Kratos (KTOS)

We’re not sold on Kratos. Its weak returns on capital suggest it doesn’t generate sufficient profits, a sign of value destruction.― StockStory Analyst Team

1. News

2. Summary

Why Kratos Is Not Exciting

Established with a commitment to supporting national security, Kratos (NASDAQ:KTOS) is a provider of advanced engineering, technology, and security solutions tailored for critical national security applications.

- Increased cash burn over the last five years raises questions about the return timeline for its investments

- Low returns on capital reflect management’s struggle to allocate funds effectively

- The good news is that its market share is on track to rise over the next 12 months as its 21.6% projected revenue growth implies demand will accelerate from its two-year trend

Kratos’s quality doesn’t meet our bar. There are more appealing investments to be made.

Why There Are Better Opportunities Than Kratos

Kratos’s stock price of $95.56 implies a valuation ratio of 115.3x forward P/E. This valuation is extremely expensive, especially for the quality you get.

There are stocks out there featuring similar valuation multiples with better fundamentals. We prefer to invest in those.

3. Kratos (KTOS) Research Report: Q4 CY2025 Update

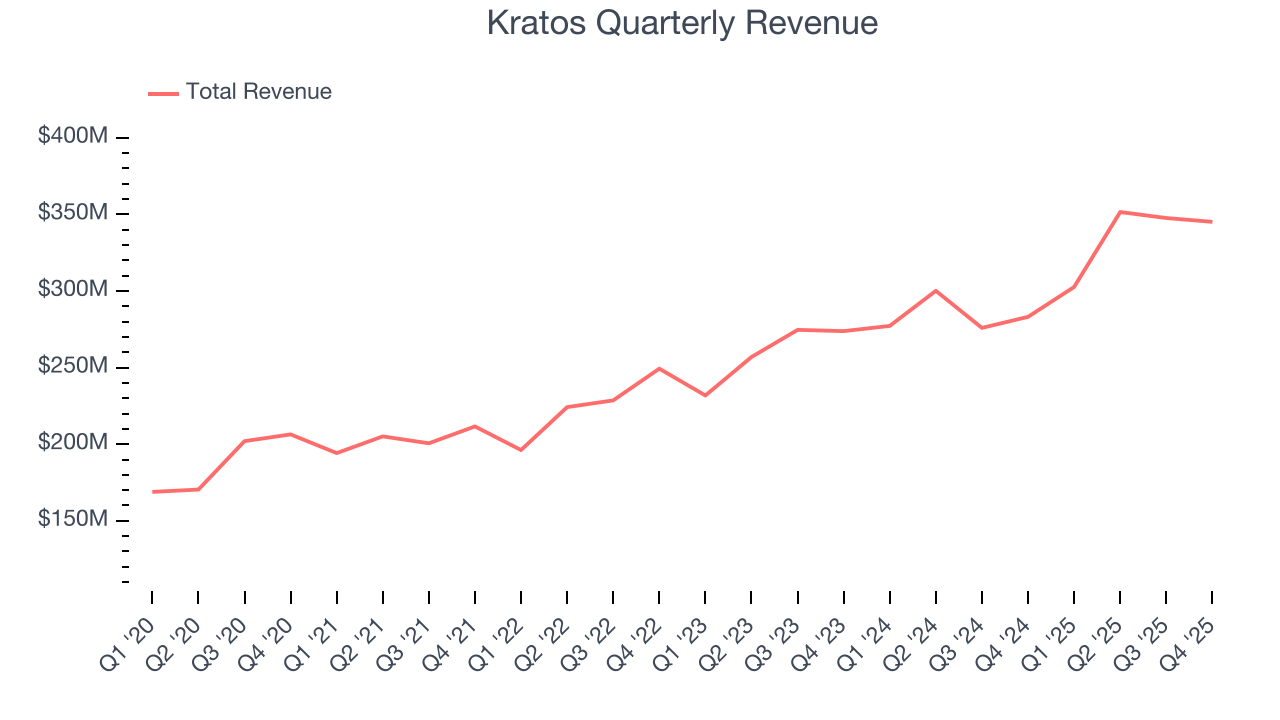

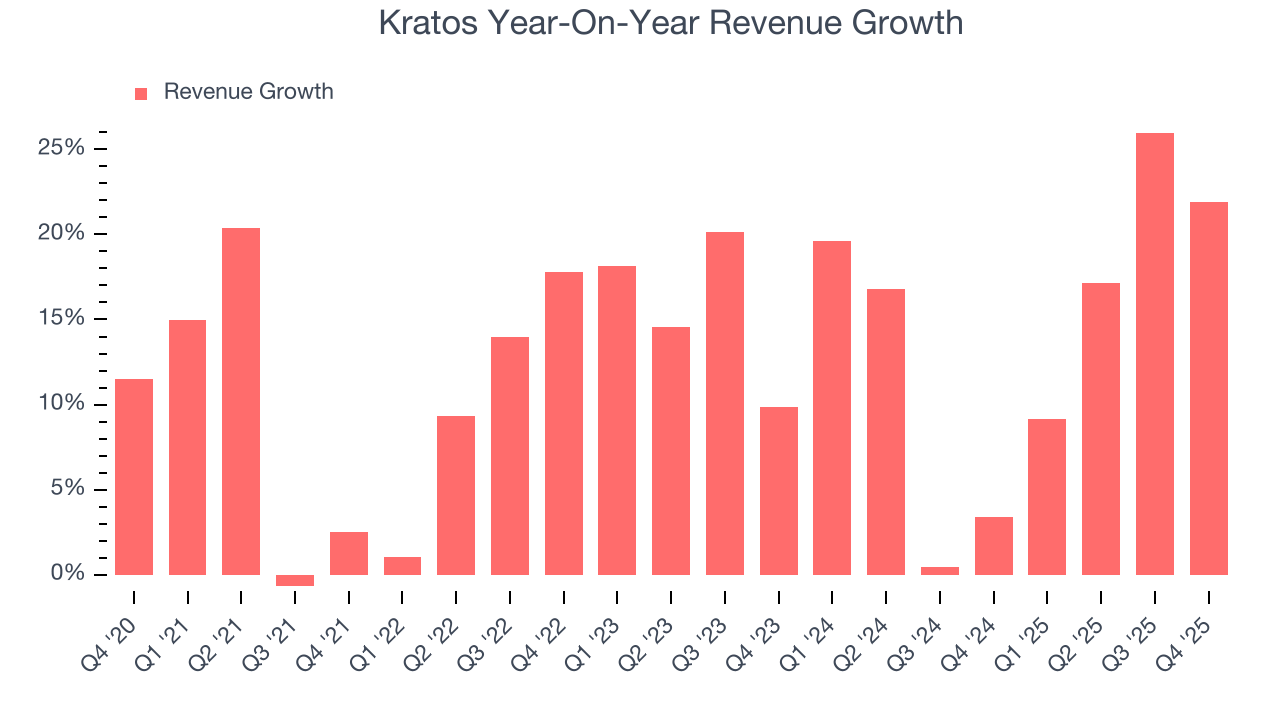

Aerospace and defense company Kratos (NASDAQ:KTOS) reported revenue ahead of Wall Street’s expectations in Q4 CY2025, with sales up 21.9% year on year to $345.1 million. Revenue guidance for the full year exceeded analysts’ estimates, but next quarter’s guidance of $340 million was less impressive, coming in 0.7% below expectations. Its non-GAAP profit of $0.18 per share was 22.1% above analysts’ consensus estimates.

Kratos (KTOS) Q4 CY2025 Highlights:

- Revenue: $345.1 million vs analyst estimates of $324.7 million (21.9% year-on-year growth, 6.3% beat)

- Adjusted EPS: $0.18 vs analyst estimates of $0.15 (22.1% beat)

- Adjusted EBITDA: $34.1 million vs analyst estimates of $31.78 million (9.9% margin, 7.3% beat)

- Revenue Guidance for Q1 CY2026 is $340 million at the midpoint, below analyst estimates of $342.4 million

- EBITDA guidance for the upcoming financial year 2026 is $162 million at the midpoint, above analyst estimates of $159.7 million

- Operating Margin: 2.4%, up from 1.1% in the same quarter last year

- Free Cash Flow was -$12.1 million, down from $32 million in the same quarter last year

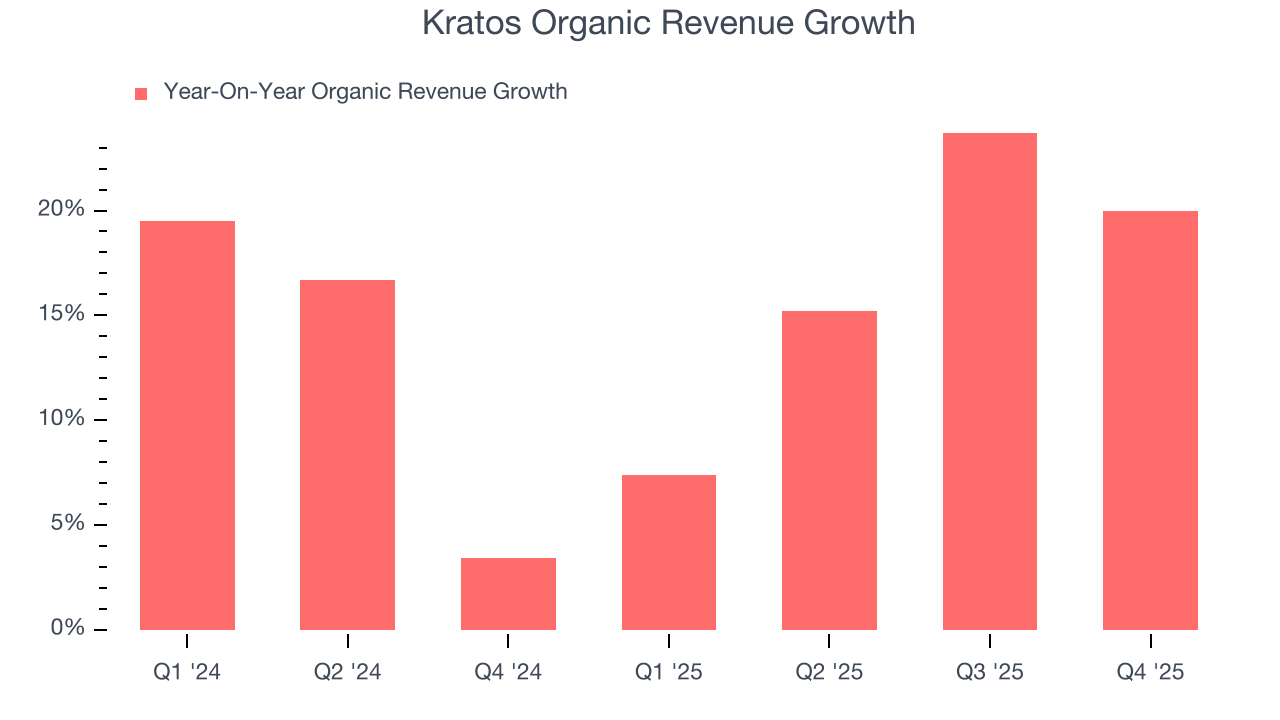

- Organic Revenue rose 20% year on year (beat)

- Market Capitalization: $16.37 billion

Company Overview

Established with a commitment to supporting national security, Kratos (NASDAQ:KTOS) is a provider of advanced engineering, technology, and security solutions tailored for critical national security applications.

Kratos was originally founded in 1994 as Wireless Facilities, a company focused on wireless communications. Over time, the company transformed significantly through a strategic series of acquisitions that began aggressively around 2004. These acquisitions were aimed at expanding its footprint in the defense and national security sectors, making Kratos a notable player in advanced military technology, satellite communications, and unmanned systems.

Today, Kratos provides advanced technologies primarily focused on the defense sector. Products range from microwave electronics to ballistic missile systems. One key area is its unmanned systems, which include aerial drones like the UTAP-22 Mako. The UTAP-22 Mako is known for its capabilities in tactical missions alongside manned aircraft, thereby extending the operational scope of conventional forces without risking pilot lives. Another important area for Kratos is its satellite communication systems. These systems are crucial for managing satellites in space, ensuring they work correctly and stay on course. Kratos' technology helps control these satellites, which is vital for everything from checking the weather to ensuring national security. Through these products, Kratos serves a diverse range of end markets including defense, intelligence, and civil government sectors across the globe.

Kratos generates revenue primarily through contracts with government and defense agencies. These contracts often provide recurring revenue streams, which support the company’s financial stability. This recurring revenue comes from long-term contracts and ongoing service agreements, ensuring a steady income as they provide updates, maintenance, and other support services. For instance, in April 2021, Kratos secured a contract supporting the Army Ground Aerial Target Control System. This contract entails updating software, conducting cyber security inspections, and replacing parts.

4. Defense Contractors

Defense contractors typically require technical expertise and government clearance. Companies in this sector can also enjoy long-term contracts with government bodies, leading to more predictable revenues. Combined, these factors create high barriers to entry and can lead to limited competition. Lately, geopolitical tensions–whether it be Russia’s invasion of Ukraine or China’s aggression towards Taiwan–highlight the need for defense spending. On the other hand, demand for these products can ebb and flow with defense budgets and even who is president, as different administrations can have vastly different ideas of how to allocate federal funds.

Kratos’ competitors include Textron (NYSE:TXT) and Northrop Grumman (NYSE:NOC)

5. Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Over the last five years, Kratos grew its sales at an excellent 12.5% compounded annual growth rate. Its growth beat the average industrials company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Kratos’s annualized revenue growth of 14% over the last two years is above its five-year trend, suggesting its demand was strong and recently accelerated.

We can better understand the company’s sales dynamics by analyzing its organic revenue, which strips out one-time events like acquisitions and currency fluctuations that don’t accurately reflect its fundamentals. Over the last two years, Kratos’s organic revenue averaged 15.1% year-on-year growth. Because this number aligns with its two-year revenue growth, we can see the company’s core operations (not acquisitions and divestitures) drove most of its results.

This quarter, Kratos reported robust year-on-year revenue growth of 21.9%, and its $345.1 million of revenue topped Wall Street estimates by 6.3%. Company management is currently guiding for a 12.4% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 16.8% over the next 12 months, an improvement versus the last two years. This projection is eye-popping and suggests its newer products and services will catalyze better top-line performance.

6. Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

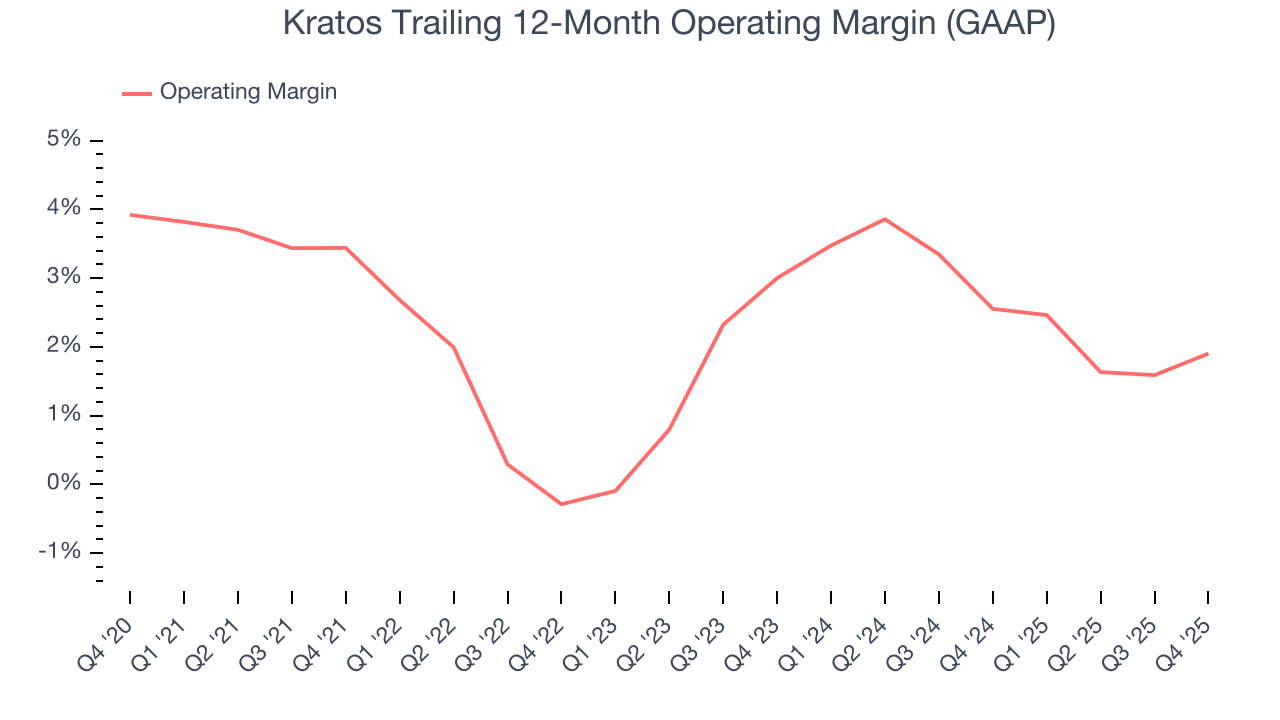

Kratos was profitable over the last five years but held back by its large cost base. Its average operating margin of 2.1% was weak for an industrials business.

Analyzing the trend in its profitability, Kratos’s operating margin decreased by 1.5 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. Kratos’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers.

In Q4, Kratos generated an operating margin profit margin of 2.4%, up 1.3 percentage points year on year. This increase was a welcome development and shows it was more efficient.

7. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

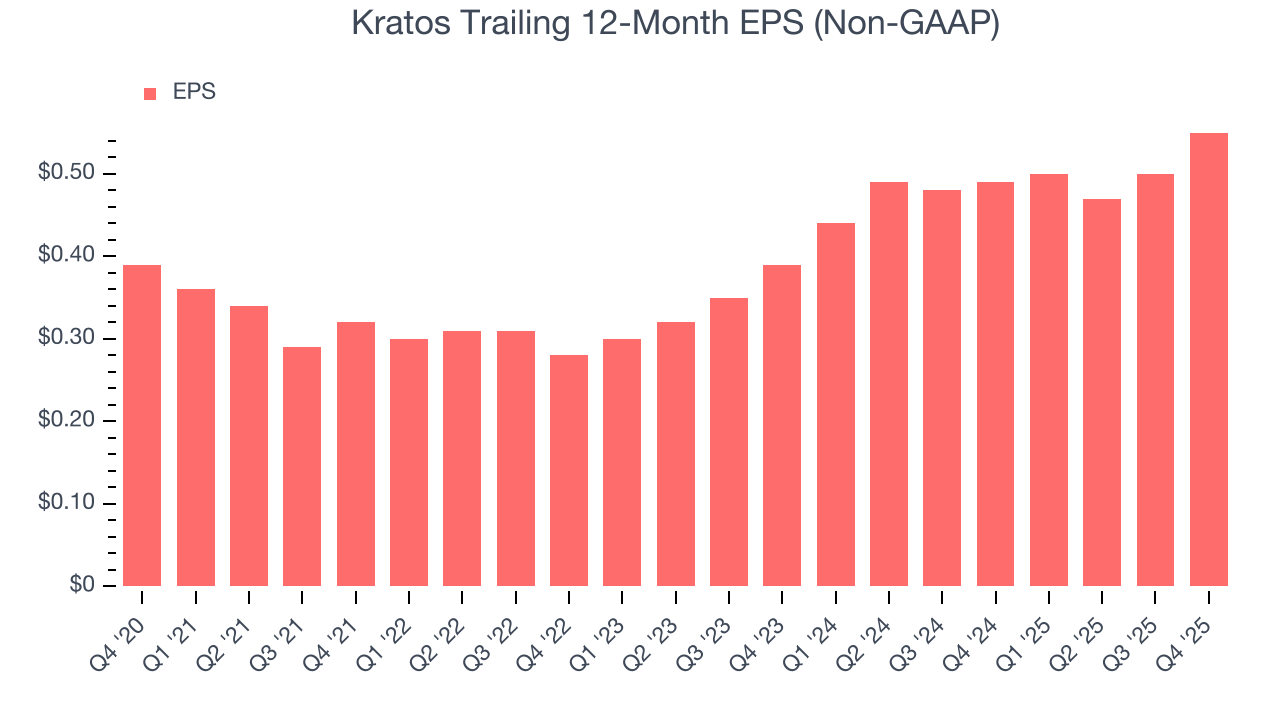

Kratos’s EPS grew at an unimpressive 7.1% compounded annual growth rate over the last five years, lower than its 12.5% annualized revenue growth. This tells us the company became less profitable on a per-share basis as it expanded.

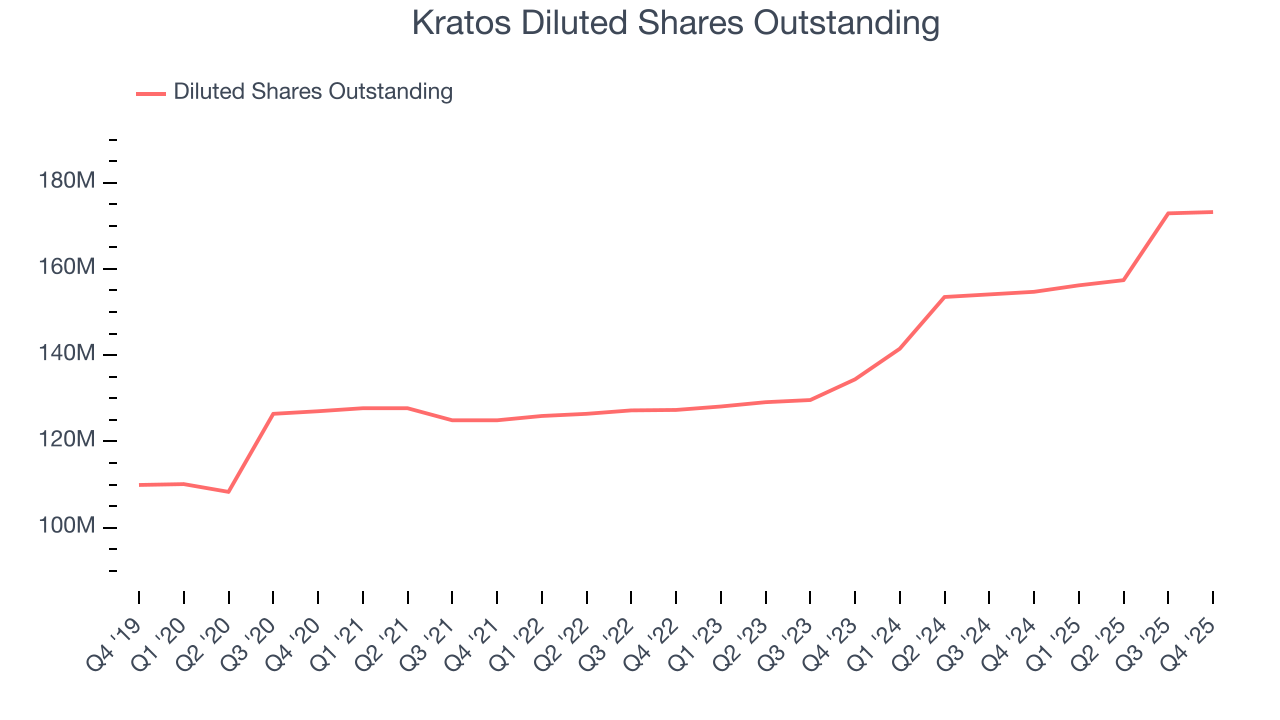

We can take a deeper look into Kratos’s earnings to better understand the drivers of its performance. As we mentioned earlier, Kratos’s operating margin expanded this quarter but declined by 1.5 percentage points over the last five years. Its share count also grew by 36.4%, meaning the company not only became less efficient with its operating expenses but also diluted its shareholders.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Kratos, its two-year annual EPS growth of 18.8% was higher than its five-year trend. This acceleration made it one of the faster-growing industrials companies in recent history.

In Q4, Kratos reported adjusted EPS of $0.18, up from $0.13 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Kratos’s full-year EPS of $0.55 to grow 41.3%.

8. Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

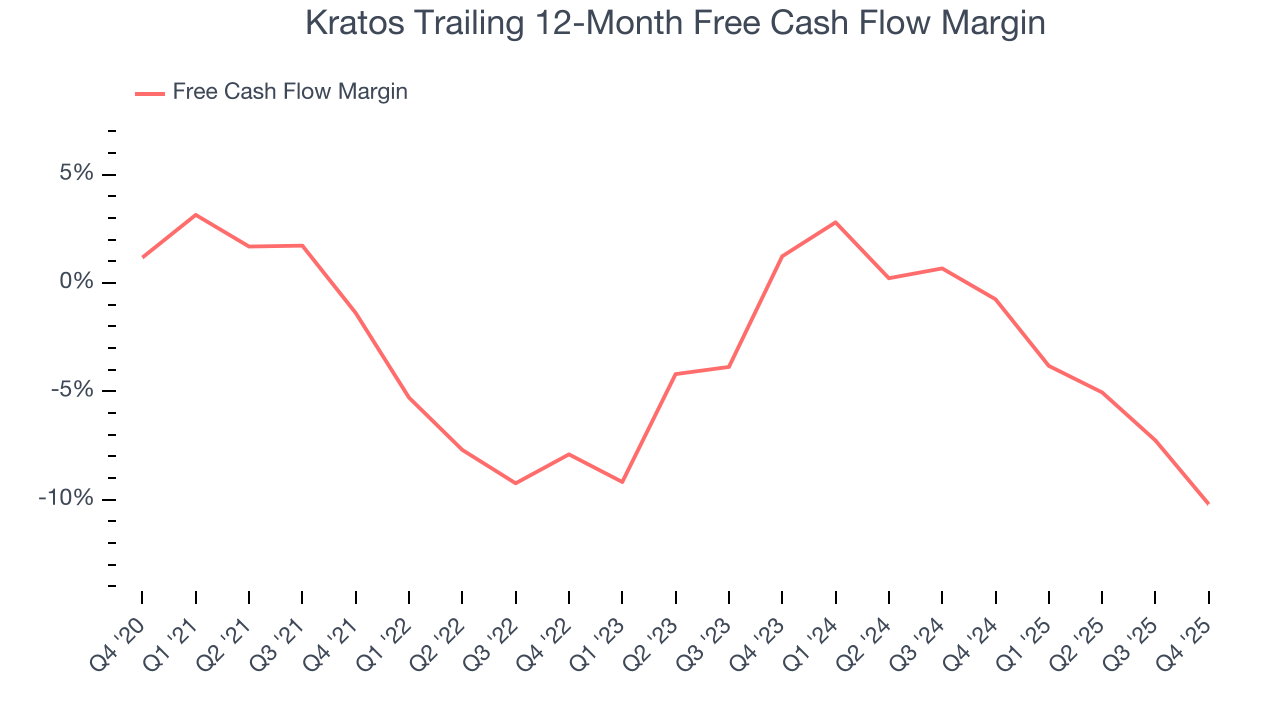

Kratos’s demanding reinvestments have drained its resources over the last five years, putting it in a pinch and limiting its ability to return capital to investors. Its free cash flow margin averaged negative 4.1%, meaning it lit $4.12 of cash on fire for every $100 in revenue.

Taking a step back, we can see that Kratos’s margin dropped by 8.8 percentage points during that time. Almost any movement in the wrong direction is undesirable because it is already burning cash. If the trend continues, it could signal it’s becoming a more capital-intensive business.

Kratos burned through $12.1 million of cash in Q4, equivalent to a negative 3.5% margin. The company’s cash flow turned negative after being positive in the same quarter last year, suggesting its historical struggles have dragged on.

9. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

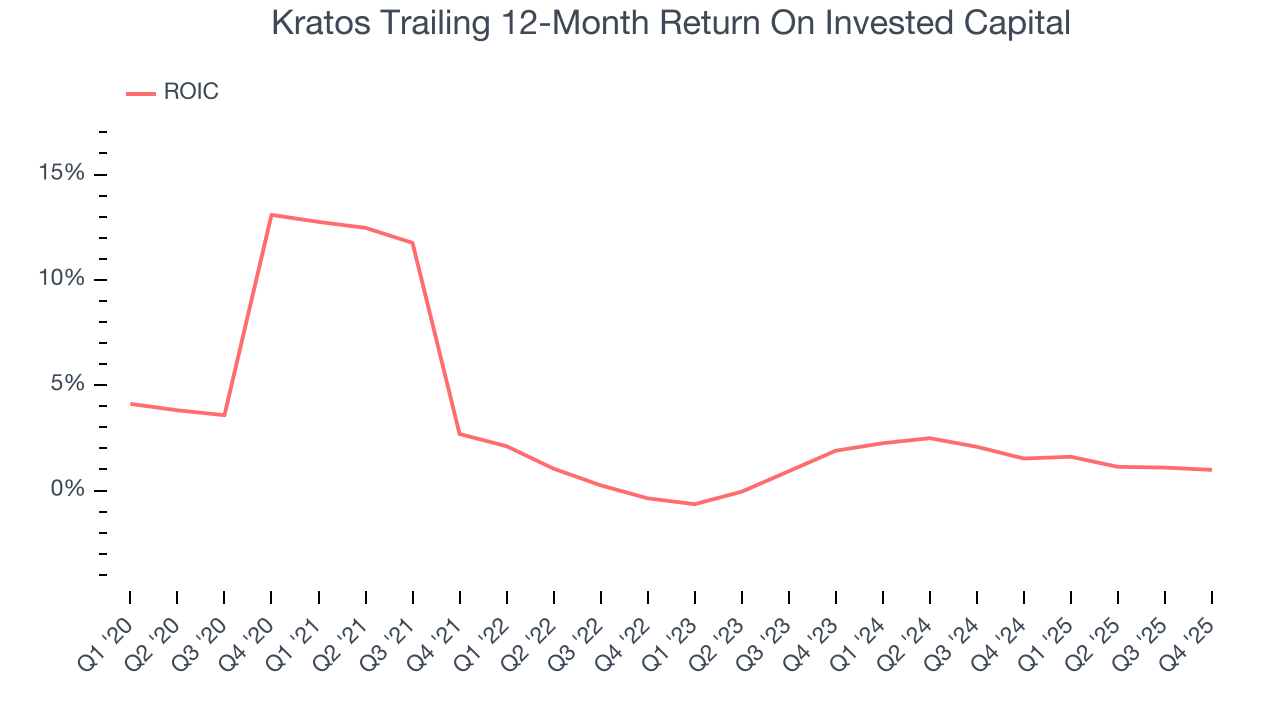

Kratos historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 1.3%, lower than the typical cost of capital (how much it costs to raise money) for industrials companies.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Unfortunately, Kratos’s ROIC has stayed the same over the last few years. If the company wants to become an investable business, it must improve its returns by generating more profitable growth.

10. Balance Sheet Assessment

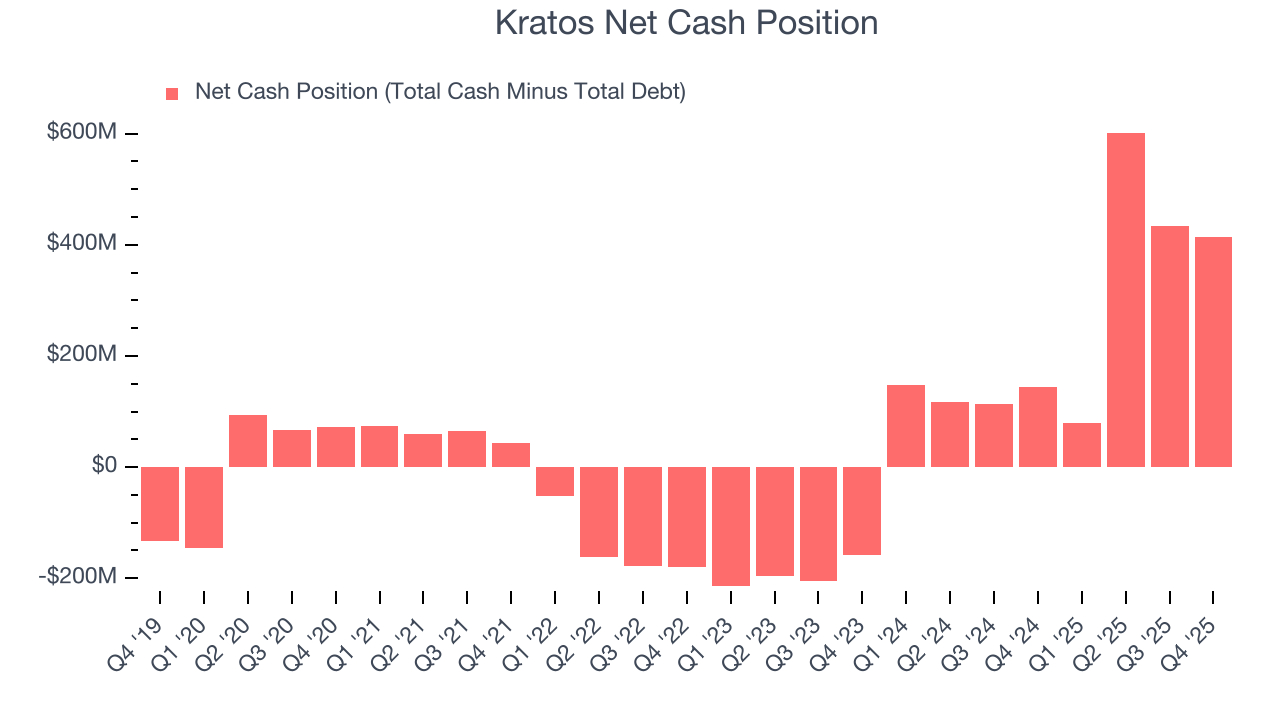

Companies with more cash than debt have lower bankruptcy risk.

Kratos is a well-capitalized company with $560.6 million of cash and $145.8 million of debt on its balance sheet. This $414.8 million net cash position is 2.5% of its market cap and gives it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

11. Key Takeaways from Kratos’s Q4 Results

We were impressed by how significantly Kratos blew past analysts’ organic revenue expectations this quarter. We were also excited its revenue outperformed Wall Street’s estimates by a wide margin. On the other hand, its EBITDA guidance for next quarter missed and its revenue guidance for next quarter fell slightly short of Wall Street’s estimates. Zooming out, we think this was a good print with some key areas of upside. The stock remained flat at $90.70 immediately after reporting.

12. Is Now The Time To Buy Kratos?

Updated: March 17, 2026 at 11:19 PM EDT

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in Kratos.

Kratos isn’t a bad business, but we’re not clamoring to buy it here and now. First off, its revenue growth was impressive over the last five years and is expected to accelerate over the next 12 months. And while Kratos’s relatively low ROIC suggests management has struggled to find compelling investment opportunities, its organic revenue growth has been marvelous.

Kratos’s P/E ratio based on the next 12 months is 115.3x. This valuation tells us it’s a bit of a market darling with a lot of good news priced in - you can find more timely opportunities elsewhere.

Wall Street analysts have a consensus one-year price target of $117.95 on the company (compared to the current share price of $95.56).