Portillo's (PTLO)

Portillo's keeps us up at night. Its sales have underperformed and its low returns on capital show it has few growth opportunities.― StockStory Analyst Team

1. News

2. Summary

Why We Think Portillo's Will Underperform

Begun as a Chicago hot dog stand in 1963, Portillo’s (NASDAQ:PTLO) is a casual restaurant chain that serves Chicago-style hot dogs and beef sandwiches as well as fries and shakes.

- Investment activity picked up over the last year, pressuring its weak free cash flow profitability

- Lagging same-store sales over the past two years suggest it might have to change its pricing and marketing strategy to stimulate demand

- Short cash runway increases the probability of a capital raise that dilutes existing shareholders

Portillo's doesn’t pass our quality test. We’d rather invest in businesses with stronger moats.

Why There Are Better Opportunities Than Portillo's

Portillo's is trading at $5.80 per share, or 30.7x forward P/E. Not only does Portillo's trade at a premium to companies in the restaurant space, but this multiple is also high for its fundamentals.

We prefer to invest in similarly-priced but higher-quality companies with superior earnings growth.

3. Portillo's (PTLO) Research Report: Q4 CY2025 Update

Casual restaurant chain Portillo’s (NASDAQ:PTLO) met Wall Street’s revenue expectations in Q4 CY2025, but sales were flat year on year at $185.7 million. Its GAAP profit of $0.08 per share was 74.3% above analysts’ consensus estimates.

Portillo's (PTLO) Q4 CY2025 Highlights:

- Revenue: $185.7 million vs analyst estimates of $185.7 million (flat year on year, in line)

- EPS (GAAP): $0.08 vs analyst estimates of $0.05 (74.3% beat)

- Adjusted EBITDA: $24.67 million vs analyst estimates of $24.57 million (13.3% margin, in line)

- Operating Margin: 5.6%, down from 7.5% in the same quarter last year

- Locations: 102 at quarter end, up from 94 in the same quarter last year

- Same-Store Sales fell 3.3% year on year (0.4% in the same quarter last year)

- Market Capitalization: $416.5 million

Company Overview

Begun as a Chicago hot dog stand in 1963, Portillo’s (NASDAQ:PTLO) is a casual restaurant chain that serves Chicago-style hot dogs and beef sandwiches as well as fries and shakes.

In addition to the signature dogs and sandwiches, Portillo’s is known for its decadent chocolate cake. Not everything will expand your waistline, though, as the chain has expanded its offerings to include healthier options such as salads and chicken breast sandwiches.

The core Portillo’s customer is diverse. Maybe it’s someone looking for convenient and indulgent food that’s a bit unique compared to the typical fast food menu. Perhaps it’s a family looking for a weekend treat where everyone can find something they like on the menu. Maybe it’s a Chicago native looking for that comfort food from the old neighborhood.

Portillo’s locations feature retro diner themes to ramp up the nostalgia and lively atmosphere. There are tables and booths that are often a feature of diners. Vintage photos featuring Chicago landmarks, celebrities, or pop culture line the walls to remind everyone of the restaurant’s roots.

4. Modern Fast Food

Modern fast food is a relatively newer category representing a middle ground between traditional fast food and sit-down restaurants. These establishments feature an expanded menu selection priced above traditional fast food options, often incorporating fresher and cleaner ingredients to serve customers prioritizing quality. These eateries are capitalizing on the perception that your drive-through burger and fries joint is detrimental to your health because of inferior ingredients.

Competitors offering convenient comfort food that can sometimes conjure nostalgia include Potbelly (NASDAQ:PBPB), Shake Shack (NYSE:SHAK), Brinker International (NYSE:EAT), and The Cheesecake Factory (NASDAQ:CAKE).

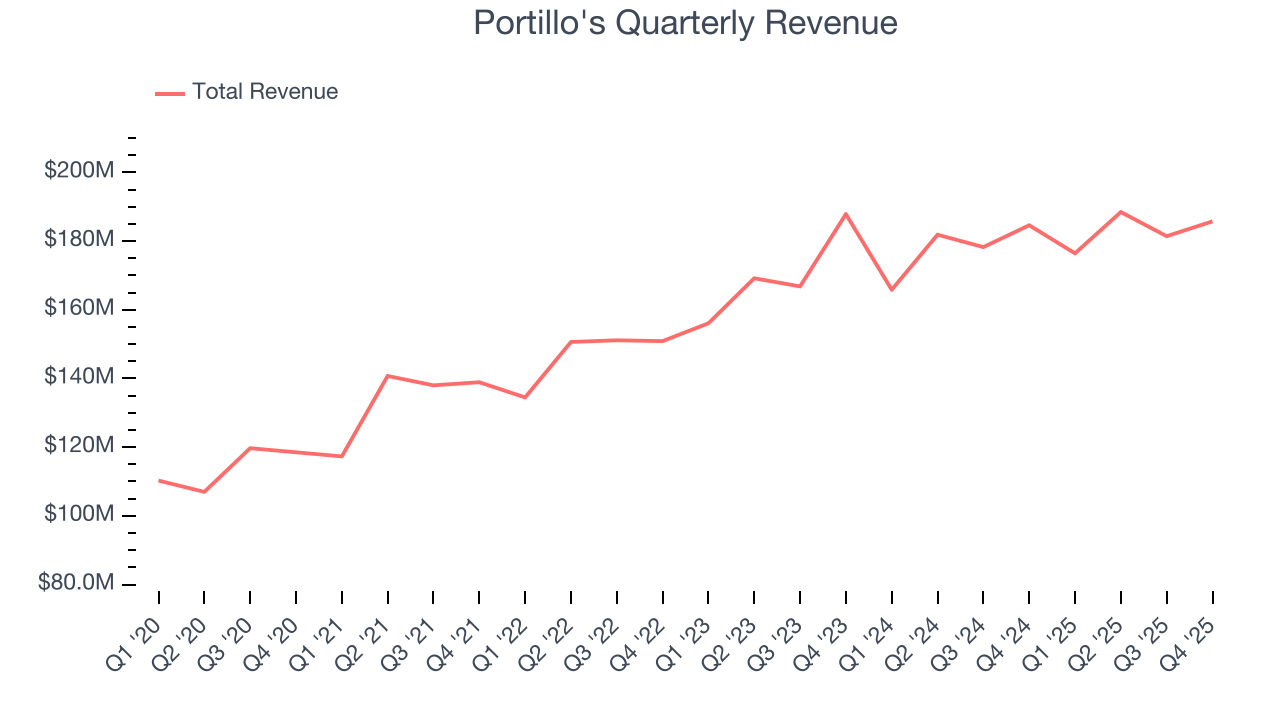

5. Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can have short-term success, but a top-tier one grows for years.

With $732.1 million in revenue over the past 12 months, Portillo's is a small restaurant chain, which sometimes brings disadvantages compared to larger competitors benefiting from better brand awareness and economies of scale. On the bright side, it can grow faster because it has more white space to build new restaurants.

As you can see below, Portillo’s sales grew at a decent 7.3% compounded annual growth rate over the last six years as it opened new restaurants and expanded its reach.

This quarter, Portillo’s $185.7 million of revenue was flat year on year and in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 7.6% over the next 12 months, similar to its six-year rate. This projection is above average for the sector and indicates its newer menu offerings will help maintain its historical top-line performance.

6. Restaurant Performance

Number of Restaurants

A restaurant chain’s total number of dining locations often determines how much revenue it can generate.

Portillo's sported 102 locations in the latest quarter. Over the last two years, it has opened new restaurants at a rapid clip by averaging 11.4% annual growth, among the fastest in the restaurant sector. This gives it a chance to scale into a mid-sized business over time.

When a chain opens new restaurants, it usually means it’s investing for growth because there’s healthy demand for its meals and there are markets where its concepts have few or no locations.

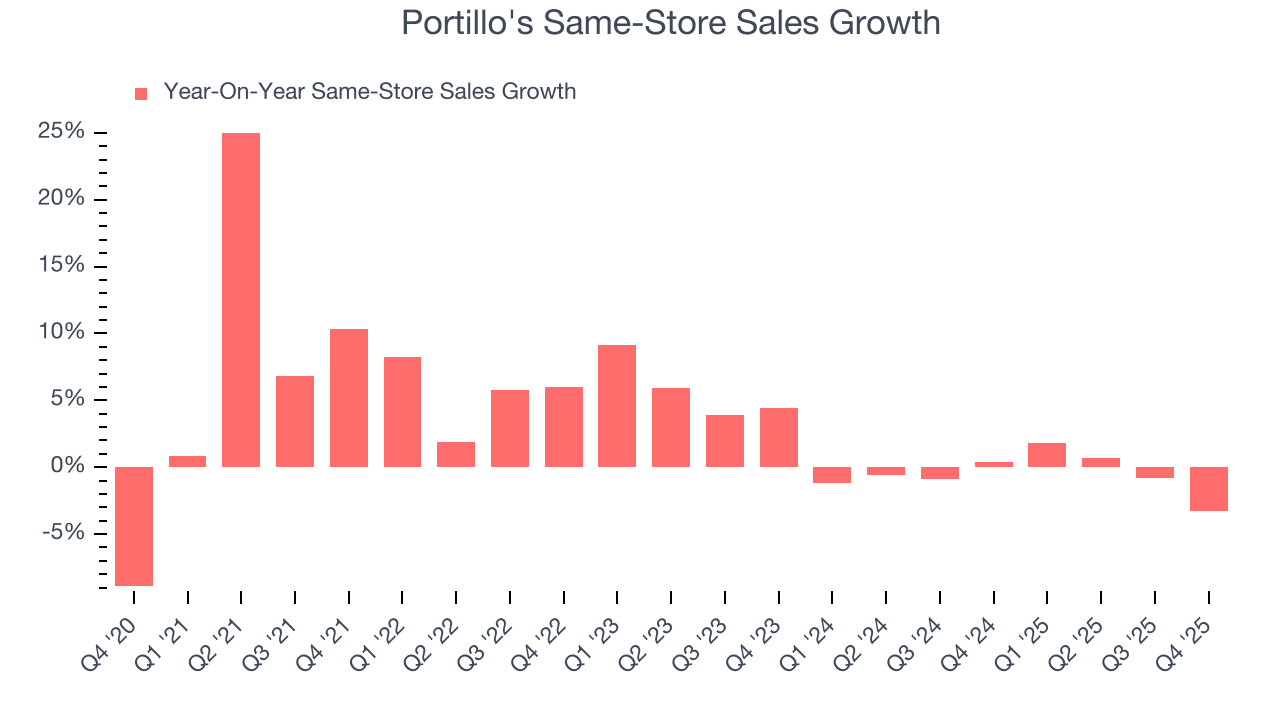

Same-Store Sales

The change in a company's restaurant base only tells one side of the story. The other is the performance of its existing locations, which informs management teams whether they should expand or downsize their physical footprints. Same-store sales provides a deeper understanding of this issue because it measures organic growth at restaurants open for at least a year.

Portillo’s demand within its existing dining locations has barely increased over the last two years as its same-store sales were flat. Portillo's should consider improving its foot traffic and efficiency before expanding its restaurant base.

In the latest quarter, Portillo’s same-store sales fell by 3.3% year on year. This decrease represents a further deceleration from its historical levels. We hope the business can get back on track.

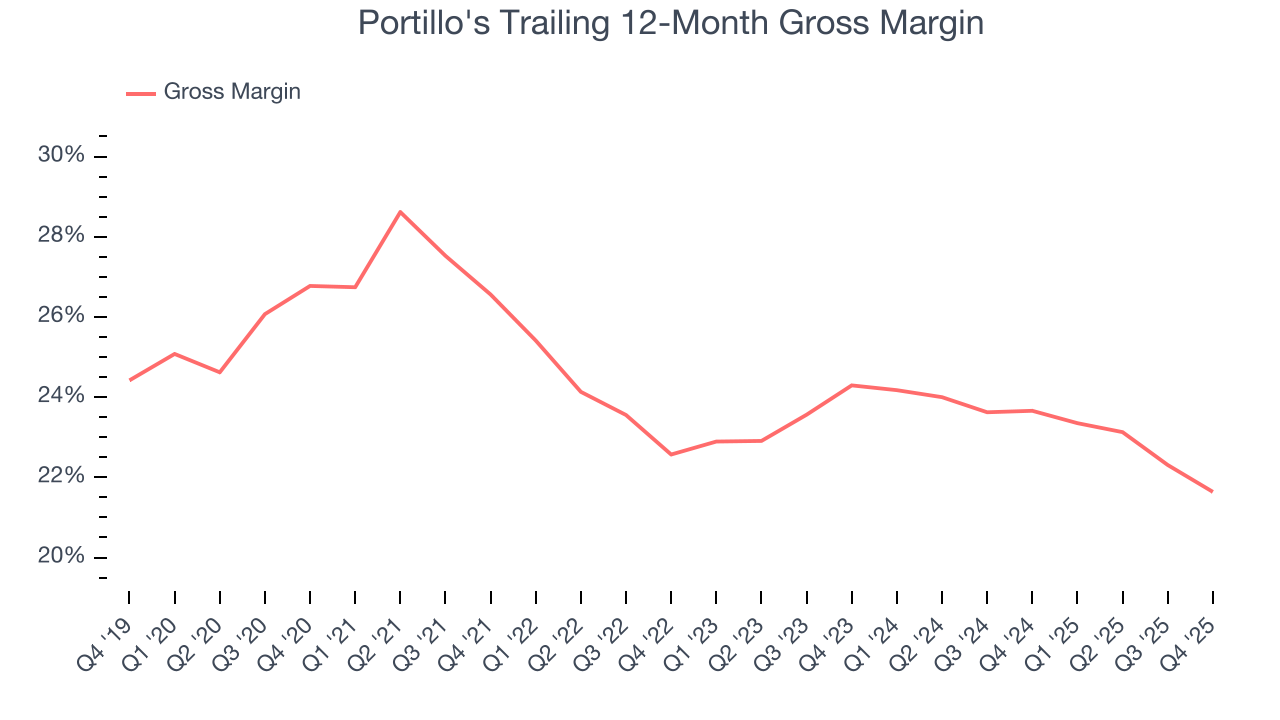

7. Gross Margin & Pricing Power

We prefer higher gross margins because they not only make it easier to generate more operating profits but also indicate pricing power and differentiation, whether it be the dining experience or quality and taste of food.

Portillo's has bad unit economics for a restaurant company, giving it less room to reinvest and grow its presence. As you can see below, it averaged a 22.6% gross margin over the last two years. Said differently, Portillo's had to pay a chunky $77.37 to its suppliers for every $100 in revenue.

Portillo’s gross profit margin came in at 21.8% this quarter, down 2.7 percentage points year on year. Portillo’s full-year margin has also been trending down over the past 12 months, decreasing by 2 percentage points. If this move continues, it could suggest a more competitive environment with some pressure to lower prices and higher input costs (such as ingredients and transportation expenses).

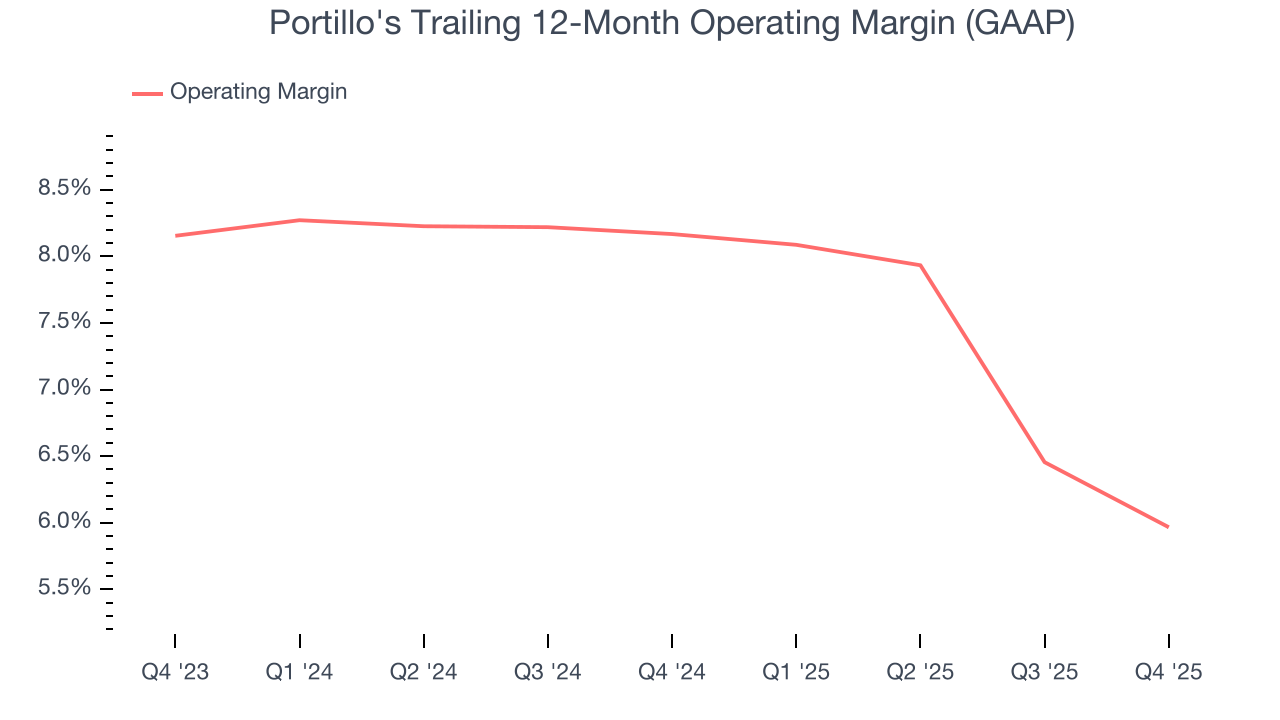

8. Operating Margin

Portillo's was profitable over the last two years but held back by its large cost base. Its average operating margin of 7.1% was weak for a restaurant business. This result isn’t too surprising given its low gross margin as a starting point.

Analyzing the trend in its profitability, Portillo’s operating margin decreased by 2.2 percentage points over the last year. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. Portillo’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers.

This quarter, Portillo's generated an operating margin profit margin of 5.6%, down 1.9 percentage points year on year. Since Portillo’s gross margin decreased more than its operating margin, we can assume its recent inefficiencies were driven more by weaker leverage on its cost of sales rather than increased marketing, and administrative overhead expenses.

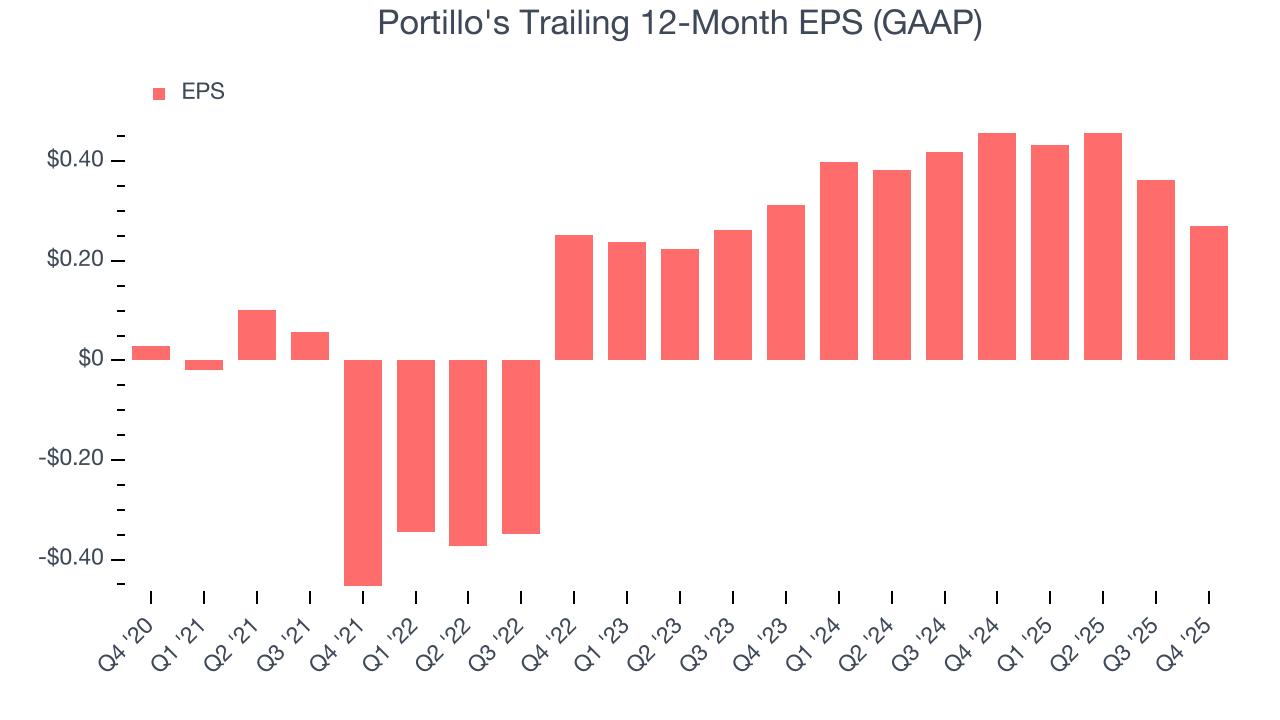

9. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Portillo’s EPS grew at a decent 16.5% compounded annual growth rate over the last six years, higher than its 7.3% annualized revenue growth. However, we take this with a grain of salt because its operating margin didn’t improve and it didn’t repurchase its shares, meaning the delta came from reduced interest expenses or taxes.

In Q4, Portillo's reported EPS of $0.08, down from $0.17 in the same quarter last year. Despite falling year on year, this print easily cleared analysts’ estimates. Over the next 12 months, Wall Street expects Portillo’s full-year EPS of $0.27 to shrink by 19.1%.

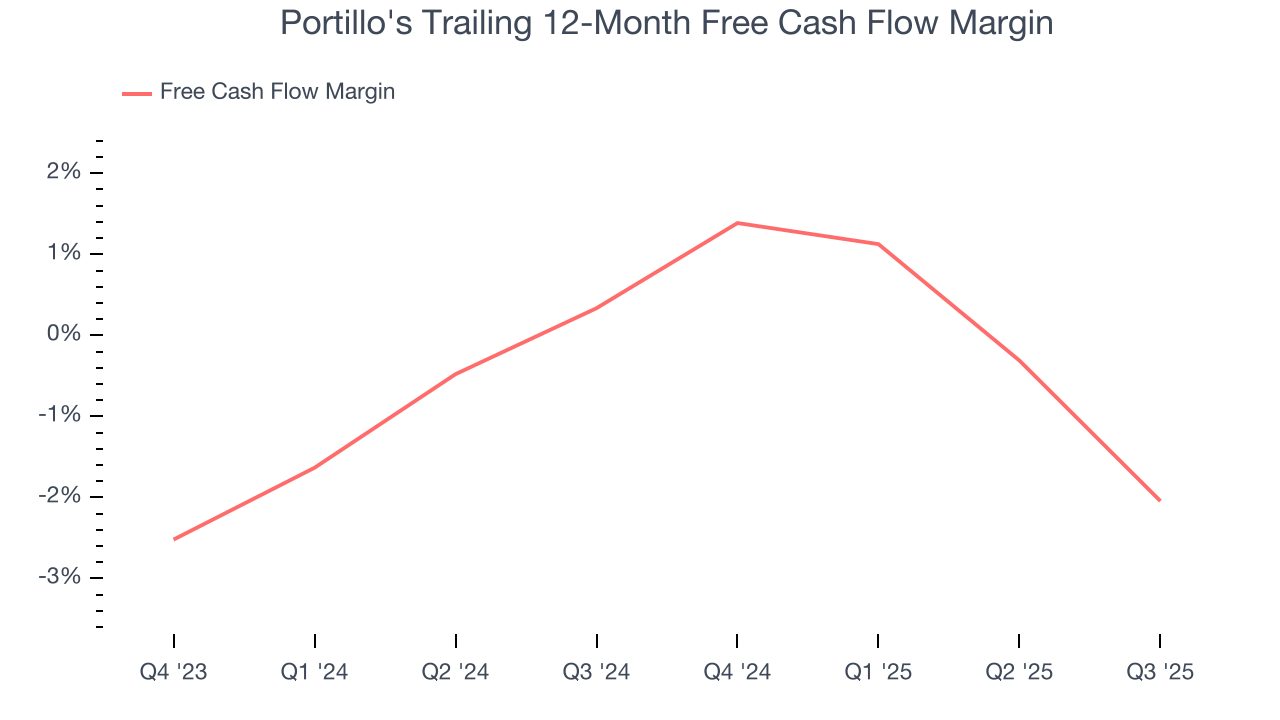

10. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Portillo's broke even from a free cash flow perspective over the last two years, giving the company limited opportunities to return capital to shareholders.

11. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Portillo's historically did a mediocre job investing in profitable growth initiatives. Its four-year average ROIC was 5.9%, somewhat low compared to the best restaurant companies that consistently pump out 15%+.

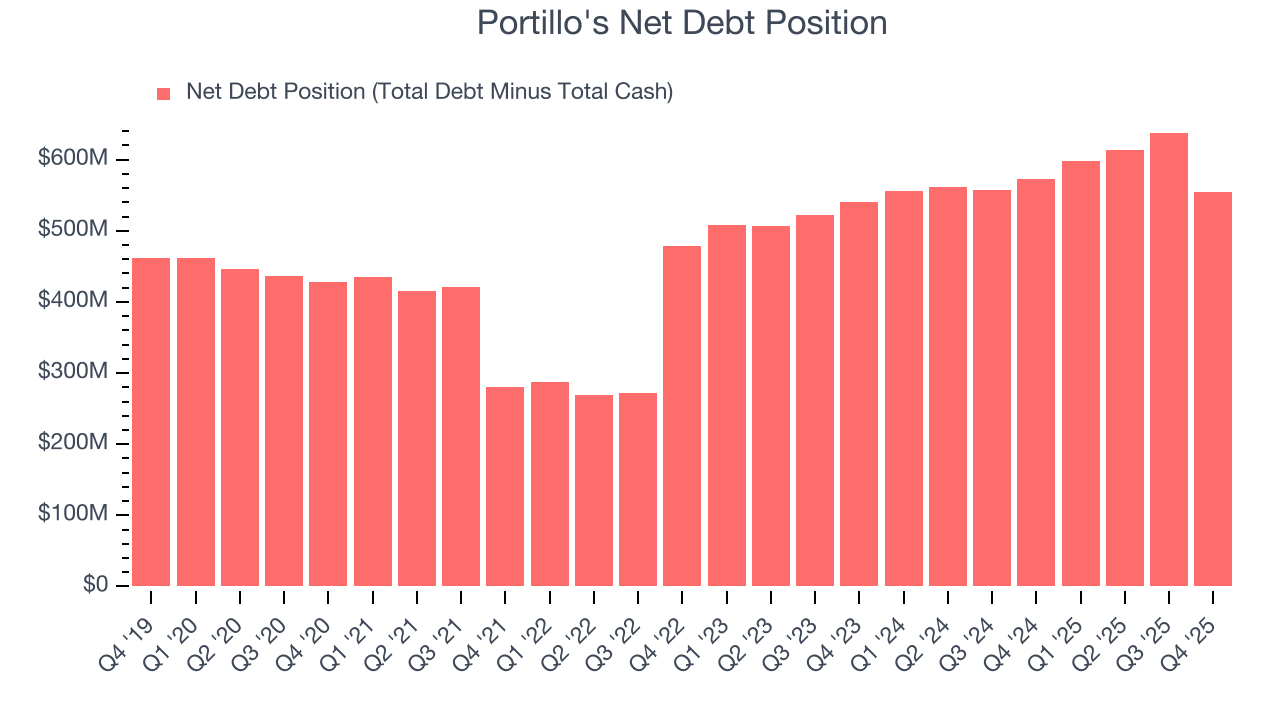

12. Balance Sheet Risk

As long-term investors, the risk we care about most is the permanent loss of capital, which can happen when a company goes bankrupt or raises money from a disadvantaged position. This is separate from short-term stock price volatility, something we are much less bothered by.

Portillo’s $574.1 million of debt exceeds the $19.96 million of cash on its balance sheet. Furthermore, its 6× net-debt-to-EBITDA ratio (based on its EBITDA of $97.33 million over the last 12 months) shows the company is overleveraged.

At this level of debt, incremental borrowing becomes increasingly expensive and credit agencies could downgrade the company’s rating if profitability falls. Portillo's could also be backed into a corner if the market turns unexpectedly – a situation we seek to avoid as investors in high-quality companies.

We hope Portillo's can improve its balance sheet and remain cautious until it increases its profitability or pays down its debt.

13. Key Takeaways from Portillo’s Q4 Results

It was good to see Portillo's beat analysts’ EPS expectations this quarter. We were also happy its same-store sales was in line with Wall Street’s estimates. Overall, we think this was still a solid quarter with some key areas of upside. The stock remained flat at $5.83 immediately after reporting.

14. Is Now The Time To Buy Portillo's?

Updated: March 17, 2026 at 10:35 PM EDT

When considering an investment in Portillo's, investors should account for its valuation and business qualities as well as what’s happened in the latest quarter.

We see the value of companies helping consumers, but in the case of Portillo's, we’re out. Although its revenue growth was decent over the last six years and Wall Street believes it will continue to grow, its projected EPS for the next year is lacking. And while the company’s new restaurant openings have increased its brand equity, the downside is its cash burn raises the question of whether it can sustainably maintain growth.

Portillo’s P/E ratio based on the next 12 months is 30.7x. This valuation tells us it’s a bit of a market darling with a lot of good news priced in - we think other companies feature superior fundamentals at the moment.

Wall Street analysts have a consensus one-year price target of $7.50 on the company (compared to the current share price of $5.80).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.