Old Dominion Freight Line (ODFL)

We’re cautious of Old Dominion Freight Line. Its poor sales growth and falling returns on capital suggest its growth opportunities are shrinking.― StockStory Analyst Team

1. News

2. Summary

Why We Think Old Dominion Freight Line Will Underperform

With its name deriving from the Commonwealth of Virginia’s nickname, Old Dominion (NASDAQ:ODFL) delivers less-than-truckload (LTL) and full-container load freight.

- Projected sales growth of 1.3% for the next 12 months suggests sluggish demand

- Annual revenue growth of 6.5% over the last five years was below our standards for the industrials sector

- On the bright side, its healthy operating margin shows it’s a well-run company with efficient processes

Old Dominion Freight Line’s quality is lacking. We’d rather invest in businesses with stronger moats.

Why There Are Better Opportunities Than Old Dominion Freight Line

At $176.61 per share, Old Dominion Freight Line trades at 35.4x forward P/E. This multiple is higher than that of industrials peers; it’s also rich for the top-line growth of the company. Not a great combination.

There are stocks out there similarly priced with better business quality. We prefer owning these.

3. Old Dominion Freight Line (ODFL) Research Report: Q4 CY2025 Update

Freight carrier Old Dominion (NASDAQ:ODFL) met Wall Streets revenue expectations in Q4 CY2025, but sales fell by 5.7% year on year to $1.31 billion. Its GAAP profit of $1.09 per share was 2.9% above analysts’ consensus estimates.

Old Dominion Freight Line (ODFL) Q4 CY2025 Highlights:

- Revenue: $1.31 billion vs analyst estimates of $1.30 billion (5.7% year-on-year decline, in line)

- EPS (GAAP): $1.09 vs analyst estimates of $1.06 (2.9% beat)

- Adjusted EBITDA: $396.9 million vs analyst estimates of $388.2 million (30.4% margin, 2.2% beat)

- Operating Margin: 23.3%, in line with the same quarter last year

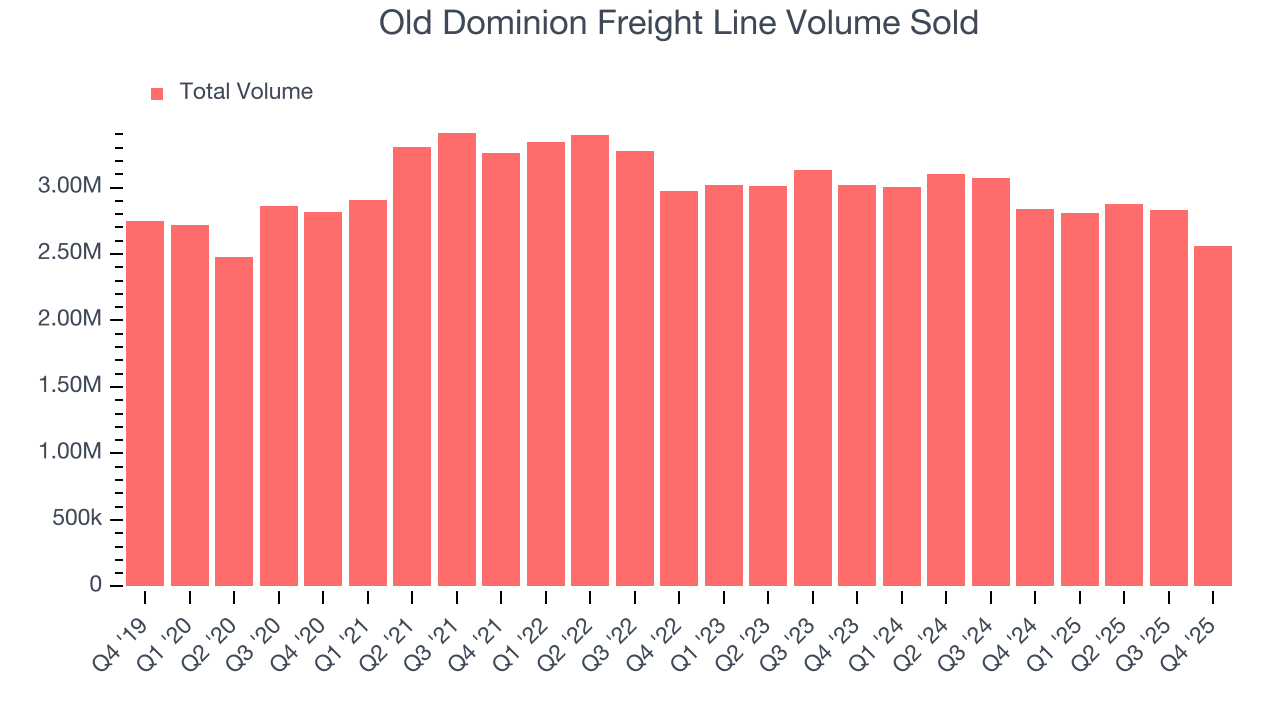

- Sales Volumes fell 9.7% year on year (-6.1% in the same quarter last year)

- Market Capitalization: $39.68 billion

Company Overview

With its name deriving from the Commonwealth of Virginia’s nickname, Old Dominion (NASDAQ:ODFL) delivers less-than-truckload (LTL) and full-container load freight.

Old Dominion was founded in 1934 as a single truck operation focusing on interstate freight throughout Virginia. Since its inception, the company has primarily expanded organically to increase its fleet and number of facilities. The company has continued to invest billions of dollars into service centers, vehicles, and information systems.

Old Dominion provides delivery services for businesses across various industries, facilitating the movement of products from distribution centers to retail stores or directly to customers' homes. The company offers full truckload deliveries, where entire truck trailers are dedicated to a single customer's shipment. This includes dry van services for standard cargo such as boxed goods and equipment, as well as refrigerated services for perishable items requiring temperature control during transport. Additionally, Old Dominion offers less-than-truckload (LTL) services, which involve consolidating smaller shipments from multiple customers into a single truck.

In terms of sales and contracts, Old Dominion engages in agreements with customers. These contracts often involve negotiated pricing based on factors such as shipment volume, frequency of shipments, and the specific transportation lanes required.

4. Ground Transportation

The growth of e-commerce and global trade continues to drive demand for shipping services, especially last-mile delivery, presenting opportunities for ground transportation companies. The industry continues to invest in data, analytics, and autonomous fleets to optimize efficiency and find the most cost-effective routes. Despite the essential services this industry provides, ground transportation companies are still at the whim of economic cycles. Consumer spending, for example, can greatly impact the demand for these companies’ offerings while fuel costs can influence profit margins.

Competitors offering similar products include J.B. Hunt (NASDAQ:JBHT), Saia (NASDAQ:SAIA), and XPO (NYSE:XPO).

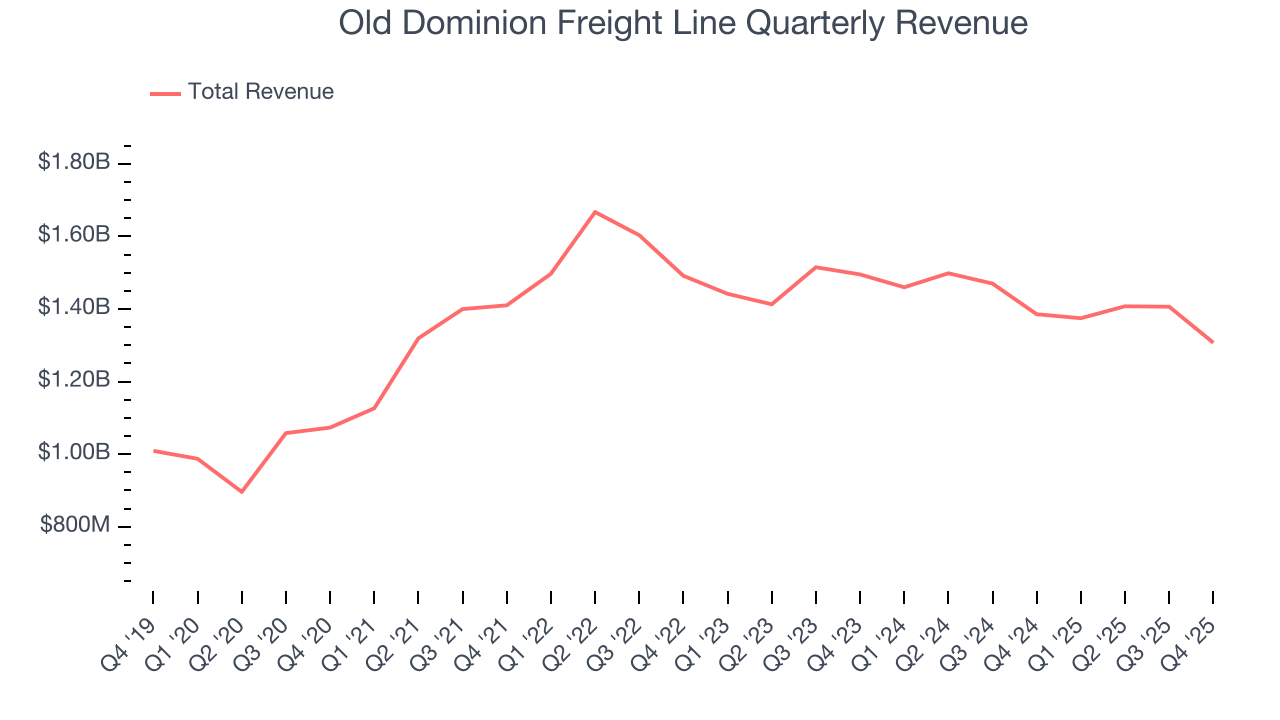

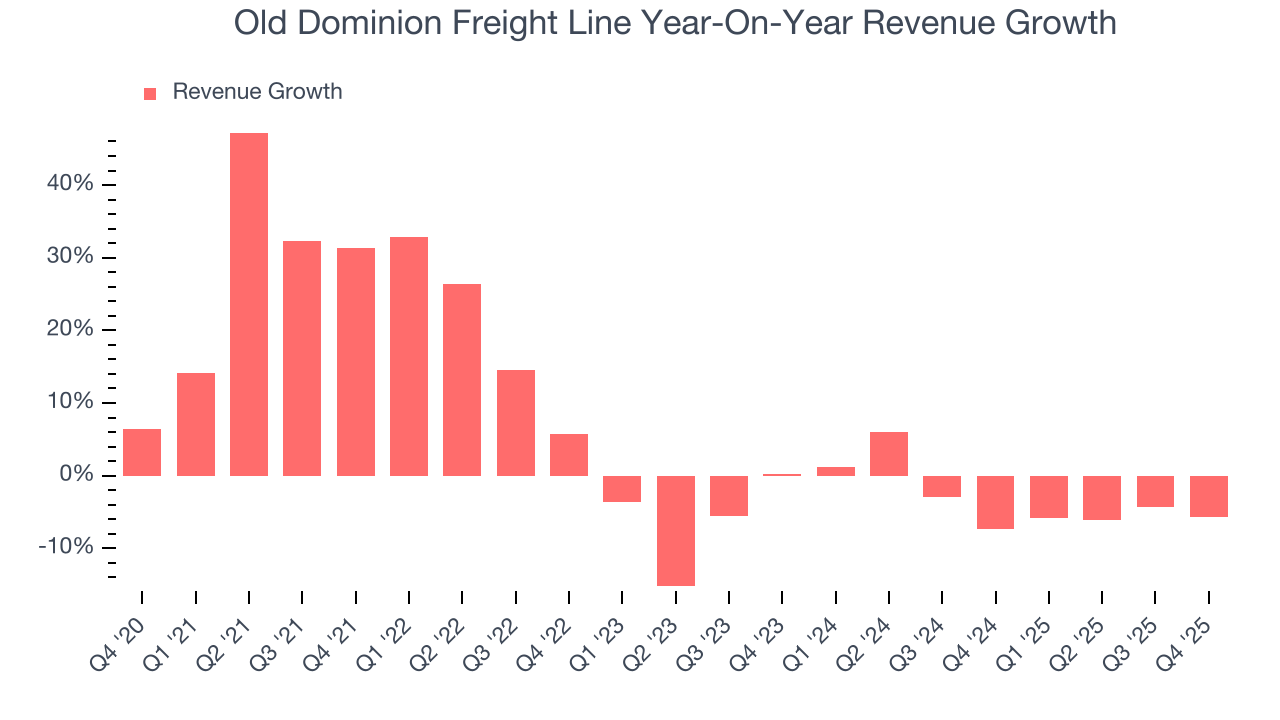

5. Revenue Growth

A company’s long-term performance is an indicator of its overall quality. Any business can have short-term success, but a top-tier one grows for years. Unfortunately, Old Dominion Freight Line’s 6.5% annualized revenue growth over the last five years was mediocre. This fell short of our benchmark for the industrials sector and is a rough starting point for our analysis.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. Old Dominion Freight Line’s performance shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 3.2% annually.

We can dig further into the company’s revenue dynamics by analyzing its number of units sold, which reached 2.56 million in the latest quarter. Over the last two years, Old Dominion Freight Line’s units sold averaged 4.6% year-on-year declines. Because this number is in line with its revenue growth, we can see the company kept its prices fairly consistent.

This quarter, Old Dominion Freight Line reported a rather uninspiring 5.7% year-on-year revenue decline to $1.31 billion of revenue, in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 1.8% over the next 12 months. Although this projection indicates its newer products and services will catalyze better top-line performance, it is still below average for the sector.

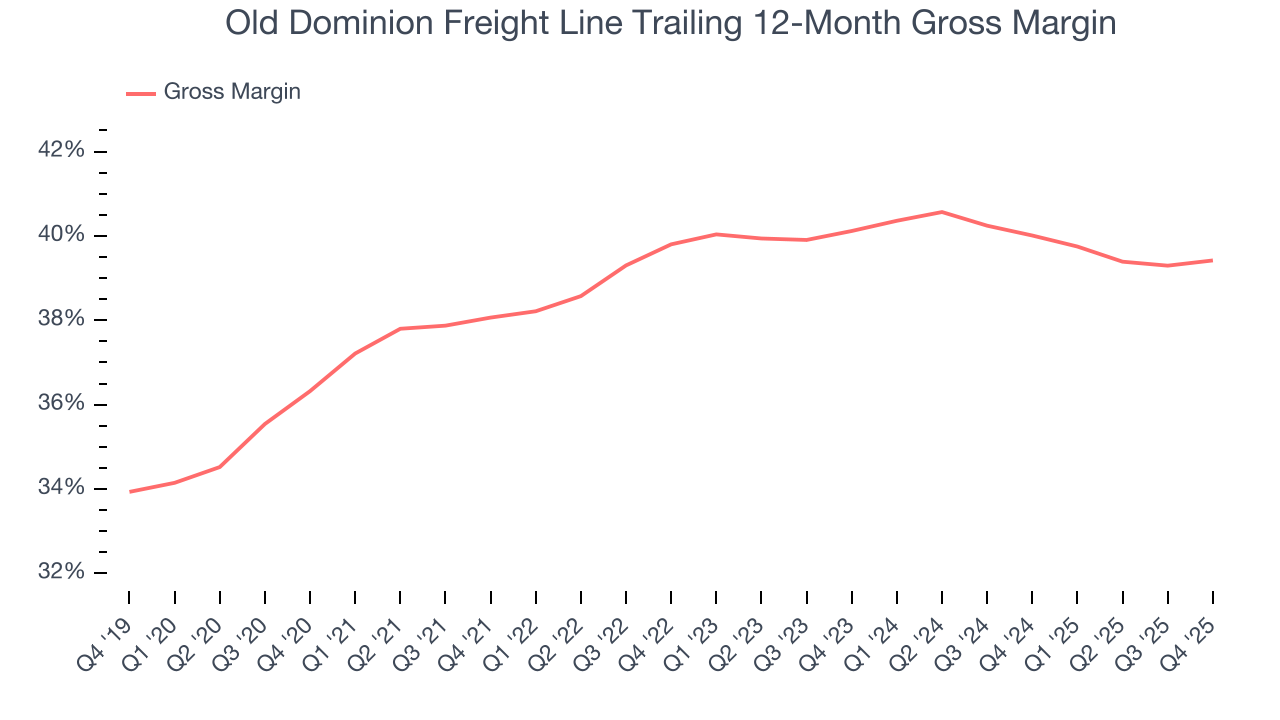

6. Gross Margin & Pricing Power

At StockStory, we prefer high gross margin businesses because they indicate the company has pricing power or differentiated products, giving it a chance to generate higher operating profits.

Old Dominion Freight Line’s unit economics are great compared to the broader industrials sector and signal that it enjoys product differentiation through quality or brand. As you can see below, it averaged an excellent 39.5% gross margin over the last five years. That means Old Dominion Freight Line only paid its suppliers $60.48 for every $100 in revenue.

In Q4, Old Dominion Freight Line produced a 39.9% gross profit margin, in line with the same quarter last year. On a wider time horizon, the company’s full-year margin has remained steady over the past four quarters, suggesting its input costs (such as raw materials and manufacturing expenses) have been stable and it isn’t under pressure to lower prices.

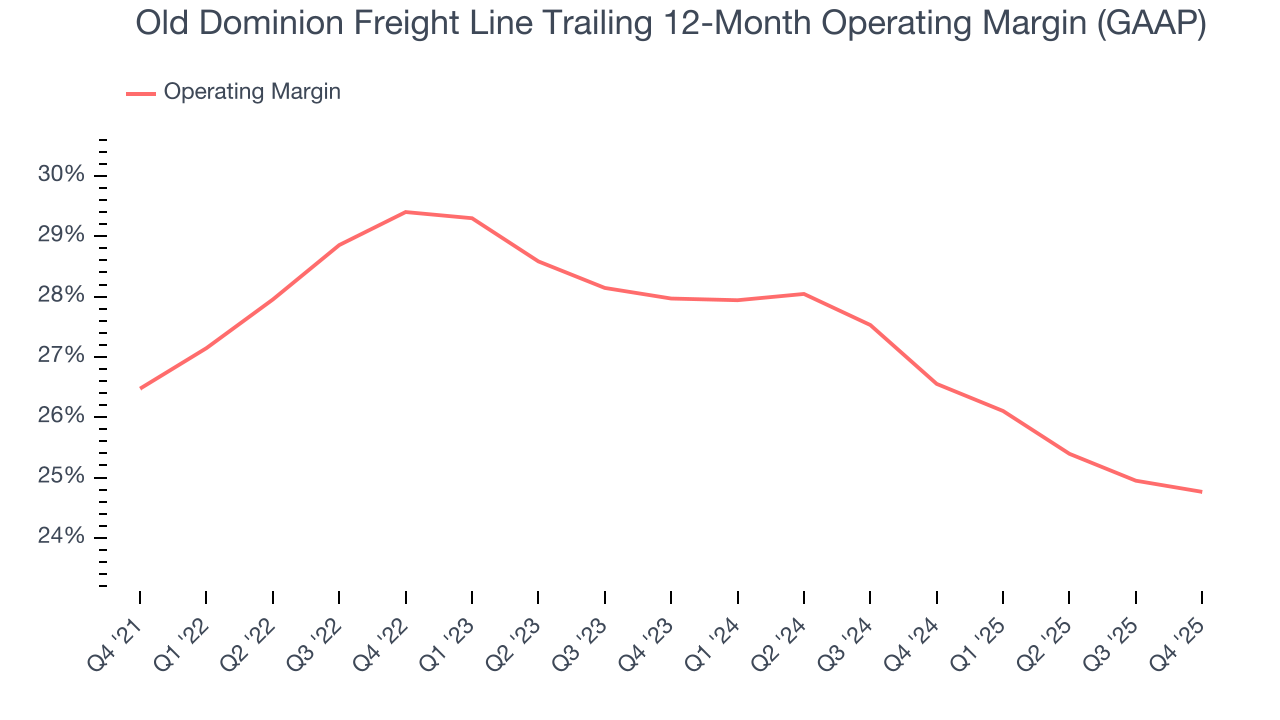

7. Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Old Dominion Freight Line has been a well-oiled machine over the last five years. It demonstrated elite profitability for an industrials business, boasting an average operating margin of 27.1%. This result isn’t surprising as its high gross margin gives it a favorable starting point.

Looking at the trend in its profitability, Old Dominion Freight Line’s operating margin decreased by 1.7 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

This quarter, Old Dominion Freight Line generated an operating margin profit margin of 23.3%, in line with the same quarter last year. This indicates the company’s cost structure has recently been stable.

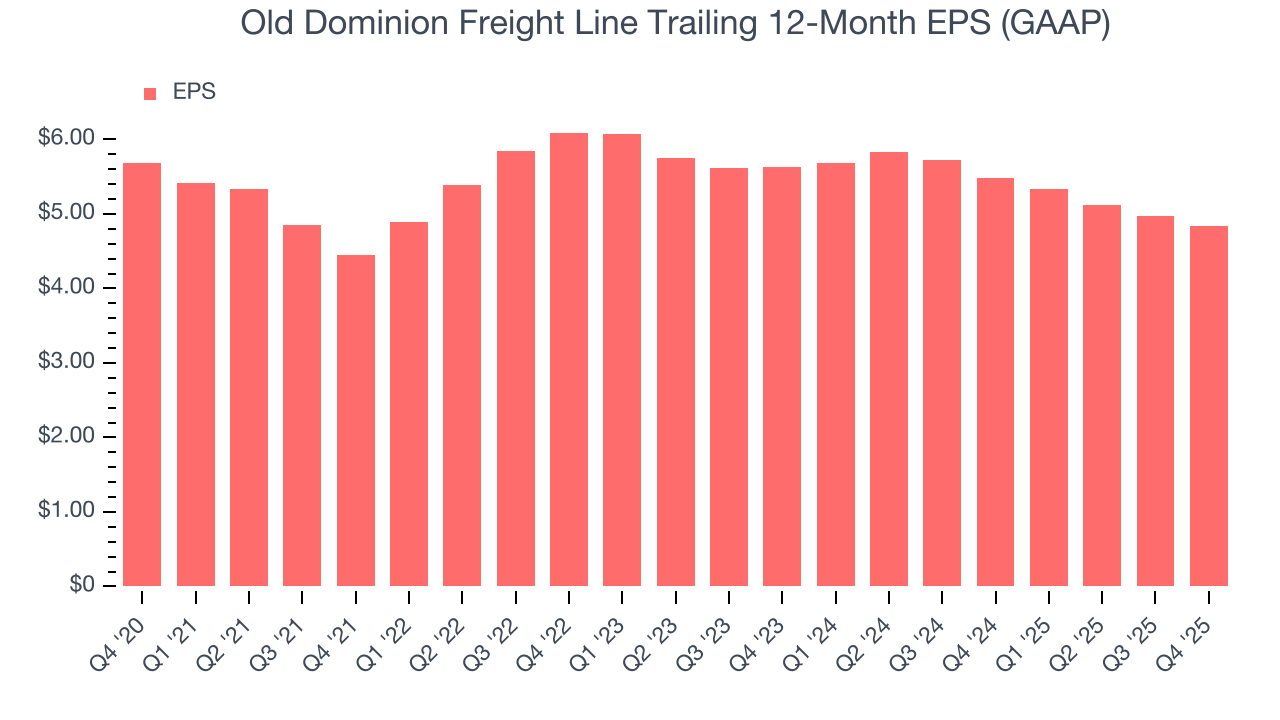

8. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Sadly for Old Dominion Freight Line, its EPS declined by 3.2% annually over the last five years while its revenue grew by 6.5%. This tells us the company became less profitable on a per-share basis as it expanded due to non-fundamental factors such as interest expenses and taxes.

Diving into the nuances of Old Dominion Freight Line’s earnings can give us a better understanding of its performance. As we mentioned earlier, Old Dominion Freight Line’s operating margin was flat this quarter but declined by 1.7 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its lower earnings; interest expenses and taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

Old Dominion Freight Line’s two-year annual EPS declines of 7.3% were bad and lower than its two-year revenue losses.

In Q4, Old Dominion Freight Line reported EPS of $1.09, down from $1.23 in the same quarter last year. Despite falling year on year, this print beat analysts’ estimates by 2.9%. Over the next 12 months, Wall Street expects Old Dominion Freight Line’s full-year EPS of $4.83 to grow 3.5%.

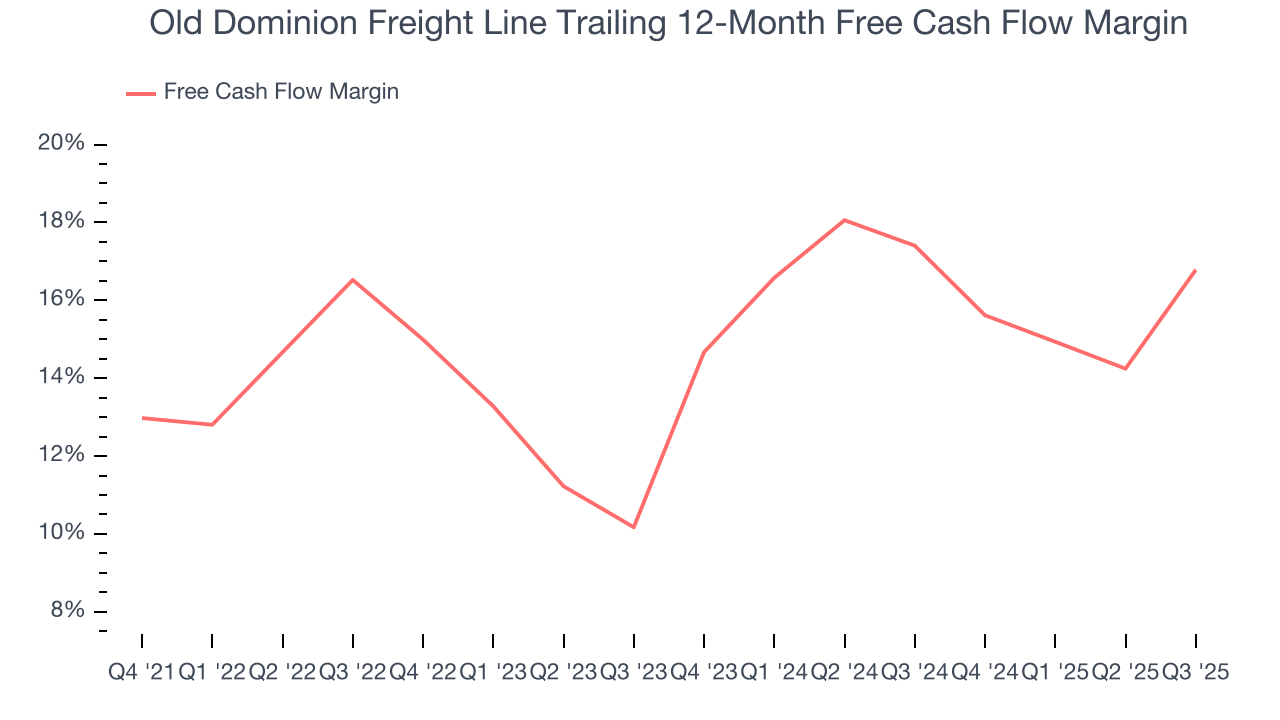

9. Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

Old Dominion Freight Line has shown terrific cash profitability, putting it in an advantageous position to invest in new products, return capital to investors, and consolidate the market during industry downturns. The company’s free cash flow margin was among the best in the industrials sector, averaging 14.9% over the last five years.

Taking a step back, we can see that Old Dominion Freight Line’s margin expanded by 3.6 percentage points during that time. This shows the company is heading in the right direction, and we can see it became a less capital-intensive business because its free cash flow profitability rose while its operating profitability fell.

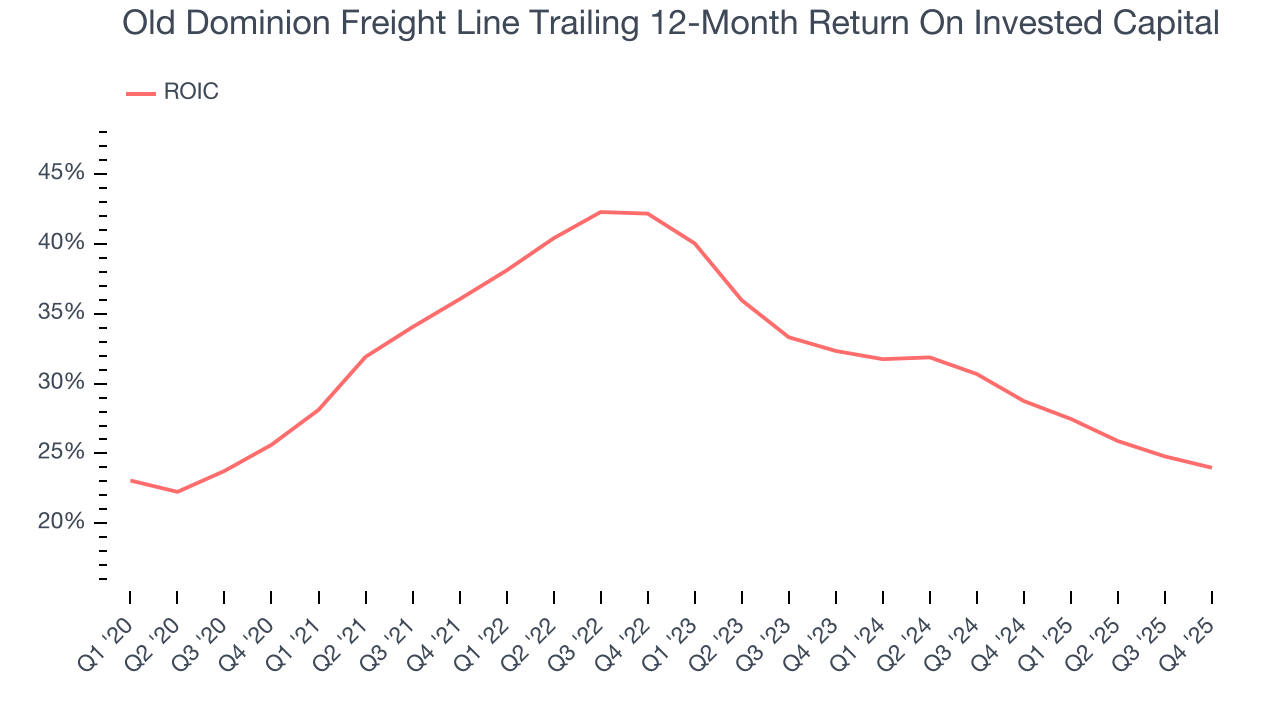

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Although Old Dominion Freight Line hasn’t been the highest-quality company lately because of its poor bottom-line (EPS) performance, it found a few growth initiatives in the past that worked out wonderfully. Its five-year average ROIC was 32.7%, splendid for an industrials business.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Over the last few years, Old Dominion Freight Line’s ROIC has unfortunately decreased significantly. We like what management has done in the past, but its declining returns are perhaps a symptom of fewer profitable growth opportunities.

11. Balance Sheet Assessment

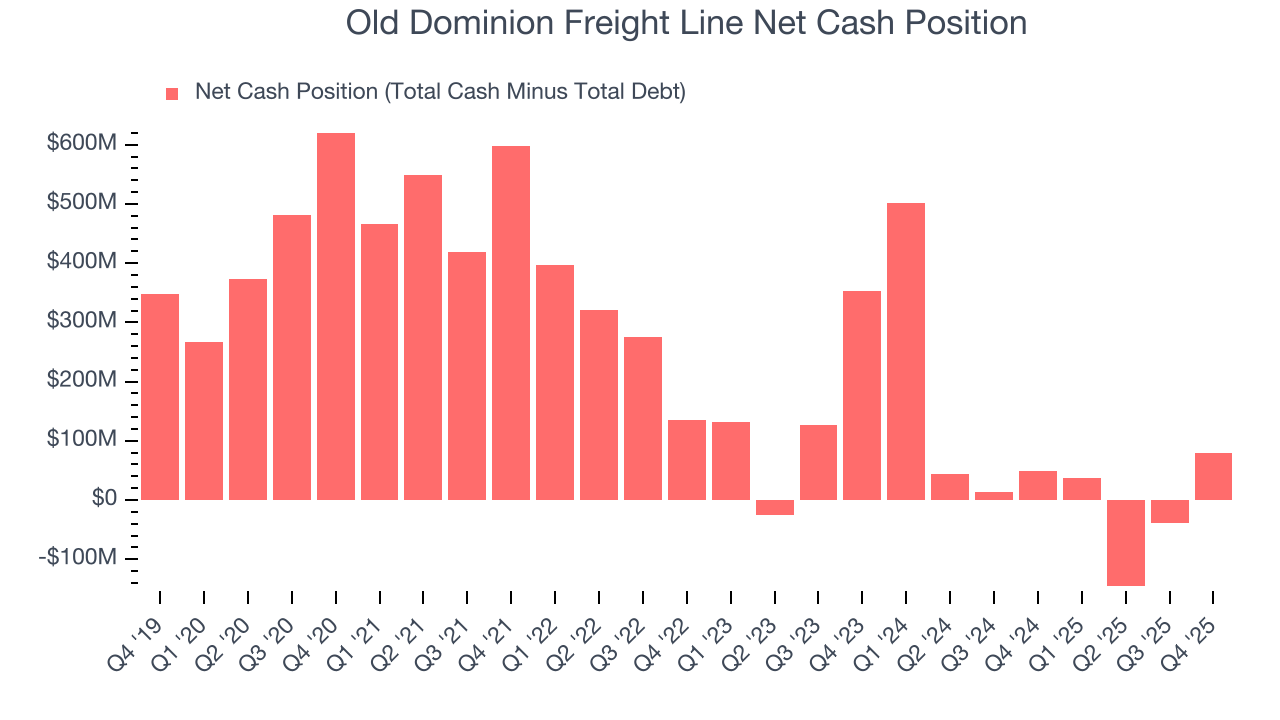

Businesses that maintain a cash surplus face reduced bankruptcy risk.

Old Dominion Freight Line is a profitable, well-capitalized company with $120.1 million of cash and $40 million of debt on its balance sheet. This $80.1 million net cash position gives it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

12. Key Takeaways from Old Dominion Freight Line’s Q4 Results

Revenue was in line, but EPS managed to beat. Overall, this print was fine. The stock remained flat at $189.78 immediately following the results.

13. Is Now The Time To Buy Old Dominion Freight Line?

Updated: March 14, 2026 at 11:33 PM EDT

When considering an investment in Old Dominion Freight Line, investors should account for its valuation and business qualities as well as what’s happened in the latest quarter.

Old Dominion Freight Line isn’t a terrible business, but it doesn’t pass our bar. First off, its revenue growth was mediocre over the last five years, and analysts expect its demand to deteriorate over the next 12 months. While its powerful free cash flow generation enables it to stay ahead of the competition through consistent reinvestment of profits, the downside is its diminishing returns show management's prior bets haven't worked out. On top of that, its unit sales declined.

Old Dominion Freight Line’s P/E ratio based on the next 12 months is 35.4x. This valuation tells us it’s a bit of a market darling with a lot of good news priced in - we think other companies feature superior fundamentals at the moment.

Wall Street analysts have a consensus one-year price target of $199.25 on the company (compared to the current share price of $176.61).