OneWater (ONEW)

OneWater keeps us up at night. Its weak sales growth and low returns on capital show it struggled to generate demand and profits.― StockStory Analyst Team

1. News

2. Summary

Why We Think OneWater Will Underperform

A public company since early 2020, OneWater Marine (NASDAQ:ONEW) sells boats, yachts, and other marine products.

- Gross margin of 23.6% is below its competitors, leaving less money for marketing and promotions

- Operating margin fell from an already low starting point over the last year, and the smaller profit dollars make it harder to react to unexpected market developments

- High net-debt-to-EBITDA ratio of 7× could force the company to raise capital at unfavorable terms if market conditions deteriorate

OneWater doesn’t meet our quality criteria. There are more appealing investments to be made.

Why There Are Better Opportunities Than OneWater

OneWater’s stock price of $8.66 implies a valuation ratio of 34.1x forward P/E. This multiple is quite expensive for the quality you get.

Paying up for elite businesses with strong earnings potential is better than investing in lower-quality companies with shaky fundamentals. That’s how you avoid big downside over the long term.

3. OneWater (ONEW) Research Report: Q4 CY2025 Update

Boat and marine products retailer OneWater Marine (NASDAQ:ONEW) met Wall Streets revenue expectations in Q4 CY2025, with sales up 1.3% year on year to $380.6 million. The company’s outlook for the full year was close to analysts’ estimates with revenue guided to $1.88 billion at the midpoint. Its non-GAAP loss of $0.04 per share was 93% above analysts’ consensus estimates.

OneWater (ONEW) Q4 CY2025 Highlights:

- Revenue: $380.6 million vs analyst estimates of $382.2 million (1.3% year-on-year growth, in line)

- Adjusted EPS: -$0.04 vs analyst estimates of -$0.58 (93% beat)

- Adjusted EBITDA: $3.60 million vs analyst estimates of $1.90 million (0.9% margin, 90.1% beat)

- The company reconfirmed its revenue guidance for the full year of $1.88 billion at the midpoint

- Management reiterated its full-year Adjusted EPS guidance of $0.50 at the midpoint

- EBITDA guidance for the full year is $75 million at the midpoint, in line with analyst expectations

- Operating Margin: -1.4%, in line with the same quarter last year

- Same-Store Sales were flat year on year (4.2% in the same quarter last year)

- Market Capitalization: $219 million

Company Overview

A public company since early 2020, OneWater Marine (NASDAQ:ONEW) sells boats, yachts, and other marine products.

The company’s product offering includes boats and yachts from well-known manufacturers such as Sea Ray and Boston Whaler as well as performance and sport vessels from brands like Yamaha and MasterCraft. In addition, OneWater Marine sells watersports equipment, marine electronics for navigation and communication, and safety gear. Lastly, the company’s locations provide financing and servicing to make them a one-stop shop for recreational boating.

The core customer is an affluent individual or and family who has means, interest in marine activities, and proximity or access to water to use the company’s products. These customers are looking for high-quality products that offer some combination of luxury and performance. They also often demand personalized support and assistance through the life of their boats or yachts.

OneWater Marine locations vary; there are small boutique-style locations to larger flagship stores. As expected, these locations usually sit near waterfront locations such as marinas and harbors. Boats are showcased both inside the showroom as well as outside. Also while inside, customers can find equipment and marine products for sale as well as well-versed associates who can talk through products, financing, and servicing.

4. Boat & Marine Retailer

Retailers that sell boats and marine products sell products, sure, but they also sell an image and lifestyle to an often wealthier customer. Unlike a car–which many use daily to get to/from work and to run personal and family errands–a boat or yacht is certainly a discretionary, luxury, nice-to-have purchase. While there is online competition, especially for research and discovery, the boat and yacht market is still very brick-and-mortar based given the magnitude of the purchase and the logistical costs associated with moving these products over long distances.

Competitors offering recreational marine products include MarineMax (NYSE:HZO), Yamaha Motor Co. (TSE:7272), and Brunswick Corp (NYSE:BC).

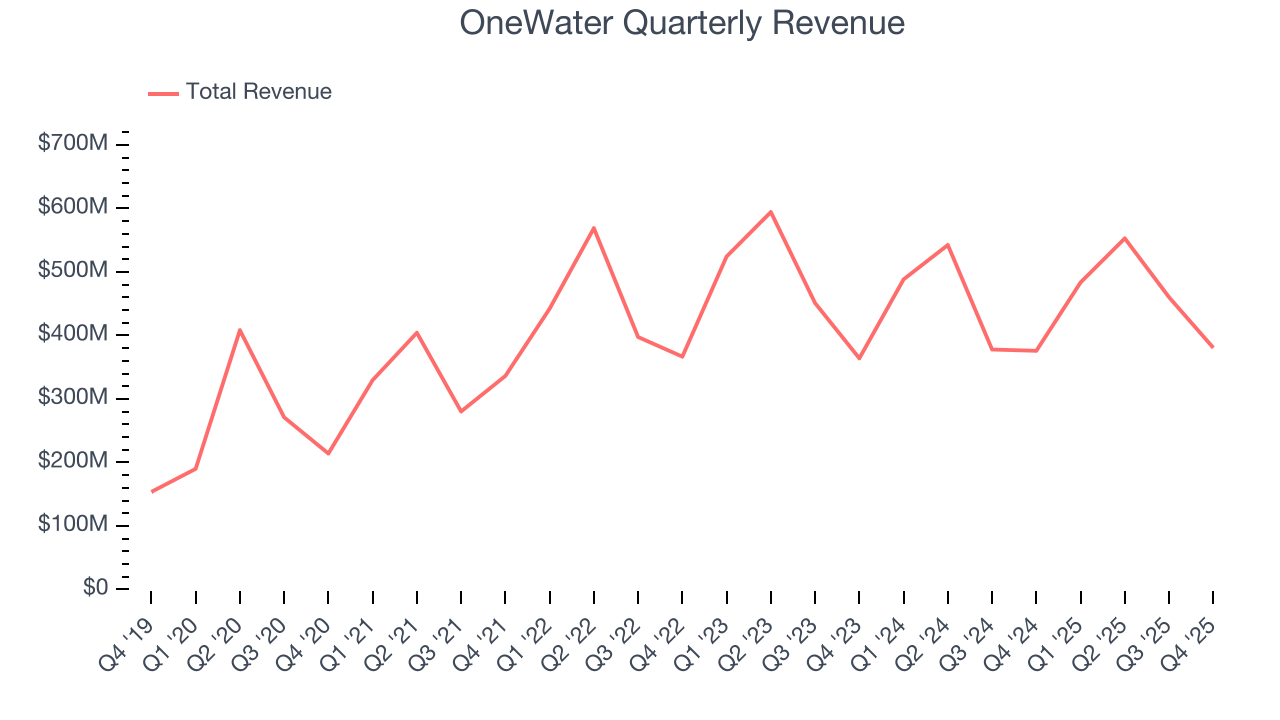

5. Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but many enduring ones grow for years.

With $1.88 billion in revenue over the past 12 months, OneWater is a small retailer, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage with suppliers.

As you can see below, OneWater’s sales grew at a sluggish 1.9% compounded annual growth rate over the last three years as it didn’t open many new stores.

This quarter, OneWater grew its revenue by 1.3% year on year, and its $380.6 million of revenue was in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to remain flat over the next 12 months. This projection is underwhelming and suggests its products will face some demand challenges.

6. Store Performance

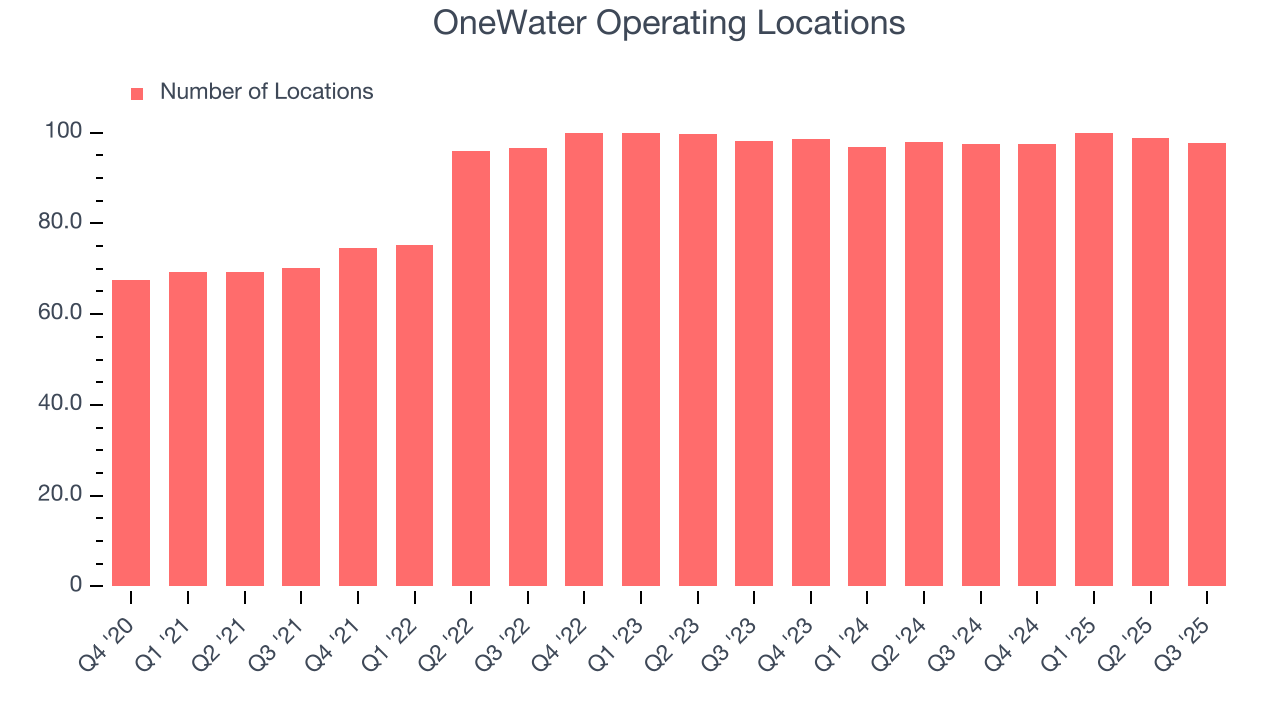

Number of Stores

A retailer’s store count often determines how much revenue it can generate.

OneWater has kept its store count flat over the last two years while other consumer retail businesses have opted for growth.

When a retailer keeps its store footprint steady, it usually means demand is stable and it’s focusing on operational efficiency to increase profitability.

Note that OneWater reports its store count intermittently, so some data points are missing in the chart below.

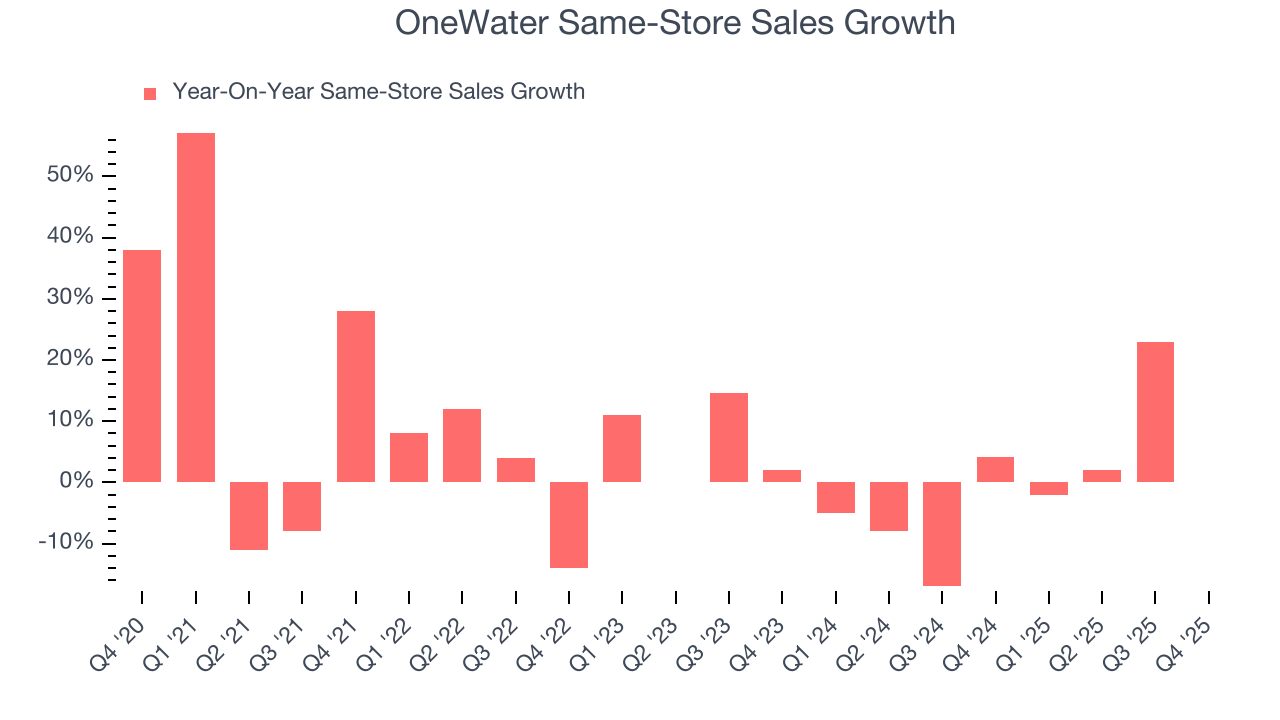

Same-Store Sales

A company's store base only paints one part of the picture. When demand is high, it makes sense to open more. But when demand is low, it’s prudent to close some locations and use the money in other ways. Same-store sales provides a deeper understanding of this issue because it measures organic growth at brick-and-mortar shops for at least a year.

OneWater’s demand within its existing locations has barely increased over the last two years as its same-store sales were flat. This performance isn’t ideal, and we’d be skeptical if OneWater starts opening new stores to artificially boost revenue growth.

In the latest quarter, OneWater’s year on year same-store sales were flat. This performance was more or less in line with its historical levels.

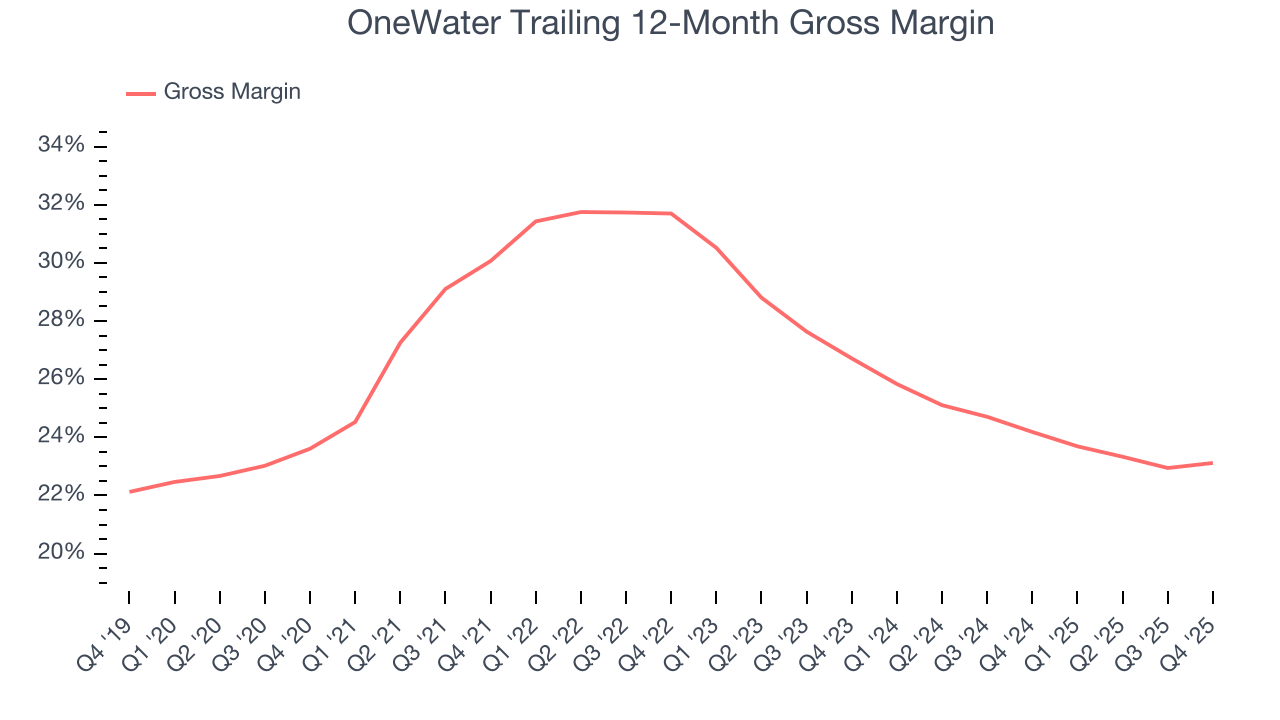

7. Gross Margin & Pricing Power

OneWater has bad unit economics for a retailer, signaling it operates in a competitive market and lacks pricing power because its inventory is sold in many places. As you can see below, it averaged a 23.6% gross margin over the last two years. That means OneWater paid its suppliers a lot of money ($76.36 for every $100 in revenue) to run its business.

OneWater produced a 23.5% gross profit margin in Q4, in line with the same quarter last year. Zooming out, OneWater’s full-year margin has been trending down over the past 12 months, decreasing by 1.1 percentage points. If this move continues, it could suggest a more competitive environment with some pressure to discount products and higher input costs (such as labor and freight expenses to transport goods).

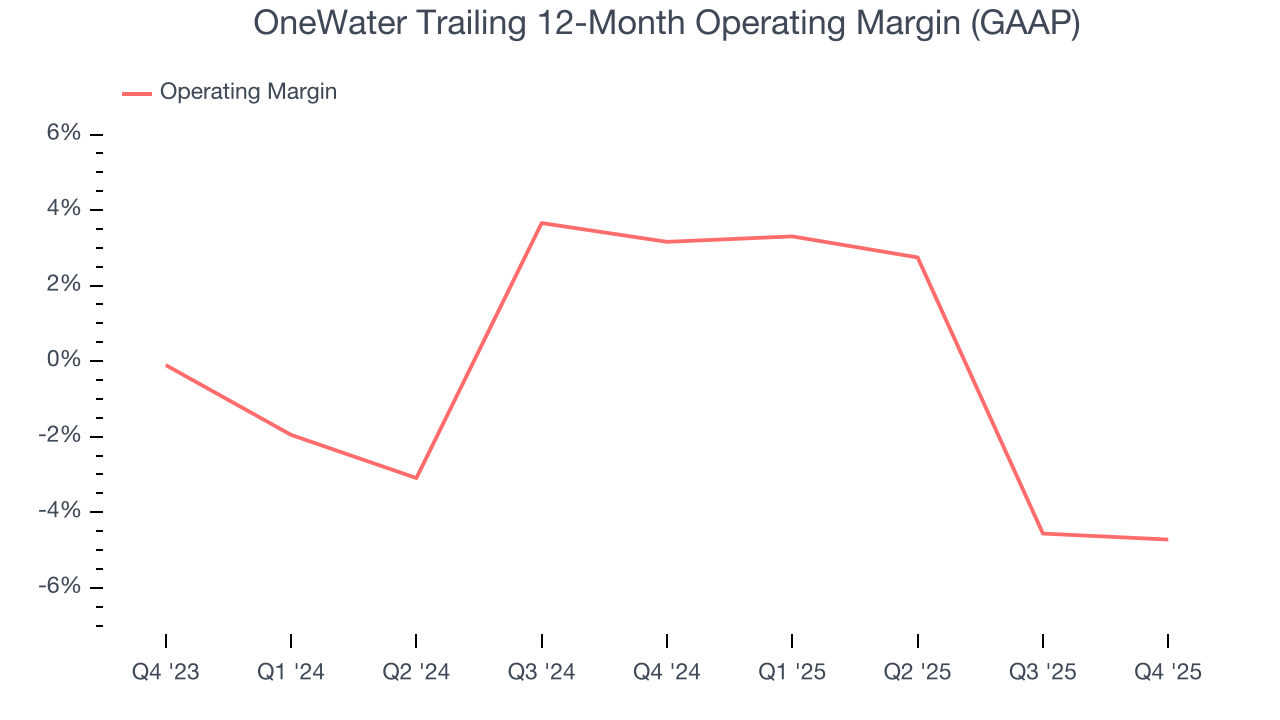

8. Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

OneWater was roughly breakeven when averaging the last two years of quarterly operating profits, one of the worst outcomes in the consumer retail sector. This result isn’t too surprising given its low gross margin as a starting point.

Analyzing the trend in its profitability, OneWater’s operating margin decreased by 7.9 percentage points over the last year. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. OneWater’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers.

This quarter, OneWater generated a negative 1.4% operating margin. The company's consistent lack of profits raise a flag.

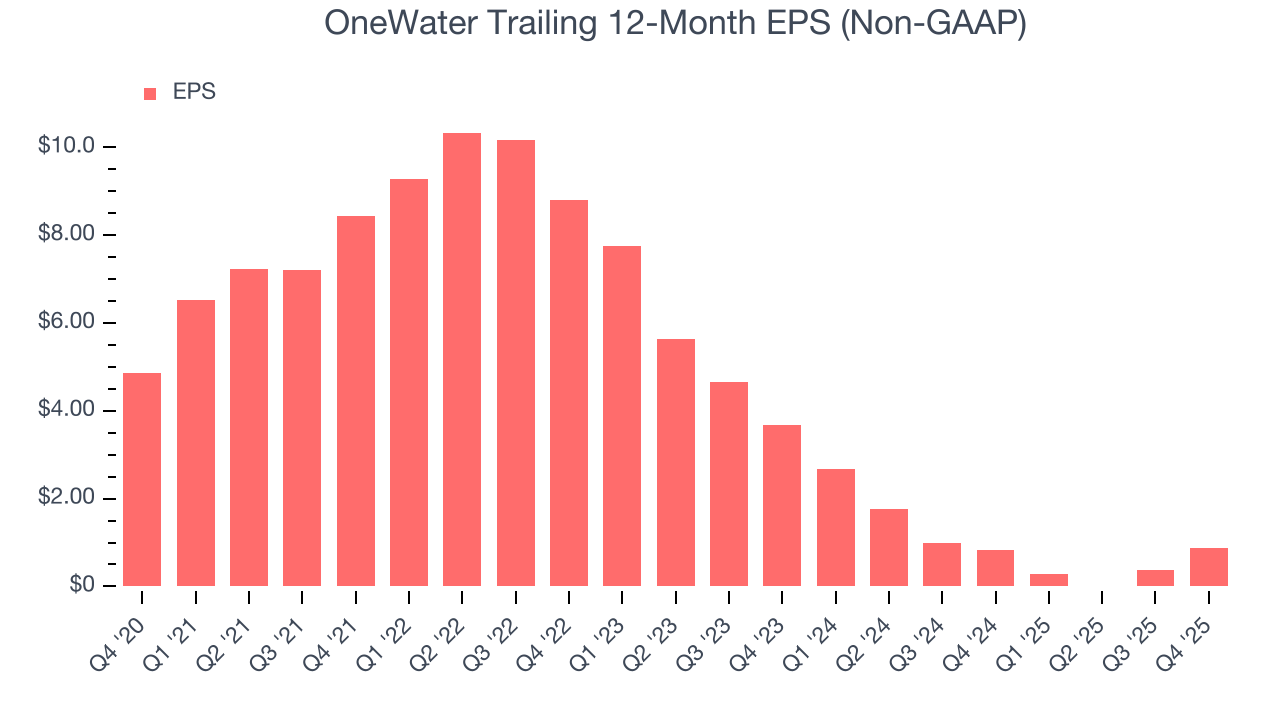

9. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Sadly for OneWater, its EPS declined by 53.6% annually over the last three years while its revenue grew by 1.9%. This tells us the company became less profitable on a per-share basis as it expanded.

In Q4, OneWater reported adjusted EPS of negative $0.04, up from negative $0.54 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects OneWater’s full-year EPS of $0.88 to shrink by 46.6%.

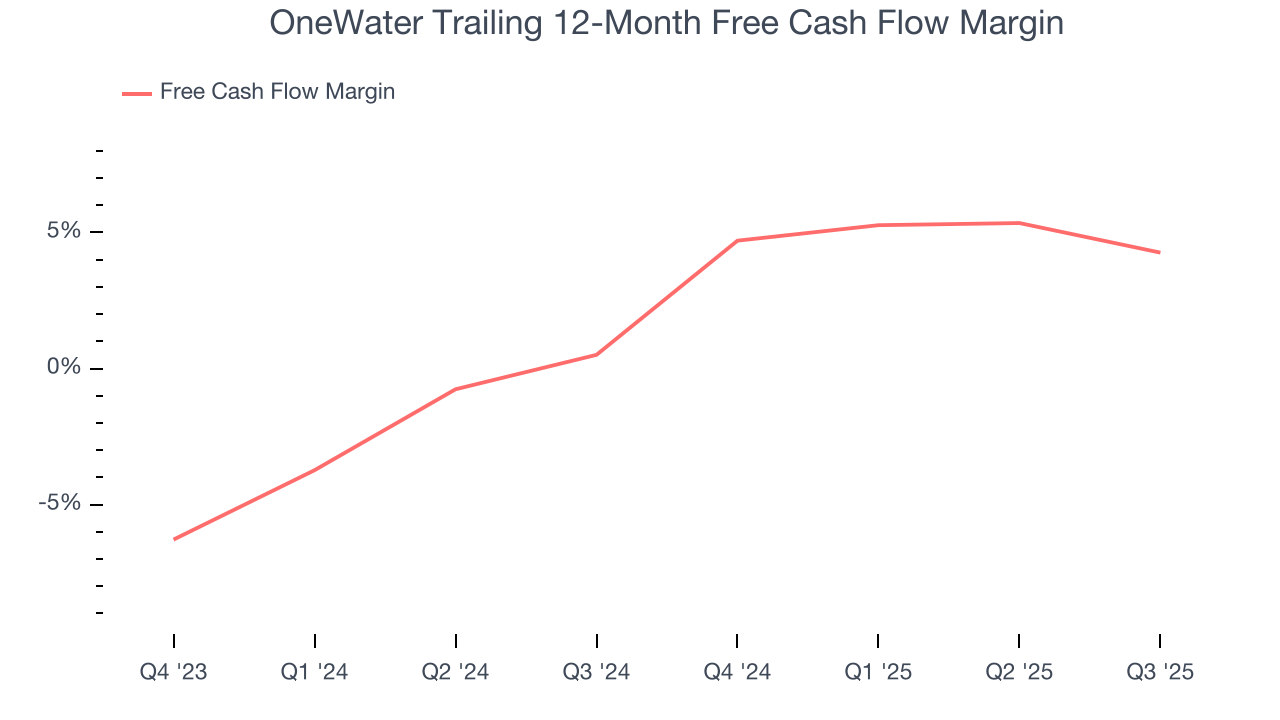

10. Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

OneWater has shown impressive cash profitability, giving it the option to reinvest or return capital to investors. The company’s free cash flow margin averaged 6.2% over the last two years, better than the broader consumer retail sector. The divergence from its underwhelming operating margin stems from the add-back of non-cash charges like depreciation and stock-based compensation. GAAP operating profit expenses these line items, but free cash flow does not.

11. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

OneWater historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 7.6%, somewhat low compared to the best consumer retail companies that consistently pump out 25%+.

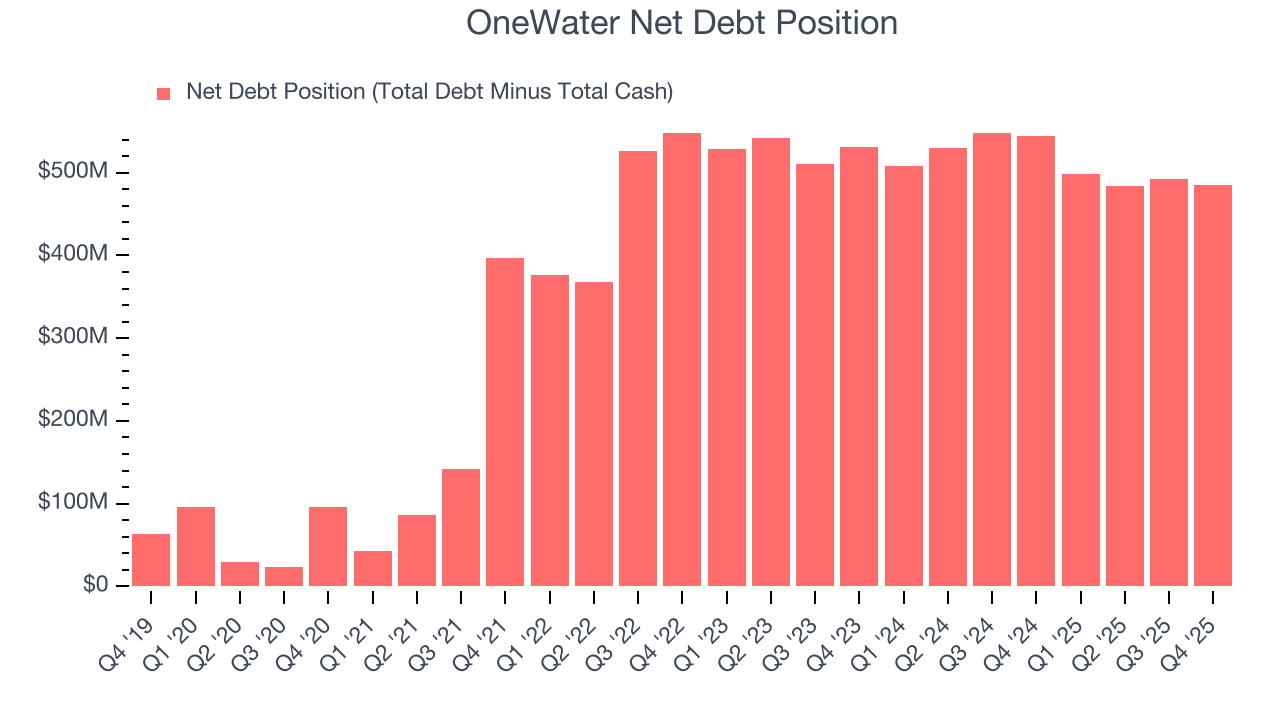

12. Balance Sheet Risk

Debt is a tool that can boost company returns but presents risks if used irresponsibly. As long-term investors, we aim to avoid companies taking excessive advantage of this instrument because it could lead to insolvency.

OneWater’s $527.7 million of debt exceeds the $42.44 million of cash on its balance sheet. Furthermore, its 7× net-debt-to-EBITDA ratio (based on its EBITDA of $71.81 million over the last 12 months) shows the company is overleveraged.

At this level of debt, incremental borrowing becomes increasingly expensive and credit agencies could downgrade the company’s rating if profitability falls. OneWater could also be backed into a corner if the market turns unexpectedly – a situation we seek to avoid as investors in high-quality companies.

We hope OneWater can improve its balance sheet and remain cautious until it increases its profitability or pays down its debt.

13. Key Takeaways from OneWater’s Q4 Results

It was good to see OneWater beat analysts’ EPS expectations this quarter. We were also excited its EBITDA outperformed Wall Street’s estimates by a wide margin. On the other hand, its revenue was in line. Overall, we think this was a decent quarter with some key metrics above expectations. The stock traded up 6.7% to $14.10 immediately after reporting.

14. Is Now The Time To Buy OneWater?

Updated: March 21, 2026 at 10:42 PM EDT

Before deciding whether to buy OneWater or pass, we urge investors to consider business quality, valuation, and the latest quarterly results.

OneWater falls short of our quality standards. For starters, its revenue growth was uninspiring over the last three years, and analysts expect its demand to deteriorate over the next 12 months. On top of that, OneWater’s declining EPS over the last three years makes it a less attractive asset to the public markets, and its projected EPS for the next year is lacking.

OneWater’s P/E ratio based on the next 12 months is 34.1x. This valuation tells us it’s a bit of a market darling with a lot of good news priced in - we think other companies feature superior fundamentals at the moment.

Wall Street analysts have a consensus one-year price target of $16.25 on the company (compared to the current share price of $8.66).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.