Park-Ohio (PKOH)

We wouldn’t recommend Park-Ohio. Its sales have underperformed and its low returns on capital show it has few growth opportunities.― StockStory Analyst Team

1. News

2. Summary

Why We Think Park-Ohio Will Underperform

Based in Cleveland, Park-Ohio (NASDAQ:PKOH) provides supply chain management services, capital equipment, and manufactured components.

- Annual sales declines of 1.8% for the past two years show its products and services struggled to connect with the market during this cycle

- Earnings per share have dipped by 6.2% annually over the past two years, which is concerning because stock prices follow EPS over the long term

- Cash-burning history makes us doubt the long-term viability of its business model

Park-Ohio’s quality is lacking. We see more lucrative opportunities elsewhere.

Why There Are Better Opportunities Than Park-Ohio

Park-Ohio is trading at $24.51 per share, or 7.9x forward P/E. Park-Ohio’s valuation may seem like a great deal, but we think there are valid reasons why it’s so cheap.

Our advice is to pay up for elite businesses whose advantages are tailwinds to earnings growth. Don’t get sucked into lower-quality businesses just because they seem like bargains. These mediocre businesses often never achieve a higher multiple as hoped, a phenomenon known as a “value trap”.

3. Park-Ohio (PKOH) Research Report: Q4 CY2025 Update

Diversified manufacturing and supply chain services provider Park-Ohio (NASDAQ:PKOH) fell short of the market’s revenue expectations in Q4 CY2025 as sales only rose 1.7% year on year to $395 million. On the other hand, the company’s full-year revenue guidance of $1.69 billion at the midpoint came in 1.6% above analysts’ estimates. Its non-GAAP profit of $0.65 per share was 11.6% below analysts’ consensus estimates.

Park-Ohio (PKOH) Q4 CY2025 Highlights:

- Revenue: $395 million vs analyst estimates of $402.9 million (1.7% year-on-year growth, 2% miss)

- Adjusted EPS: $0.65 vs analyst expectations of $0.74 (11.6% miss)

- Adjusted EBITDA: $35.3 million vs analyst estimates of $34.45 million (8.9% margin, 2.5% beat)

- Adjusted EPS guidance for the upcoming financial year 2026 is $3.05 at the midpoint, missing analyst estimates by 3.2%

- Operating Margin: 2.5%, down from 4.1% in the same quarter last year

- Free Cash Flow Margin: 9.1%, up from 4.2% in the same quarter last year

- Market Capitalization: $361.3 million

Company Overview

Based in Cleveland, Park-Ohio (NASDAQ:PKOH) provides supply chain management services, capital equipment, and manufactured components.

The company operates through three reportable segments: Supply Technologies, Assembly Components, and Engineered Products.

The Supply Technologies segment offers "Total Supply Management", an approach to managing the supply chain for production components. This segment operates ~80 logistics service centers across North America, Europe, and Asia that supply nearly 300k globally sourced production components. Supply Technologies serves various industries, including heavy-duty trucking, aerospace and defense, automotive, and consumer electronics.

The Assembly Components segment focuses on manufacturing products oriented toward fuel efficiency, reduced emissions, and vehicle electrification. This segment designs and produces fuel rails, fuel filler pipes, and flexible multi-layer plastic and rubber assemblies for the automotive industry. Assembly Components operates over 10 manufacturing facilities across the United States, Mexico, China, the United Kingdom, and the Czech Republic.

The Engineered Products segment encompasses niche manufacturing businesses that design and manufacture highly engineered products. These include induction heating and melting systems, pipe threading systems, and forged and machined products. This segment has 30+ facilities across North America, Europe, and Asia and serves industries such as ferrous and non-ferrous metals, oil and gas, aerospace and defense, and rail.

4. Engineered Components and Systems

Engineered components and systems companies possess technical know-how in sometimes narrow areas such as metal forming or intelligent robotics. Lately, automation and connected equipment collecting analyzable data have been trending, creating new demand. On the other hand, like the broader industrials sector, engineered components and systems companies are at the whim of economic cycles. Consumer spending and interest rates, for example, can greatly impact the industrial production that drives demand for these companies’ offerings.

Competitors of Park-Ohio include NN (NASDAQ:NNBR), Lawson Products (NASDAQ:LAWS), and DXP Enterprises (NASDAQ:DXPE).

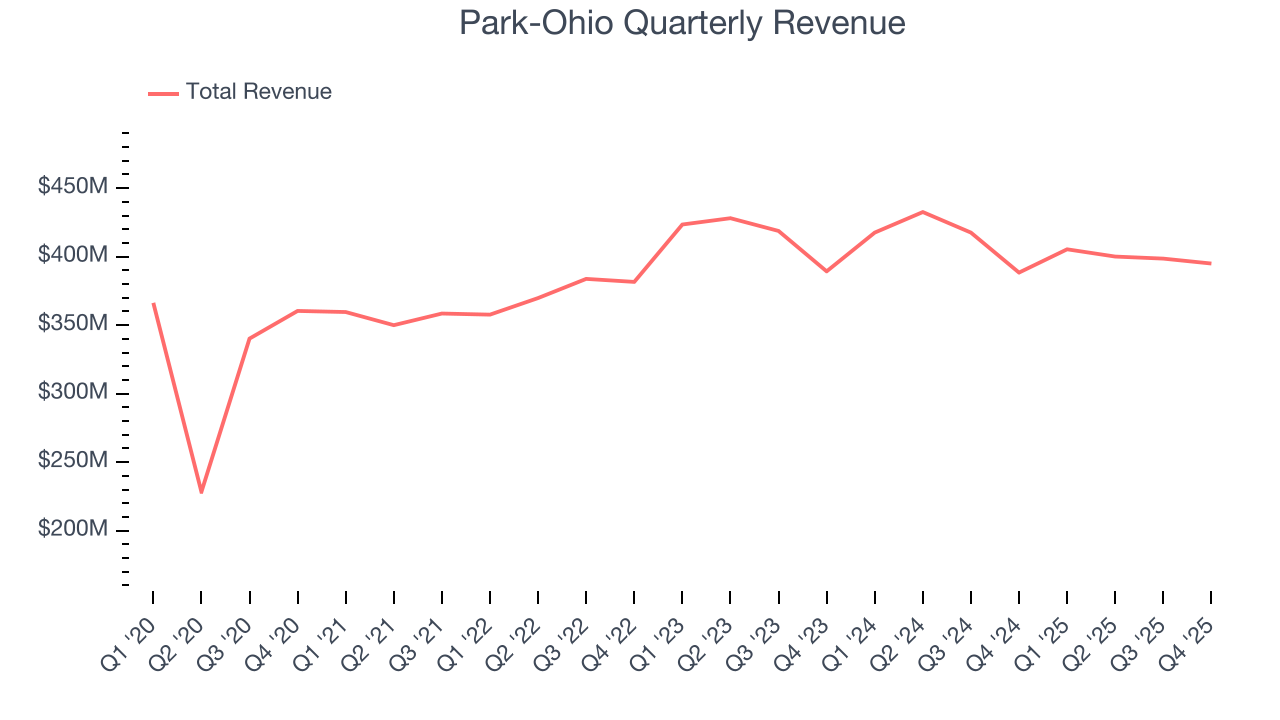

5. Revenue Growth

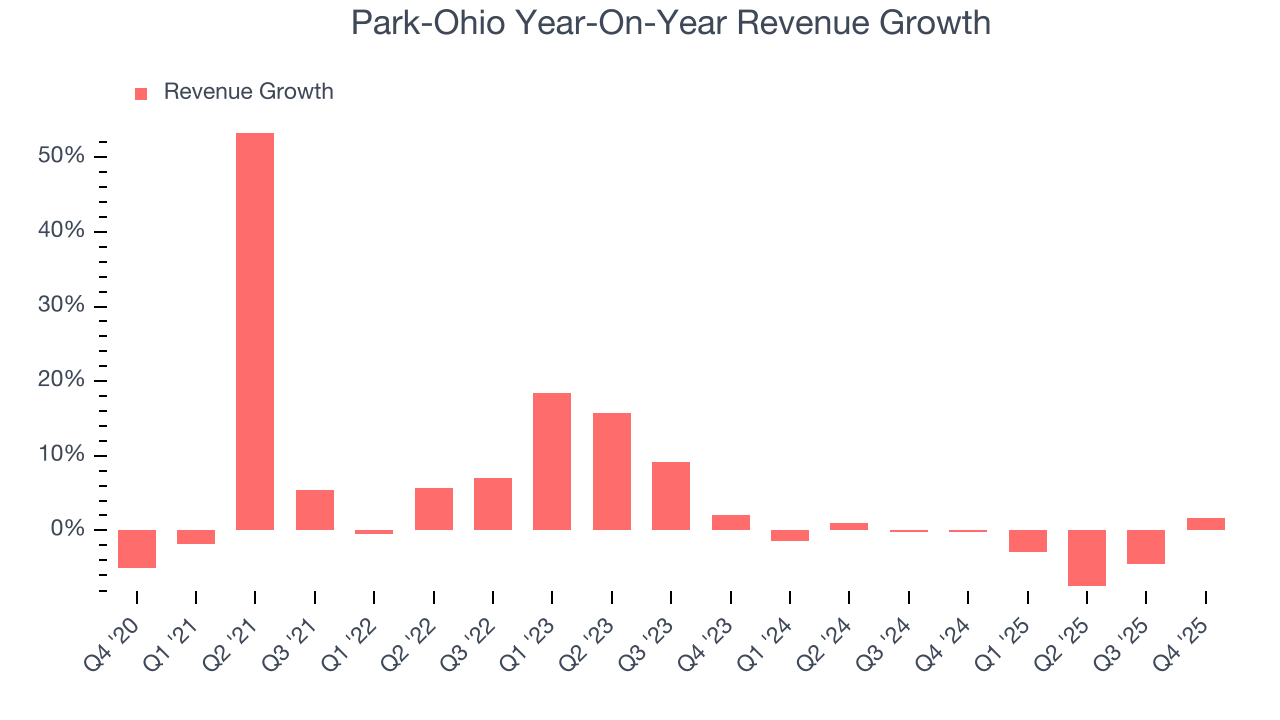

A company’s long-term sales performance can indicate its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Regrettably, Park-Ohio’s sales grew at a sluggish 4.3% compounded annual growth rate over the last five years. This fell short of our benchmark for the industrials sector and is a poor baseline for our analysis.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Park-Ohio’s performance shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 1.8% annually.

This quarter, Park-Ohio’s revenue grew by 1.7% year on year to $395 million, falling short of Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 4.2% over the next 12 months. While this projection suggests its newer products and services will catalyze better top-line performance, it is still below the sector average.

6. Gross Margin & Pricing Power

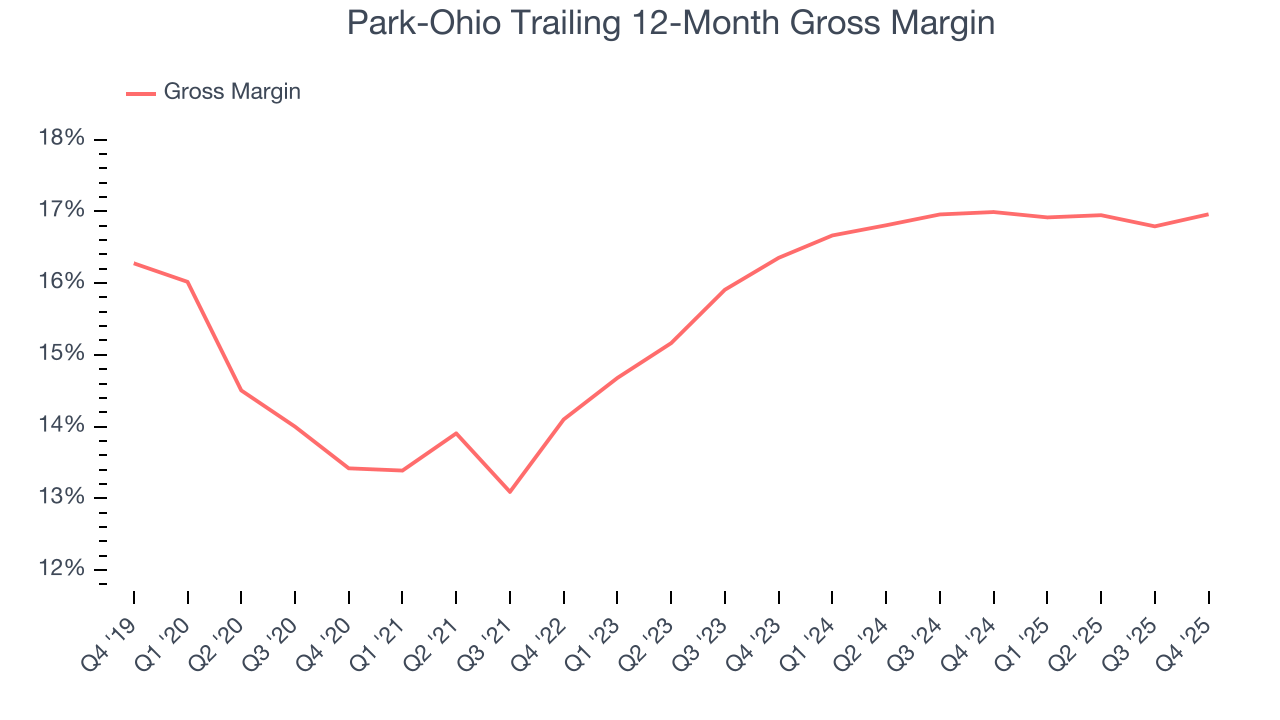

Park-Ohio has bad unit economics for an industrials business, signaling it operates in a competitive market. As you can see below, it averaged a 15.6% gross margin over the last five years. Said differently, Park-Ohio had to pay a chunky $84.35 to its suppliers for every $100 in revenue.

Park-Ohio produced a 17.3% gross profit margin in Q4, in line with the same quarter last year. Zooming out, the company’s full-year margin has remained steady over the past 12 months, suggesting its input costs (such as raw materials and manufacturing expenses) have been stable and it isn’t under pressure to lower prices.

7. Operating Margin

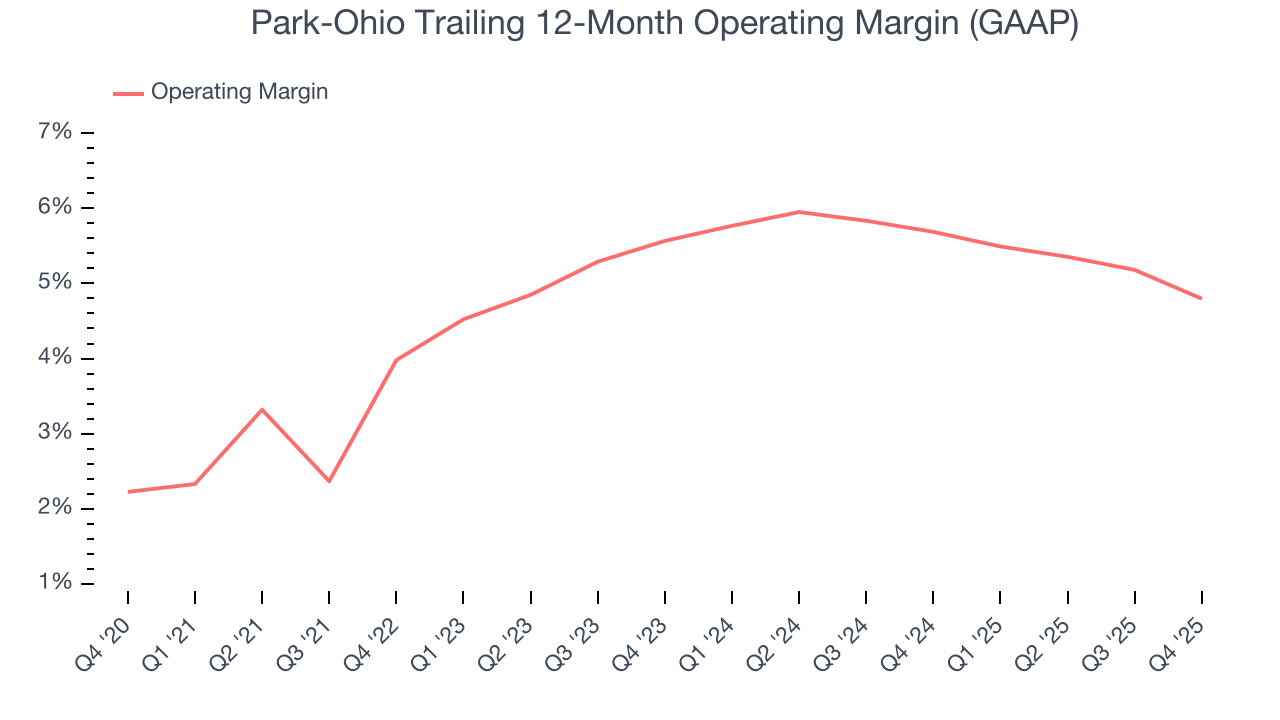

Park-Ohio was profitable over the last five years but held back by its large cost base. Its average operating margin of 4.6% was weak for an industrials business. This result isn’t too surprising given its low gross margin as a starting point.

On the plus side, Park-Ohio’s operating margin rose by 3.8 percentage points over the last five years, as its sales growth gave it operating leverage.

This quarter, Park-Ohio generated an operating margin profit margin of 2.5%, down 1.5 percentage points year on year. Since Park-Ohio’s operating margin decreased more than its gross margin, we can assume it was less efficient because expenses such as marketing, R&D, and administrative overhead increased.

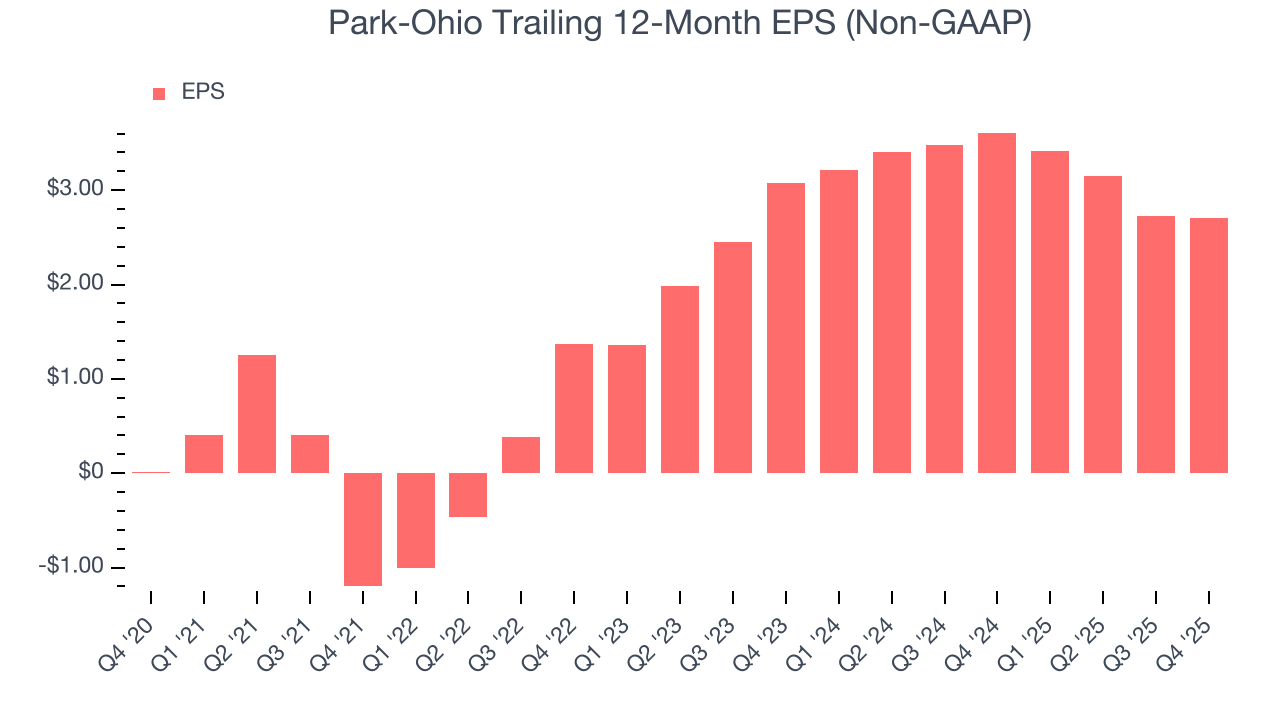

8. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Park-Ohio’s EPS grew at 207% compounded annual growth rate over the last five years, higher than its 4.3% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

We can take a deeper look into Park-Ohio’s earnings to better understand the drivers of its performance. As we mentioned earlier, Park-Ohio’s operating margin declined this quarter but expanded by 3.8 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its higher earnings; interest expenses and taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Park-Ohio, its two-year annual EPS declines of 6.2% mark a reversal from its (seemingly) healthy five-year trend. We hope Park-Ohio can return to earnings growth in the future.

In Q4, Park-Ohio reported adjusted EPS of $0.65, down from $0.67 in the same quarter last year. This print missed analysts’ estimates, but we care more about long-term adjusted EPS growth than short-term movements. Over the next 12 months, Wall Street expects Park-Ohio’s full-year EPS of $2.71 to grow 16.2%.

9. Cash Is King

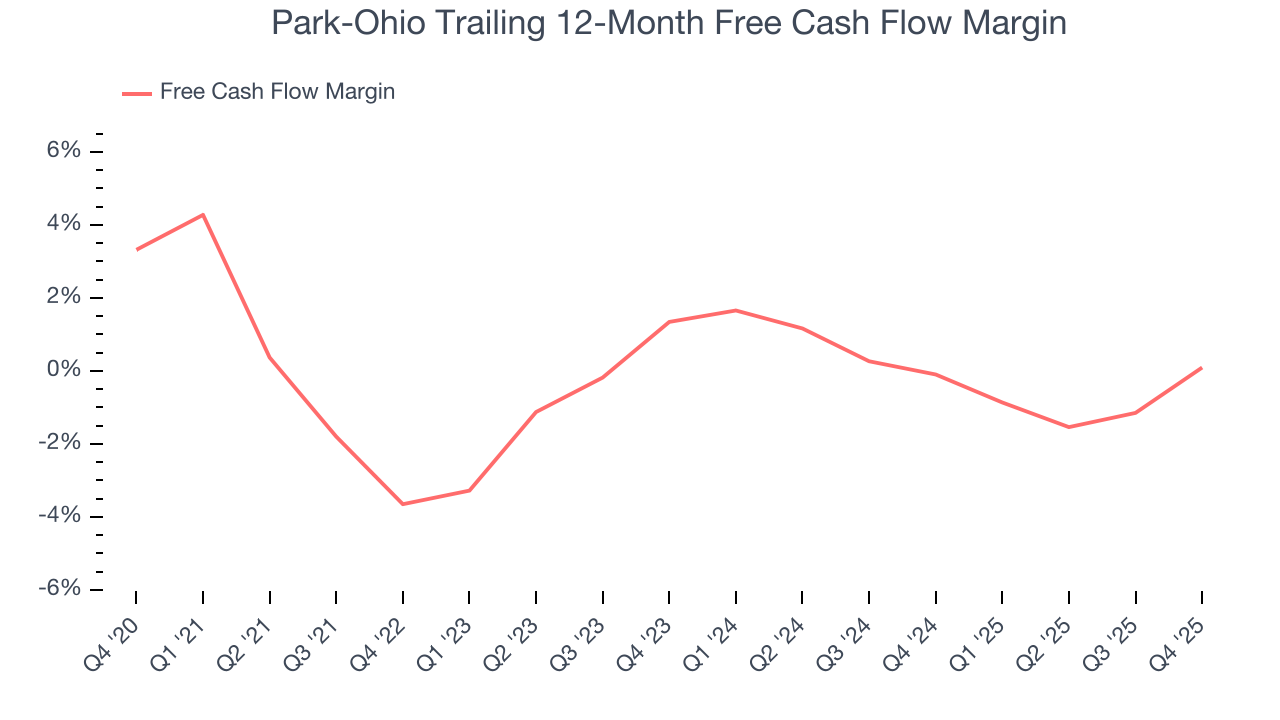

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

While Park-Ohio posted positive free cash flow this quarter, the broader story hasn’t been so clean. Park-Ohio’s demanding reinvestments have drained its resources over the last five years, putting it in a pinch and limiting its ability to return capital to investors. Its free cash flow margin averaged negative 1.1%, meaning it lit $1.11 of cash on fire for every $100 in revenue.

Taking a step back, an encouraging sign is that Park-Ohio’s margin expanded by 1.9 percentage points during that time. Despite its improvement and recent free cash flow generation, we’d like to see more quarters of positive cash flow before recommending the stock.

Park-Ohio’s free cash flow clocked in at $36 million in Q4, equivalent to a 9.1% margin. This result was good as its margin was 4.9 percentage points higher than in the same quarter last year, building on its favorable historical trend.

10. Return on Invested Capital (ROIC)

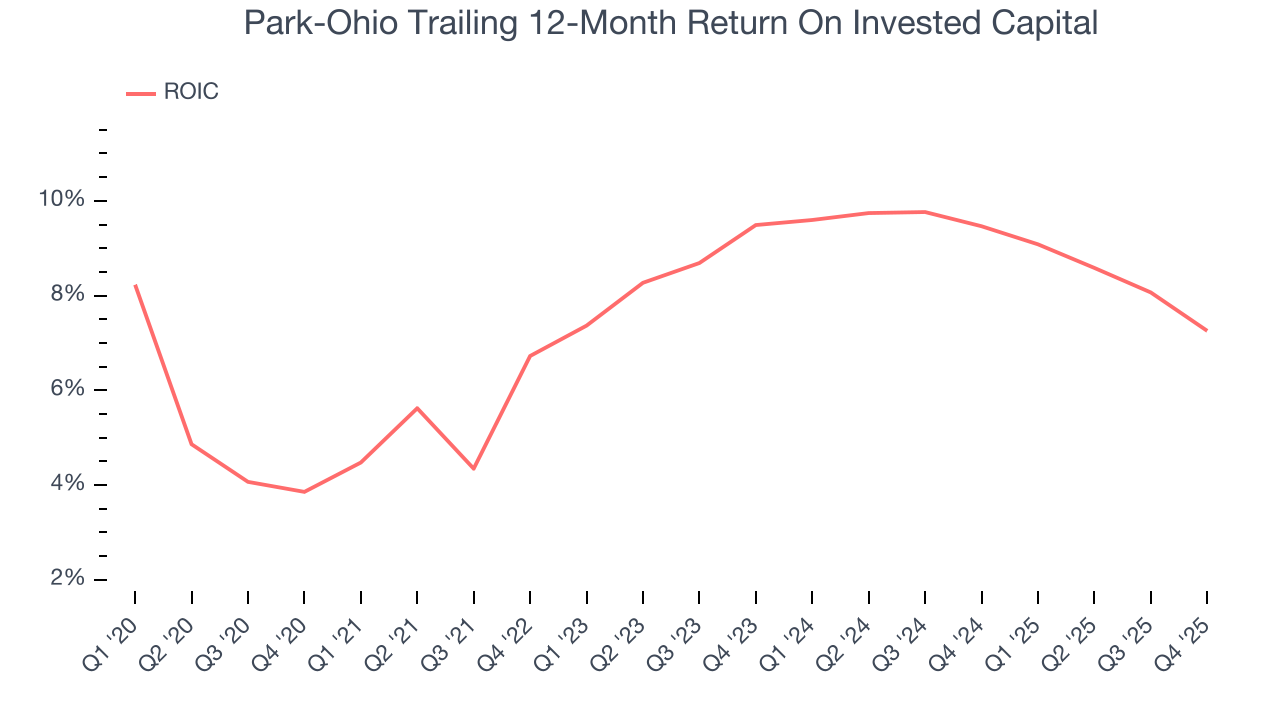

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Park-Ohio historically did a mediocre job investing in profitable growth initiatives. Its four-year average ROIC was 8.2%, somewhat low compared to the best industrials companies that consistently pump out 20%+.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Unfortunately, Park-Ohio’s ROIC has stayed the same over the last few years. If the company wants to become an investable business, it must improve its returns by generating more profitable growth.

11. Balance Sheet Assessment

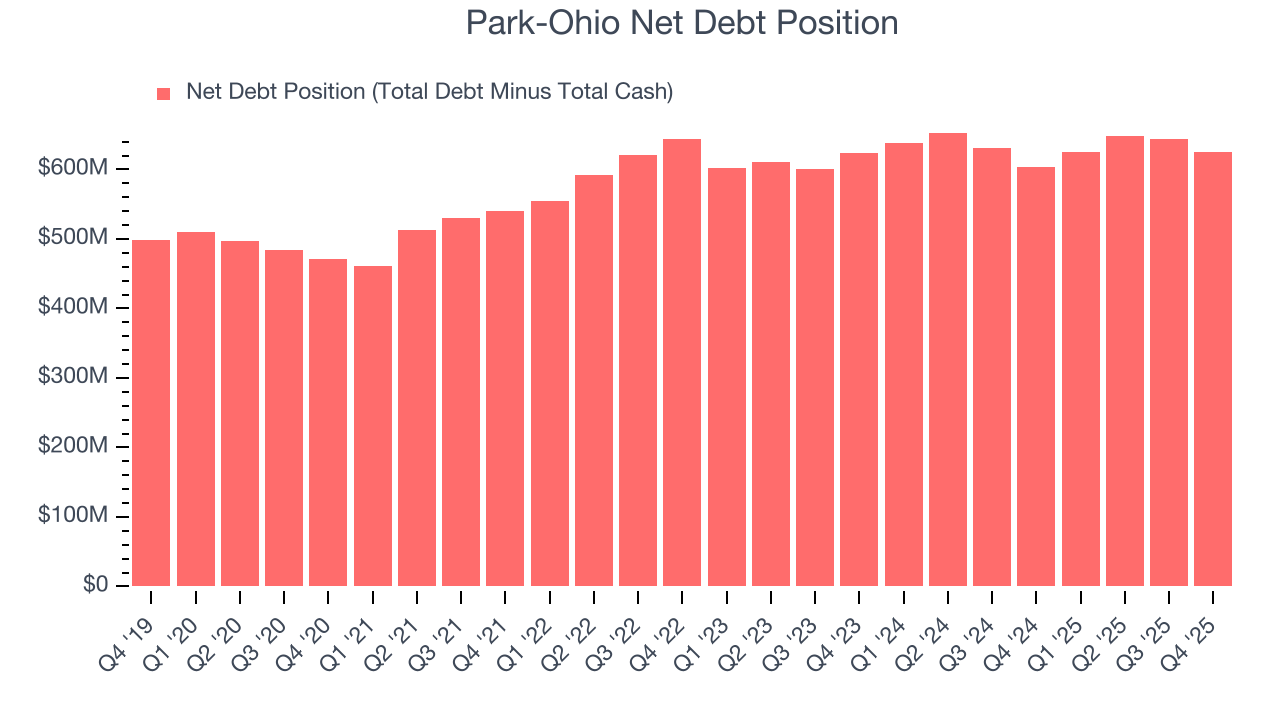

Park-Ohio reported $44.8 million of cash and $670.3 million of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $138.6 million of EBITDA over the last 12 months, we view Park-Ohio’s 4.5× net-debt-to-EBITDA ratio as safe. We also see its $47.5 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

12. Key Takeaways from Park-Ohio’s Q4 Results

It was great to see Park-Ohio’s full-year revenue guidance top analysts’ expectations. We were also happy its EBITDA outperformed Wall Street’s estimates. On the other hand, its full-year EPS guidance missed and its EPS fell short of Wall Street’s estimates. Overall, this was a softer quarter. The stock remained flat at $26.50 immediately after reporting.

13. Is Now The Time To Buy Park-Ohio?

Updated: March 14, 2026 at 11:23 PM EDT

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in Park-Ohio.

Park-Ohio doesn’t pass our quality test. First off, its revenue growth was uninspiring over the last five years. While its astounding EPS growth over the last five years shows its profits are trickling down to shareholders, the downside is its cash burn raises the question of whether it can sustainably maintain growth. On top of that, its low gross margins indicate some combination of competitive pressures and high production costs.

Park-Ohio’s P/E ratio based on the next 12 months is 7.9x. While this valuation is optically cheap, the potential downside is huge given its shaky fundamentals. There are more exciting stocks to buy at the moment.

Wall Street analysts have a consensus one-year price target of $37 on the company (compared to the current share price of $24.51).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.