Fluence Energy (FLNC)

Fluence Energy is a great business. The electric demand for its offerings has propelled a significant increase in its deployed megawatts for digital contracts.― StockStory Analyst Team

1. News

2. Summary

Why We Like Fluence Energy

Pioneering the use of lithium-ion batteries for grid storage, Fluence (NASDAQ:FLNC) helps store renewable energy sources with battery systems.

- Market share has increased this cycle as its 32.2% annual revenue growth over the last five years was exceptional

- Earnings growth has trumped its peers over the last three years as its EPS has compounded at 36.4% annually

- Market share is on track to rise over the next 12 months as its 48.3% projected revenue growth implies demand will accelerate from its two-year trend

We have an affinity for Fluence Energy. No surprise this ranks among our best industrials stocks.

Is Now The Time To Buy Fluence Energy?

At $31.92 per share, Fluence Energy trades at 107x forward EV-to-EBITDA. There are high expectations given this pricey multiple; we can’t deny that.

Do you like the business model and believe in the company’s future? If so, you can own a smaller position, as our work shows that high-quality companies outperform the market over a multi-year period regardless of valuation at entry.

3. Fluence Energy (FLNC) Research Report: Q4 CY2025 Update

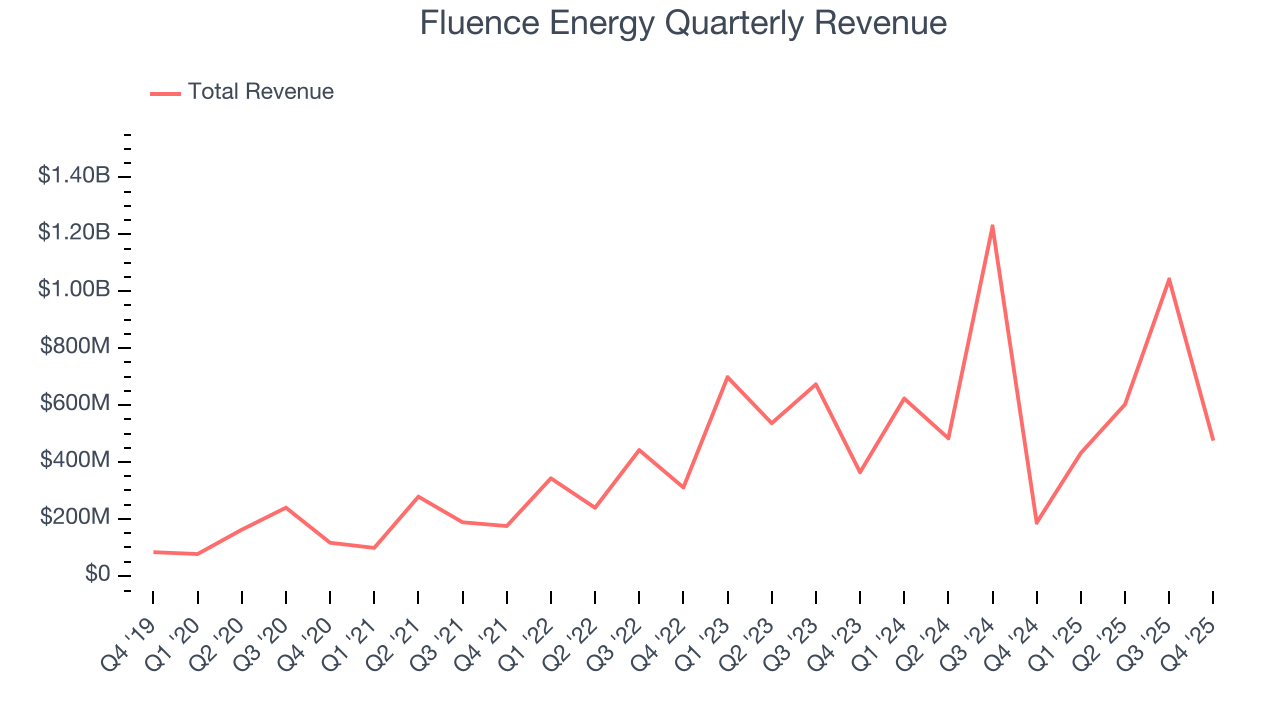

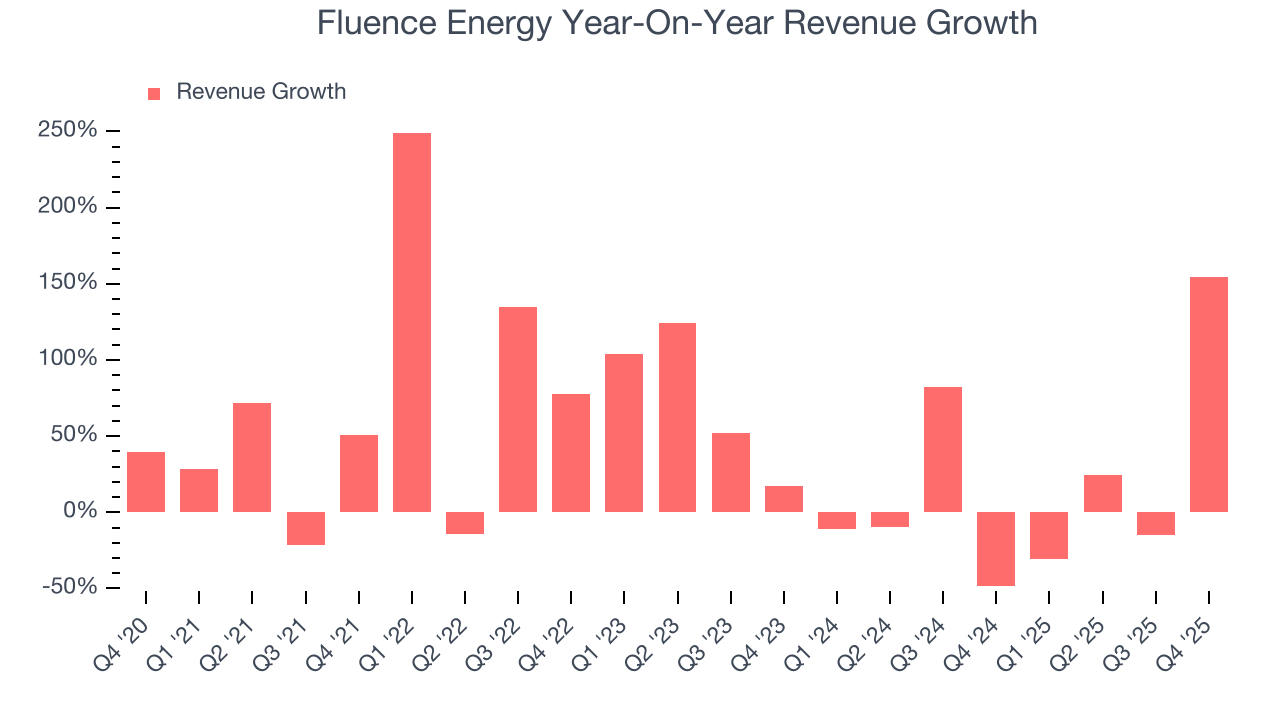

Electricity storage and software provider Fluence (NASDAQ:FLNC) fell short of the market’s revenue expectations in Q4 CY2025, but sales rose 154% year on year to $475.2 million. On the other hand, the company’s full-year revenue guidance of $3.4 billion at the midpoint came in 1.3% above analysts’ estimates. Its GAAP loss of $0.34 per share was 63% below analysts’ consensus estimates.

Fluence Energy (FLNC) Q4 CY2025 Highlights:

- Revenue: $475.2 million vs analyst estimates of $484.3 million (154% year-on-year growth, 1.9% miss)

- EPS (GAAP): -$0.34 vs analyst expectations of -$0.21 (63% miss)

- Adjusted EBITDA: -$52.06 million (-11% margin, 4.8% year-on-year decline)

- The company reconfirmed its revenue guidance for the full year of $3.4 billion at the midpoint

- EBITDA guidance for the full year is $50 million at the midpoint, below analyst estimates of $51.5 million

- Adjusted EBITDA Margin: -11%, up from -26.6% in the same quarter last year

- Free Cash Flow was -$236.1 million compared to -$216.4 million in the same quarter last year

- Backlog: $5.5 billion at quarter end, up 7.8% year on year

- Market Capitalization: $4.26 billion

Company Overview

Pioneering the use of lithium-ion batteries for grid storage, Fluence (NASDAQ:FLNC) helps store renewable energy sources with battery systems.

Fluence was established in 2018 as a joint venture between Siemens and AES, originating from AES's work in energy storage. Over the years, Fluence has grown by making acquisitions such as Nispera’s software services in 2022. This was significant as it provided technologies that improved predictions and maintenance of renewable energy systems.

Today, Fluence helps store and manage electricity from renewable sources like solar and wind. It makes products like Gridstack, Sunstack, and Edgestack, which are big battery systems that can be customized and expanded. These systems help keep the electric grid stable by storing extra energy when demand is low and releasing it when demand is high.

Additionally, Fluence offers software that monitors energy use to help detect problems before happening and ensure the energy systems are functioning properly. The software is typically offered on a subscription basis rather than as a one-time purchase, and it is an additional service that customers pay for separately from the equipment.

Fluence’s customers include power companies, grid managers, and renewable energy developers who typically purchase its products in large quantities to outfit large-scale projects. It offers volume discounts for customers who buy its products in bulk as an incentive for large-scale acquisitions. Many customers supplement their equipment purchases by entering into service agreements with Fluence, which span the equipment’s operational lifetime. These service contracts generate additional revenue for Fluence.

4. Renewable Energy

Renewable energy companies are buoyed by the secular trend of green energy that is upending traditional power generation. Those who innovate and evolve with this dynamic market can win share while those who continue to rely on legacy technologies can see diminishing demand, which includes headwinds from increasing regulation against “dirty” energy. Additionally, these companies are at the whim of economic cycles, as interest rates can impact the willingness to invest in renewable energy projects.

Competitors of Fluence Energy include Tesla (NASDAQ:TSLA) and private companies LG Chem Energy SOlutions and BYD Company.

5. Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Over the last five years, Fluence Energy grew its sales at an incredible 33.8% compounded annual growth rate. Its growth surpassed the average industrials company and shows its offerings resonate with customers, a great starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Fluence Energy’s recent performance shows its demand has slowed significantly as its annualized revenue growth of 6% over the last two years was well below its five-year trend.

This quarter, Fluence Energy achieved a magnificent 154% year-on-year revenue growth rate, but its $475.2 million of revenue fell short of Wall Street’s lofty estimates.

Looking ahead, sell-side analysts expect revenue to grow 37.1% over the next 12 months, an improvement versus the last two years. This projection is eye-popping and suggests its newer products and services will catalyze better top-line performance.

6. Gross Margin & Pricing Power

Gross profit margin is a critical metric to track because it sheds light on its pricing power, complexity of products, and ability to procure raw materials, equipment, and labor.

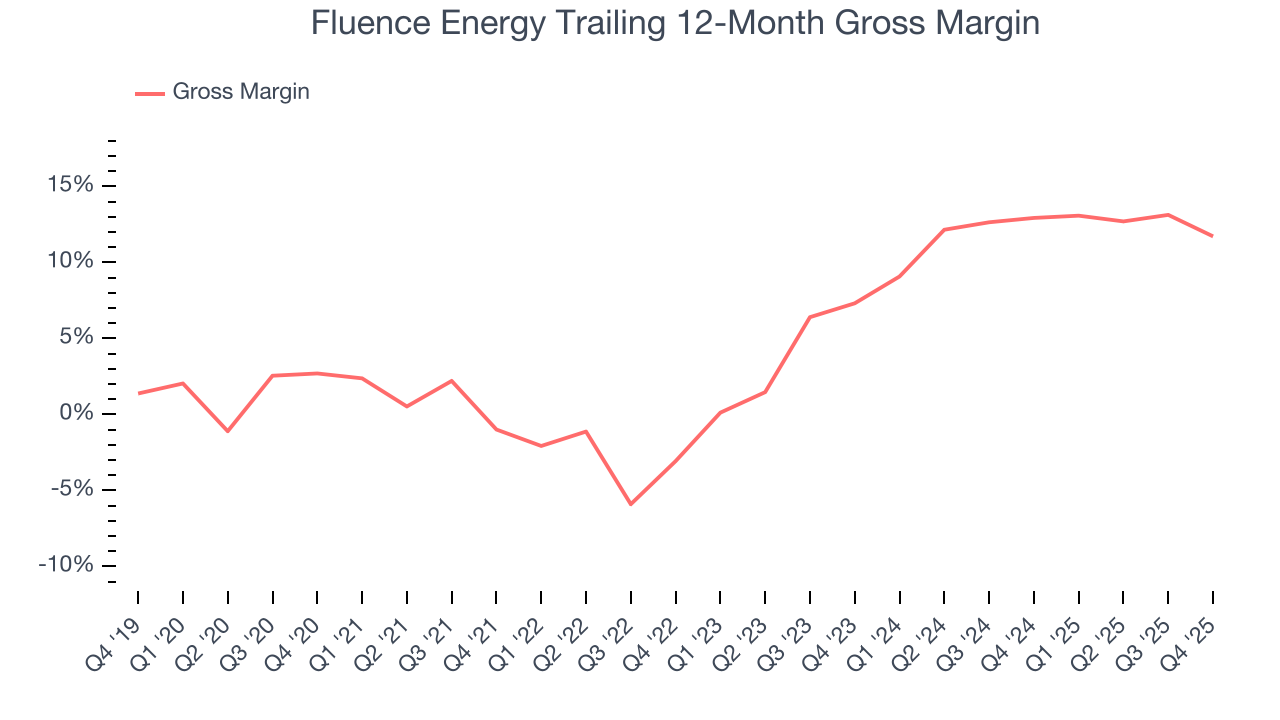

Fluence Energy has bad unit economics for an industrials business, signaling it operates in a competitive market. As you can see below, it averaged a 7.9% gross margin over the last five years. That means Fluence Energy paid its suppliers a lot of money ($92.12 for every $100 in revenue) to run its business.

In Q4, Fluence Energy produced a 4.9% gross profit margin, down 6.5 percentage points year on year. Fluence Energy’s full-year margin has also been trending down over the past 12 months, decreasing by 1.2 percentage points. If this move continues, it could suggest a more competitive environment with some pressure to lower prices and higher input costs (such as raw materials and manufacturing expenses).

7. Operating Margin

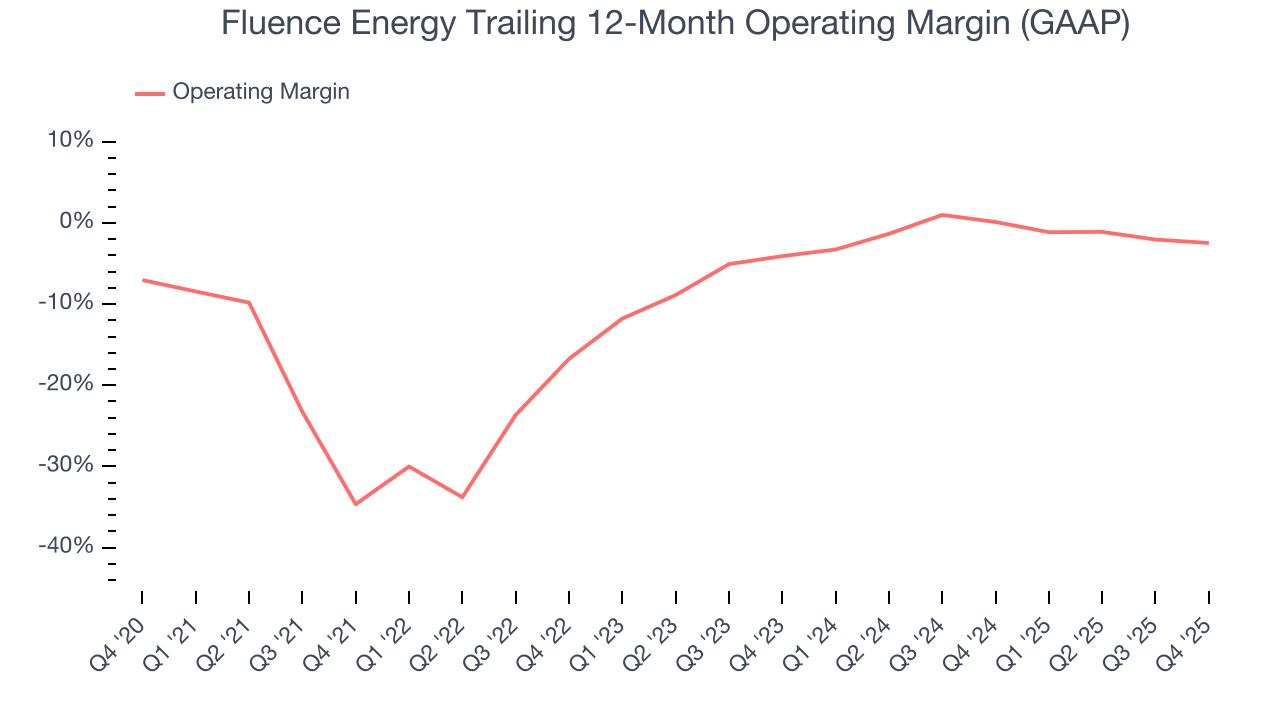

Fluence Energy’s high expenses have contributed to an average operating margin of negative 6.7% over the last five years. Unprofitable industrials companies require extra attention because they could get caught swimming naked when the tide goes out.

On the plus side, Fluence Energy’s operating margin rose by 32.2 percentage points over the last five years, as its sales growth gave it operating leverage. Still, it will take much more for the company to reach long-term profitability.

In Q4, Fluence Energy generated a negative 14.8% operating margin.

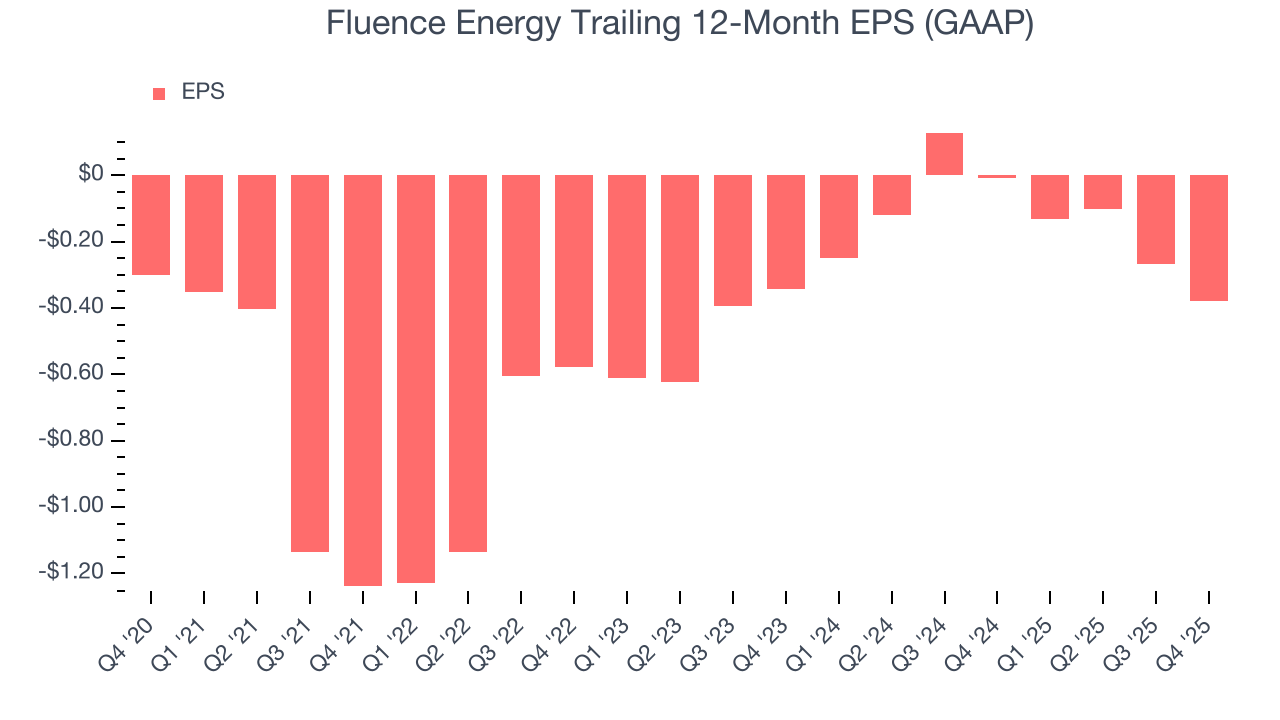

8. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Fluence Energy’s earnings losses deepened over the last five years as its EPS dropped 4.6% annually. We tend to steer our readers away from companies with falling EPS, where diminishing earnings could imply changing secular trends and preferences. If the tide turns unexpectedly, Fluence Energy’s low margin of safety could leave its stock price susceptible to large downswings.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Fluence Energy, its two-year annual EPS declines of 5.1% are similar to its five-year trend. These results were bad no matter how you slice the data.

In Q4, Fluence Energy reported EPS of negative $0.34, down from negative $0.23 in the same quarter last year. This print missed analysts’ estimates. Over the next 12 months, Wall Street expects Fluence Energy to improve its earnings losses. Analysts forecast its full-year EPS of negative $0.38 will advance to negative $0.08.

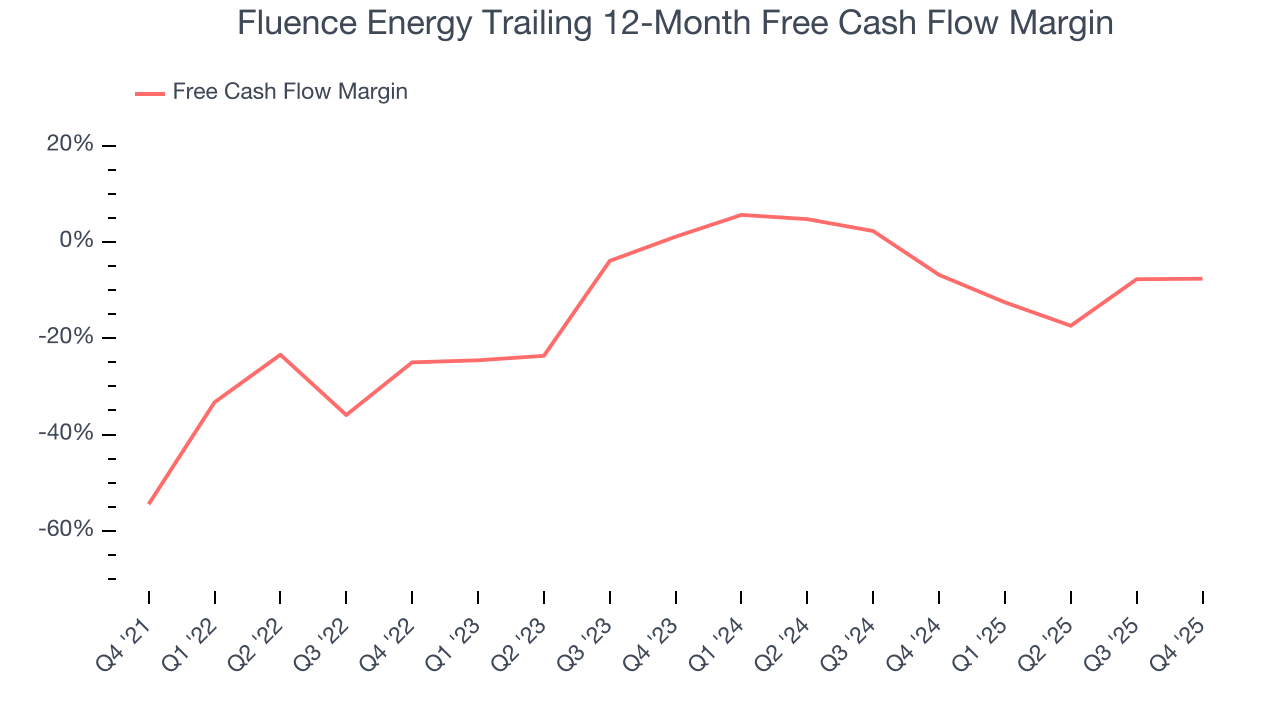

9. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Fluence Energy’s demanding reinvestments have drained its resources over the last five years, putting it in a pinch and limiting its ability to return capital to investors. Its free cash flow margin averaged negative 11.5%, meaning it lit $11.46 of cash on fire for every $100 in revenue.

Taking a step back, an encouraging sign is that Fluence Energy’s margin expanded by 46.8 percentage points during that time. In light of its glaring cash burn, however, this improvement is a bucket of hot water in a cold ocean.

Fluence Energy burned through $236.1 million of cash in Q4, equivalent to a negative 49.7% margin. The company’s cash burn was similar to its $216.4 million of lost cash in the same quarter last year.

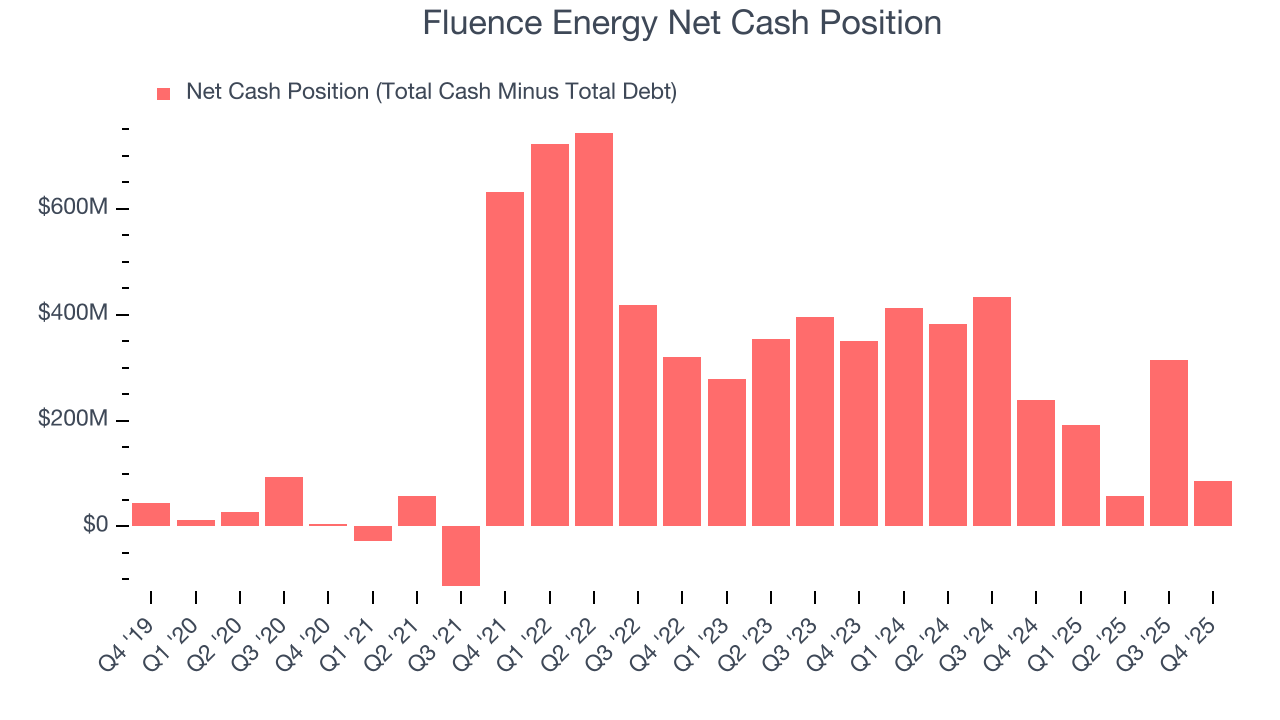

10. Balance Sheet Assessment

Businesses that maintain a cash surplus face reduced bankruptcy risk.

Fluence Energy is a well-capitalized company with $477.8 million of cash and $391.3 million of debt on its balance sheet. This $86.52 million net cash position is 2% of its market cap and gives it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

11. Key Takeaways from Fluence Energy’s Q4 Results

It was good to see Fluence Energy provide full-year revenue guidance that slightly beat analysts’ expectations. On the other hand, its EBITDA missed and its EPS fell short of Wall Street’s estimates. Overall, this was a softer quarter. The stock traded down 11.5% to $25.68 immediately after reporting.

12. Is Now The Time To Buy Fluence Energy?

Updated: February 4, 2026 at 10:41 PM EST

A common mistake we notice when investors are deciding whether to buy a stock or not is that they simply look at the latest earnings results. Business quality and valuation matter more, so we urge you to understand these dynamics as well.

For starters, its revenue growth was exceptional over the last five years and is expected to accelerate over the next 12 months. And while its operating margins reveal poor profitability compared to other industrials companies, its backlog growth has been marvelous. Additionally, Fluence Energy’s rising cash profitability gives it more optionality.

Fluence Energy’s EV-to-EBITDA ratio based on the next 12 months is 63.4x. While this valuation is fair, the upside isn’t great compared to the potential downside. We're fairly confident there are better stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $19.37 on the company (compared to the current share price of $27.28).