Magnite (MGNI)

We admire Magnite. Its revenue is growing quickly while its profitability is rising, giving it multiple ways to win.― StockStory Analyst Team

1. News

2. Summary

Why We Like Magnite

Born from the 2020 merger of Rubicon Project and Telaria, Magnite (NASDAQ:MGNI) operates the world's largest independent sell-side advertising platform that automates the buying and selling of digital advertising inventory across all channels and formats.

- Market share has increased this cycle as its 26.4% annual revenue growth over the last five years was exceptional

- Earnings growth has massively outpaced its peers over the last five years as its EPS has compounded at 57.1% annually

- Projected revenue growth of 15.1% for the next 12 months is above its two-year trend, pointing to accelerating demand

We see a bright future for Magnite. The valuation looks reasonable in light of its quality, so this could be a good time to buy some shares.

Why Is Now The Time To Buy Magnite?

Magnite’s stock price of $12.13 implies a valuation ratio of 11x forward P/E. Valuation is lower than most companies in the business services space, and we believe Magnite is attractively-priced for its quality.

Our analysis and backtests consistently tell us that buying high-quality companies and holding them for many years leads to market outperformance. Entry price matters less, but if you can get a good one, all the better.

3. Magnite (MGNI) Research Report: Q4 CY2025 Update

Digital advertising platform Magnite (NASDAQ:MGNI) missed Wall Street’s revenue expectations in Q4 CY2025, but sales rose 5.9% year on year to $205.4 million. Its non-GAAP profit of $0.34 per share was 3.9% below analysts’ consensus estimates.

Magnite (MGNI) Q4 CY2025 Highlights:

- Revenue: $205.4 million vs analyst estimates of $211.2 million (5.9% year-on-year growth, 2.8% miss)

- Adjusted EPS: $0.34 vs analyst expectations of $0.35 (3.9% miss)

- Adjusted EBITDA: $52.93 million vs analyst estimates of $80.88 million (25.8% margin, 34.6% miss)

- Operating Margin: 25.3%, up from 20.7% in the same quarter last year

- Free Cash Flow Margin: 50.2%, down from 57.2% in the same quarter last year

- Market Capitalization: $1.68 billion

Company Overview

Born from the 2020 merger of Rubicon Project and Telaria, Magnite (NASDAQ:MGNI) operates the world's largest independent sell-side advertising platform that automates the buying and selling of digital advertising inventory across all channels and formats.

Magnite's technology serves as the crucial intermediary between publishers (sellers of advertising space) and advertisers (buyers of that space) in the complex digital advertising ecosystem. The company's platform processes trillions of ad requests monthly, providing publishers with tools to maximize the value of their advertising inventory while giving advertisers access to premium digital content across websites, mobile apps, and connected TV (CTV).

CTV has become a strategic focus for Magnite following its acquisitions of SpotX and SpringServe in 2021, which significantly expanded its capabilities in streaming television advertising. These acquisitions positioned Magnite as the largest independent CTV advertising marketplace, enabling streaming content providers and broadcasters to monetize their programming through programmatic advertising.

For publishers, Magnite offers sophisticated yield management tools that help optimize revenue from their digital properties. A streaming platform might use Magnite's technology to automatically fill commercial breaks with relevant ads while maintaining viewing experience quality through features like frequency capping (preventing the same ad from appearing too often) and competitive separation (ensuring competing brands don't appear in the same ad break).

Advertisers and media buyers use Magnite's platform to reach specific audiences across thousands of publishers in a brand-safe environment. For example, an automotive company looking to promote a new vehicle might use Magnite to programmatically purchase ad space across premium CTV content that reaches their target demographic of affluent professionals.

Magnite generates revenue primarily through taking a percentage of the advertising transactions facilitated through its platform. The company operates globally with established presence in North America, Europe, and Australia, and developing operations in Asia and South America.

4. Advertising & Marketing Services

The sector is on the precipice of both disruption and growth as AI, programmatic advertising, and data-driven marketing reshape how things are done. For example, the advent of the Internet broadly and programmatic advertising specifically means that brand building is not a relationship business anymore but instead one based on data and technology, which could hurt traditional ad agencies. On the other hand, the companies in the sector that beef up their tech chops by automating the buying of ad inventory or facilitating omnichannel marketing, for example, stand to benefit. With or without advances in digitization and AI, the sector is still highly levered to the macro, and economic uncertainty may lead to fluctuating ad spend, particularly in cyclical industries.

Magnite competes with large tech companies that have their own advertising inventory and technology, including Google (NASDAQ: GOOGL), Meta (NASDAQ: META), and Amazon (NASDAQ: AMZN). In the sell-side platform space, its competitors include PubMatic (NASDAQ: PUBM), The Trade Desk (NASDAQ: TTD), and privately-held companies like Index Exchange and OpenX.

5. Revenue Growth

A company’s long-term performance is an indicator of its overall quality. Any business can have short-term success, but a top-tier one grows for years.

With $714 million in revenue over the past 12 months, Magnite is a small player in the business services space, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and numerous distribution channels. On the bright side, it can grow faster because it has more room to expand.

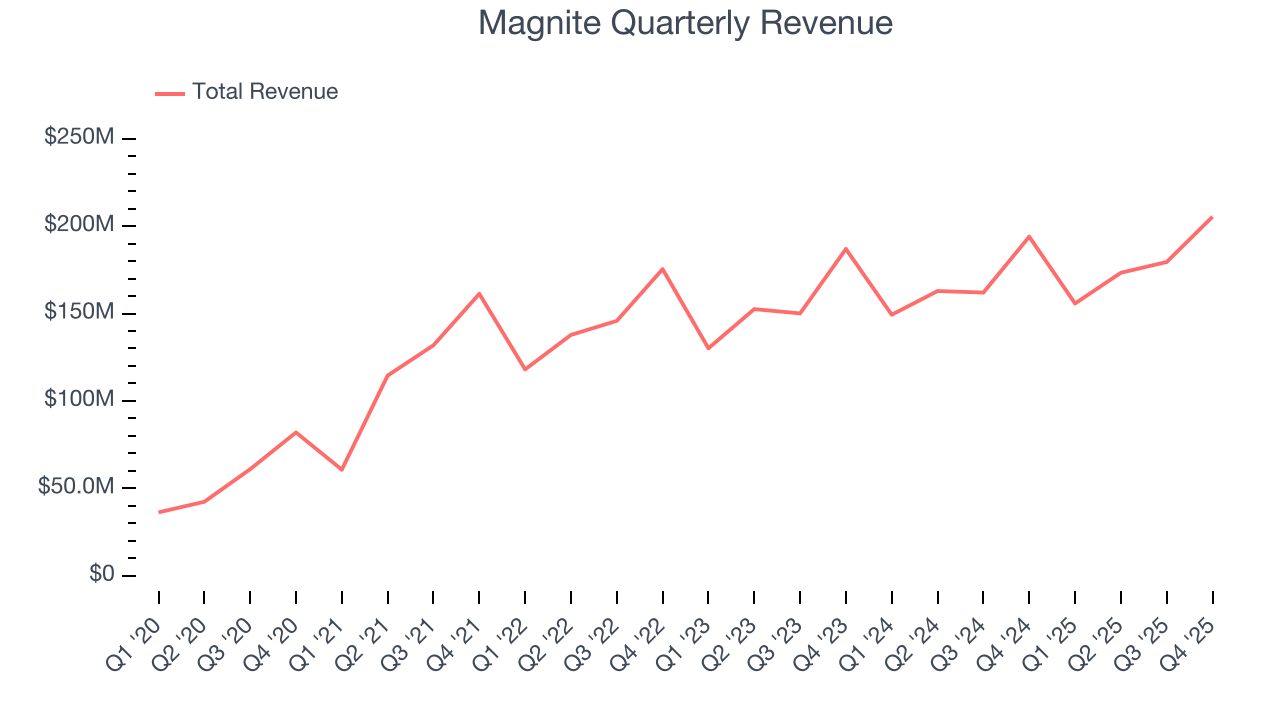

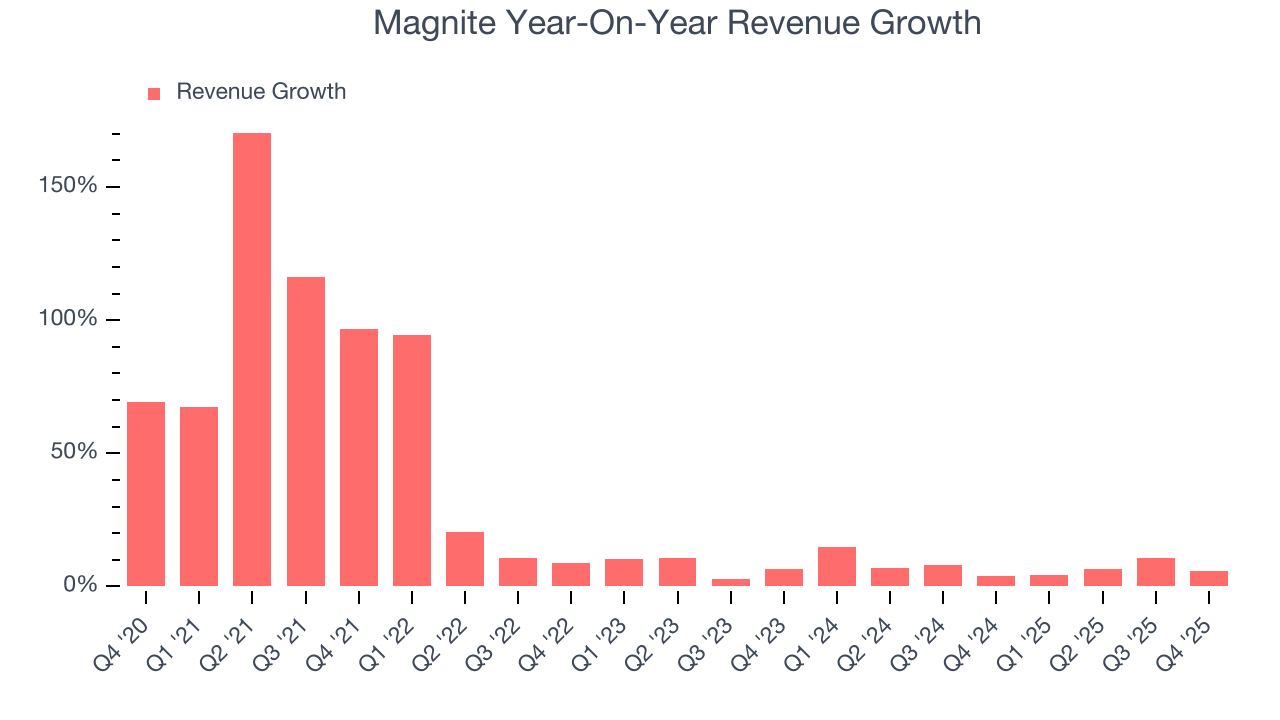

As you can see below, Magnite’s sales grew at an incredible 26.4% compounded annual growth rate over the last five years. This is a great starting point for our analysis because it shows Magnite’s demand was higher than many business services companies.

Long-term growth is the most important, but within business services, a half-decade historical view may miss new innovations or demand cycles. Magnite’s annualized revenue growth of 7.3% over the last two years is below its five-year trend, but we still think the results suggest healthy demand.

This quarter, Magnite’s revenue grew by 5.9% year on year to $205.4 million, missing Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 14.3% over the next 12 months, an improvement versus the last two years. This projection is commendable and implies its newer products and services will catalyze better top-line performance.

6. Operating Margin

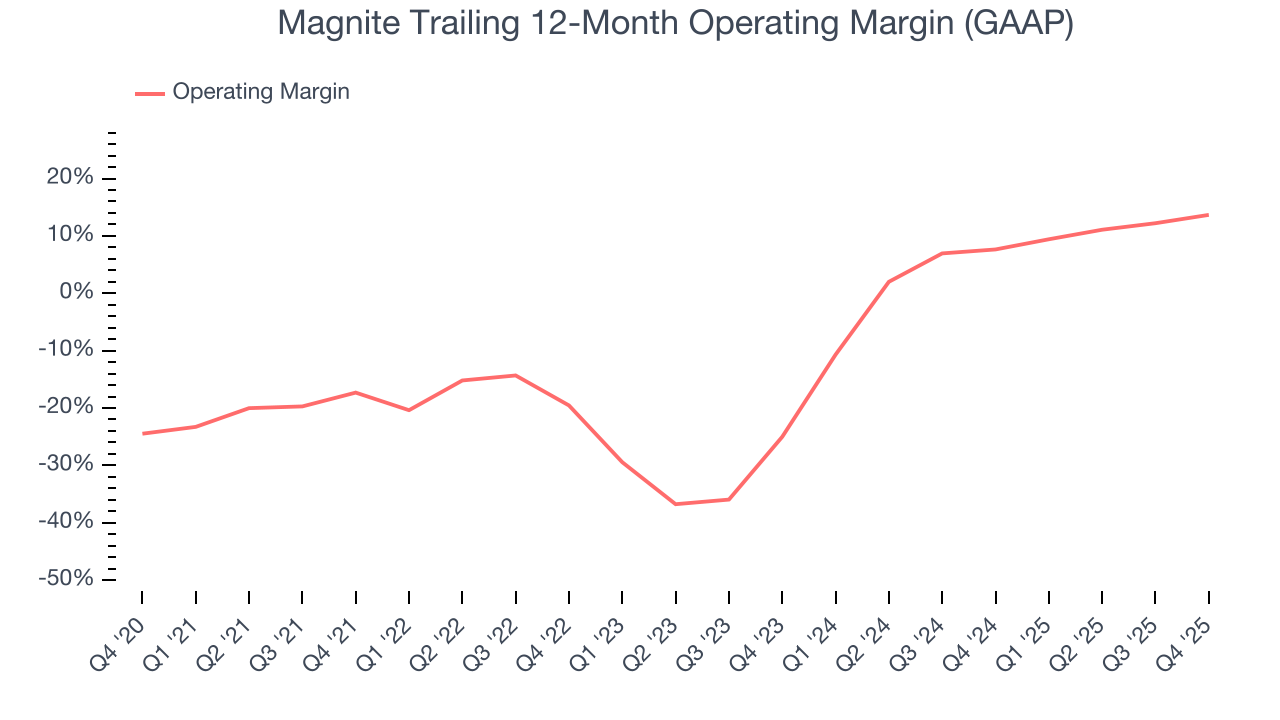

Although Magnite was profitable this quarter from an operational perspective, it’s generally struggled over a longer time period. Its expensive cost structure has contributed to an average operating margin of negative 6.6% over the last five years. Unprofitable business services companies require extra attention because they could get caught swimming naked when the tide goes out.

On the plus side, Magnite’s operating margin rose by 31 percentage points over the last five years, as its sales growth gave it operating leverage. Still, it will take much more for the company to show consistent profitability.

This quarter, Magnite generated an operating margin profit margin of 25.3%, up 4.6 percentage points year on year. This increase was a welcome development and shows it was more efficient.

7. Earnings Per Share

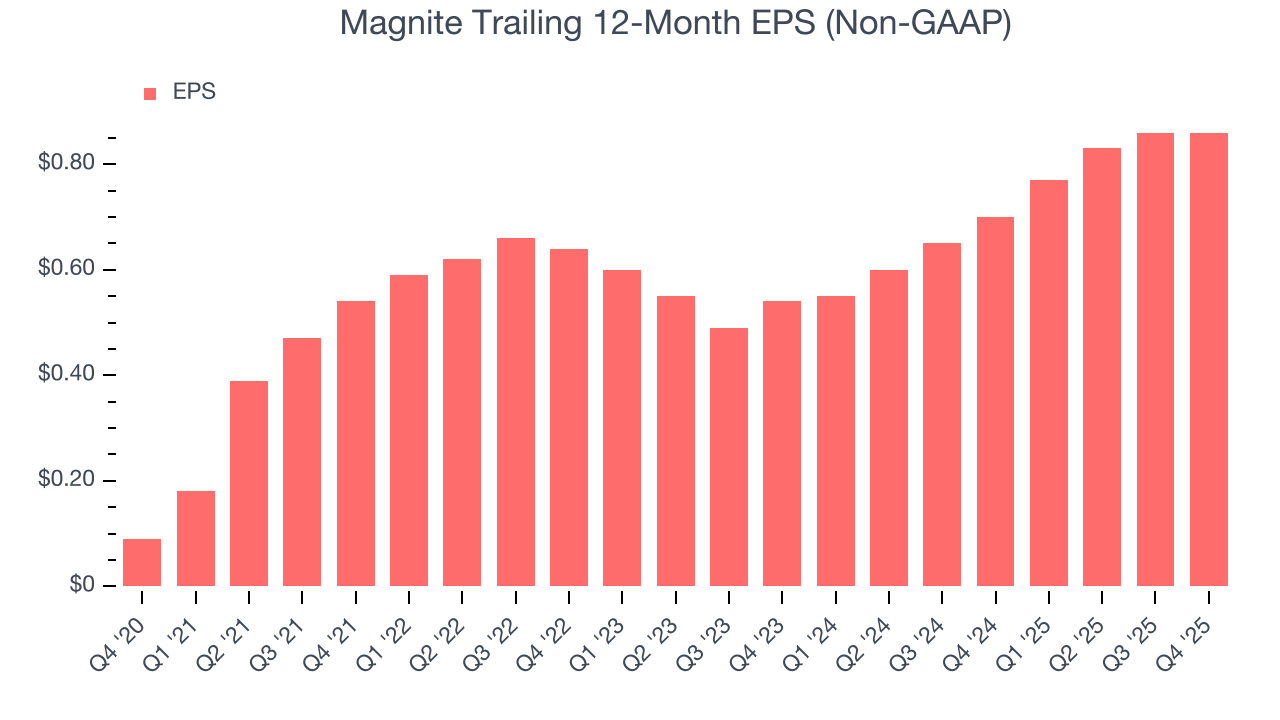

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Magnite’s EPS grew at an astounding 57.1% compounded annual growth rate over the last five years, higher than its 26.4% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

We can take a deeper look into Magnite’s earnings quality to better understand the drivers of its performance. As we mentioned earlier, Magnite’s operating margin expanded by 31 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its higher earnings; interest expenses and taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Magnite, its two-year annual EPS growth of 26.2% was lower than its five-year trend. We still think its growth was good and hope it can accelerate in the future.

In Q4, Magnite reported adjusted EPS of $0.34, in line with the same quarter last year. This print missed analysts’ estimates, but we care more about long-term adjusted EPS growth than short-term movements. Over the next 12 months, Wall Street expects Magnite’s full-year EPS of $0.86 to grow 28.3%.

8. Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

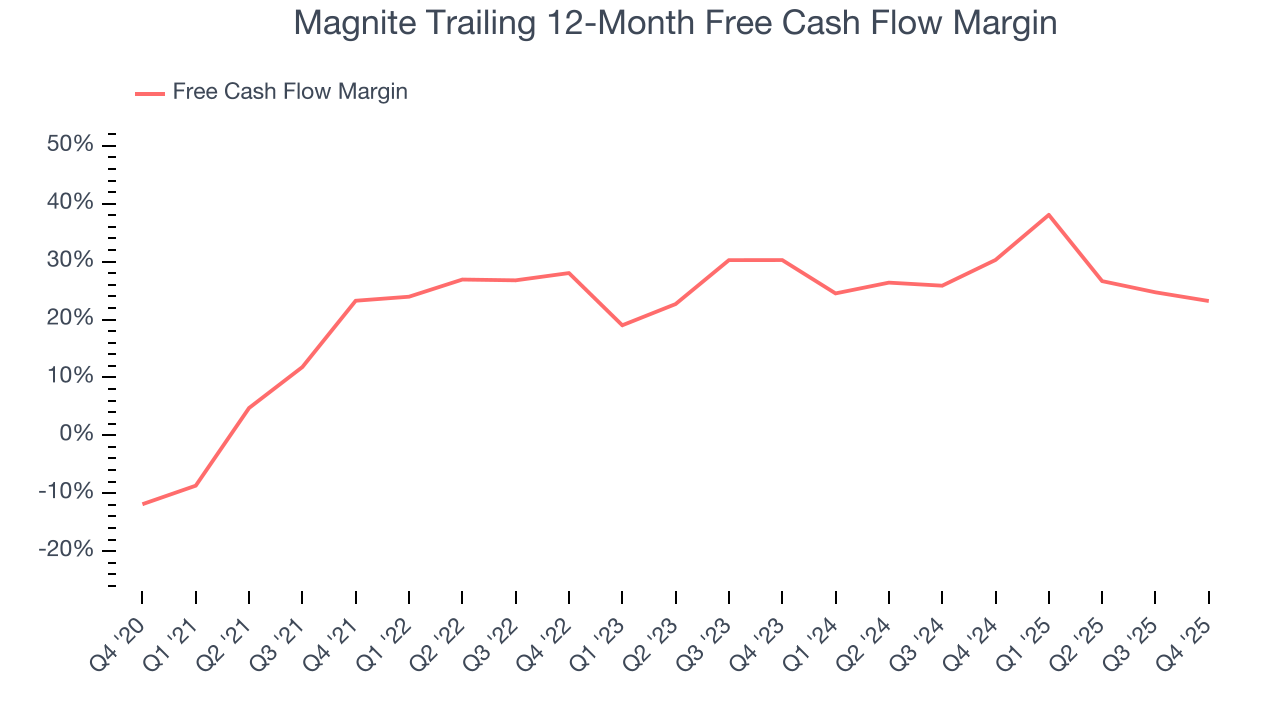

Magnite has shown terrific cash profitability, enabling it to reinvest, return capital to investors, and stay ahead of the competition while maintaining an ample cushion. The company’s free cash flow margin was among the best in the business services sector, averaging 27.1% over the last five years. The divergence from its underwhelming operating margin stems from the add-back of non-cash charges like depreciation and stock-based compensation. GAAP operating profit expenses these line items, but free cash flow does not.

Magnite’s free cash flow clocked in at $103.1 million in Q4, equivalent to a 50.2% margin. The company’s cash profitability regressed as it was 7 percentage points lower than in the same quarter last year, but it’s still above its five-year average. We wouldn’t read too much into this quarter’s decline because investment needs can be seasonal, leading to short-term swings. Long-term trends trump temporary fluctuations.

9. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

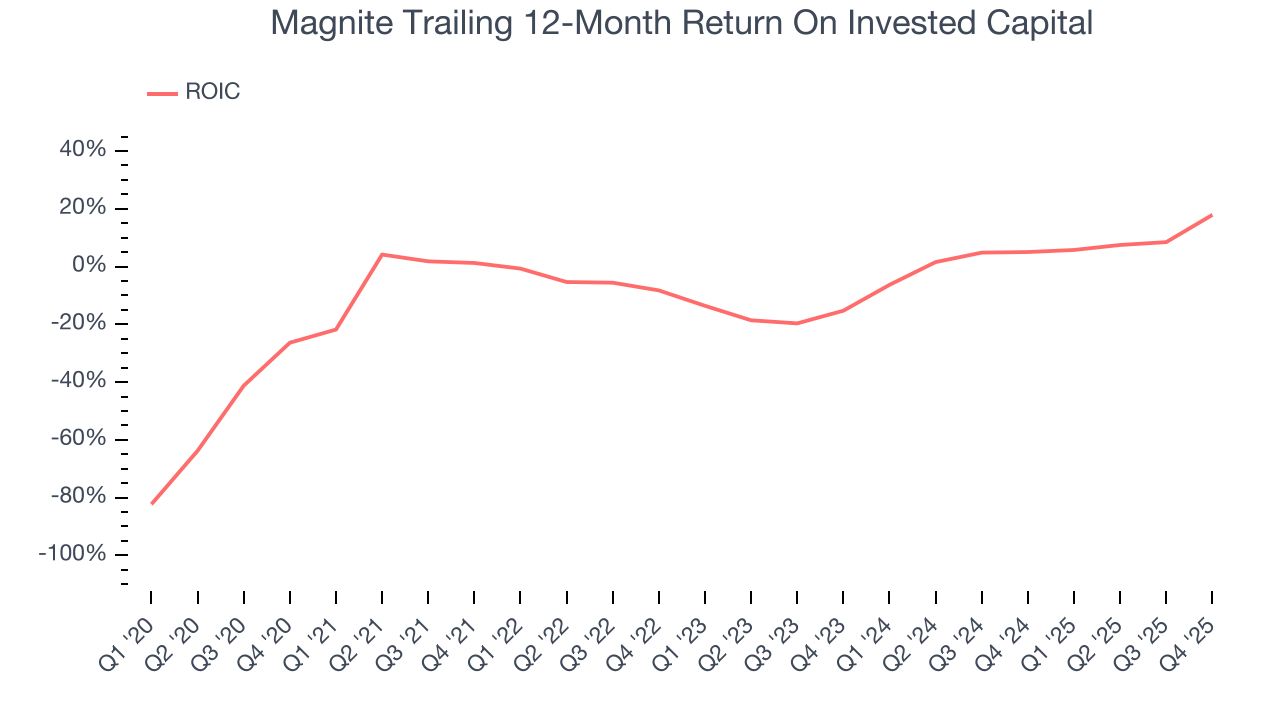

Although Magnite has shown solid fundamentals lately, it historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 0.1%, lower than the typical cost of capital (how much it costs to raise money) for business services companies.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Over the last few years, Magnite’s ROIC has increased. This is a good sign, but we recognize its lack of profitable growth during the COVID era was the primary reason for the change.

10. Balance Sheet Assessment

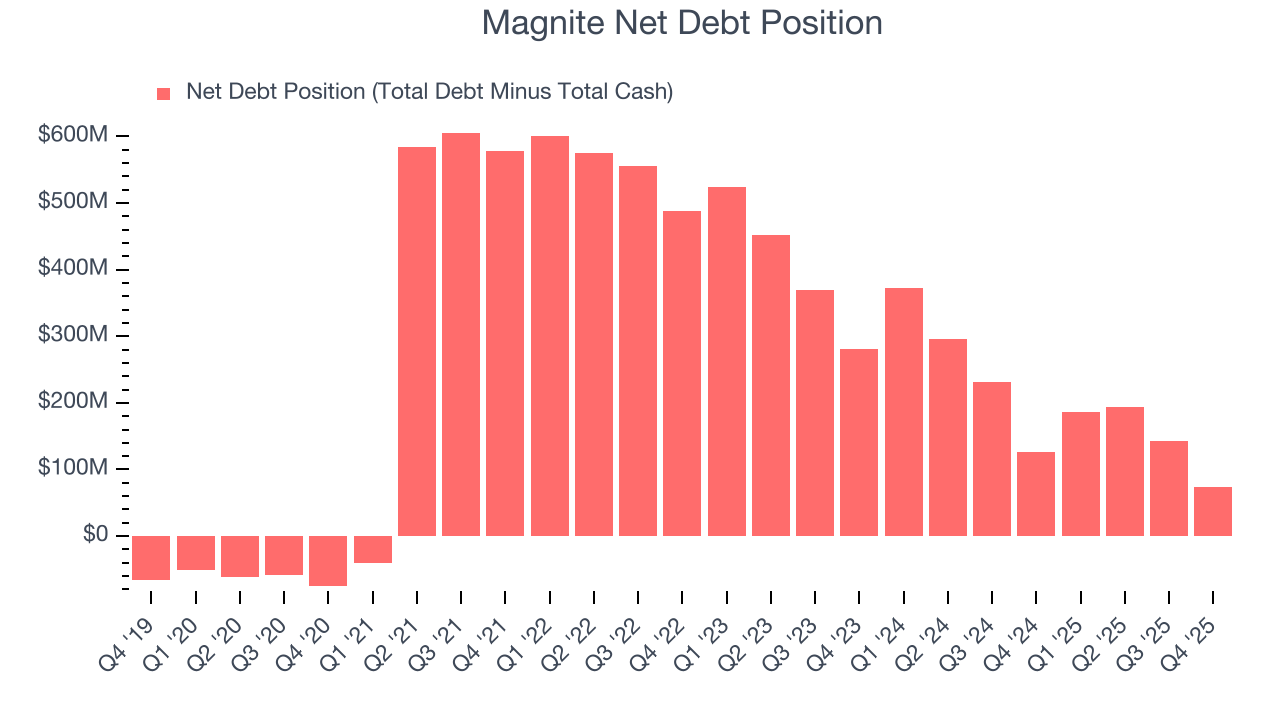

Magnite reported $553.4 million of cash and $626.4 million of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $201.3 million of EBITDA over the last 12 months, we view Magnite’s 0.4× net-debt-to-EBITDA ratio as safe. We also see its $10.91 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

11. Key Takeaways from Magnite’s Q4 Results

We struggled to find many positives in these results. Its revenue missed and its EPS fell short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock traded down 2.1% to $11.72 immediately following the results.

12. Is Now The Time To Buy Magnite?

Updated: March 17, 2026 at 12:36 AM EDT

Before deciding whether to buy Magnite or pass, we urge investors to consider business quality, valuation, and the latest quarterly results.

There are several reasons why we think Magnite is a great business. First of all, the company’s revenue growth was exceptional over the last five years. And while its relatively low ROIC suggests management has struggled to find compelling investment opportunities, its powerful free cash flow generation enables it to stay ahead of the competition through consistent reinvestment of profits. On top of that, Magnite’s expanding adjusted operating margin shows the business has become more efficient.

Magnite’s P/E ratio based on the next 12 months is 11x. Looking across the spectrum of business services companies today, Magnite’s fundamentals shine bright. We like the stock at this price.

Wall Street analysts have a consensus one-year price target of $22.07 on the company (compared to the current share price of $12.13), implying they see 82% upside in buying Magnite in the short term.