GoodRx (GDRX)

GoodRx is up against the odds. Its negative returns on capital show it destroyed shareholder value by losing money.― StockStory Analyst Team

1. News

2. Summary

Why We Think GoodRx Will Underperform

Started in 2011 to tackle the problem of high prescription drug costs in America, GoodRx (NASDAQ:GDRX) operates a digital platform that helps consumers find lower prices on prescription medications through price comparison tools and discount codes.

- Customer additions have disappointed over the past two years, indicating the company’s value proposition may not be resonating

- Negative returns on capital show that some of its growth strategies have backfired

- Smaller revenue base of $796.9 million means it hasn’t achieved the economies of scale that some industry juggernauts enjoy

GoodRx doesn’t meet our quality criteria. There’s a wealth of better opportunities.

Why There Are Better Opportunities Than GoodRx

GoodRx’s stock price of $2.28 implies a valuation ratio of 6.7x forward P/E. This is a cheap valuation multiple, but for good reason. You get what you pay for.

Our advice is to pay up for elite businesses whose advantages are tailwinds to earnings growth. Don’t get sucked into lower-quality businesses just because they seem like bargains. These mediocre businesses often never achieve a higher multiple as hoped, a phenomenon known as a “value trap”.

3. GoodRx (GDRX) Research Report: Q4 CY2025 Update

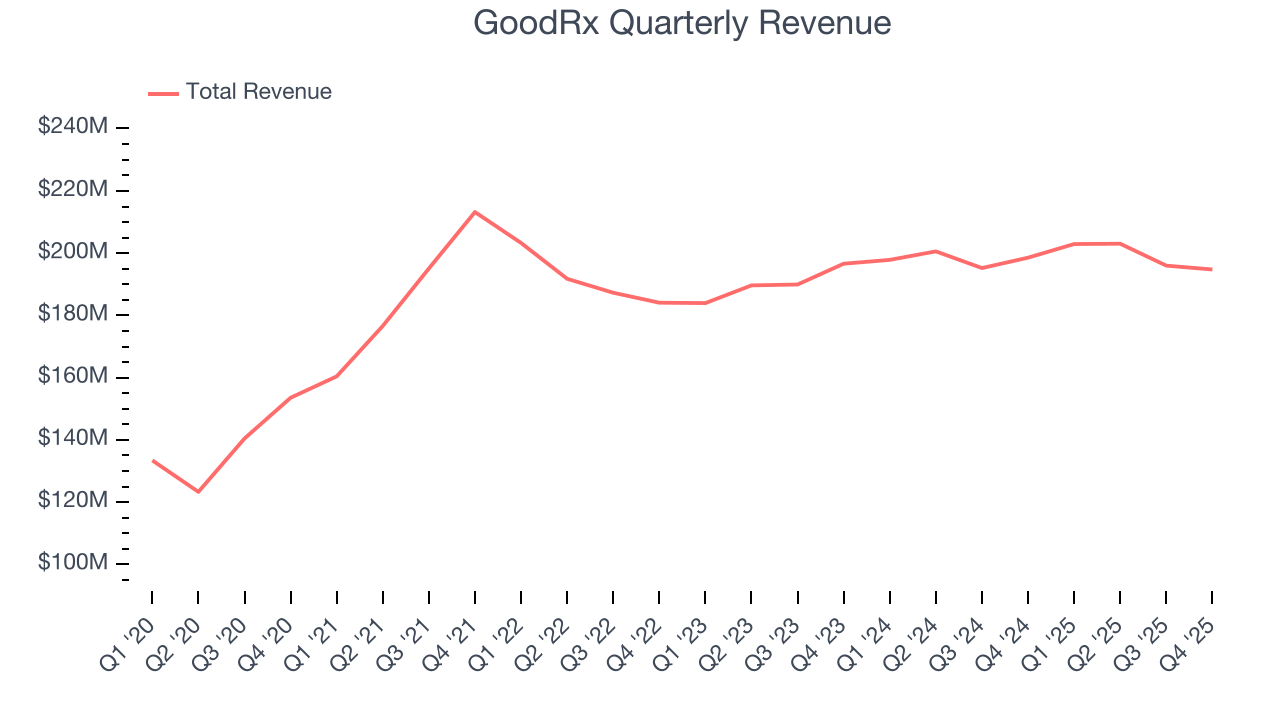

Healthcare tech company GoodRx (NASDAQ:GDRX) reported Q4 CY2025 results beating Wall Street’s revenue expectations, but sales fell by 1.9% year on year to $194.8 million. On the other hand, the company’s full-year revenue guidance of $765 million at the midpoint came in 6.2% below analysts’ estimates. Its non-GAAP profit of $0.09 per share was in line with analysts’ consensus estimates.

GoodRx (GDRX) Q4 CY2025 Highlights:

- Revenue: $194.8 million vs analyst estimates of $193.2 million (1.9% year-on-year decline, 0.8% beat)

- Adjusted EPS: $0.09 vs analyst estimates of $0.09 (in line)

- Adjusted EBITDA: $65.02 million vs analyst estimates of $64.81 million (33.4% margin, in line)

- EBITDA guidance for the upcoming financial year 2026 is $230 million at the midpoint, below analyst estimates of $282.1 million

- Operating Margin: 11.6%, up from 9.2% in the same quarter last year

- Free Cash Flow was -$38.85 million, down from $44.58 million in the same quarter last year

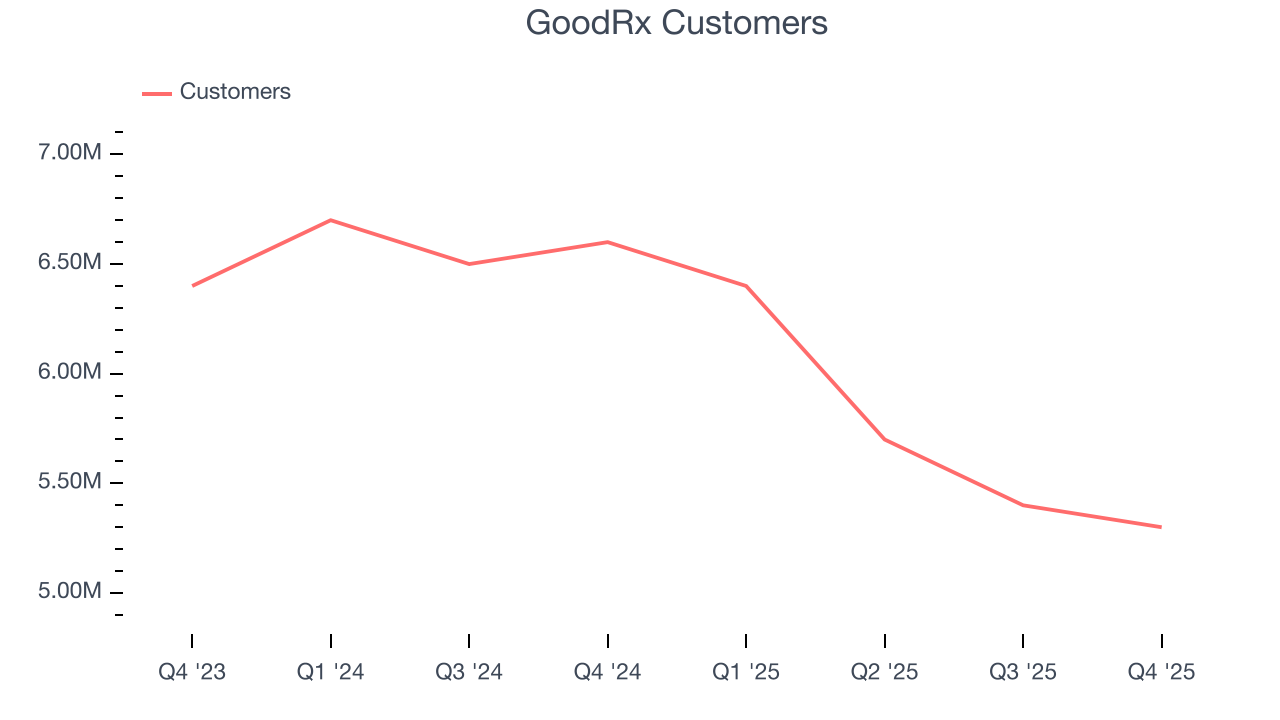

- Customers: 5.3 million, down from 5.4 million in the previous quarter

- Market Capitalization: $804.5 million

Company Overview

Started in 2011 to tackle the problem of high prescription drug costs in America, GoodRx (NASDAQ:GDRX) operates a digital platform that helps consumers find lower prices on prescription medications through price comparison tools and discount codes.

GoodRx's platform processes over 320 billion pricing data points daily to provide consumers with geographically relevant prescription pricing information. When users find a lower price through GoodRx, they receive a discount code that can be presented at nearly any retail pharmacy in the United States. Once a consumer uses a GoodRx code at a pharmacy, that code is stored in the pharmacy's database for future refills, creating ongoing value for both the consumer and GoodRx.

The company generates revenue primarily when consumers use GoodRx codes to save money on prescriptions compared to pharmacy list prices. GoodRx has expanded beyond its core prescription price comparison tool to offer subscription services that provide even deeper discounts. Its Gold subscription offers lower prices at select pharmacies, mail delivery options, and other benefits for a monthly or annual fee.

For example, a consumer prescribed a common cholesterol medication might pay $150 at their local pharmacy using insurance, but could find the same medication for $20 using a GoodRx discount code. A Gold subscriber might access that same medication for just $10.

GoodRx also partners with pharmaceutical manufacturers to advertise and integrate their affordability solutions for brand-name medications into its platform. The company's business model creates a network effect: as more consumers use GoodRx, the company gains leverage to negotiate better prices with pharmacy benefit managers (PBMs) and pharmacies, which in turn attracts more consumers.

Beyond prescription savings, GoodRx has expanded into telehealth through its GoodRx Care platform, which offers consumers access to virtual medical consultations on a cash-pay basis. The company also provides healthcare information through GoodRx Health, a content platform launched in 2021 that offers educational resources about medications and health conditions.

4. Healthcare Technology for Patients

The consumer-focused healthcare technology sector leverages digital platforms to make healthcare more accessible and affordable, offering services like telemedicine and prescription discounts. Looking forward, growth is supported by increasing consumer comfort with telehealth and the demand for cost-saving tools amidst rising healthcare expenses. AI-powered diagnostics and personalized digital care also present significant opportunities. However, the sector faces headwinds from heightened competition as large technology and established healthcare companies expand their digital presence.

GoodRx competes with other prescription discount providers like SingleCare and RxSaver, pharmacy benefit managers such as CVS Caremark (NYSE:CVS) and Express Scripts (part of Cigna Group, NYSE:CI), and digital healthcare platforms including Amazon Pharmacy (NASDAQ:AMZN) and Mark Cuban Cost Plus Drug Company.

5. Revenue Scale

Larger companies benefit from economies of scale, where fixed costs like infrastructure, technology, and administration are spread over a higher volume of goods or services, reducing the cost per unit. Scale can also lead to bargaining power with suppliers, greater brand recognition, and more investment firepower. A virtuous cycle can ensue if a scaled company plays its cards right.

With just $796.9 million in revenue over the past 12 months, GoodRx is a small company in an industry where scale matters. This makes it difficult to build trust with customers because healthcare is heavily regulated, complex, and resource-intensive.

6. Revenue Growth

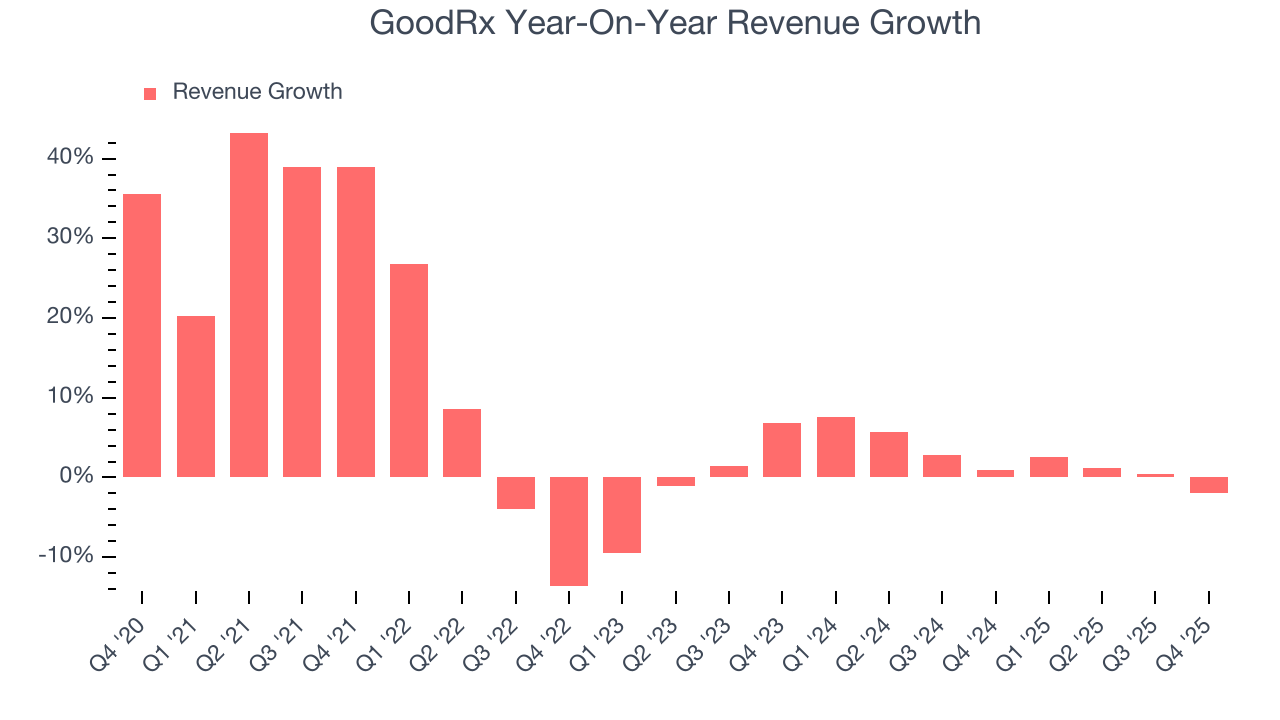

A company’s long-term sales performance is one signal of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Thankfully, GoodRx’s 7.7% annualized revenue growth over the last five years was decent. Its growth was slightly above the average healthcare company and shows its offerings resonate with customers.

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. GoodRx’s recent performance shows its demand has slowed as its annualized revenue growth of 2.4% over the last two years was below its five-year trend. We’re wary when companies in the sector see decelerations in revenue growth, as it could signal changing consumer tastes aided by low switching costs.

We can dig further into the company’s revenue dynamics by analyzing its number of customers, which reached 5.3 million in the latest quarter. Over the last two years, GoodRx’s customer base averaged 9.5% year-on-year declines. Because this number is lower than its revenue growth, we can see the average customer spent more money each year on the company’s products and services.

This quarter, GoodRx’s revenue fell by 1.9% year on year to $194.8 million but beat Wall Street’s estimates by 0.8%.

Looking ahead, sell-side analysts expect revenue to grow 2.2% over the next 12 months, similar to its two-year rate. This projection doesn't excite us and implies its newer products and services will not catalyze better top-line performance yet.

7. Adjusted Operating Margin

Adjusted operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies because it excludes non-recurring expenses, interest on debt, and taxes.

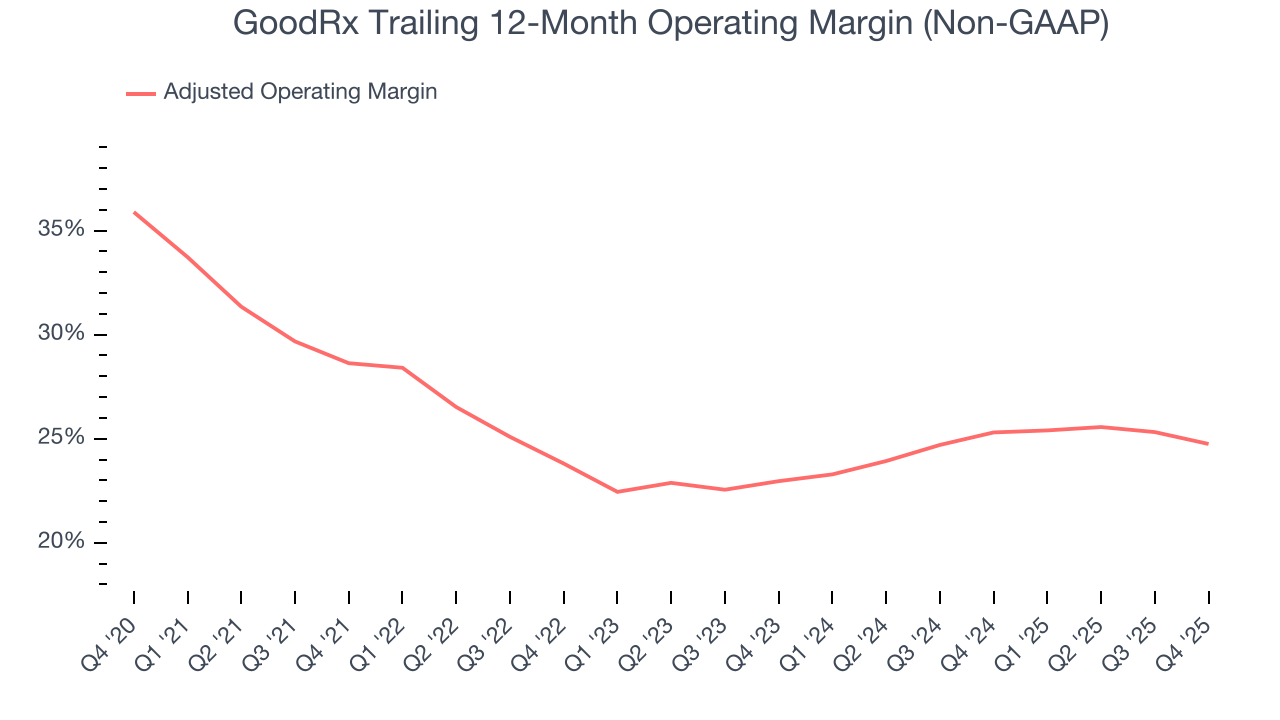

GoodRx has been an efficient company over the last five years. It was one of the more profitable businesses in the healthcare sector, boasting an average adjusted operating margin of 25.1%.

Analyzing the trend in its profitability, GoodRx’s adjusted operating margin decreased by 3.9 percentage points over the last five years, but it rose by 1.8 percentage points on a two-year basis. Still, shareholders will want to see GoodRx become more profitable in the future.

In Q4, GoodRx generated an adjusted operating margin profit margin of 23.3%, down 2.3 percentage points year on year. This contraction shows it was less efficient because its expenses increased relative to its revenue.

8. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

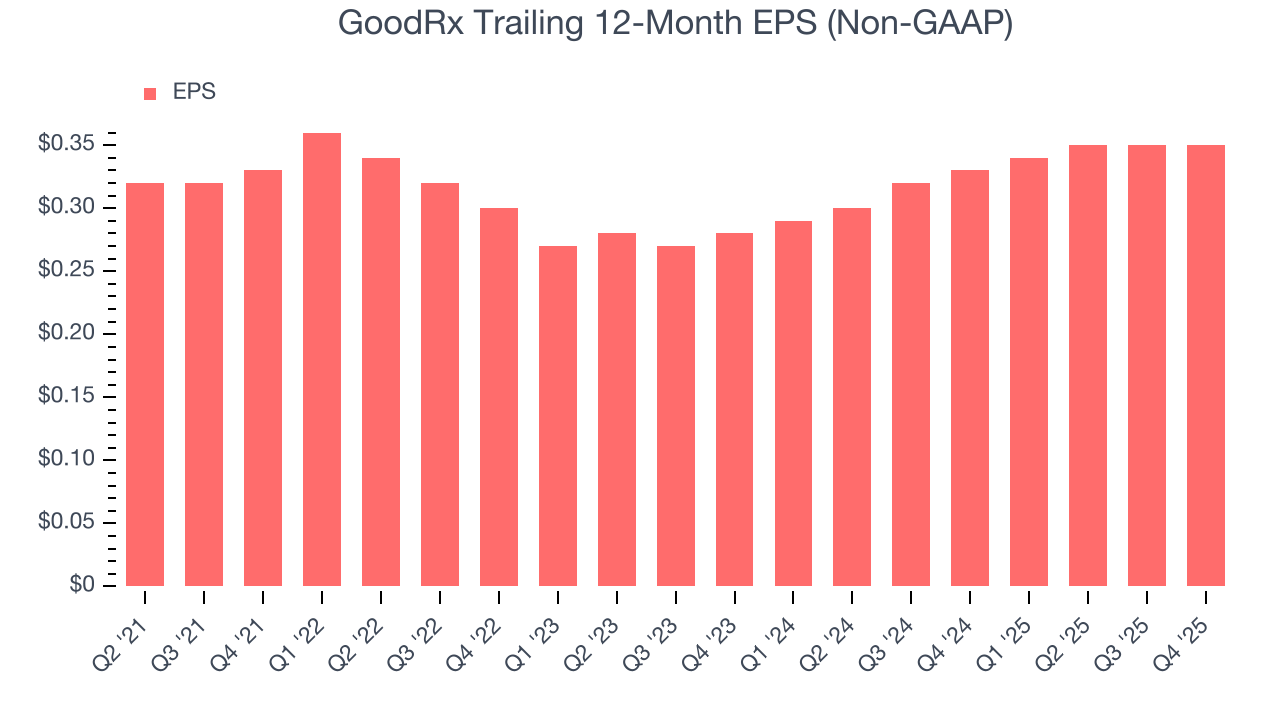

GoodRx’s flat EPS over the last five years was below its 7.7% annualized revenue growth. This tells us the company became less profitable on a per-share basis as it expanded due to non-fundamental factors such as interest expenses and taxes.

Diving into the nuances of GoodRx’s earnings can give us a better understanding of its performance. As we mentioned earlier, GoodRx’s adjusted operating margin declined by 3.9 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its lower earnings; interest expenses and taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

In Q4, GoodRx reported adjusted EPS of $0.09, in line with the same quarter last year. This print slightly missed analysts’ estimates. Over the next 12 months, Wall Street expects GoodRx’s full-year EPS of $0.35 to grow 21.3%.

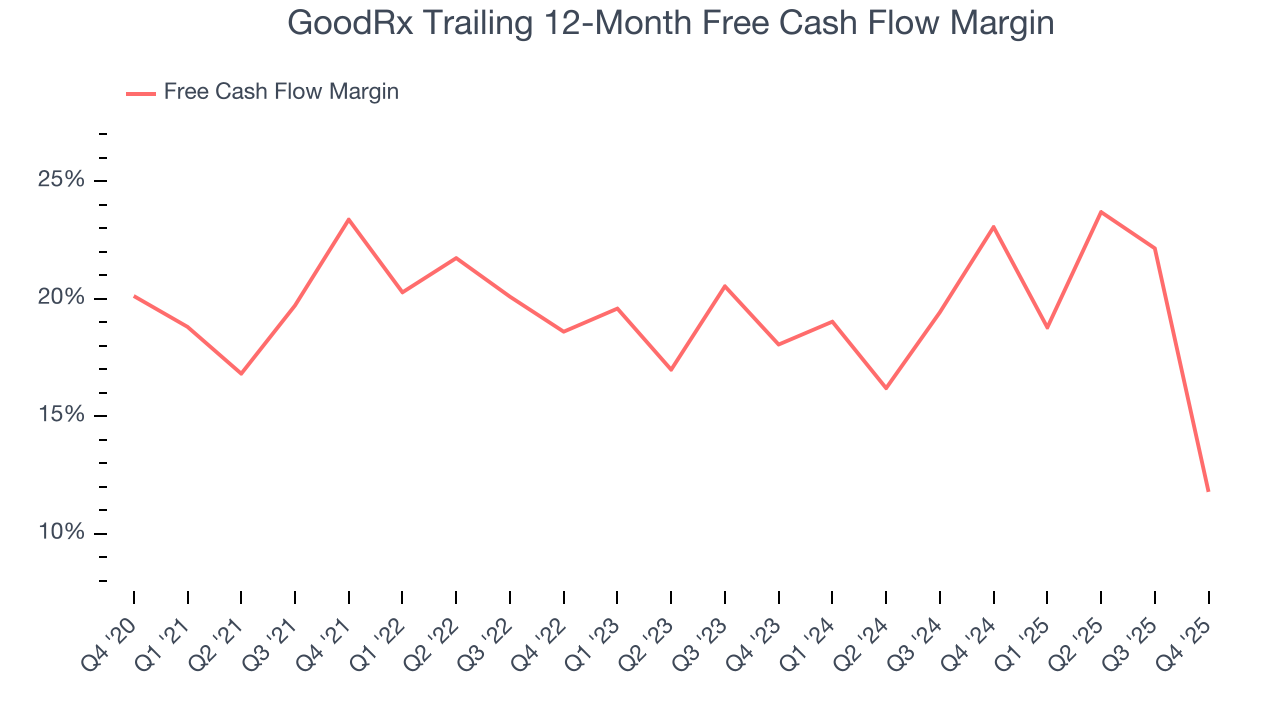

9. Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

GoodRx has shown robust cash profitability, giving it an edge over its competitors and the ability to reinvest or return capital to investors. The company’s free cash flow margin averaged 18.9% over the last five years, quite impressive for a healthcare business.

Taking a step back, we can see that GoodRx’s margin dropped by 11.6 percentage points during that time. If its declines continue, it could signal increasing investment needs and capital intensity.

GoodRx burned through $38.85 million of cash in Q4, equivalent to a negative 19.9% margin. The company’s cash flow turned negative after being positive in the same quarter last year, suggesting its historical struggles have dragged on.

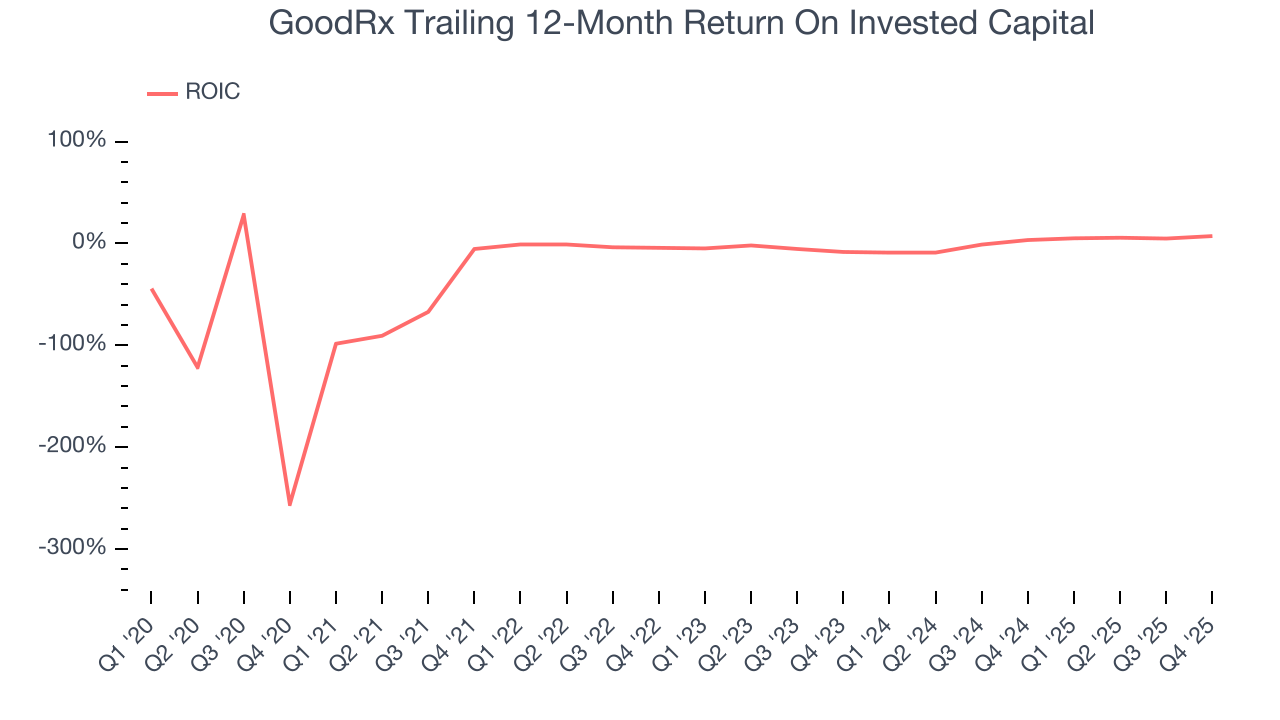

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

GoodRx’s five-year average ROIC was negative 1.5%, meaning management lost money while trying to expand the business. Investors are likely hoping for a change soon.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. GoodRx’s ROIC has increased significantly over the last few years. This is a good sign, and we hope the company can continue improving.

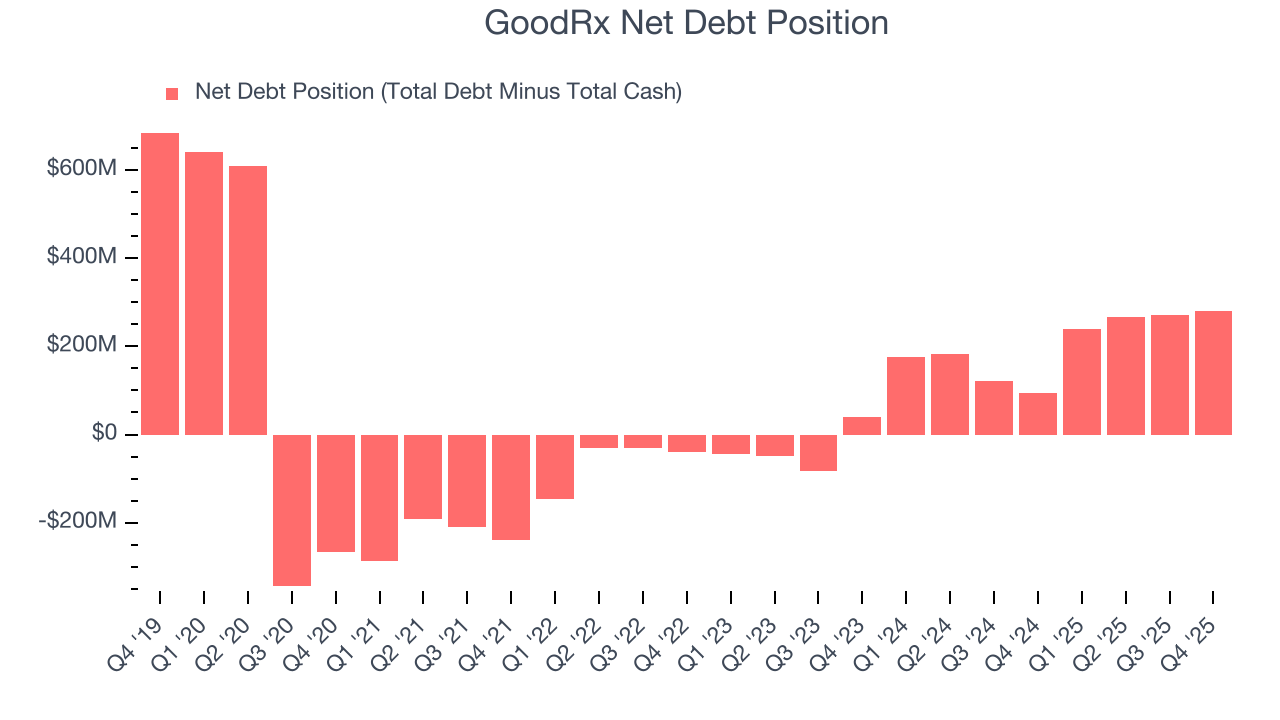

11. Balance Sheet Assessment

GoodRx reported $261.8 million of cash and $542.8 million of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $270.5 million of EBITDA over the last 12 months, we view GoodRx’s 1.0× net-debt-to-EBITDA ratio as safe. We also see its $14.64 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

12. Key Takeaways from GoodRx’s Q4 Results

It was good to see GoodRx narrowly top analysts’ revenue expectations this quarter. On the other hand, its full-year revenue guidance missed and its full-year EBITDA guidance fell short of Wall Street’s estimates. Overall, this quarter could have been better. The stock traded down 11.8% to $2.18 immediately following the results.

13. Is Now The Time To Buy GoodRx?

Updated: March 20, 2026 at 11:18 PM EDT

We think that the latest earnings result is only one piece of the bigger puzzle. If you’re deciding whether to own GoodRx, you should also grasp the company’s longer-term business quality and valuation.

We see the value of companies making people healthier, but in the case of GoodRx, we’re out. Although its revenue growth was decent over the last five years, it’s expected to deteriorate over the next 12 months and its relatively low ROIC suggests management has struggled to find compelling investment opportunities. And while the company’s rising returns show management's prior bets are at least better than before, the downside is its subscale operations give it fewer distribution channels than its larger rivals.

GoodRx’s P/E ratio based on the next 12 months is 6.6x. While this valuation is optically cheap, the potential downside is huge given its shaky fundamentals. There are better stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $2.82 on the company (compared to the current share price of $2.08).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.