Scholastic (SCHL)

Scholastic is in for a bumpy ride. Its sales have underperformed and its low returns on capital show it has few growth opportunities.― StockStory Analyst Team

1. News

2. Summary

Why We Think Scholastic Will Underperform

Creator of the legendary Scholastic Book Fair, Scholastic (NASDAQ:SCHL) is an international company specializing in children's publishing, education, and media services.

- Lackluster 6.4% annual revenue growth over the last five years indicates the company is losing ground to competitors

- Subpar operating margin constrains its ability to invest in process improvements or effectively respond to new competitive threats

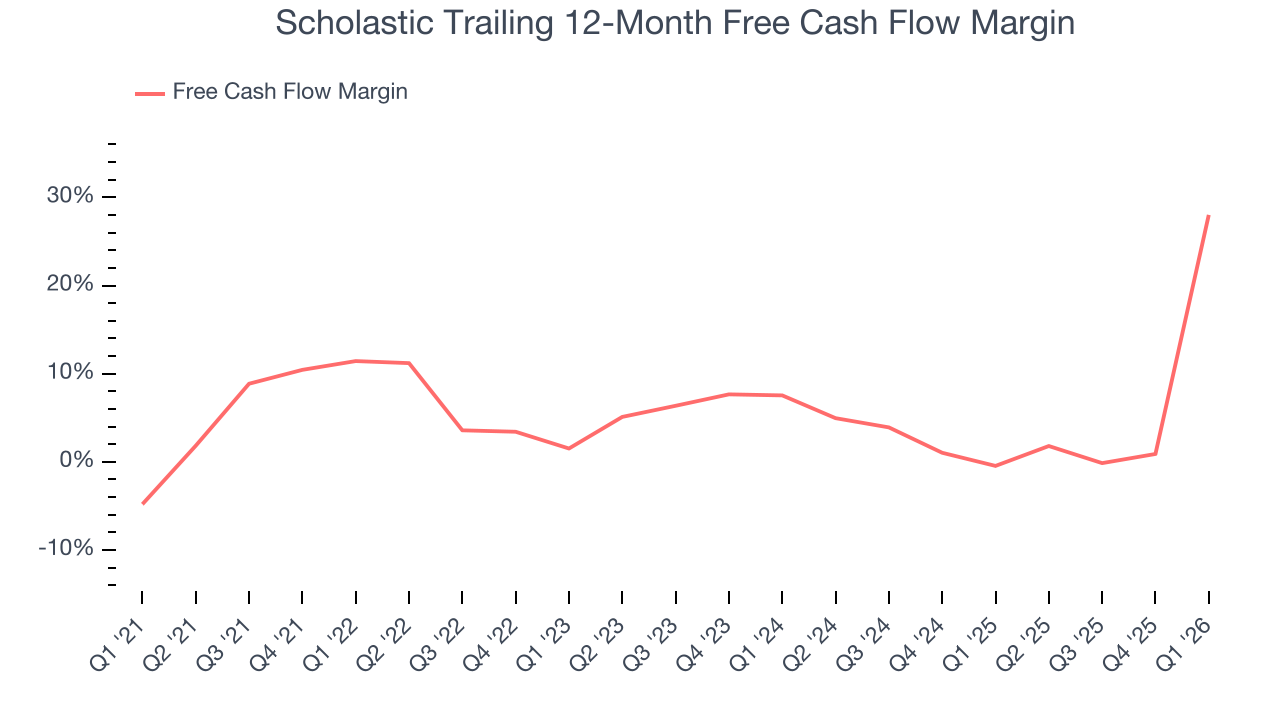

- Ability to fund investments or reward shareholders with increased buybacks or dividends is restricted by its weak free cash flow margin of 13.9% for the last two years

Scholastic’s quality isn’t great. We’re looking for better stocks elsewhere.

Why There Are Better Opportunities Than Scholastic

At $39.16 per share, Scholastic trades at 17.4x forward P/E. While valuation is appropriate for the quality you get, we’re still not buyers.

There are stocks out there featuring similar valuation multiples with better fundamentals. We prefer to invest in those.

3. Scholastic (SCHL) Research Report: Q1 CY2026 Update

Educational publishing and media company Scholastic (NASDAQ:SCHL) fell short of the market’s revenue expectations in Q1 CY2026, with sales falling 1.9% year on year to $329.1 million. Its non-GAAP loss of $0.15 per share was 58.9% above analysts’ consensus estimates.

Scholastic (SCHL) Q1 CY2026 Highlights:

- Revenue: $329.1 million vs analyst estimates of $331 million (1.9% year-on-year decline, 0.6% miss)

- Adjusted EPS: -$0.15 vs analyst estimates of -$0.37 (58.9% beat)

- Adjusted EBITDA: $0 vs analyst estimates of $3.57 million (0% margin, significant miss)

- EBITDA guidance for the full year is $151 million at the midpoint, in line with analyst expectations

- Operating Margin: -8.2%, down from -6.7% in the same quarter last year

- Free Cash Flow was $407 million, up from -$30.7 million in the same quarter last year

- Market Capitalization: $849.5 million

Company Overview

Creator of the legendary Scholastic Book Fair, Scholastic (NASDAQ:SCHL) is an international company specializing in children's publishing, education, and media services.

Scholastic was founded in 1920 with the launch of "The Western Pennsylvania Scholastic" magazine, aimed at enriching the educational experience of students and teachers. This initial step marked the beginning of Scholastic's journey toward becoming a key player in children's education through the production of materials and content for young readers.

Today, Scholastic's offerings encompass books, magazines, educational software, and digital resources, addressing the challenge of keeping children engaged and informed. These products and services cater to both classroom and home education environments, promoting literacy and creativity.

Scholastic's revenue is derived from book sales, subscriptions to educational programs, and content distribution and licensing. Its business model combines educational value with entertainment, making Scholastic a preferred choice among educators, parents, and children.

4. Consumer Discretionary - Media

The Consumer Discretionary sector, by definition, is made up of companies selling non-essential goods and services. When economic conditions deteriorate or tastes shift, consumers can easily cut back or eliminate these purchases. For long-term investors with five-year holding periods, this creates a structural challenge: the sector is inherently hit-driven, with low switching costs and fickle customers. As a result, only a handful of companies can reliably grow demand and compound earnings over long periods, which is why our bar is high and High Quality ratings are rare.

Media companies create, aggregate, and distribute content—including news, entertainment, and advertising—across television, print, digital, and out-of-home channels. Tailwinds include growing digital advertising budgets, content licensing opportunities, and global audience expansion through streaming and social platforms. Headwinds are substantial: traditional advertising revenue from print and linear TV continues its structural decline as audiences migrate to digital alternatives. Content creation costs are escalating amid intense competition for talent and intellectual property. Media fragmentation makes it difficult to build sustainable audience scale, while AI-generated content threatens to commoditize production and disrupt established business models.

Competitors in the publishing industry include John Wiley & Sons (NYSE:JW.A), Disney (NYSE:DIS), and The New York Times (NYSE:NYT).

5. Revenue Growth

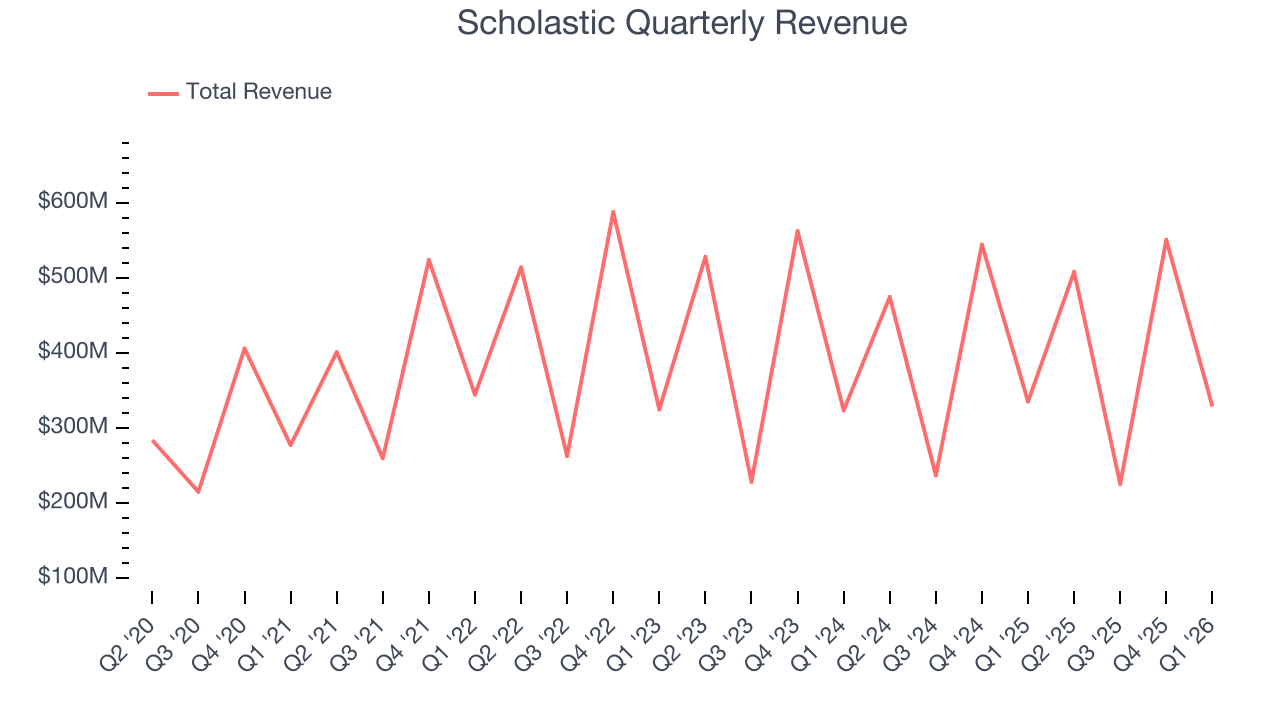

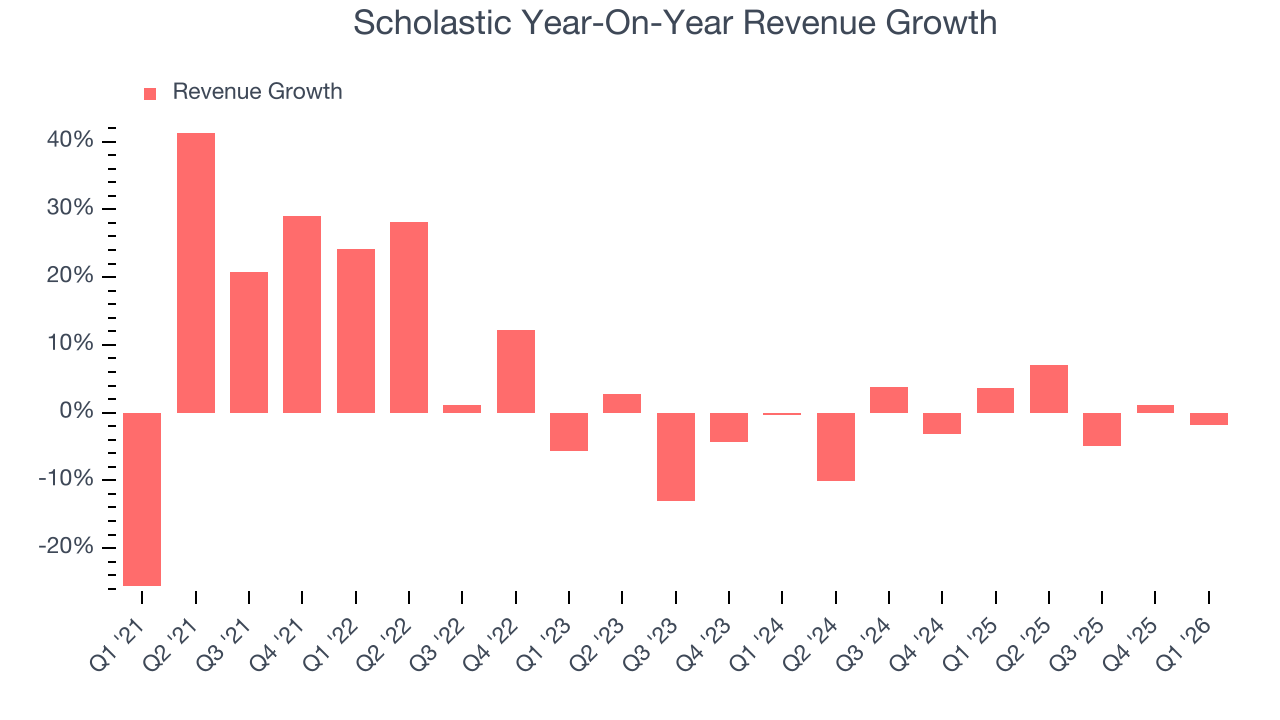

Examining a company’s long-term performance can provide clues about its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Regrettably, Scholastic’s sales grew at a weak 6.4% compounded annual growth rate over the last five years. This was below our standard for the consumer discretionary sector and is a rough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new product or trend. Scholastic’s recent performance shows its demand has slowed as its revenue was flat over the last two years.

This quarter, Scholastic missed Wall Street’s estimates and reported a rather uninspiring 1.9% year-on-year revenue decline, generating $329.1 million of revenue.

Looking ahead, sell-side analysts expect revenue to grow 2.5% over the next 12 months. While this projection implies its newer products and services will catalyze better top-line performance, it is still below average for the sector.

6. Operating Margin

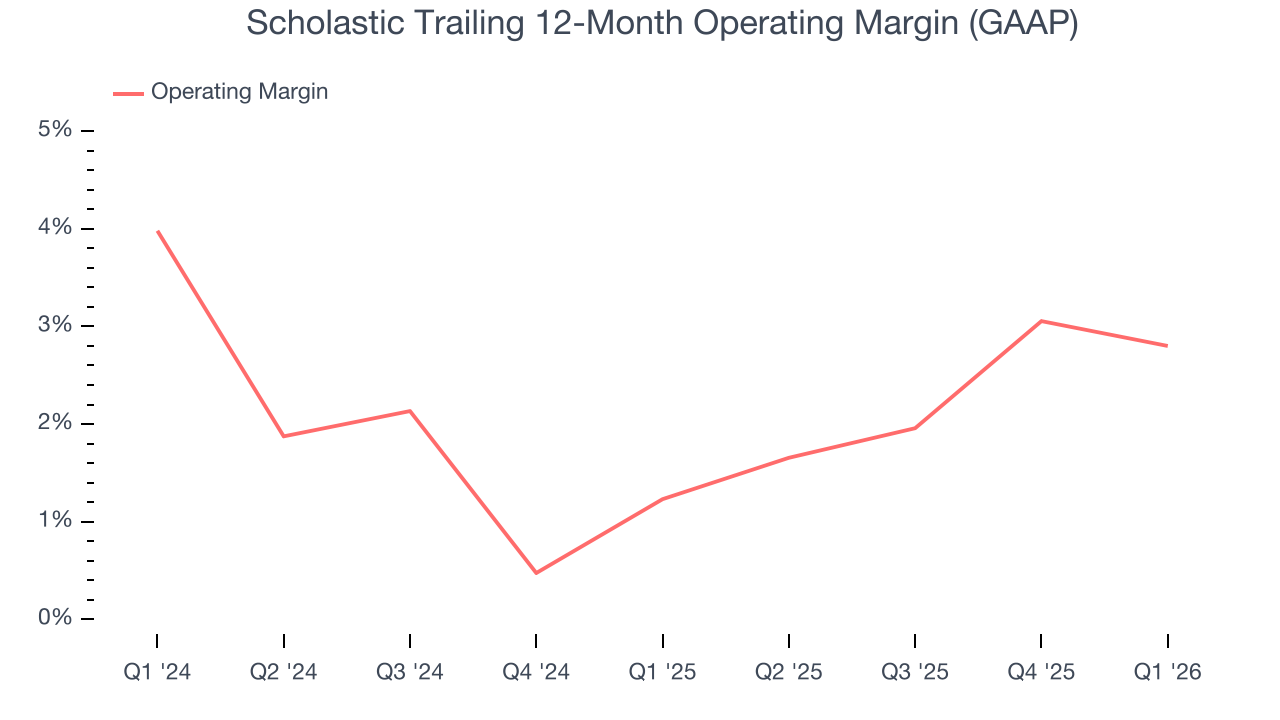

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Scholastic’s operating margin has been trending up over the last 12 months and averaged 2% over the last two years. The company’s higher efficiency is a breath of fresh air, but its suboptimal cost structure means it still sports inadequate profitability for a consumer discretionary business.

In Q1, Scholastic generated an operating margin profit margin of negative 8.2%, down 1.4 percentage points year on year. This reduction is quite minuscule and indicates the company’s overall cost structure has been relatively stable.

7. Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

Scholastic has shown poor cash profitability relative to peers over the last two years, giving the company fewer opportunities to return capital to shareholders. Its free cash flow margin averaged 13.9%, below what we’d expect for a consumer discretionary business.

Scholastic’s free cash flow clocked in at $407 million in Q1, equivalent to a 124% margin. Its cash flow turned positive after being negative in the same quarter last year, but we wouldn’t read too much into the short term because investment needs can be seasonal, leading to temporary swings. Long-term trends carry greater meaning.

8. Balance Sheet Assessment

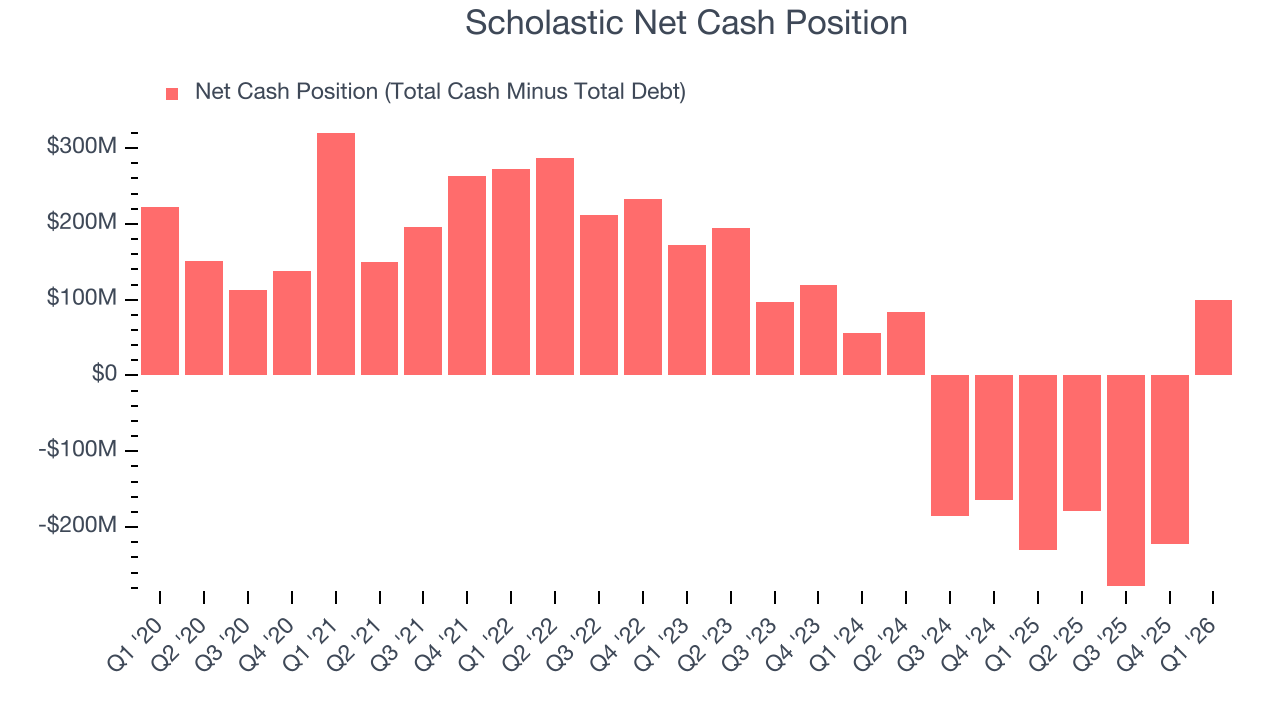

Companies with more cash than debt have lower bankruptcy risk.

Scholastic is a profitable, well-capitalized company with $104.6 million of cash and $5.6 million of debt on its balance sheet. This $99 million net cash position is 11.7% of its market cap and gives it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

9. Key Takeaways from Scholastic’s Q1 Results

It was good to see Scholastic beat analysts’ EPS expectations this quarter. On the other hand, its EBITDA missed and its revenue fell slightly short of Wall Street’s estimates. Overall, this was a softer quarter. The stock traded up 7.6% to $36.87 immediately after reporting.

10. Is Now The Time To Buy Scholastic?

Updated: March 24, 2026 at 10:09 PM EDT

Are you wondering whether to buy Scholastic or pass? We urge investors to not only consider the latest earnings results but also longer-term business quality and valuation as well.

We see the value of companies helping consumers, but in the case of Scholastic, we’re out. While its projected EPS for the next year implies the company will start generating shareholder value, the downside is its relatively low ROIC suggests management has struggled to find compelling investment opportunities. On top of that, its low free cash flow margins give it little breathing room.

Scholastic’s P/E ratio based on the next 12 months is 17.4x. While this valuation is reasonable, we don’t see a big opportunity at the moment. There are better investments elsewhere.

Wall Street analysts have a consensus one-year price target of $41 on the company (compared to the current share price of $39.16).