Monster (MNST)

Not many stocks excite us like Monster. It generates heaps of cash that are reinvested into the business, creating a virtuous cycle of returns.― StockStory Analyst Team

1. News

2. Summary

Why We Like Monster

Founded in 2002 as a natural soda and juice company, Monster Beverage (NASDAQ:MNST) is a pioneer of the energy drink category, and its Monster Energy brand targets a young, active demographic.

- Excellent operating margin highlights the strength of its business model, and it turbocharged its profits by achieving some fixed cost leverage

- Impressive free cash flow profitability enables the company to fund new investments or reward investors with share buybacks/dividends, and its recently improved profitability means it has even more resources to invest or distribute

- ROIC punches in at 35.7%, illustrating management’s expertise in identifying profitable investments, and its returns are climbing as it finds even more attractive growth opportunities

Monster is a no-brainer. Any surprise this is one of our favorite stocks?

Is Now The Time To Buy Monster?

Monster is trading at $76.83 per share, or 34x forward P/E. The lofty multiple means expectations are high for this company over the next six to twelve months.

Do you like the business model and believe in the company’s future? If so, you can own a smaller position, as our work shows that high-quality companies outperform the market over a multi-year period regardless of valuation at entry.

3. Monster (MNST) Research Report: Q4 CY2025 Update

Energy drink company Monster Beverage (NASDAQ:MNST) reported Q4 CY2025 results beating Wall Street’s revenue expectations, with sales up 17.6% year on year to $2.13 billion. Its non-GAAP profit of $0.51 per share was 4.7% above analysts’ consensus estimates.

Monster (MNST) Q4 CY2025 Highlights:

- Revenue: $2.13 billion vs analyst estimates of $2.04 billion (17.6% year-on-year growth, 4.6% beat)

- Adjusted EPS: $0.51 vs analyst estimates of $0.49 (4.7% beat)

- Operating Margin: 25.5%, up from 21% in the same quarter last year

- Market Capitalization: $83.45 billion

Company Overview

Founded in 2002 as a natural soda and juice company, Monster Beverage (NASDAQ:MNST) is a pioneer of the energy drink category, and its Monster Energy brand targets a young, active demographic.

The energy drink category was new and catered to a niche demographic early in the company’s history. Its beverages sought to disrupt the huge soda market as consumers began to shy away from drinks with too much sugar. Monster helped create and capitalized on the demand for better-for-you functional beverages.

The unique selling proposition of Monster Beverage is a reliable energy source with a refreshing taste. This is achieved through a proprietary blend of caffeine, taurine, B vitamins, and herbal extracts. Monster also partners with popular and alternative sports to further cement the brand image as one for active lifestyles, not couch potatoes who want something to wash down some fast food with.

Monster Beverage's products have achieved widespread distribution over time and can be found on the shelves of convenience stores, gas stations, supermarkets, and mass merchandise retailers. Sports arenas, movie theaters, and other venues also sell Monster's products. Lastly, the company launched its e-commerce platform in 2015, allowing consumers to purchase beverages and merchandise directly from their website.

4. Beverages, Alcohol, and Tobacco

These companies' performance is influenced by brand strength, marketing strategies, and shifts in consumer preferences. Changing consumption patterns are particularly relevant and can be seen in the rise of cannabis, craft beer, and vaping or the steady decline of soda and cigarettes. Companies that spend on innovation to meet consumers where they are with regards to trends can reap huge demand benefits while those who ignore trends can see stagnant volumes. Finally, with the advent of the social media, the cost of starting a brand from scratch is much lower, meaning that new entrants can chip away at the market shares of established players.

Competitors that offer energy drinks or alternatives to energy drinks include Rockstar Energy from PepsiCo (NASDAQ:PEP), Coca-Cola Energy and Full Throttle from Coca-Cola (NYSE:KO), and Celsius (NASDAQ:CELH).

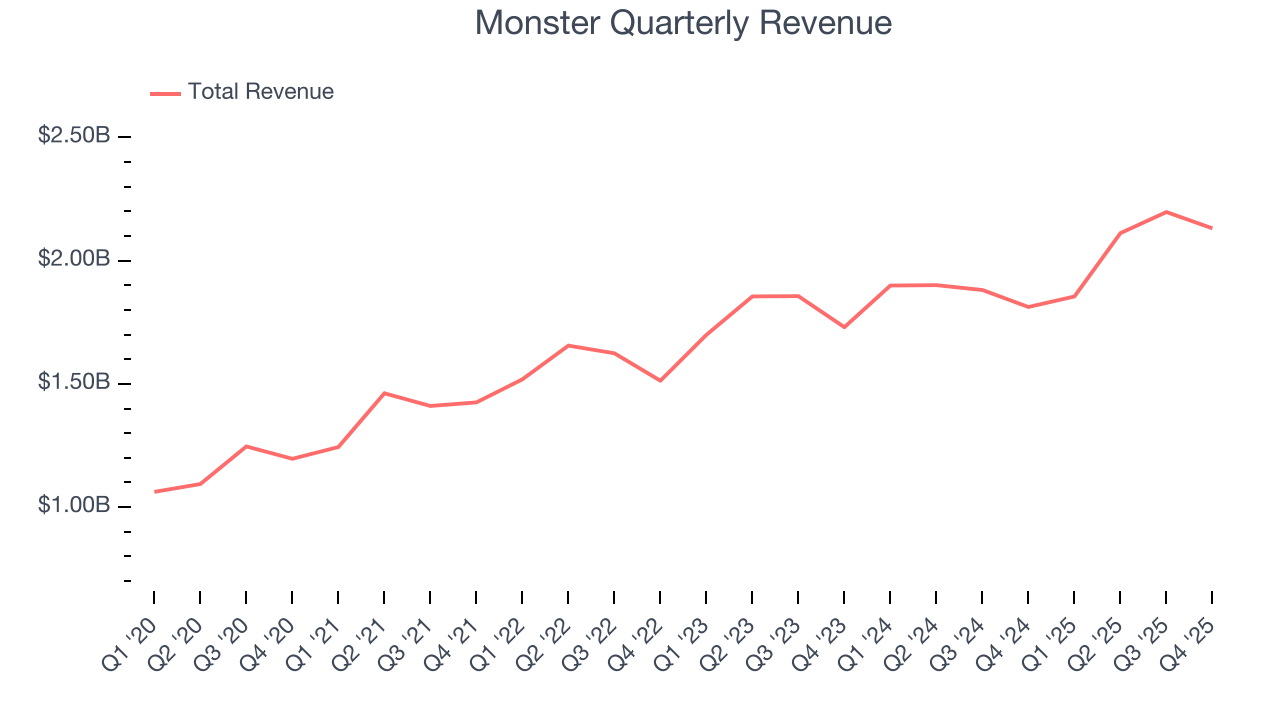

5. Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can have short-term success, but a top-tier one grows for years.

With $8.29 billion in revenue over the past 12 months, Monster is one of the larger consumer staples companies and benefits from a well-known brand that influences purchasing decisions.

As you can see below, Monster’s sales grew at a decent 9.5% compounded annual growth rate over the last three years. This shows its offerings generated slightly more demand than the average consumer staples company, a helpful starting point for our analysis.

This quarter, Monster reported year-on-year revenue growth of 17.6%, and its $2.13 billion of revenue exceeded Wall Street’s estimates by 4.6%.

Looking ahead, sell-side analysts expect revenue to grow 8.4% over the next 12 months, similar to its three-year rate. Still, this projection is noteworthy and indicates the market is forecasting success for its products.

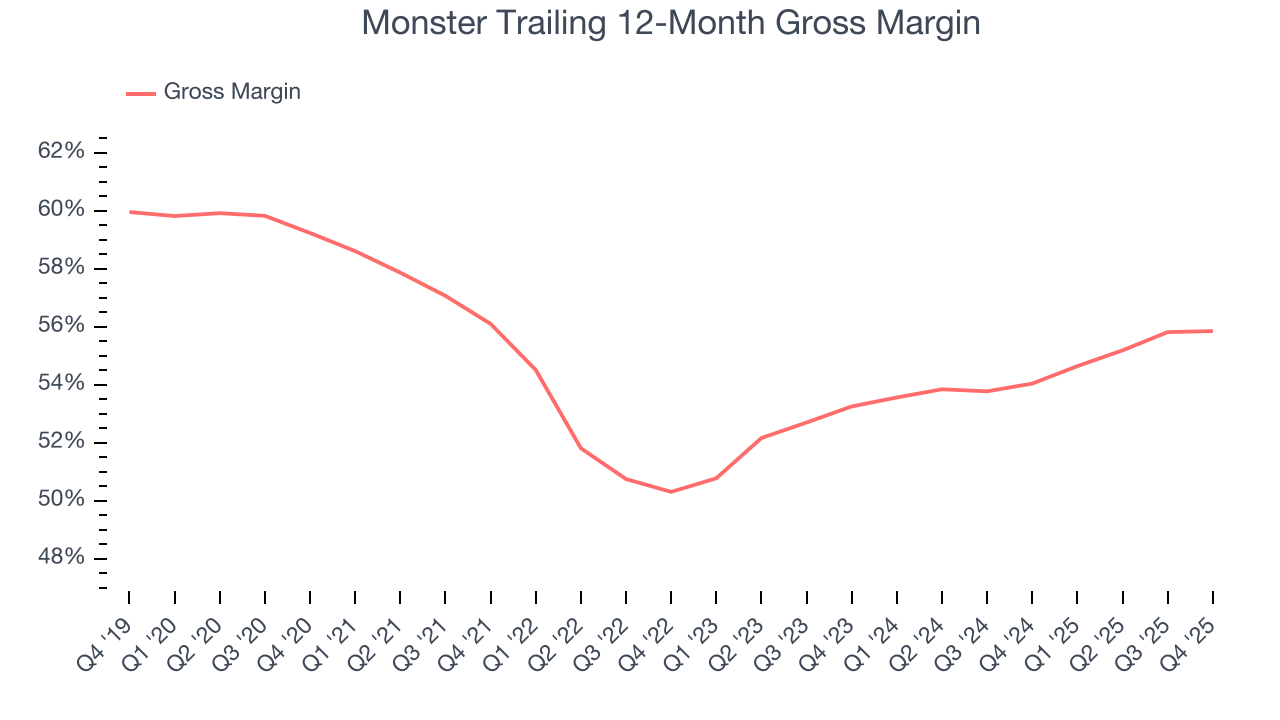

6. Gross Margin & Pricing Power

All else equal, we prefer higher gross margins because they usually indicate that a company sells more differentiated products, has a stronger brand, and commands pricing power.

Monster has best-in-class unit economics for a consumer staples company, enabling it to invest in areas such as marketing and talent. As you can see below, it averaged an elite 55% gross margin over the last two years. That means Monster only paid its suppliers $45.01 for every $100 in revenue.

This quarter, Monster’s gross profit margin was 55.5%, in line with the same quarter last year. On a wider time horizon, Monster’s full-year margin has been trending up over the past 12 months, increasing by 1.8 percentage points. If this move continues, it could suggest better unit economics due to more leverage from its growing sales on the fixed portion of its cost of goods sold (such as manufacturing expenses).

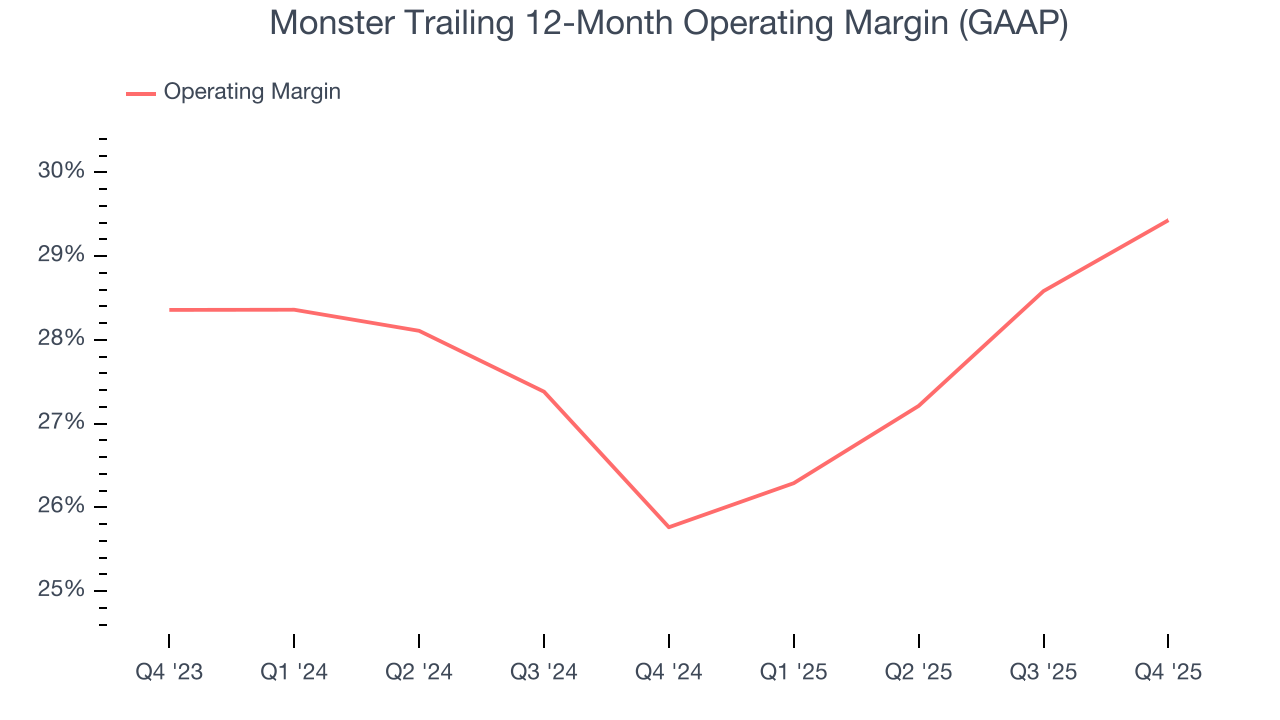

7. Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Monster has been a well-oiled machine over the last two years. It demonstrated elite profitability for a consumer staples business, boasting an average operating margin of 27.7%. This result isn’t surprising as its high gross margin gives it a favorable starting point.

Analyzing the trend in its profitability, Monster’s operating margin rose by 3.7 percentage points over the last year, as its sales growth gave it operating leverage.

This quarter, Monster generated an operating margin profit margin of 25.5%, up 4.4 percentage points year on year. The increase was encouraging, and because its operating margin rose more than its gross margin, we can infer it was more efficient with expenses such as marketing, and administrative overhead.

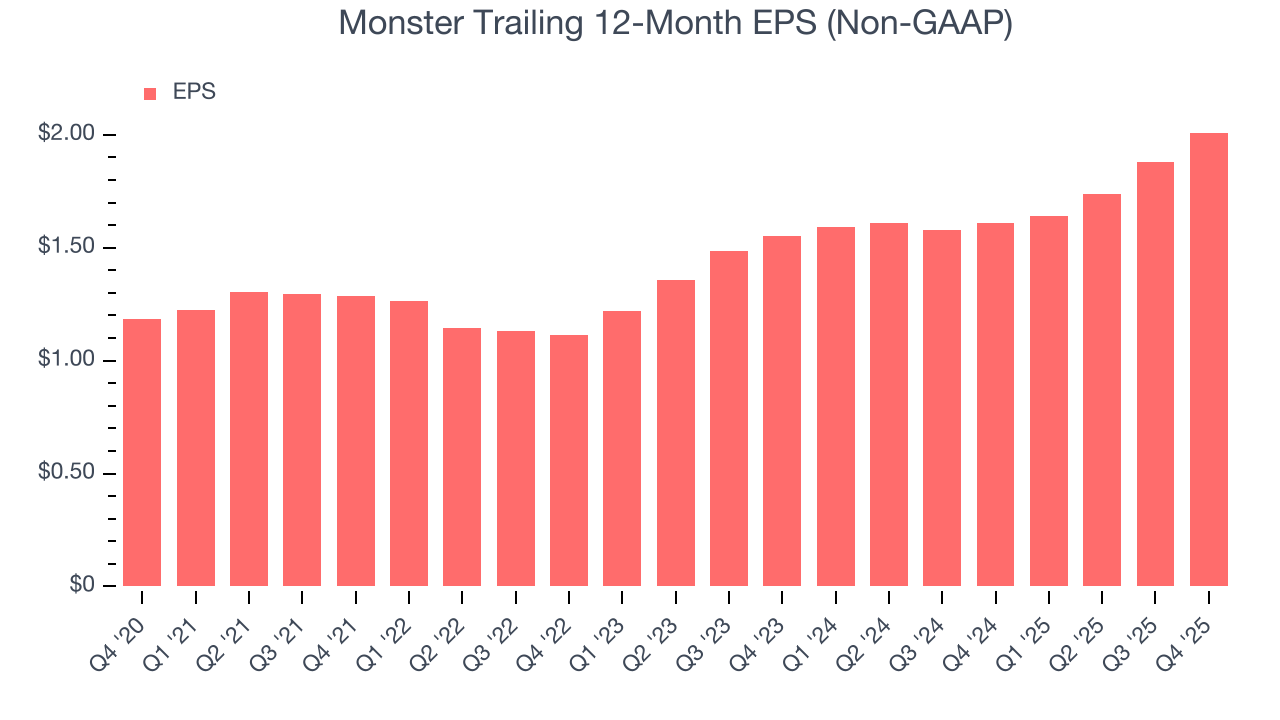

8. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Monster’s EPS grew at a spectacular 21.7% compounded annual growth rate over the last three years, higher than its 9.5% annualized revenue growth. However, this alone doesn’t tell us much about its business quality because its operating margin didn’t improve.

In Q4, Monster reported adjusted EPS of $0.51, up from $0.38 in the same quarter last year. This print beat analysts’ estimates by 4.7%. Over the next 12 months, Wall Street expects Monster’s full-year EPS of $2.01 to grow 12.9%.

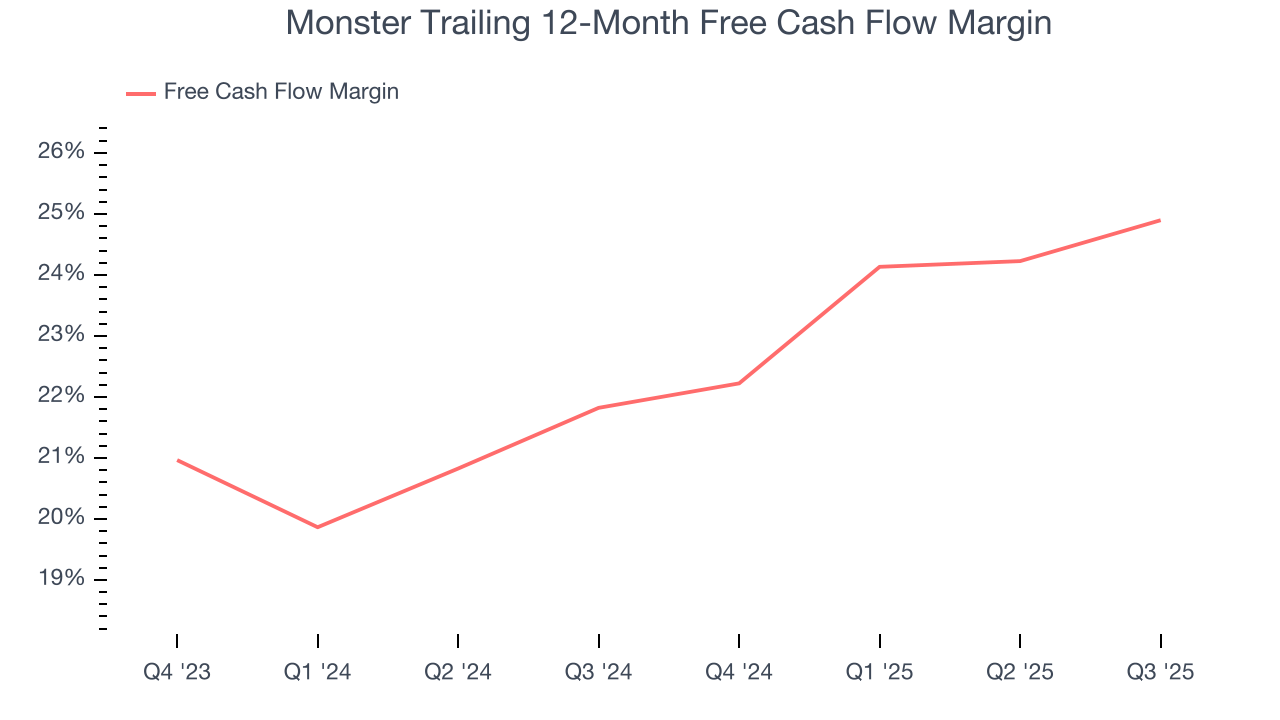

9. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Monster has shown terrific cash profitability, driven by its lucrative business model that enables it to reinvest, return capital to investors, and stay ahead of the competition. The company’s free cash flow margin was among the best in the consumer staples sector, averaging 24% over the last two years.

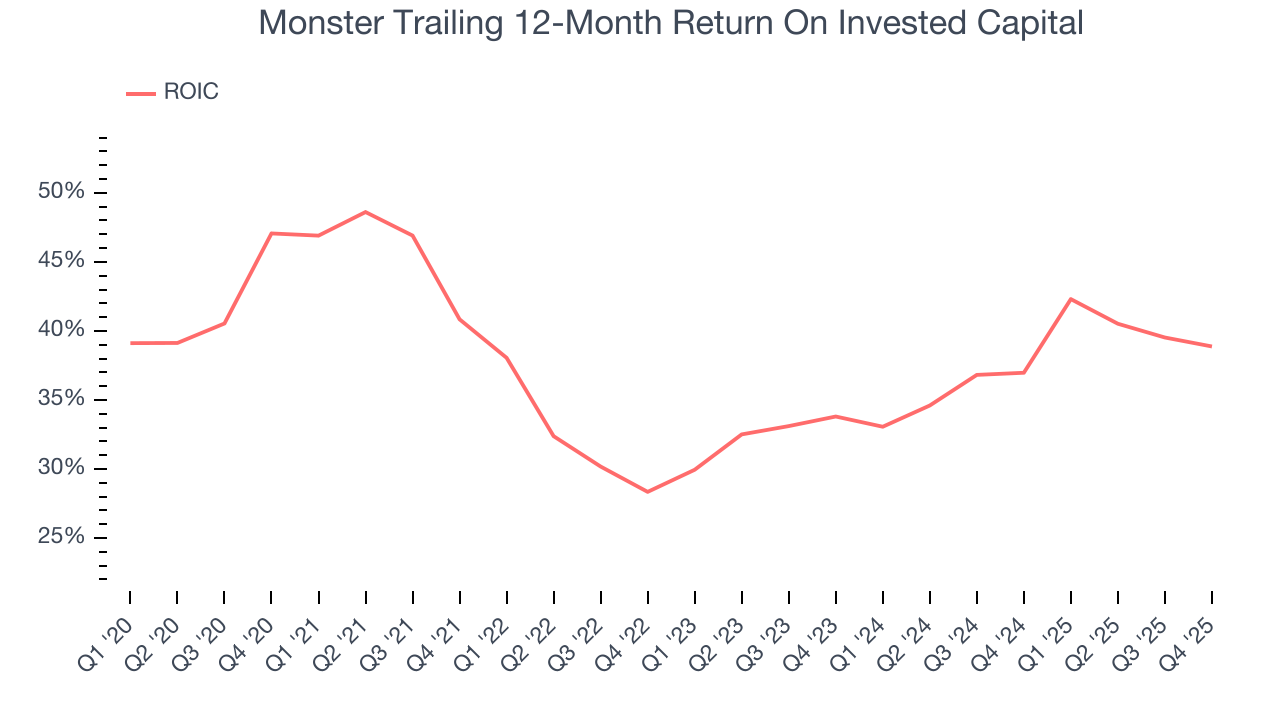

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Monster’s five-year average ROIC was 35.8%, placing it among the best consumer staples companies. This illustrates its management team’s ability to invest in highly profitable ventures and produce tangible results for shareholders.

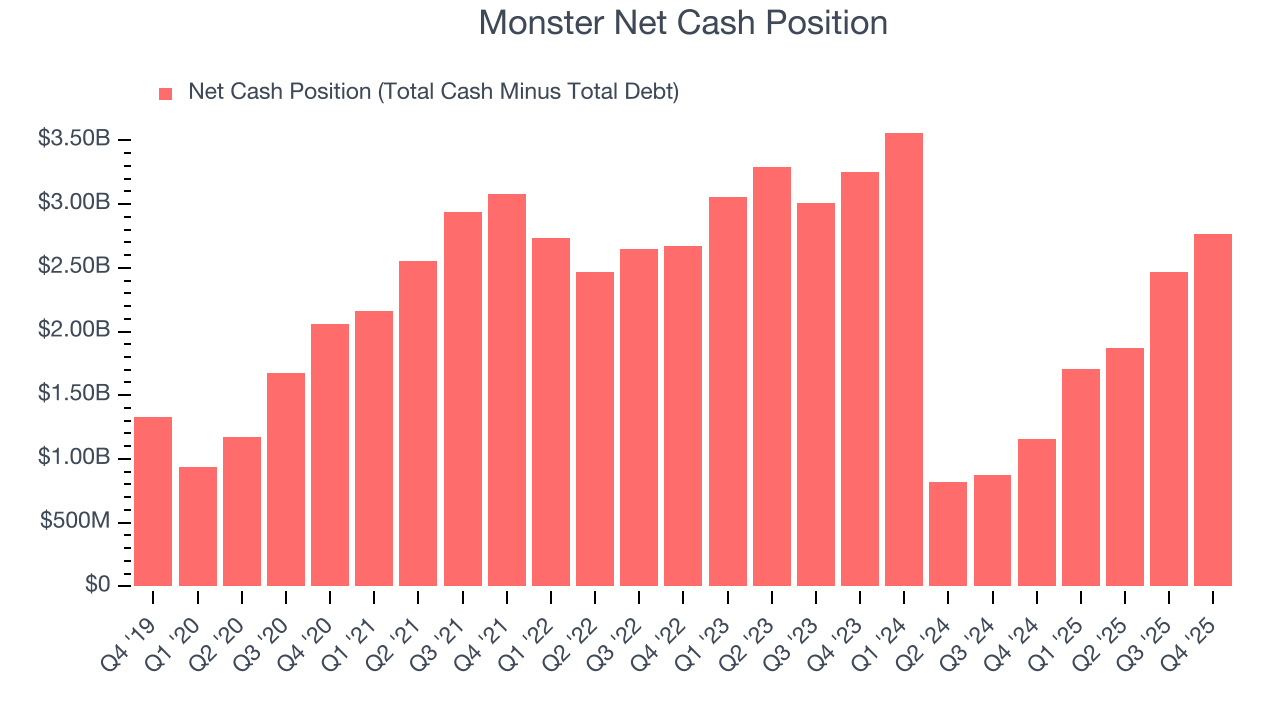

11. Balance Sheet Assessment

One of the best ways to mitigate bankruptcy risk is to hold more cash than debt.

Monster is a profitable, well-capitalized company with $2.77 billion of cash and no debt. This position is 3.3% of its market cap and gives it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

12. Key Takeaways from Monster’s Q4 Results

We enjoyed seeing Monster beat analysts’ revenue expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. On the other hand, its gross margin slightly missed. Overall, we think this was a decent quarter with some key metrics above expectations. The market seemed to be hoping for more, and the stock traded down 3% to $84.13 immediately after reporting.

13. Is Now The Time To Buy Monster?

Updated: March 13, 2026 at 10:48 PM EDT

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in Monster.

Monster is an amazing business ranking highly on our list. To begin with, its revenue growth was solid over the last three years, and its growth over the next 12 months is expected to accelerate. On top of that, its impressive operating margins show it has a highly efficient business model, and its powerful free cash flow generation enables it to stay ahead of the competition through consistent reinvestment of profits.

Monster’s P/E ratio based on the next 12 months is 34x. This multiple isn’t necessarily cheap, but we’ll happily own Monster as its fundamentals illustrate it’s clearly doing something special. Investments like this should be held patiently for at least three to five years as they benefit from the power of long-term compounding, which more than makes up for any short-term price volatility that comes with relatively high valuations.

Wall Street analysts have a consensus one-year price target of $87.46 on the company (compared to the current share price of $76.83).