Natera (NTRA)

Natera is a compelling stock. Its spectacular 19.5% growth in sales volumes shows customers can’t get enough of its products.― StockStory Analyst Team

1. News

2. Summary

Why We Like Natera

Founded in 2003 as Gene Security Network before rebranding in 2012, Natera (NASDAQ:NTRA) develops and commercializes genetic tests for prenatal screening, cancer detection, and organ transplant monitoring using its proprietary cell-free DNA technology.

- Impressive 42.4% annual revenue growth over the last five years indicates it’s winning market share this cycle

- Expected revenue growth of 20.2% for the next year suggests its market share will rise

- The stock is a timely buy because it’s trading at a reasonable price relative to its growth prospects

We expect great things from Natera. The valuation seems fair when considering its quality, so this could be a favorable time to invest in some shares.

Why Is Now The Time To Buy Natera?

Natera is trading at $186.11 per share, or 10.3x forward price-to-sales. Looking at the healthcare landscape today, Natera’s qualities really stand out, and we like it at this price.

It seems like an opportune time to buy the stock if you believe in the long-term prospects of the business.

3. Natera (NTRA) Research Report: Q3 CY2025 Update

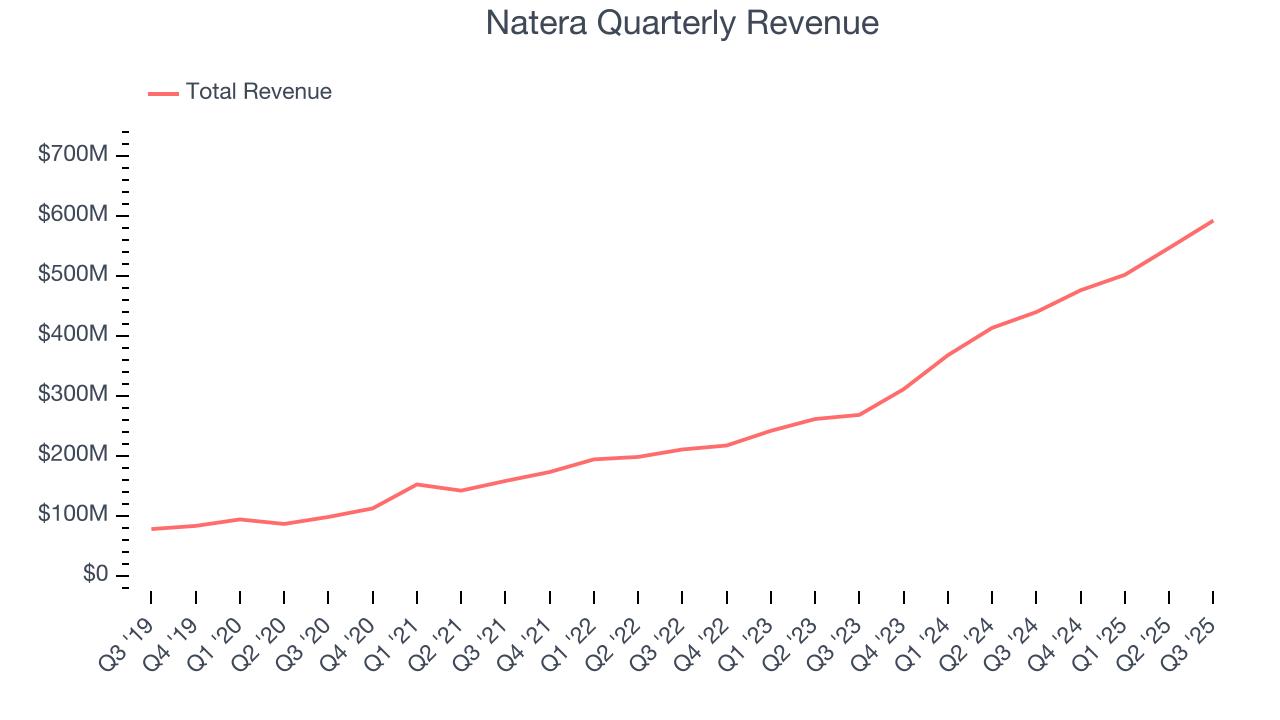

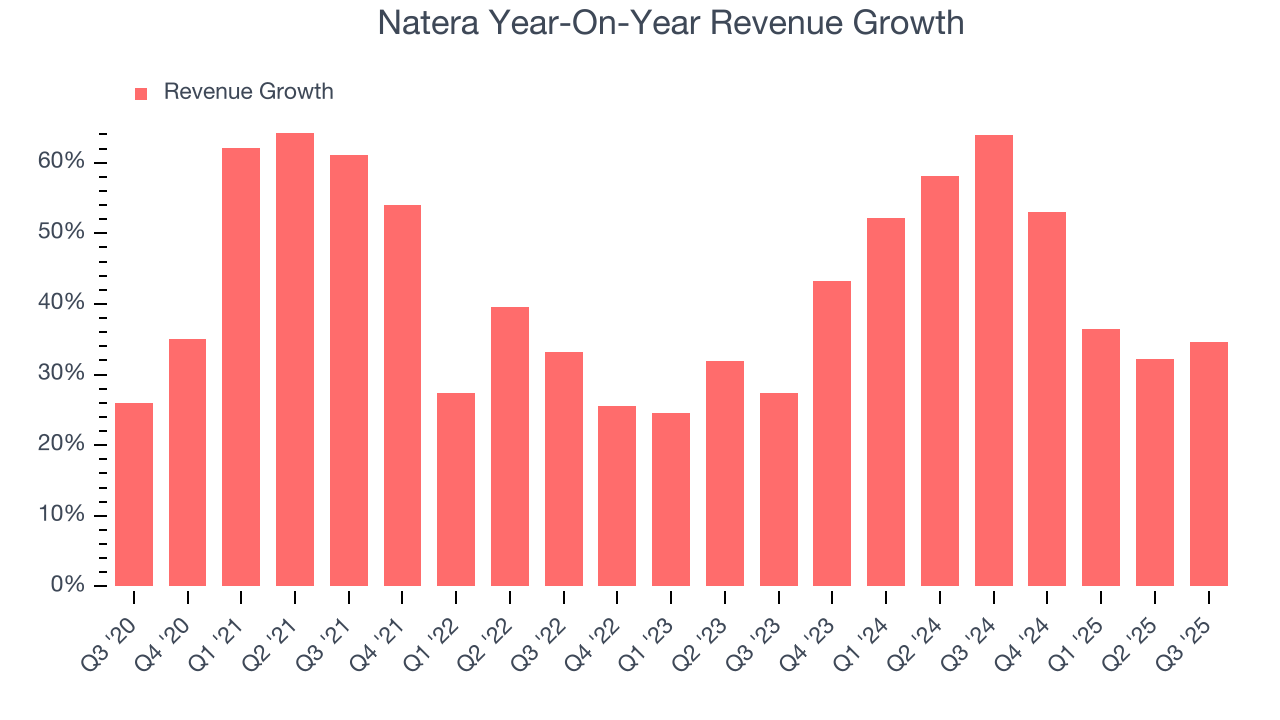

Genetic testing company Natera (NASDAQ:NTRA). announced better-than-expected revenue in Q3 CY2025, with sales up 34.7% year on year to $592.2 million. The company’s full-year revenue guidance of $2.22 billion at the midpoint came in 6.1% above analysts’ estimates. Its GAAP loss of $0.64 per share was 74.5% below analysts’ consensus estimates.

Natera (NTRA) Q3 CY2025 Highlights:

- Revenue: $592.2 million vs analyst estimates of $514.4 million (34.7% year-on-year growth, 15.1% beat)

- EPS (GAAP): -$0.64 vs analyst expectations of -$0.37 (74.5% miss)

- The company lifted its revenue guidance for the full year to $2.22 billion at the midpoint from $2.06 billion, a 7.8% increase

- Operating Margin: -16.5%, down from -8.9% in the same quarter last year

- Sales Volumes rose 21.4% year on year (28% in the same quarter last year)

- Market Capitalization: $27.44 billion

Company Overview

Founded in 2003 as Gene Security Network before rebranding in 2012, Natera (NASDAQ:NTRA) develops and commercializes genetic tests for prenatal screening, cancer detection, and organ transplant monitoring using its proprietary cell-free DNA technology.

Natera's technology platform combines molecular biology and computational techniques to analyze tiny amounts of DNA from blood samples, enabling non-invasive testing across its three main business segments: women's health, oncology, and organ health.

In women's health, Natera's flagship product is Panorama, a non-invasive prenatal test (NIPT) that screens for chromosomal abnormalities like Down syndrome and other genetic conditions as early as nine weeks into pregnancy. The company also offers Horizon, a carrier screening test that helps identify if prospective parents carry genetic variations that could cause inherited conditions in their children. Additional products include tests for hereditary cancer screening, preimplantation genetic testing for IVF, and miscarriage tissue analysis.

Natera's oncology portfolio is anchored by Signatera, a personalized blood test that detects molecular residual disease (MRD) and monitors for cancer recurrence. Unlike standard liquid biopsy panels that screen for generic mutations, Signatera creates a custom assay for each patient based on their tumor's unique mutational signature. This approach allows for earlier detection of residual disease than standard clinical or radiological methods, potentially enabling more timely treatment decisions. The company also offers Altera, a comprehensive genomic profiling test that helps identify potential treatment options based on a patient's tumor biomarkers.

In organ health, Natera's Prospera tests measure donor-derived cell-free DNA in transplant recipients' blood to assess rejection in kidney, heart, and lung transplants. This provides a non-invasive alternative to traditional biopsies. The company also offers Renasight, a genetic test for chronic kidney disease that helps identify underlying genetic causes.

Natera distributes its tests through both direct sales to healthcare providers and a network of over 100 laboratory and distribution partners worldwide. The company's cloud-based Constellation software platform enables partner laboratories to run Natera's molecular workflows locally while accessing its bioinformatics algorithms remotely, expanding the global reach of its technology.

4. Immuno-Oncology

Over the next few years, immuno-oncology companies, which harness the immune system to fight illnesses such as cancer, faces strong tailwinds from advancements in precision medicine (including the use of AI to improve hit rates) and growing demand for treatments targeting rare diseases. However, headwinds such as rising scrutiny over drug pricing, regulatory unknowns, and competition from larger, more resourced pharmaceutical companies could weigh on growth.

In women's health, Natera competes with Laboratory Corporation of America (LabCorp), Myriad Genetics, Quest Diagnostics, Illumina's Verinata, BillionToOne, and PerkinElmer. In oncology, its competitors include Guardant Health, NeoGenomics, Tempus Labs, Exact Sciences, and Personalis. In organ health, Natera's primary competitor is CareDx.

5. Revenue Scale

Larger companies benefit from economies of scale, where fixed costs like infrastructure, technology, and administration are spread over a higher volume of goods or services, reducing the cost per unit. Scale can also lead to bargaining power with suppliers, greater brand recognition, and more investment firepower. A virtuous cycle can ensue if a scaled company plays its cards right.

With just $2.12 billion in revenue over the past 12 months, Natera lacks scale in an industry where it matters. This makes it difficult to build trust with customers because healthcare is heavily regulated, complex, and resource-intensive. On the bright side, Natera’s smaller revenue base allows it to grow faster if it can execute well.

6. Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Thankfully, Natera’s 42.4% annualized revenue growth over the last five years was incredible. Its growth surpassed the average healthcare company and shows its offerings resonate with customers, a great starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within healthcare, a half-decade historical view may miss recent innovations or disruptive industry trends. Natera’s annualized revenue growth of 46.3% over the last two years is above its five-year trend, suggesting its demand was strong and recently accelerated.

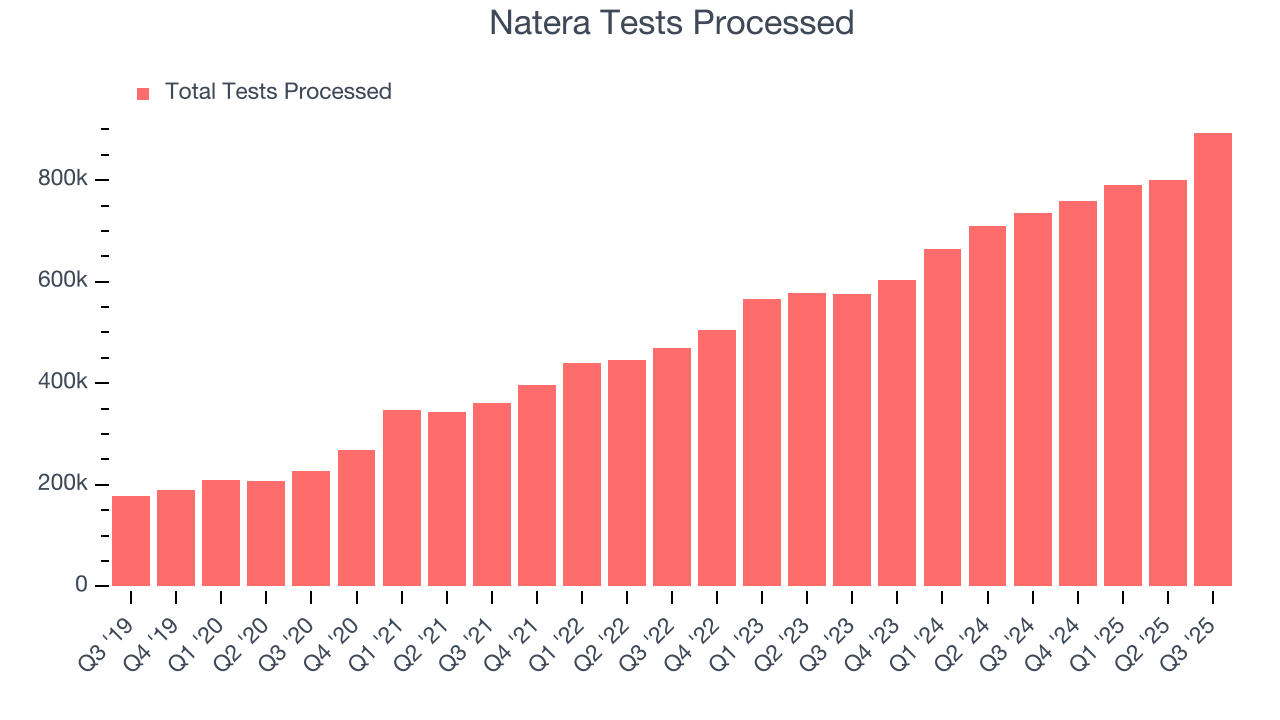

Natera also reports its number of tests processed, which reached 893,600 in the latest quarter. Over the last two years, Natera’s tests processed averaged 20.8% year-on-year growth. Because this number is lower than its revenue growth, we can see the company benefited from price increases.

This quarter, Natera reported wonderful year-on-year revenue growth of 34.7%, and its $592.2 million of revenue exceeded Wall Street’s estimates by 15.1%.

Looking ahead, sell-side analysts expect revenue to grow 9.1% over the next 12 months, a deceleration versus the last two years. Despite the slowdown, this projection is commendable and indicates the market sees success for its products and services.

7. Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

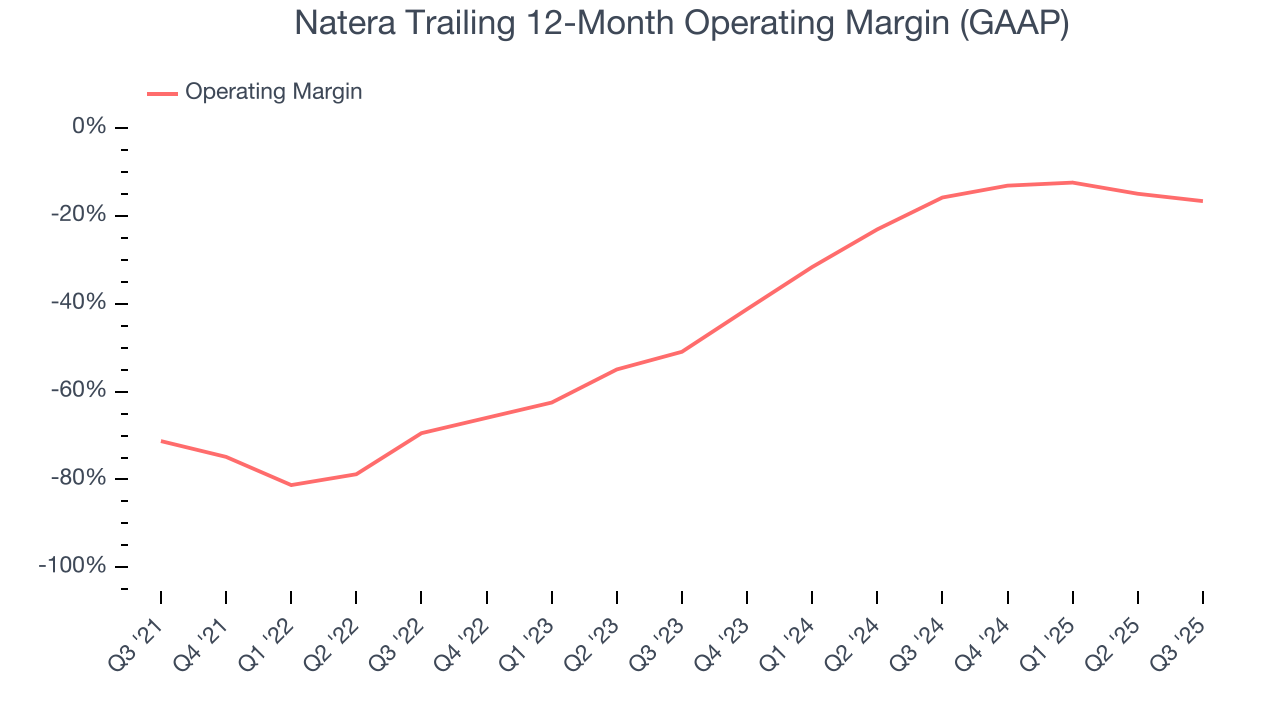

Natera’s high expenses have contributed to an average operating margin of negative 34.1% over the last five years. Unprofitable healthcare companies require extra attention because they could get caught swimming naked when the tide goes out.

On the plus side, Natera’s operating margin rose by 54.6 percentage points over the last five years, as its sales growth gave it operating leverage. Zooming in on its more recent performance, we can see the company’s trajectory is intact as its margin has also increased by 34.3 percentage points on a two-year basis. These data points are very encouraging and show momentum is on its side.

This quarter, Natera generated a negative 16.5% operating margin.

8. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

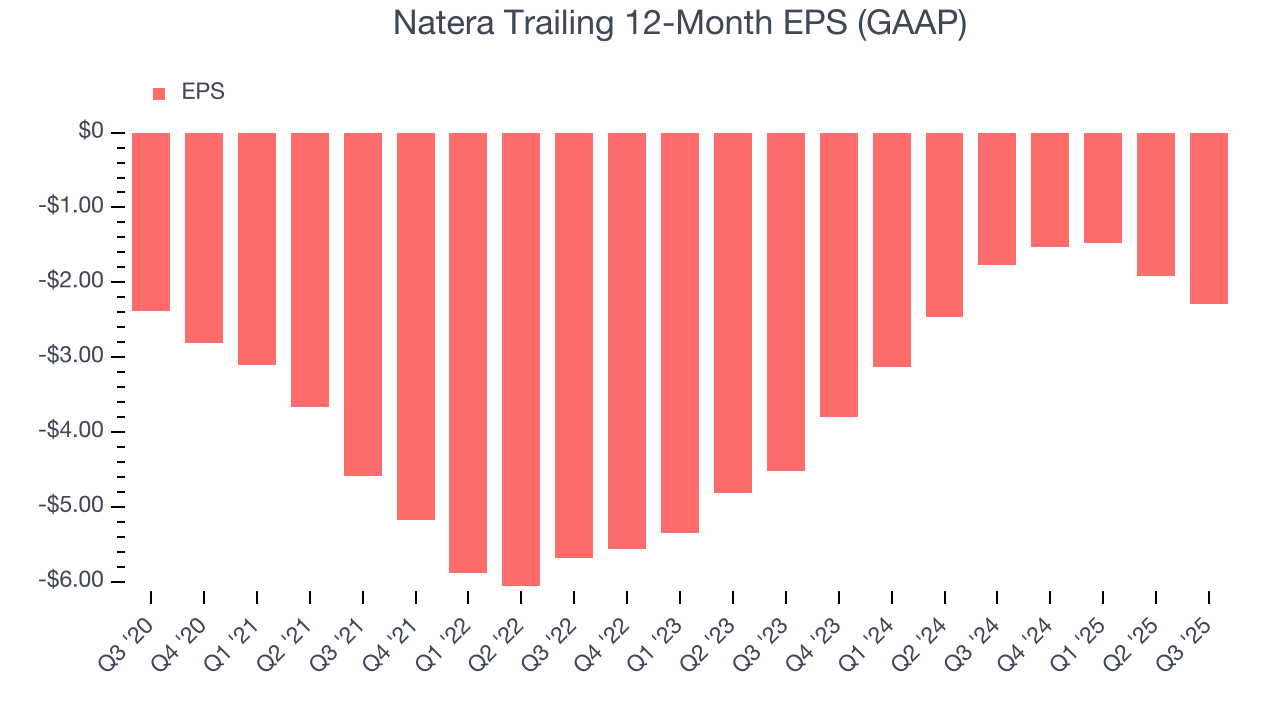

Natera’s full-year EPS was flat over the last five years. Its performance was underwhelming, but at least the company is doing well in other parts of the business.

In Q3, Natera reported EPS of negative $0.64, down from negative $0.26 in the same quarter last year. This print missed analysts’ estimates. Over the next 12 months, Wall Street expects Natera to improve its earnings losses. Analysts forecast its full-year EPS of negative $2.29 will advance to negative $1.20.

9. Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

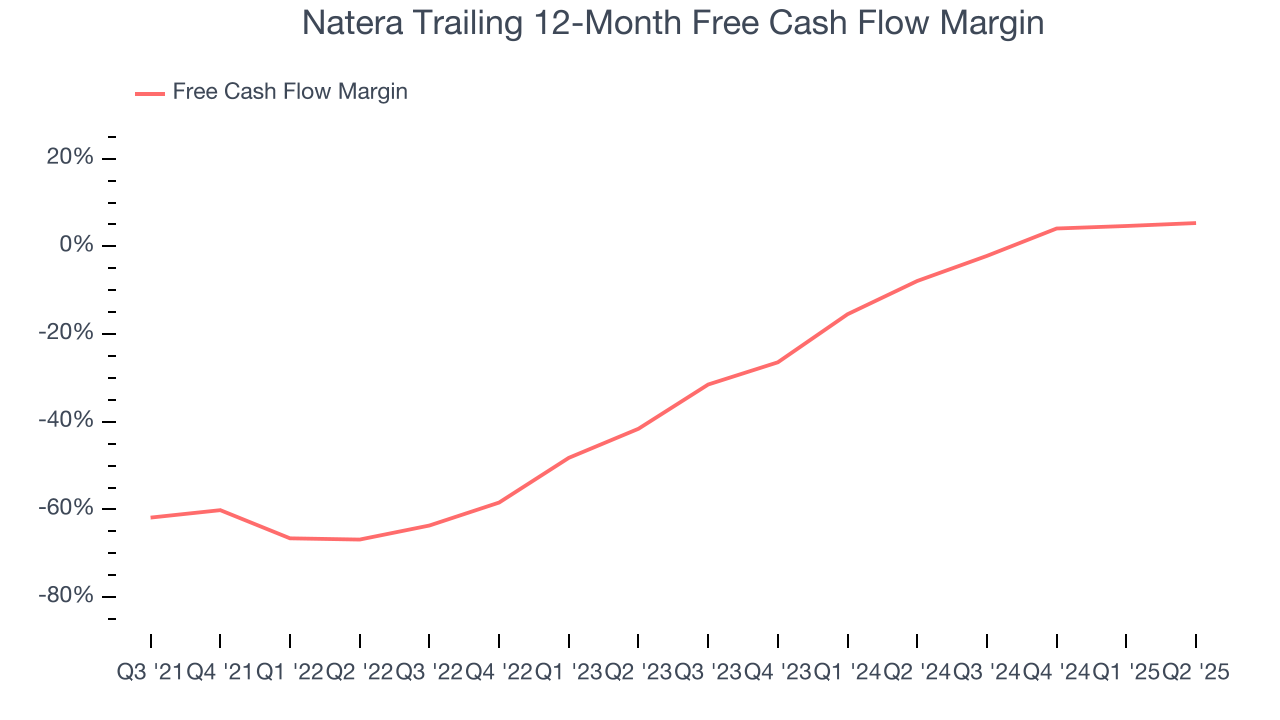

Natera’s demanding reinvestments have drained its resources over the last five years, putting it in a pinch and limiting its ability to return capital to investors. Its free cash flow margin averaged negative 20.8%, meaning it lit $20.77 of cash on fire for every $100 in revenue.

Taking a step back, an encouraging sign is that Natera’s margin expanded by 64.8 percentage points during that time. In light of its glaring cash burn, however, this improvement is a bucket of hot water in a cold ocean.

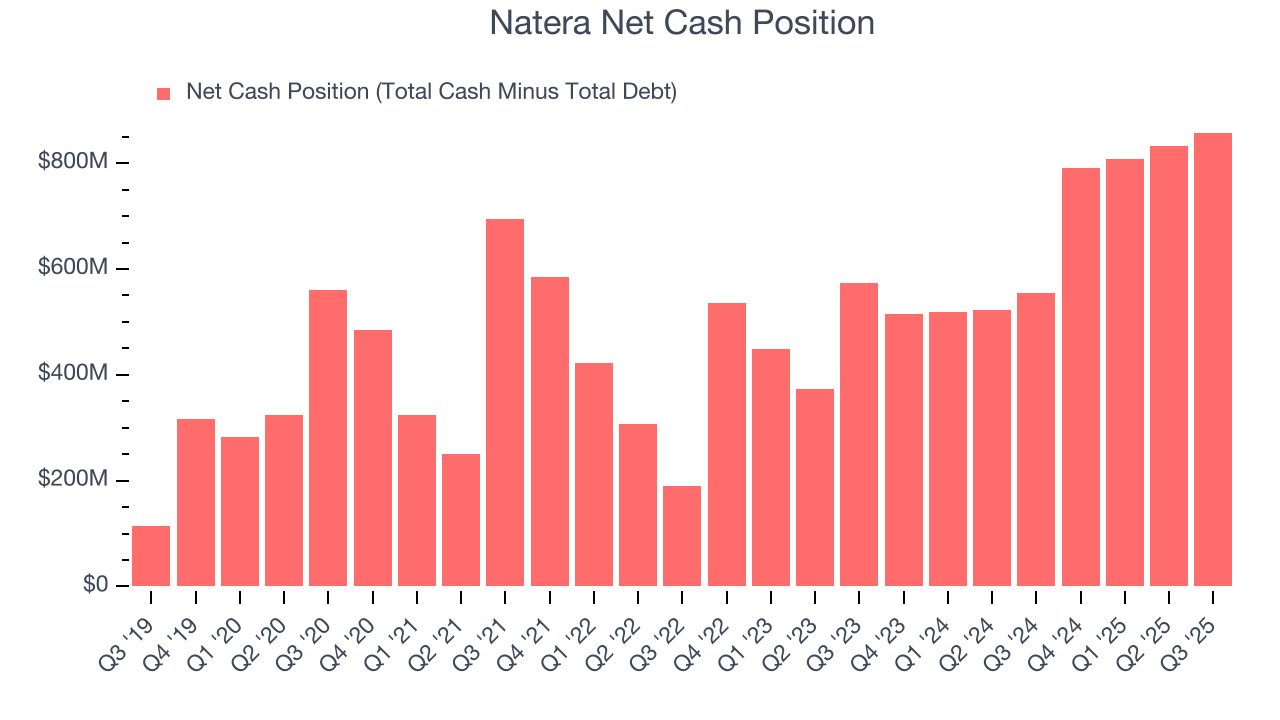

10. Balance Sheet Assessment

Companies with more cash than debt have lower bankruptcy risk.

Natera is a well-capitalized company with $1.04 billion of cash and $184.7 million of debt on its balance sheet. This $857.7 million net cash position is 3.1% of its market cap and gives it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

11. Key Takeaways from Natera’s Q3 Results

We were impressed by how significantly Natera blew past analysts’ revenue expectations this quarter. We were also glad its full-year revenue guidance trumped Wall Street’s estimates. On the other hand, its EPS missed. Overall, we think this was a decent quarter with some key metrics above expectations. The stock traded up 4.8% to $208 immediately after reporting.

12. Is Now The Time To Buy Natera?

Updated: March 13, 2026 at 11:25 PM EDT

We think that the latest earnings result is only one piece of the bigger puzzle. If you’re deciding whether to own Natera, you should also grasp the company’s longer-term business quality and valuation.

Natera is an amazing business ranking highly on our list. First of all, the company’s revenue growth was exceptional over the last five years. And while its operating margins reveal poor profitability compared to other healthcare companies, its rising cash profitability gives it more optionality. Additionally, Natera’s expanding adjusted operating margin shows the business has become more efficient.

Natera’s forward price-to-sales ratio is 10.3x. Looking at the healthcare landscape today, Natera’s qualities really stand out, and we like it at this price.

Wall Street analysts have a consensus one-year price target of $260.65 on the company (compared to the current share price of $186.11), implying they see 40.1% upside in buying Natera in the short term.