested, creating an asset base supported by a liability structure. Book value captures this dynamic by measuring:

- Assets (investment portfolio, cash, reinsurance recoverables) - liabilities (claim reserves, debt, future policy benefits)

BVPS is essentially the residual value for shareholders.

We therefore consider BVPS very important to track for insurers and a metric that sheds light on business quality because it reflects long-term capital growth and is harder to manipulate than more commonly-used metrics like EPS.

Erie Indemnity’s BVPS grew at an exceptional 14% annual clip over the last five years. BVPS growth has also accelerated recently, growing by 17.2% annually over the last two years from $31.80 to $43.67 per share.

9. Balance Sheet Assessment

The debt-to-equity ratio is a widely used measure to assess a company's balance sheet health. A higher ratio means that a business aggressively financed its growth with debt. This can result in higher earnings (if the borrowed funds are invested profitably) but also increases risk.

If debt levels are too high, there could be difficulties in meeting obligations, especially during economic downturns or periods of rising interest rates if the debt has variable-rate payments.

Erie Indemnity has no debt, so leverage is not an issue here.

10. Return on Equity

Return on equity (ROE) serves as a comprehensive measure of an insurer's performance, showing how efficiently it converts shareholder capital into profits. Strong ROE performance typically translates to better returns for investors through a combination of earnings retention, share repurchases, and dividend distributions.

Over the last five years, Erie Indemnity has averaged an ROE of 27.5%, exceptional for a company operating in a sector where the average shakes out around 12.5% and those putting up 20%+ are greatly admired. This shows Erie Indemnity has a strong competitive moat.

11. Key Takeaways from Erie Indemnity’s Q4 Results

We struggled to find many positives in these results. Its EPS missed and its revenue fell short of Wall Street’s estimates. Overall, this quarter could have been better. The stock traded down 1.6% to $259.50 immediately after reporting.

12. Is Now The Time To Buy Erie Indemnity?

Updated: March 14, 2026 at 12:22 AM EDT

When considering an investment in Erie Indemnity, investors should account for its valuation and business qualities as well as what’s happened in the latest quarter.

Erie Indemnity is an amazing business ranking highly on our list. First of all, the company’s revenue growth was solid over the last five years. On top of that, its stellar ROE suggests it has been a well-run company historically, and its BVPS growth was exceptional over the last five years.

Erie Indemnity’s P/E ratio based on the next 12 months is 18x. This multiple isn’t necessarily cheap, but we’ll happily own Erie Indemnity as its fundamentals shine bright. It’s often wise to hold investments like this for at least three to five years, as the power of long-term compounding negates short-term price swings that can accompany relatively high valuations.