Oaktree Specialty Lending (OCSL)

We wouldn’t buy Oaktree Specialty Lending. Its poor returns on capital indicate it barely generated any profits, a must for high-quality companies.― StockStory Analyst Team

1. News

2. Summary

Why We Think Oaktree Specialty Lending Will Underperform

Managed by Oaktree Capital Management, one of the world's premier alternative investment firms, Oaktree Specialty Lending (NASDAQ:OCSL) is a business development company that provides customized financing solutions to mid-market companies across various industries.

- Products and services are facing significant end-market challenges during this cycle as sales have declined by 12.4% annually over the last two years

- Performance over the past two years shows each sale was less profitable as its earnings per share dropped by 18.1% annually, worse than its revenue

- Products and services are facing significant credit quality challenges during this cycle as tangible book value per share has declined by 4.5% annually over the last five years

Oaktree Specialty Lending doesn’t satisfy our quality benchmarks. We’ve identified better opportunities elsewhere.

Why There Are Better Opportunities Than Oaktree Specialty Lending

At $11.37 per share, Oaktree Specialty Lending trades at 7.6x forward P/E. Oaktree Specialty Lending’s valuation may seem like a great deal, but we think there are valid reasons why it’s so cheap.

We’d rather pay up for companies with elite fundamentals than get a bargain on weak ones. Cheap stocks can be value traps, and as their performance deteriorates, they will stay cheap or get even cheaper.

3. Oaktree Specialty Lending (OCSL) Research Report: Q4 CY2025 Update

Business development company Oaktree Specialty Lending (NASDAQ:OCSL) met Wall Streets revenue expectations in Q4 CY2025, but sales fell by 13.3% year on year to $75.1 million. Its non-GAAP profit of $0.06 per share was 84.1% below analysts’ consensus estimates.

Oaktree Specialty Lending (OCSL) Q4 CY2025 Highlights:

- Assets Under Management: $2.95 billion vs analyst estimates of $2.9 billion (4% year-on-year growth, 1.7% beat)

- Revenue: $75.1 million vs analyst estimates of $75.19 million (13.3% year-on-year decline, in line)

- Pre-tax Profit: $36.72 million (48.9% margin)

- Adjusted EPS: $0.06 vs analyst expectations of $0.38 (84.1% miss)

- Market Capitalization: $1.07 billion

Company Overview

Managed by Oaktree Capital Management, one of the world's premier alternative investment firms, Oaktree Specialty Lending (NASDAQ:OCSL) is a business development company that provides customized financing solutions to mid-market companies across various industries.

As a business development company (BDC), Oaktree Specialty Lending operates under regulations that require it to distribute at least 90% of its taxable income to shareholders. The company primarily focuses on providing debt financing to established middle-market companies, typically with annual EBITDA between $10 million and $250 million. These loans generally range from $5 million to $75 million, filling a crucial financing gap for businesses that may be too large for traditional bank loans but too small for public debt offerings.

The company's investment portfolio spans multiple sectors including software, healthcare, financial services, and manufacturing. A typical transaction might involve providing growth capital to a healthcare technology company expanding its operations, or financing for a manufacturing business making strategic acquisitions. Oaktree employs a rigorous due diligence process, analyzing potential borrowers' financial health, competitive positioning, and growth prospects before extending credit.

Oaktree Specialty Lending generates revenue primarily through interest income on its debt investments, which often feature floating rates that can adjust with market conditions. The company also occasionally takes equity positions in portfolio companies, which can provide additional returns through capital appreciation. As a publicly traded BDC, it offers retail investors access to private credit investments that would typically be available only to institutional investors. The company benefits from the extensive resources and expertise of its investment advisor, Oaktree Capital Management, which brings decades of experience in credit markets and distressed investing.

4. Specialty Finance

Specialty finance companies provide targeted lending or financial services for specific industries or needs. They benefit from expertise in particular sectors, often reduced competition in specialized niches, and tailored underwriting that can yield higher margins. Challenges include concentration risk in specific industries, difficulty achieving scale efficiencies, and potential vulnerability during sector-specific downturns affecting their specialized markets.

Oaktree Specialty Lending competes with other publicly traded business development companies including Ares Capital Corporation (NASDAQ:ARCC), FS KKR Capital Corp. (NYSE:FSK), and Main Street Capital Corporation (NYSE:MAIN), as well as private credit funds managed by large asset managers.

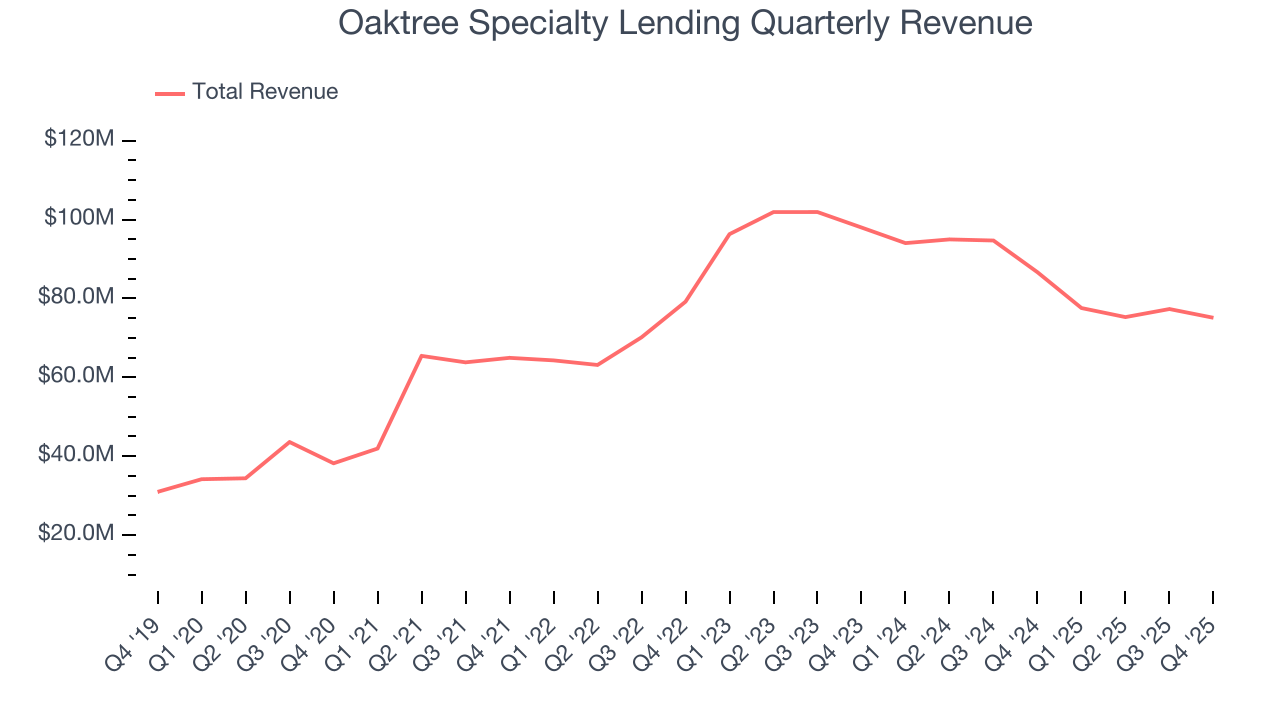

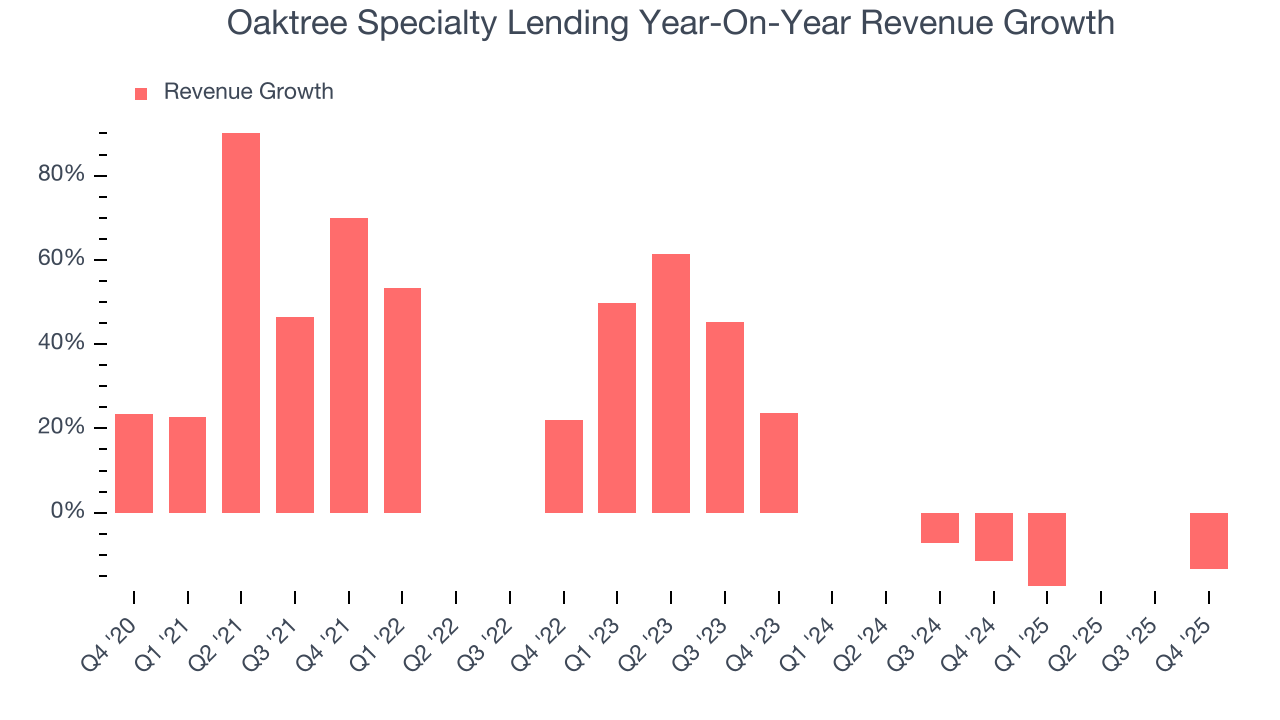

5. Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Luckily, Oaktree Specialty Lending’s revenue grew at an impressive 15.2% compounded annual growth rate over the last five years. Its growth beat the average financials company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within financials, a half-decade historical view may miss recent interest rate changes, market returns, and industry trends. Oaktree Specialty Lending’s recent performance marks a sharp pivot from its five-year trend as its revenue has shown annualized declines of 12.4% over the last two years.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, Oaktree Specialty Lending reported a rather uninspiring 13.3% year-on-year revenue decline to $75.1 million of revenue, in line with Wall Street’s estimates.

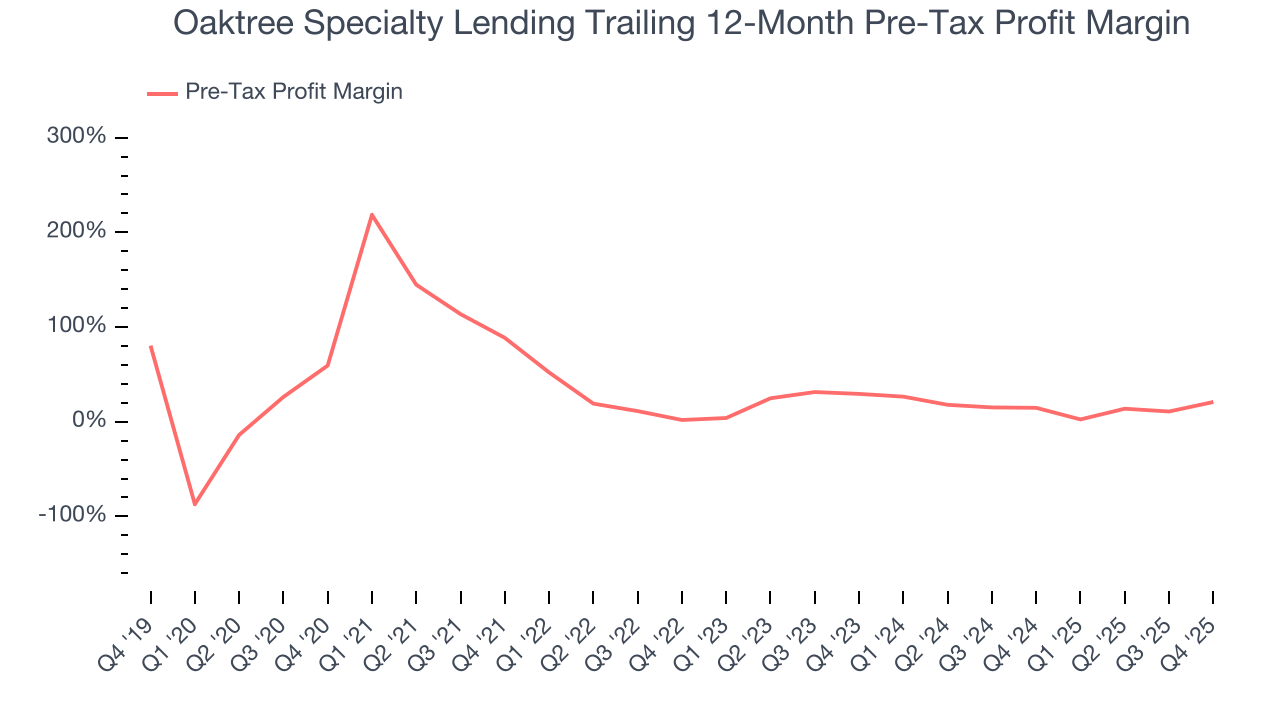

6. Pre-Tax Profit Margin

Revenue growth is one major determinant of business quality, and the efficiency of operations is another. For Specialty Finance companies, we look at pre-tax profit rather than the operating margin that defines sectors such as consumer, tech, and industrials.

Interest income and expenses play a big role in financial institutions' profitability, so they should be factored into the definition of profit. Taxes, however, should not as they are largely out of a company's control. This is pre-tax profit by definition.

Over the last five years, Oaktree Specialty Lending’s pre-tax profit margin has risen by 38.5 percentage points, going from 88.6% to 20.9%. It has also declined by 8.6 percentage points on a two-year basis, showing its expenses have consistently increased at a faster rate than revenue. This usually raises questions unless the company is in high-growth mode and reinvesting its profits into attractive ventures.

In Q4, Oaktree Specialty Lending’s pre-tax profit margin was 48.9%. This result was 40.4 percentage points better than the same quarter last year.

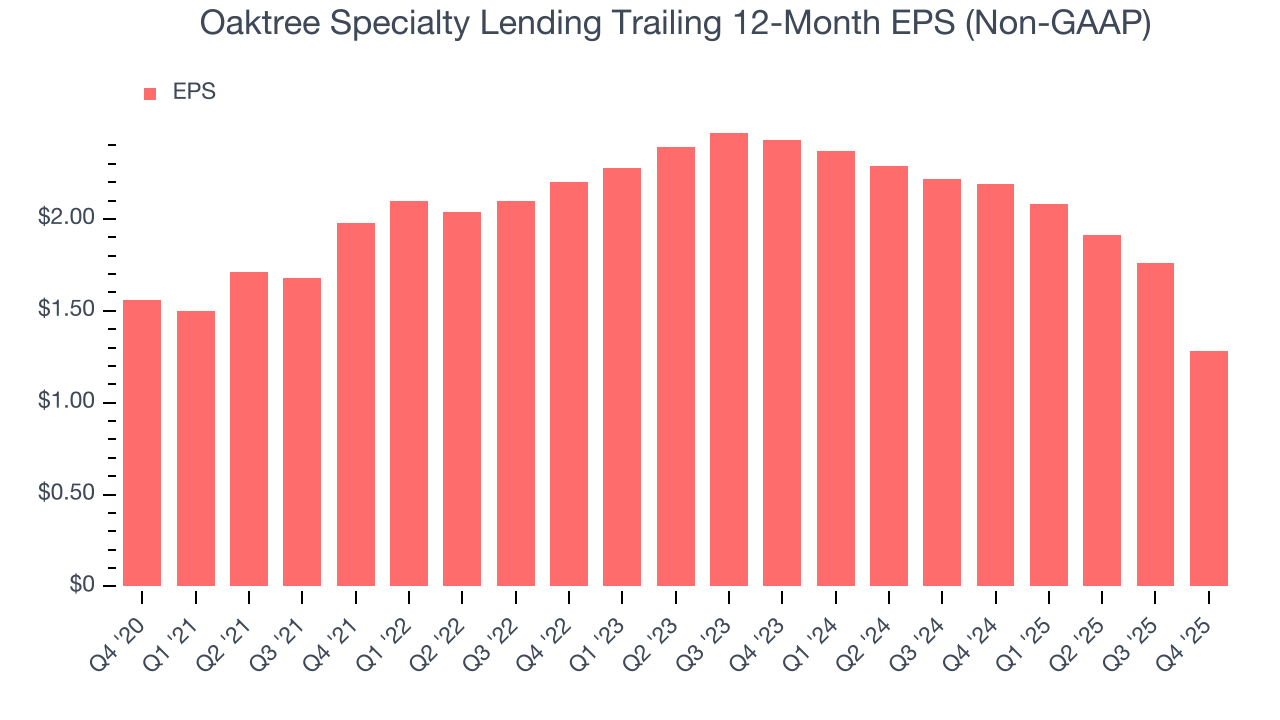

7. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Sadly for Oaktree Specialty Lending, its EPS declined by 3.9% annually over the last five years while its revenue grew by 15.2%. This tells us the company became less profitable on a per-share basis as it expanded.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Oaktree Specialty Lending, its two-year annual EPS declines of 27.4% show it’s continued to underperform. These results were bad no matter how you slice the data.

In Q4, Oaktree Specialty Lending reported adjusted EPS of $0.06, down from $0.54 in the same quarter last year. This print missed analysts’ estimates. Over the next 12 months, Wall Street expects Oaktree Specialty Lending’s full-year EPS of $1.28 to grow 17.4%.

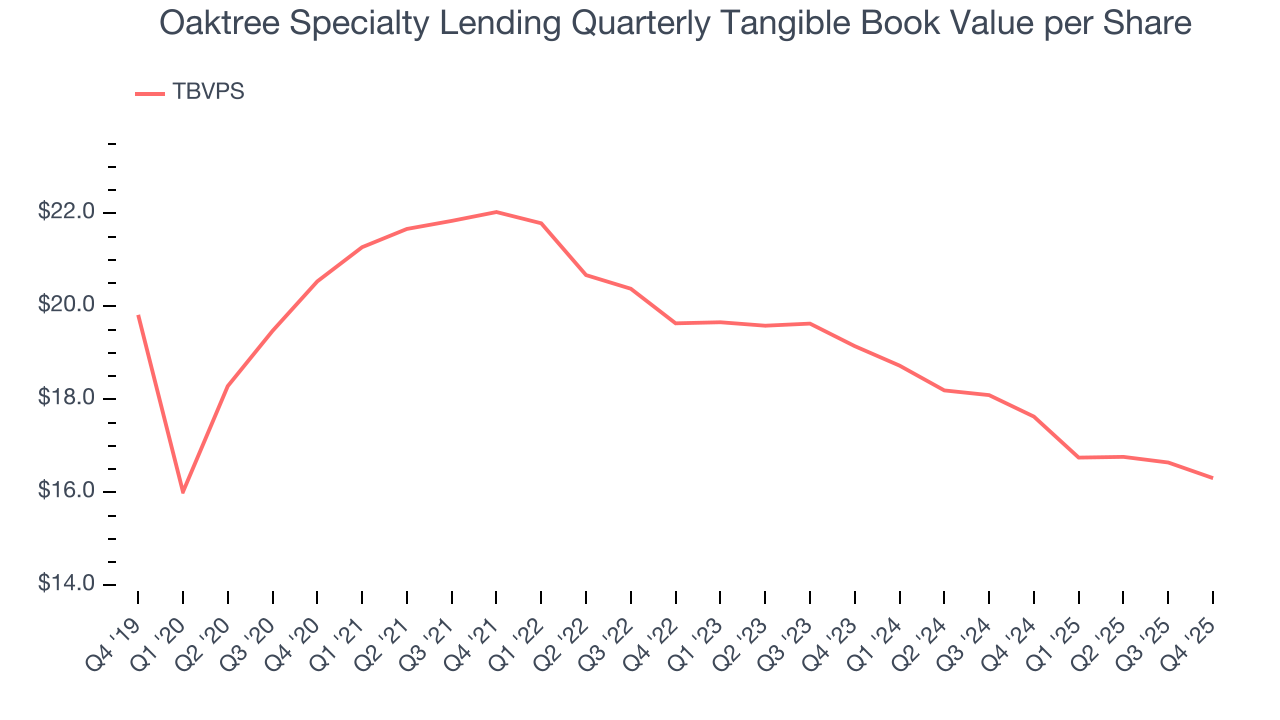

8. Tangible Book Value Per Share (TBVPS)

Financial institutions with multiple business lines manage complex balance sheets that span various financial activities. Market valuations reflect this operational complexity, prioritizing balance sheet strength and sustainable book value growth across all business segments.

This is why we consider tangible book value per share (TBVPS) an important metric for the sector. TBVPS represents the real net worth per share across all business segments, providing a clear measure of shareholder equity regardless of the complexity of operations. Other (and more commonly known) per-share metrics like EPS can sometimes be murky due to the complexity of multiple business lines, M&A activity, or accounting rules that vary across different financial services segments.

Oaktree Specialty Lending’s TBVPS declined at a 4.5% annual clip over the last five years. A turnaround doesn’t seem to be in sight as its TBVPS also dropped by 7.7% annually over the last two years ($19.14 to $16.30 per share).

9. Return on Equity

Return on equity, or ROE, tells us how much profit a company generates for each dollar of shareholder equity, a key funding source for banks. Over a long period, banks with high ROE tend to compound shareholder wealth faster through retained earnings, buybacks, and dividends.

Over the last five years, Oaktree Specialty Lending has averaged an ROE of 6.5%, uninspiring for a company operating in a sector where the average shakes out around 10%.

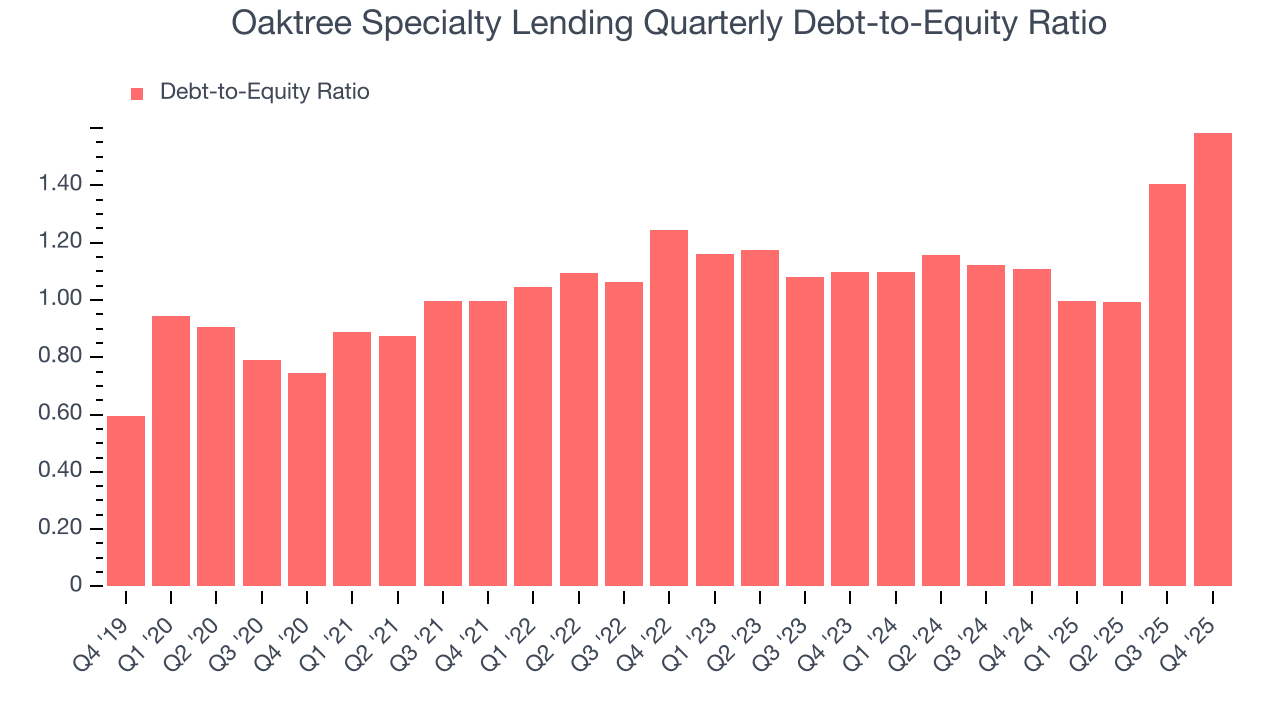

10. Balance Sheet Assessment

The debt-to-equity ratio is a widely used measure to assess a company's balance sheet health. A higher ratio means that a business aggressively financed its growth with debt. This can result in higher earnings (if the borrowed funds are invested profitably) but also increases risk.

If debt levels are too high, there could be difficulties in meeting obligations, especially during economic downturns or periods of rising interest rates if the debt has variable-rate payments.

Oaktree Specialty Lending currently has $2.28 billion of debt and $1.44 billion of shareholder's equity on its balance sheet, and over the past four quarters, has averaged a debt-to-equity ratio of 1.2×. We think this is safe and raises no red flags. In general, we’re comfortable with any ratio below 3.5× for a financials business.

11. Key Takeaways from Oaktree Specialty Lending’s Q4 Results

It was encouraging to see Oaktree Specialty Lending beat analysts’ AUM expectations this quarter. On the other hand, its EPS missed. Overall, this quarter could have been better. The stock remained flat at $12.12 immediately after reporting.

12. Is Now The Time To Buy Oaktree Specialty Lending?

Updated: March 14, 2026 at 1:06 AM EDT

Before investing in or passing on Oaktree Specialty Lending, we urge you to understand the company’s business quality (or lack thereof), valuation, and the latest quarterly results - in that order.

We see the value of companies driving economic growth, but in the case of Oaktree Specialty Lending, we’re out. Although its revenue growth was impressive over the last five years, it’s expected to deteriorate over the next 12 months and its declining pre-tax profit margin shows the business has become less efficient. On top of that, the company’s TBVPS has declined over the last five years.

Oaktree Specialty Lending’s P/E ratio based on the next 12 months is 7.6x. While this valuation is optically cheap, the potential downside is huge given its shaky fundamentals. There are better investments elsewhere.

Wall Street analysts have a consensus one-year price target of $12.77 on the company (compared to the current share price of $11.37).