Scholastic (SCHL)

We wouldn’t buy Scholastic. Its sales have underperformed and its low returns on capital show it has few growth opportunities.― StockStory Analyst Team

1. News

2. Summary

Why We Think Scholastic Will Underperform

Creator of the legendary Scholastic Book Fair, Scholastic (NASDAQ:SCHL) is an international company specializing in children's publishing, education, and media services.

- Muted 4.9% annual revenue growth over the last five years shows its demand lagged behind its consumer discretionary peers

- Poor expense management has led to an operating margin that is below the industry average

- Poor free cash flow generation means it has few chances to reinvest for growth, repurchase shares, or distribute capital

Scholastic doesn’t meet our quality standards. There are more rewarding stocks elsewhere.

Why There Are Better Opportunities Than Scholastic

Scholastic is trading at $33.40 per share, or 22.4x forward P/E. Not only does Scholastic trade at a premium to companies in the consumer discretionary space, but this multiple is also high for its top-line growth.

There are stocks out there featuring similar valuation multiples with better fundamentals. We prefer to invest in those.

3. Scholastic (SCHL) Research Report: Q4 CY2025 Update

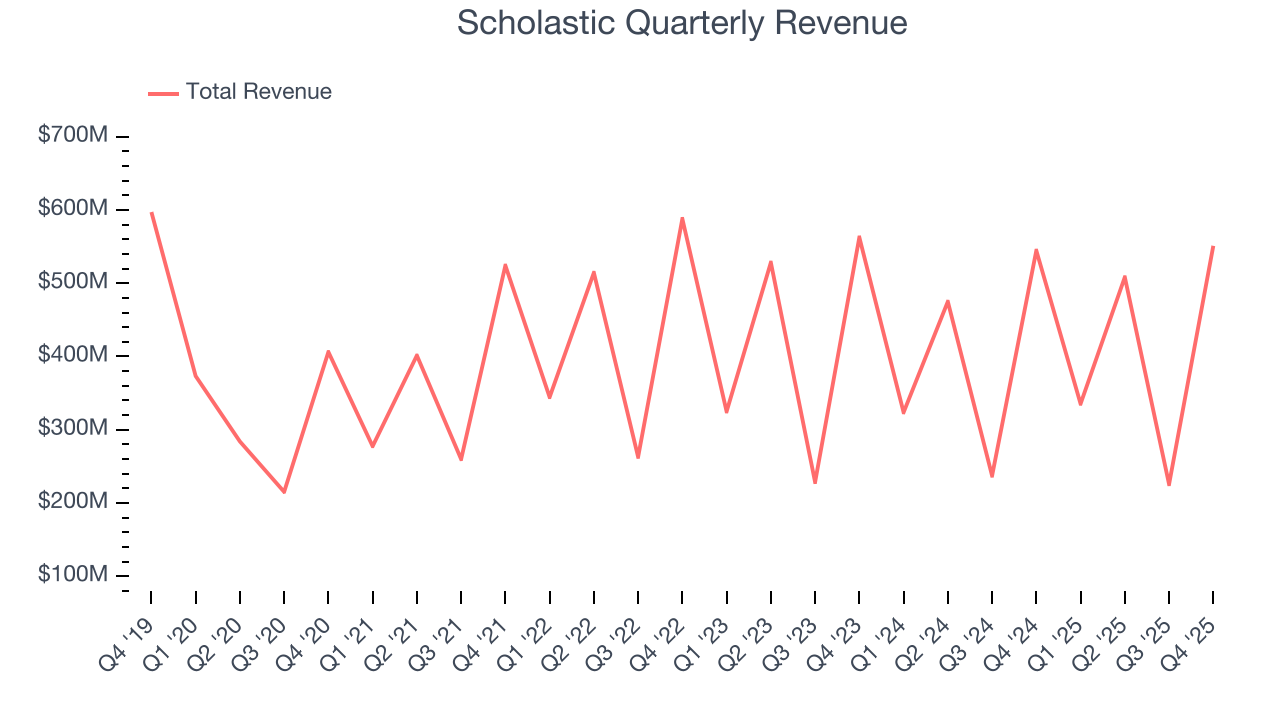

Educational publishing and media company Scholastic (NASDAQ:SCHL) missed Wall Street’s revenue expectations in Q4 CY2025 as sales only rose 1.2% year on year to $551.1 million. Its non-GAAP profit of $2.57 per share was 24.2% above analysts’ consensus estimates.

Scholastic (SCHL) Q4 CY2025 Highlights:

- Revenue: $551.1 million vs analyst estimates of $556.7 million (1.2% year-on-year growth, 1% miss)

- Adjusted EPS: $2.57 vs analyst estimates of $2.07 (24.2% beat)

- Adjusted EBITDA: $122.5 million vs analyst estimates of $109.8 million (22.2% margin, 11.6% beat)

- EBITDA guidance for the full year is $151 million at the midpoint, below analyst estimates of $159.9 million

- Operating Margin: 15%, in line with the same quarter last year

- Free Cash Flow Margin: 10.7%, up from 7.8% in the same quarter last year

- Market Capitalization: $720.2 million

Company Overview

Creator of the legendary Scholastic Book Fair, Scholastic (NASDAQ:SCHL) is an international company specializing in children's publishing, education, and media services.

Scholastic was founded in 1920 with the launch of "The Western Pennsylvania Scholastic" magazine, aimed at enriching the educational experience of students and teachers. This initial step marked the beginning of Scholastic's journey toward becoming a key player in children's education through the production of materials and content for young readers.

Today, Scholastic's offerings encompass books, magazines, educational software, and digital resources, addressing the challenge of keeping children engaged and informed. These products and services cater to both classroom and home education environments, promoting literacy and creativity.

Scholastic's revenue is derived from book sales, subscriptions to educational programs, and content distribution and licensing. Its business model combines educational value with entertainment, making Scholastic a preferred choice among educators, parents, and children.

4. Media

The advent of the internet changed how shows, films, music, and overall information flow. As a result, many media companies now face secular headwinds as attention shifts online. Some have made concerted efforts to adapt by introducing digital subscriptions, podcasts, and streaming platforms. Time will tell if their strategies succeed and which companies will emerge as the long-term winners.

Competitors in the publishing industry include John Wiley & Sons (NYSE:JW.A), Disney (NYSE:DIS), and The New York Times (NYSE:NYT).

5. Revenue Growth

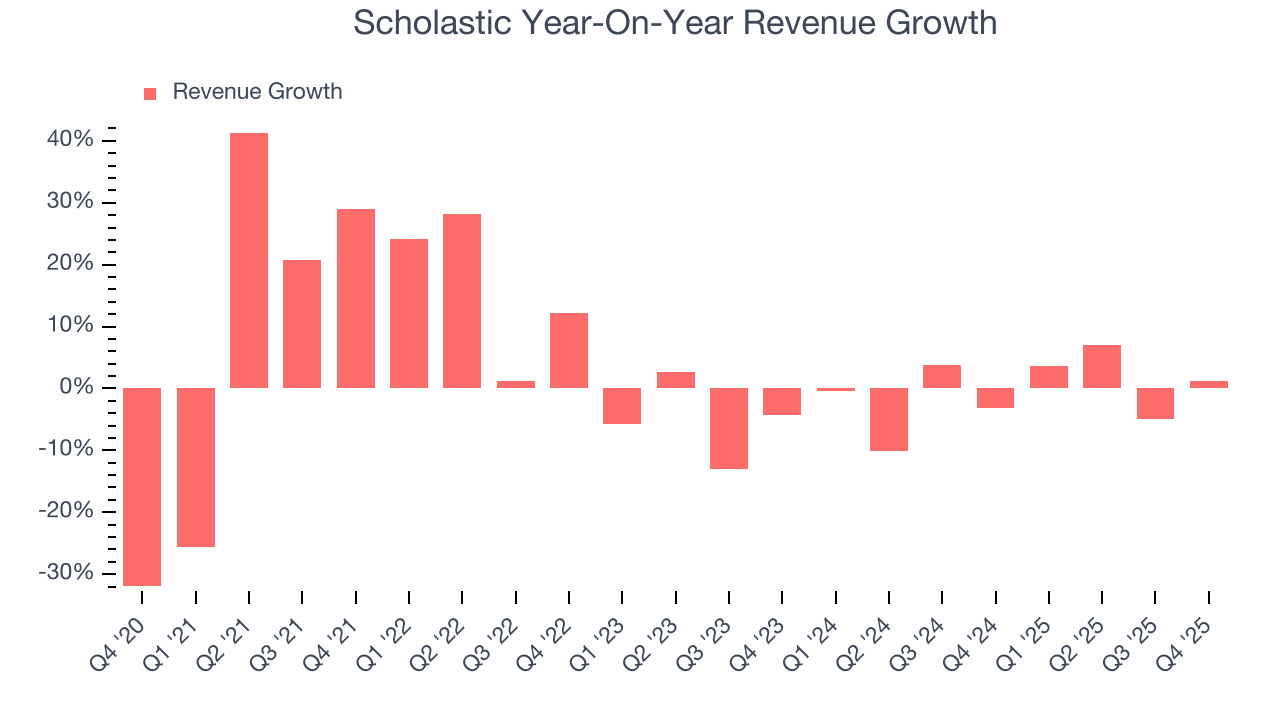

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Unfortunately, Scholastic’s 4.9% annualized revenue growth over the last five years was weak. This fell short of our benchmark for the consumer discretionary sector and is a tough starting point for our analysis.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. Scholastic’s recent performance shows its demand has slowed as its revenue was flat over the last two years.

This quarter, Scholastic’s revenue grew by 1.2% year on year to $551.1 million, falling short of Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 3.2% over the next 12 months. While this projection indicates its newer products and services will catalyze better top-line performance, it is still below average for the sector.

6. Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

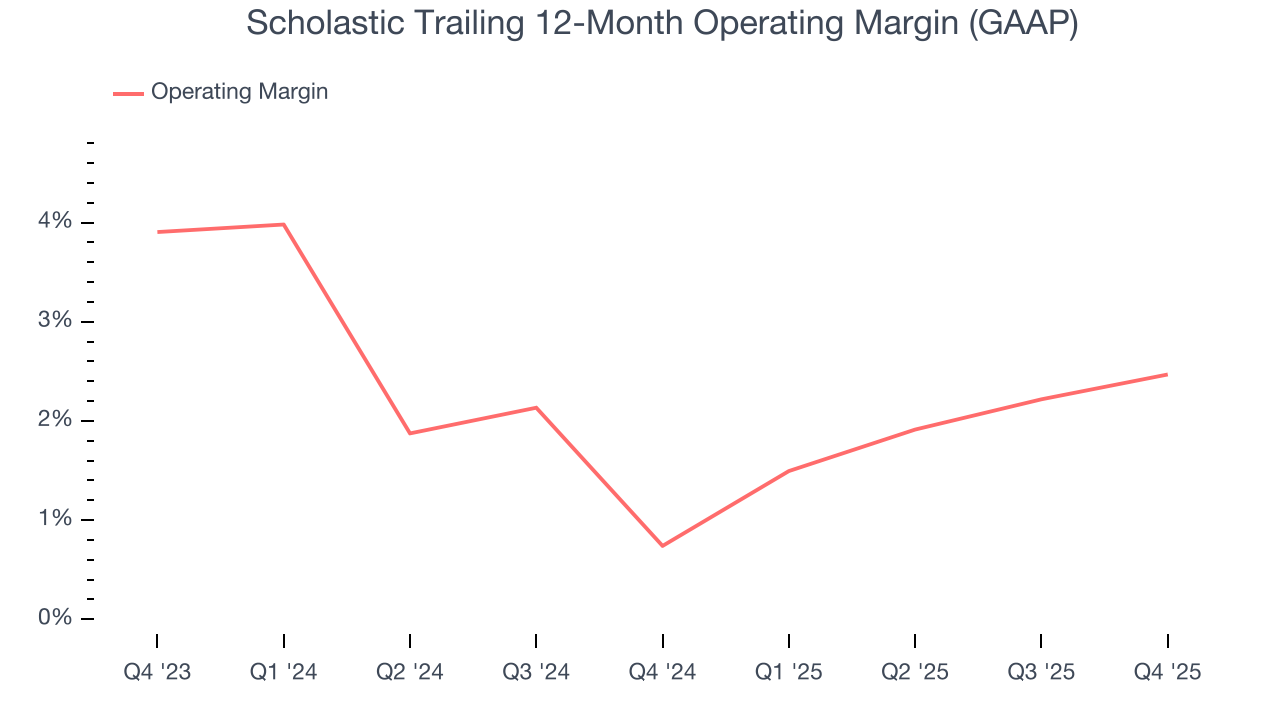

Scholastic’s operating margin has been trending up over the last 12 months and averaged 1.6% over the last two years. The company’s higher efficiency is a breath of fresh air, but its suboptimal cost structure means it still sports inadequate profitability for a consumer discretionary business.

In Q4, Scholastic generated an operating margin profit margin of 15%, in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

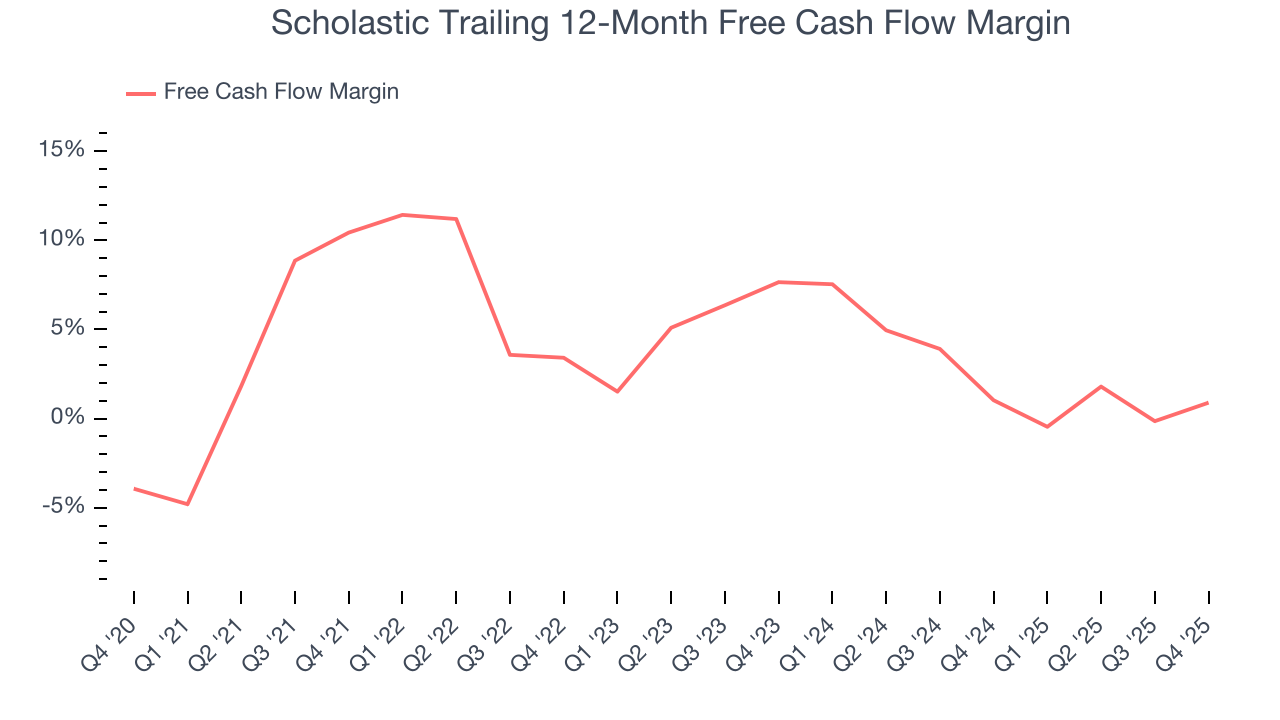

7. Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Scholastic broke even from a free cash flow perspective over the last two years, giving the company limited opportunities to return capital to shareholders.

Scholastic’s free cash flow clocked in at $59.2 million in Q4, equivalent to a 10.7% margin. This result was good as its margin was 3 percentage points higher than in the same quarter last year, but we wouldn’t read too much into the short term because investment needs can be seasonal, causing temporary swings. Long-term trends trump fluctuations.

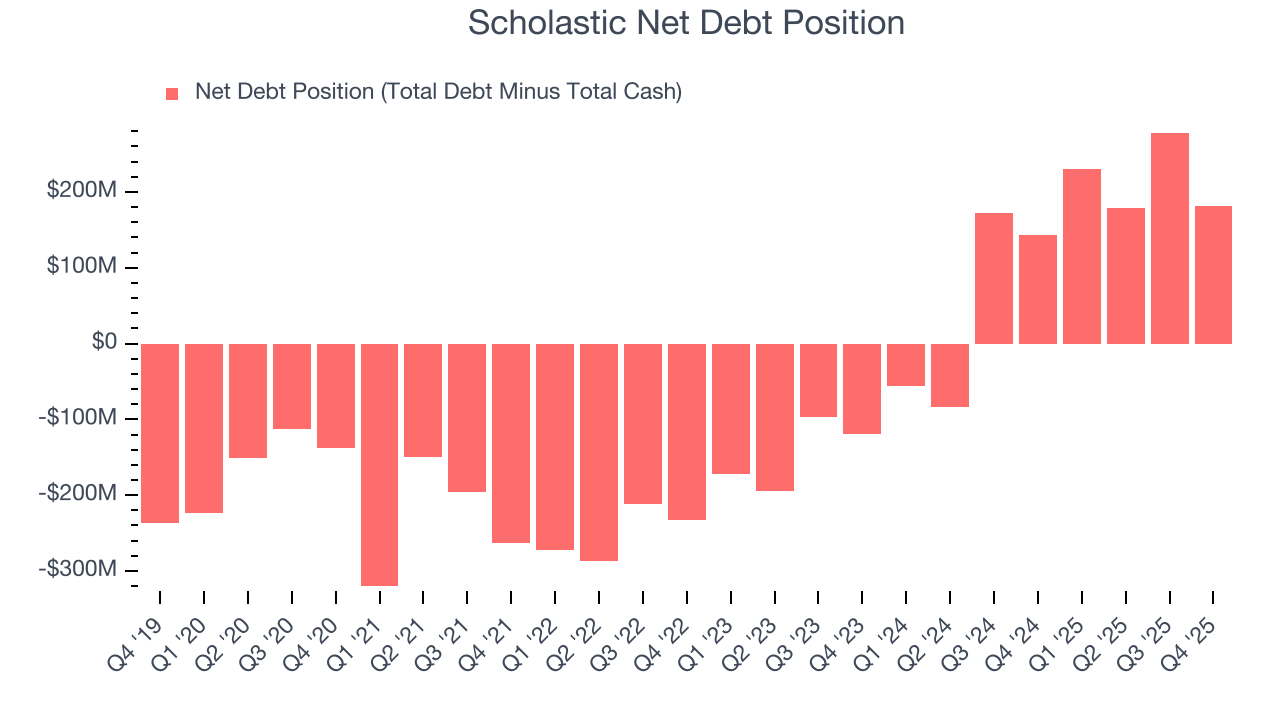

8. Balance Sheet Assessment

Scholastic reported $99.3 million of cash and $280.6 million of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $164 million of EBITDA over the last 12 months, we view Scholastic’s 1.1× net-debt-to-EBITDA ratio as safe. We also see its $18.1 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

9. Key Takeaways from Scholastic’s Q4 Results

It was good to see Scholastic beat analysts’ EPS expectations this quarter. We were also happy its EBITDA outperformed Wall Street’s estimates. On the other hand, its full-year EBITDA guidance missed and its revenue fell slightly short of Wall Street’s estimates. Zooming out, we think this was a mixed quarter. The stock remained flat at $29.15 immediately after reporting.

10. Is Now The Time To Buy Scholastic?

Updated: March 14, 2026 at 11:02 PM EDT

A common mistake we notice when investors are deciding whether to buy a stock or not is that they simply look at the latest earnings results. Business quality and valuation matter more, so we urge you to understand these dynamics as well.

We see the value of companies helping consumers, but in the case of Scholastic, we’re out. While its projected EPS for the next year implies the company will start generating shareholder value, the downside is its relatively low ROIC suggests management has struggled to find compelling investment opportunities. On top of that, its low free cash flow margins give it little breathing room.

Scholastic’s P/E ratio based on the next 12 months is 22.4x. At this valuation, there’s a lot of good news priced in - we think other companies feature superior fundamentals at the moment.

Wall Street analysts have a consensus one-year price target of $36 on the company (compared to the current share price of $33.40).