Plexus (PLXS)

We’re skeptical of Plexus. Its weak sales growth and declining returns on capital show its demand and profits are shrinking.― StockStory Analyst Team

1. News

2. Summary

Why Plexus Is Not Exciting

With over 20,000 team members across 26 global facilities, Plexus (NASDAQ:PLXS) designs, manufactures, and services complex electronic products for companies in aerospace/defense, healthcare, and industrial sectors.

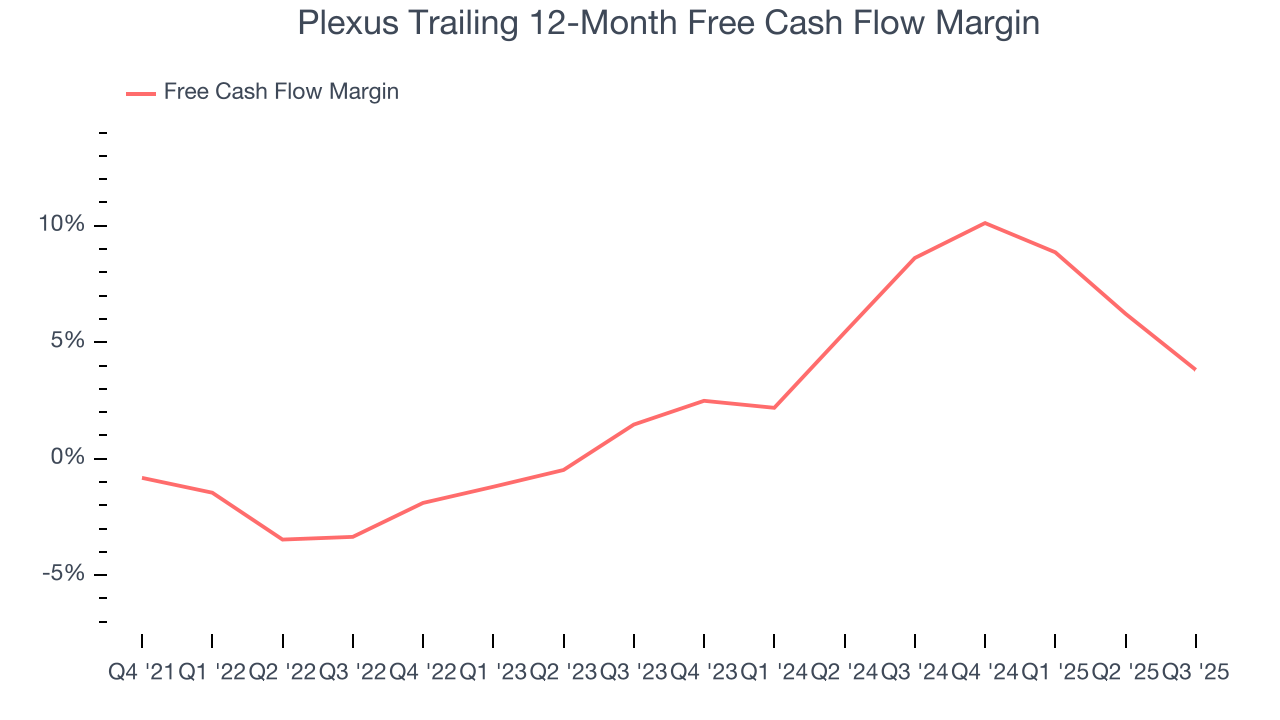

- Ability to fund investments or reward shareholders with increased buybacks or dividends is restricted by its weak free cash flow margin of 2.4% for the last five years

- Subpar adjusted operating margin constrains its ability to invest in process improvements or effectively respond to new competitive threats

- On the plus side, its estimated revenue growth of 11.8% for the next 12 months implies demand will accelerate from its two-year trend

Plexus doesn’t fulfill our quality requirements. There are better opportunities in the market.

Why There Are Better Opportunities Than Plexus

Plexus is trading at $203.01 per share, or 24.5x forward P/E. This multiple is higher than most business services companies, and we think it’s quite expensive for the weaker revenue growth you get.

We prefer to invest in similarly-priced but higher-quality companies with superior earnings growth.

3. Plexus (PLXS) Research Report: Q4 CY2025 Update

Electronic manufacturing services company Plexus (NASDAQ:PLXS) met Wall Streets revenue expectations in Q4 CY2025, with sales up 9.6% year on year to $1.07 billion. The company expects next quarter’s revenue to be around $1.13 billion, coming in 4.1% above analysts’ estimates. Its non-GAAP profit of $1.78 per share was 2.7% above analysts’ consensus estimates.

Plexus (PLXS) Q4 CY2025 Highlights:

- Revenue: $1.07 billion vs analyst estimates of $1.07 billion (9.6% year-on-year growth, in line)

- Adjusted EPS: $1.78 vs analyst estimates of $1.73 (2.7% beat)

- Revenue Guidance for Q1 CY2026 is $1.13 billion at the midpoint, above analyst estimates of $1.09 billion

- Adjusted EPS guidance for Q1 CY2026 is $1.88 at the midpoint, above analyst estimates of $1.76

- Operating Margin: 5.1%, in line with the same quarter last year

- Market Capitalization: $4.64 billion

Company Overview

With over 20,000 team members across 26 global facilities, Plexus (NASDAQ:PLXS) designs, manufactures, and services complex electronic products for companies in aerospace/defense, healthcare, and industrial sectors.

Plexus operates as a contract manufacturer that specializes in handling technically challenging products with demanding regulatory requirements. Unlike traditional electronics manufacturers that focus on high-volume consumer goods, Plexus targets complex, mission-critical products where precision and reliability are paramount.

The company provides end-to-end solutions throughout a product's lifecycle. This begins with design and development services at its six global design centers, where engineers create new products with manufacturability and serviceability in mind. Plexus then manages supply chain logistics, handles new product introductions, and conducts full-scale manufacturing at its facilities across the Americas, Asia-Pacific, and EMEA regions.

A medical device company might partner with Plexus to design and manufacture life-saving equipment like ventilators or patient monitoring systems. Plexus would handle everything from initial design to sourcing specialized components, manufacturing the devices in clean room environments, and providing ongoing repair services.

Plexus generates revenue primarily through manufacturing services, charging customers for both the production work and the procurement of materials. The company typically operates on a turnkey basis, where it purchases and manages all materials needed for assembly, though it sometimes works on a consignment model where customers provide materials.

All Plexus facilities maintain ISO9001:2015 quality certification, with additional capabilities to meet specialized regulatory requirements like FDA standards for medical devices. This focus on quality management and regulatory compliance allows Plexus to serve industries where product failures could have serious consequences.

4. Electronic Components & Manufacturing

The sector could see higher demand as the prevalence of advanced electronics increases in industries such as automotive, healthcare, aerospace, and computing. The high-performance components and contract manufacturing expertise required for autonomous vehicles and cloud computing datacenters, for instance, will benefit companies in the space. However, headwinds include geopolitical risks, particularly U.S.-China trade tensions that could disrupt component sourcing and production as the Trump administration takes an increasingly antagonizing stance on foreign relations. Additionally, stringent environmental regulations on e-waste and emissions could force the industry to pivot in potentially costly ways.

Plexus competes with other electronic manufacturing services providers including Jabil (NYSE:JBL), Flex (NASDAQ:FLEX), Benchmark Electronics (NYSE:BHE), and Celestica (NYSE:CLS), though Plexus differentiates itself by focusing specifically on complex, highly regulated products rather than high-volume consumer electronics.

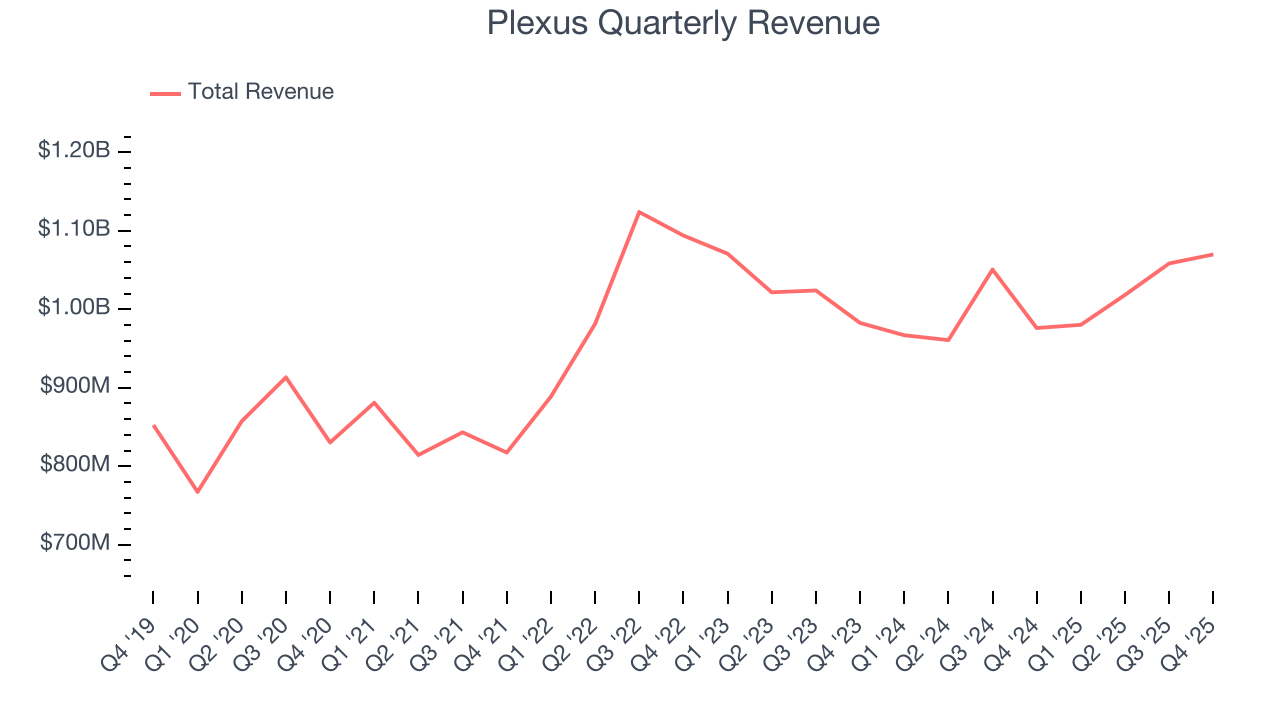

5. Revenue Growth

A company’s long-term performance is an indicator of its overall quality. Any business can have short-term success, but a top-tier one grows for years.

With $4.13 billion in revenue over the past 12 months, Plexus is one of the larger companies in the business services industry and benefits from a well-known brand that influences purchasing decisions. However, its scale is a double-edged sword because it’s harder to find incremental growth when you’ve penetrated most of the market. To expand meaningfully, Plexus likely needs to tweak its prices, innovate with new offerings, or enter new markets.

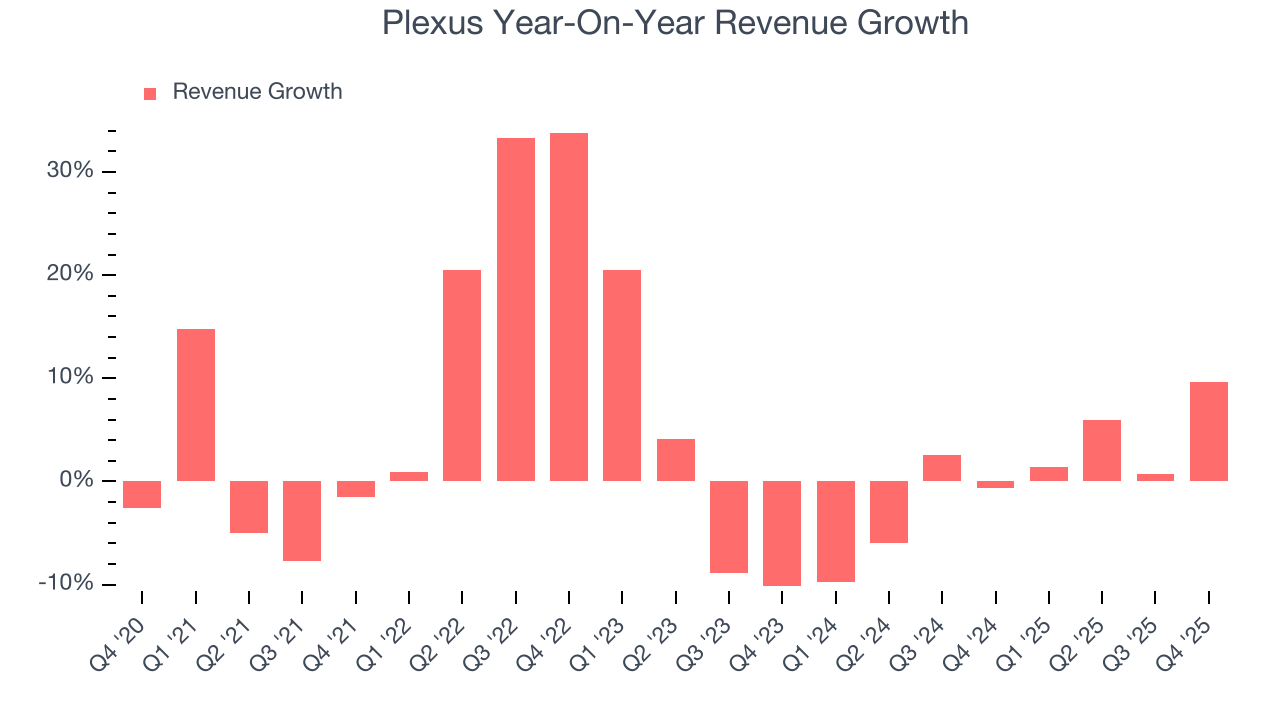

As you can see below, Plexus’s 4.1% annualized revenue growth over the last five years was mediocre. This shows it couldn’t generate demand in any major way and is a tough starting point for our analysis.

Long-term growth is the most important, but within business services, a half-decade historical view may miss new innovations or demand cycles. Plexus’s recent performance shows its demand has slowed as its revenue was flat over the last two years.

This quarter, Plexus grew its revenue by 9.6% year on year, and its $1.07 billion of revenue was in line with Wall Street’s estimates. Company management is currently guiding for a 15.3% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 7.6% over the next 12 months, an improvement versus the last two years. This projection is commendable and implies its newer products and services will spur better top-line performance.

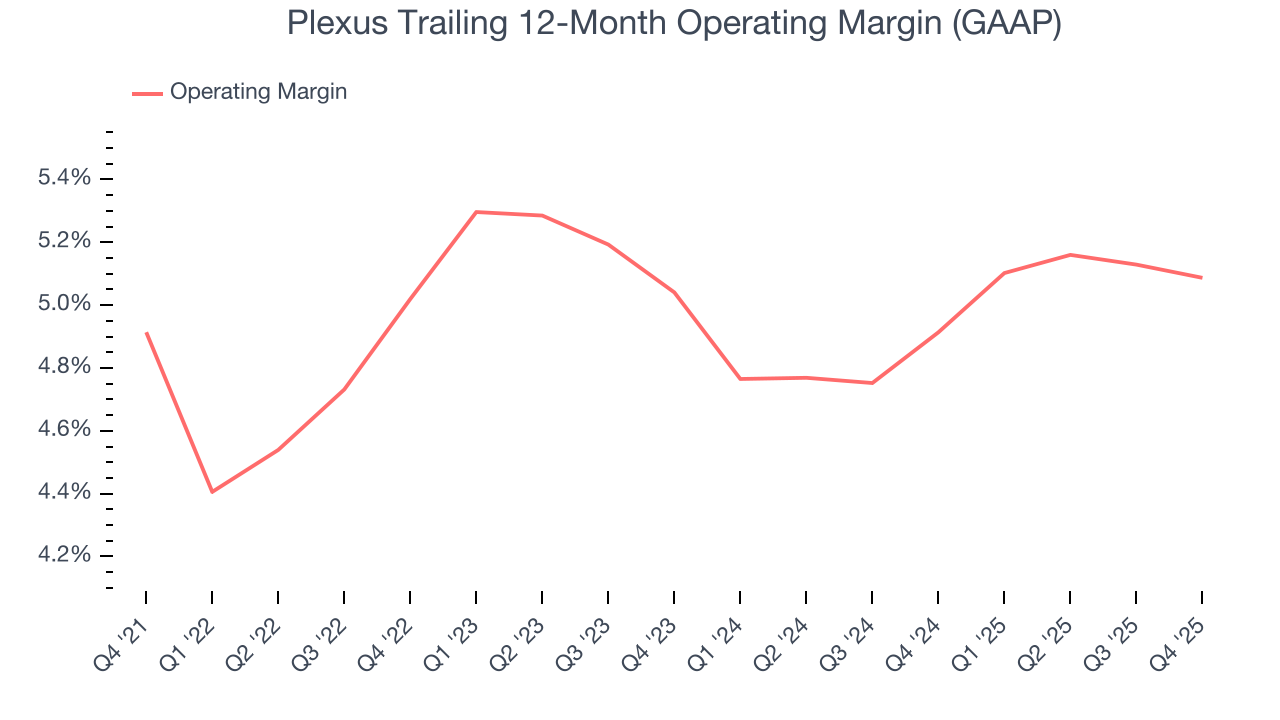

6. Operating Margin

Plexus’s operating margin might fluctuated slightly over the last 12 months but has remained more or less the same, averaging 5% over the last five years. This profitability was lousy for a business services business and caused by its suboptimal cost structure.

Analyzing the trend in its profitability, Plexus’s operating margin might fluctuated slightly but has generally stayed the same over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

This quarter, Plexus generated an operating margin profit margin of 5.1%, in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

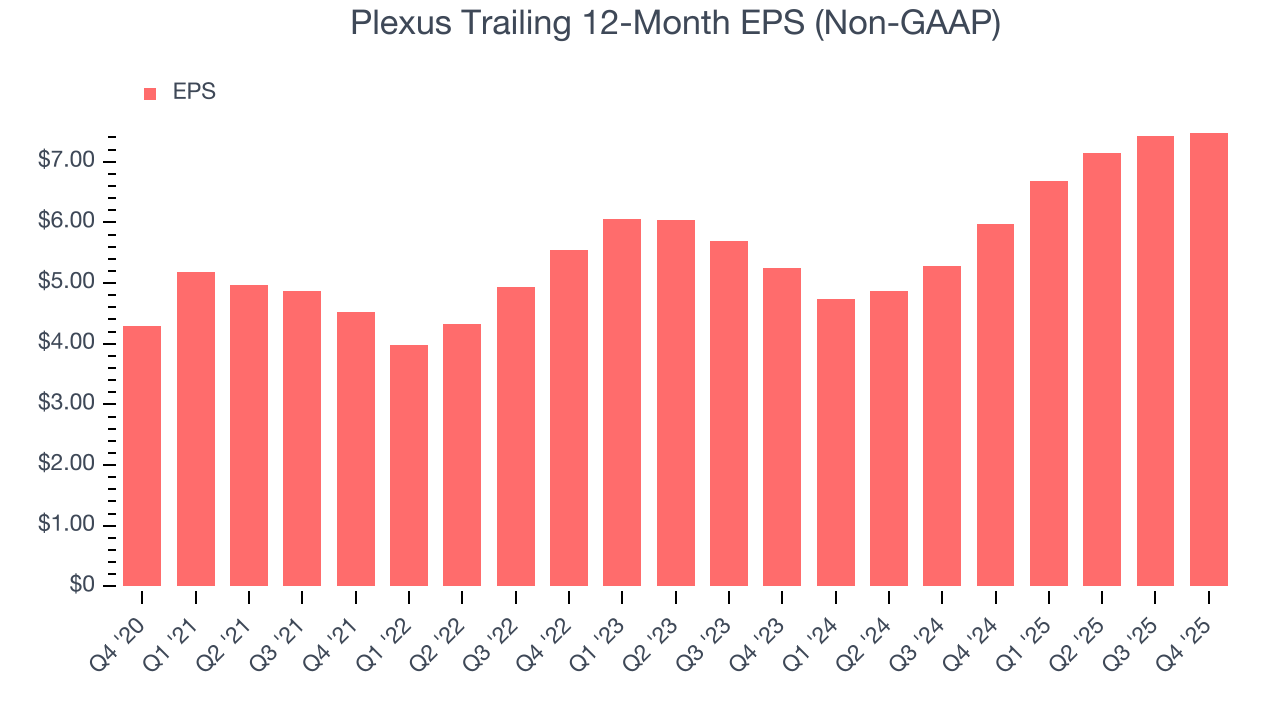

7. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Plexus’s EPS grew at a remarkable 11.7% compounded annual growth rate over the last five years, higher than its 4.1% annualized revenue growth. However, this alone doesn’t tell us much about its business quality because its operating margin didn’t improve.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Plexus, its two-year annual EPS growth of 19.4% was higher than its five-year trend. We love it when earnings growth accelerates, especially when it accelerates off an already high base.

In Q4, Plexus reported adjusted EPS of $1.78, up from $1.73 in the same quarter last year. This print beat analysts’ estimates by 2.7%. Over the next 12 months, Wall Street expects Plexus’s full-year EPS of $7.48 to grow 1.8%.

8. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Plexus has shown weak cash profitability over the last five years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 2.8%, subpar for a business services business.

9. Return on Invested Capital (ROIC)

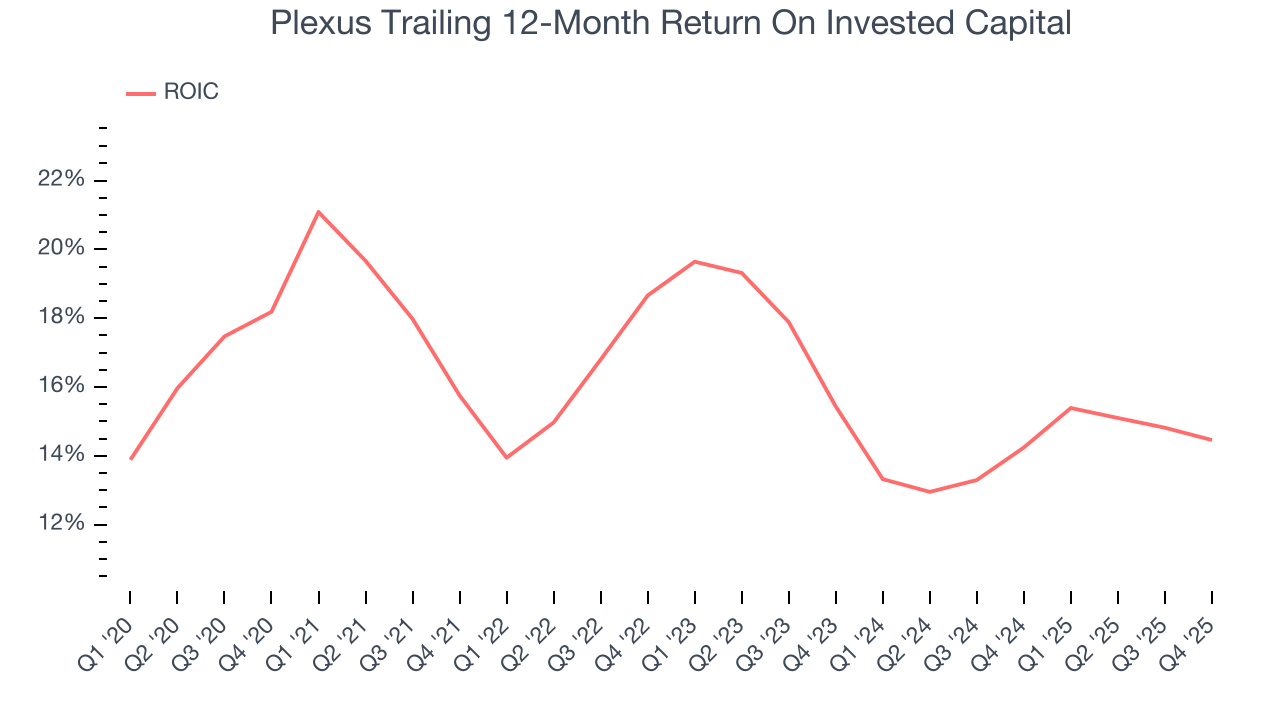

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Although Plexus hasn’t been the highest-quality company lately, it historically found a few growth initiatives that worked. Its five-year average ROIC was 15.7%, higher than most business services businesses.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. On average, Plexus’s ROIC decreased by 2.9 percentage points annually over the last few years. We like what management has done in the past, but its declining returns are perhaps a symptom of fewer profitable growth opportunities.

10. Balance Sheet Assessment

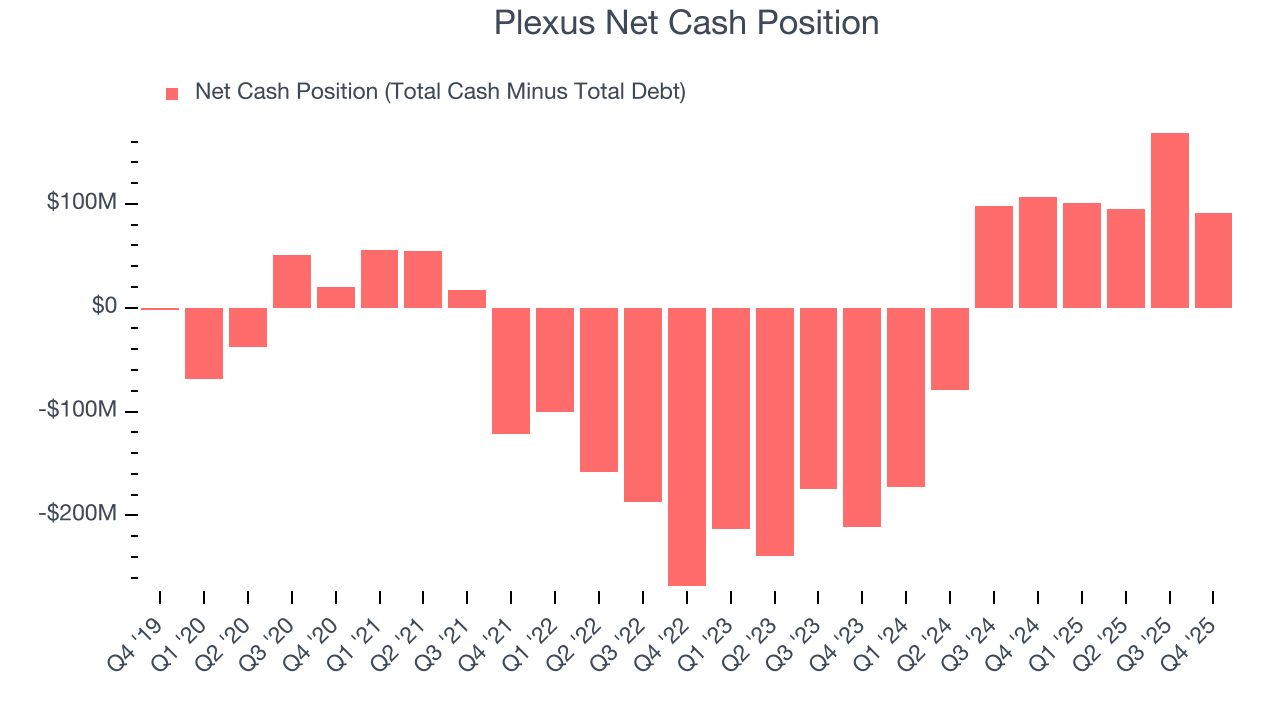

Businesses that maintain a cash surplus face reduced bankruptcy risk.

Plexus is a profitable, well-capitalized company with $248.8 million of cash and $158 million of debt on its balance sheet. This $90.85 million net cash position gives it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

11. Key Takeaways from Plexus’s Q4 Results

We were impressed by how significantly Plexus blew past analysts’ EPS guidance for next quarter expectations this quarter. We were also glad its revenue guidance for next quarter trumped Wall Street’s estimates. On the other hand, its revenue was in line. Zooming out, we think this quarter featured some important positives. The stock remained flat at $180.81 immediately following the results.

12. Is Now The Time To Buy Plexus?

Updated: March 23, 2026 at 10:05 PM EDT

Before making an investment decision, investors should account for Plexus’s business fundamentals and valuation in addition to what happened in the latest quarter.

Plexus’s business quality ultimately falls short of our standards. To kick things off, its revenue growth was mediocre over the last five years. While its remarkable EPS growth over the last five years shows its profits are trickling down to shareholders, the downside is its low free cash flow margins give it little breathing room. On top of that, its operating margins are low compared to other business services companies.

Plexus’s P/E ratio based on the next 12 months is 24.5x. At this valuation, there’s a lot of good news priced in - you can find more timely opportunities elsewhere.

Wall Street analysts have a consensus one-year price target of $200.80 on the company (compared to the current share price of $203.01).