Lovesac (LOVE)

Lovesac is in for a bumpy ride. Its weak sales growth and low returns on capital show it struggled to generate demand and profits.― StockStory Analyst Team

1. News

2. Summary

Why We Think Lovesac Will Underperform

Known for its oversized, premium beanbags, Lovesac (NASDAQ:LOVE) is a specialty furniture brand selling modular furniture.

- Muted 19.5% annual revenue growth over the last five years shows its demand lagged behind its consumer discretionary peers

- Subpar operating margin constrains its ability to invest in process improvements or effectively respond to new competitive threats

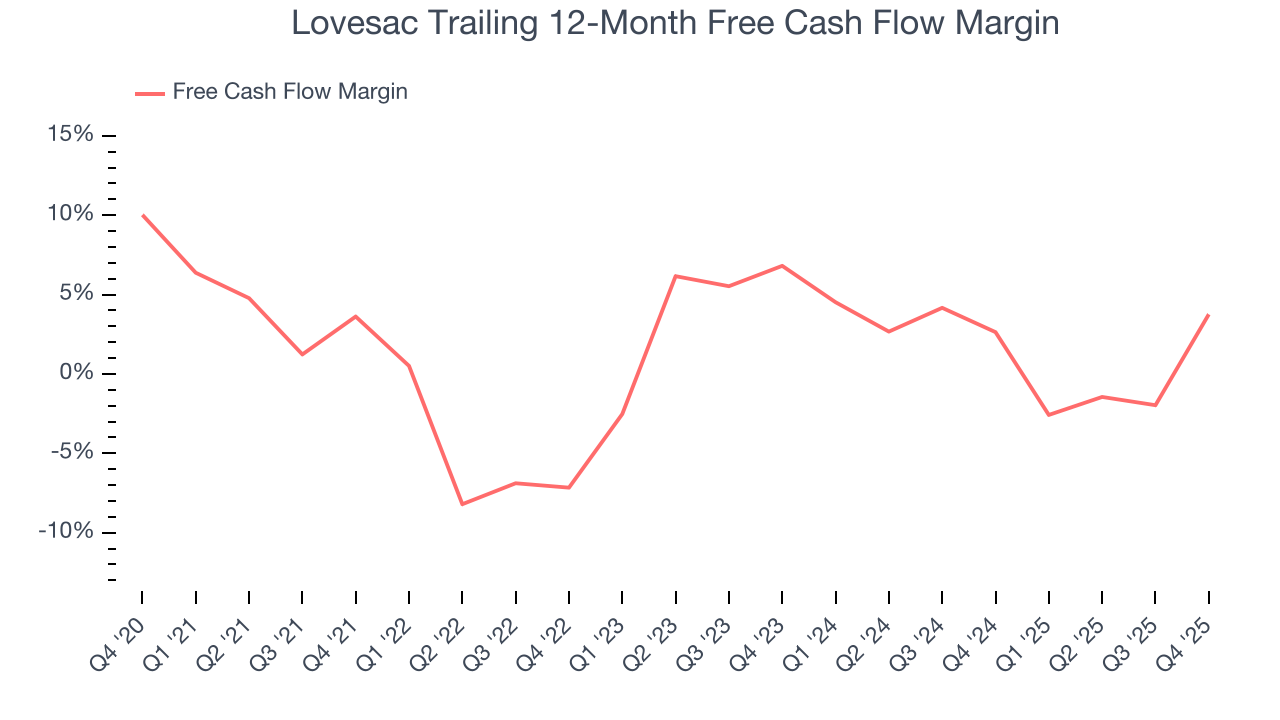

- Ability to fund investments or reward shareholders with increased buybacks or dividends is restricted by its weak free cash flow margin of 1.1% for the last two years

Lovesac doesn’t meet our quality standards. More profitable opportunities exist elsewhere.

Why There Are Better Opportunities Than Lovesac

Lovesac is trading at $11.58 per share, or 9.6x forward EV-to-EBITDA. The current valuation may be fair, but we’re still passing on this stock due to better alternatives out there.

We’d rather pay a premium for quality. Cheap stocks can look like a great deal at first glance, but they can be value traps. Less earnings power means more reliance on a re-rating to generate good returns; this can be an unlikely scenario for low-quality companies.

3. Lovesac (LOVE) Research Report: Q4 CY2025 Update

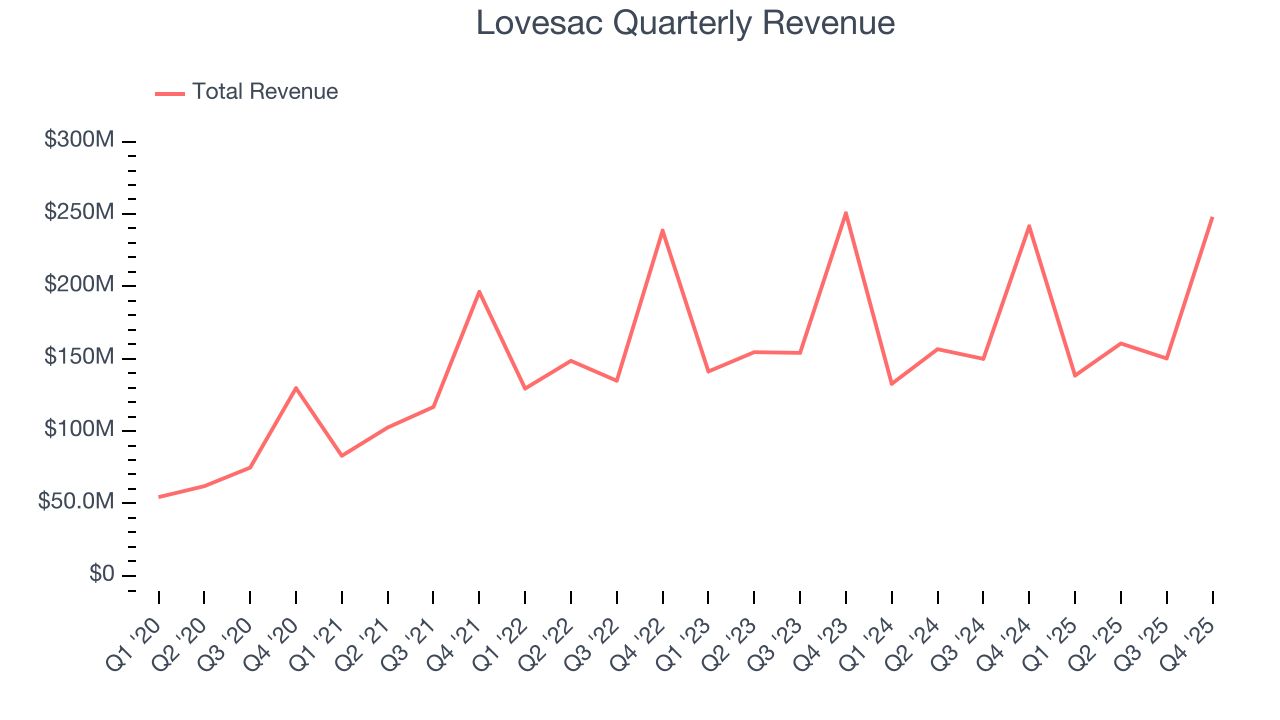

Furniture company Lovesac (NASDAQ:LOVE) beat Wall Street’s revenue expectations in Q4 CY2025, with sales up 2.7% year on year to $248 million. On the other hand, next quarter’s revenue guidance of $136 million was less impressive, coming in 5.5% below analysts’ estimates. Its GAAP profit of $2.19 per share was 7.2% above analysts’ consensus estimates.

Lovesac (LOVE) Q4 CY2025 Highlights:

- Revenue: $248 million vs analyst estimates of $242 million (2.7% year-on-year growth, 2.5% beat)

- EPS (GAAP): $2.19 vs analyst estimates of $2.04 (7.2% beat)

- Adjusted EBITDA: $49.65 million vs analyst estimates of $51.92 million (20% margin, 4.4% miss)

- Revenue Guidance for Q1 CY2026 is $136 million at the midpoint, below analyst estimates of $144 million

- EPS (GAAP) guidance for the upcoming financial year 2027 is $0.65 at the midpoint, missing analyst estimates by 19.2%

- EBITDA guidance for the upcoming financial year 2027 is $38.5 million at the midpoint, below analyst estimates of $43.56 million

- Operating Margin: 18.1%, down from 19.7% in the same quarter last year

- Free Cash Flow Margin: 31.6%, up from 16% in the same quarter last year

- Market Capitalization: $165 million

Company Overview

Known for its oversized, premium beanbags, Lovesac (NASDAQ:LOVE) is a specialty furniture brand selling modular furniture.

The company started with its signature product, the "Lovesac", which is a large and durable beanbag chair. It has since expanded to offer a unique line of modular sectional couches known as Sactionals.

Lovesac's Sactionals are a distinctive product in the furniture market, offering adaptability and customization. These modular couches have sections that can be combined in various configurations to fit any room size or shape, making them a practical choice for diverse living spaces. The Sactionals' design is user-friendly, allowing for easy assembly, reconfiguration, and expansion.

Lovasac products are quite expensive: its beanbags can cost $800 and some Sactionals are upwards of $10,000. As such, the company's products appeal to customers who like experimenting with their furniture and are willing to pay up for home decor.

4. Consumer Discretionary - Home Furnishings

The Consumer Discretionary sector, by definition, is made up of companies selling non-essential goods and services. When economic conditions deteriorate or tastes shift, consumers can easily cut back or eliminate these purchases. For long-term investors with five-year holding periods, this creates a structural challenge: the sector is inherently hit-driven, with low switching costs and fickle customers. As a result, only a handful of companies can reliably grow demand and compound earnings over long periods, which is why our bar is high and High Quality ratings are rare.

Home furnishings companies design, manufacture, and sell furniture, décor, bedding, and related household products for residential and commercial spaces. Tailwinds include e-commerce expansion enabling broader distribution, continued remote-work trends sustaining home improvement interest, and premiumization as consumers invest in living spaces. However, headwinds are considerable: demand is closely tied to housing market activity, and rising mortgage rates have slowed home sales—a key purchase trigger. Bulky products carry high shipping costs and complex logistics. Intense competition from low-cost imports and mass-market retailers compresses margins, while consumer spending on furnishings is among the first categories deferred during economic downturns.

Lovesac’s primary competitors include La-Z-Boy (NYSE:LZB), Wayfair (NYSE:W), West Elm (owned by Williams-Sonoma NYSE:WSM), and private companies IKEA and Ashley Furniture

5. Revenue Growth

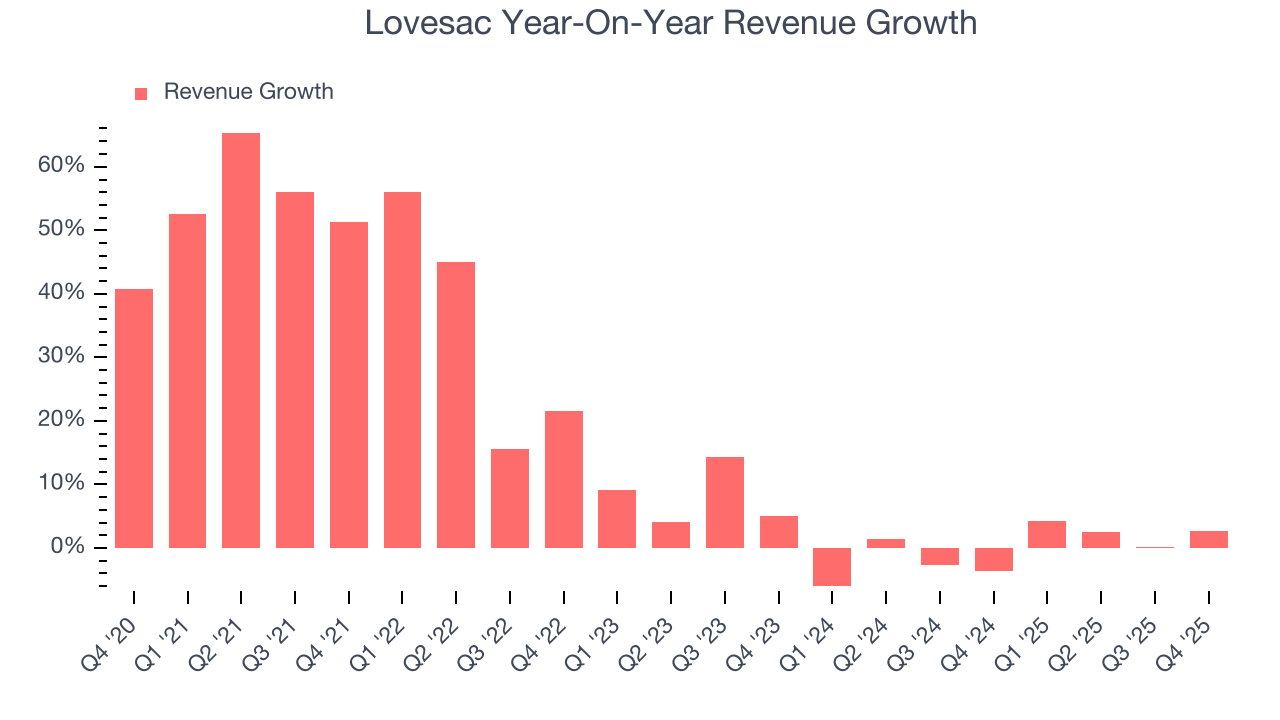

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last five years, Lovesac grew its sales at a 16.8% annual rate. Though this growth is acceptable on an absolute basis, we need to see more than just topline growth for the consumer discretionary sector, which can display significant earnings volatility. This means our bar for the sector is particularly high, reflecting the non-essential and hit-driven nature of the products and services offered. Additionally, five-year CAGR starts around Covid, when revenue was depressed then rebounded.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new product or trend. Lovesac’s recent performance shows its demand has slowed as its revenue was flat over the last two years.

This quarter, Lovesac reported modest year-on-year revenue growth of 2.7% but beat Wall Street’s estimates by 2.5%. Company management is currently guiding for a 1.7% year-on-year decline in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 4.9% over the next 12 months. Although this projection indicates its newer products and services will fuel better top-line performance, it is still below the sector average.

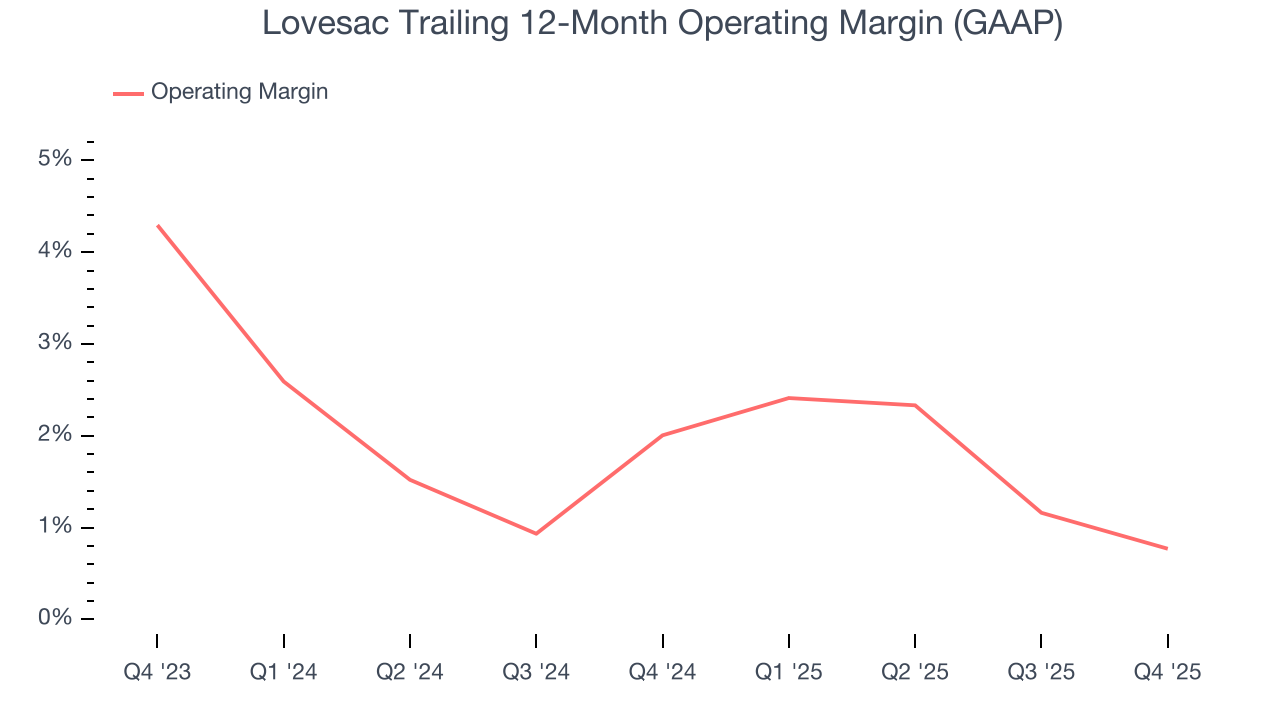

6. Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Lovesac’s operating margin has shrunk over the last 12 months and averaged 1.4% over the last two years. The company’s profitability was mediocre for a consumer discretionary business and shows it couldn’t pass its higher operating expenses onto its customers.

This quarter, Lovesac generated an operating margin profit margin of 18.1%, down 1.6 percentage points year on year. This reduction is quite minuscule and indicates the company’s overall cost structure has been relatively stable.

7. Earnings Per Share

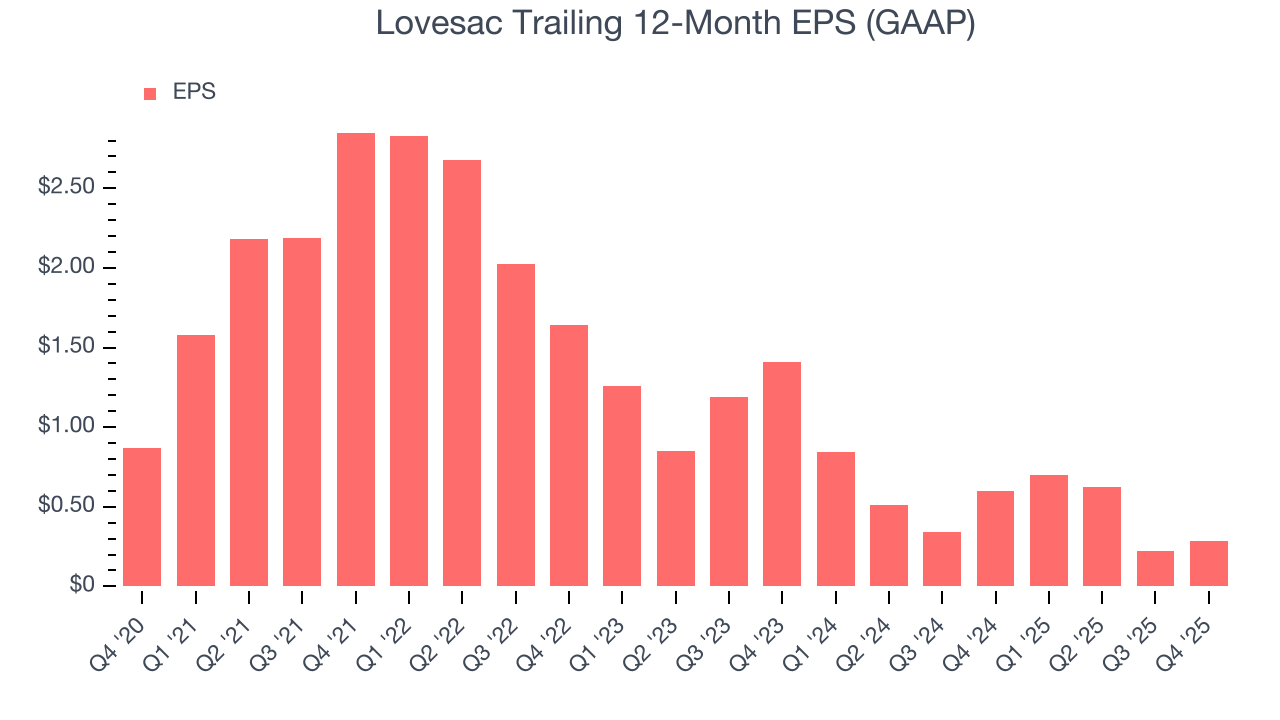

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Sadly for Lovesac, its EPS declined by 20.1% annually over the last five years while its revenue grew by 16.8%. We can see the difference stemmed from higher interest expenses or taxes as the company actually improved its operating margin and repurchased its shares during this time.

In Q4, Lovesac reported EPS of $2.19, up from $2.13 in the same quarter last year. This print beat analysts’ estimates by 7.2%. Over the next 12 months, Wall Street expects Lovesac’s full-year EPS of $0.28 to grow 84.1%.

8. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Lovesac has shown poor cash profitability relative to peers over the last two years, giving the company fewer opportunities to return capital to shareholders. Its free cash flow margin averaged 3.2%, below what we’d expect for a consumer discretionary business.

Lovesac’s free cash flow clocked in at $78.5 million in Q4, equivalent to a 31.6% margin. This result was good as its margin was 15.6 percentage points higher than in the same quarter last year, but we wouldn’t read too much into the short term because investment needs can be seasonal, causing temporary swings. Long-term trends trump fluctuations.

Over the next year, analysts predict Lovesac’s cash conversion will slightly fall. Their consensus estimates imply its free cash flow margin of 3.8% for the last 12 months will decrease to 2.1%.

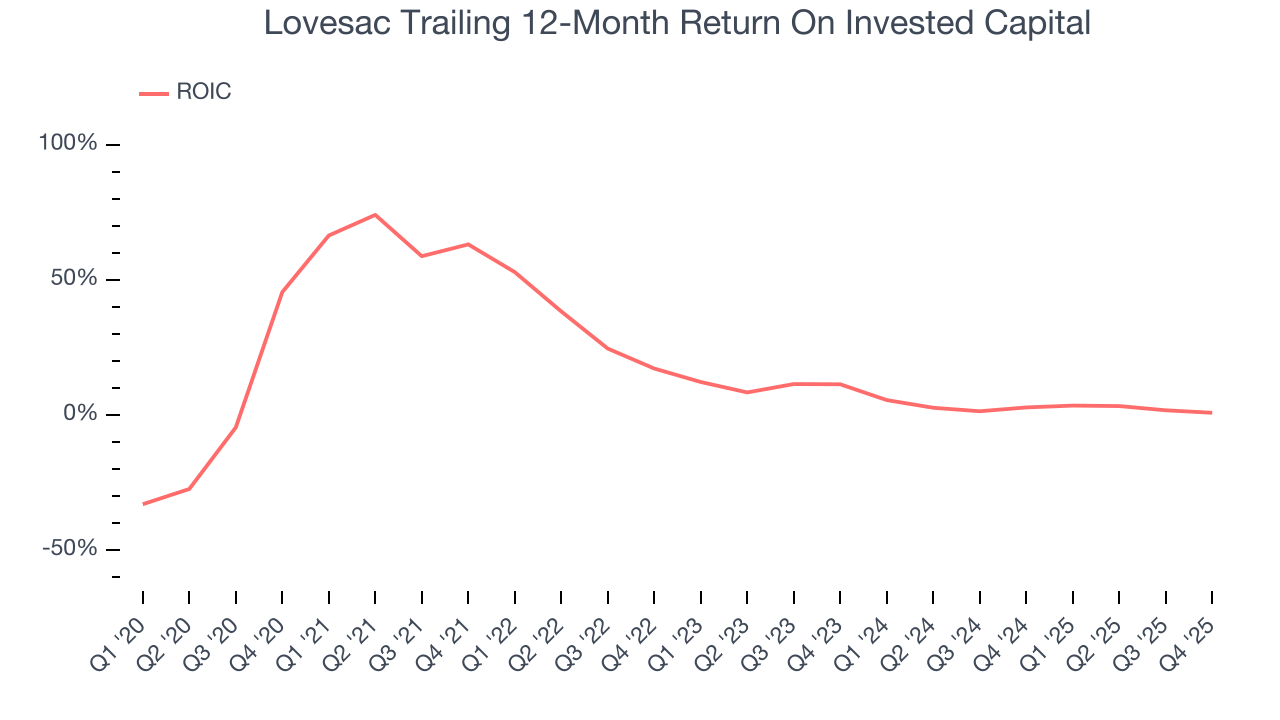

9. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Lovesac historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 19%, somewhat low compared to the best consumer discretionary companies that consistently pump out 25%+.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Over the last few years, Lovesac’s ROIC has unfortunately decreased significantly. Paired with its already low returns, these declines suggest its profitable growth opportunities are few and far between.

10. Balance Sheet Assessment

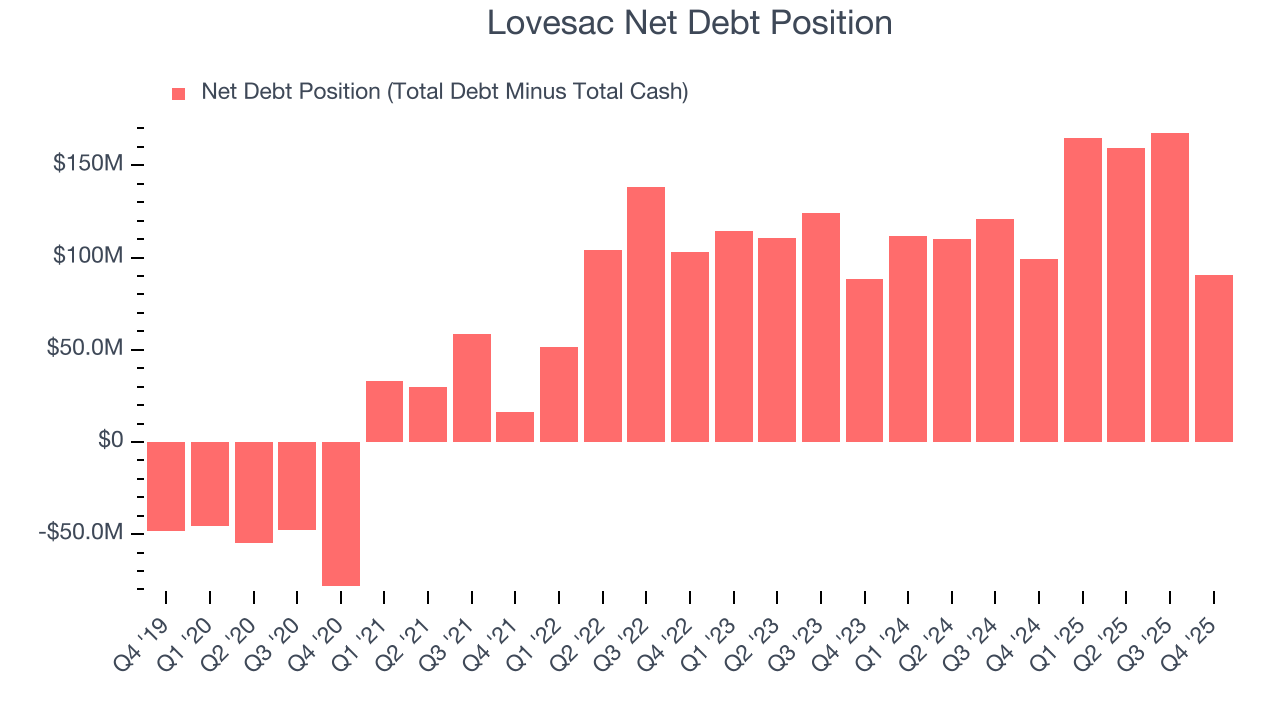

Lovesac reported $101.9 million of cash and $192.5 million of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $36.07 million of EBITDA over the last 12 months, we view Lovesac’s 2.5× net-debt-to-EBITDA ratio as safe. We also see its $1.30 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

11. Key Takeaways from Lovesac’s Q4 Results

We were impressed by Lovesac’s optimistic EBITDA guidance for next quarter, which blew past analysts’ expectations. We were also happy its revenue outperformed Wall Street’s estimates. On the other hand, its full-year EBITDA guidance missed and its revenue guidance for next quarter fell short of Wall Street’s estimates. Overall, this was a mixed quarter, but it seems like expectations were low and a relief rally is ensuing. The stock traded up 18.8% to $13.16 immediately following the results.

12. Is Now The Time To Buy Lovesac?

Updated: March 26, 2026 at 11:23 PM EDT

When considering an investment in Lovesac, investors should account for its valuation and business qualities as well as what’s happened in the latest quarter.

Lovesac doesn’t pass our quality test. While its projected EPS for the next year implies the company’s fundamentals will improve, the downside is its declining EPS over the last five years makes it a less attractive asset to the public markets. On top of that, its relatively low ROIC suggests management has struggled to find compelling investment opportunities.

Lovesac’s EV-to-EBITDA ratio based on the next 12 months is 6.9x. This valuation multiple is fair, but we don’t have much confidence in the company. There are more exciting stocks to buy at the moment.

Wall Street analysts have a consensus one-year price target of $25.17 on the company (compared to the current share price of $13.88).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.