Sotera Health Company (SHC)

We’re wary of Sotera Health Company. Its underwhelming revenue growth and failure to generate meaningful free cash flow is a concerning trend.― StockStory Analyst Team

1. News

2. Summary

Why We Think Sotera Health Company Will Underperform

With a critical role in ensuring the safety of millions of patients worldwide, Sotera Health (NASDAQGS:SHC) provides sterilization services, lab testing, and advisory services to ensure medical devices, pharmaceuticals, and food products are safe for use.

- Subscale operations are evident in its revenue base of $1.16 billion, meaning it has fewer distribution channels than its larger rivals

- Earnings per share were flat over the last four years and fell short of the peer group average

- A silver lining is that its successful business model is illustrated by its impressive adjusted operating margin

Sotera Health Company’s quality is inadequate. There are more appealing investments to be made.

Why There Are Better Opportunities Than Sotera Health Company

Sotera Health Company’s stock price of $13.88 implies a valuation ratio of 14x forward P/E. Sotera Health Company’s valuation may seem like a bargain, especially when stacked up against other healthcare companies. We remind you that you often get what you pay for, though.

We’d rather pay up for companies with elite fundamentals than get a bargain on weak ones. Cheap stocks can be value traps, and as their performance deteriorates, they will stay cheap or get even cheaper.

3. Sotera Health Company (SHC) Research Report: Q4 CY2025 Update

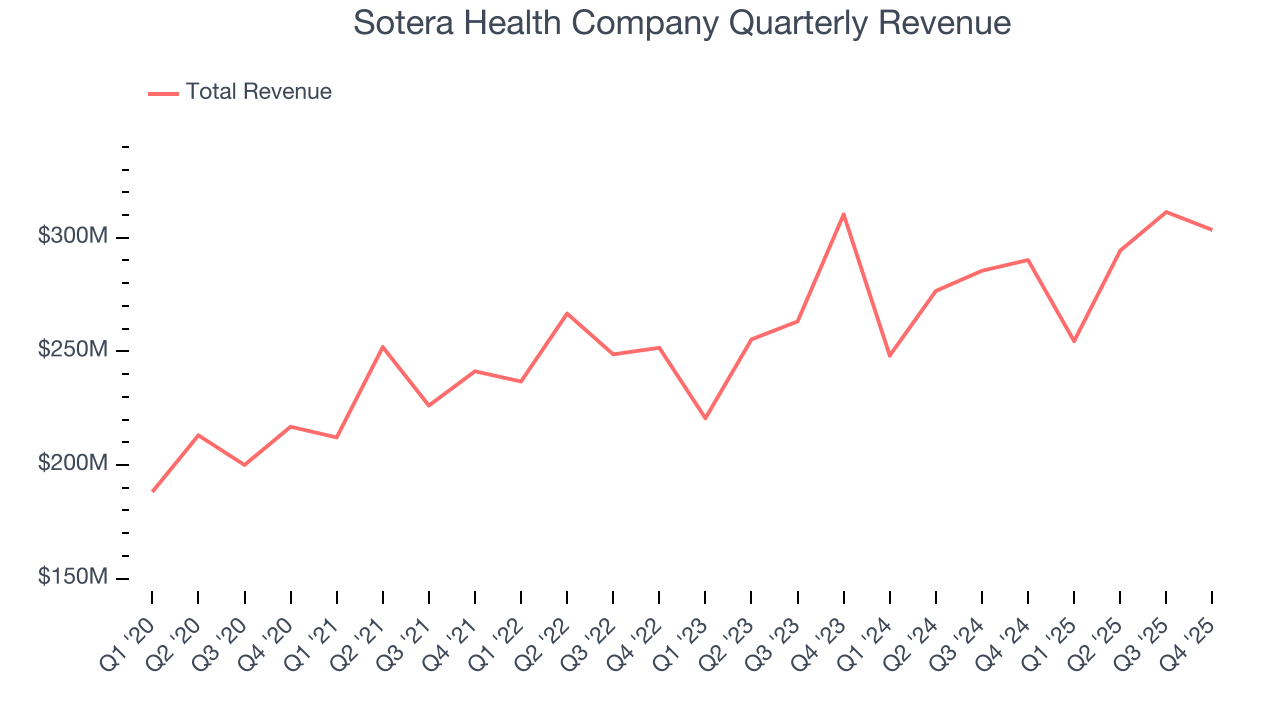

Healthcare services company Sotera Health (NASDAQ:) reported Q4 CY2025 results exceeding the market’s revenue expectations, with sales up 4.6% year on year to $303.4 million. The company’s full-year revenue guidance of $1.24 billion at the midpoint came in 1.1% above analysts’ estimates. Its non-GAAP profit of $0.26 per share was 7% above analysts’ consensus estimates.

Sotera Health Company (SHC) Q4 CY2025 Highlights:

- Revenue: $303.4 million vs analyst estimates of $299.9 million (4.6% year-on-year growth, 1.2% beat)

- Adjusted EPS: $0.26 vs analyst estimates of $0.24 (7% beat)

- Adjusted EBITDA: $157 million vs analyst estimates of $154.4 million (51.8% margin, 1.7% beat)

- Adjusted EPS guidance for the upcoming financial year 2026 is $0.97 at the midpoint, beating analyst estimates by 3.3%

- Operating Margin: 23.2%, down from 30% in the same quarter last year

- Free Cash Flow was $52.41 million, up from -$10.15 million in the same quarter last year

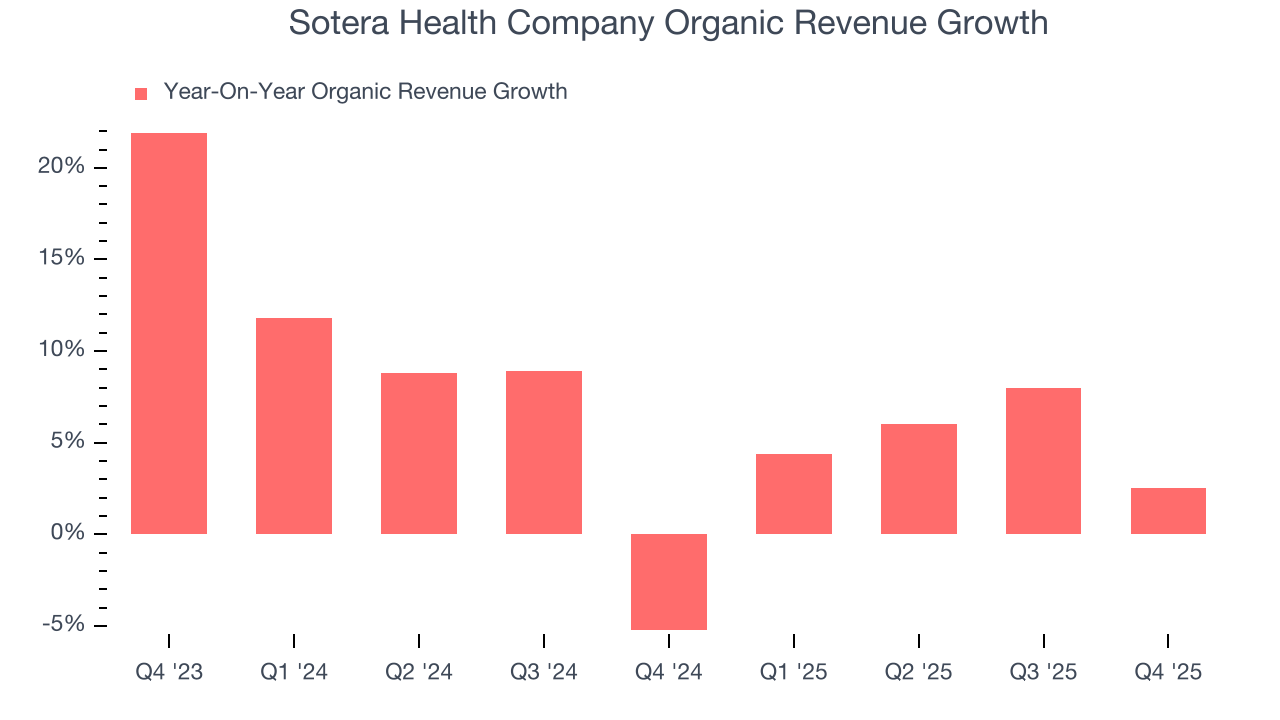

- Organic Revenue rose 2.5% year on year (miss)

- Market Capitalization: $4.97 billion

Company Overview

With a critical role in ensuring the safety of millions of patients worldwide, Sotera Health (NASDAQGS:SHC) provides sterilization services, lab testing, and advisory services to ensure medical devices, pharmaceuticals, and food products are safe for use.

Sotera Health operates through three main business segments: Sterigenics, Nordion, and Nelson Labs. Each plays a distinct role in the healthcare product safety ecosystem.

Sterigenics, with 48 facilities across 13 countries, provides terminal sterilization services using three primary technologies: gamma irradiation, ethylene oxide (EO) processing, and electron beam (E-beam) irradiation. Terminal sterilization is the critical final step in manufacturing medical products before they reach healthcare providers and patients. The company sterilizes items like surgical kits, implants, syringes, catheters, wound care products, and personal protective equipment.

Nordion is the leading global provider of Cobalt-60 (Co-60), a radioactive isotope essential for gamma sterilization processes. Co-60 naturally decays at approximately 12% annually, creating recurring demand as customers must regularly purchase new supply. Nordion sources Co-60 through long-term contracts with nuclear reactor operators in several countries and designs, installs, and maintains gamma irradiation systems that house the Co-60 sources.

Nelson Labs provides over 900 different microbiological and analytical chemistry tests for medical device and pharmaceutical manufacturers. These services span the entire product lifecycle, from development and validation testing to ongoing quality control. The company employs approximately 600 scientists, technicians, and specialists who help customers navigate complex regulatory requirements.

Sotera Health's services represent a small fraction of customers' end-product costs but are essential for regulatory compliance and patient safety. This dynamic has helped the company build long-term relationships with approximately 5,000 customers in over 50 countries, including 40 of the top 50 medical device companies and nine of the top ten global pharmaceutical companies.

The company's business model benefits from high switching costs, as customers must often re-register with regulatory authorities like the FDA if they change sterilization facilities. This contributes to Sotera Health's high customer retention rates, with 100% renewal among its top ten Sterigenics customers for more than five consecutive years.

4. Research Tools & Consumables

The life sciences subsector specializing in research tools and consumables enables scientific discoveries across academia, biotechnology, and pharmaceuticals. These firms supply a wide range of essential laboratory products, ensuring a recurring revenue stream through repeat purchases and replenishment. Their business models benefit from strong customer loyalty, a diversified product portfolio, and exposure to both the research and clinical markets. However, challenges include high R&D investment to maintain technological leadership, pricing pressures from budget-conscious institutions, and vulnerability to fluctuations in research funding cycles. Looking ahead, this subsector stands to benefit from tailwinds such as growing demand for tools supporting emerging fields like synthetic biology and personalized medicine. There is also a rise in automation and AI-driven solutions in laboratories that could create new opportunities to sell tools and consumables. Nevertheless, headwinds exist. These companies tend to be at the mercy of supply chain disruptions and sensitivity to macroeconomic conditions that impact funding for research initiatives.

Sotera Health's main competitor in the sterilization services market is STERIS plc's Applied Sterilization Technologies segment. In the laboratory testing space, Nelson Labs competes with various testing laboratories including Eurofins Scientific, WuXi AppTec, and SGS. For Nordion's Co-60 supply business, competitors include other nuclear reactor operators and isotope suppliers.

5. Revenue Scale

Larger companies benefit from economies of scale, where fixed costs like infrastructure, technology, and administration are spread over a higher volume of goods or services, reducing the cost per unit. Scale can also lead to bargaining power with suppliers, greater brand recognition, and more investment firepower. A virtuous cycle can ensue if a scaled company plays its cards right.

With just $1.16 billion in revenue over the past 12 months, Sotera Health Company is a small company in an industry where scale matters. This makes it difficult to build trust with customers because healthcare is heavily regulated, complex, and resource-intensive.

6. Revenue Growth

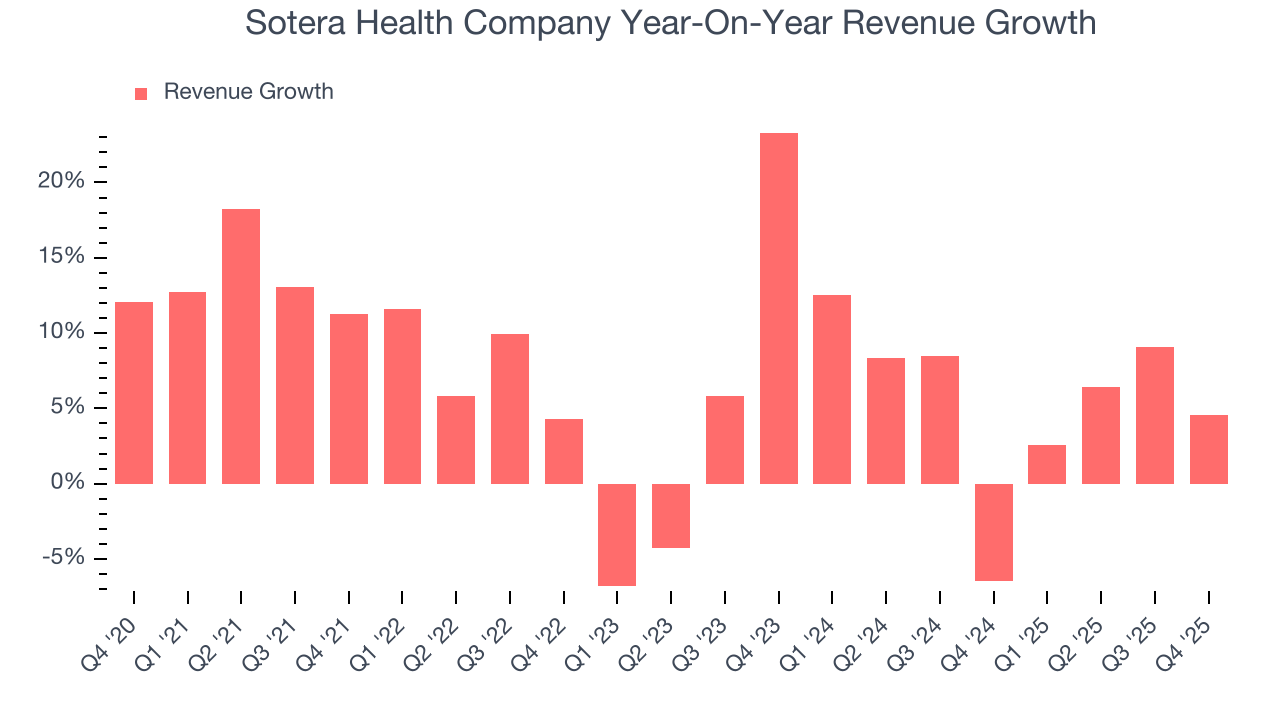

A company’s long-term sales performance is one signal of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Over the last five years, Sotera Health Company grew its sales at a mediocre 7.3% compounded annual growth rate. This was below our standard for the healthcare sector and is a rough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within healthcare, a half-decade historical view may miss recent innovations or disruptive industry trends. Sotera Health Company’s recent performance shows its demand has slowed as its annualized revenue growth of 5.3% over the last two years was below its five-year trend. We’re wary when companies in the sector see decelerations in revenue growth, as it could signal changing consumer tastes aided by low switching costs.

We can dig further into the company’s sales dynamics by analyzing its organic revenue, which strips out one-time events like acquisitions and currency fluctuations that don’t accurately reflect its fundamentals. Over the last two years, Sotera Health Company’s organic revenue averaged 5.7% year-on-year growth. Because this number aligns with its two-year revenue growth, we can see the company’s core operations (not acquisitions and divestitures) drove most of its results.

This quarter, Sotera Health Company reported modest year-on-year revenue growth of 4.6% but beat Wall Street’s estimates by 1.2%.

Looking ahead, sell-side analysts expect revenue to grow 5.4% over the next 12 months, similar to its two-year rate. This projection is above average for the sector and indicates its newer products and services will help sustain its recent top-line performance.

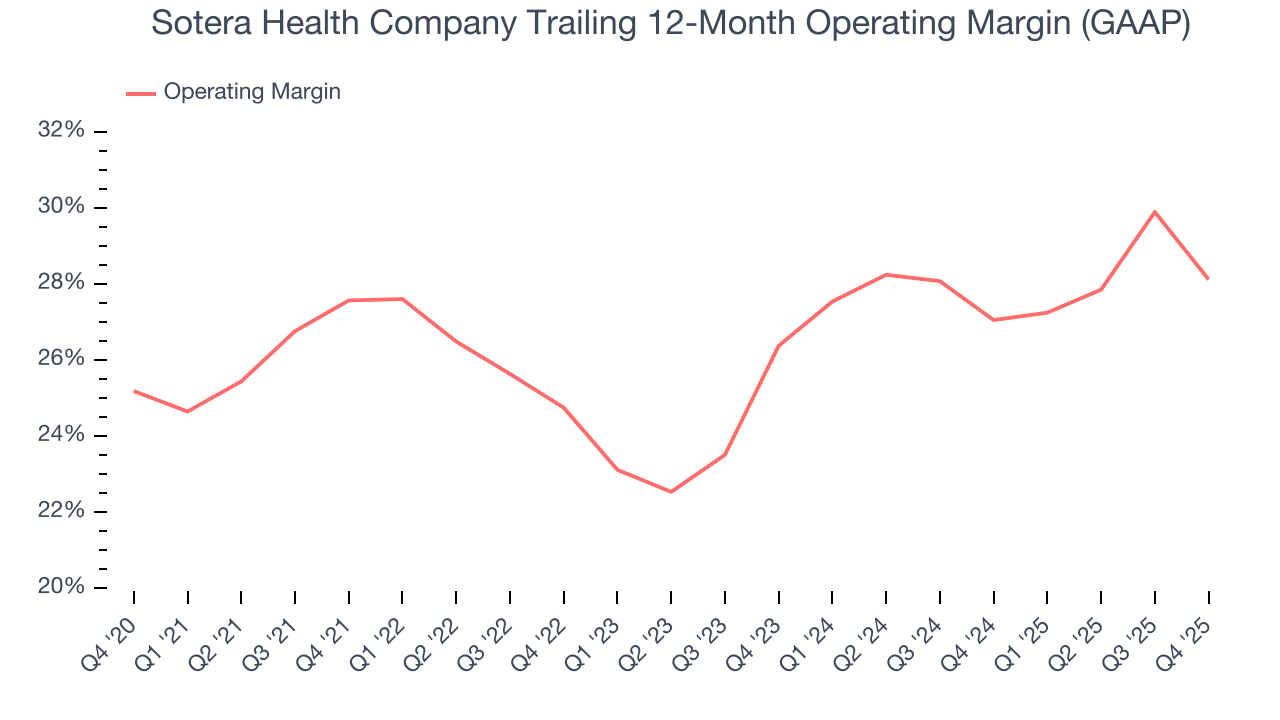

7. Operating Margin

Sotera Health Company’s operating margin has risen over the last 12 months and averaged 26.8% over the last five years. On top of that, its profitability was top-notch for a healthcare business, showing it’s an well-run company with an efficient cost structure.

Looking at the trend in its profitability, Sotera Health Company’s operating margin of 28.1% for the trailing 12 months may be around the same as five years ago, but it has increased by 1.7 percentage points over the last two years.

In Q4, Sotera Health Company generated an operating margin profit margin of 23.2%, down 6.8 percentage points year on year. This contraction shows it was less efficient because its expenses grew faster than its revenue.

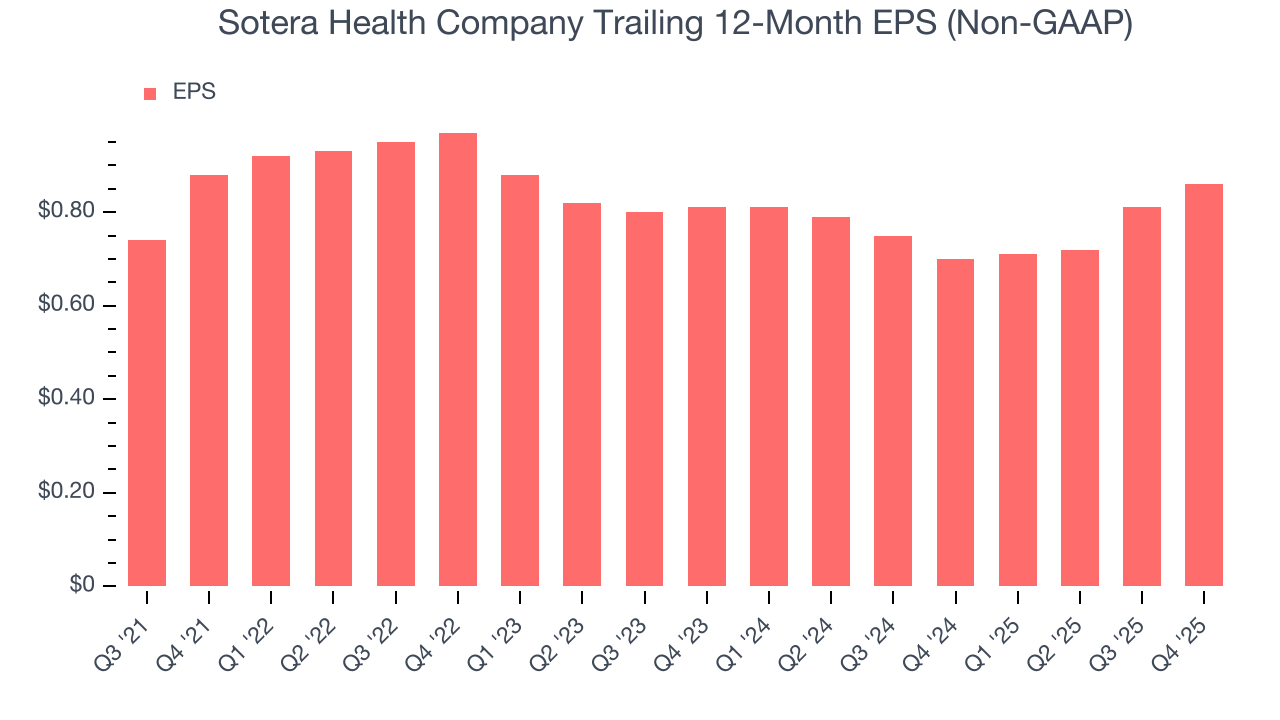

8. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Sotera Health Company’s full-year EPS was flat over the last four years, worse than the broader healthcare sector.

In Q4, Sotera Health Company reported adjusted EPS of $0.26, up from $0.21 in the same quarter last year. This print beat analysts’ estimates by 7%. Over the next 12 months, Wall Street expects Sotera Health Company’s full-year EPS of $0.86 to grow 9.4%.

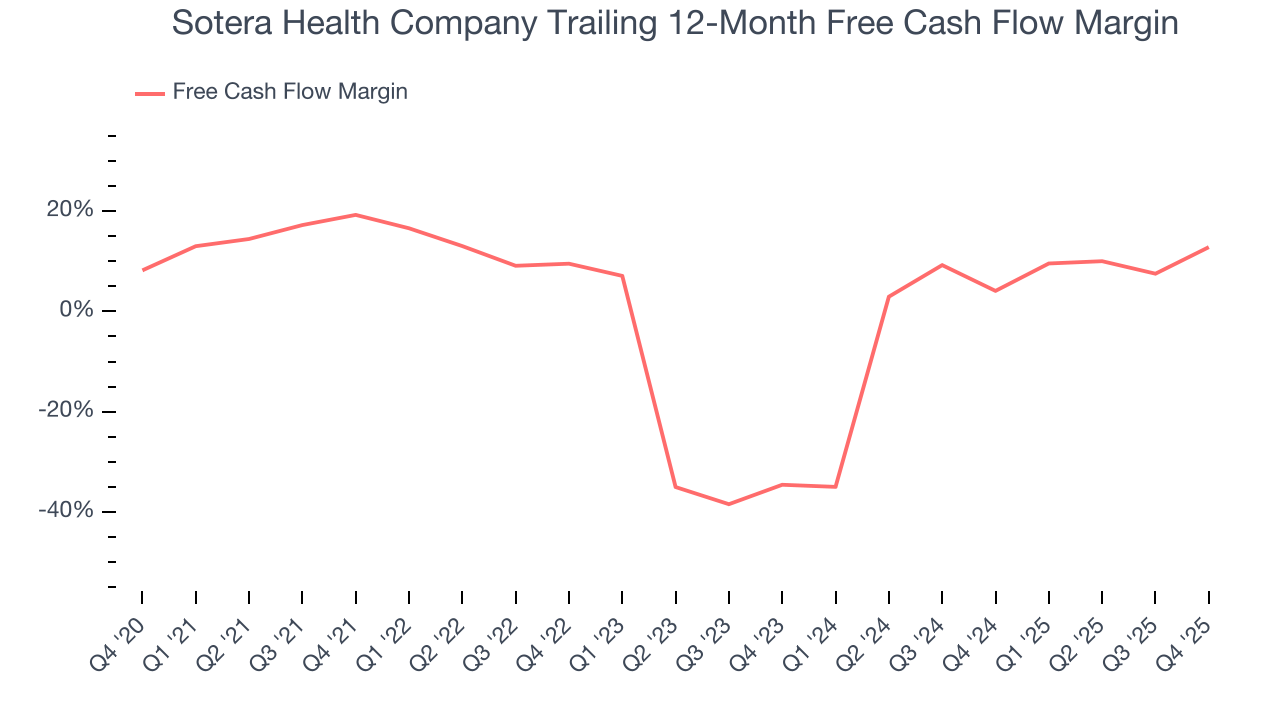

9. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Sotera Health Company has shown mediocre cash profitability over the last five years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 2%, subpar for a healthcare business. The divergence from its good operating margin stems from its capital-intensive business model, which requires Sotera Health Company to make large cash investments in working capital and capital expenditures.

Taking a step back, we can see that Sotera Health Company’s margin dropped by 6.4 percentage points during that time. It may have ticked higher more recently, but shareholders are likely hoping for its margin to at least revert to its historical level. Almost any movement in the wrong direction is undesirable because of its already low cash conversion. If the longer-term trend returns, it could signal it’s becoming a more capital-intensive business.

Sotera Health Company’s free cash flow clocked in at $52.41 million in Q4, equivalent to a 17.3% margin. Its cash flow turned positive after being negative in the same quarter last year, but we wouldn’t read too much into the short term because investment needs can be seasonal, causing temporary swings. Long-term trends trump fluctuations.

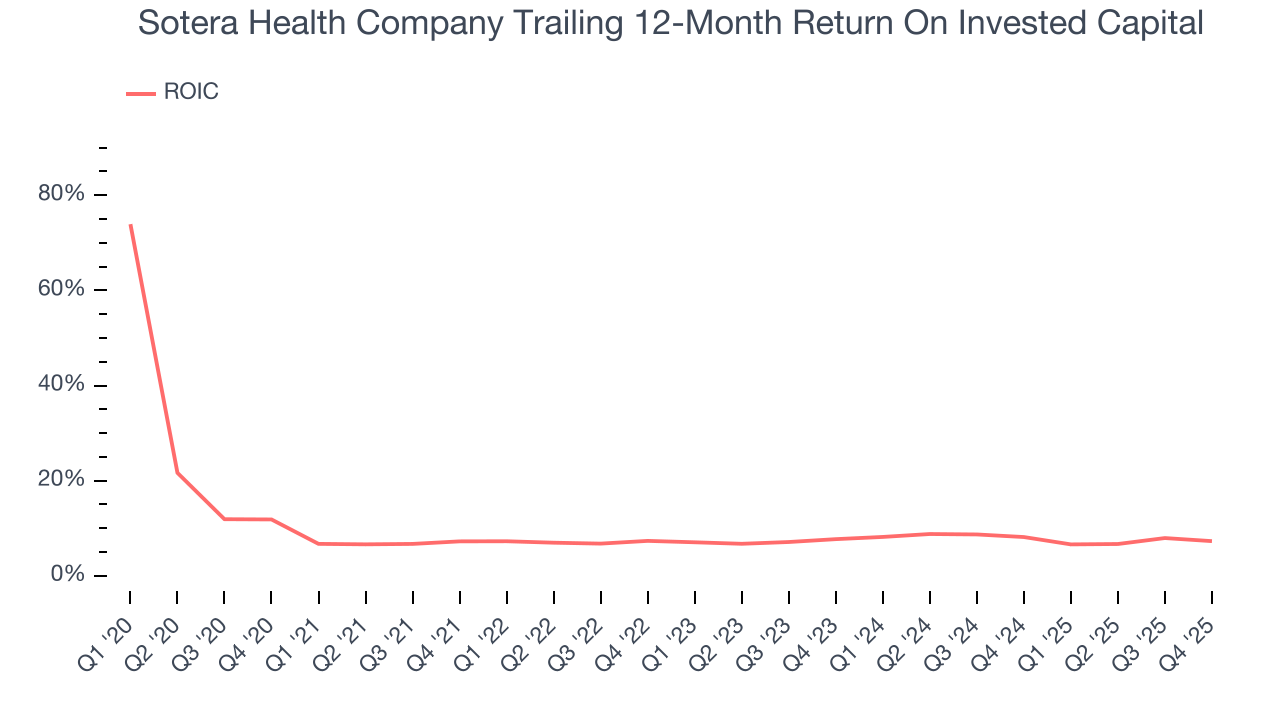

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Sotera Health Company’s management team makes decent investment decisions and generates value for shareholders. Its five-year average ROIC was 7.5%, slightly better than typical healthcare business.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Uneventfully, Sotera Health Company’s ROIC has stayed the same over the last few years. Given the company’s underwhelming financial performance in other areas, we’d like to see its returns improve before recommending the stock.

11. Balance Sheet Assessment

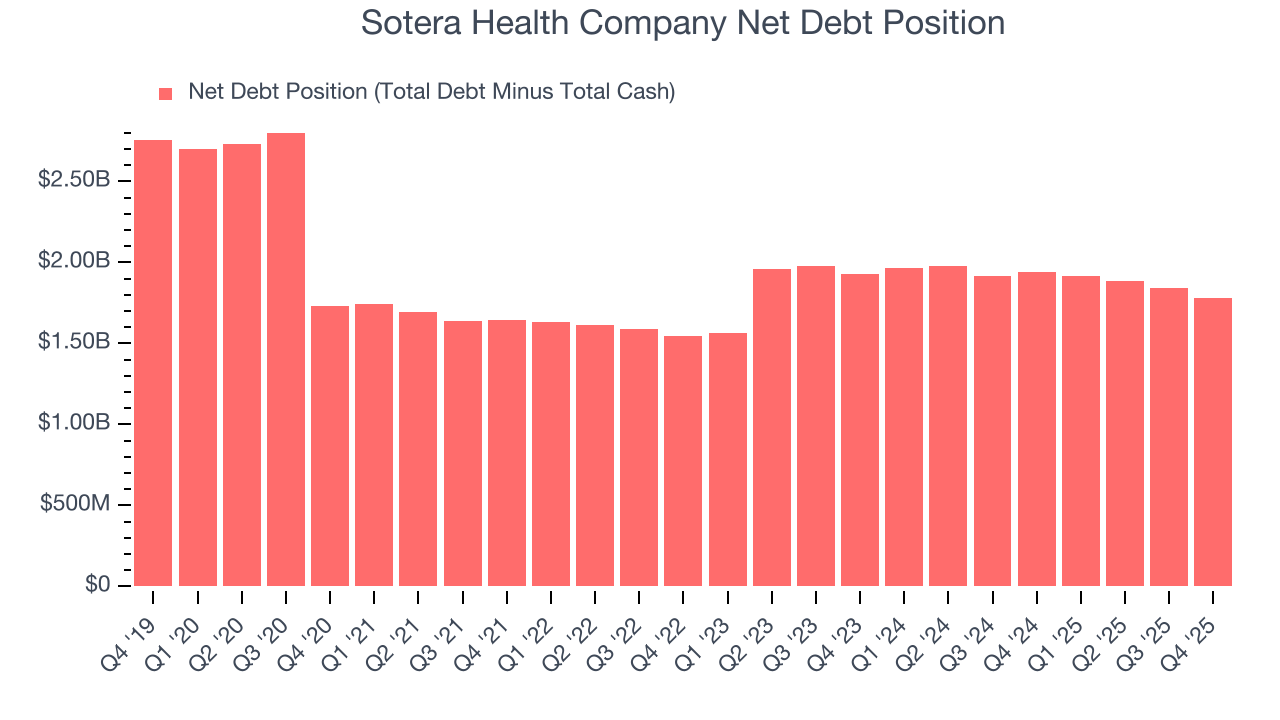

Sotera Health Company reported $346.5 million of cash and $2.13 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $593.8 million of EBITDA over the last 12 months, we view Sotera Health Company’s 3.0× net-debt-to-EBITDA ratio as safe. We also see its $85.63 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

12. Key Takeaways from Sotera Health Company’s Q4 Results

We enjoyed seeing Sotera Health Company beat analysts’ full-year EPS guidance expectations this quarter. We were also glad its full-year revenue guidance slightly exceeded Wall Street’s estimates. On the other hand, its organic revenue slightly missed. Overall, this print had some key positives. The stock traded up 1.5% to $17.75 immediately after reporting.

13. Is Now The Time To Buy Sotera Health Company?

Updated: March 23, 2026 at 11:01 PM EDT

Before investing in or passing on Sotera Health Company, we urge you to understand the company’s business quality (or lack thereof), valuation, and the latest quarterly results - in that order.

Sotera Health Company isn’t a terrible business, but it isn’t one of our picks. For starters, its revenue growth was mediocre over the last five years, and analysts don’t see anything changing over the next 12 months. While its impressive operating margins show it has a highly efficient business model, the downside is its subscale operations give it fewer distribution channels than its larger rivals. On top of that, its weak EPS growth over the last four years shows it’s failed to produce meaningful profits for shareholders.

Sotera Health Company’s P/E ratio based on the next 12 months is 14x. Investors with a higher risk tolerance might like the company, but we don’t really see a big opportunity at the moment. We're pretty confident there are more exciting stocks to buy at the moment.

Wall Street analysts have a consensus one-year price target of $20.75 on the company (compared to the current share price of $13.88).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.