Robinhood (HOOD)

Robinhood is in a league of its own. Its fusion of growth, outstanding profitability, and encouraging prospects makes it a beloved asset.― StockStory Analyst Team

1. News

2. Summary

Why We Like Robinhood

With a mission to democratize finance, Robinhood (NASDAQ:HOOD) is an online consumer finance platform known for its commission-free stock and crypto trading.

- Impressive 48.8% annual revenue growth over the last three years indicates it’s winning market share

- Notable projected revenue growth of 25.7% for the next 12 months hints at market share gains

- Platform is difficult to replicate at scale and results in a best-in-class gross margin of 93.2%

Robinhood is a remarkable business. The price looks fair when considering its quality, and we think now is the time to buy.

Why Is Now The Time To Buy Robinhood?

At $81.55 per share, Robinhood trades at 21.7x forward EV/EBITDA. Looking at the consumer internet space, we think the valuation is fair - potentially even too low - for the business quality.

Where you buy a stock impacts returns. Our analysis shows that business quality is a much bigger determinant of market outperformance over the long term compared to entry price, but getting a good deal on a stock certainly isn’t a bad thing.

3. Robinhood (HOOD) Research Report: Q4 CY2025 Update

Financial services company Robinhood (NASDAQ:HOOD) fell short of the market’s revenue expectations in Q4 CY2025, but sales rose 26.5% year on year to $1.28 billion. Its GAAP profit of $0.66 per share was 3.8% above analysts’ consensus estimates.

Robinhood (HOOD) Q4 CY2025 Highlights:

- Revenue: $1.28 billion vs analyst estimates of $1.34 billion (26.5% year-on-year growth, 3.9% miss)

- EPS (GAAP): $0.66 vs analyst estimates of $0.64 (3.8% beat)

- Adjusted EBITDA: $761 million vs analyst estimates of $832.3 million (59.3% margin, 8.6% miss)

- Operating Margin: 51.5%, down from 54.8% in the same quarter last year

- Free Cash Flow was -$950 million compared to -$1.59 billion in the previous quarter

- Market Capitalization: $77.83 billion

Company Overview

With a mission to democratize finance, Robinhood (NASDAQ:HOOD) is an online consumer finance platform known for its commission-free stock and crypto trading.

Historically, the average person would pay high broker fees to place buy and sell orders. Robinhood’s founders, Vlad Tenev and Baiju Bhatt (mathematicians and roommates at Stanford), sought to lower the barriers to entry by pioneering commission-free trading.

Commission-free trading uses algorithms to take customer orders and route them to market makers. In exchange for sourcing the trade, the router takes a percentage of the market maker's profit. This is called payment for order flow, and it is a huge chunk of Robinhood’s trading revenue.

Today, Robinhood not only generates revenue from payment for order flow but also interest on margin trading loans, interest on uninvested cash, and subscription fees for Robinhood Gold. Robinhood Gold costs $5 per month and gives users access to premium features such as 24/7 trading, cheaper margin loans, boosted interest rates on uninvested cash, and research reports. Because it's a software company, Robinhood has fewer employees and a more efficient cost base than its legacy competitors.

Robinhood's long-term strategy is to increase its users and assets under custody by becoming a one-stop shop for consumer finance. It plans to achieve this by rolling out products like retirement accounts and credit cards. Investors under the age of 35 comprise a majority of Robinhood's user base as it has no account minimums and initially built its products exclusively for mobile devices.

4. Financial Technology

Financial technology companies benefit from the increasing consumer demand for digital payments, banking, and finance. Tailwinds fueling this trend include e-commerce along with improvements in blockchain infrastructure and AI-driven credit underwriting, which make access to money faster and cheaper. Despite regulatory scrutiny and resistance from traditional financial institutions, fintechs are poised for long-term growth as they disrupt legacy systems by expanding financial services to underserved population segments.

Robinhood’s competitors include Charles Schwab (NYSE:SCHW), Fidelity (NYSE:FNF), Interactive Brokers (NASDAQ:IBKR), Coinbase (NASDAQ:COIN), and private companies M1 Finance and Webull.

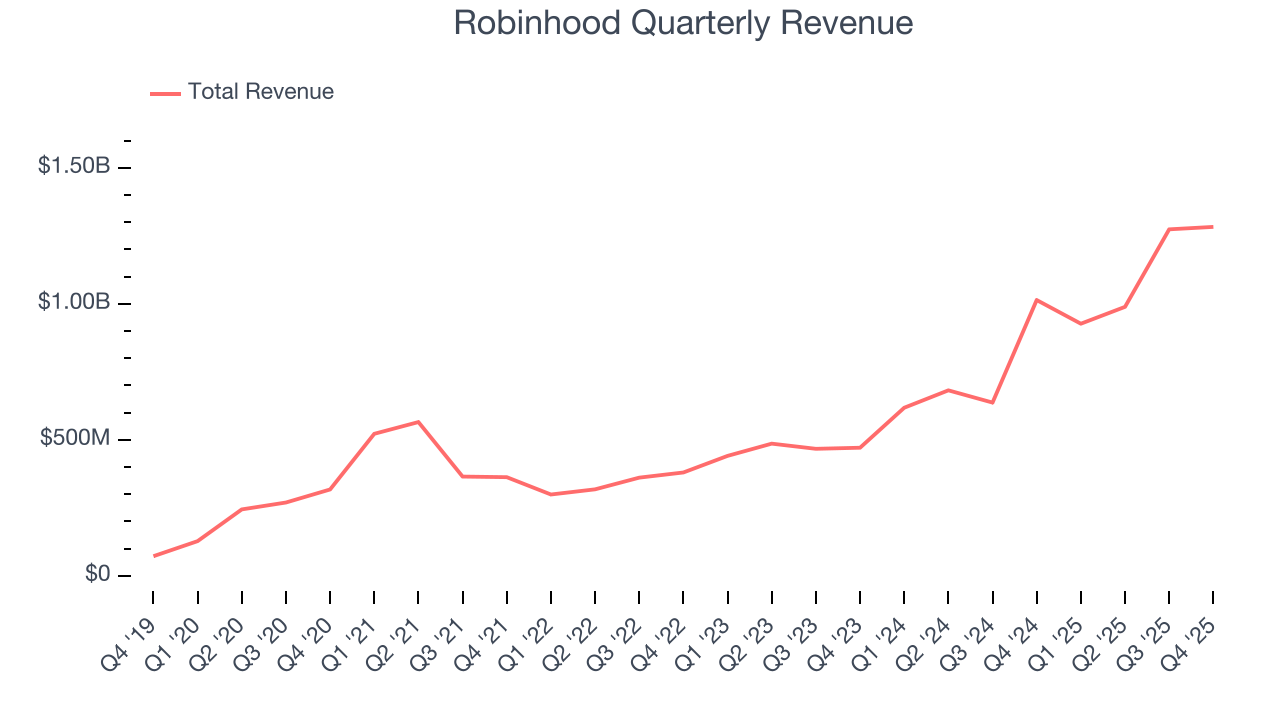

5. Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Thankfully, Robinhood’s 48.8% annualized revenue growth over the last three years was incredible. Its growth surpassed the average consumer internet company and shows its offerings resonate with customers, a great starting point for our analysis.

This quarter, Robinhood generated an excellent 26.5% year-on-year revenue growth rate, but its $1.28 billion of revenue fell short of Wall Street’s high expectations.

Looking ahead, sell-side analysts expect revenue to grow 25.7% over the next 12 months, a deceleration versus the last three years. Despite the slowdown, this projection is admirable and suggests the market is baking in success for its products and services.

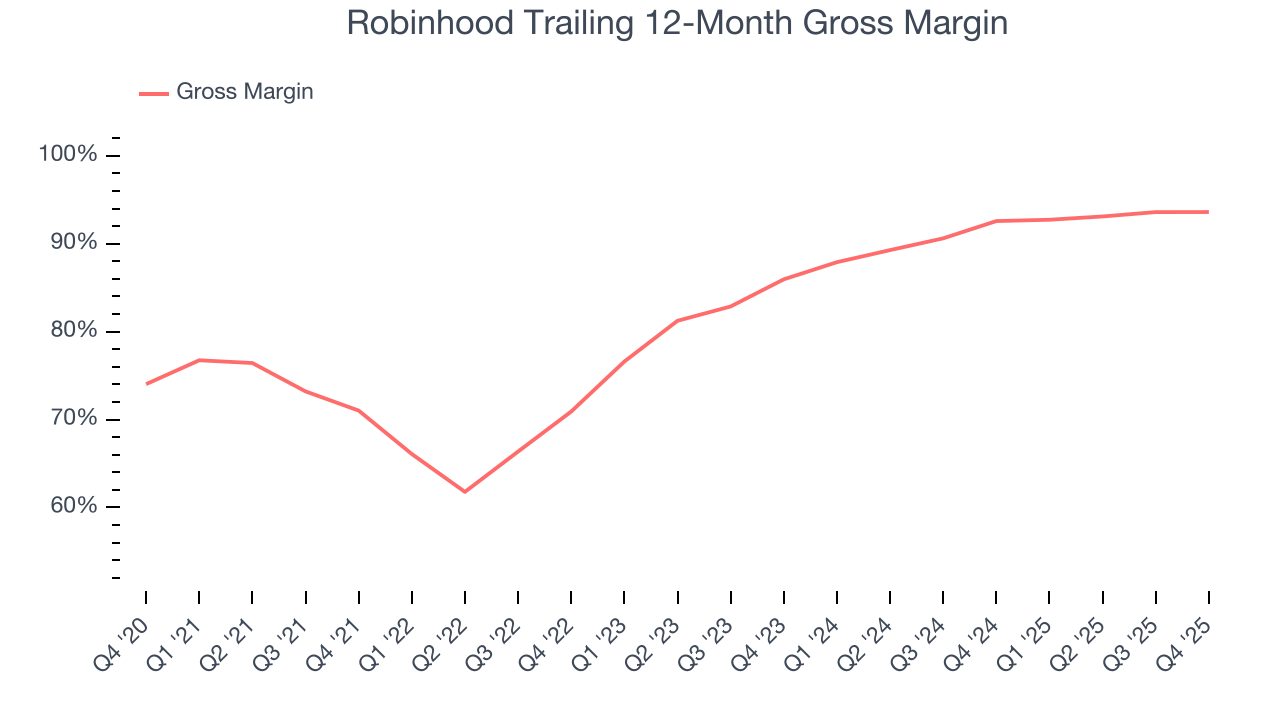

6. Gross Margin & Pricing Power

A company’s gross profit margin has a significant impact on its ability to exert pricing power, develop new products, and invest in marketing. These factors can determine the winner in a competitive market.

For fintech businesses like Robinhood, gross profit tells us how much money the company gets to keep after covering the base cost of its products and services, which typically include transaction/payment processing, hosting, and bandwidth fees in addition to the costs necessary to onboard customers, such as identity verification.

Robinhood’s gross margin is one of the best in the consumer internet sector, an output of its asset-lite business model and strong pricing power. It also enables the company to fund large investments in new products and marketing during periods of rapid growth to achieve higher profits in the future. As you can see below, it averaged an elite 93.2% gross margin over the last two years. That means Robinhood only paid its providers $6.80 for every $100 in revenue.

Robinhood produced a 97% gross profit margin in Q4, in line with the same quarter last year. On a wider time horizon, Robinhood’s full-year margin has been trending up over the past 12 months, increasing by 1 percentage points. If this move continues, it could suggest better unit economics due to more leverage from its growing sales on the fixed portion of its cost of goods sold (such as servers).

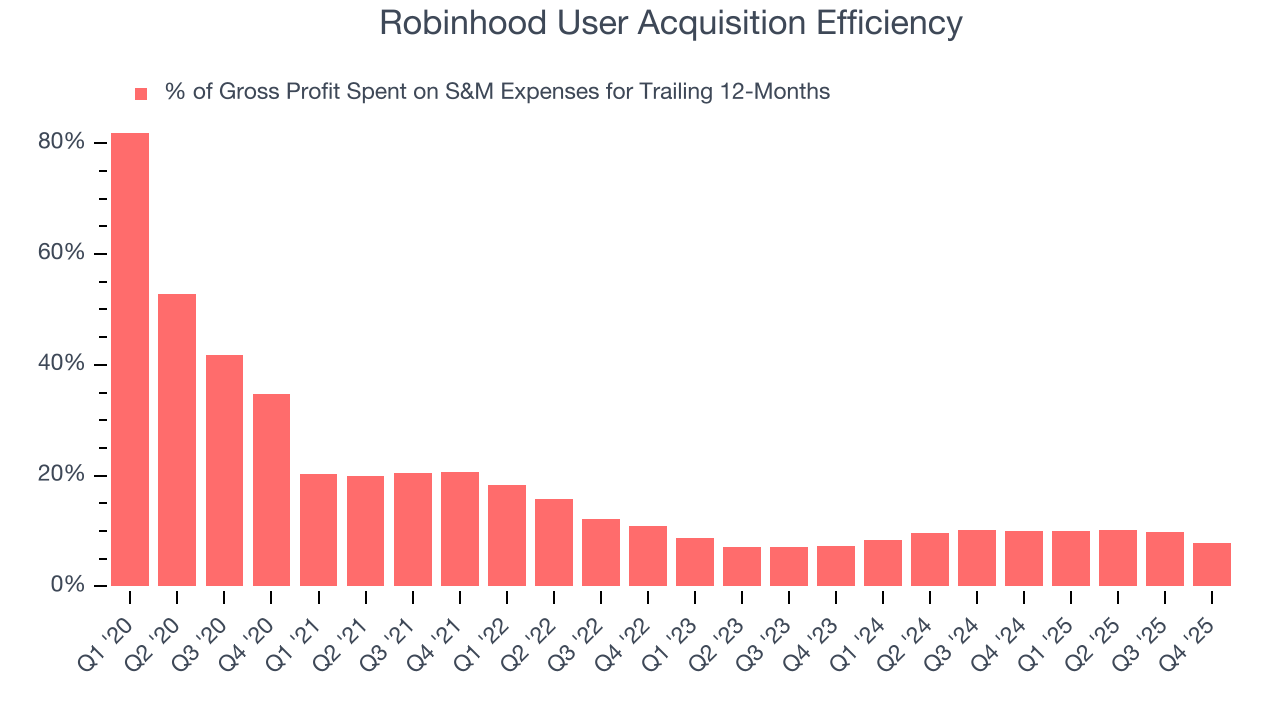

7. User Acquisition Efficiency

Unlike enterprise software that’s typically sold by dedicated sales teams, consumer internet businesses like Robinhood grow from a combination of product virality, paid advertisement, and incentives.

Robinhood is extremely efficient at acquiring new users, spending only 7.9% of its gross profit on sales and marketing expenses over the last year. This efficiency indicates that it has a highly differentiated product offering and strong brand reputation, giving Robinhood the freedom to invest its resources into new growth initiatives while maintaining optionality.

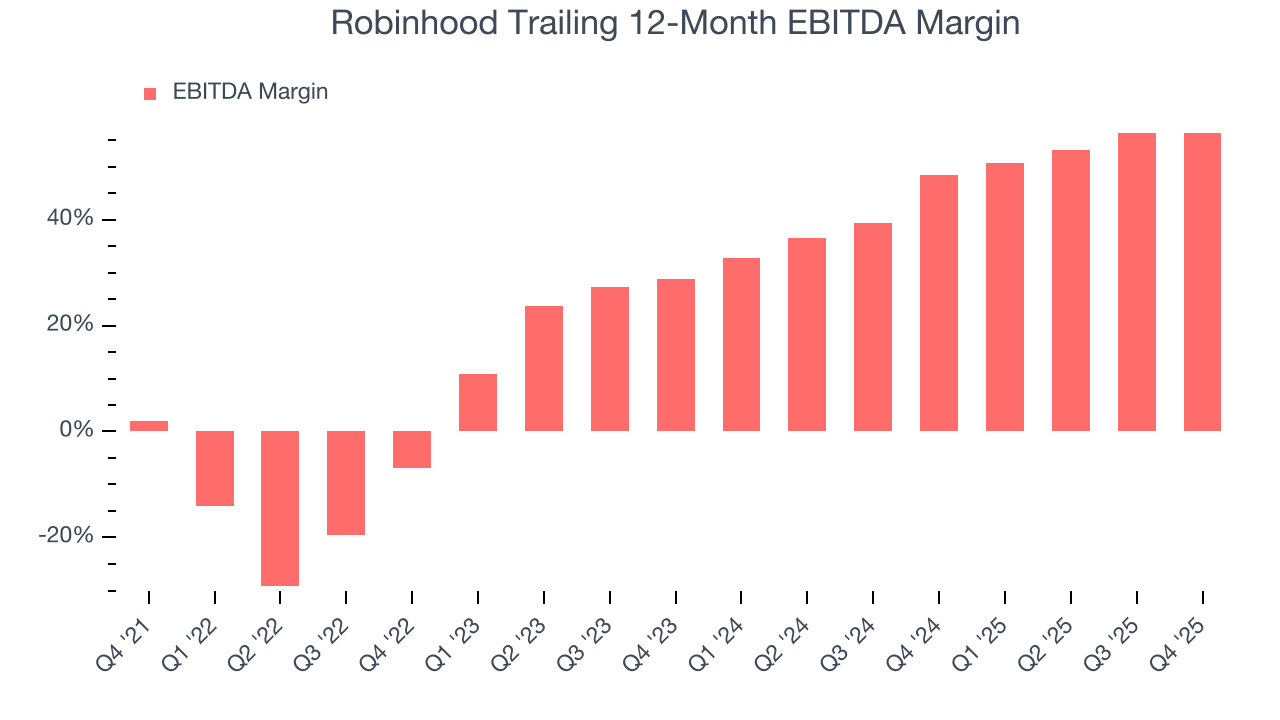

8. EBITDA

Investors regularly analyze operating income to understand a company’s profitability. Similarly, EBITDA is a common profitability metric for consumer internet companies because it excludes various one-time or non-cash expenses, offering a better perspective of the business’s profit potential.

Robinhood has been a well-oiled machine over the last two years. It demonstrated elite profitability for a consumer internet business, boasting an average EBITDA margin of 53.2%. This result isn’t surprising as its high gross margin gives it a favorable starting point.

Analyzing the trend in its profitability, Robinhood’s EBITDA margin rose by 63.3 percentage points over the last few years, as its sales growth gave it immense operating leverage.

In Q4, Robinhood generated an EBITDA margin profit margin of 59.3%, down 1.1 percentage points year on year. Since Robinhood’s EBITDA margin decreased more than its gross margin, we can assume it was less efficient because expenses such as marketing, R&D, and administrative overhead increased.

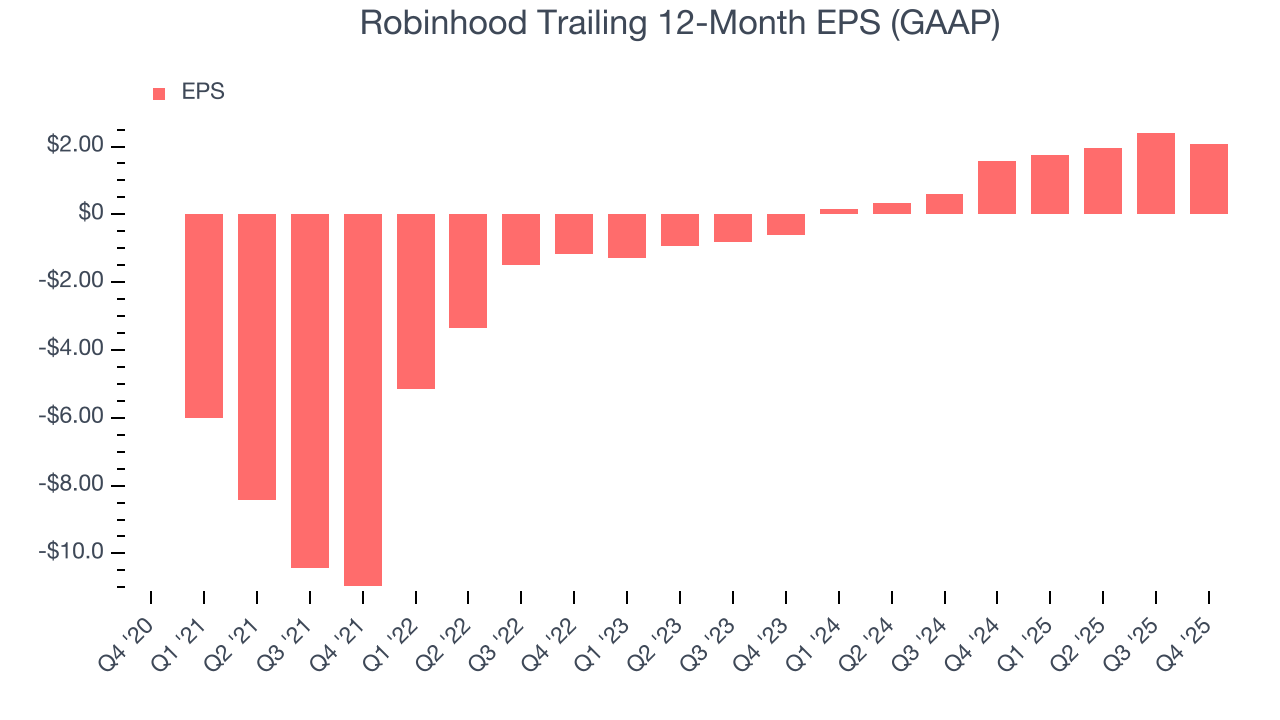

9. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Robinhood’s full-year EPS flipped from negative to positive over the last three years. This is a good sign and shows it’s at an inflection point.

In Q4, Robinhood reported EPS of $0.66, down from $1.01 in the same quarter last year. Despite falling year on year, this print beat analysts’ estimates by 3.8%. Over the next 12 months, Wall Street expects Robinhood’s full-year EPS of $2.06 to grow 22.3%.

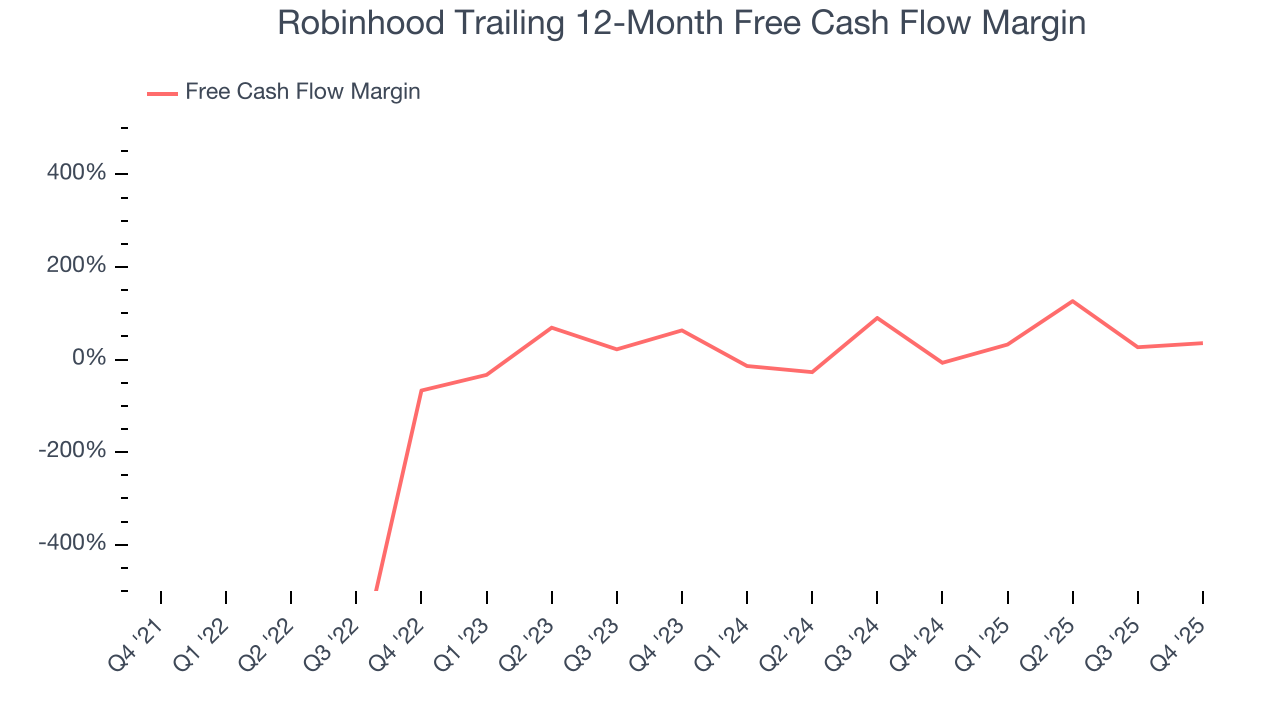

10. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Robinhood has shown robust cash profitability, driven by its attractive business model and cost-effective customer acquisition strategy that enable it to invest in new products and services rather than sales and marketing. The company’s free cash flow margin averaged 18.5% over the last two years, quite impressive for a consumer internet business.

Taking a step back, we can see that Robinhood’s margin expanded meaningfully over the last few years. This is encouraging, and we can see it became a less capital-intensive business because its free cash flow profitability rose more than its operating profitability.

Robinhood burned through $950 million of cash in Q4, equivalent to a negative 74% margin. The company’s cash burn slowed from $1.42 billion of lost cash in the same quarter last year. These numbers deviate from its longer-term margin, but we wouldn’t read too much into the short term because investment needs can be seasonal, leading to temporary swings.

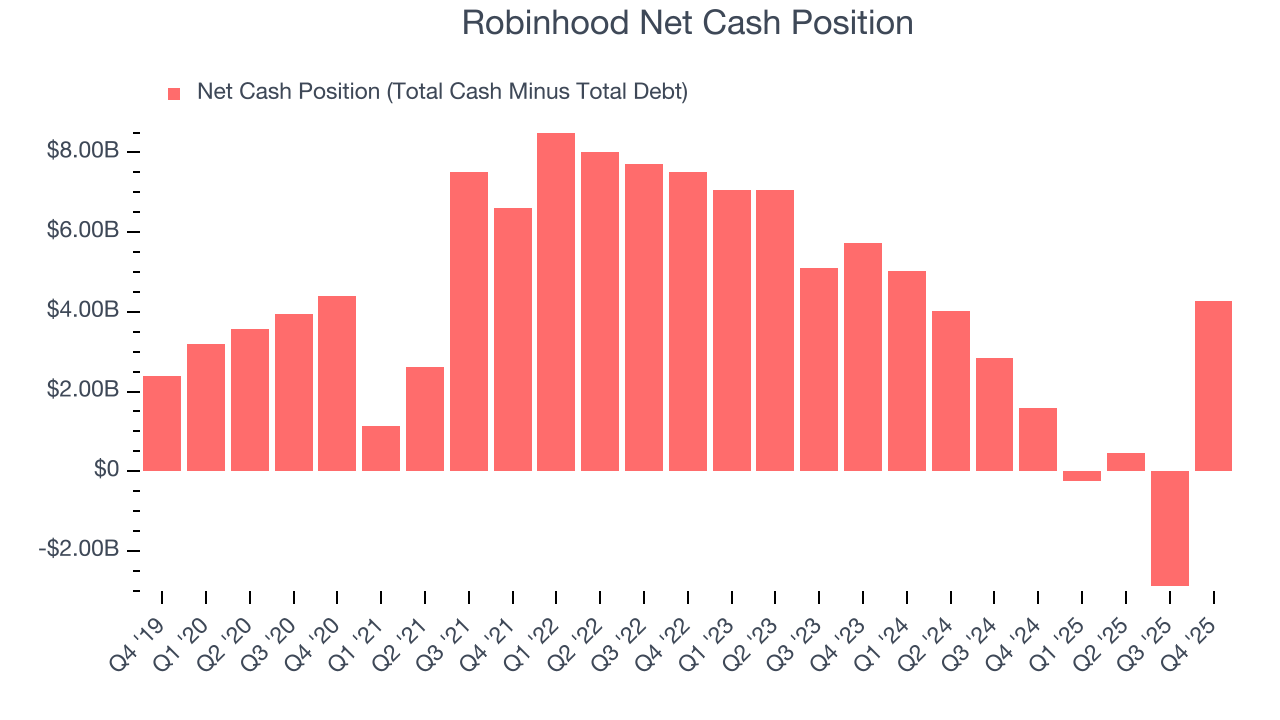

11. Balance Sheet Assessment

Businesses that maintain a cash surplus face reduced bankruptcy risk.

Robinhood is a profitable, well-capitalized company with $4.26 billion of cash and no debt. This position is 5.5% of its market cap and gives it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

12. Key Takeaways from Robinhood’s Q4 Results

We struggled to find many positives in these results. Its revenue missed and its EBITDA fell short of Wall Street’s estimates. Overall, this was a softer quarter. The stock traded down 5% to $81.55 immediately after reporting.

13. Is Now The Time To Buy Robinhood?

Updated: February 10, 2026 at 9:21 PM EST

When considering an investment in Robinhood, investors should account for its valuation and business qualities as well as what’s happened in the latest quarter.

There are multiple reasons why we think Robinhood is an elite consumer internet company. For starters, its revenue growth was exceptional over the last three years. On top of that, its admirable gross margins are a wonderful starting point for the overall profitability of the business, and its impressive EBITDA margins show it has a highly efficient business model.

Robinhood’s EV/EBITDA ratio based on the next 12 months is 21.6x. Analyzing the consumer internet landscape today, Robinhood’s positive attributes shine bright. We think it’s one of the best businesses in our coverage and like the stock at this price.

Wall Street analysts have a consensus one-year price target of $146.34 on the company (compared to the current share price of $81.55), implying they see 79.5% upside in buying Robinhood in the short term.