Great Lakes Dredge & Dock (GLDD)

We’re skeptical of Great Lakes Dredge & Dock. Its weak sales growth and low returns on capital show it struggled to generate demand and profits.― StockStory Analyst Team

1. News

2. Summary

Why Great Lakes Dredge & Dock Is Not Exciting

Founded as Lydon & Drews dredging company, Great Lakes Dredge & Dock (NASDAQ:GLDD) provides dredging services, land reclamation, and coastal protection projects in the United States and internationally.

- Negative free cash flow raises questions about the return timeline for its investments

- High input costs result in an inferior gross margin of 16.9% that must be offset through higher volumes

- Earnings growth over the last five years fell short of the peer group average as its EPS only increased by 2% annually

Great Lakes Dredge & Dock’s quality doesn’t meet our hurdle. Our attention is focused on better businesses.

Why There Are Better Opportunities Than Great Lakes Dredge & Dock

Great Lakes Dredge & Dock is trading at $16.92 per share, or 17.3x forward P/E. Great Lakes Dredge & Dock’s multiple may seem like a great deal among industrials peers, but we think there are valid reasons why it’s this cheap.

It’s better to pay up for high-quality businesses with higher long-term earnings potential rather than to buy lower-quality stocks because they appear cheap. These challenged businesses often don’t re-rate, a phenomenon known as a “value trap”.

3. Great Lakes Dredge & Dock (GLDD) Research Report: Q3 CY2025 Update

Dredging and coastal protection company Great Lakes Dredge & Dock (NASDAQ:GLDD) missed Wall Street’s revenue expectations in Q3 CY2025 as sales rose 2.1% year on year to $195.2 million. Its GAAP profit of $0.26 per share was 50.7% above analysts’ consensus estimates.

Great Lakes Dredge & Dock (GLDD) Q3 CY2025 Highlights:

- Revenue: $195.2 million vs analyst estimates of $201.3 million (2.1% year-on-year growth, 3% miss)

- EPS (GAAP): $0.26 vs analyst estimates of $0.17 (50.7% beat)

- Adjusted EBITDA: $39.27 million vs analyst estimates of $31.73 million (20.1% margin, 23.8% beat)

- Operating Margin: 14.4%, up from 8.7% in the same quarter last year

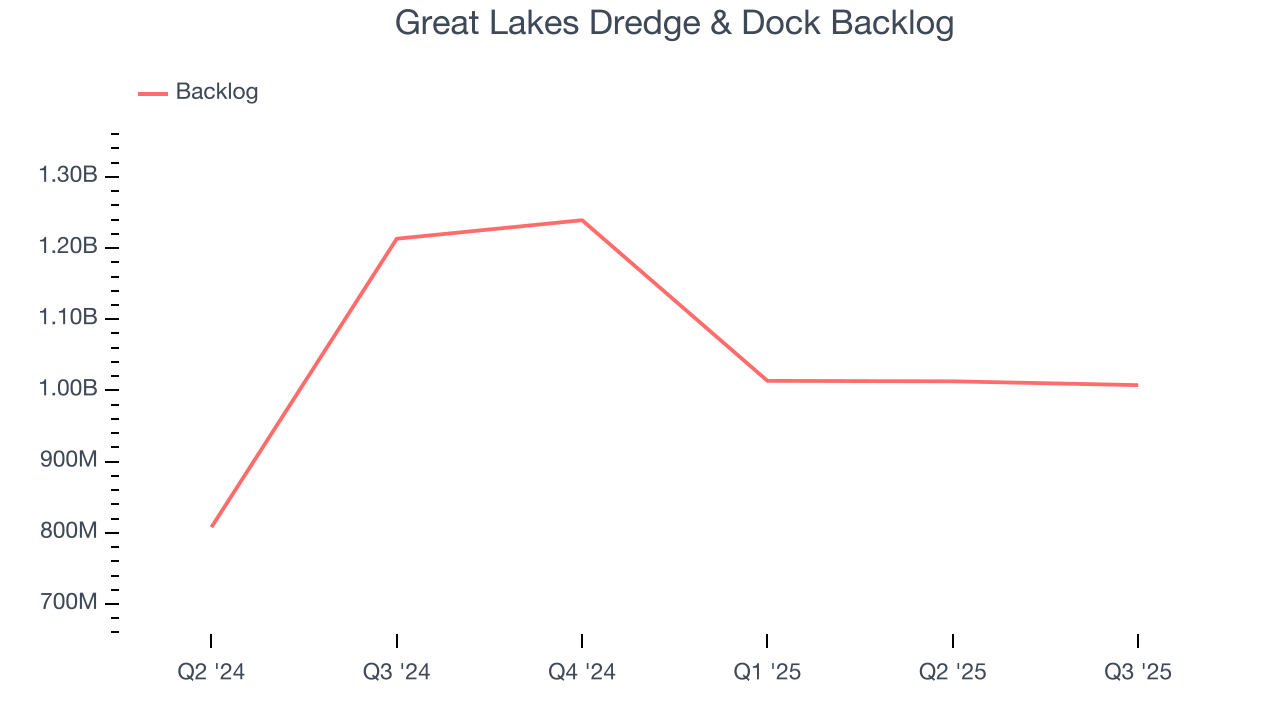

- Backlog: $1.01 billion at quarter end, down 17% year on year

- Market Capitalization: $773.8 million

Company Overview

Founded as Lydon & Drews dredging company, Great Lakes Dredge & Dock (NASDAQ:GLDD) provides dredging services, land reclamation, and coastal protection projects in the United States and internationally.

Great Lakes Dredge & Dock's first projects include creating shoreline structures for Chicago's Columbian Exposition. The company expanded operations throughout the Great Lakes, adopting the name Great Lakes Dredge and Dock Company in 1905. It played significant roles in early 20th-century infrastructure projects, including the construction of major Chicago landmarks and naval facilities. Following World War II, it extended into oil-related dredging in the Gulf of Mexico.

Today, Great Lakes Dredge & Dock provides dredging services, including capital dredging, coastal protection, and maintenance. Its projects support port expansions, enhance coastal resilience against erosion, and maintain waterway navigability. For instance, the company's coastal protection projects often involve beach nourishment, which protects shorelines while supporting local tourism and real estate. Similarly, its capital dredging projects not only facilitate modern maritime needs by accommodating larger vessels but also support commercial development through enhanced port facilities.

The company has also recently engaged in the U.S. offshore wind market representing a strategic diversification. This move not only broadens its revenue streams but also aligns with global energy transition trends.

Revenue for Great Lakes primarily derives from a mix of federal, state, local, and international contracts. Recurring revenue comes from maintenance dredging, required regularly due to natural sedimentation and post-storm recovery, ensuring steady demand for its services.

4. Construction and Maintenance Services

Construction and maintenance services companies not only boast technical know-how in specialized areas but also may hold special licenses and permits. Those who work in more regulated areas can enjoy more predictable revenue streams - for example, fire escapes need to be inspected every five years. More recently, services to address energy efficiency and labor availability are also creating incremental demand. But like the broader industrials sector, construction and maintenance services companies are at the whim of economic cycles as external factors like interest rates can greatly impact the new construction that drives incremental demand for these companies’ offerings.

Competitors in the dredging and related services industry include Orion Group (NYSE:ORN), Sterling Construction Company (NASDAQ:STRL), and Dycom Industries (NYSE:DY)

5. Revenue Growth

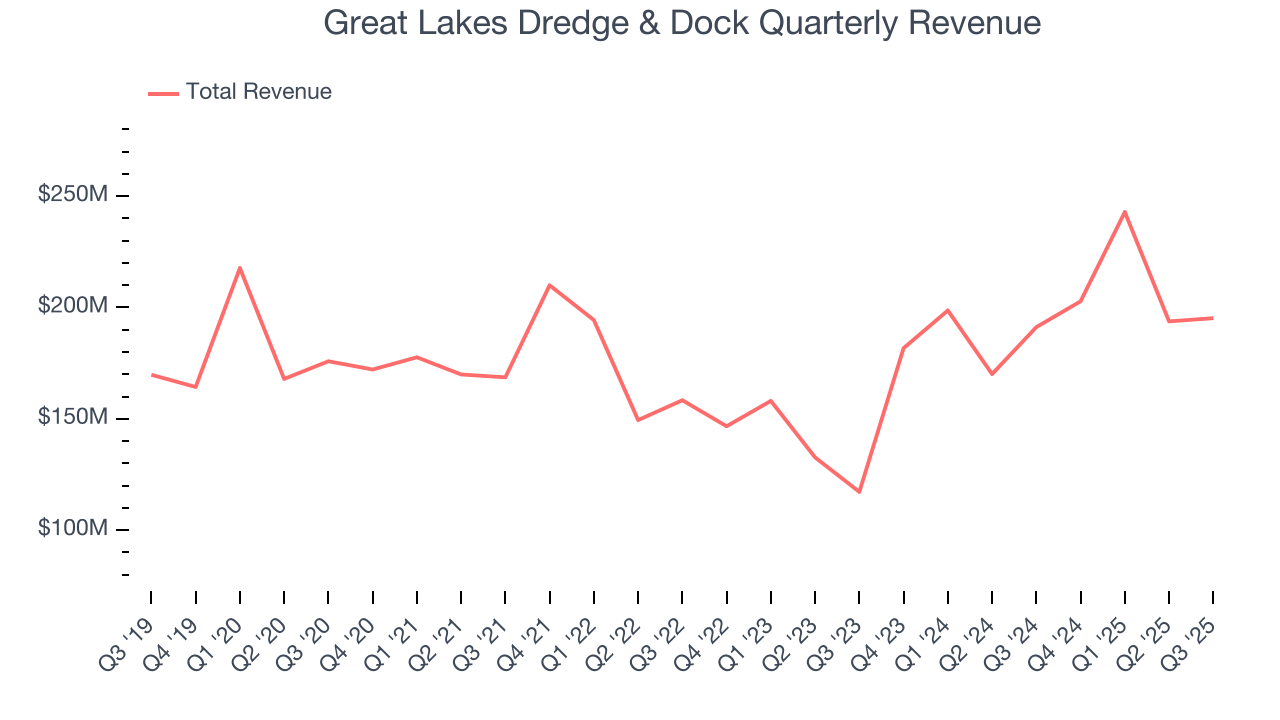

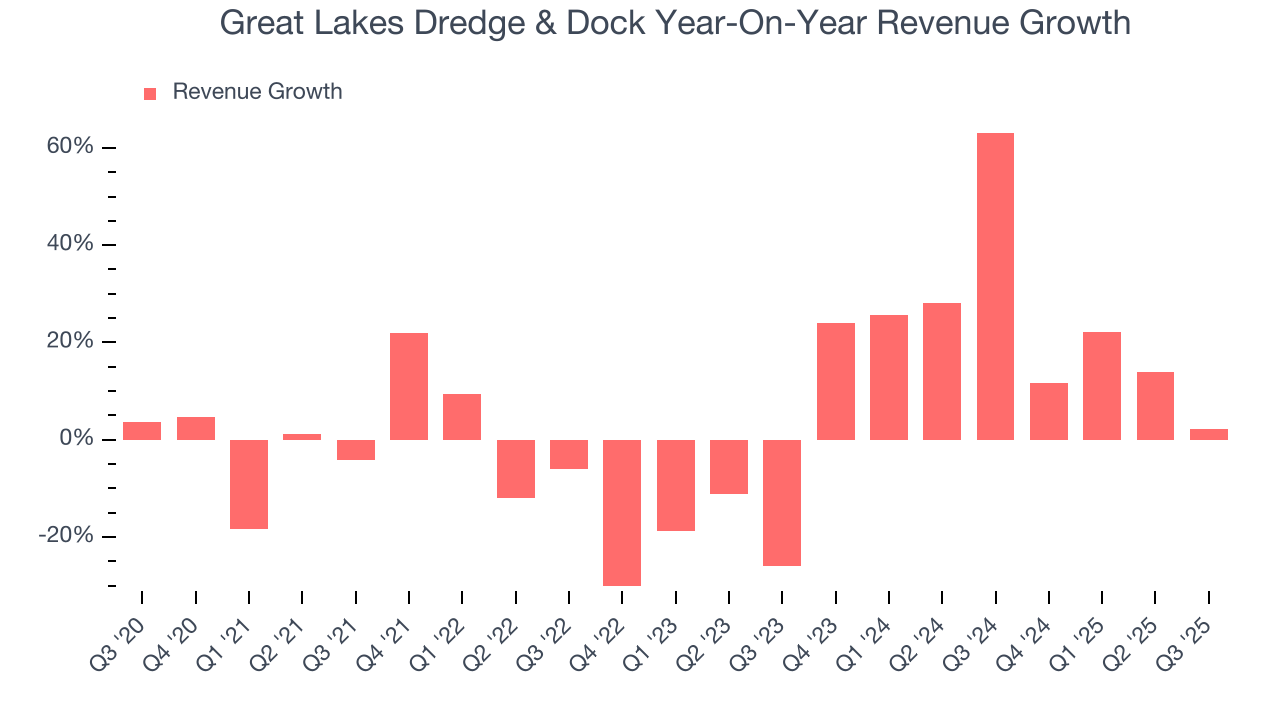

Reviewing a company’s long-term sales performance reveals insights into its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Regrettably, Great Lakes Dredge & Dock’s sales grew at a sluggish 2.8% compounded annual growth rate over the last five years. This fell short of our benchmarks and is a tough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Great Lakes Dredge & Dock’s annualized revenue growth of 22.7% over the last two years is above its five-year trend, suggesting its demand recently accelerated.

We can dig further into the company’s revenue dynamics by analyzing its backlog, or the value of its outstanding orders that have not yet been executed or delivered. Great Lakes Dredge & Dock’s backlog reached $1.01 billion in the latest quarter and averaged 4.2% year-on-year growth over the last two years. Because this number is lower than its revenue growth, we can see the company fulfilled orders at a faster rate than it added new orders to the backlog. This implies Great Lakes Dredge & Dock was operating efficiently but raises questions about the health of its sales pipeline.

This quarter, Great Lakes Dredge & Dock’s revenue grew by 2.1% year on year to $195.2 million, falling short of Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 4.8% over the next 12 months, a deceleration versus the last two years. This projection is underwhelming and indicates its products and services will face some demand challenges.

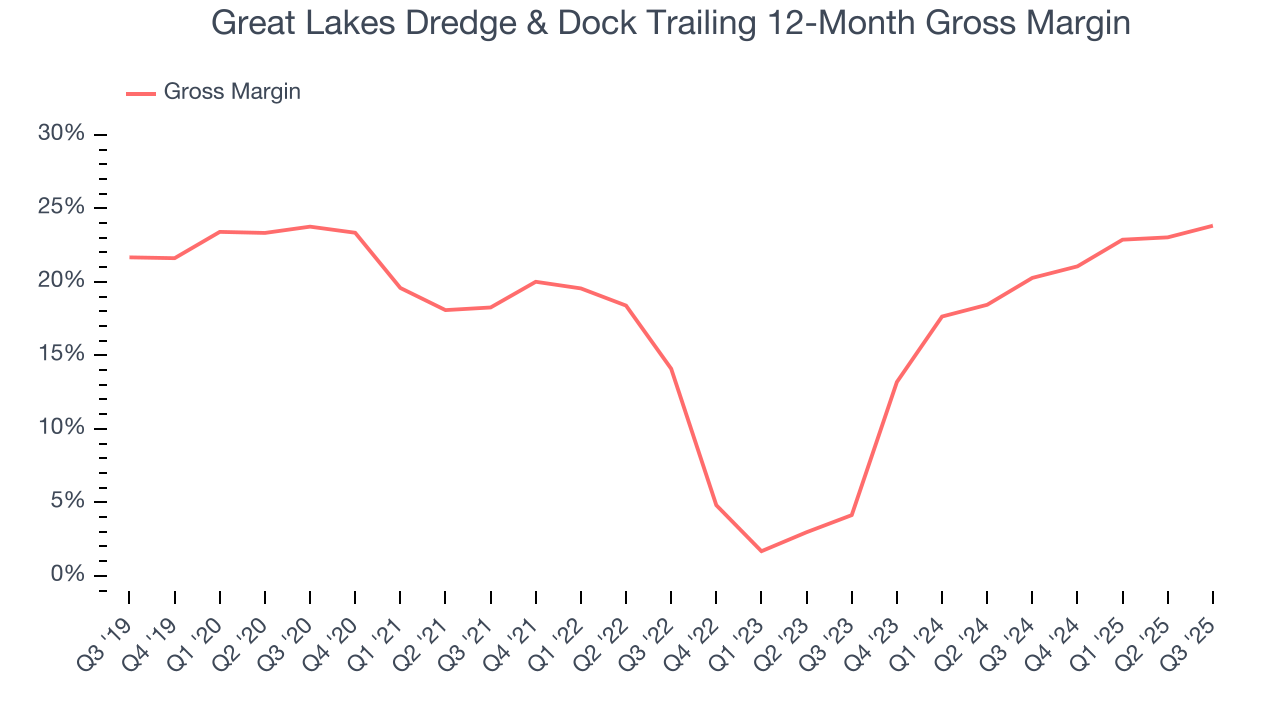

6. Gross Margin & Pricing Power

Gross profit margin is a critical metric to track because it sheds light on its pricing power, complexity of products, and ability to procure raw materials, equipment, and labor.

Great Lakes Dredge & Dock has bad unit economics for an industrials business, signaling it operates in a competitive market. As you can see below, it averaged a 16.9% gross margin over the last five years. That means Great Lakes Dredge & Dock paid its suppliers a lot of money ($83.07 for every $100 in revenue) to run its business.

This quarter, Great Lakes Dredge & Dock’s gross profit margin was 22.4%, marking a 3.5 percentage point increase from 19% in the same quarter last year. Great Lakes Dredge & Dock’s full-year margin has also been trending up over the past 12 months, increasing by 3.5 percentage points. If this move continues, it could suggest better unit economics due to more leverage from its growing sales on the fixed portion of its cost of goods sold (such as manufacturing expenses).

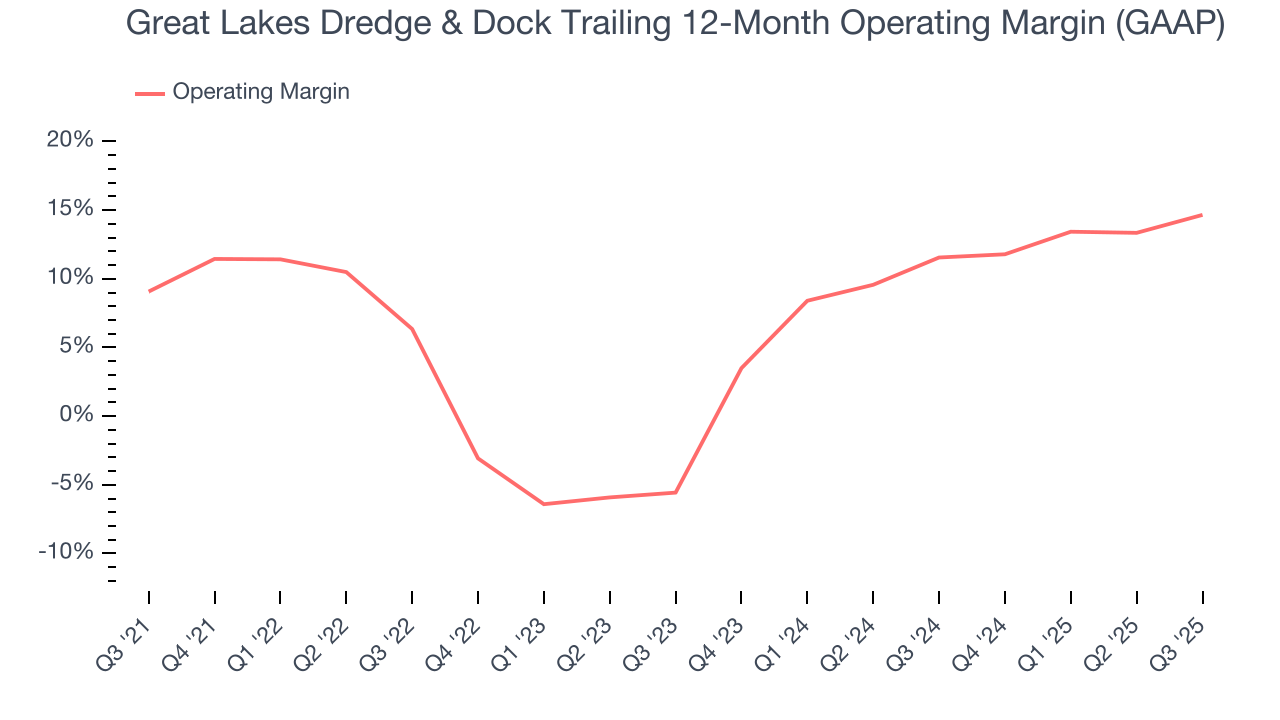

7. Operating Margin

Great Lakes Dredge & Dock has done a decent job managing its cost base over the last five years. The company has produced an average operating margin of 8.1%, higher than the broader industrials sector.

Looking at the trend in its profitability, Great Lakes Dredge & Dock’s operating margin rose by 5.6 percentage points over the last five years, as its sales growth gave it operating leverage.

This quarter, Great Lakes Dredge & Dock generated an operating margin profit margin of 14.4%, up 5.7 percentage points year on year. The increase was solid, and because its operating margin rose more than its gross margin, we can infer it was more efficient with expenses such as marketing, R&D, and administrative overhead.

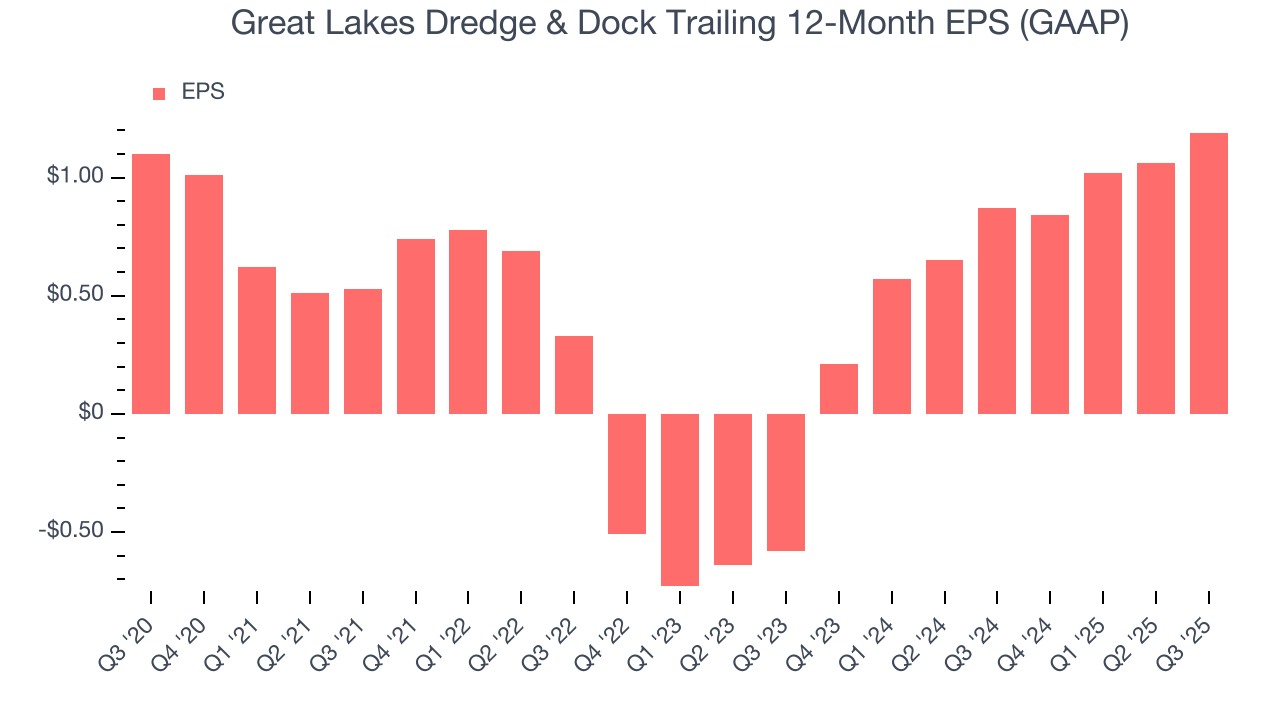

8. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Great Lakes Dredge & Dock’s weak 1.6% annual EPS growth over the last five years aligns with its revenue performance. On the bright side, this tells us its incremental sales were profitable.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Great Lakes Dredge & Dock, its two-year annual EPS growth of 101% was higher than its five-year trend. This acceleration made it one of the faster-growing industrials companies in recent history.

In Q3, Great Lakes Dredge & Dock reported EPS of $0.26, up from $0.13 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Great Lakes Dredge & Dock’s full-year EPS of $1.19 to shrink by 24.2%.

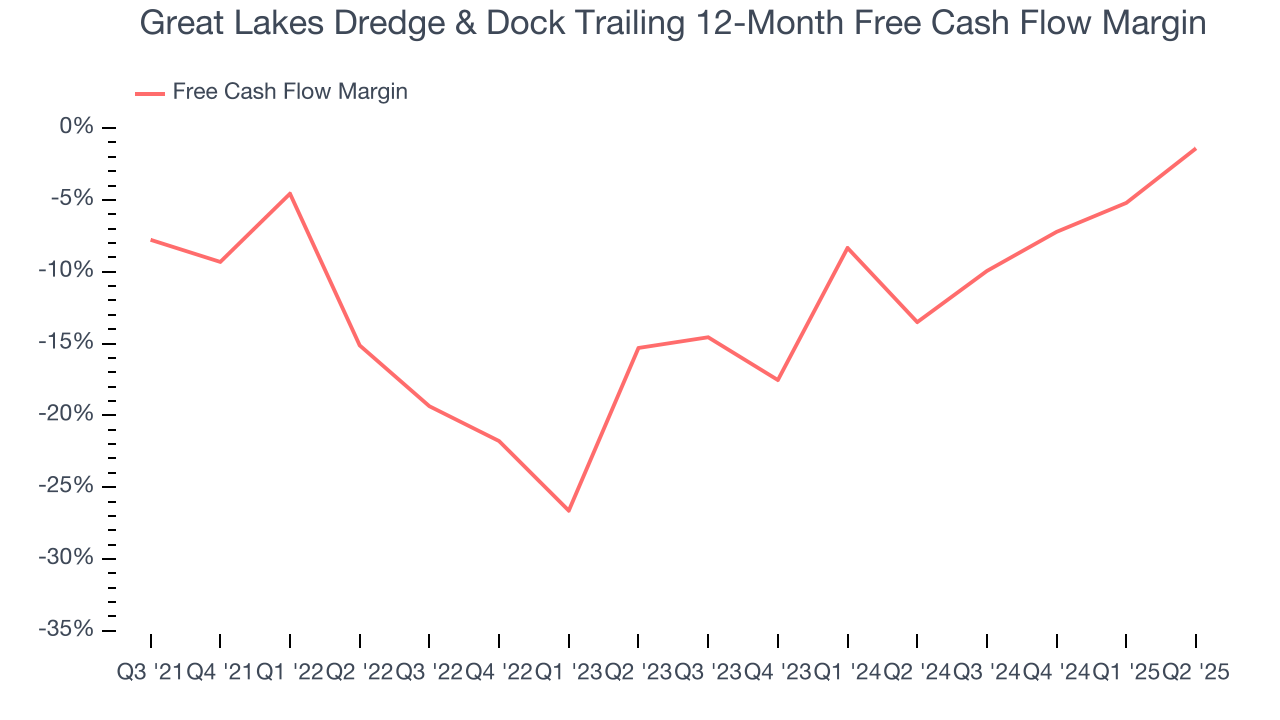

9. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Great Lakes Dredge & Dock’s demanding reinvestments have drained its resources over the last five years, putting it in a pinch and limiting its ability to return capital to investors. Its free cash flow margin averaged negative 10.4%, meaning it lit $10.38 of cash on fire for every $100 in revenue.

Taking a step back, an encouraging sign is that Great Lakes Dredge & Dock’s margin expanded by 8.4 percentage points during that time. In light of its glaring cash burn, however, this improvement is a bucket of hot water in a cold ocean.

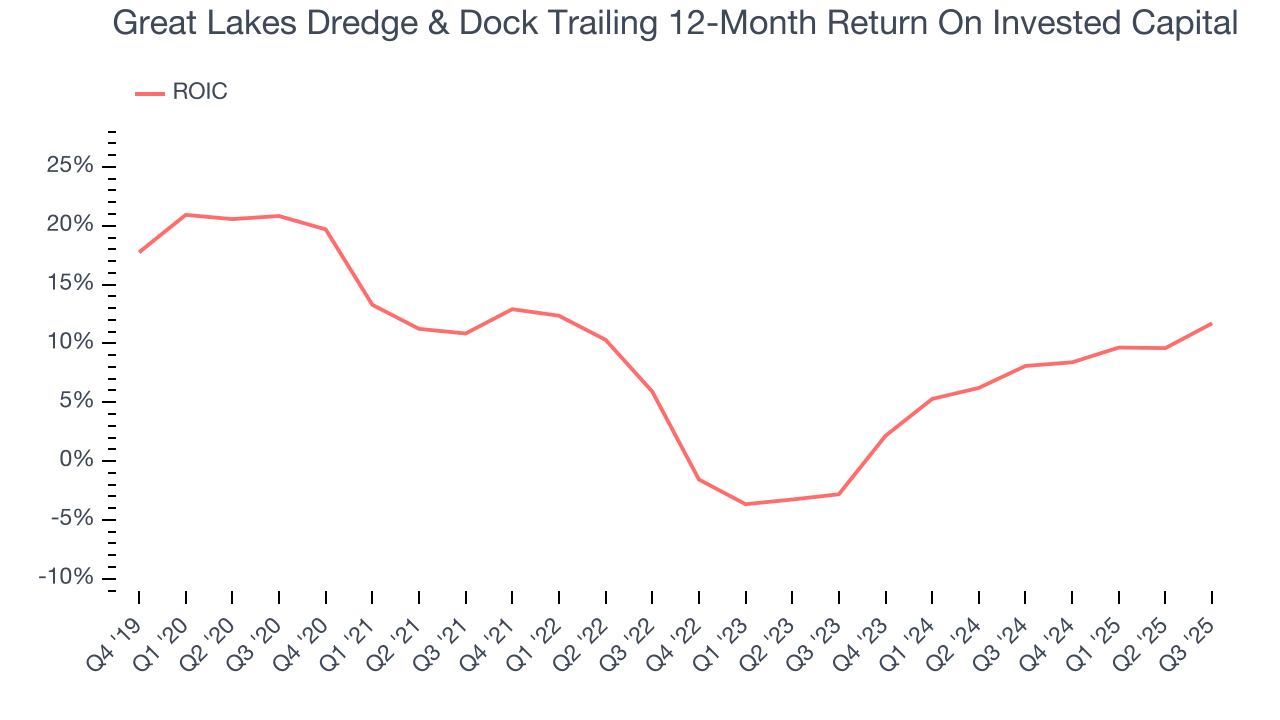

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Great Lakes Dredge & Dock historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 6.7%, somewhat low compared to the best industrials companies that consistently pump out 20%+.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Fortunately, Great Lakes Dredge & Dock’s ROIC averaged 1.5 percentage point increases over the last few years. This is a good sign, and if its returns keep rising, there’s a chance it could evolve into an investable business.

11. Balance Sheet Assessment

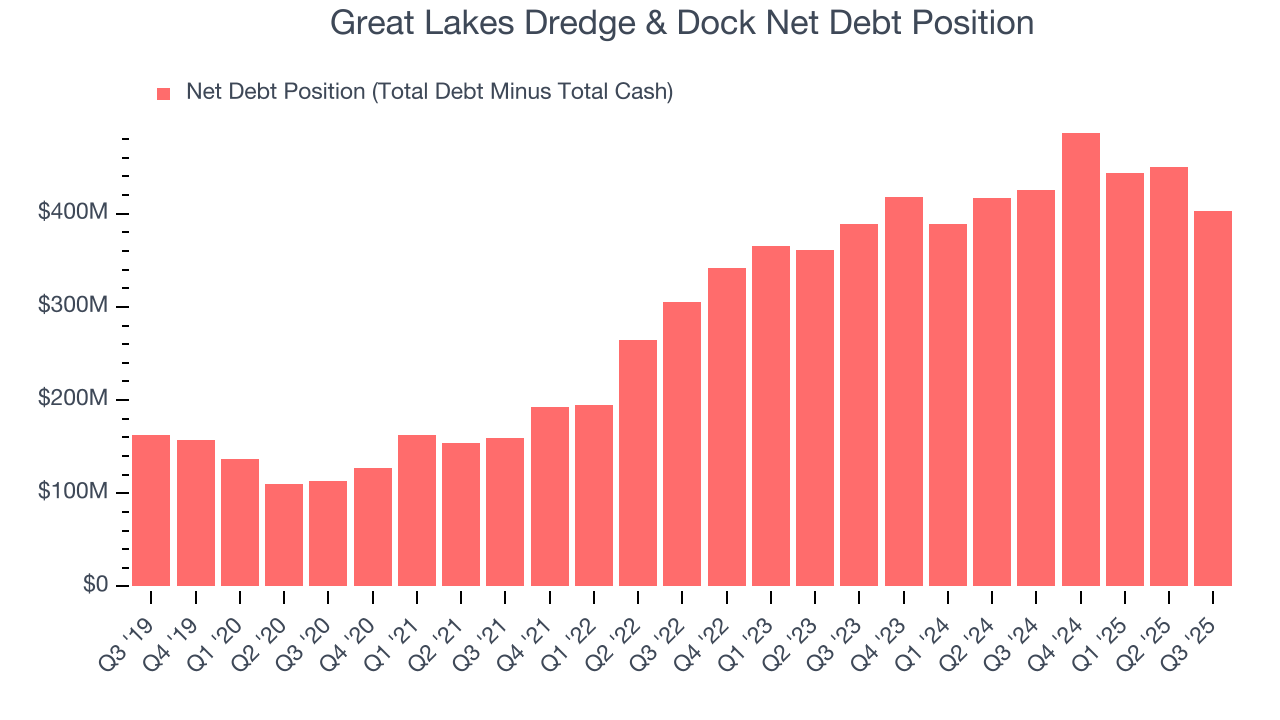

Great Lakes Dredge & Dock reported $12.67 million of cash and $415.3 million of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $167.6 million of EBITDA over the last 12 months, we view Great Lakes Dredge & Dock’s 2.4× net-debt-to-EBITDA ratio as safe. We also see its $18.13 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

12. Key Takeaways from Great Lakes Dredge & Dock’s Q3 Results

It was good to see Great Lakes Dredge & Dock beat analysts’ EPS expectations this quarter. We were also excited its EBITDA outperformed Wall Street’s estimates by a wide margin. On the other hand, its revenue missed. Overall, we think this was a decent quarter with some key metrics above expectations. The stock traded up 5.3% to $11.98 immediately following the results.

13. Is Now The Time To Buy Great Lakes Dredge & Dock?

Updated: March 13, 2026 at 11:44 PM EDT

When considering an investment in Great Lakes Dredge & Dock, investors should account for its valuation and business qualities as well as what’s happened in the latest quarter.

Great Lakes Dredge & Dock isn’t a terrible business, but it doesn’t pass our bar. For starters, its revenue growth was weak over the last five years. While its rising cash profitability gives it more optionality, the downside is its projected EPS for the next year is lacking. On top of that, its cash burn raises the question of whether it can sustainably maintain growth.

Great Lakes Dredge & Dock’s P/E ratio based on the next 12 months is 17.3x. While this valuation is reasonable, we don’t really see a big opportunity at the moment. We're pretty confident there are more exciting stocks to buy at the moment.

Wall Street analysts have a consensus one-year price target of $17 on the company (compared to the current share price of $16.92).