Omnicell (OMCL)

Omnicell faces an uphill battle. Its sales have underperformed and its low returns on capital show it has few growth opportunities.― StockStory Analyst Team

1. News

2. Summary

Why We Think Omnicell Will Underperform

Driven by the vision of an "Autonomous Pharmacy" with zero medication errors, Omnicell (NASDAQ:OMCL) provides medication management automation and adherence tools that help healthcare systems and pharmacies reduce errors and improve efficiency.

- Earnings per share fell by 8.6% annually over the last five years while its revenue grew, showing its incremental sales were much less profitable

- Revenue base of $1.18 billion puts it at a disadvantage compared to larger competitors exhibiting economies of scale

- Below-average returns on capital indicate management struggled to find compelling investment opportunities, and its falling returns suggest its earlier profit pools are drying up

Omnicell falls short of our quality standards. We’re hunting for superior stocks elsewhere.

Why There Are Better Opportunities Than Omnicell

Omnicell is trading at $40.28 per share, or 24x forward P/E. Not only is Omnicell’s multiple richer than most healthcare peers, but it’s also expensive for its revenue characteristics.

We’d rather invest in similarly-priced but higher-quality companies with more reliable earnings growth.

3. Omnicell (OMCL) Research Report: Q4 CY2025 Update

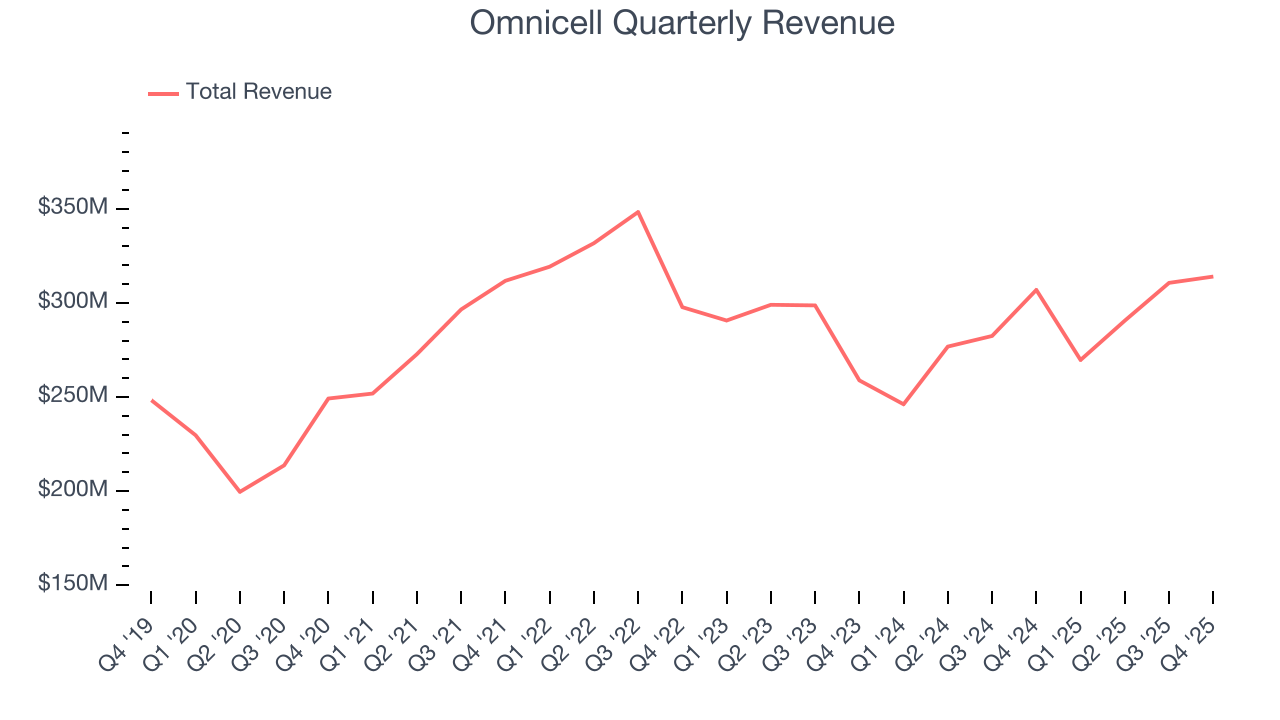

Healthcare tech company Omnicell (NASDAQ:OMCL) met Wall Street’s revenue expectations in Q4 CY2025, with sales up 2.3% year on year to $314 million. The company expects next quarter’s revenue to be around $305 million, coming in 8.2% above analysts’ estimates. Its non-GAAP profit of $0.40 per share was 19.4% below analysts’ consensus estimates.

Omnicell (OMCL) Q4 CY2025 Highlights:

- Revenue: $314 million vs analyst estimates of $314.2 million (2.3% year-on-year growth, in line)

- Adjusted EPS: $0.40 vs analyst expectations of $0.50 (19.4% miss)

- Adjusted EBITDA: $36.79 million vs analyst estimates of $41.13 million (11.7% margin, 10.5% miss)

- Revenue Guidance for Q1 CY2026 is $305 million at the midpoint, above analyst estimates of $281.8 million

- Adjusted EPS guidance for the upcoming financial year 2026 is $1.75 at the midpoint, missing analyst estimates by 7%

- EBITDA guidance for the upcoming financial year 2026 is $152.5 million at the midpoint, below analyst estimates of $158.2 million

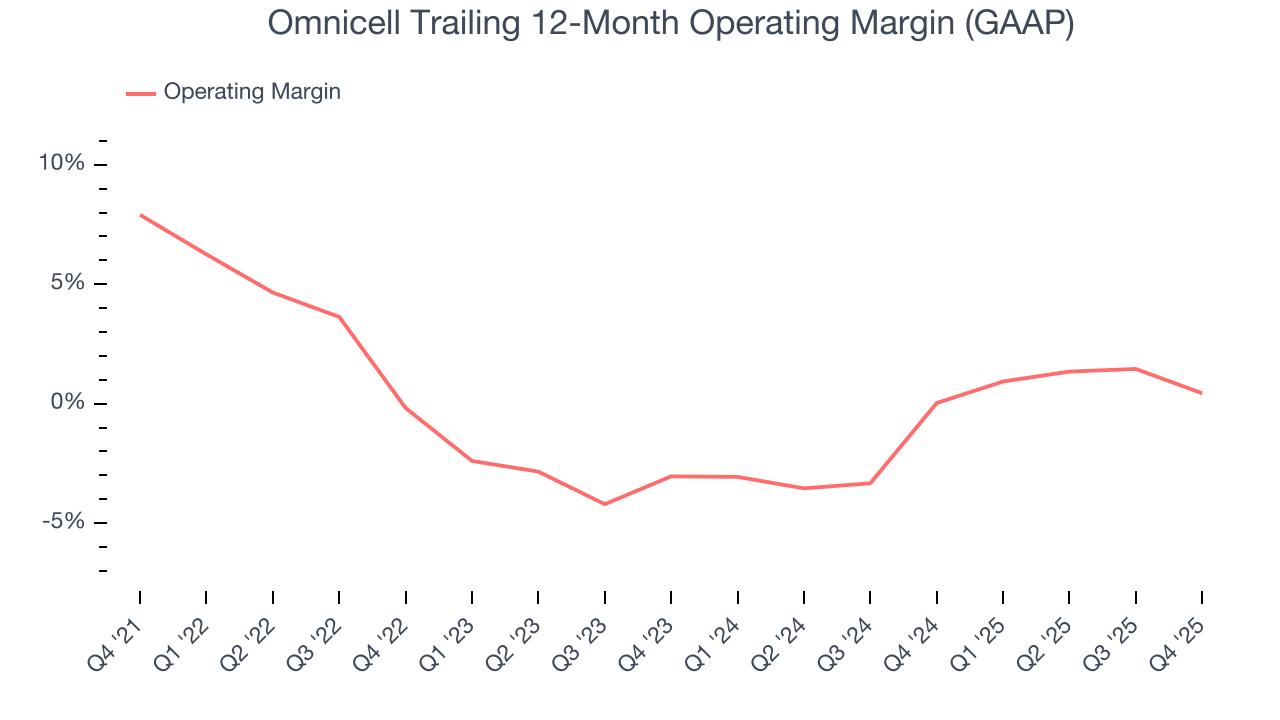

- Operating Margin: 0.1%, down from 4% in the same quarter last year

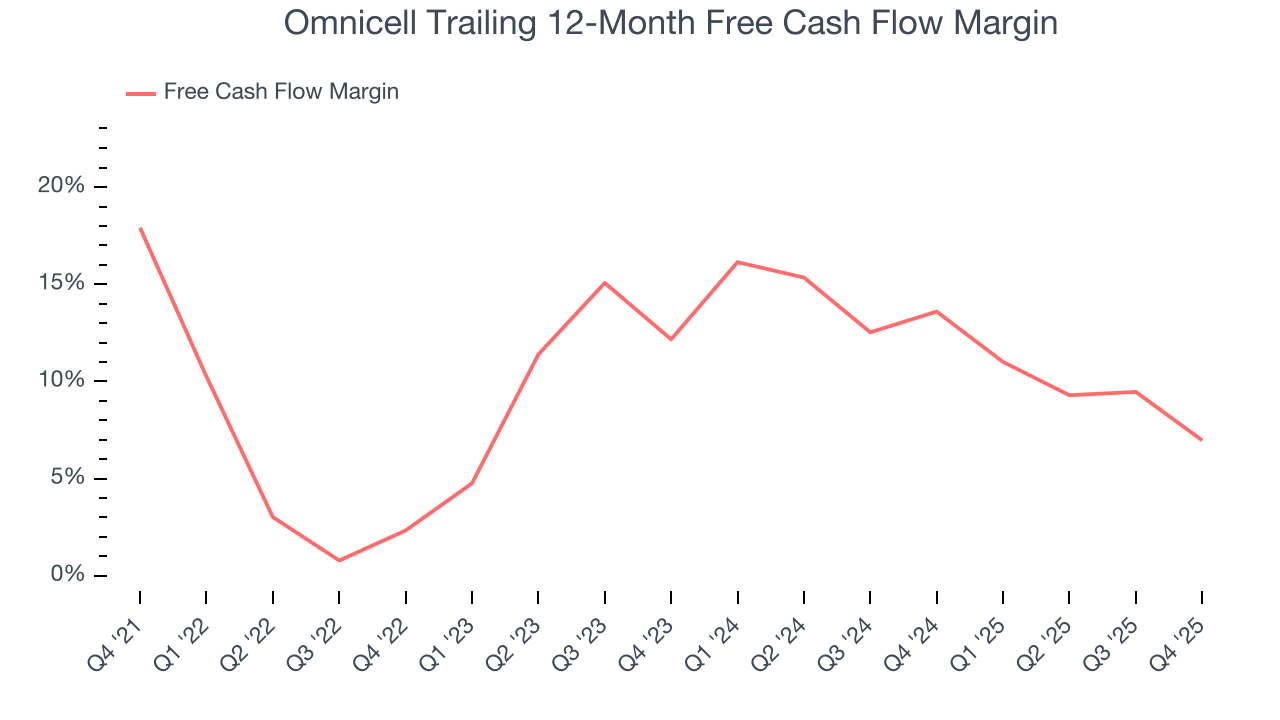

- Free Cash Flow Margin: 5.8%, down from 15.4% in the same quarter last year

- Market Capitalization: $2.10 billion

Company Overview

Driven by the vision of an "Autonomous Pharmacy" with zero medication errors, Omnicell (NASDAQ:OMCL) provides medication management automation and adherence tools that help healthcare systems and pharmacies reduce errors and improve efficiency.

Omnicell's solutions span the entire medication management process across various healthcare settings. The company's point-of-care systems include automated dispensing cabinets placed in nursing units, operating rooms, and emergency departments that securely store medications and track inventory. These systems integrate with electronic health records to streamline workflows and enhance accuracy.

In central pharmacies, Omnicell offers robotic dispensing systems that automate medication preparation and reduce human error. Their IV Compounding Service combines advanced robotics with clinical expertise to optimize the preparation of intravenous medications, helping hospitals reduce outsourcing costs and medication waste while improving safety.

A hospital pharmacy might use Omnicell's central pharmacy robots to automatically fill thousands of medication doses daily, while nurses on patient floors access these medications through secure automated cabinets that verify the right medication is being retrieved for the right patient.

Beyond acute care settings, Omnicell provides medication adherence solutions for long-term care facilities and retail pharmacies, including automated packaging systems that organize multiple medications into clearly labeled blister packs to help patients take the right medications at the right times.

The company generates revenue through equipment sales, multi-year leases, and subscription-based services. Many of Omnicell's offerings now combine hardware, software, and expert services in comprehensive packages. For example, their Specialty Pharmacy Services help healthcare providers establish and manage in-house specialty pharmacies, including assistance with licensing, payer contracting, and access to limited-distribution drugs.

Omnicell primarily serves the U.S. healthcare market, which accounts for approximately 88% of its revenue, with additional presence in Europe and other international markets. The company sells directly to healthcare facilities in the U.S. and Canada, and works with Group Purchasing Organizations that represent hospital networks.

4. Healthcare Technology for Providers

The healthcare technology sector provides software and data analytics to help hospitals and clinics streamline operations and improve patient outcomes, often through value-based care models. Future growth is expected as providers prioritize digital transformation to manage rising costs and patient demands. Tailwinds include the adoption of AI-driven tools and government incentives for digitization. There challenges as well, including long sales cycles and slow adoption by providers, who may be resistance to change. Tightening hospital budgets and cybersecurity threats are additional risks that could slow adoption.

Omnicell's competitors include BD (Becton, Dickinson and Company) (NYSE:BDX) with its Pyxis medication dispensing systems, Baxter International (NYSE:BAX) with its DoseEdge IV workflow solutions, and privately-held companies like ARxIUM and Swisslog Healthcare that offer pharmacy automation systems.

5. Revenue Scale

Larger companies benefit from economies of scale, where fixed costs like infrastructure, technology, and administration are spread over a higher volume of goods or services, reducing the cost per unit. Scale can also lead to bargaining power with suppliers, greater brand recognition, and more investment firepower. A virtuous cycle can ensue if a scaled company plays its cards right.

With just $1.18 billion in revenue over the past 12 months, Omnicell is a small company in an industry where scale matters. This makes it difficult to build trust with customers because healthcare is heavily regulated, complex, and resource-intensive.

6. Revenue Growth

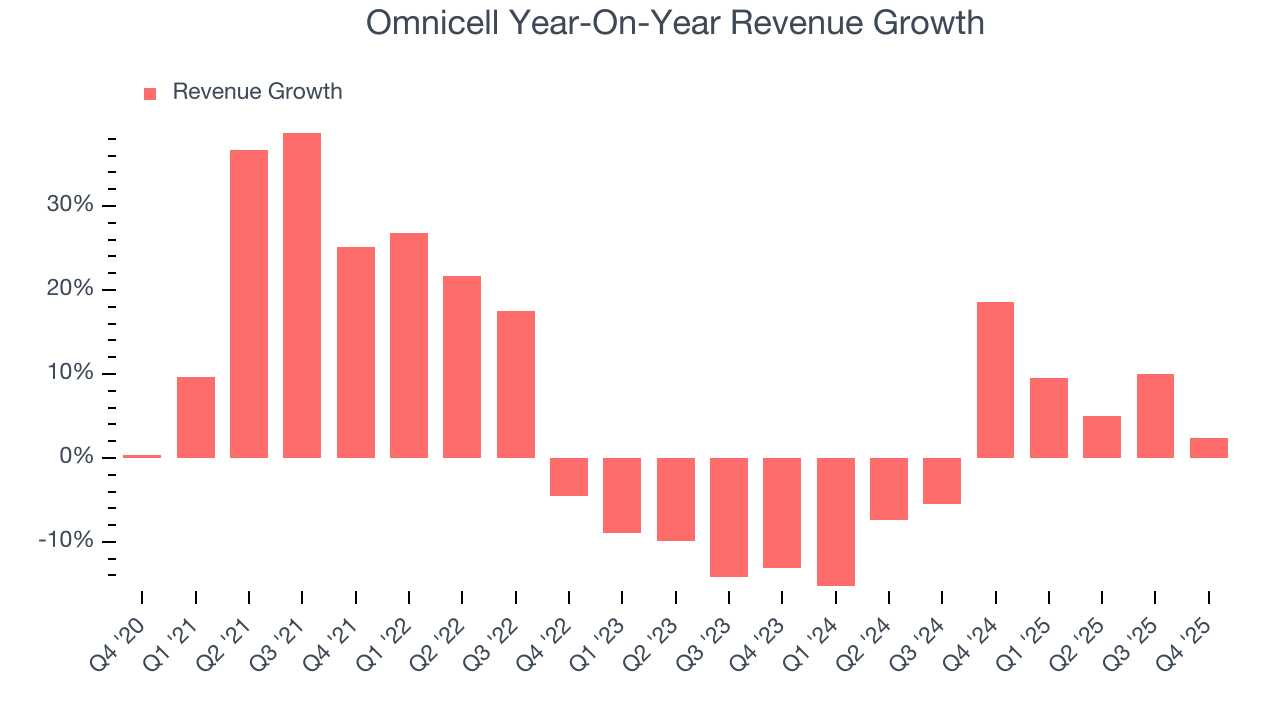

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Regrettably, Omnicell’s sales grew at a mediocre 5.8% compounded annual growth rate over the last five years. This was below our standard for the healthcare sector and is a tough starting point for our analysis.

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. Omnicell’s recent performance shows its demand has slowed as its annualized revenue growth of 1.6% over the last two years was below its five-year trend.

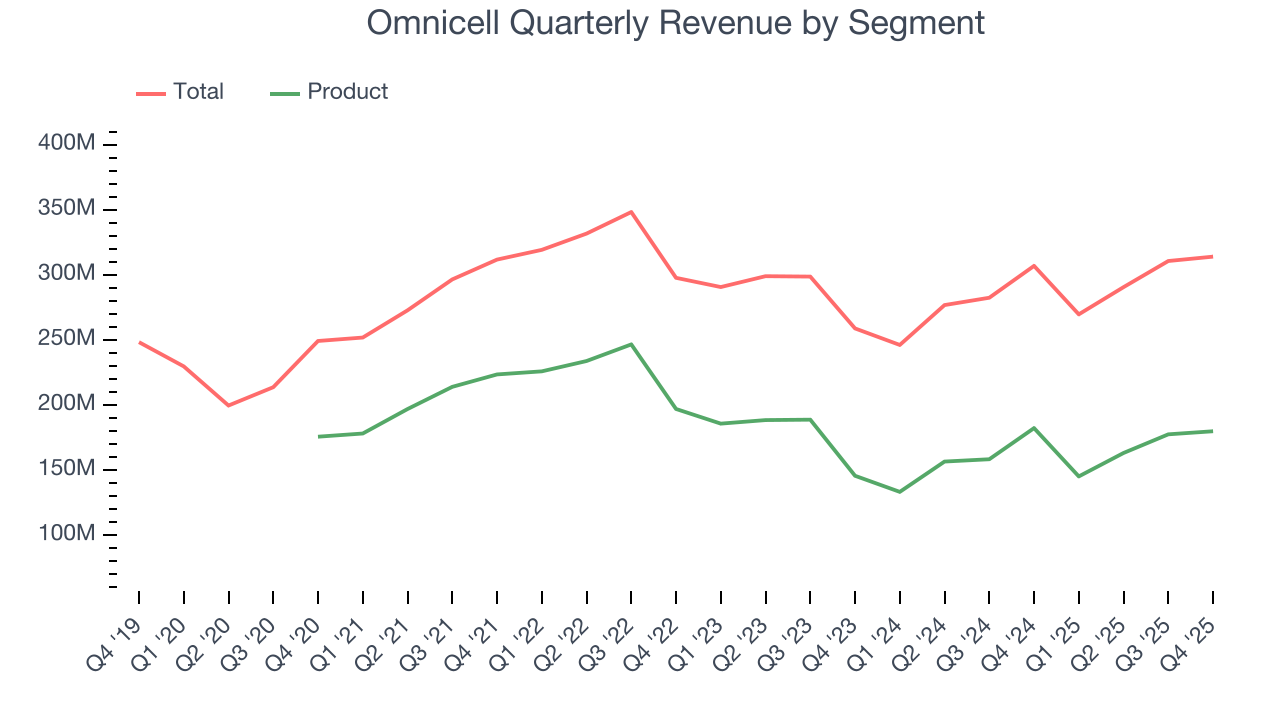

We can better understand the company’s revenue dynamics by analyzing its most important segment, Product. Over the last two years, Omnicell’s Product revenue averaged 1.5% year-on-year declines. This segment has lagged the company’s overall sales.

This quarter, Omnicell grew its revenue by 2.3% year on year, and its $314 million of revenue was in line with Wall Street’s estimates. Company management is currently guiding for a 13.1% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 4.3% over the next 12 months. While this projection suggests its newer products and services will catalyze better top-line performance, it is still below the sector average.

7. Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Omnicell was roughly breakeven when averaging the last five years of quarterly operating profits, lousy for a healthcare business.

Analyzing the trend in its profitability, Omnicell’s operating margin decreased by 7.5 percentage points over the last five years, but it rose by 3.5 percentage points on a two-year basis. Still, shareholders will want to see Omnicell become more profitable in the future.

In Q4, Omnicell’s breakeven margin was 0.1%, down 3.9 percentage points year on year. This contraction shows it was less efficient because its expenses grew faster than its revenue.

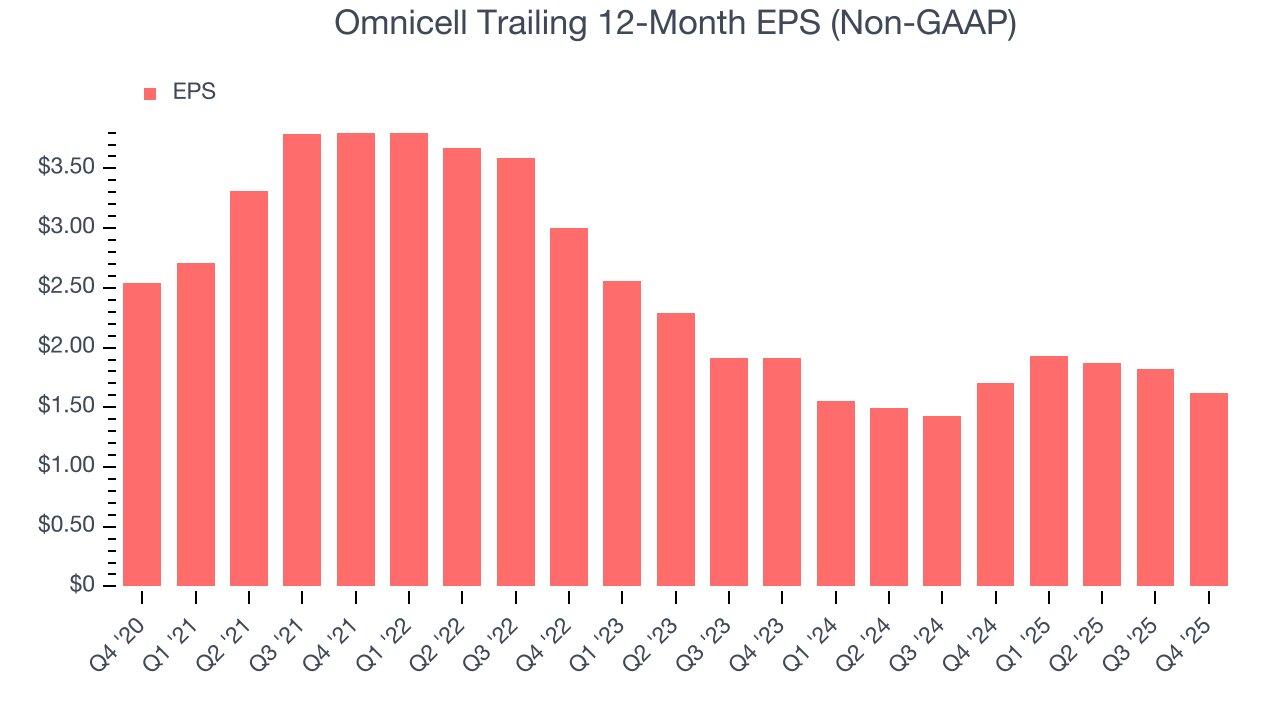

8. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Sadly for Omnicell, its EPS declined by 8.6% annually over the last five years while its revenue grew by 5.8%. This tells us the company became less profitable on a per-share basis as it expanded.

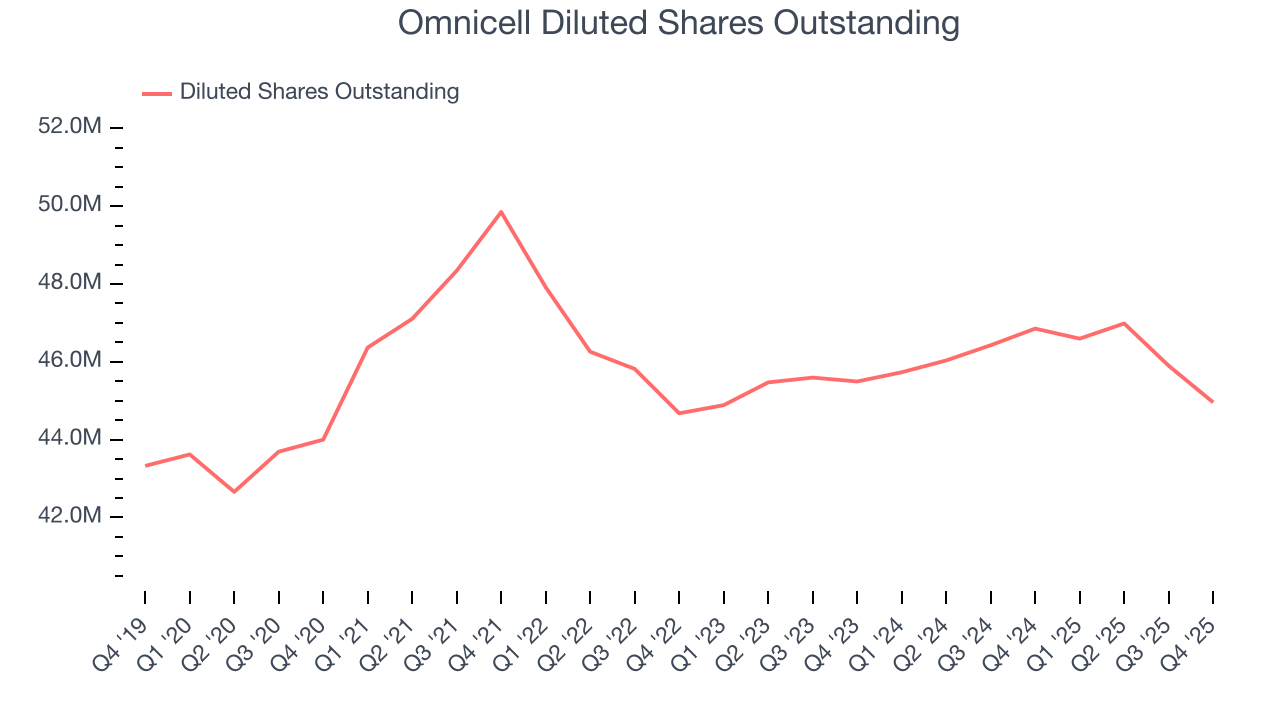

We can take a deeper look into Omnicell’s earnings to better understand the drivers of its performance. As we mentioned earlier, Omnicell’s operating margin declined by 7.5 percentage points over the last five years. Its share count also grew by 2.2%, meaning the company not only became less efficient with its operating expenses but also diluted its shareholders.

In Q4, Omnicell reported adjusted EPS of $0.40, down from $0.60 in the same quarter last year. This print missed analysts’ estimates. Over the next 12 months, Wall Street expects Omnicell’s full-year EPS of $1.62 to grow 16%.

9. Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

Omnicell has shown impressive cash profitability, giving it the option to reinvest or return capital to investors. The company’s free cash flow margin averaged 10.3% over the last five years, better than the broader healthcare sector. The divergence from its underwhelming operating margin stems from the add-back of non-cash charges like depreciation and stock-based compensation. GAAP operating profit expenses these line items, but free cash flow does not.

Taking a step back, we can see that Omnicell’s margin dropped by 10.9 percentage points during that time. If its declines continue, it could signal increasing investment needs and capital intensity.

Omnicell’s free cash flow clocked in at $18.36 million in Q4, equivalent to a 5.8% margin. The company’s cash profitability regressed as it was 9.5 percentage points lower than in the same quarter last year, suggesting its historical struggles have dragged on.

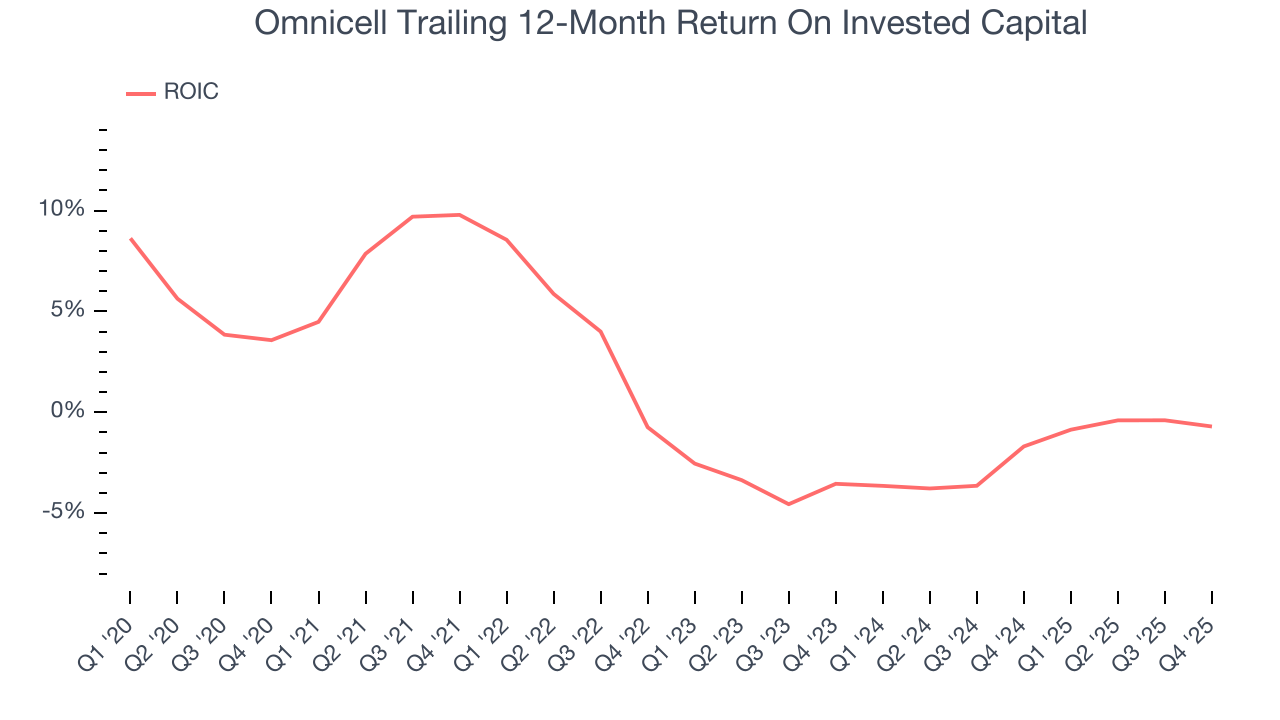

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Omnicell historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 0.6%, lower than the typical cost of capital (how much it costs to raise money) for healthcare companies.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Over the last few years, Omnicell’s ROIC has unfortunately decreased. Paired with its already low returns, these declines suggest its profitable growth opportunities are few and far between.

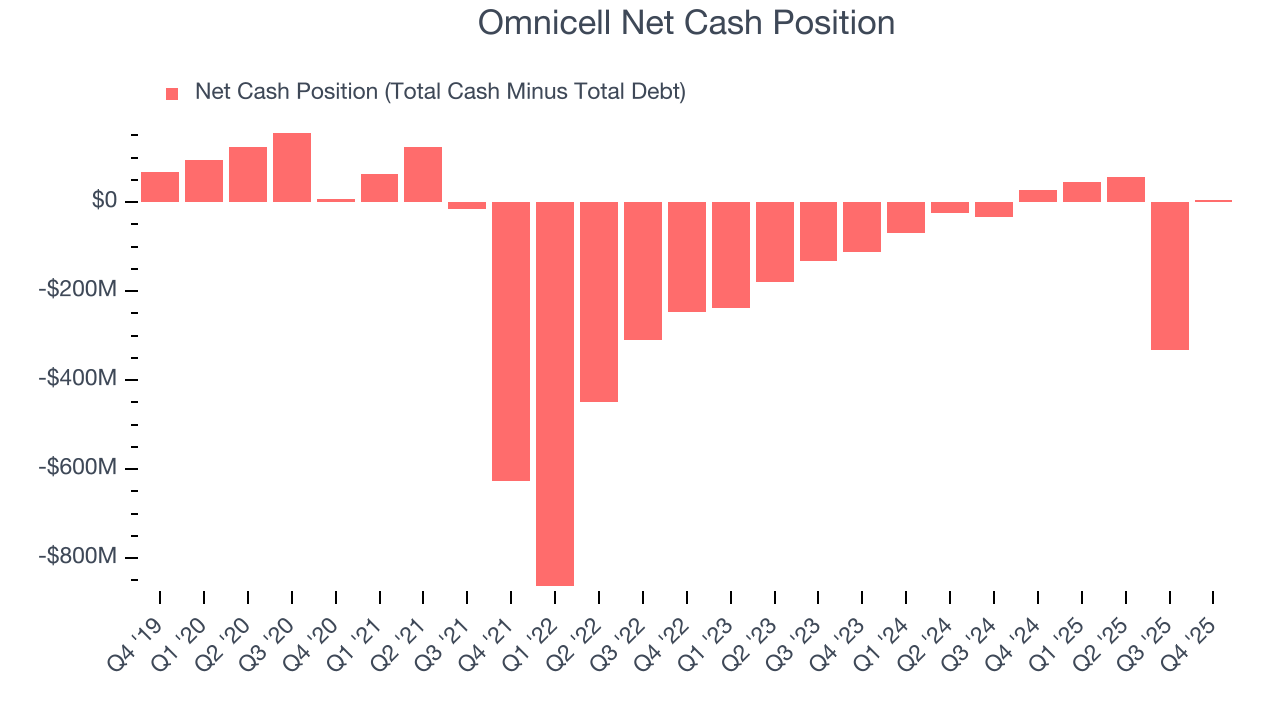

11. Balance Sheet Assessment

Businesses that maintain a cash surplus face reduced bankruptcy risk.

Omnicell is a profitable, well-capitalized company with $196.5 million of cash and $192.4 million of debt on its balance sheet. This $4.13 million net cash position gives it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

12. Key Takeaways from Omnicell’s Q4 Results

We were impressed by Omnicell’s optimistic EBITDA guidance for next quarter, which blew past analysts’ expectations. We were also excited its EPS guidance for next quarter outperformed Wall Street’s estimates by a wide margin. On the other hand, its full-year EPS guidance missed and its EPS fell short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock remained flat at $46.72 immediately after reporting.

13. Is Now The Time To Buy Omnicell?

Updated: March 1, 2026 at 11:31 PM EST

A common mistake we notice when investors are deciding whether to buy a stock or not is that they simply look at the latest earnings results. Business quality and valuation matter more, so we urge you to understand these dynamics as well.

We cheer for all companies helping people live better, but in the case of Omnicell, we’ll be cheering from the sidelines. For starters, its revenue growth was mediocre over the last five years, and analysts expect its demand to deteriorate over the next 12 months. While its solid free cash flow generation gives it reinvestment options, the downside is its declining EPS over the last five years makes it a less attractive asset to the public markets. On top of that, its declining adjusted operating margin shows the business has become less efficient.

Omnicell’s P/E ratio based on the next 12 months is 24x. At this valuation, there’s a lot of good news priced in - you can find more timely opportunities elsewhere.

Wall Street analysts have a consensus one-year price target of $57.43 on the company (compared to the current share price of $40.28).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.