Marqeta (MQ)

Marqeta doesn’t impress us. Its underwhelming sales growth and operating losses make us question the sustainability of its business model.― StockStory Analyst Team

1. News

2. Summary

Why Marqeta Is Not Exciting

Powering the cards behind innovative fintech services like Block's Cash App, Marqeta (NASDAQ:MQ) provides a cloud-based platform that allows businesses to create customized payment card programs and process card transactions.

- Operating margin declined by 2.6 percentage points over the last year as its sales cratered

- Historical operating margin losses point to an inefficient cost structure

- A silver lining is that its software platform has product-market fit given the rapid recovery of its customer acquisition costs

Marqeta is in the doghouse. We believe there are better opportunities elsewhere.

Why There Are Better Opportunities Than Marqeta

At $4.01 per share, Marqeta trades at 2.5x forward price-to-sales. This sure is a cheap multiple, but you get what you pay for.

It’s better to pay up for high-quality businesses with higher long-term earnings potential rather than to buy lower-quality stocks because they appear cheap. These challenged businesses often don’t re-rate, a phenomenon known as a “value trap”.

3. Marqeta (MQ) Research Report: Q4 CY2025 Update

Payment technology company Marqeta (NASDAQ:MQ) beat Wall Street’s revenue expectations in Q4 CY2025, with sales up 26.7% year on year to $172.1 million. The company expects next quarter’s revenue to be around $164.1 million, close to analysts’ estimates. Its GAAP loss of $0 per share was $0.01 above analysts’ consensus estimates.

Marqeta (MQ) Q4 CY2025 Highlights:

- Revenue: $172.1 million vs analyst estimates of $167.1 million (26.7% year-on-year growth, 3% beat)

- EPS (GAAP): $0 vs analyst estimates of -$0.01 ($0.01 beat)

- Adjusted EBITDA: $30.68 million vs analyst estimates of $26.09 million (17.8% margin, 17.6% beat)

- Revenue Guidance for Q1 CY2026 is $164.1 million at the midpoint, roughly in line with what analysts were expecting

- Operating Margin: -4.8%, up from -27.6% in the same quarter last year

- Free Cash Flow Margin: 27%, down from 48.1% in the previous quarter

- Market Capitalization: $1.8 billion

Company Overview

Powering the cards behind innovative fintech services like Block's Cash App, Marqeta (NASDAQ:MQ) provides a cloud-based platform that allows businesses to create customized payment card programs and process card transactions.

Marqeta operates at the intersection of banking and technology, modernizing the traditional payments infrastructure. The company serves as both an issuer processor and card program manager, helping businesses embed payment capabilities into their offerings without needing to build the complex infrastructure themselves. This allows companies to create tailored card experiences—whether debit, prepaid, or credit—with features like real-time funding, dynamic spending controls, and instant digital card issuance.

The platform is particularly valuable for companies wanting to offer financial services without becoming banks themselves. For example, a gig economy platform might use Marqeta to create instant payment cards for workers, a retail company could launch a branded credit card with custom rewards, or a fintech app might offer virtual cards with specialized spending limits. Marqeta's "Just-in-Time" funding capability is a key differentiator, allowing cards to maintain zero balance until a transaction is approved, at which point funds are automatically transferred.

Marqeta generates revenue primarily through processing fees from card transactions flowing through its platform. The company works with issuing banks like Sutton Bank who provide the regulated banking infrastructure, while Marqeta supplies the technology layer and manages relationships with card networks such as Visa and Mastercard. This positions Marqeta as an essential intermediary in the payments ecosystem, enabling the card features behind many modern financial products without needing to be a bank itself.

4. Payments Software

Consumers want the ability to make payments whenever and wherever they prefer – and to do so without having to worry about fraud or other security threats. However, building payments infrastructure from scratch is extremely resource-intensive for engineering teams. That drives demand for payments platforms that are easy to integrate into consumer applications and websites.

Marqeta competes with traditional payment processors like Fiserv (NASDAQ:FISV) and Fidelity National Information Services (NYSE:FIS), as well as newer fintech platforms including Galileo (owned by SoFi, NASDAQ:SOFI), Stripe (private), and Adyen (OTC:ADYEY).

5. Revenue Growth

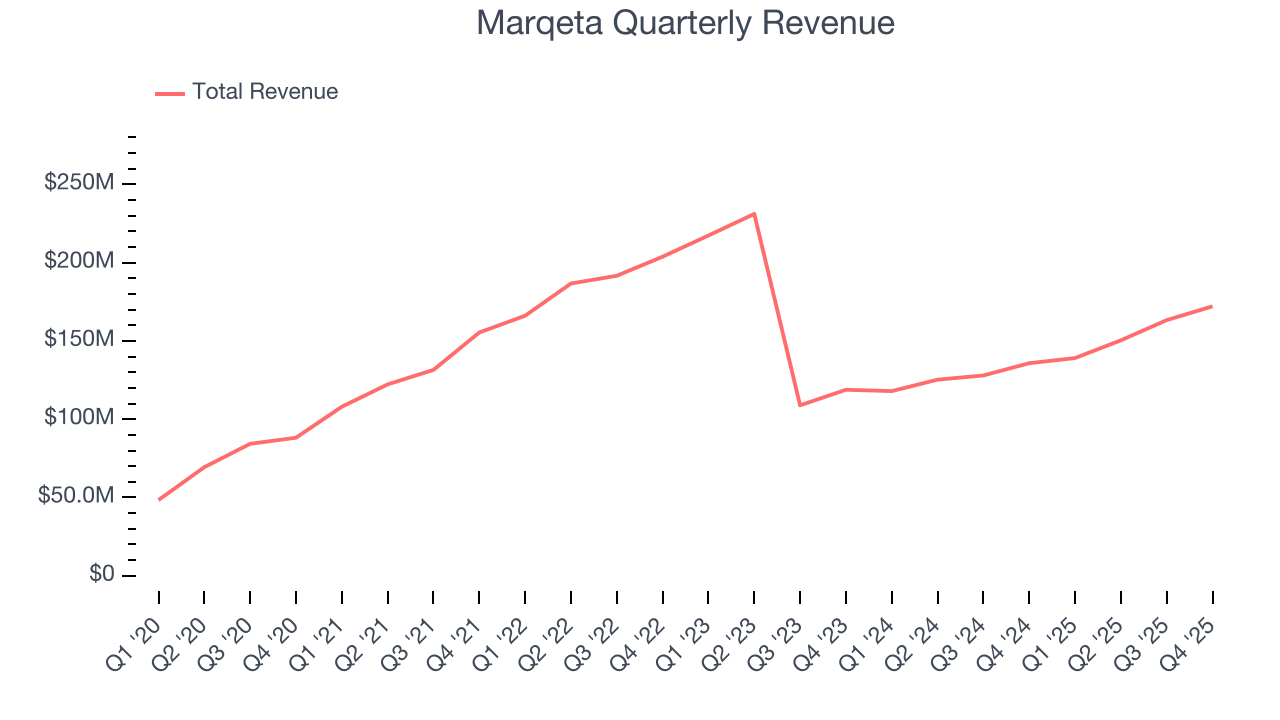

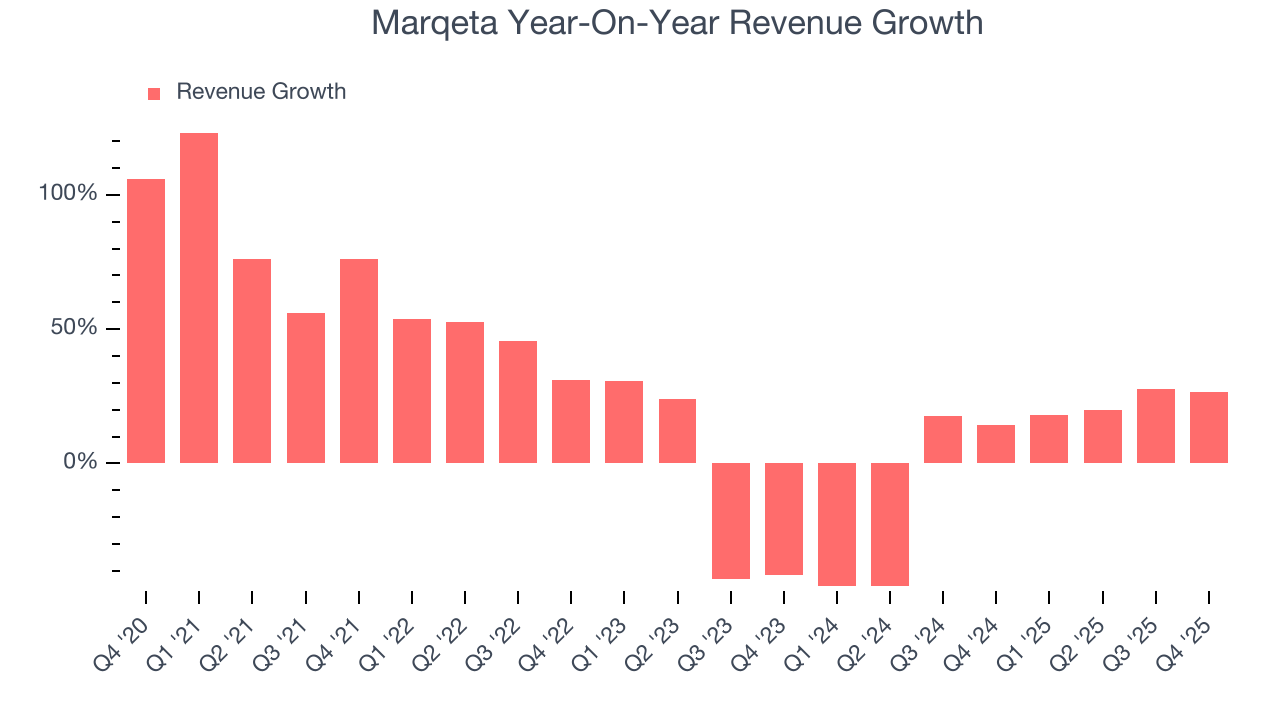

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last five years, Marqeta grew its sales at a 16.6% annual rate. Though this growth is acceptable on an absolute basis, we need to see more than just topline growth for the software sector, which can display significant earnings volatility. This means our bar for the sector is particularly high, reflecting the non-essential and hit-driven nature of the products and services offered. Additionally, five-year CAGR starts around Covid, when revenue was depressed then rebounded.

We at StockStory place the most emphasis on long-term growth, but within software, a half-decade historical view may miss recent innovations or disruptive industry trends. Marqeta’s performance shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 3.9% annually.

This quarter, Marqeta reported robust year-on-year revenue growth of 26.7%, and its $172.1 million of revenue topped Wall Street estimates by 3%. Company management is currently guiding for a 18% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 17% over the next 12 months, an improvement versus the last two years. This projection is healthy and indicates its newer products and services will catalyze better top-line performance.

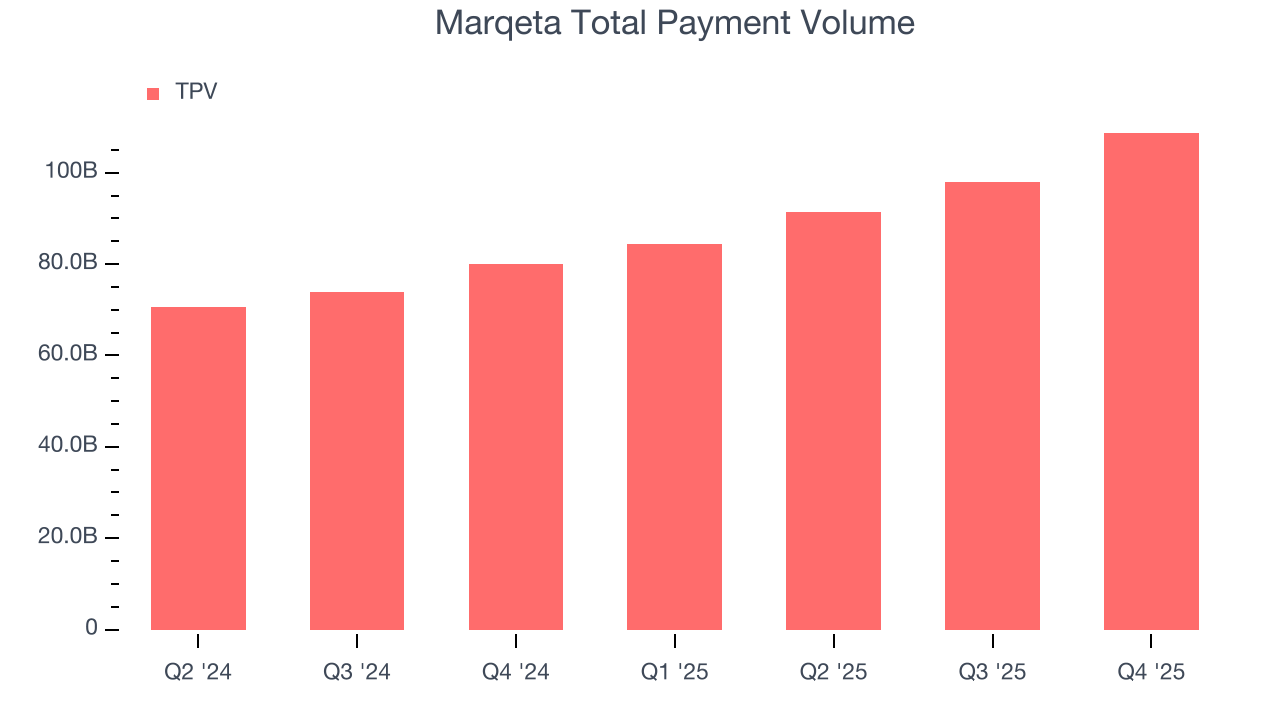

6. Total Payment Volume

TPV, or total processing volume, is the aggregate dollar value of transactions flowing through Marqeta’s platform. This is the number from which the company will ultimately collect fees, and the higher it is, the more chances Marqeta has to upsell additional services (like banking).

Marqeta’s TPV punched in at $108.7 billion in Q4, and over the last four quarters, its growth was fantastic as it averaged 32.7% year-on-year increases. This alternate topline metric grew faster than total sales, which could mean that take rates have declined. However, we can’t automatically assume the company is reducing its fees because take rates can also vary depending on the type of products sold on its platform.

7. Customer Acquisition Efficiency

The customer acquisition cost (CAC) payback period represents the months required to recover the cost of acquiring a new customer. Essentially, it’s the break-even point for sales and marketing investments. A shorter CAC payback period is ideal, as it implies better returns on investment and business scalability.

Marqeta is extremely efficient at acquiring new customers, and its CAC payback period checked in at 0.6 months this quarter. The company’s rapid recovery of its customer acquisition costs indicates it has a highly differentiated product offering and a strong brand reputation. These dynamics give Marqeta more resources to pursue new product initiatives while maintaining the flexibility to increase its sales and marketing investments.

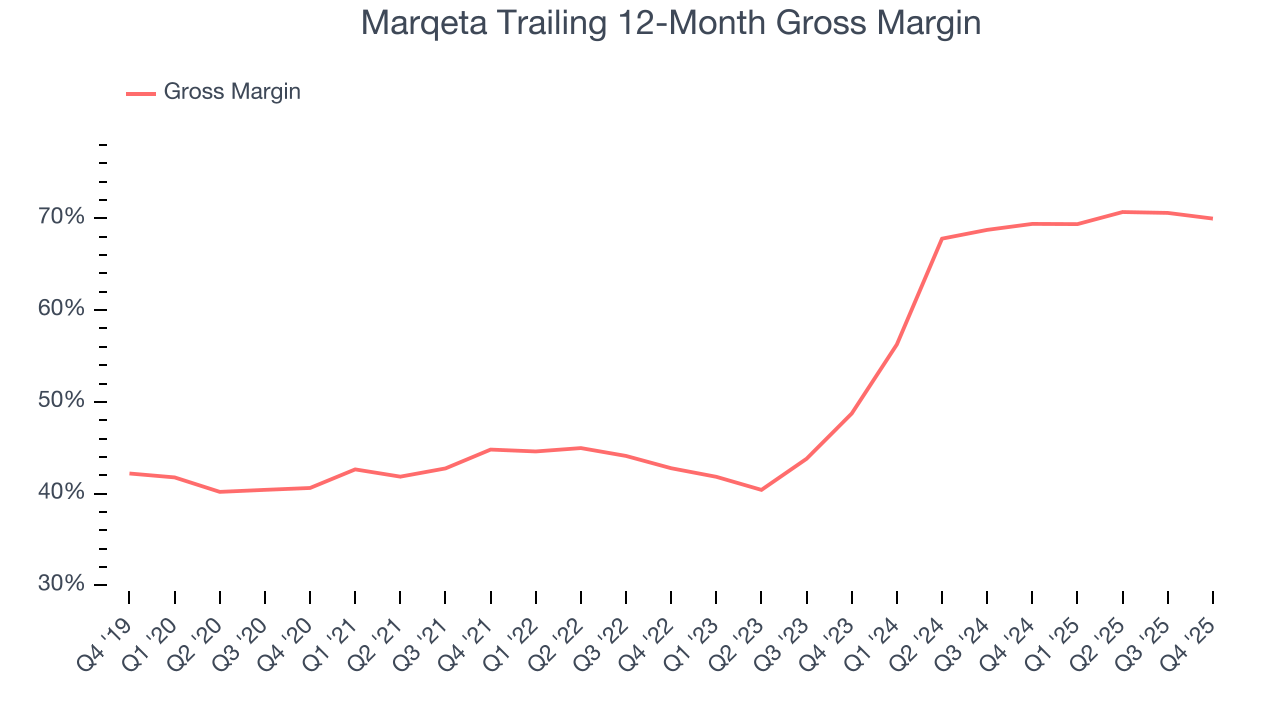

8. Gross Margin & Pricing Power

For software companies like Marqeta, gross profit tells us how much money remains after paying for the base cost of products and services (typically servers, licenses, and certain personnel). These costs are usually low as a percentage of revenue, explaining why software is more lucrative than other sectors.

Marqeta’s gross margin is worse than the software industry average, giving it less room than its competitors to hire new talent that can expand its products and services. As you can see below, it averaged a 70% gross margin over the last year. That means Marqeta paid its providers a lot of money ($30.02 for every $100 in revenue) to run its business.

The market not only cares about gross margin levels but also how they change over time because expansion creates firepower for profitability and free cash generation. Marqeta has seen gross margins improve by 21.2 percentage points over the last 2 year, which is elite in the software space.

Marqeta’s gross profit margin came in at 69.7% this quarter, down 2.6 percentage points year on year. On a wider time horizon, the company’s full-year margin has remained steady over the past four quarters, suggesting its input costs have been stable and it isn’t under pressure to lower prices.

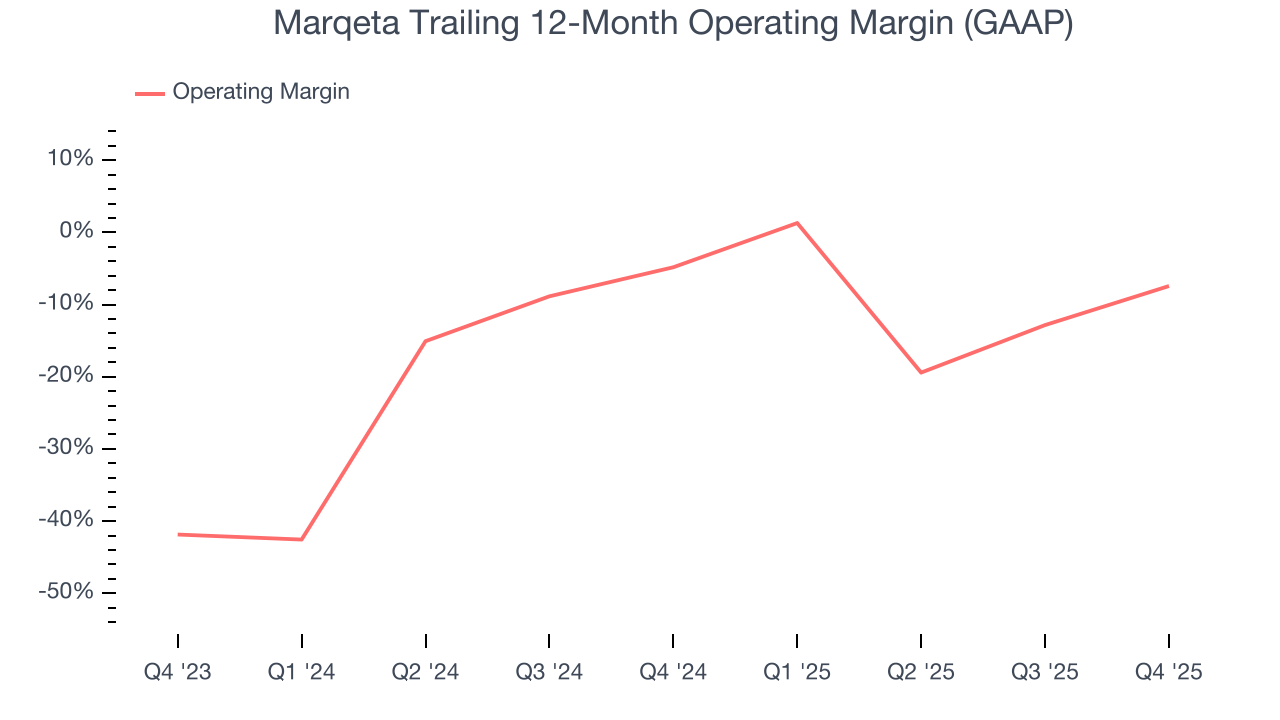

9. Operating Margin

Marqeta’s expensive cost structure has contributed to an average operating margin of negative 7.4% over the last year. Unprofitable software companies require extra attention because they spend heaps of money to capture market share. As seen in its historically underwhelming revenue performance, this strategy hasn’t worked so far, and it’s unclear what would happen if Marqeta reeled back its investments. Wall Street seems to be optimistic about its growth, but we have some doubts.

Looking at the trend in its profitability, Marqeta’s operating margin decreased by 2.6 percentage points over the last two years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. Marqeta’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers.

In Q4, Marqeta generated a negative 4.8% operating margin. The company's consistent lack of profits raise a flag.

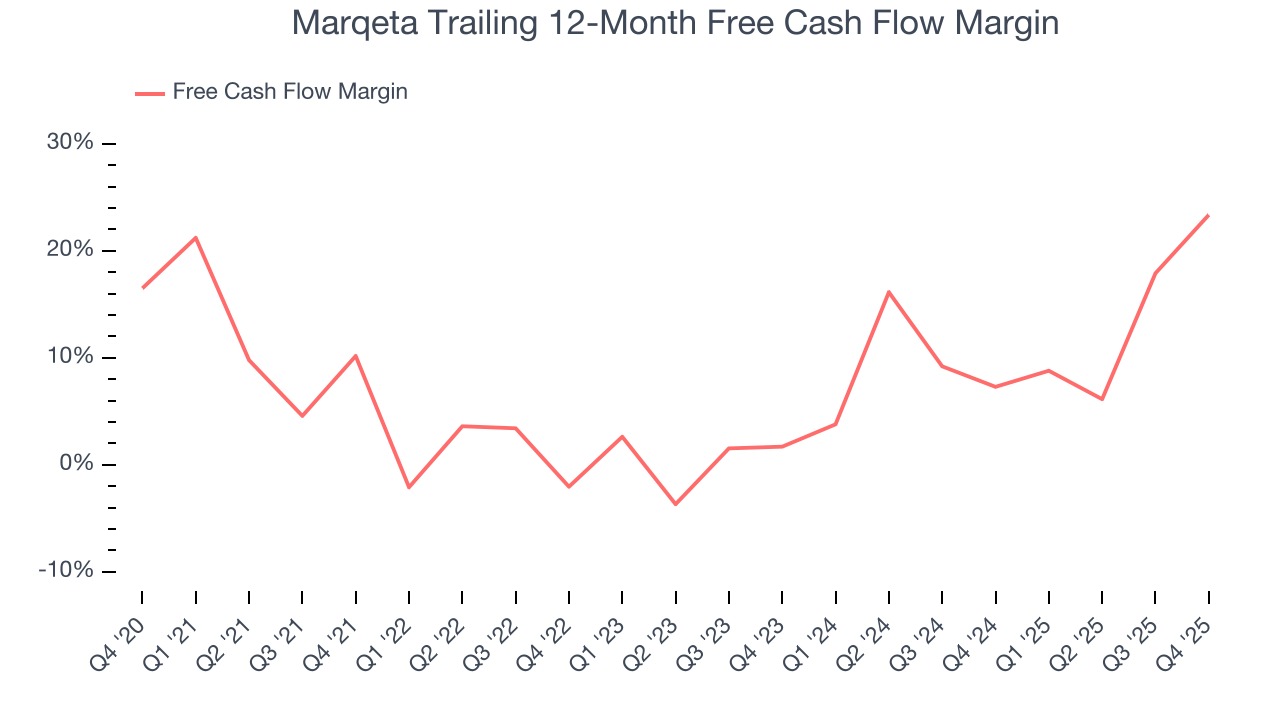

10. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Marqeta has shown robust cash profitability, driven by its cost-effective customer acquisition strategy that enables it to invest in new products and services rather than sales and marketing. The company’s free cash flow margin averaged 23.4% over the last year, quite impressive for a software business. The divergence from its underwhelming operating margin stems from the add-back of non-cash charges like depreciation and stock-based compensation. GAAP operating profit expenses these line items, but free cash flow does not.

Marqeta’s free cash flow clocked in at $46.52 million in Q4, equivalent to a 27% margin. This result was good as its margin was 22.7 percentage points higher than in the same quarter last year, but we wouldn’t put too much weight on the short term because investment needs can be seasonal, causing temporary swings. Long-term trends carry greater meaning.

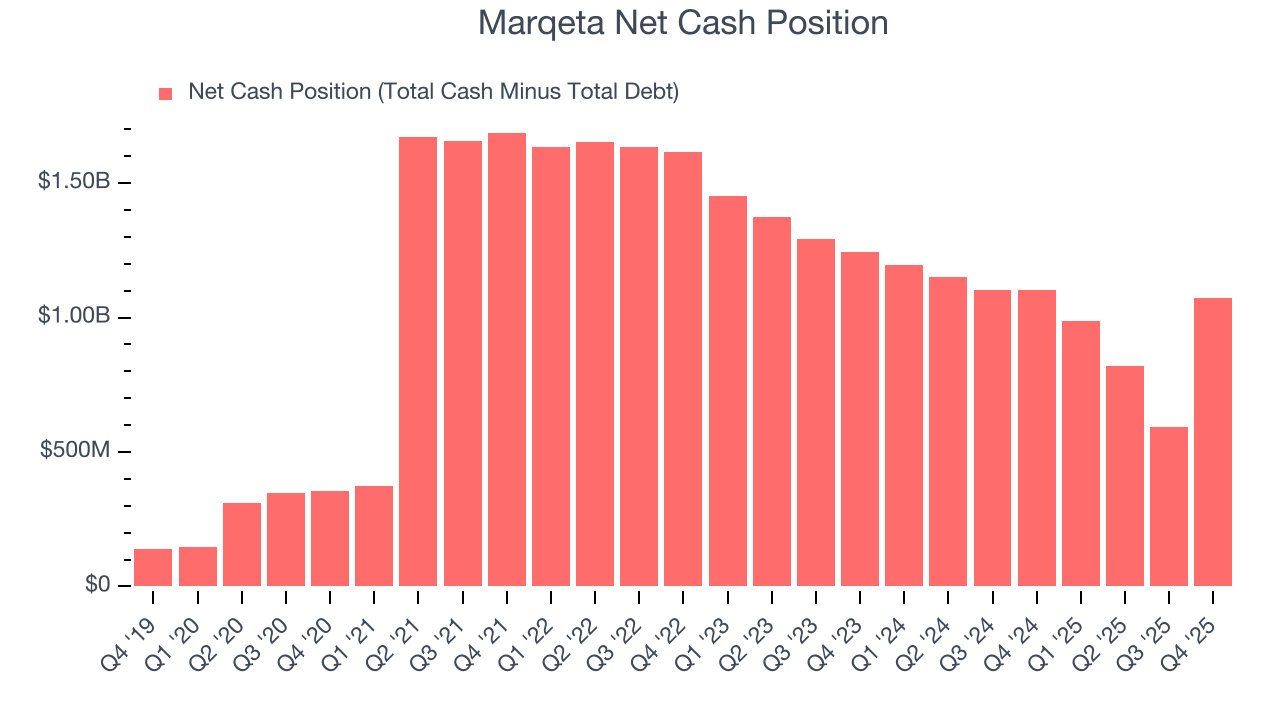

11. Balance Sheet Assessment

Companies with more cash than debt have lower bankruptcy risk.

Marqeta is a well-capitalized company with $1.08 billion of cash and $5.54 million of debt on its balance sheet. This $1.07 billion net cash position is 59.7% of its market cap and gives it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

12. Key Takeaways from Marqeta’s Q4 Results

We were impressed by how significantly Marqeta blew past analysts’ EBITDA expectations this quarter. We were also happy its revenue outperformed Wall Street’s estimates. On the other hand, its revenue guidance for next quarter was just in line. Investors were likely hoping for more, and shares traded down 7.5% to $3.84 immediately following the results.

13. Is Now The Time To Buy Marqeta?

Updated: March 16, 2026 at 10:34 PM EDT

Before making an investment decision, investors should account for Marqeta’s business fundamentals and valuation in addition to what happened in the latest quarter.

Marqeta has a few positive attributes, but it doesn’t top our wishlist. Although its revenue growth was mediocre over the last five years and analysts expect growth to slow over the next 12 months, its efficient sales strategy allows it to target and onboard new users at scale. Investors should still be cautious, however, as Marqeta’s declining operating margin shows it’s becoming less efficient at building and selling its software.

Marqeta’s price-to-sales ratio based on the next 12 months is 2.5x. This valuation is reasonable, but the company’s shakier fundamentals present too much downside risk. We're pretty confident there are superior stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $5.21 on the company (compared to the current share price of $4.01).