Golden Entertainment (GDEN)

We wouldn’t recommend Golden Entertainment. Its low returns on capital and plummeting sales suggest it struggles to generate demand and profits, a red flag.― StockStory Analyst Team

1. News

2. Summary

Why We Think Golden Entertainment Will Underperform

Founded in 2001, Golden Entertainment (NASDAQ:GDEN) is a gaming company operating casinos, taverns, and distributed gaming platforms.

- Products and services have few die-hard fans as sales have declined by 1.8% annually over the last five years

- Subpar operating margin constrains its ability to invest in process improvements or effectively respond to new competitive threats

- Lacking free cash flow limits its freedom to invest in growth initiatives, execute share buybacks, or pay dividends

Golden Entertainment doesn’t measure up to our expectations. Better stocks can be found in the market.

Why There Are Better Opportunities Than Golden Entertainment

Golden Entertainment’s stock price of $26.62 implies a valuation ratio of 30.7x forward P/E. Not only is Golden Entertainment’s multiple richer than most consumer discretionary peers, but it’s also expensive for its revenue characteristics.

There are stocks out there featuring similar valuation multiples with better fundamentals. We prefer to invest in those.

3. Golden Entertainment (GDEN) Research Report: Q4 CY2025 Update

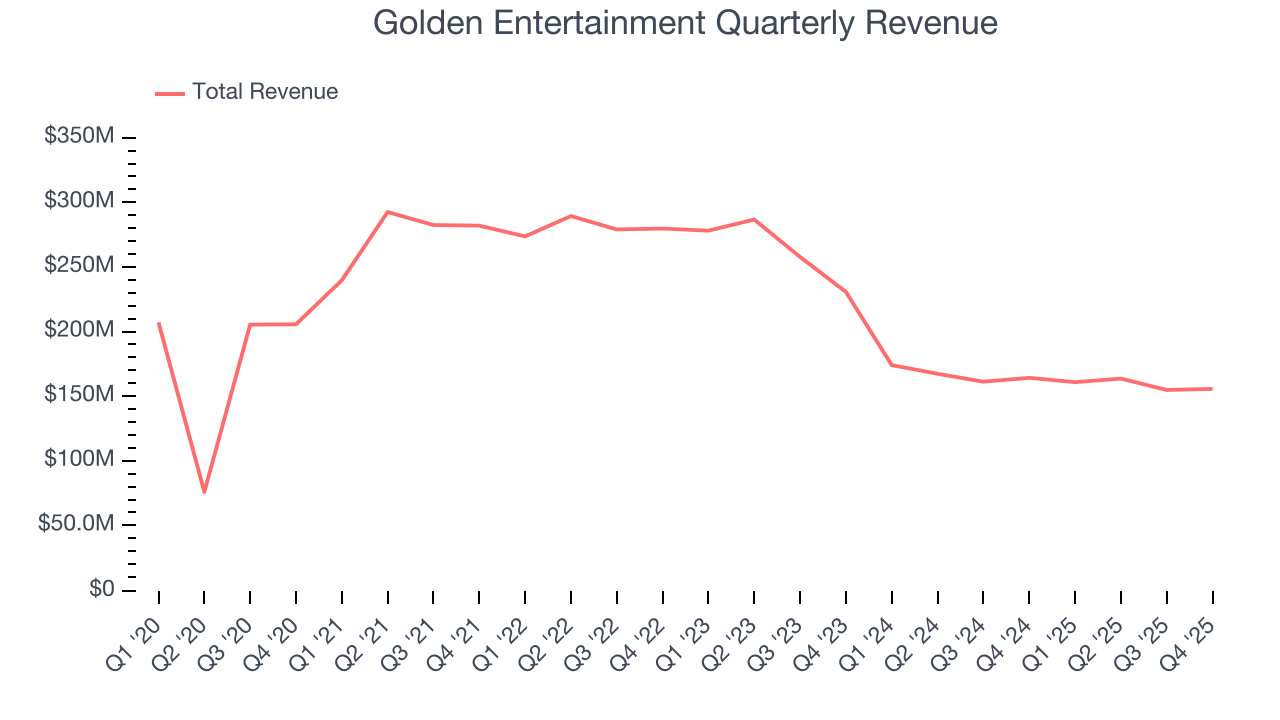

Casino, tavern, and slot machine operator Golden Entertainment (NASDAQ:GDEN) missed Wall Street’s revenue expectations in Q4 CY2025, with sales falling 5.2% year on year to $155.6 million. Its GAAP loss of $0.33 per share was significantly below analysts’ consensus estimates.

Golden Entertainment (GDEN) Q4 CY2025 Highlights:

- Revenue: $155.6 million vs analyst estimates of $164.7 million (5.2% year-on-year decline, 5.5% miss)

- EPS (GAAP): -$0.33 vs analyst estimates of $0.14 (significant miss)

- Adjusted EBITDA: $33.53 million vs analyst estimates of $37.69 million (21.5% margin, 11% miss)

- Operating Margin: -1.5%, down from 7.1% in the same quarter last year

- Market Capitalization: $752.1 million

Company Overview

Founded in 2001, Golden Entertainment (NASDAQ:GDEN) is a gaming company operating casinos, taverns, and distributed gaming platforms.

Golden Entertainment emerged to provide a diversified gaming experience, capturing a unique market position by offering both traditional casino gaming and localized tavern gaming experiences. The company seeks to serve both casual gamers and gambling enthusiasts.

Golden Entertainment's services encompass comprehensive gaming options, including slot machines and table games. It also manages distributed gaming platforms, where it sells its slot machines to various non-casino locations like restaurants and convenience stores. This range caters to different customer preferences, from the vibrant casino environment to the convenience of casual neighborhood tavern gaming.

The company's revenues are derived from its casino operations, distributed gaming platforms, and tavern gaming and dining.

4. Consumer Discretionary - Casino Operator

The Consumer Discretionary sector, by definition, is made up of companies selling non-essential goods and services. When economic conditions deteriorate or tastes shift, consumers can easily cut back or eliminate these purchases. For long-term investors with five-year holding periods, this creates a structural challenge: the sector is inherently hit-driven, with low switching costs and fickle customers. As a result, only a handful of companies can reliably grow demand and compound earnings over long periods, which is why our bar is high and High Quality ratings are rare.

Casino operators run gaming resorts and facilities that generate revenue from gambling, hospitality, food and beverage, and entertainment offerings. Tailwinds include pent-up travel demand, expansion into new jurisdictions legalizing gaming, and growing interest in integrated resort developments in Asia and the Middle East. However, the industry faces notable headwinds: heavy regulatory and licensing requirements limit operational flexibility, capital expenditure for property development and renovation is substantial, and revenue is highly sensitive to macroeconomic conditions and consumer confidence. Rising competition from online gambling platforms, regional saturation in mature markets, and geopolitical risks in key international jurisdictions add further uncertainty.

Competitors in the gaming and entertainment sector include Boyd Gaming (NYSE:BYD), Caesars Entertainment (NASDAQ:CZR), and Red Rock Resorts (NASDAQ:RRR).

5. Revenue Growth

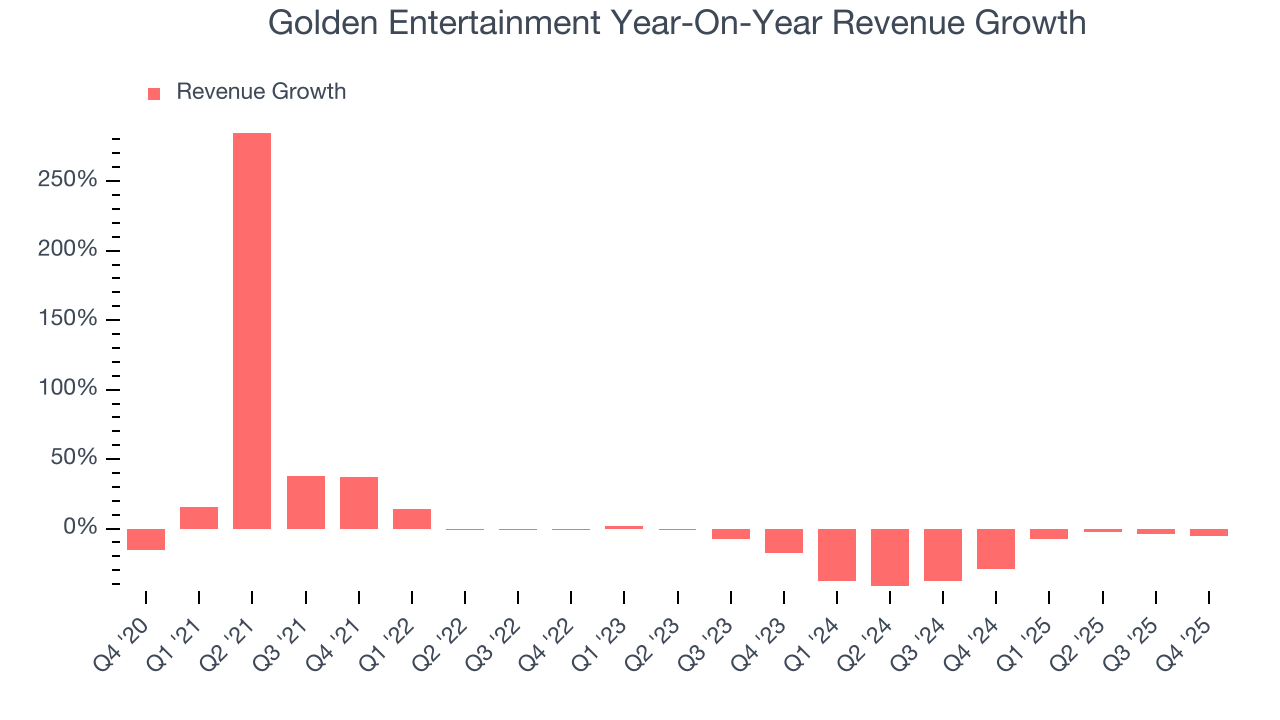

A company’s long-term sales performance can indicate its overall quality. Any business can have short-term success, but a top-tier one grows for years. Golden Entertainment struggled to consistently generate demand over the last five years as its sales dropped at a 1.8% annual rate. This was below our standards and is a sign of poor business quality.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. Golden Entertainment’s recent performance shows its demand remained suppressed as its revenue has declined by 22.4% annually over the last two years. Note that COVID hurt Golden Entertainment’s business in 2020 and part of 2021, and it bounced back in a big way thereafter.

This quarter, Golden Entertainment missed Wall Street’s estimates and reported a rather uninspiring 5.2% year-on-year revenue decline, generating $155.6 million of revenue.

Looking ahead, sell-side analysts expect revenue to grow 3.3% over the next 12 months. Although this projection suggests its newer products and services will catalyze better top-line performance, it is still below average for the sector.

6. Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

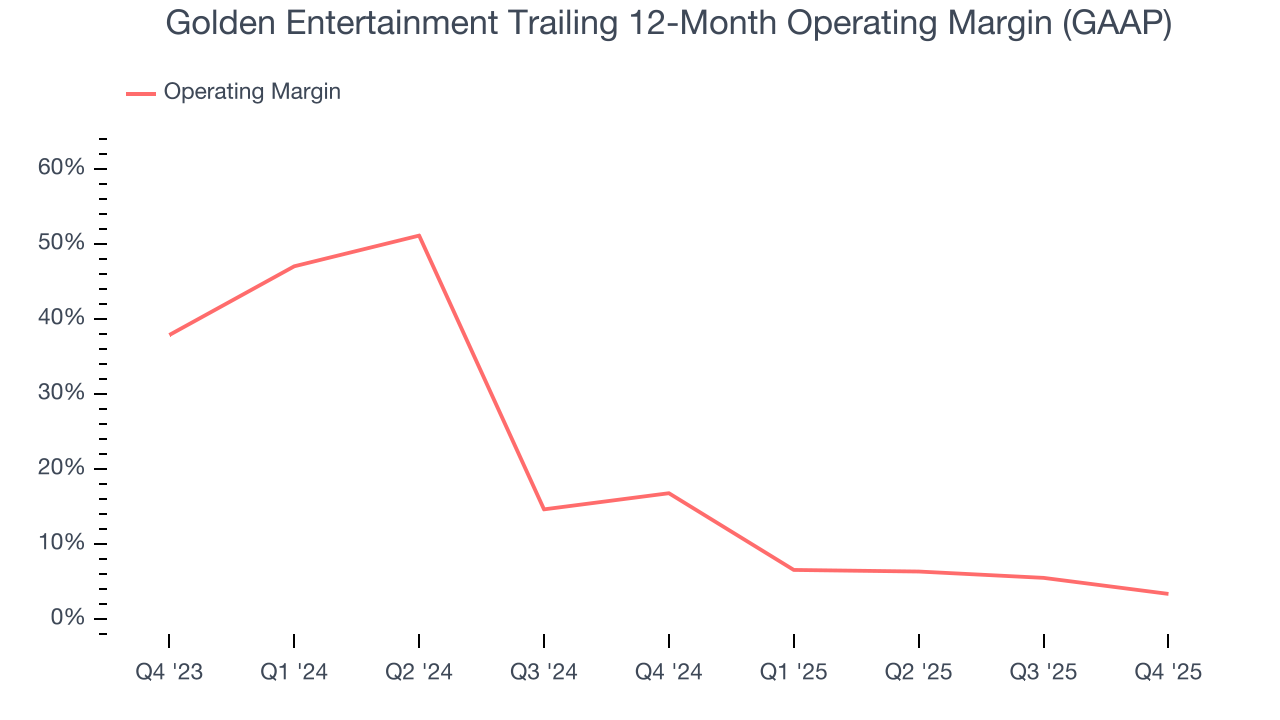

Golden Entertainment’s operating margin has shrunk over the last 12 months and averaged 10.3% over the last two years. The company’s profitability was mediocre for a consumer discretionary business and shows it couldn’t pass its higher operating expenses onto its customers.

This quarter, Golden Entertainment generated an operating margin profit margin of negative 1.5%, down 8.6 percentage points year on year. This contraction shows it was less efficient because its expenses increased relative to its revenue.

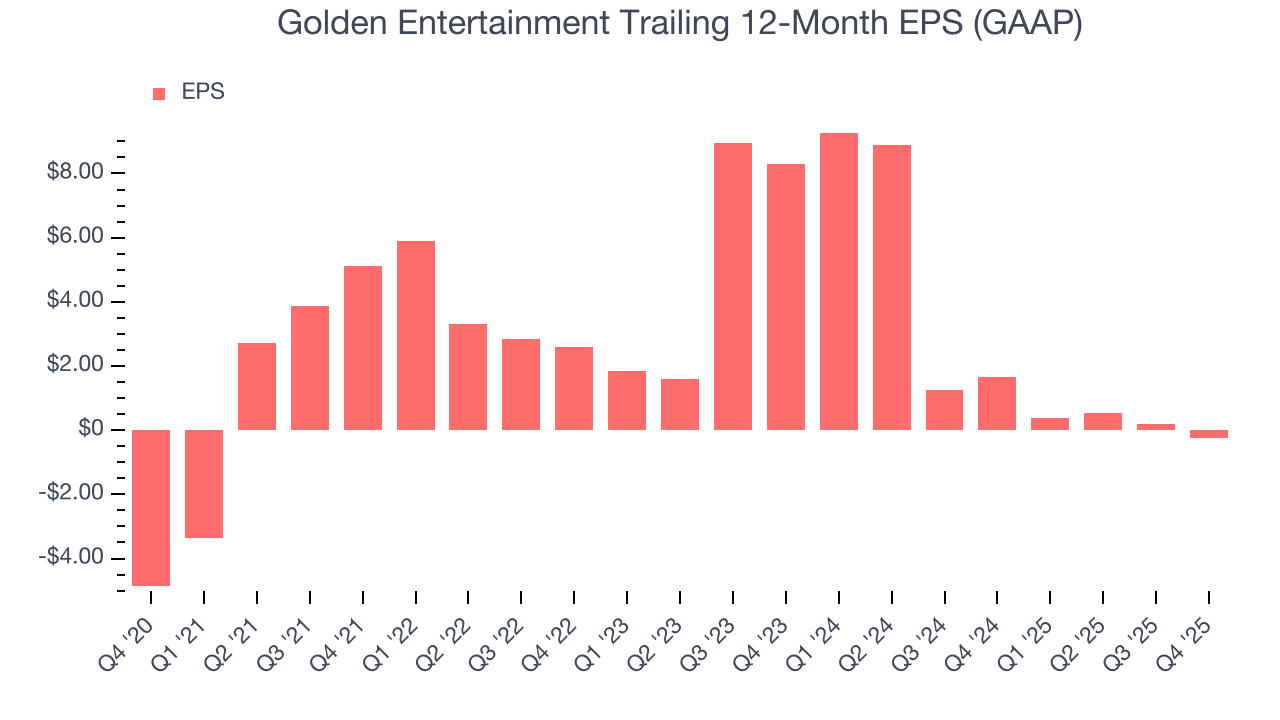

7. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Although Golden Entertainment’s full-year earnings are still negative, it reduced its losses and improved its EPS by 44.9% annually over the last five years. The next few quarters will be critical for assessing its long-term profitability.

In Q4, Golden Entertainment reported EPS of negative $0.33, down from $0.10 in the same quarter last year. This print missed analysts’ estimates. Over the next 12 months, Wall Street is optimistic. Analysts forecast Golden Entertainment’s full-year EPS of negative $0.25 will flip to positive $0.75.

8. Cash Is King

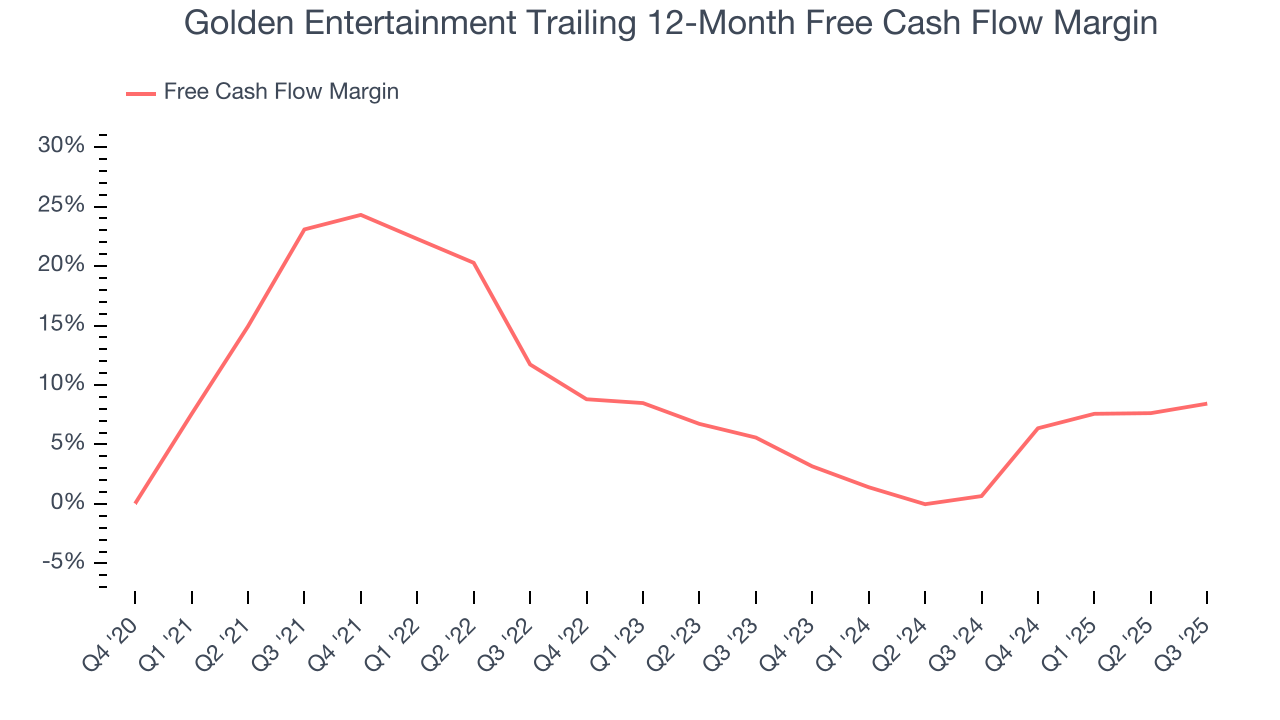

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Golden Entertainment has shown poor cash profitability over the last two years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 7.2%, lousy for a consumer discretionary business.

9. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Golden Entertainment historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 16.8%, somewhat low compared to the best consumer discretionary companies that consistently pump out 25%+.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Over the last few years, Golden Entertainment’s ROIC has increased. This is a good sign, and we hope the company can continue improving.

10. Balance Sheet Assessment

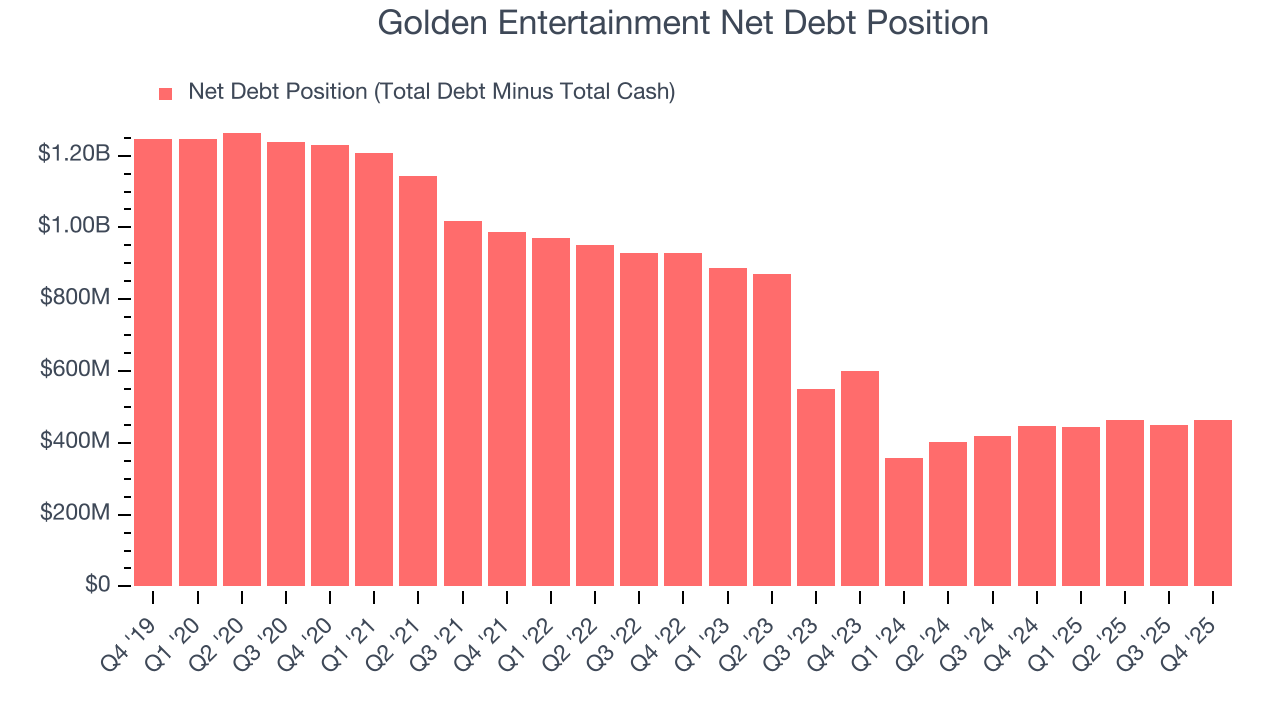

Golden Entertainment reported $55.33 million of cash and $518 million of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $140 million of EBITDA over the last 12 months, we view Golden Entertainment’s 3.3× net-debt-to-EBITDA ratio as safe. We also see its $30.67 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

11. Key Takeaways from Golden Entertainment’s Q4 Results

We struggled to find many positives in these results. Its revenue missed and its EPS fell short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock remained flat at $28.73 immediately following the results.

12. Is Now The Time To Buy Golden Entertainment?

Updated: March 24, 2026 at 10:53 PM EDT

Before investing in or passing on Golden Entertainment, we urge you to understand the company’s business quality (or lack thereof), valuation, and the latest quarterly results - in that order.

We cheer for all companies serving everyday consumers, but in the case of Golden Entertainment, we’ll be cheering from the sidelines. While its projected EPS for the next year implies the company’s fundamentals will improve, the downside is its relatively low ROIC suggests management has struggled to find compelling investment opportunities. On top of that, its low free cash flow margins give it little breathing room.

Golden Entertainment’s P/E ratio based on the next 12 months is 30.7x. At this valuation, there’s a lot of good news priced in - we think other companies feature superior fundamentals at the moment.

Wall Street analysts have a consensus one-year price target of $30.50 on the company (compared to the current share price of $26.62).