Plug Power (PLUG)

We’re cautious of Plug Power. Its sales have recently flopped and its historical cash burn means it has few resources to reignite growth.― StockStory Analyst Team

1. News

2. Summary

Why Plug Power Is Not Exciting

Powering forklifts for Walmart’s distribution centers, Plug Power (NASDAQ:PLUG) provides hydrogen fuel cells used to power electric motors.

- Negative 44.6% gross margin means it loses money on every sale and must pivot or scale quickly to survive

- Suboptimal cost structure is highlighted by its history of operating margin losses

- Limited cash reserves may force the company to seek unfavorable financing terms that could dilute shareholders

Plug Power doesn’t measure up to our expectations. We believe there are better businesses elsewhere.

Why There Are Better Opportunities Than Plug Power

At $2.15 per share, Plug Power trades at 3.7x forward price-to-sales. The market typically values companies like Plug Power based on their anticipated profits for the next 12 months, but it expects the business to lose money. We also think the upside isn’t great compared to the potential downside here - there are more exciting stocks to buy.

We’d rather pay up for companies with elite fundamentals than get a bargain on poor ones. Cheap stocks can be value traps, and as their performance deteriorates, they will stay cheap or get even cheaper.

3. Plug Power (PLUG) Research Report: Q4 CY2025 Update

Fuel cell technology Plug Power (NASDAQ:PLUG) reported Q4 CY2025 results exceeding the market’s revenue expectations, with sales up 17.6% year on year to $225.2 million. Its non-GAAP loss of $0.06 per share was 43.9% above analysts’ consensus estimates.

Plug Power (PLUG) Q4 CY2025 Highlights:

- Revenue: $225.2 million vs analyst estimates of $217.6 million (17.6% year-on-year growth, 3.5% beat)

- Adjusted EPS: -$0.06 vs analyst estimates of -$0.11 (43.9% beat)

- Adjusted EBITDA: -$757.7 million (-336% margin, 40% year-on-year growth)

- Adjusted EBITDA Margin: -336%, up from -660% in the same quarter last year

- Free Cash Flow was -$153 million compared to -$165.2 million in the same quarter last year

- Market Capitalization: $2.48 billion

Company Overview

Powering forklifts for Walmart’s distribution centers, Plug Power (NASDAQ:PLUG) provides hydrogen fuel cells used to power electric motors.

Plug Power was founded in 1997 and initially focused on developing fuel cell technology. Fuel cells are devices that generate electricity through a chemical reaction rather than by burning fuel. They work like a battery but instead of being recharged, they produce electricity as long as they have a hydrogen supply.

Since its founding, Plug Power has grown through the acquisitions, both small and large, that enhanced its technological capabilities. Notably, it acquired United Hydrogen Group and Giner ELX in 2020, which helped it make and supply more hydrogen essential for its fuel cell technology.

Today, Plug Power's GenDrive systems use fuel cells to power electric forklifts, delivery vans, and drones. To keep its fuel cells running, Plug Power provides GenFuel, a complete setup for producing, storing, and dispensing hydrogen on-site. This means companies don’t have to worry about where to get hydrogen or how to transport it. Lastly, it offers reliable backup power sources for places like data centers or communication towers.

Plug Power primarily engages in long-term contracts that outline agreements regarding equipment supply, maintenance services, hydrogen fuel delivery, and performance guarantees. These contracts often range from three to five years.

4. Renewable Energy

Renewable energy companies are buoyed by the secular trend of green energy that is upending traditional power generation. Those who innovate and evolve with this dynamic market can win share while those who continue to rely on legacy technologies can see diminishing demand, which includes headwinds from increasing regulation against “dirty” energy. Additionally, these companies are at the whim of economic cycles, as interest rates can impact the willingness to invest in renewable energy projects.

Competitors of Plug Power include Ballard Power Systems (NASDAQ:BLDP), FuelCell Energy (NASDAQ:FCEL), and Bloom Energy (NYSE:BE).

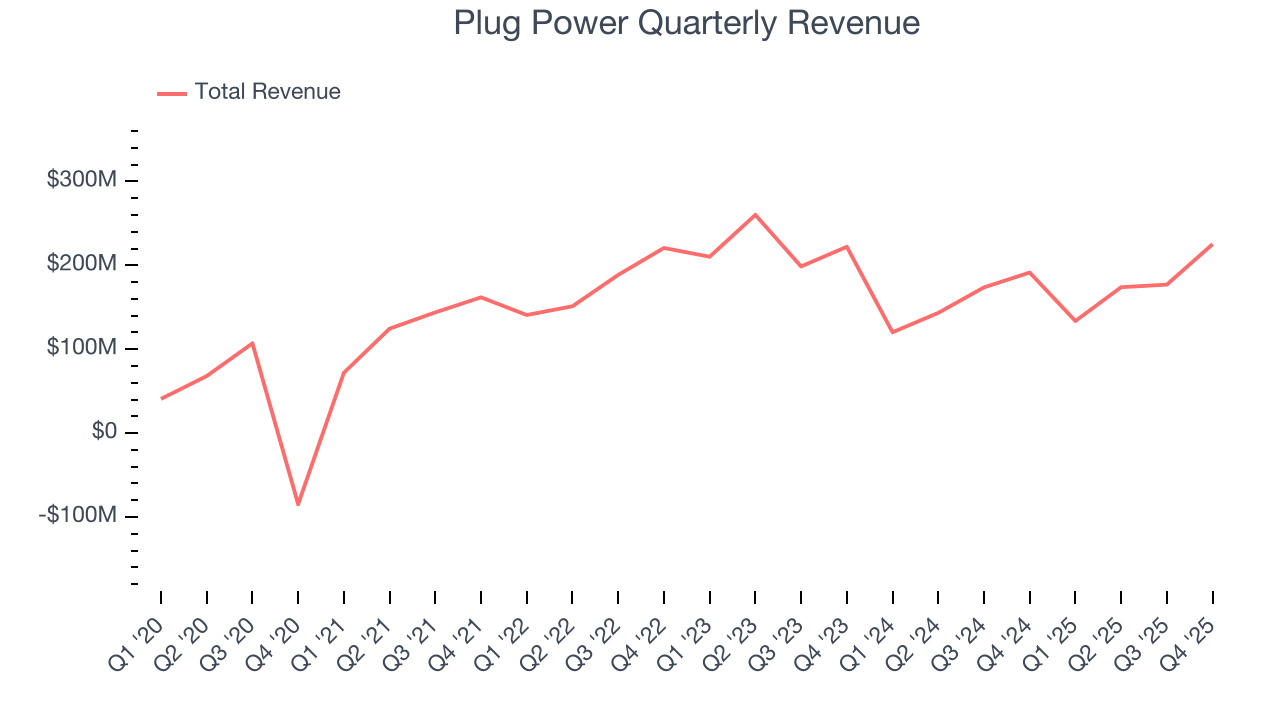

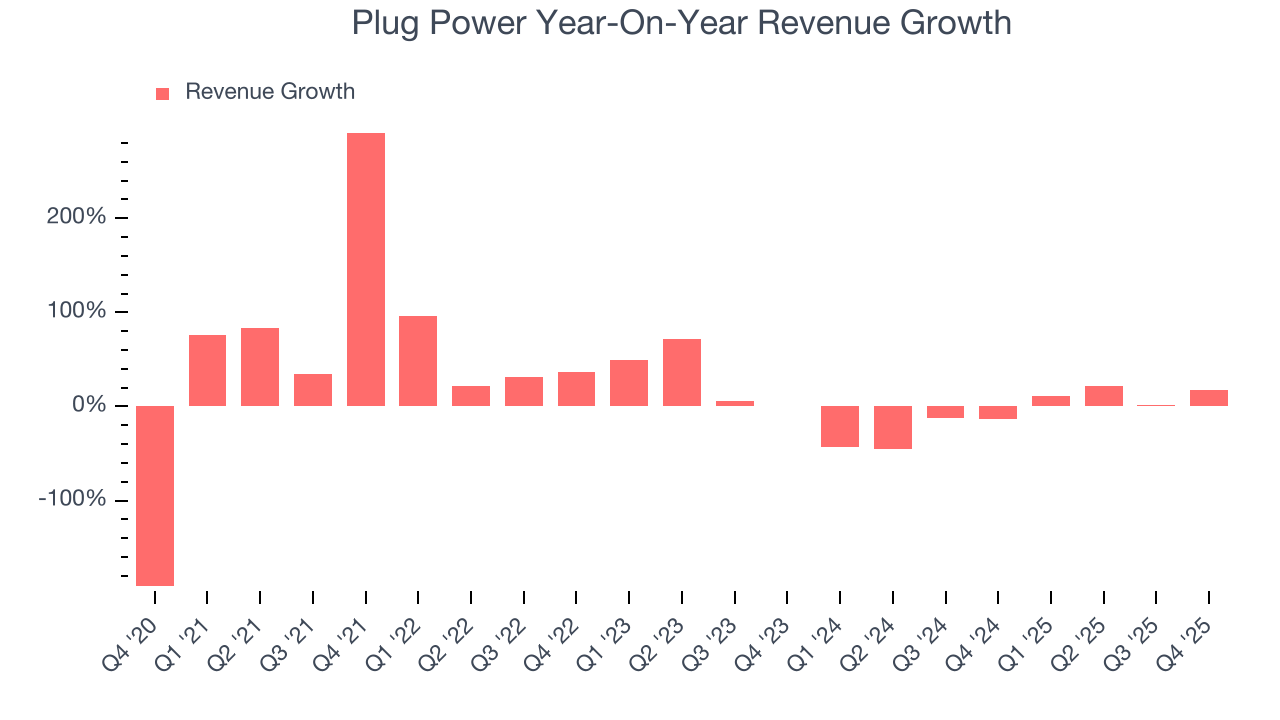

5. Revenue Growth

A company’s long-term performance is an indicator of its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Luckily, Plug Power’s sales grew at an incredible 40.2% compounded annual growth rate over the last five years. Its growth beat the average industrials company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Plug Power’s recent performance marks a sharp pivot from its five-year trend as its revenue has shown annualized declines of 10.8% over the last two years.

This quarter, Plug Power reported year-on-year revenue growth of 17.6%, and its $225.2 million of revenue exceeded Wall Street’s estimates by 3.5%.

Looking ahead, sell-side analysts expect revenue to grow 18.2% over the next 12 months, an improvement versus the last two years. This projection is eye-popping and indicates its newer products and services will spur better top-line performance.

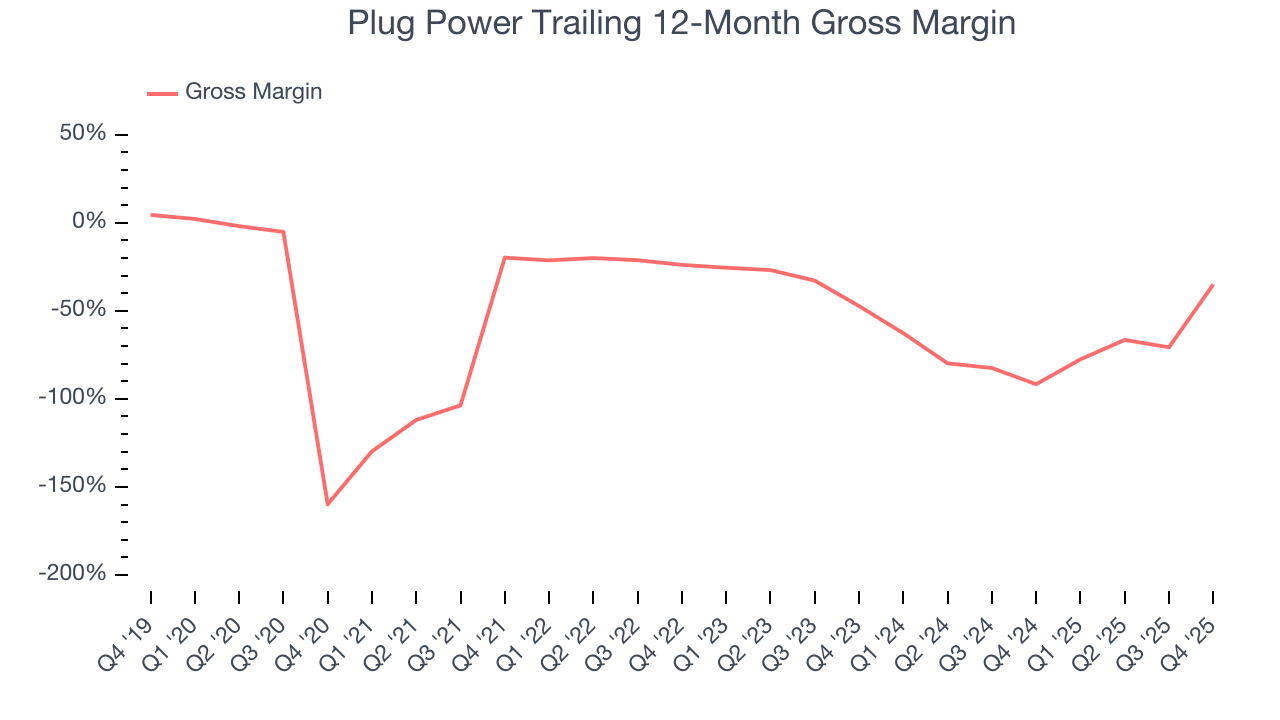

6. Gross Margin & Pricing Power

Plug Power has bad unit economics for an industrials business, signaling it operates in a competitive market. As you can see below, it averaged a negative 44.1% gross margin over the last five years. That means Plug Power lost $44.06 for every $100 in revenue.

This quarter, Plug Power’s gross profit margin was 2.4%, up 119.5 percentage points year on year. However, company was unprofitable on a full-year basis, suggesting it needs to make changes.

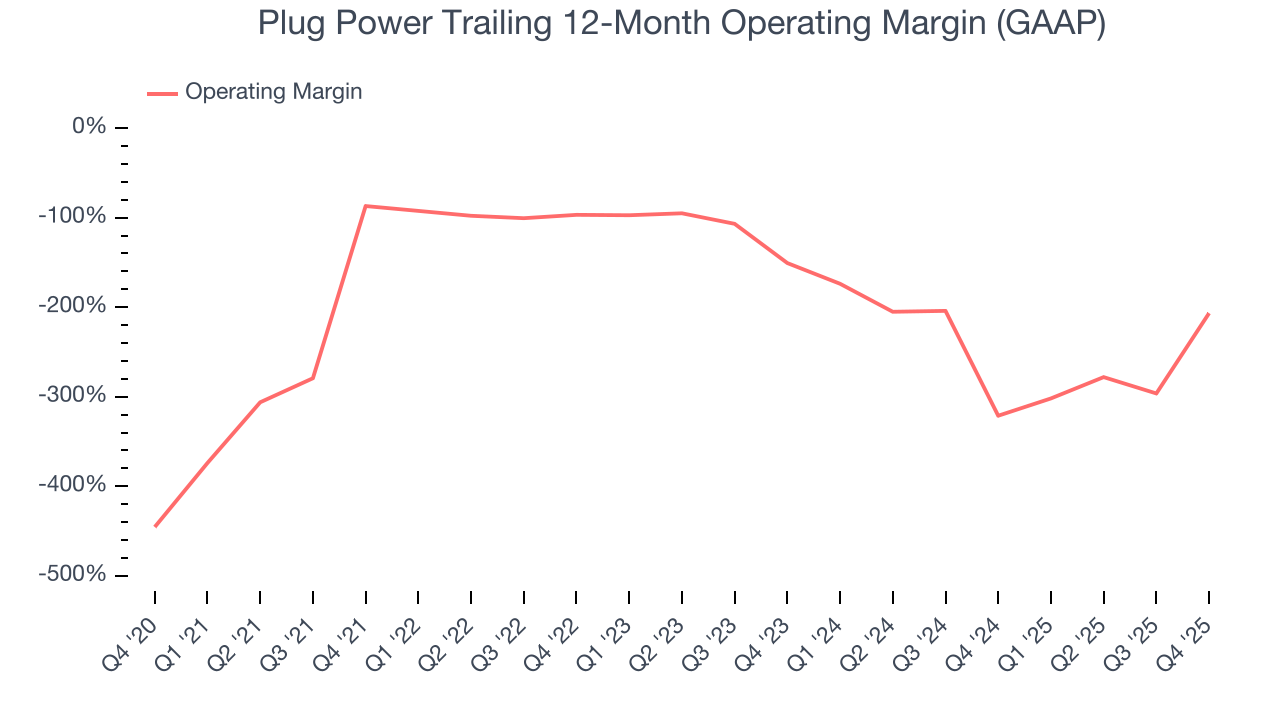

7. Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Plug Power’s high expenses have contributed to an average operating margin of negative 173% over the last five years. Unprofitable industrials companies require extra attention because they could get caught swimming naked when the tide goes out. It’s hard to trust that the business can endure a full cycle.

Looking at the trend in its profitability, Plug Power’s operating margin decreased significantly over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. Plug Power’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers.

In Q4, Plug Power generated a negative 339% operating margin.

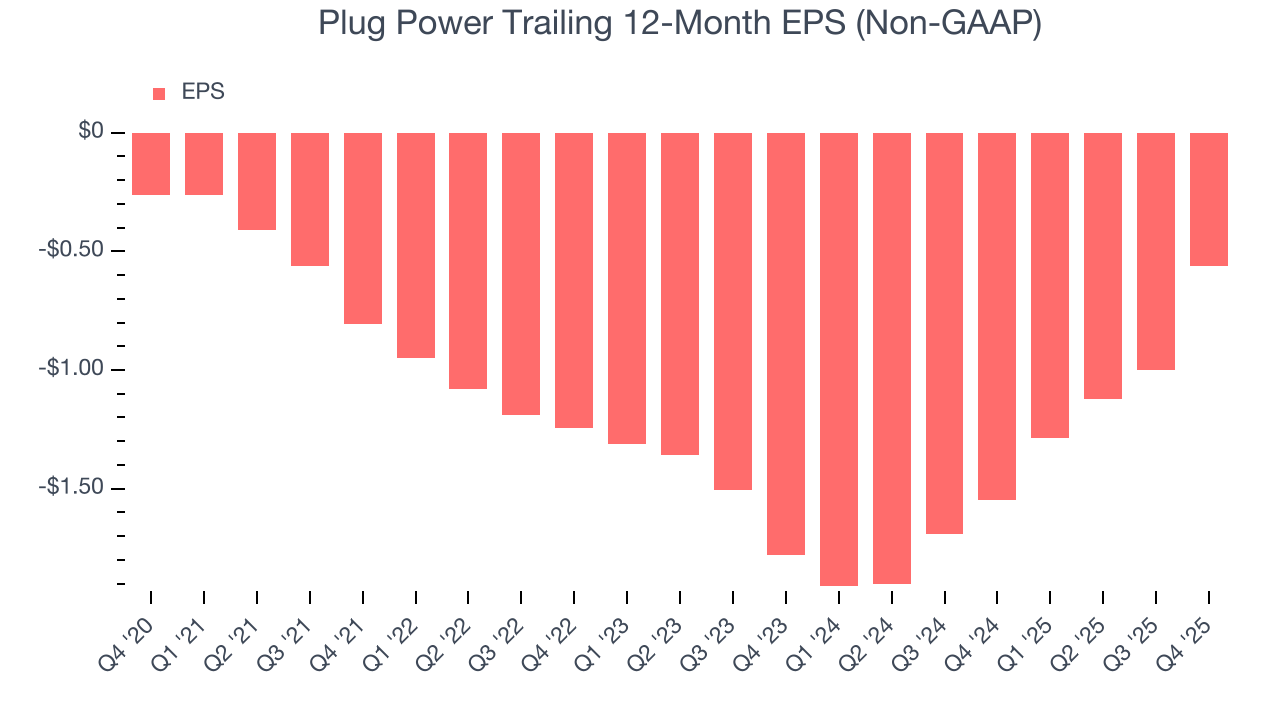

8. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Plug Power’s earnings losses deepened over the last five years as its EPS dropped 16.4% annually. We tend to steer our readers away from companies with falling EPS, where diminishing earnings could imply changing secular trends and preferences. If the tide turns unexpectedly, Plug Power’s low margin of safety could leave its stock price susceptible to large downswings.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Plug Power, its two-year annual EPS growth of 43.8% was higher than its five-year trend. Its improving earnings is an encouraging data point, but a caveat is that its EPS is still in the red.

In Q4, Plug Power reported adjusted EPS of negative $0.06, up from negative $0.50 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Plug Power to improve its earnings losses. Analysts forecast its full-year EPS of negative $0.56 will advance to negative $0.31.

9. Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

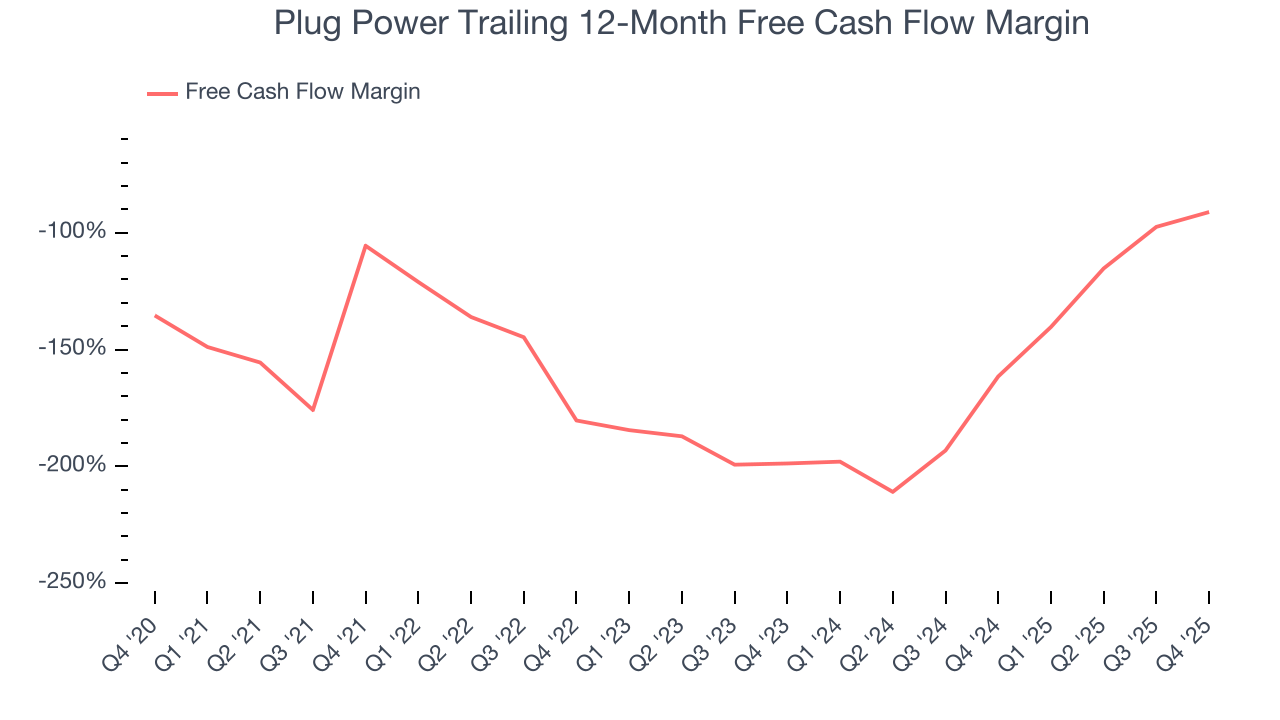

Plug Power’s demanding reinvestments have drained its resources over the last five years, putting it in a pinch and limiting its ability to return capital to investors. Its free cash flow margin averaged negative 152%, meaning it lit $152.31 of cash on fire for every $100 in revenue.

Taking a step back, an encouraging sign is that Plug Power’s margin expanded by 14.4 percentage points during that time. In light of its glaring cash burn, however, this improvement is a bucket of hot water in a cold ocean.

Plug Power burned through $153 million of cash in Q4, equivalent to a negative 67.9% margin. The company’s cash burn was similar to its $165.2 million of lost cash in the same quarter last year.

10. Balance Sheet Risk

As long-term investors, the risk we care about most is the permanent loss of capital, which can happen when a company goes bankrupt or raises money from a disadvantaged position. This is separate from short-term stock price volatility, something we are much less bothered by.

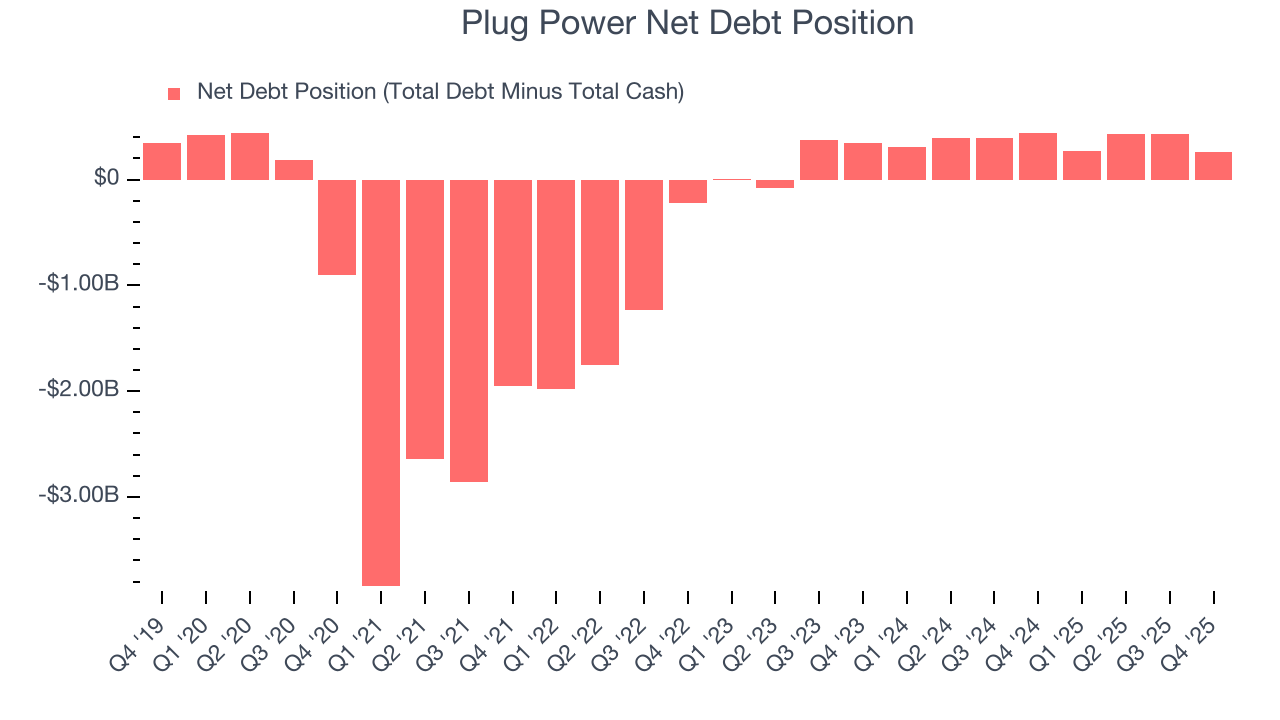

Plug Power burned through $647 million of cash over the last year, and its $627.3 million of debt exceeds the $368.5 million of cash on its balance sheet. This is a deal breaker for us because indebted loss-making companies spell trouble.

Unless the Plug Power’s fundamentals change quickly, it might find itself in a position where it must raise capital from investors to continue operating. Whether that would be favorable is unclear because dilution is a headwind for shareholder returns.

We remain cautious of Plug Power until it generates consistent free cash flow or any of its announced financing plans materialize on its balance sheet.

11. Key Takeaways from Plug Power’s Q4 Results

It was good to see Plug Power beat analysts’ EPS expectations this quarter. We were also excited its revenue outperformed Wall Street’s estimates by a wide margin. On the other hand, its EBITDA missed. Overall, we think this was a decent quarter with some key metrics above expectations. The stock traded up 7.7% to $1.96 immediately following the results.

12. Is Now The Time To Buy Plug Power?

Updated: March 14, 2026 at 11:41 PM EDT

A common mistake we notice when investors are deciding whether to buy a stock or not is that they simply look at the latest earnings results. Business quality and valuation matter more, so we urge you to understand these dynamics as well.

Plug Power’s business quality ultimately falls short of our standards. Although its revenue growth was exceptional over the last five years, it’s expected to deteriorate over the next 12 months and its declining EPS over the last five years makes it a less attractive asset to the public markets. And while the company’s rising cash profitability gives it more optionality, the downside is its declining operating margin shows the business has become less efficient.

Plug Power’s forward price-to-sales ratio is 3.7x. The market typically values companies like Plug Power based on their anticipated profits for the next 12 months, but it expects the business to lose money. We also think the upside isn’t great compared to the potential downside here - there are more exciting stocks to buy.

Wall Street analysts have a consensus one-year price target of $2.74 on the company (compared to the current share price of $2.15).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.