Limbach (LMB)

Limbach is an exciting business. Its outstanding and increasing returns on capital imply its market position is becoming more dominant.― StockStory Analyst Team

1. News

2. Summary

Why We Like Limbach

Established in 1901, Limbach (NASDAQ: LMB) provides integrated building systems solutions, including mechanical, electrical, and plumbing services.

- Incremental sales over the last five years have been highly profitable as its earnings per share increased by 38% annually, topping its revenue gains

- Industry-leading 21.1% return on capital demonstrates management’s skill in finding high-return investments, and its returns are growing as it capitalizes on even better market opportunities

- Market share is on track to rise over the next 12 months as its 14.8% projected revenue growth implies demand will accelerate from its two-year trend

Limbach is a market leader. The price seems fair in light of its quality, so this could be a good time to invest in some shares.

Why Is Now The Time To Buy Limbach?

At $79.23 per share, Limbach trades at 17.6x forward P/E. This multiple is lower than most industrials companies, and we think the stock is a deal when considering its quality characteristics.

Entry price matters far less than business fundamentals if you’re investing for a multi-year period. But if you can get a bargain price it’s certainly icing on the cake.

3. Limbach (LMB) Research Report: Q4 CY2025 Update

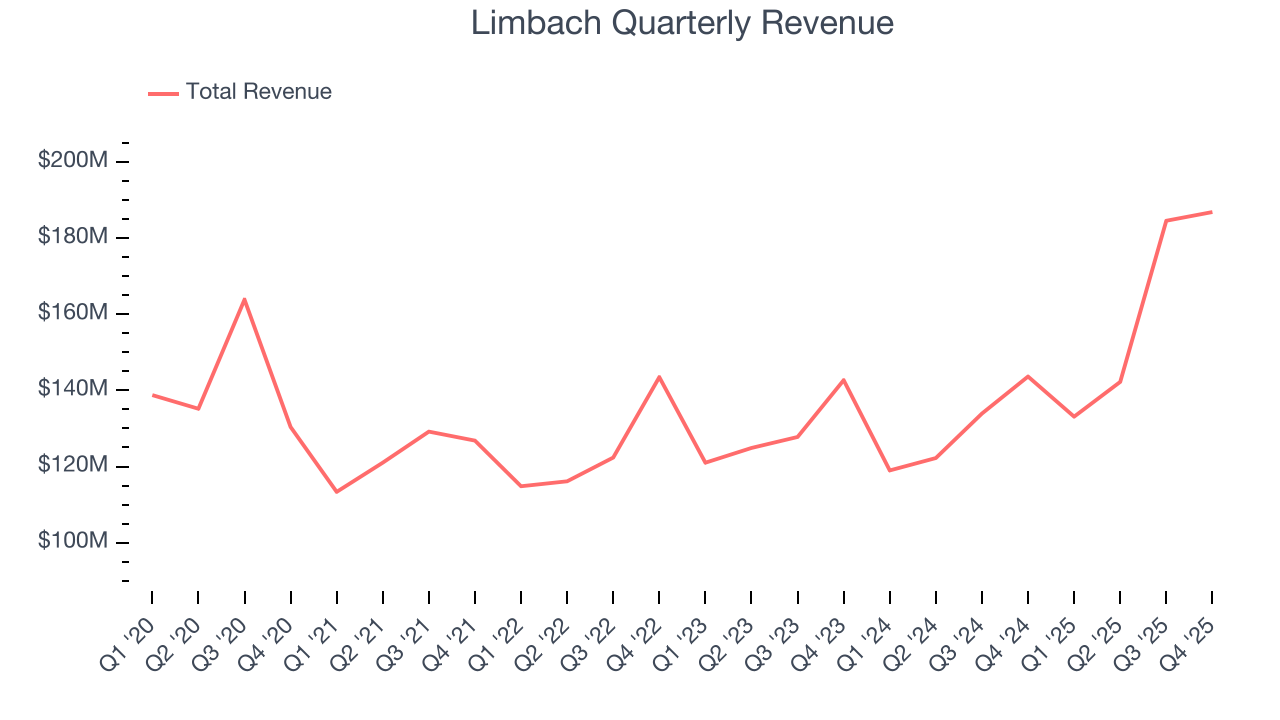

Building systems company Limbach (NASDAQ:LMB) fell short of the market’s revenue expectations in Q4 CY2025, but sales rose 30.1% year on year to $186.9 million. On the other hand, the company’s outlook for the full year was close to analysts’ estimates with revenue guided to $745 million at the midpoint. Its non-GAAP profit of $1.40 per share was 13.3% above analysts’ consensus estimates.

Limbach (LMB) Q4 CY2025 Highlights:

- Revenue: $186.9 million vs analyst estimates of $197.6 million (30.1% year-on-year growth, 5.4% miss)

- Adjusted EPS: $1.40 vs analyst estimates of $1.24 (13.3% beat)

- Adjusted EBITDA: $27.22 million vs analyst estimates of $26.57 million (14.6% margin, 2.4% beat)

- EBITDA guidance for the upcoming financial year 2026 is $92 million at the midpoint, below analyst estimates of $93.48 million

- Operating Margin: 9.4%, in line with the same quarter last year

- Free Cash Flow Margin: 14.9%, up from 12.5% in the same quarter last year

- Market Capitalization: $1.06 billion

Company Overview

Established in 1901, Limbach (NASDAQ: LMB) provides integrated building systems solutions, including mechanical, electrical, and plumbing services.

The company originally focused on architectural and roofing work for residential, industrial, and institutional clients, a foundation that set the stage for its expansion into more complex building services.

Today, Limbach offers building solutions encompassing mechanical, electrical, and plumbing systems, primarily targeting critical infrastructures in healthcare, industrial, data centers, and educational sectors. The company's services include the design, installation, and maintenance of HVAC systems, electrical setups, and plumbing frameworks. Limbach's projects are tailored to enhance the functionality and efficiency of buildings, addressing the specific needs of facilities like hospitals and universities where reliable infrastructure is crucial.

Limbach's revenue streams are diversified across new construction projects, renovations, and ongoing maintenance services, secured through General Contractor Relationships (GCR) and Owner Direct Relationships (ODR). The GCR category involves competitive bidding on projects where Limbach provides specialized construction services. In contrast, the ODR category focuses on direct engagements with building owners for maintenance and system upgrades, offering a steady source of recurring revenue.

4. Construction and Maintenance Services

Construction and maintenance services companies not only boast technical know-how in specialized areas but also may hold special licenses and permits. Those who work in more regulated areas can enjoy more predictable revenue streams - for example, fire escapes need to be inspected every five years. More recently, services to address energy efficiency and labor availability are also creating incremental demand. But like the broader industrials sector, construction and maintenance services companies are at the whim of economic cycles as external factors like interest rates can greatly impact the new construction that drives incremental demand for these companies’ offerings.

Competitors in the building services industry include Comfort Systems USA (NYSE:FIX), EMCOR Group (NYSE:EME), and Dycom Industries (NYSE:DY)

5. Revenue Growth

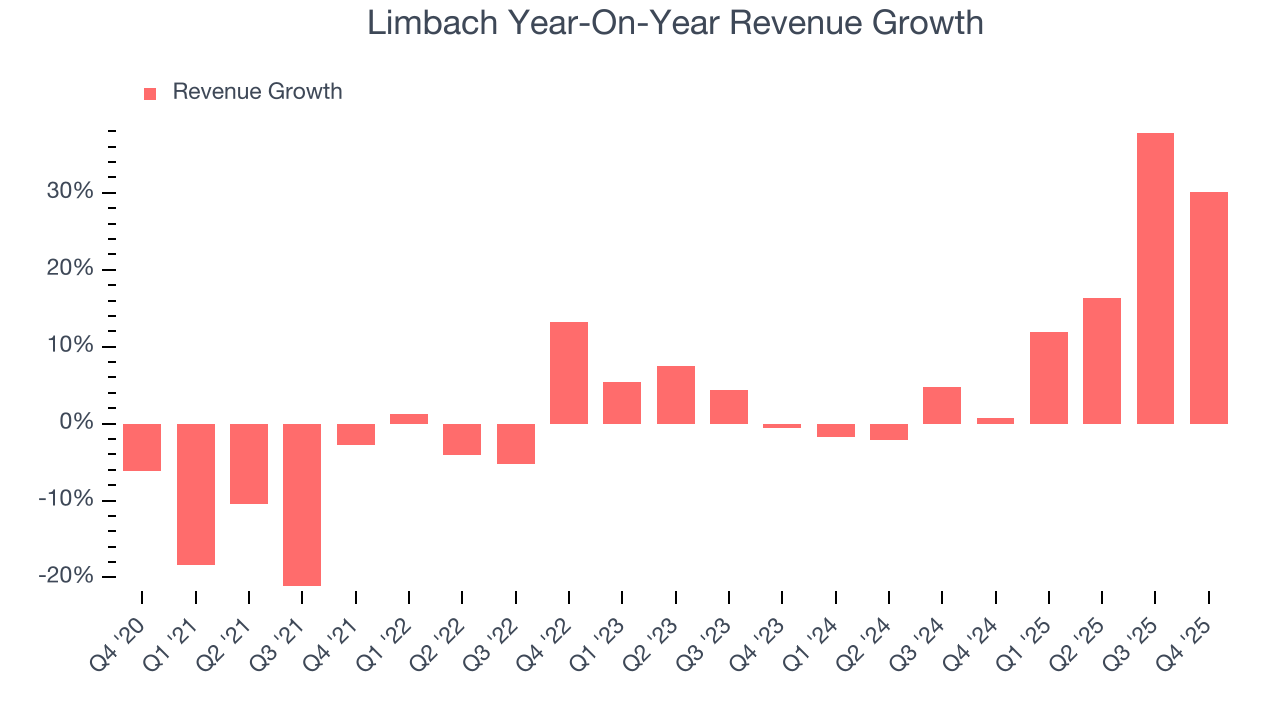

Reviewing a company’s long-term sales performance reveals insights into its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Over the last five years, Limbach grew its sales at a sluggish 2.6% compounded annual growth rate. This wasn’t a great result, but there are still things to like about Limbach.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Limbach’s annualized revenue growth of 11.9% over the last two years is above its five-year trend, suggesting its demand recently accelerated.

This quarter, Limbach pulled off a wonderful 30.1% year-on-year revenue growth rate, but its $186.9 million of revenue fell short of Wall Street’s rosy estimates.

Looking ahead, sell-side analysts expect revenue to grow 14.3% over the next 12 months, an improvement versus the last two years. This projection is commendable and suggests its newer products and services will spur better top-line performance.

6. Gross Margin & Pricing Power

Gross profit margin is a critical metric to track because it sheds light on its pricing power, complexity of products, and ability to procure raw materials, equipment, and labor.

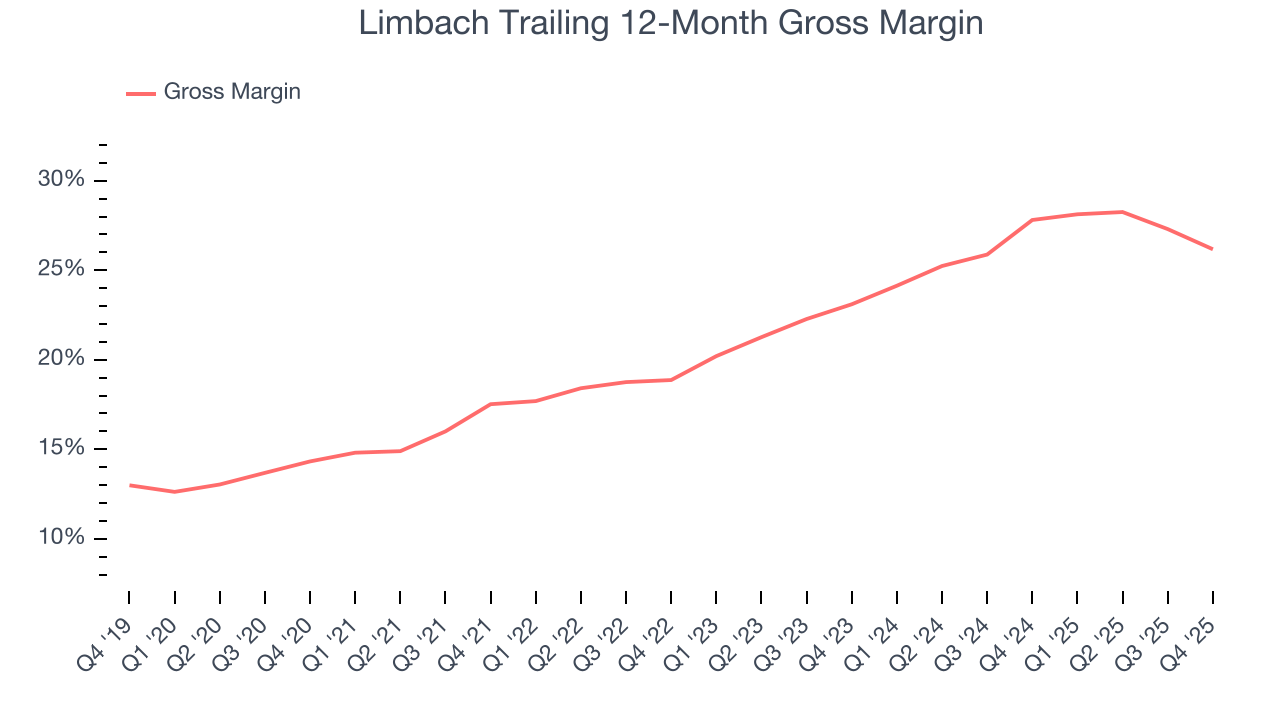

Limbach has bad unit economics for an industrials company, giving it less room to reinvest and develop new offerings. As you can see below, it averaged a 22.9% gross margin over the last five years. That means Limbach paid its suppliers a lot of money ($77.05 for every $100 in revenue) to run its business.

Limbach’s gross profit margin came in at 25.7% this quarter , marking a 4.6 percentage point decrease from 30.3% in the same quarter last year. Limbach’s full-year margin has also been trending down over the past 12 months, decreasing by 1.6 percentage points. If this move continues, it could suggest a more competitive environment with some pressure to lower prices and higher input costs (such as raw materials and manufacturing expenses).

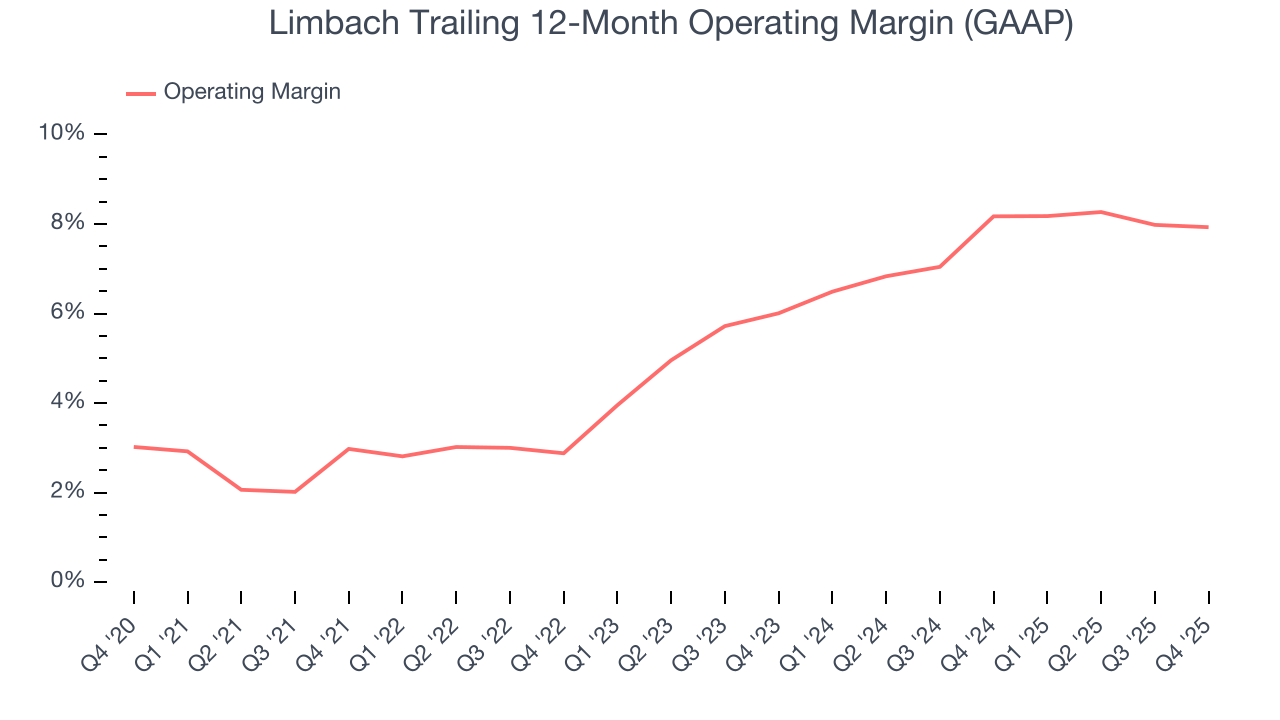

7. Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Limbach was profitable over the last five years but held back by its large cost base. Its average operating margin of 5.8% was weak for an industrials business. This result isn’t too surprising given its low gross margin as a starting point.

On the plus side, Limbach’s operating margin rose by 5 percentage points over the last five years, as its sales growth gave it operating leverage.

This quarter, Limbach generated an operating margin profit margin of 9.4%, in line with the same quarter last year. This indicates the company’s cost structure has recently been stable.

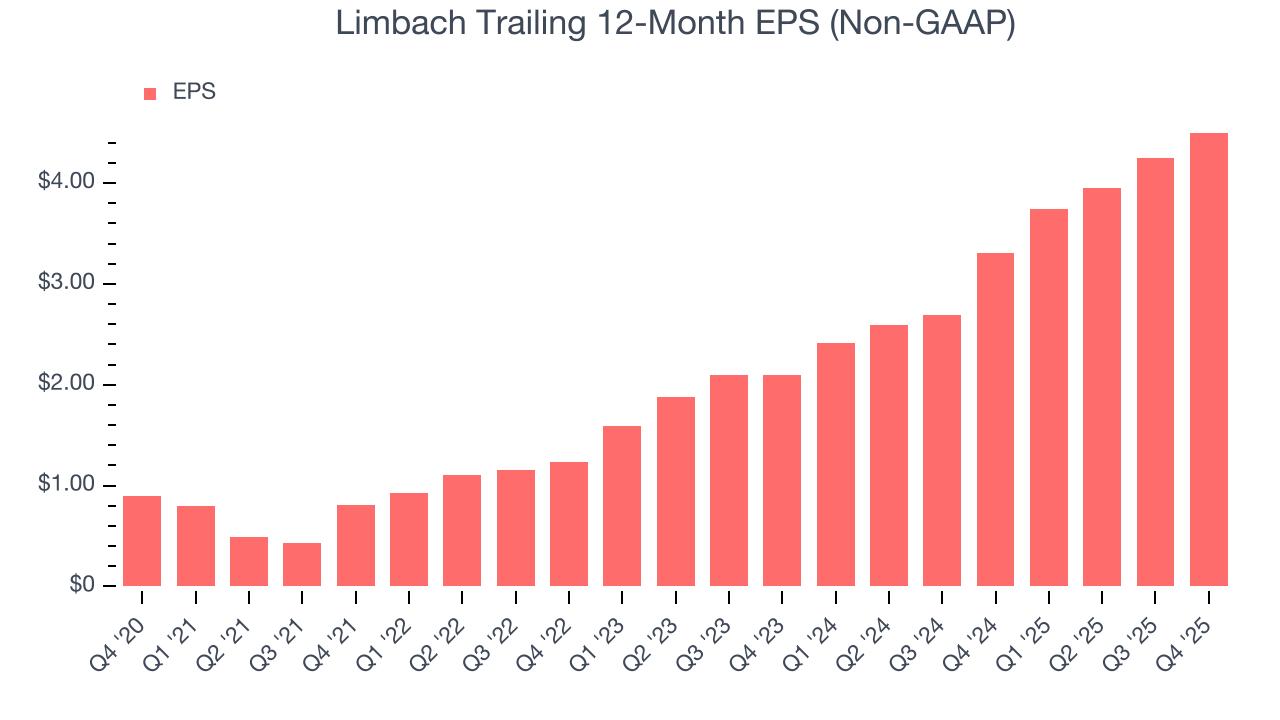

8. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Limbach’s EPS grew at an astounding 38% compounded annual growth rate over the last five years, higher than its 2.6% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

We can take a deeper look into Limbach’s earnings to better understand the drivers of its performance. As we mentioned earlier, Limbach’s operating margin was flat this quarter but expanded by 5 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its higher earnings; interest expenses and taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Limbach, its two-year annual EPS growth of 46.5% was higher than its five-year trend. We love it when earnings growth accelerates, especially when it accelerates off an already high base.

In Q4, Limbach reported adjusted EPS of $1.40, up from $1.15 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Limbach’s full-year EPS of $4.50 to shrink by 3.6%.

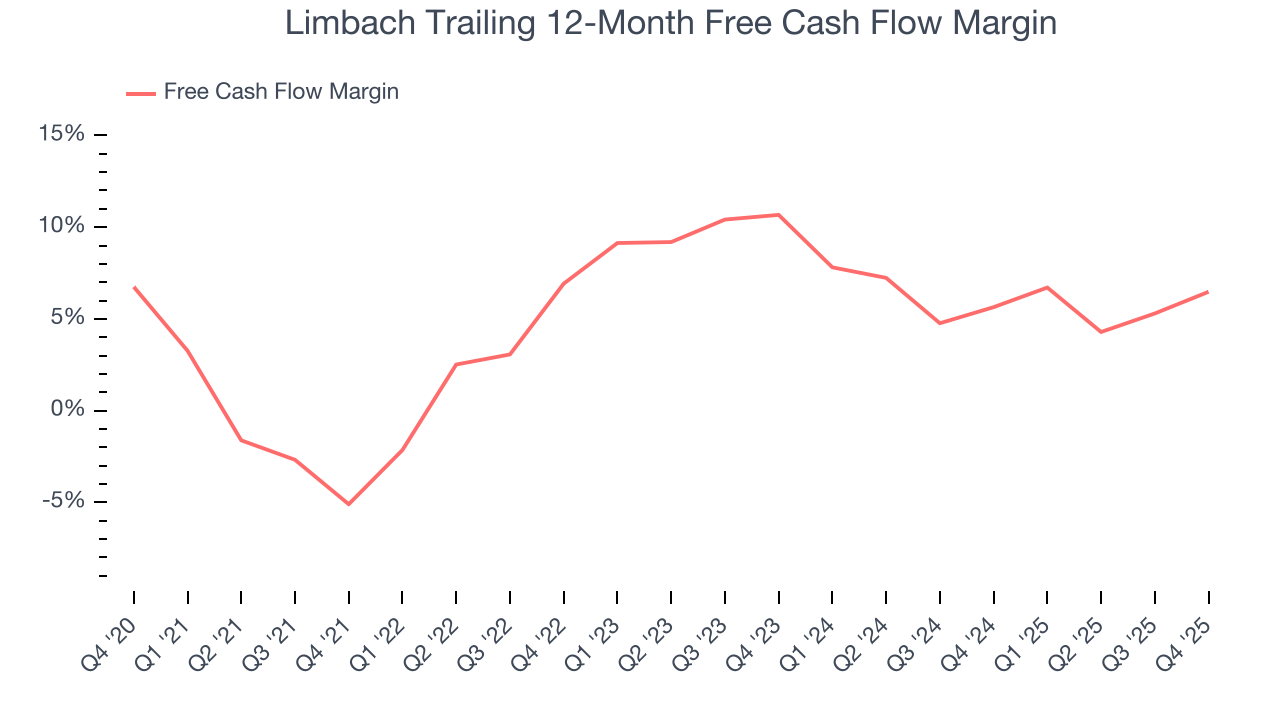

9. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Limbach has shown mediocre cash profitability over the last five years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 5.1%, subpar for an industrials business.

Taking a step back, an encouraging sign is that Limbach’s margin expanded by 11.6 percentage points during that time. The company’s improvement shows it’s heading in the right direction, and we can see it became a less capital-intensive business because its free cash flow profitability rose more than its operating profitability.

Limbach’s free cash flow clocked in at $27.88 million in Q4, equivalent to a 14.9% margin. This result was good as its margin was 2.4 percentage points higher than in the same quarter last year, building on its favorable historical trend.

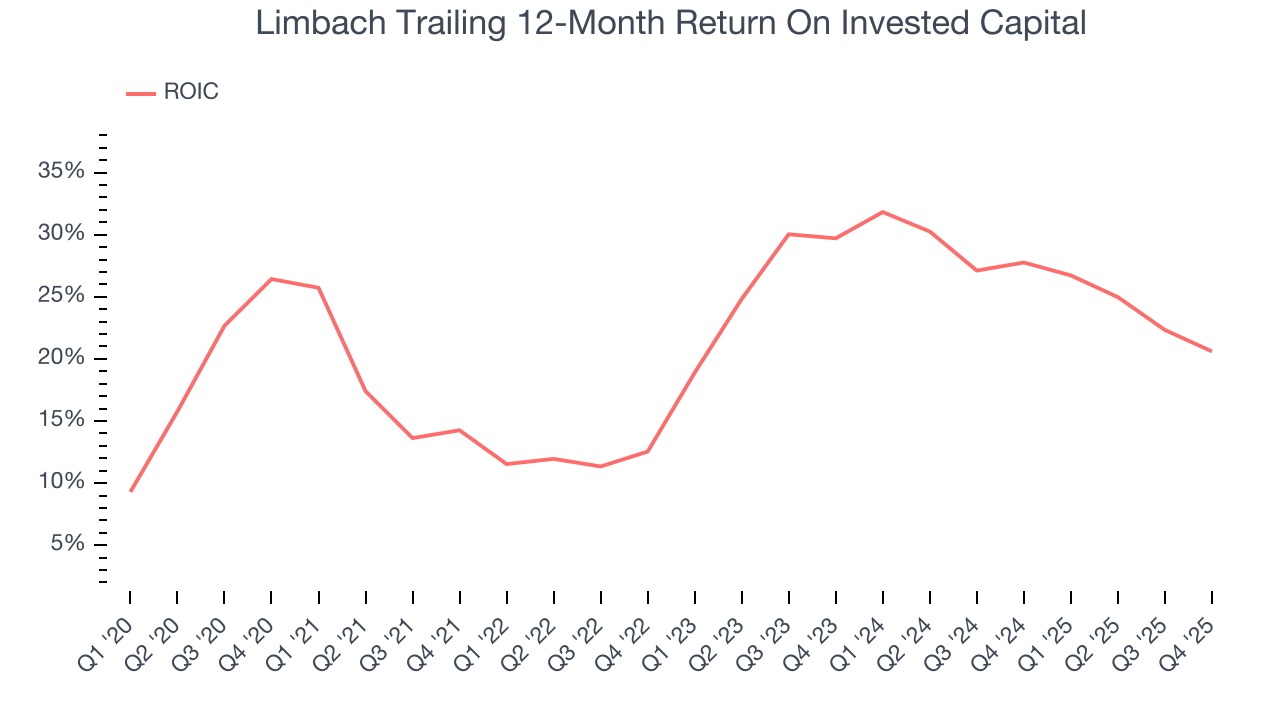

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Limbach’s five-year average ROIC was 21%, placing it among the best industrials companies. This illustrates its management team’s ability to invest in highly profitable ventures and produce tangible results for shareholders.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Fortunately, Limbach’s ROIC has increased significantly over the last few years. This is a great sign when paired with its already strong returns. It could suggest its competitive advantage or profitable growth opportunities are expanding.

11. Balance Sheet Assessment

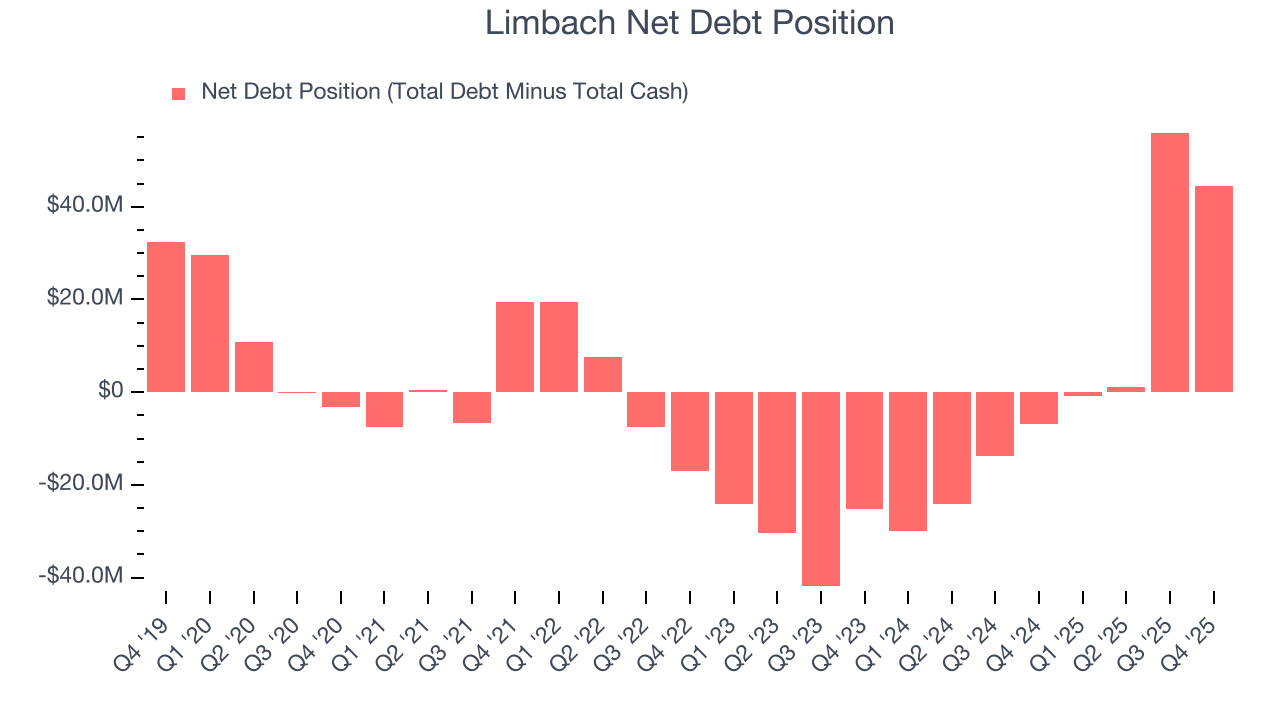

Limbach reported $11.41 million of cash and $55.87 million of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $81.8 million of EBITDA over the last 12 months, we view Limbach’s 0.5× net-debt-to-EBITDA ratio as safe. We also see its $897,000 of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

12. Key Takeaways from Limbach’s Q4 Results

It was good to see Limbach beat analysts’ EPS expectations this quarter. We were also happy its EBITDA outperformed Wall Street’s estimates. On the other hand, its revenue missed and its full-year EBITDA guidance fell short of Wall Street’s estimates. Overall, this quarter could have been better. The stock traded down 5% to $85.05 immediately following the results.

13. Is Now The Time To Buy Limbach?

Updated: March 15, 2026 at 11:48 PM EDT

When considering an investment in Limbach, investors should account for its valuation and business qualities as well as what’s happened in the latest quarter.

Limbach is an amazing business ranking highly on our list. Although its revenue growth was weak over the last five years, its growth over the next 12 months is expected to be higher. And while its projected EPS for the next year is lacking, its rising cash profitability gives it more optionality. In addition, Limbach’s astounding EPS growth over the last five years shows its profits are trickling down to shareholders.

Limbach’s P/E ratio based on the next 12 months is 17.6x. Looking at the industrials landscape today, Limbach’s fundamentals really stand out, and we like it at this price.

Wall Street analysts have a consensus one-year price target of $118.60 on the company (compared to the current share price of $79.23), implying they see 49.7% upside in buying Limbach in the short term.